Electronic Skin Patches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

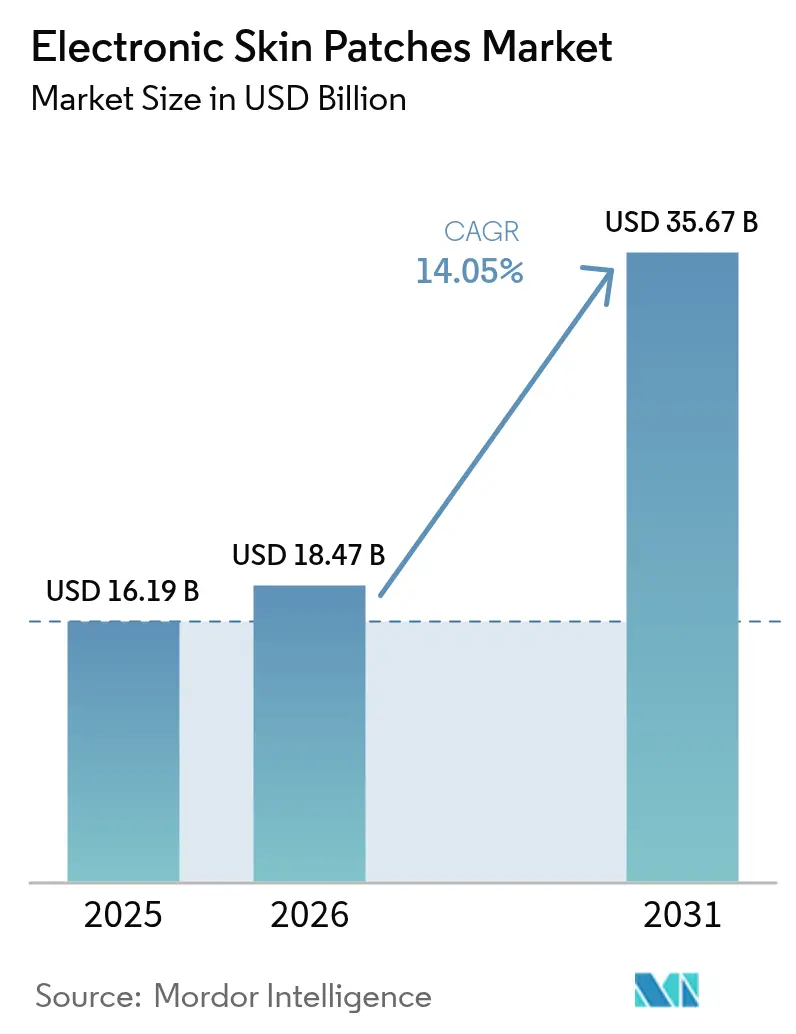

| Market Size (2026) | USD 18.47 Billion |

| Market Size (2031) | USD 35.67 Billion |

| Growth Rate (2026 - 2031) | 14.05% CAGR |

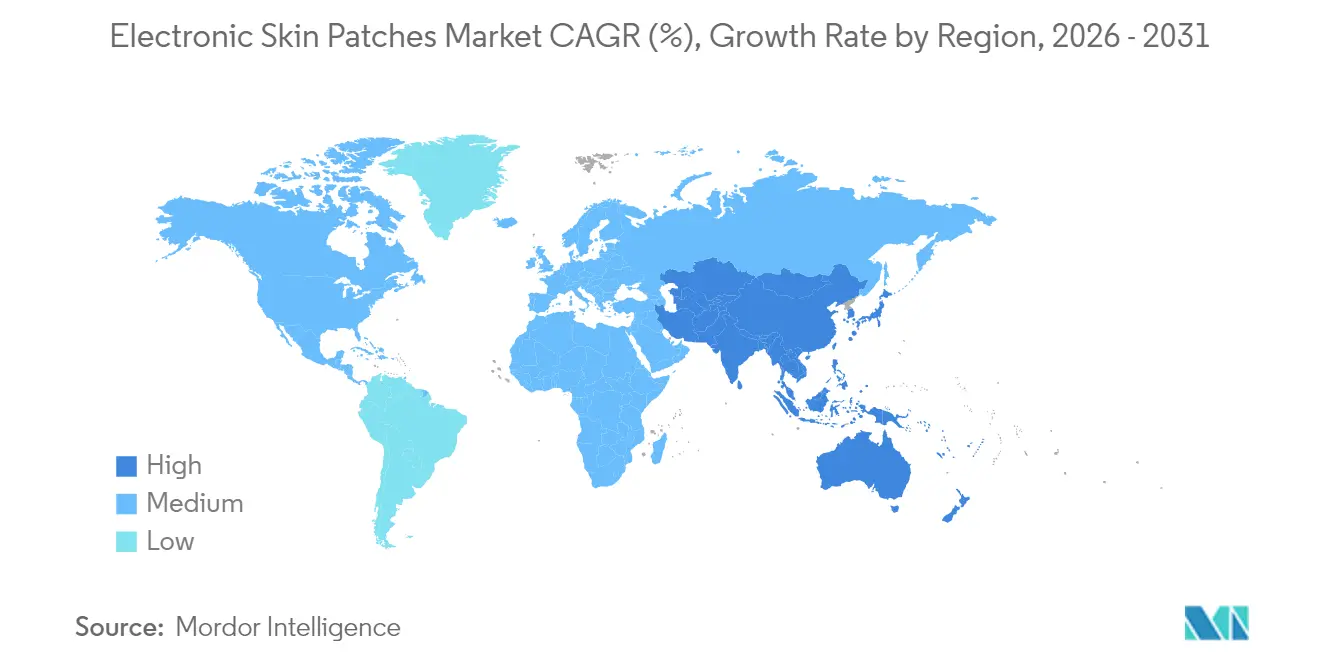

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Skin Patches Market Analysis by Mordor Intelligence

Electronic Skin Patches Market size in 2026 is estimated at USD 18.47 billion, growing from 2025 value of USD 16.19 billion with 2031 projections showing USD 35.67 billion, growing at 14.05% CAGR over 2026-2031.

Sensing and Diagnostic Patches hold the largest 46% revenue share in 2024, while Energy-Harvesting Smart Patches, enabled by battery-less power architectures, post the strongest 21.8% CAGR outlook. Cardiovascular Monitoring leads all applications at 38.2% share, but Women’s Health and Fertility registers the fastest 19.51% CAGR, as at-home breast ultrasound and hormone tracking patches attract new users. Regionally, North America commands a 37.9% share, backed by the FDA clearance of over-the-counter continuous glucose monitors (CGMs) from Dexcom and Abbott in 2024. In contrast, the Asia Pacific region accelerates at a 16.5% CAGR, underpinned by large-scale electronics manufacturing and supportive innovation programs. Investment momentum remains high: VitalConnect and Biolinq each secured USD 100 million rounds in 2025 to expand high-volume manufacturing and regulatory submissions, illustrating how funding channels reward platforms that blend clinically validated sensors with consumer-grade usability.[1]Andrew Rhew, “VitalConnect Raises USD 100 Million for Remote Monitoring Expansion,” medtechdive.com

Key Report Takeaways

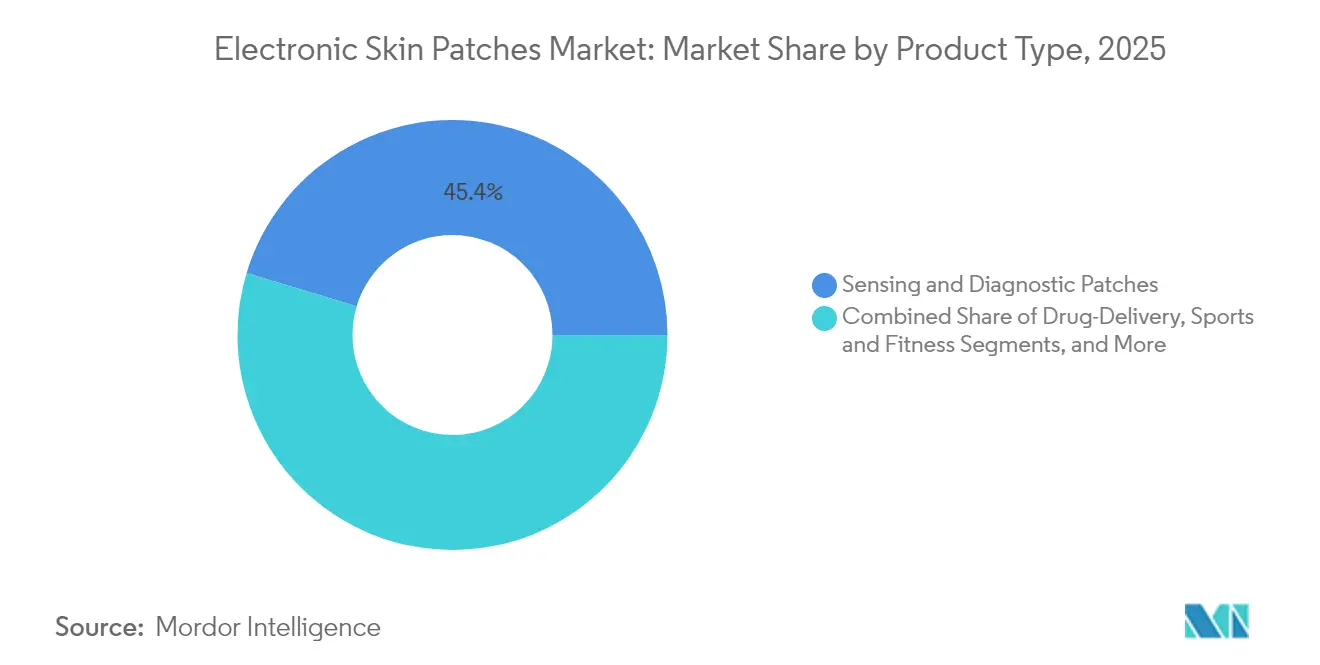

- By product type, Sensing and Diagnostic Patches led with 45.35% revenue share in 2025, while Energy-Harvesting Smart Patches are forecast to expand at 21.23% CAGR through 2031.

- By application, Cardiovascular Monitoring held 37.55% of the electronic skin patch market share in 2025; Women’s Health and Fertility is projected to expand at a 19.04% CAGR.

- By technology, Electrochemical Biosensors accounted for 34.82% share of the electronic skin patch market size in 2025, whereas Energy-Harvesting and Battery-less platforms are advancing at a 23.05% CAGR.

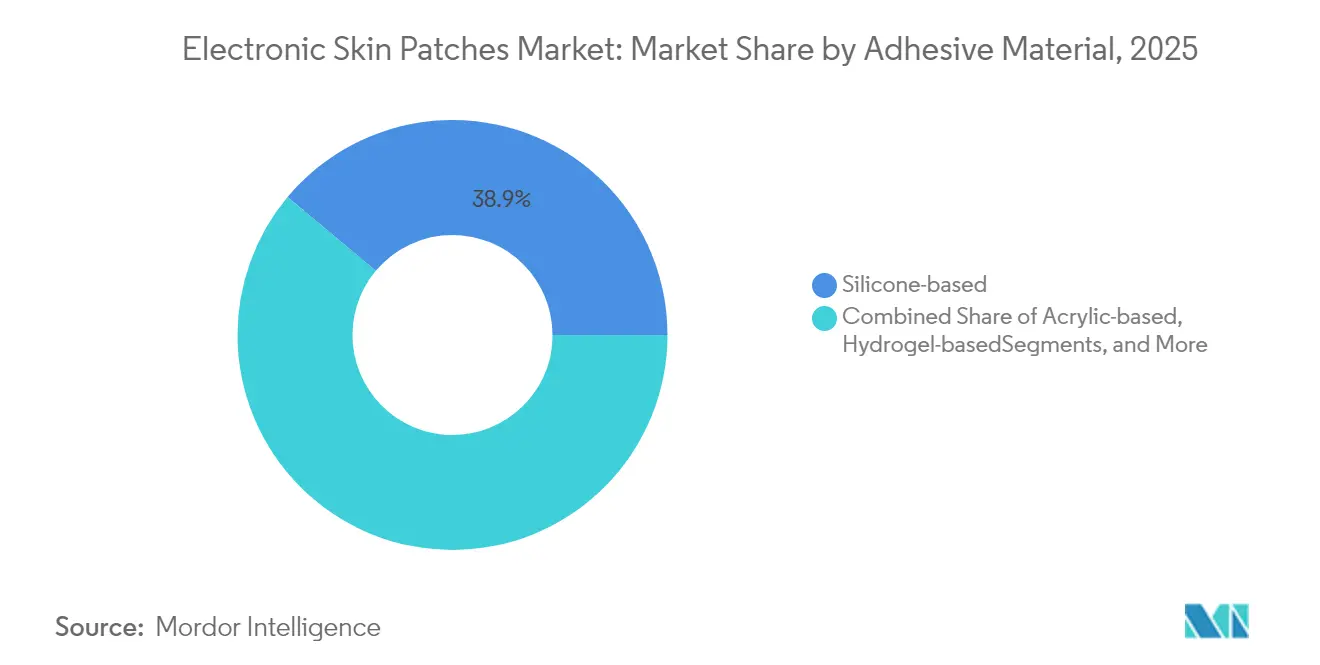

- By adhesive material, Silicone-based systems captured 38.92% share in 2025, while Hydrogel-based formulations grow quickest at 17.02% CAGR.

- By end-user, Hospitals and Clinics retained a 41.86% share in 2025; Home Healthcare is set to rise at 17.92% CAGR as reimbursement expands for remote monitoring.

- By geography, North America led with 37.55% market share in 2025; Asia Pacific records the fastest 16.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Skin Patches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous glucose-monitoring patch adoption surge | +3.2% | Global, North America leading | Short term (≤ 2 years) |

| Home-based cardiac telemetry reimbursement | +2.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Ageing population and chronic-care decentralisation | +2.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Flexible biofuel-cell power sources in mass production | +1.9% | Global, Asia Pacific manufacturing hubs | Medium term (2-4 years) |

| Hospital-at-home CPT codes for connected patches | +1.5% | North America, pilot programs in EU | Short term (≤ 2 years) |

| API-level integration with digital-therapeutics | +1.3% | Global, led by North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continuous Glucose-Monitoring (CGM) Patch Adoption Surge

FDA clearance of Dexcom Stelo and Abbott Lingo in 2024 removed prescription barriers and opened the CGM category to 25 million U.S. type 2 diabetics not on insulin, while also legitimizing consumer-grade biosensing for preventive metabolic health.[2]U.S. Food and Drug Administration, “FDA Allows Marketing of First Over-the-Counter Continuous Glucose Monitors,” fda.gov Disposable, all-in-one designs such as Dexcom’s Simplera lower training costs for payers and providers, fostering rapid uptake in pharmacy channels. Dexcom projects USD 40 million first-year revenue from Stelo, signaling strong elasticity in the newly addressable segment. Pharmaceutical firms are now embedding CGM data streams into weight-loss and metabolic-syndrome programs, expanding device demand beyond the core diabetes cohort. Growth is global, yet North America captures early volumes due to favorable reimbursement. Vendors are racing to integrate glucose telemetry into closed-loop therapy ecosystems, accelerating replacement of finger-stick meters in home settings.

Home-Based Cardiac Telemetry Reimbursement Expansion

Medicare, major U.S. commercial insurers, and several EU payers now reimburse 14-day and 30-day patch ECG services, citing up to 30% lower readmission rates compared with traditional telemetry. VitalConnect earmarked its 2025 USD 100 million raise to triple VitalPatch output for Hospital-at-Home contracts. Complementary platforms such as the LEAF Patient Monitoring System, covered under fall-prevention DRGs, illustrate how multiparameter patches can bundle cardiology and safety use-cases. Reimbursement clarity attracts health-system procurement budgets, which favor patches over bulky holter monitors for elderly patients. Expansion is strongest in the United States today, yet Germany, France, and Japan have introduced pilot codes that should unlock medium-term European and Asian volume.

Ageing Population and Chronic-Care Decentralisation

United Nations forecasts show the global 65+ cohort rising to 1.03 billion by 2030, straining facility-based care. Electronic skin patch market demand benefits as remote multiparameter sensing permits continuous, low-touch management of hypertension, heart failure, and COPD at home. Self-healing “e-skin” substrates that recover 80% mechanical integrity within 10 seconds now mitigate durability concerns for frail users. AI engines running on edge processors convert dense raw signals into actionable alerts, allowing clinicians to triage before symptom escalation. Governments that bundle remote monitoring into capitated payment models, such as the U.K. Integrated Care Systems are demonstrating lower total cost of care, reinforcing long-run growth tailwinds.

Flexible Biofuel-Cell Power Sources Hit Mass Production

Asia Pacific foundries began high-volume roll-to-roll printing of sweat-powered nanogenerators that charge small IoT devices in 6 minutes from 0.6 mL perspiration.[3]A. Nguyen, “Sweat-Powered Nanogenerators Ready for Mass Production,” cen.acs.org University of Waterloo’s thermoelectric yarns convert body heat plus ambient light into continuous 300-µW output, adequate for BLE streaming. Piezoelectric harvesters now deliver 280-fold greater conversion efficiency than early-generation films, allowing patches to run indefinitely on human motion.[4]S. Choi et al., “280-Fold-Efficiency Piezoelectric Energy Harvester for Wearables,” dgist.ac.kr Removing the battery sub-assembly cuts BOM cost by up to 25%, eliminates environmentally regulated lithium waste, and improves device thinness, which boosts user comfort and therefore adherence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and privacy compliance costs | –2.1% | Global, highest in EU and North America | Short term (≤ 2 years) |

| Adhesion / skin-irritation failure rates | –1.8% | Global, varies with climate and demographics | Medium term (2-4 years) |

| Battery-disposal and e-waste regulation pressure | –1.3% | EU leading, global adoption rising | Long term (≥ 4 years) |

| Patch reimbursement gaps in emerging economies | –0.9% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security and Privacy Compliance Costs

Patches that blur medical-device and consumer-wellness categories face fragmented regulation. HIPAA exempts many direct-to-consumer wearables, while GDPR imposes strict consent, encryption, and data-minimization obligations. Building dual-stack architectures capable of satisfying both frameworks can add 15-20% to R&D budgets for small manufacturers. Only 20 U.S. states have explicit wearable data laws, creating legal uncertainty that drives conservative security investments. Larger incumbents use existing SOC-2 and ISO-27001 programs to spread compliance fixed costs, widening the competitiveness gap.

Adhesion / Skin-Irritation Failure Rates

Silicone and acrylic adhesives provoke erythema in up to 25% of users after 72-hour wear. Hydrogel formulations lower irritation but cost 40-60% more and complicate automated dispensing lines. Manufacturers must validate multiple glue chemistries to serve varying humidity and skin-type profiles, inflating inventory SKUs. Self-healing hydrogels restore adhesion under shear stress, yet require multi-site clinical trials to win clinician trust, delaying broad roll-outs. Failure to manage dermatologic tolerability suppresses reorder rates and limits multi-week monitoring protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Energy-Harvesting Patches Drive Innovation

Energy-Harvesting Smart Patches are growing at a 21.23% CAGR, overtaking traditional, battery-powered sensing platforms in demand velocity. The electronic skin patch market size for this sub-category is projected to more than triple between 2026 and 2031 as power-autonomous designs remove both environmental waste and user inconvenience linked to weekly sensor swaps. Sensing and Diagnostic Patches, while mature, still control 45.35% 2025 revenue and remain essential in regulated care pathways where clinicians prioritize accuracy and established reimbursement. Drug-Delivery Patches keep steady adoption in pain and hormone therapy, but lack the growth inflection energy-harvesting variants enjoy. Cosmetic and Wellness Patches, driven by consumer focus on anti-aging and hydration analytics, form a modest but rising revenue line that attracts beauty majors eager for data-rich personalization.Recent academic-industry collaboration produced sweat-powered micro-supercapacitors that output 20 mA cm⁻² after a six-minute charge, validating real-world readiness beyond lab prototypes. University of Waterloo researchers knit thermoelectric yarns directly into biocompatible substrates, integrating power and sensor arrays without added thickness. Such advances align with OEM roadmaps to re-engineer housings around thinner, more flexible stacks, allowing devices to conform to high-motion anatomical sites like elbows and knees. As IP matures, licensing deals between chipmakers, adhesive formulators, and consumer-health brands should accelerate, further boosting electronic skin patch market penetration in outpatient protocols and lifestyle segments alike.

By Application: Women’s Health Emerges as Growth Leader

Cardiovascular Monitoring held a commanding 37.55% electronic skin patch market share in 2025, upheld by payer focus on reducing readmissions through rhythm surveillance. Yet Women’s Health and Fertility applications, projected at 19.04% CAGR, now represent the most dynamic vector as long-neglected clinical needs receive venture backing. MIT’s portable breast ultrasound patch exemplifies how self-contained imaging can transition from hospitals to living rooms. Fertility-tracking companies leverage hormone-sensing hydrogels for continuous luteinizing hormone readouts, empowering users with cycle predictions more precise than basal-temperature charts.Pain and Musculoskeletal management harnesses electrical-stimulation patches that gate nerve signals, offering opioid-free analgesia. Diabetes Management remains sizeable due to CGM volume, yet its growth moderates as penetration approaches saturation in insulin-dependent cohorts. Neuro-mental health remains nascent but promising: electrodermal-activity patches, coupled with machine-learning classifiers, screen for anxiety episodes, enabling timely behavioral cues. The diversification across applications reduces revenue cyclicality and underscores the electronic skin patch industry’s ability to pivot toward underserved populations.

By Technology: Battery-less Solutions Lead Innovation

Electrochemical biosensors, accounting for 34.82% 2025 revenue, maintain market shepherd status by converting analyte-specific reactions into quantifiable signals with proven clinical accuracy. Nevertheless, Energy-Harvesting and Battery-less architectures outpace at 23.05% CAGR, spotlighting the sector’s shift toward maintenance-free wearables. MEMS-enabled microfluidics now route sub-microliter sweat samples through multiplexed assay chambers, while RF-ID/NFC links power patch read-outs via smartphone taps, removing onboard batteries entirely.Piezoelectric harvesters anchored on PZT micro-domes achieve 280× efficiency improvements over 2018 benchmarks, allowing cardiac-motion energy to sustain Bluetooth Low Energy telemetries. Optical/PPG sensor stacks grow sophisticating, embedding multi-wavelength emitters that derive SpO₂, blood pressure proxies, and hydration indices without added photodiode count. Edge AI compression reduces data packets by 90%, sustaining weekly transmission on micro-amp budgets. Taken together, these advances enable the electronic skin patch market to address long-wear military and industrial scenarios where battery logistics are prohibitive.

By Adhesive Material: Hydrogels Transform Biocompatibility

Silicone adhesives remain ubiquitous, capturing 38.92% 2025 share, favored for process familiarity and broad-spectrum skin compatibility. Yet the segment’s growth moderates as hydrogels clock a brisk 17.02% CAGR. The electronic skin patch market size for hydrogel-based products rises in tandem with user demand for multi-week comfort. Hydrogel matrices loaded with ionic liquids now double as conductive pathways, merging adhesion and sensing functions, a design convergence that trims bill-of-materials. Researchers at the Terasaki Institute engineered self-healing hydrogel networks that restore 80% tensile strength within seconds, curbing delamination after sudden strain. Conductive polymer grafts maintain impedance stability even after 50 wash cycles, opening sports-garment integration. Hybrid silicone-hydrogel stacks meet sweat-rich sport users while preserving low-cost mass-production lines. Adhesive material diversification ultimately raises total addressable segments and lowers dermatologic discontinuation rates, thereby lifting overall electronic skin patch market penetration,

By End-User: Home Healthcare Drives Decentralization

Hospitals and Clinics own 41.86% revenue share in 2025, leveraging bundled procurement and established payor relationships to deploy high-accuracy patches in acute and outpatient settings. However, Home Healthcare surges at 17.92% CAGR, supported by CPT codes that reimburse continuous remote physiologic monitoring. The electronic skin patch industry now sees consumer retail chains and telehealth providers procuring devices in bulk, reflecting care migration out of brick-and-mortar sites.Sports and Fitness centers integrate lactate and hydration patches into athlete performance dashboards, while Military and Emergency Services deploy multi-parameter platforms to monitor soldier core temperature and stress markers. Research Institutions pilot next-generation sensing chemistries, such as cortisol assays, accelerating path-to-market for mental-health applications. Cosmetic and Dermatology clinics add micro-needling drug-delivery patches to anti-aging portfolios, demonstrating cross-industry uptake that cushions demand volatility tied to any single healthcare vertical.

Geography Analysis

North America commands 37.55% electronic skin patch market share in 2025, benefited by FDA pathways that brought OTC CGMs to pharmacy shelves, thus expanding unit volumes beyond endocrinology clinics. Hospital-at-Home reimbursement codes convert remote monitoring into predictable revenue streams for providers, sustaining purchase orders even after pandemic peaks. Canada experiments with provincial remote-cardiac programs, while Mexican maquiladoras attract OEM assembly due to tariff-free USMCA logistics, shaving 8-10% off landed costs.Asia Pacific delivers the fastest 16.32% CAGR, powered by China’s Healthy China 2030 blueprint that funds digital-health pilots and by Japan’s Silver Economy demand spike. South Korea’s ODM fabs tout vertical integration—from flex-PCB etching to sterile packaging—slashing lead times for Western brands entering the region. India’s National Digital Health Mission reimburses Bluetooth LE-enabled patches in pilot diabetes programs, albeit with price caps that favor energy-harvesting models over battery-heavy imports.Europe grows steadily despite GDPR friction: stringent data controls catalyze investments in on-patch encryption ASICs, yielding differentiated products able to command premium ASPs. The bloc’s Battery Regulation, effective 2027, pushes manufacturers toward biofuel-cell power, aligning with eco-design incentives. Germany leverages public-private clusters in Baden-Württemberg for polymer research, while the U.K. NHS integrates patches into virtual-ward targets aimed at freeing 5,000 acute beds by 2026. Nordic e-prescription networks automatically link CGM data, enabling algorithmic insulin dosing in primary care.

Competitive Landscape

The electronic skin patch market displays moderate fragmentation: no single vendor exceeds a 15% revenue share, yet the top five hold roughly 48%, creating room for both incumbents and niche entrants. Legacy device majors—Medtronic, Abbott, Dexcom—exploit regulatory expertise, multi-channel distribution, and post-market surveillance infrastructure to sustain hospital contracts. Conversely, specialists such as VitalConnect and Biolinq orient around single-use, high-resolution patches and rely on venture funding to turn rapid design iterations into FDA clearances.

Competitive differentiation shifts from raw sensing accuracy to holistic platform play. Leaders bundle multi-modal sensors, edge analytics, and FHIR-compatible APIs, making their patches sticky inside provider workflows. Intellectual-property defenses have moved upstream into advanced materials: Shin-Etsu Chemical patented a silver-nanowire bio-electrode that maintains conductivity under 50% strain while reducing dermatitis incidents by 60%. M&A activity is likely as full-stack vendors seek novel adhesives, power solutions, or AI algorithms unavailable in-house.

Consumer-wellness entrants, often born in Silicon Valley, compete on design and subscription-based insights rather than regulated endpoints. While margins are thinner, volume potential is higher, especially as pharmacies merchandise patches adjacent to fitness trackers. Industrial-safety use-cases form a nascent battleground where established medical OEMs lack domain contacts, allowing newcomers with gas-sensor or heat-stress expertise to win early contracts. Over the forecast horizon, strategic alliances between chipmakers, polymer suppliers, and healthcare platforms will determine who captures incremental market share.

Electronic Skin Patches Industry Leaders

Vital Connect Inc.

Leaf Healthcare Inc.

Quad Industries

L'Oréal SA

Sensium Healthcare Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Biolinq closed USD 100 million Series C to transition its multi-analyte sensor patch from late-stage trials to U.S. launch plans.

- April 2025: Dexcom obtained FDA clearance for G7 15-Day CGM, extending sensor life and targeting an H2 2025 rollout.

- February 2025: VitalConnect secured USD 100 million to scale VitalPatch production for Hospital-at-Home monitoring.

- August 2024: Medtronic gained FDA approval for Simplera CGM and partnered with Abbott to co-develop integrated systems.

Global Electronic Skin Patches Market Report Scope

The electronic skin patches deploy devices, such as sensors and actuators, directly on to the body, whih gives real-time information about the vitals of a person's body, such as temperature, UV radiation absorption, and oxygen levels in the blood. The report segments the market by application and geography.

| Sensing and Diagnostic Patches |

| Drug-Delivery Patches |

| Electrical-Stimulation Patches |

| Cosmetic and Wellness Patches |

| Energy-Harvesting Smart Patches |

| Cardiovascular Monitoring |

| Diabetes Management |

| Pain / Musculoskeletal |

| Infectious-Disease and Fever |

| Women's Health and Fertility |

| Neuro and Mental Health |

| Sports and Fitness |

| Drug-Delivery |

| Electrochemical Biosensors |

| Optical / PPG Sensors |

| MEMS and Microfluidics |

| RFID / NFC Smart Patches |

| Energy-Harvesting and Battery-less |

| Silicone-based |

| Acrylic-based |

| Hydrogel-based |

| Others (PU, Hybrid) |

| Hospitals and Clinics |

| Home Healthcare |

| Sports and Fitness Centres |

| Military and Emergency Services |

| Cosmetic and Dermatology Clinics |

| Research Institutions |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Sensing and Diagnostic Patches | ||

| Drug-Delivery Patches | |||

| Electrical-Stimulation Patches | |||

| Cosmetic and Wellness Patches | |||

| Energy-Harvesting Smart Patches | |||

| By Application | Cardiovascular Monitoring | ||

| Diabetes Management | |||

| Pain / Musculoskeletal | |||

| Infectious-Disease and Fever | |||

| Women's Health and Fertility | |||

| Neuro and Mental Health | |||

| Sports and Fitness | |||

| Drug-Delivery | |||

| By Technology | Electrochemical Biosensors | ||

| Optical / PPG Sensors | |||

| MEMS and Microfluidics | |||

| RFID / NFC Smart Patches | |||

| Energy-Harvesting and Battery-less | |||

| By Adhesive Material | Silicone-based | ||

| Acrylic-based | |||

| Hydrogel-based | |||

| Others (PU, Hybrid) | |||

| By End-User | Hospitals and Clinics | ||

| Home Healthcare | |||

| Sports and Fitness Centres | |||

| Military and Emergency Services | |||

| Cosmetic and Dermatology Clinics | |||

| Research Institutions | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the electronic skin patch market?

The market stands at USD 18.47 billion in 2026 and is forecast to reach USD 35.67 billion by 2031 at a 14.05% CAGR.

Which product segment grows fastest through 2031?

Energy-Harvesting Smart Patches post the highest 21.23% CAGR as battery-less power technology reaches mass production.

Why is North America the largest regional market?

FDA clearance of over-the-counter CGMs and supportive reimbursement for Hospital-at-Home programs give North America 37.55% 2025 share and strong forward momentum.

What factors restrain wider adoption of electronic skin patches?

Data-security compliance costs and skin-irritation issues tied to adhesive materials collectively trim the forecast CAGR by nearly 4 percentage points.

How are electronic skin patches powered without batteries?

Sweat-based biofuel cells, thermoelectric yarns, and advanced piezoelectric harvesters convert body energy into electricity, enabling multi-year operation without battery replacement.

Which application shows the most rapid growth?

Women’s Health & Fertility leads with 19.04% CAGR, propelled by at-home breast imaging and hormone-tracking innovations.

Page last updated on: