Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

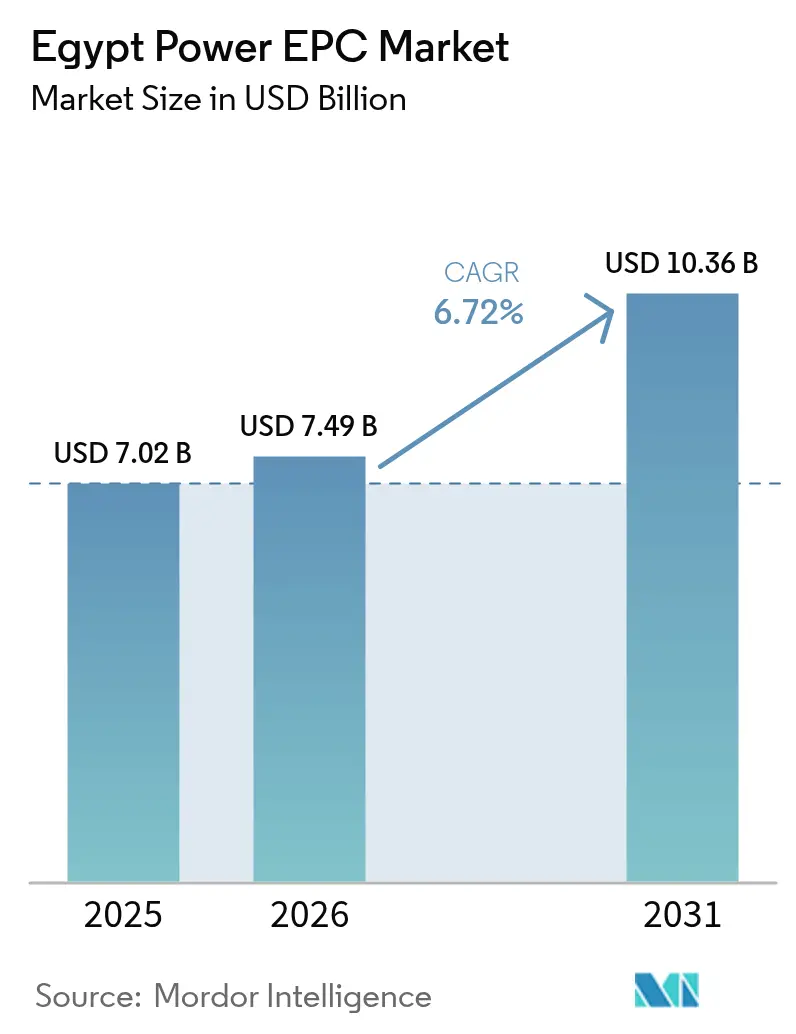

| Base Year Market Size (2025) | USD 7.02 Billion |

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 10.36 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

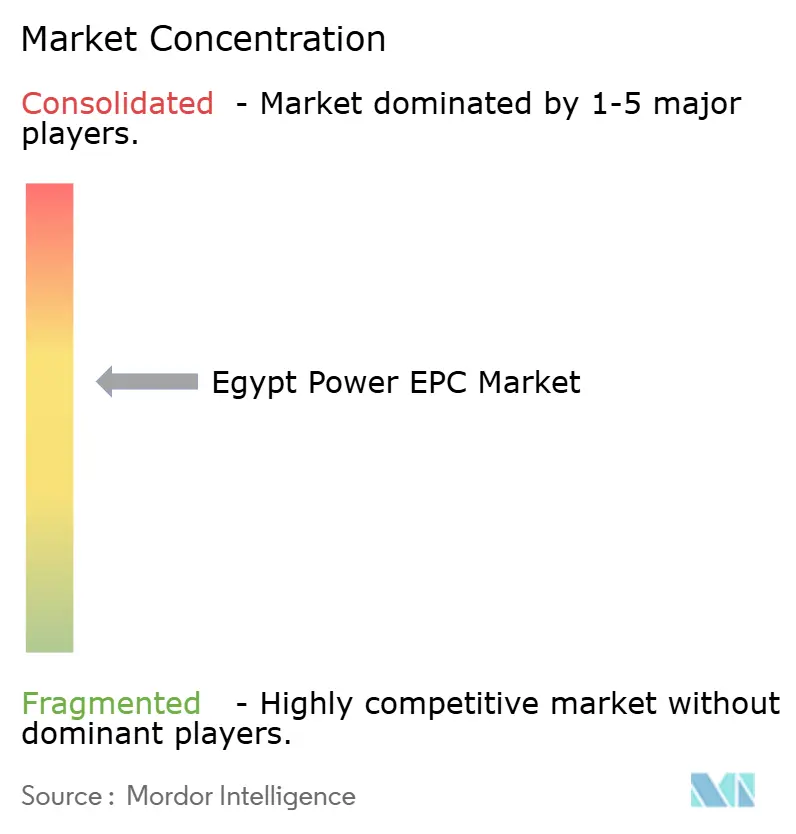

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Power EPC Market Analysis by Mordor Intelligence

The Egypt Power EPC Market size in 2026 is estimated at USD 7.49 billion, growing from 2025 value of USD 7.02 billion with 2031 projections showing USD 10.36 billion, growing at 6.72% CAGR over 2026-2031.

Robust government policy, population-driven electricity demand, and multilateral financing combine to sustain the Egyptian power EPC market’s momentum. Contractors benefit from the Integrated Sustainable Energy Strategy 2035, which targets 42% renewable capacity by 2030 and pushes a steady pipeline of solar, wind, and grid projects. Foreign-exchange volatility raised imported equipment costs in 2024, yet it simultaneously accelerated local manufacturing and spurred joint ventures. Rapid industrialization around the Suez Canal Economic Zone (SCZONE) and the New Administrative Capital boosts captive-power construction, while cross-border HVDC links with Saudi Arabia and Europe position Egypt as a regional energy hub. Competitive intensity grows as local majors Elsewedy Electric and Orascom Construction defend share against Siemens, GE, and China Energy Engineering.

Key Report Takeaways

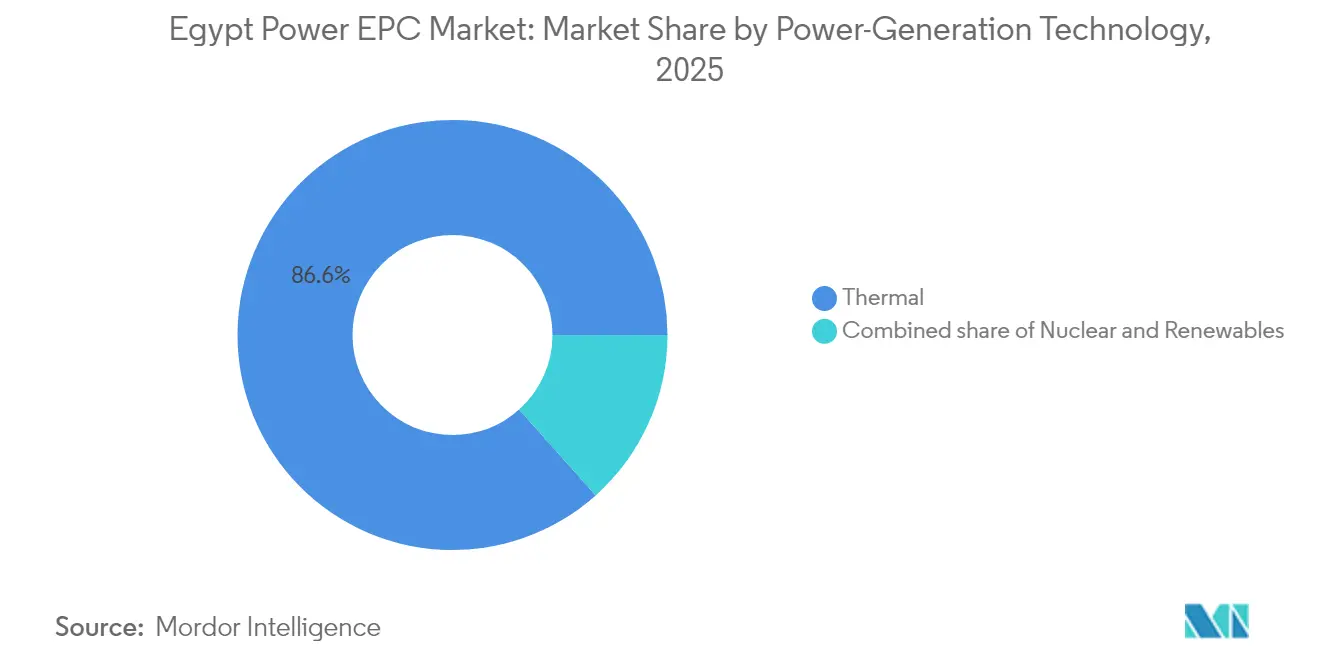

- By power-generation technology, thermal generation led with 86.60% of Egypt's power EPC market share in 2025, while renewables are forecast to expand at a 13.9% CAGR through 2031.

- By capacity band, projects exceeding 500 MW accounted for 59.30% of the Egyptian power EPC market size in 2025; systems below 100 MW are projected to grow at a 13.05% CAGR between 2026 and 2031.

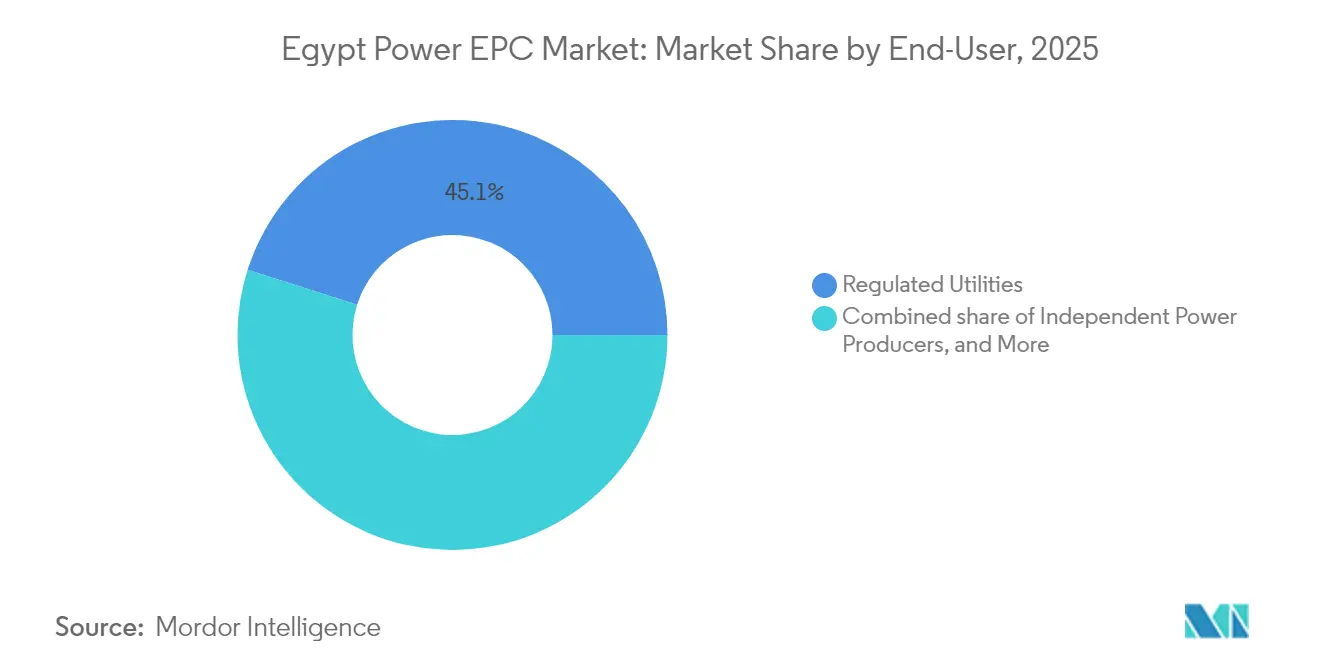

- By end-user, regulated utilities held 45.10% of Egypt's power EPC market share in 2025, whereas independent power producers are expected to advance at a 12.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government renewable-energy targets (ISES 2035) | +2.10% | National, concentrated in Upper Egypt and Red Sea coast | Medium term (2-4 years) |

| Rapid demand growth from population & industrialisation | +1.80% | National, with highest growth in Greater Cairo and New Administrative Capital | Short term (≤ 2 years) |

| Green-hydrogen export MoUs driving new RE capacity | +1.40% | SCZONE, Ain Sokhna, Mediterranean coast | Long term (≥ 4 years) |

| Multilateral concessional financing (WB, AfDB, EBRD) | +1.00% | National, priority to grid reinforcement in southern regions | Medium term (2-4 years) |

| Cross-border HVDC interconnectors (KSA, EuroAfrica) | +0.70% | Eastern Desert (Saudi link), Mediterranean coast (Europe link) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Renewable-Energy Targets Drive Unprecedented EPC Pipeline

Egypt’s 42% renewable-capacity target by 2030 requires roughly 20 GW of new installations, translating into USD 15 billion of cumulative EPC awards over the period. In 2024, the New and Renewable Energy Authority (NREA) approved 3.2 GW of solar and wind—180% above 2023 levels—indicating strong regulatory momentum. The New Administrative Capital’s pledge to source 100% clean power by 2028 underpins demand for smart-grid and storage EPC packages. A 30% mandatory local-content rule now applies to renewable projects, steering procurement toward contractors with Egyptian manufacturing partners and reshaping supply chains. These conditions collectively anchor mid-term growth for the Egyptian power EPC market.

Population Growth and Industrial Expansion Strain Grid Infrastructure

Egypt’s population reached 106 million in 2024, while industrial electricity demand grew 8.2% year-on-year, placing immediate stress on generation and transmission assets.(1)Central Agency for Public Mobilization and Statistics, “Population and Energy Bulletin 2024,” capmas.gov.eg The New Administrative Capital alone requires 1.2 GW of new capacity, and SCZONE’s factories will need 800 MW of captive generation by 2027. Transmission bottlenecks south of Cairo limit renewable evacuation; USD 1.2 billion of grid-modernization EPC contracts are therefore slated through 2026. Manufacturers are increasingly ordering on-site solar and gas microgrids to hedge against outages, driving the distributed-energy subsegment to its current double-digit growth. These dynamics reinforce near-term opportunities across generation, T&D, and distributed systems within the Egyptian power EPC market.

Green-Hydrogen Export Agreements Create Specialized EPC Opportunities

Framework deals worth more than USD 40 billion with European offtakers position Egypt as a future green-hydrogen exporter.(2) Suez Canal Economic Zone, “Hydrogen Corridor Masterplan,” sczone.eg AMEA Power’s 1.4 GW hydrogen project in Ain Sokhna, which closed financing in September 2024, unlocked an EPC package valued at about USD 2.8 billion. SCZONE has reserved 7,600 km² for hydrogen and ammonia plants, indicating potential EPC demand of USD 12 billion to 2030 as memoranda evolve into construction contracts. Projects require integrated engineering for renewables, desalination, electrolysis, and storage, favoring firms with multi-disciplinary credentials. Hydrogen thus introduces a long-term growth vector for the Egyptian power EPC market.

Multilateral Financing Accelerates Grid Modernization Projects

The Nexus of Water, Food, and Energy (NWFE) platform mobilized USD 3.2 billion in 2024, including a EUR 200 million EBRD loan targeting grid reinforcement.(3)European Bank for Reconstruction and Development, “NWFE Electricity Grid Reinforcement,” ebrd.com The World Bank’s USD 500 million Egypt Electricity Grid Reinforcement Project, approved in March 2024, funds substation upgrades across 14 governorates. Concessional rates reduce borrowing costs by up to 300 basis points, making previously unbankable projects bankable and expanding the addressable EPC pool. Contractors experienced in multilateral safeguards and procurement procedures gain a competitive advantage, helping to stabilize the Egyptian power EPC market’s financing environment.

Cross-Border Interconnectors Position Egypt as a Regional Power Hub

The USD 1.8 billion Egypt-Saudi HVDC link reached detailed-design completion in 2024, creating EPC demand for submarine cables and converter stations.(4)Saudi Electricity Company, “Egypt-KSA HVDC Link Project Update,” sec.com.sa With 3 GW of bidirectional capacity, the line lets Egypt export surplus renewables and import power during peaks, optimizing regional generation assets. The 2 GW EuroAfrica Interconnector, which is estimated to cost USD 3.5 billion and will run through Cyprus, advances feasibility, further embedding Egypt in the Mediterranean energy trade. These ventures require HVDC, marine cable, and international grid synchronization expertise, enriching the technology mix in the Egyptian power EPC market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency depreciation inflating imported EPC inputs | -1.20% | National, affecting all import-dependent projects | Short term (≤ 2 years) |

| High sovereign-debt risk raising project WACC | -0.80% | National, particularly affecting large-scale projects | Medium term (2-4 years) |

| Grid bottlenecks south of Cairo delaying RE integration | -0.60% | Upper Egypt, Aswan, Red Sea governorates | Medium term (2-4 years) |

| Local-content rules constraining tech/vendor choice | -0.40% | National, affecting renewable and grid modernization projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Disrupts EPC Cost Structures and Financing

The pound slipped from 31 EGP/USD to 49 EGP/USD in 2024, inflating imported-equipment prices by roughly 58%. Elsewedy Electric booked EGP 2.1 billion in FX losses, and Orascom Construction renegotiated contracts to shift exchange risk. The IMF’s flexible-rate mandate implies more volatility, prompting EPC contractors to seek escalation clauses, up-front payments, and local-currency hedges. Imported gas turbines, transformers, and HV equipment still represent 60-70% of project capex, so currency swings can erode margins and delay financial close within the Egyptian power EPC market.

Grid Infrastructure Bottlenecks Constrain Renewable Energy Integration

Transmission corridors south of Cairo lack the capacity to evacuate 1.8 GW of contracted renewables, delaying commercial operation. Upgrading the 500 kV spine requires USD 1.2 billion and faces land acquisition delays that have stretched schedules by 12-18 months. Developers now factor connection uncertainty into cash-flow models, which raises working-capital requirements and pushes some PPAs beyond their grid-ready dates. Specialized T&D EPC firms gain opportunities, but the overall market velocity slows until bottlenecks are eased.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power-Generation Technology: Thermal Dominance Faces Renewable Disruption

Thermal assets held 86.60% of Egypt's power EPC market share in 2025, anchored by abundant natural gas and Siemens' 14.4 GW combined-cycle complex. Nuclear adds scale via Rosatom's USD 25 billion El Dabaa project, Egypt's largest single EPC contract. Renewable capacity, however, is projected to grow at an annual rate of 13.9%, driven by policy targets and exceptional solar and wind resources. The 1.65 GW Benban Solar Park proved bankability for utility-scale solar, while PowerChina's January 2025 award for a 1.1 GW Suez wind farm underscores continued foreign appetite. Over the 2026-2031 period, renewables will steadily carve out larger slices of Egypt's power EPC market, compelling thermal specialists to diversify their offerings.

Historically, thermal EPC recorded a 3.2% CAGR between 2019-2024, whereas renewables now expand at nearly five times that rate. The engineering scope evolves accordingly: thermal contractors invest in emissions controls and efficiency upgrades, while renewable specialists focus on bundling storage and ensuring grid code compliance. Nuclear EPC introduces long-dated cash-flow schedules and stringent safety norms, broadening the competence matrix of the Egyptian power EPC market.

By Capacity Band: Megaprojects Drive Value While Distributed Systems Grow Fastest

Projects above 500 MW captured 59.30% of Egypt's power EPC market size in 2025, led by mega-plants such as El Dabaa and Siemens' tri-site complex. These ventures require deep project management capabilities, heavy-lift logistics, and large, skilled workforces that only a select few contractors can provide. The 100-499 MW band thrives on wind farms in the Gulf of Suez, where scale balances grid-fit and bankability.

Systems below 100 MW, though smaller in value, register the highest 13.05% CAGR through 2031. Industrial clients are leveraging net-metering rules issued in 2024 to install rooftop PV and gas cogeneration systems, thereby reducing their energy bills and enhancing reliability. Remote resorts and communities on the Red Sea coast deploy microgrids that integrate PV, batteries, and diesel backup. Specialized integrators thus tap a vibrant distributed-energy niche inside the Egyptian power EPC market.

By End-User: Regulated Utilities Lead While IPPs Accelerate

Regulated utilities, primarily subsidiaries of the Egyptian Electricity Holding Company, account for 45.10% of current EPC demand through centralized procurement and sovereign guarantees. Their grid modernization and generation projects offer stable cash flows but involve rigid tender processes. Independent power producers exhibit the quickest 12.35% CAGR as Egypt widens private-sector participation. Competitive auctions under the renewable-energy framework draw IPPs such as ACWA Power, Masdar, and AMEA Power, all of which are attracted by bankable PPAs.

Industrial captive-power customers gain ground as factories seek self-sufficiency. Elsewedy Electric and Arab Contractors have tailored turnkey offerings for this group, bundling finance and O&M services. Public-sector entities, including the New Urban Communities Authority, maintain steady demand; however, budget constraints temper growth. Together, these patterns diversify revenue streams across the Egyptian power EPC market.

Geography Analysis

Greater Cairo and the Nile Delta account for roughly 39.20% of EPC value, anchored by Siemens’ combined-cycle plants and ongoing grid-digitalization programs. The New Administrative Capital alone commands USD 800 million in power infrastructure and aims for a 100% renewable supply by 2028, opening contracts for smart meters, rooftop PV, and BESS. Upper Egypt forms the renewable heartland, hosting the Benban Solar Park and planned wind farms across Aswan and the Red Sea coast. High solar irradiance and vacant land facilitate large projects, though transmission upgrades remain critical.

SCZONE on the Suez Canal is Egypt’s industrial powerhouse. Its hydrogen corridor reserves 7,600 km² for electrolyzers and ammonia plants, valued at USD 12 billion, through 2030. EPC scope spans port upgrades, desalination, and high-capacity feeders, rewarding multi-disciplinary contractors. Coastal governorates benefit from cross-border links: the Egypt-Saudi HVDC route boosts eastern desert works, while the EuroAfrica proposal enhances Mediterranean demand for converter station EPC.

Resource-driven dispersion shifts the historical concentration in the Nile Valley toward frontier zones. Contractors adapt to remote logistics, desert climates, and marine works, broadening expertise and reinforcing geographic diversification within the Egyptian power EPC market.

Regulatory Landscape

Egypts power-sector EPC activity is governed by Electricity Law No. 87 of 2015 and its executive regulations, which define licensing, market roles, and the pathway toward a more competitive structure under independent oversight. The Egyptian Electric Utility and Consumer Protection Regulatory Agency (EgyptERA) is the primary regulator for licensing and monitoring electricity production, transmission, and distribution, while the Ministry of Electricity and Renewable Energy (MOEE) sets sector policy and the Egyptian Electricity Holding Company (EEHC) anchors state-utility implementation.

Renewables project development is shaped by the Integrated Sustainable Energy Strategy (ISES 2035) and the institutional framework led by the New and Renewable Energy Authority (NREA). Recent policy anchors include Law No. 11 of 2022, which amended the NREA establishment law and the 2014 renewable generation law to facilitate private-sector participation, and Presidential Decree No. 628 of 2024, which allocated 350 square kilometers in the Red Sea Governorate to NREA for renewable energy projects. This supports a larger pipeline of wind and solar siting and related grid-connection EPC works.

Competitive Landscape

The Egyptian power EPC market shows moderate concentration. Local giants Elsewedy Electric and Orascom Construction leverage domestic supply chains and government ties. Siemens and GE secure turnkey contracts by bundling advanced turbines with project finance, as showcased by the 14.4 GW megaproject, which cut delivery time to 27 months and trained 6,000 Egyptian workers. Chinese entrants, led by PowerChina’s 1.1 GW Suez mandate, intensify competition through lower capex and vendor financing.

Local-content rules of 30% for renewables favor Egyptian fabricators of cables, towers, and civil works. Currency risk weeds out thin-margined players, giving the edge to firms with hedging programs and hard-currency revenues. Strategic alliances surge: Elsewedy partners with Schneider for smart grids, and Orascom teams with Rosatom for nuclear civil works. Niche firms specializing in storage, microgrids, and hydrogen balance-of-plant carve out defensible positions as the Egyptian power EPC industry evolves.

Egypt Power EPC Industry Leaders

Siemens AG

Mitsubishi Corp (Mitsubishi Hitachi Power Systems)

AMEA Power LLC

ElSewedy Electric Co -

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The active procurement shift toward hybrid renewables and flexibility assets is widening EPC scope beyond generation-only packages. In June 2026, Sterling and Wilson Renewable Energy, via a 50:50 joint venture with Hassan Allam Construction, secured a USD 560 million EPC contract for the 1,000 MWac West Minya solar project that includes a 600 MWh BESS. The Ministry of Electricity and Renewable Energy also highlighted concurrent additions combining 1,000 MW of renewables with 600 MWh of storage (including a 270 MW expansion at Benban).

Grid reinforcement and modernization remain central to converting contracted renewables into delivered energy, keeping substations, high-voltage lines, and control upgrades in the immediate EPC pipeline alongside utility plant upgrades. The World Bank's March 2024 approval of a USD 500 million grid reinforcement project and the EBRD financing under the NWFE platform support multi-governorate transmission and substation work, which favors EPC firms experienced with multilateral procurement and safeguards. New-build opportunities also extend through bankable PPAs and IPP-led renewables, such as ENGIEs March 2026 PPA with EETC for a 900 MW wind project near Ras Shokeir, and through SCZONE-linked power infrastructure for hydrogen and industrial loads, where EPC packages bundle renewables, power evacuation, and site utilities.

Recent Industry Developments

- June 2026: Sterling and Wilson Renewable Energy (SWREL) and Hassan Allam Construction, in a 50:50 joint venture, secured a USD 560 million EPC contract for the 1,000 MWac West Minya solar project, which includes a 600 MWh battery energy storage system. The award reinforces the shift toward solar-plus-storage EPC packages in Egypt, expanding scope into storage integration, grid compliance, and commissioning capabilities.

- April 2026: GE Vernova secured an order from Middle Delta Electricity Production Company to modernize the Banha and Nubaria power plants using Advanced Gas Path technology, alongside multiyear service agreements. The work extends EPC and outage-management demand around life-extension and efficiency upgrades for existing thermal assets, supporting generation reliability while renewable and grid projects scale.

- September 2024: AMEA Power reached financial close for its 1.4 GW green hydrogen project in Ain Sokhna, opening a large integrated EPC package spanning renewables, desalination, electrolysis, storage, and export infrastructure. The milestone strengthened the SCZONE-linked pipeline where power EPC contractors compete on multi-disciplinary balance-of-plant execution and complex interfaces.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Egypt power EPC market is defined as the value of engineering, procurement, and construction work delivered for power generation plants and transmission and distribution network projects executed within Egypt.

Scope exclusions: We exclude routine operations and maintenance, pure equipment-only sales with no EPC scope, and upstream fuel infrastructure that is not part of power-asset construction.

Segmentation Overview

- By Power-Generation Technology

- Thermal

- Nuclear

- Renewables

- By Capacity Band

- Up to 100 MW (DER, micro-grid)

- 100 to 499 MW

- Above 500 MW

- By End-User

- Regulated Utilities

- Independent Power Producers

- Industrial Captive Power

- Public Sector & SOE

- By Power Transmission and Distribution (T&D) - (Qualitative Analysis Only)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the project and demand context that sits behind EPC revenues in Egypt. We mainly relied on public sources such as electricity capacity and generation statistics from agencies like IEA, project and sector updates from IRENA, and macro indicators from the World Bank and IMF.

To keep assumptions grounded, we also reviewed regulator and ministry releases (such as national energy strategy notes), utility and developer announcements, and company filings and investor presentations for awarded contracts and completion timelines. Where needed, we used a paid subscription for company financials and a contracts and tenders database to cross-check award values and the timing of major packages. These desk research sources are illustrative, and we also drew on additional public references to collect, validate, and clarify specific data points.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to test what the desk data could not confirm, especially around EPC scope split between generation and grid works, typical contract structures, and how quickly prices are changing for key cost heads. We spoke with EPC contractors, project owners, engineering consultants, and supply chain participants across Egypt, and we rechecked inputs when there were timing mismatches between awards, financial close, and on-site execution.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | |

| Mid tier: 53% | Functional/Unit leaders: 40% | |

| Smaller Players: 20% | Managers: 44% |

Market-Sizing & Forecasting

Sizing was started using a top-down build that links Egypts power-build activity to EPC value, where capacity additions, grid expansion programs, and typical EPC cost ranges help reconstruct the annual revenue pool. The model was then stress-tested with selective bottom-up checks, including sampling recent project awards, using observed contract values, and applying realistic execution phasing before final totals were adjusted.

Key inputs used in the model include the pipeline of new generation capacity by technology, transmission and distribution investment plans, awarded and under-execution project counts, typical EPC scope split between civil, electrical, and balance-of-plant, and changes in import-dependent equipment costs that can shift EPC pricing. For forecasting, we used scenario analysis supported by a simple regression view on drivers such as electricity demand growth, planned capacity additions, and public capex intent, and then we confirmed the final path through expert expectations gathered during interviews. When project values were not disclosed, gaps were handled using comparable project benchmarks and conservative scope assumptions, and these were rechecked with primary feedback.

Data Validation & Update Cycle

Results were triangulated across multiple signals, and unusual jumps were flagged for a second review before sign-off. We compared the modeled market totals against independent markers such as announced awards, visible construction activity, and country-level investment and capacity trends. We also checked that implied EPC value per MW or per network-km stayed within a realistic band.

The work goes through multi-step analyst reviews, and follow-up calls are triggered when there is a large variance between desk indicators and interview feedback. Reports are refreshed annually, with interim updates when major policy, currency, or project award events materially change the outlook. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Egypt Power Epc Market Size Versus Other Published Estimates

Published market sizes for Egypt power EPC do not always match because teams may count different work scopes, use different base years, or treat pricing and currency timing in their own ways. Differences can also come from how each model treats project phasing, especially when awards are announced but execution stretches over several years.

Award announcements, tender trackers, and EPC value-per-MW reasonableness checks are used to keep Mordor Intelligence's estimate aligned with what is actually being contracted and executed in Egypt, rather than mixing in adjacent spending that sits outside EPC delivery. Another common gap driver is scope, since some estimates bundle long-term O&M, owner costs, or broader construction activity into the same figure, which can inflate the headline value quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.02 B (2025) | |

| Industry Database A | USD 3.36 B (2024) | Uses an earlier current-year point and appears to bundle EPC with EPC plus O&M in the same scope, which can shift the boundary and also changes how multi-year project execution is recognized into annual market value. |

| Market Publisher B | USD 714.67 B (2023) | The stated figure is not consistent with typical Egypt power project economics and likely reflects a scope or unit issue, such as mixing wider power construction spending, owner costs, or a different currency or scaling convention that is not normalized to EPC revenues. |

The spread across the three figures mainly comes down to what gets counted as EPC and how timing and units are handled. By keeping the market tied to disclosed awards, realistic execution phasing, and practical price and currency checks, the approach produces a number that is easier to trace back to clear drivers and update consistently year to year.

Key Questions Answered in the Report

What is the current value of the Egypt power EPC market?

The Egypt power EPC market size stands at USD 7.49 billion in 2026 and is forecast to rise to USD 10.36 billion by 2031.

Which technology segment is expanding fastest in Egypt?

Renewable energy EPC, particularly solar and wind, is growing at a 13.9% CAGR through 2031 due to the 42% clean-capacity target.

How does currency volatility affect EPC projects?

Depreciation of the Egyptian pound raised imported-equipment costs by about 58% in 2024, prompting contractors to hedge and renegotiate contract terms.

Where are the main geographic hotspots for new EPC work?

Greater Cairo for grid upgrades, Upper Egypt for utility-scale renewables, and the Suez Canal Economic Zone for hydrogen infrastructure lead current opportunities.

Which end-user group shows the highest growth?

Independent power producers are the fastest-growing customer group, expanding at a 12.35% CAGR on the back of competitive renewable auctions.

Page last updated on: