Eddy-Current Testing (ET) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

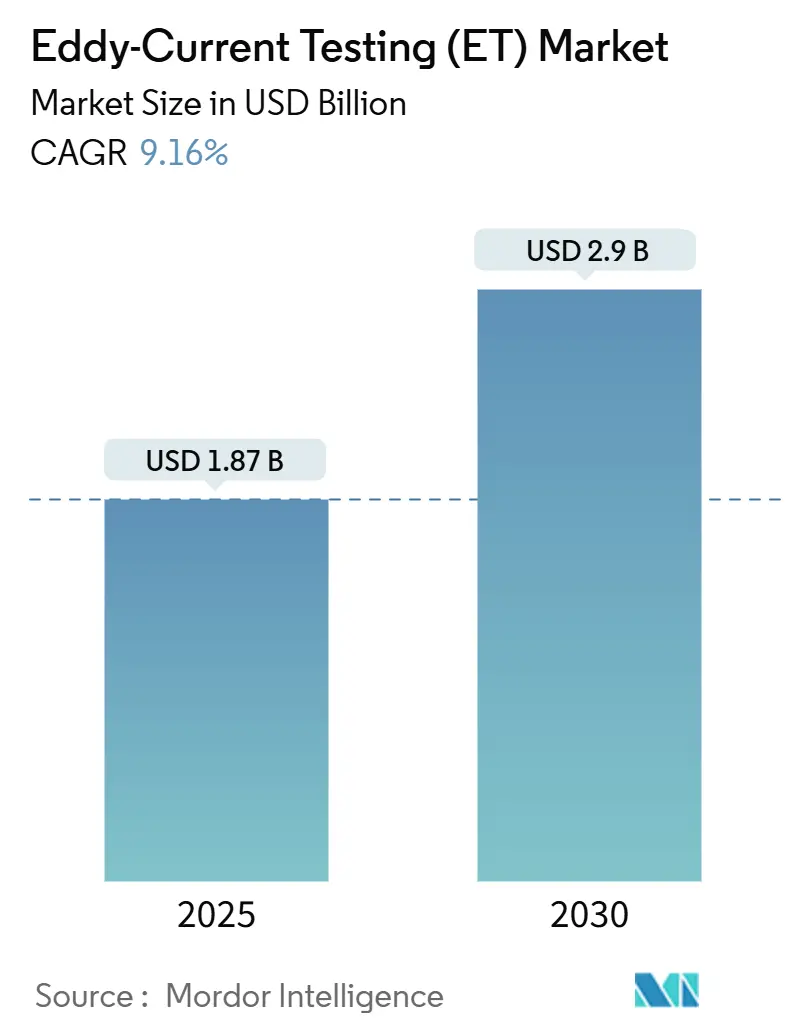

| Market Size (2025) | USD 1.87 Billion |

| Market Size (2030) | USD 2.9 Billion |

| Growth Rate (2025 - 2030) | 9.16% CAGR |

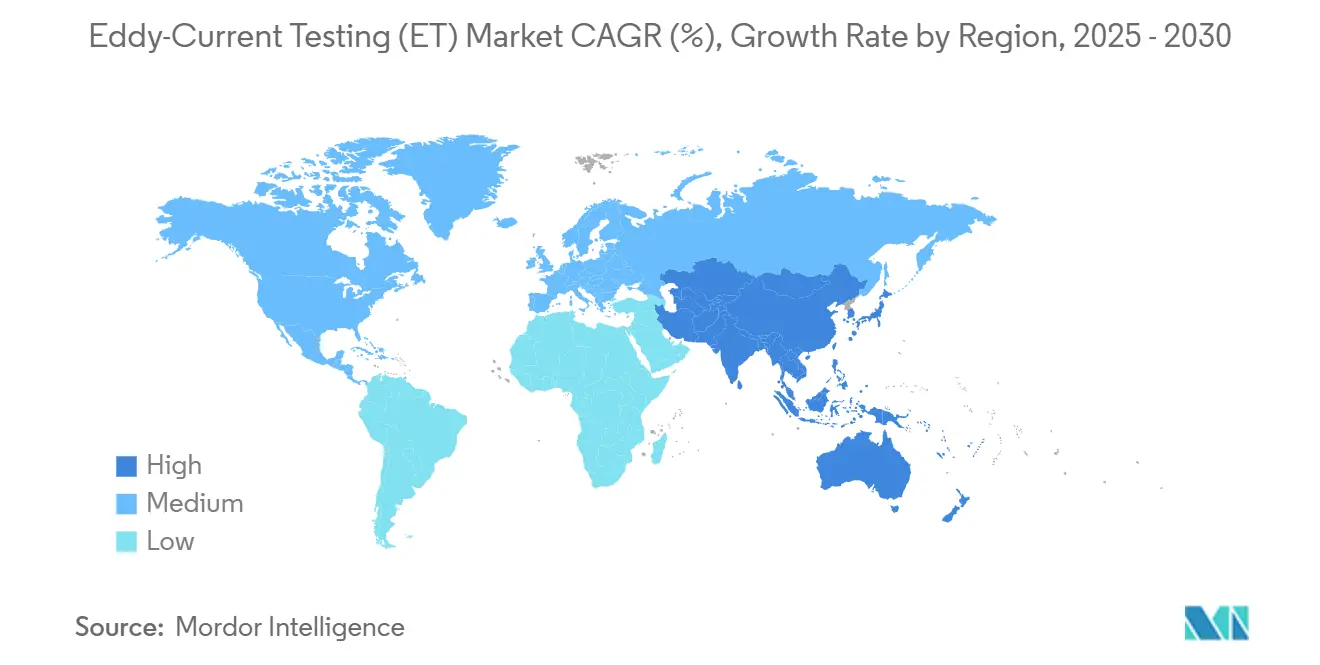

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

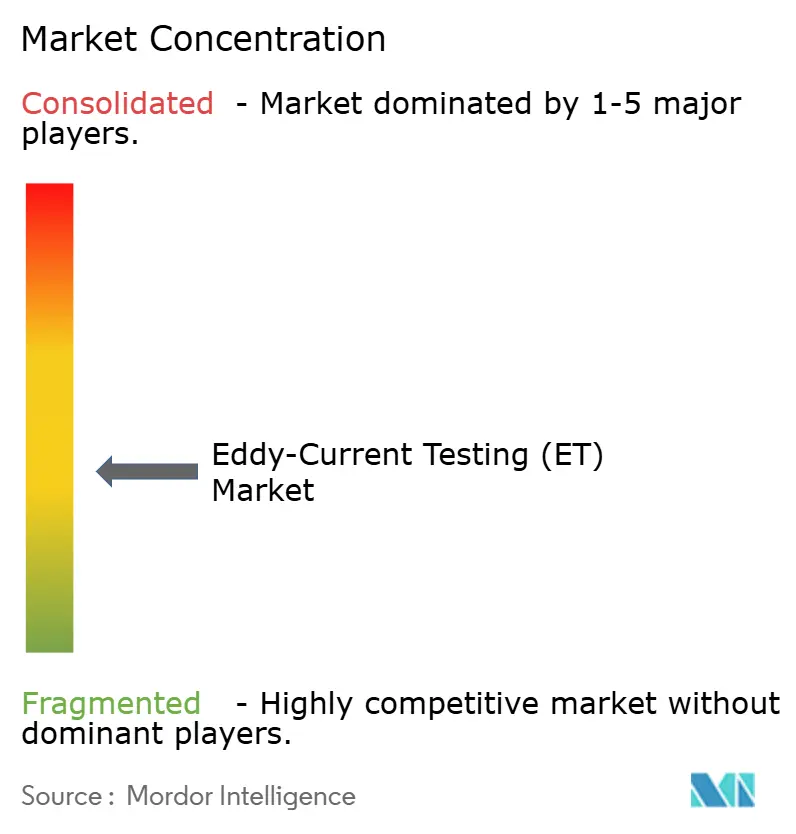

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eddy-Current Testing (ET) Market Analysis by Mordor Intelligence

The Eddy-Current Testing market size reached USD 1.87 billion in 2025 and is projected to advance to USD 2.9 billion by 2030, reflecting a 9.16% CAGR over the forecast period. This steep growth trajectory reflects the technology’s increasing importance in monitoring aging infrastructure, particularly where conventional inspection methods struggle to detect subsurface flaws. Growth catalysts include expanding aerospace maintenance programs, life-extension projects across oil and gas assets, and the rapid integration of Industry 4.0 digital frameworks that convert inspection data into predictive-maintenance intelligence. The Asia-Pacific region leads the regional race, supported by large-scale manufacturing automation and nuclear power investment, while portable and handheld systems dominate shipments due to their field versatility. Automated and robotic solutions, however, are capturing the strongest momentum as manufacturers embed inline quality checks to meet zero-defect mandates.

Key Report Takeaways

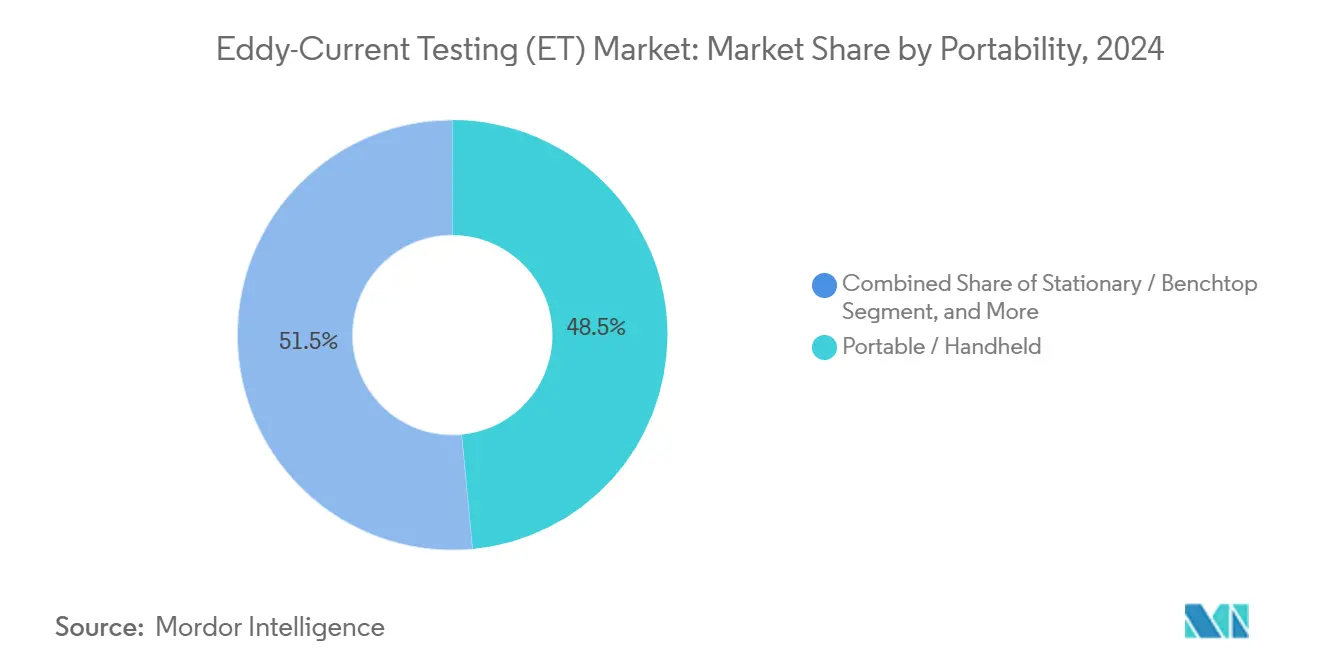

- By portability, portable and handheld systems captured 48.5% of the Eddy-Current Testing market share in 2024; automated and robotic platforms are forecast to expand at a 13.9% CAGR through 2030.

- By testing technique, conventional eddy-current methods led with 37.1% revenue share in 2024, while eddy-current array solutions register the highest projected CAGR at 14.2% to 2030.

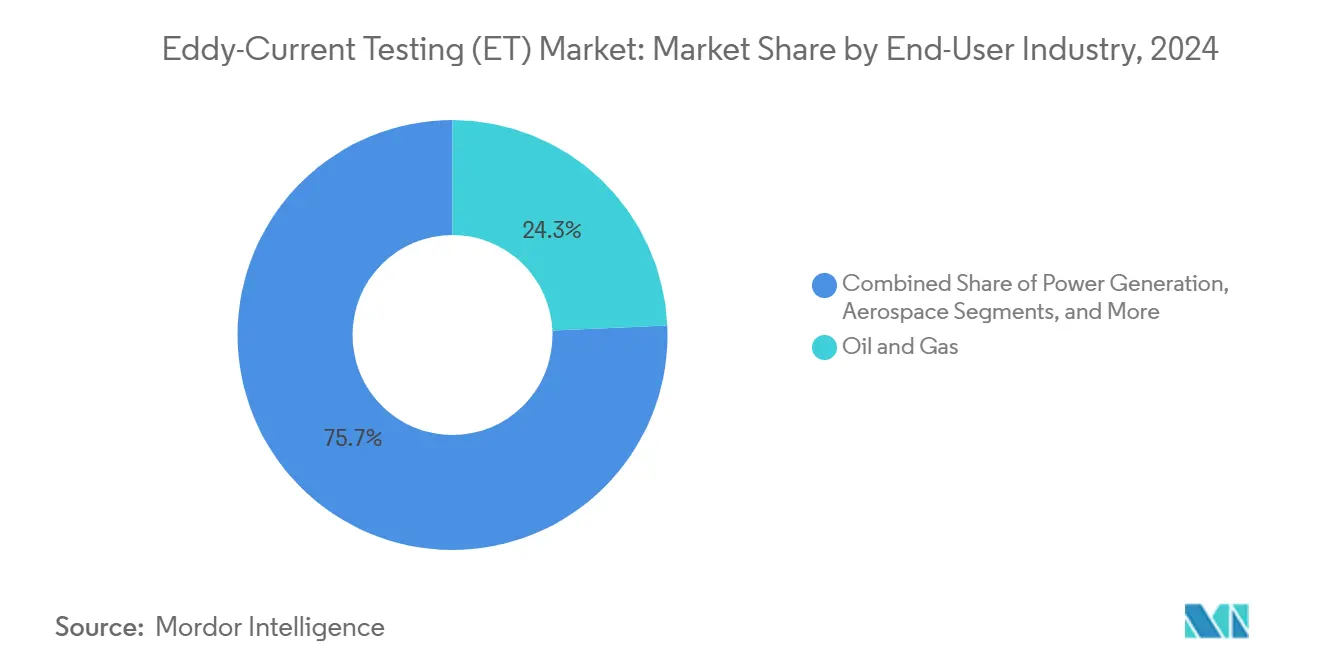

- By end-user industry, oil and gas accounted for 24.3% of the Eddy-Current Testing market size in 2024, whereas automotive and transportation are set to grow the fastest at 13.4% CAGR to 2030.

- By geography, Asia-Pacific held 37.4% revenue share in 2024 and is advancing at a regional-leading CAGR of 10.6% across the forecast horizon.

Global Eddy-Current Testing (ET) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace MRO demand for lightweight-alloy inspection | +1.8% | Global – North America and Europe core | Medium term (2-4 years) |

| Expansion of oil and gas life-extension projects | +2.1% | Global – North America, Middle East, Asia-Pacific | Long term (≥ 4 years) |

| Automation push in inline manufacturing quality control | +1.6% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Aging nuclear and power-generation assets | +1.4% | Global | Long term (≥ 4 years) |

| Industry 4.0 digital-twin adoption linking ET data | +1.2% | Advanced manufacturing regions | Medium term (2-4 years) |

| Stricter sustainability audits favoring non-contact NDT | +0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Aerospace MRO Demand for Lightweight-Alloy Inspection

Commercial and defense fleets now rely on carbon-fiber composites and aluminum-lithium alloys that demand higher-precision inspection than legacy metals. Recent NASA work confirmed that eddy-current arrays detect defects as small as 0.5 mm in aluminum-lithium panels, outperforming comparable ultrasonic tools.[1]NASA, “Eddy Current Array Applications for Spacecraft Component Inspection,” NASA Technical Reports, nasa.gov Regulatory bodies have tightened maintenance intervals on composite structures, creating repeat business for certified service vendors. Automated eddy-current rigs installed inside large airline hangars are reducing inspection time by 40% while enhancing reliability, promoting long-term adoption. The combination of surging passenger traffic, fleet renewals, and next-generation fighter procurement underwrites stable demand for eddy-current solutions through 2030.

Expansion of Oil and Gas Life-Extension Projects

Operators are diverting capital from green-field exploration toward maximizing mature assets, necessitating advanced corrosion-under-insulation (CUI) checks. Pulsed eddy-current tools now detect wall loss through up to 150 mm of insulation, eliminating costly stripping and reapplication steps. North American and Middle Eastern regulations are mandating more frequent inline assessments, while digitized sensor networks enable remote monitoring, reducing crew exposure in hazardous zones. These economic and compliance factors jointly drive long-term demand, resulting in a 2.1% CAGR increase for the Eddy-Current Testing market.

Automation Push in Inline Manufacturing Quality Control

Industry 4.0 programs prioritize zero-defect output, and inline eddy-current stations meet this goal at line speeds of up to 6 m/s, while maintaining defect sensitivity below 30 µm.[2]Salem Design and Manufacturing, “Eddy Current Inspection Machines,” salemndt.com Real-time rejection of flawed pieces saves downstream processing cost and embeds quality assurance inside the production flow. Machine-learning software refines probe settings on the fly, trimming false rejects that once discouraged automation. Adoption is most pronounced in Asia-Pacific steel and auto plants, but North American and European factories are following suit as energy and labor pressures sharpen focus on scrap reduction.

Adoption of Industry 4.0 Digital Twins Linking ET Data

Digital twins combine eddy-current waveforms with operational telemetry, such as temperature, vibration, and pressure, to create asset-health models that flag fatigue long before failure. Cloud analytics enable centralized teams to oversee remote facilities, while tamper-proof logs meet the requirements of ISO 9001 audits. Rotating machinery and pressure vessels benefit notably, as early-stage crack detection minimizes unplanned outages. These predictive capabilities are reshaping maintenance budgets, steering spending from periodic to condition-based programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of ET-certified technicians | -1.3% | Global – acute in North America and Europe | Long term (≥ 4 years) |

| High capital cost of multi-channel ET systems | -0.9% | Global – stronger in emerging markets | Medium term (2-4 years) |

| Limited penetration depth in ferromagnetic materials | -0.6% | Global | Long term (≥ 4 years) |

| Competition from ultrasonic phased-array solutions | -0.8% | Global – high-end applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of ET-Certified Technicians

Roughly 30% of certified inspectors are expected to retire within the next five years, yet the number of new certifications has decreased by 15% since 2022.[3]American Society for Nondestructive Testing, “NDT Workforce Development Report,” asnt.org Nuclear and aerospace work requires the highest certification levels, which can magnify bottlenecks. Training capacity is shrinking as vocational schools shelve NDT programs due to instructor shortages and capital costs. Vendors are fast-tracking AI-assisted interpretation to offset human gaps, but regulators still insist on qualified oversight for critical components, tempering the near-term relief offered by automation.

High Capital Cost of Multi-Channel Systems

Advanced array consoles can cost over USD 500,000, excluding probes, software, and operator training. Total ownership often doubles over a decade once calibration and maintenance are factored in. Small and mid-size manufacturers in emerging economies struggle to justify such outlays, restraining broader diffusion. Leasing and service-based offerings alleviate capex but carry premiums that elongate payback periods. Modular, incremental upgrades are helpful, yet they often trade off high-end capabilities that drive digital transformation benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability – Mobility Drives Market Leadership

Portable platforms remained the principal revenue contributor, accounting for 48.5% of the Eddy-Current Testing market share in 2024. Many field operators prefer handheld units that can access pipelines, airframes, or turbine blades without requiring the dismantling of assemblies. Continued advances in battery and electronics technology now enable these devices to rival benchtop sensitivity, offering multi-frequency operation in compact footprints. As a result, the Eddy-Current Testing market size generated by portable equipment continues to increase each year.

Automated and robotic stations, although smaller in absolute volume, are expanding at a 13.9% CAGR as production lines demand inspected-in quality. Integrated robots guide probes across hot steel or spinning shafts, a feat manual crews cannot achieve safely or repetitively. Suppliers embed AI routines that automatically tune coil parameters based on alloy and geometry, elevating productivity while alleviating technician shortages. Stationary systems, still prized for their lab precision, will hold niche roles where environmental control takes precedence over mobility.

By Testing Technique – Conventional Methods Face Array Competition

Conventional single-coil testing preserved 37.1% revenue share in 2024, thanks to broad technician familiarity and attractive cost profiles. These systems meet routine surface-crack hunts on aircraft wheels or heat-exchanger tubes. In contrast, eddy-current array solutions, growing at a 14.2% CAGR, sweep wider areas faster and map flaw geometry in greater detail, aligning with predictive-maintenance analytics. The Eddy-Current Testing market size linked to array platforms, therefore, climbs steeply as operators pursue throughput gains.

Pulsed variants dominate corrosion under insulation, where deep penetration proves vital, while alternating-current field measurement serves long-seam pipeline surveys. Remote-field and near-field array techniques target heat-exchanger tubes or ferromagnetic casings, bridging access constraints that traditional coils cannot overcome. Partial-saturation methods, although specialized, are increasingly attracting users who need to discriminate between surface and subsurface anomalies in thick ferrous parts.

By End-User Industry – Energy Sectors Lead Diverse Applications

Oil and gas installations led all verticals, accounting for a 24.3% share in 2024, driven by strict integrity-management regimes on thousands of miles of pipelines. Steam generators within nuclear plants and high-temperature boiler tubing in coal stations further bolster demand across the broader power-generation complex. Together, these segments reinforce the Eddy-Current Testing market and maintain service revenues resilient in the face of fluctuations in commodity prices.

Automotive and transportation applications, however, represent the fastest expansion at 13.4% CAGR. Battery casings, weld seams on aluminum bodies, and high-speed rail axles all require non-contact flaw detection that integrates smoothly into takt-time schedules. Aerospace commands premium pricing because composite skins and titanium bulkheads require ultrahigh sensitivity, but volumes lag behind those of mass-automotive plants. Manufacturing, defense, petrochemical, marine, and electronics users add a steady baseline demand that diversifies revenue streams and cushions sector-specific downturns.

Geography Analysis

The Asia-Pacific region held the largest regional share at 37.4% in 2024 and is expected to continue posting the fastest growth at a 10.6% CAGR. Heavy investment in high-speed rail, refinery upgrades, and new nuclear reactors keeps inspection activity brisk, while export-oriented automotive and electronics factories adopt inline eddy-current checks to secure foreign buyer quality audits. China anchors volume, Japan supplies high-precision niches, and India scales automotive uptake alongside infrastructure roll-outs.

North America ranks second, driven by life-extension campaigns on pipelines installed half a century ago and by rigorous aerospace maintenance mandates. Pulsed systems excel in detecting corrosion beneath insulators on long-haul oil pipelines crossing diverse terrains. Nuclear license renewals further lock in periodic steam-generator tube inspections, turning the Eddy-Current Testing market into a dependable service annuity.

Europe blends the modernization of legacy industrial plants with aggressive renewable energy build-outs. Wind-turbine blade and gearbox suppliers favor eddy-current array scans to preempt warranty claims, while automakers pursue inline coil stations to safeguard lightweight-alloy weld seams. Eco-centric regulations spur the adoption of non-contact NDT, which lowers scrap and conserves resources.

The Middle East and Africa experience healthy yet uneven growth. Gulf refineries and petrochemical complexes boost demand, but technician scarcity and budget constraints limit penetration in smaller states. South Africa’s mining and power sectors represent growth pockets ripe for portable systems. Latin America remains nascent; however, industrial upgrading in Brazil and Mexico suggests a potential future acceleration as manufacturers recognize the cost of defects in export markets.

Competitive Landscape

The Eddy-Current Testing market currently exhibits moderate fragmentation. Olympus Corporation, Eddyfi Technologies, ibg NDT Systems, and Zetec comprise the established core, but nimble automation specialists and regional service firms maintain high competitive pressure. Consolidation is underway as hardware vendors acquire software and robotics startups to offer turnkey inspection ecosystems rather than standalone boxes.

Artificial-intelligence modules that auto-classify signal indications now differentiate market leaders. For example, ibg’s multi-frequency AI Cube claims higher detection accuracy and lower false-positive rates than conventional rule-based filters.[4]ibg NDT Systems Corp., “Automatic Verification of Induction Hardening Using Eddy Current,” thomasnet.com Eddyfi’s nuclear-qualified array probes, validated through steam generator trials, open premium markets that carry stringent qualification requirements.

Strategic partnerships are common: equipment makers team up with integrators to place robots on automotive assembly lines, while cloud analytics firms collaborate with oil majors to harvest sensor data for digital twins. Price competition intensifies in commoditized portable gear, but high-end array consoles and nuclear-grade probes retain robust margins. Vendors that bundle financing, training, and maintenance contracts improve stickiness, especially in emerging markets where capital shortage hampers outright purchases.

Eddy-Current Testing (ET) Industry Leaders

Olympus Corporation

Eddyfi Technologies

Waygate Technologies (GE Inspection Technologies)

Zetec Inc.

Mistras Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Salem Design and Manufacturing released next-generation robotic eddy-current cells with embedded AI classification for automotive and aerospace lines.

- August 2024: Nanjing BKN Automation unveiled cost-effective offline flaw detectors priced at USD 40,000-150,000, targeting small manufacturers.

- June 2024: Eddywise integrated grade-sorting units with MES connectivity for real-time alloy verification.

- May 2024: German Society for Non-Destructive Testing published validation of eddy-current techniques on aged nuclear parts.

Global Eddy-Current Testing (ET) Market Report Scope

| Portable / Handheld |

| Stationary / Benchtop |

| Automated / Robotic |

| Conventional Eddy Current Testing |

| Eddy Current Array |

| Pulsed Eddy Current Testing |

| Alternating Current Field Measurement |

| Remote Field Testing |

| Near-field Testing / Near-field Array |

| Partial Saturation Eddy Current |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and semiconductor |

| Mining |

| Medical Devices |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Portability | Portable / Handheld | |

| Stationary / Benchtop | ||

| Automated / Robotic | ||

| By Testing Technique | Conventional Eddy Current Testing | |

| Eddy Current Array | ||

| Pulsed Eddy Current Testing | ||

| Alternating Current Field Measurement | ||

| Remote Field Testing | ||

| Near-field Testing / Near-field Array | ||

| Partial Saturation Eddy Current | ||

| By End-user Industry | Oil and Gas | |

| Power Generation | ||

| Aerospace | ||

| Defense | ||

| Automotive and Transportation | ||

| Manufacturing and Heavy Engineering | ||

| Construction and Infrastructure | ||

| Chemical and Petrochemical | ||

| Marine and Ship Building | ||

| Electronics and semiconductor | ||

| Mining | ||

| Medical Devices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Eddy-Current Testing market?

The market is valued at USD 1.87 billion in 2025.

What is the market's expected growth rate?

It is forecast to log a 9.16% CAGR, climbing to USD 2.9 billion by 2030.

Which region leads global demand?

The Asia-Pacific region holds a 37.4% share and posts the highest regional CAGR of 10.6%.

Which segment is growing the quickest?

Automated and robotic inspection platforms are expanding at a 13.9% CAGR.

What is the main restraint on market growth?

A global shortage of certified eddy-current technicians is curbing expansion.

How are companies addressing technician shortages?

Vendors embed AI analytics and robotic handling to cut reliance on manual interpretation.

Page last updated on: