Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

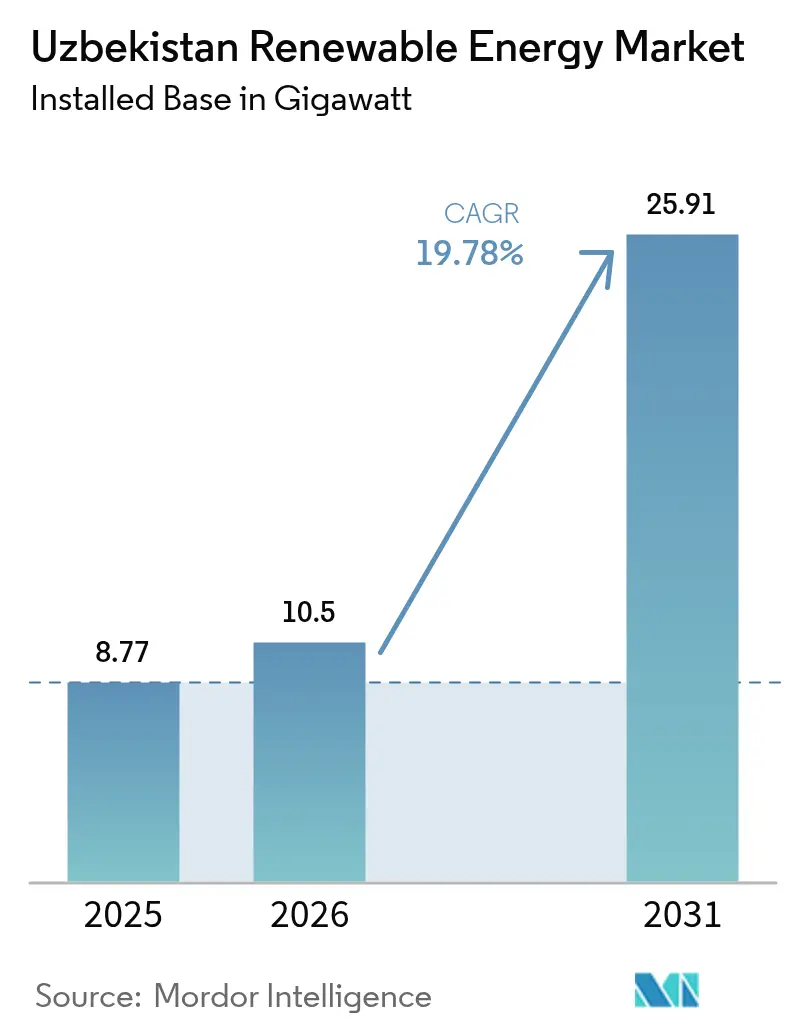

| Base Year Market Size (2025) | 8.77 gigawatt |

| Market Volume (2026) | 10.5 gigawatt |

| Market Volume (2031) | 25.91 gigawatt |

| Growth Rate (2026 - 2031) | 19.78% CAGR |

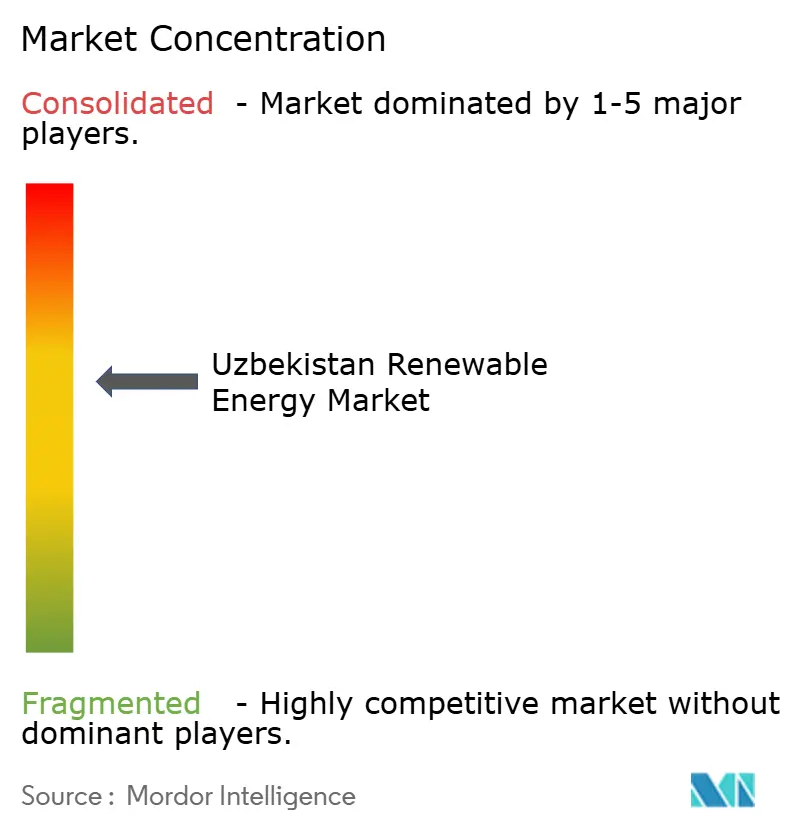

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uzbekistan Renewable Energy Market Analysis by Mordor Intelligence

The Uzbekistan Renewable Energy Market size in terms of installed base is expected to grow from 8.77 gigawatt in 2025 to 10.5 gigawatt in 2026 and is forecast to reach 25.91 gigawatt by 2031 at 19.78% CAGR over 2026-2031.

The Uzbekistan renewable energy market is expanding due to the government's increased commitment to renewables, with a goal of 54% by 2030, the accelerated retirement of thermal plants that have been in service for more than 30 years, and the prioritization of multilateral-backed solar and wind projects. Competitive tariffs in early tenders fell below USD 0.03 per kWh, drawing Gulf and Chinese developers that supply capital, engines, and EPC services. Declining domestic gas production and rising export opportunities further tilt the new generation toward renewables. Grid modernization, battery-storage bundling, and corporate demand for I-REC-certified power provide added momentum.

Key Report Takeaways

- By technology, solar energy led with 46.55% of the Uzbekistan renewable energy market share in 2025, while wind energy is projected to expand at a 36.96% CAGR through 2031.

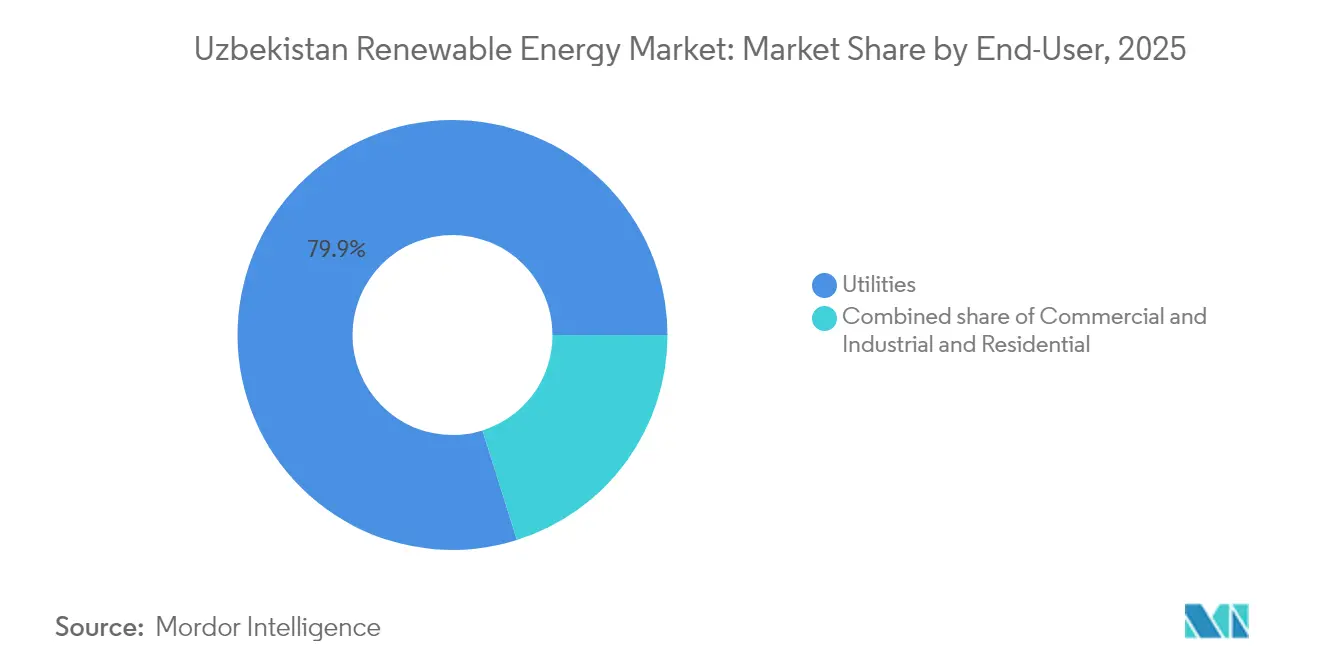

- By end-user, utilities accounted for an 79.85% share of the Uzbekistan renewable energy market in 2025, and they are forecasted to grow at a 21.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Uzbekistan Renewable Energy Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upcoming solar & wind tenders (2025-2029) | +4.2% | National, high in Bukhara, Navoi, Karakalpakstan, Samarkand | Short term (≤ 2 years) |

| Ambitious 25 GW renewable target by 2030 | +3.8% | National | Medium term (2-4 years) |

| Multilateral development-bank financing | +3.5% | National, priority in Jizzakh, Samarkand, Syrdarya | Medium term (2-4 years) |

| Grid-parity PPAs from textile exporters | +2.1% | Fergana Valley textile hubs | Medium term (2-4 years) |

| Cross-border green-hydrogen memoranda | +1.9% | Tashkent–Almaty corridor | Long term (≥ 4 years) |

| Declining domestic natural-gas production | +2.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Upcoming Solar and Wind Tenders Drive Investment Acceleration

The structured pipeline for 22 solar and wind stations under construction, totalling 9 GW, clarifies project sequencing and improves supply-chain planning for developers, thus catalyzing the Uzbekistan power market. Winning bids such as Masdar’s 300 MW Kashkadarya plant at 3.0 cents per kWh underscore a trend toward record-low tariffs that reinforce grid-parity economics.(1)Ministry of Energy of the Republic of Uzbekistan, “Kashkadarya solar tender results,” minenergy.uz Tender rules now require storage blocks of 100-500 MWh, embedding resilience in project design and smoothing variable generation curves. Payment guarantees issued through the National Electric Grid of Uzbekistan cut counterparty risk, which in turn unlocks competitively priced project debt from global lenders.

Ambitious 25 GW Renewable Target Reshapes the Energy Mix

The 25 GW target redirects capital flow toward clean assets and demands an annual build-out of roughly 3.5 GW, a rate that has never been attempted in Central Asia before.(2)International Energy Agency, “Uzbekistan renewable roadmap 2030,” iea.orgImplementation hinges on the Public-Private Partnership law of 2019 that secures long-term offtake and offers tax holidays, thereby lowering the hurdle rate for sponsors. Solar capacity will dominate at 12 GW, supported by wind (8 GW) and small hydro (5 GW), with each technology matched to region-specific resource endowments. Complementary plans to erect 2,700 km of transmission and modernise substations help accommodate energy flows from remote generation zones to urban load pockets.

Multilateral Development Bank Financing Unlocks the Project Pipeline

Annual commitments from the ADB, EBRD, and the World Bank exceed USD 2 billion and typically include risk-sharing structures, such as partial credit guarantees or political risk insurance. The Scaling Solar framework alone mobilised 1 GW of solar and 500 MW of wind between 2020 and 2024, proving the scalability of blended finance templates. Co-financing arrangements align currency baskets with power-purchase settlements, thereby limiting foreign exchange mismatch exposure for developers and the National Electric Grid of Uzbekistan.

Cross-Border Green-Hydrogen Memoranda Spur Export Ambitions

Agreements with Kazakhstan outline collaborative pathways for green hydrogen and associated ammonia exports, positioning western Uzbekistan as a synthetic-fuel bridge to Caspian Sea hubs.(3)Asian Development Bank, “Green hydrogen partnership MOUs,” adb.org Early studies highlight favorable wind speeds that can anchor co-located electrolyser complexes, complementing domestic demand growth while adding a new export revenue stream.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited grid transmission capacity | -2.8% | National, acute in Bukhara, Navoi, Karakalpakstan | Short term (≤ 2 years) |

| Currency-convertibility & offtaker bankability risk | -1.9% | National | Medium term (2-4 years) |

| Slow land-lease approvals at provincial hokimiyats | -1.3% | Provincial, particularly in Samarkand, Fergana, Kashkadarya | Short term (≤ 2 years) |

| Lack of local technical workforce and supply chain capacity | -1.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Grid Transmission Capacity Constrains Renewable Integration

Legacy grids were engineered for centralised thermal plants and now struggle to manage dispersed renewable inputs, creating curtailment risks in wind-rich Karakalpakstan. The Digitize to Decarbonize program, worth USD 125 million, introduces supervisory control systems that enhance dispatch flexibility. Construction of 944 km of new high-voltage lines and six substations is underway, yet commissioning delays could stall projects queued for connection. Real-time monitoring aims to reduce technical losses, currently pegged at 12-15% of generation, a prerequisite for the stable expansion of the Uzbekistan power market.

Currency Convertibility and Offtaker Bankability Create Investment Uncertainty

The som’s volatility, despite IMF Article VIII compliance, prompts lenders to demand hard-currency power-purchase contracts plus third-party guarantees. Planned bank-sector reforms intend to privatise 60% of state-owned banks by 2025 to deepen credit intermediation.(4)U.S. Department of Commerce, “Uzbekistan country commercial guide,” trade.gov Meanwhile, development banks extend local-currency tranches and hedging instruments that cushion forex shocks, although transaction costs remain elevated relative to markets with stable currencies. Tariff reforms scheduled through 2026 aim for full cost recovery, thereby improving the balance sheet of the National Electric Grid and lifting its credit profile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wind Acceleration Outpaces Solar Maturity

Solar held 46.55% of installed capacity in 2025 and remains the core of the Uzbekistan renewable energy market. Tariffs below USD 0.03 per kWh and high irradiation of more than 1,800 kWh /m² sustain this position. Wind is climbing faster, with a projected 36.96% CAGR to 2031, anchored by the 521.7 MW Zarafshan project and other large farms where average speeds reach 7–8 m/s. Hydropower operates at 2,382 MW and is expanding to 3,000 micro-hydro stations, which will add 160 MW by 2026, extending clean power to mountain villages. Bioenergy moves from pilot to portfolio scale, with eight waste-to-energy plants set to handle 4.7 million t of refuse and supply 2.1 billion kWh each year. Geothermal studies are still in their early stages, and ocean energy is not relevant in Uzbekistan, which is landlocked.

Utility-scale wind investment below USD 1.3 million per MW, combined with improvements in rotor technology, lowers the levelized costs, helping the segment close the price gap with solar. Storage pairing of 1,800 MW in 2025 tenders further levels dispatch profiles between the two resources. Solar developers test agrivoltaic models that integrate crop production, which may unlock additional land in densely farmed regions. Hydropower rehabilitation and new micro-hydro plants cater to off-grid demand without extensive transmission build. Bioenergy supports municipal waste goals and serves as a substitute for gas in baseload supply, complementing variable wind and solar energy.

By End-User: Utilities Anchor Growth, C&I Demand Emerges

Utilities owned 79.85% of capacity in 2025. Long-term PPAs with dollar indexing and sovereign backing enable high leverage and a forecast 21.83% CAGR. ACWA Power and Masdar each control multi-gigawatt pipelines that integrate solar, wind, and storage, confirming utility leadership in the Uzbekistan renewable energy market size statistics. Commercial and industrial buyers are starting to sign virtual PPAs after Uzbekistan’s 2025 entry into the I-REC system, with textile exporters being the most active as they prepare for EU carbon rules. Data centers in Tashkent also plan to install on-site solar plus storage to hedge against rising tariffs.

True bilateral wheeling remains absent because NEGU remains the sole buyer, so C&I deals rely on financial settlement. Even so, grid-parity economics improve as business tariffs rose in 2023 and residential rates climbed in 2024. Residential uptake remains low despite a 1,000-sum/kWh subsidy, as paybacks exceed eight years and consumer loans are scarce. Battery-based EV charging hubs, such as Huawei’s 720 kW station in Tashkent, may create new retail demand pockets and showcase distributed models that bridge the utility and commercial and industrial (C&I) segments.

Geography Analysis

Karakalpakstan leads wind development thanks to sustained speeds above 7 m/s, hosting ACWA Power’s Kungrad cluster and Masdar’s Zarafshan project that collectively exceed 1 GW and supply households across multiple provinces. Samarkand and Jizzakh emerge as solar heartlands, combining high irradiation with short interconnection distances to main load centres; EBRD-backed 220 MW farms and China Datang’s 263 MW facility illustrate the region’s appeal. The Fergana Valley experiences robust demand growth tied to export-oriented textile production, prompting firms to adopt captive solar and storage solutions to secure competitively priced electricity.

Tashkent province remains the principal demand node and hosts the largest announced battery storage facilities, providing ancillary services that stabilise the national grid. Southern oblasts, such as Kashkadarya and Surkhandarya, attract international sponsors through land availability and government incentives, and they benefit from ADB-supported urban infrastructure programs that incorporate energy-efficient public buildings. Navoi and Bukhara diversify their energy sources with hybrid solar-wind schemes tailored to resource complementarity, thereby enhancing their year-round output profiles.

Western regions face acute network congestion, necessitating the installation of 500 kV lines to evacuate power eastward. Multilateral agencies co-finance these backbones and integrate digital control layers that optimise power flow. The Kazakhstan-Azerbaijan-Uzbekistan green energy corridor remains a strategic priority that could channel up to 20 GW of renewable surplus toward European markets, translating local capacity growth into cross-border revenue. Rural areas still face access deficits, so decentralized solar home systems and mini-grids, financed by the UNDP, expand their social impact while enlarging the addressable base of the Uzbekistan power market.

Competitive Landscape

The sector exhibits moderate concentration, as JSC Uzbekgidroenergo retains control of legacy infrastructure and manages approximately 98% of current electricity needs; however, private capacity additions are diluting that dominance. ACWA Power pledges USD 15 billion and lines up multi-gigawatt solar-wind-storage ventures, while Masdar cements its foothold through competitively priced tenders, such as Zarafshan. Voltalia leverages hybrid clusters to capture value across day-night load cycles, underscoring an industry trend toward technology stacking.

White-space opportunities emerge in distributed generation for industrial estates, rural electrification packages, and ancillary-service storage systems. Chinese actors such as China Datang and PowerChina supply EPC expertise and tier-one modules, facilitated by diplomatic ties and cost advantages, thereby intensifying price competition. Technology differentiation centres on advanced battery chemistries and AI-enabled grid-management platforms that maximise renewable dispatchability. New entrants in the Uzbekistan power industry are targeting data analytics and predictive maintenance for wind farms, a niche that aligns with the rising operational complexity.

Policy consistency under the PPP framework ensures bankable cash flows that attract investors from Western, Gulf, and Asian regions alike. The financial close for a EUR 1.2 billion, 1.6 GW combined-cycle gas project illustrates ongoing fuel diversification and hedging against renewable intermittency. Meanwhile, state-led nuclear collaboration with France’s Orano on uranium mining seeks to secure future baseload options, adding another layer to the competitive mosaic.

Uzbekistan Renewable Energy Industry Leaders

JSC Uzbekgidroenergo

Masdar

Voltalia SA

TotalEnergies SE

ACWA Power

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ACWA Power commenced green hydrogen production at its pilot facility, with an annual capacity of 3,000 tonnes, in preparation for a 500,000-tonne ammonia plant in Chirchik.

- May 2025: The Ministry of Economy and Finance has signed a cooperation agreement with ILF Consulting Engineers to implement energy-efficiency upgrades across 149 public buildings nationwide.

- April 2025: ADB and AIIB agreed with Azerbaijan and Kazakhstan to fund feasibility studies for the Caspian Green Energy Corridor Project

- December 2024: Masdar inaugurated its 500 MW Zarafshan wind farm, which supplies 500,000 households and avoids 1.1 million tonnes of CO₂ per year.

Uzbekistan Renewable Energy Market Report Scope

Renewable energy sources include sources such as sunlight, wind, water movement, and geothermal heat that naturally replenish themselves on a human timescale. The market for renewable energy in Uzbekistan is growing quickly and is expected to reach a 40% share of renewable energy by 2030. Major investments in wind and solar projects, backed by goal alliances, are essential categories. The establishment of research institutions and innovation hubs is further enhancing technological breakthroughs. The evolution of the industry is driven by the need for a varied energy mix and growing energy demand. The combined components determine the scope and growth potential of the renewable energy industry in Uzbekistan.

The Uzbekistani renewable energy market is segmented by Technology (Solar Energy (PV and CSP), Wind Energy (Onshore and Offshore), Hydropower (Small, Large, PSH), Bioenergy, Geothermal, Ocean Energy (Tidal and Wave)), by End-User (Utilities, Commercial and Industrial, Residential). The report provides the installed capacity and forecasts in megawatts (MW) for all the aforementioned segments.

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large was renewable capacity in Uzbekistan at the end of 2026?

Installed renewable capacity reached 10.5 GW.

What is the forecast growth rate for renewable power through 2031?

Capacity is projected to expand at a 19.78% CAGR from 2026 to 2031.

Which technology segment is expected to grow the fastest?

Wind energy is forecast to post a 36.96% CAGR, the fastest of all segments.

What share of capacity did utilities own in 2025?

Utilities controlled 79.85% of total renewable capacity.

Why are corporate PPAs becoming more common?

Uzbekistan joined the I-REC system in 2025, allowing exporters to document green power use for EU carbon compliance.

What is the main barrier to faster deployment?

Limited grid transmission capacity, especially in remote solar and wind zones, is the leading short-term bottleneck.

Page last updated on: