Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

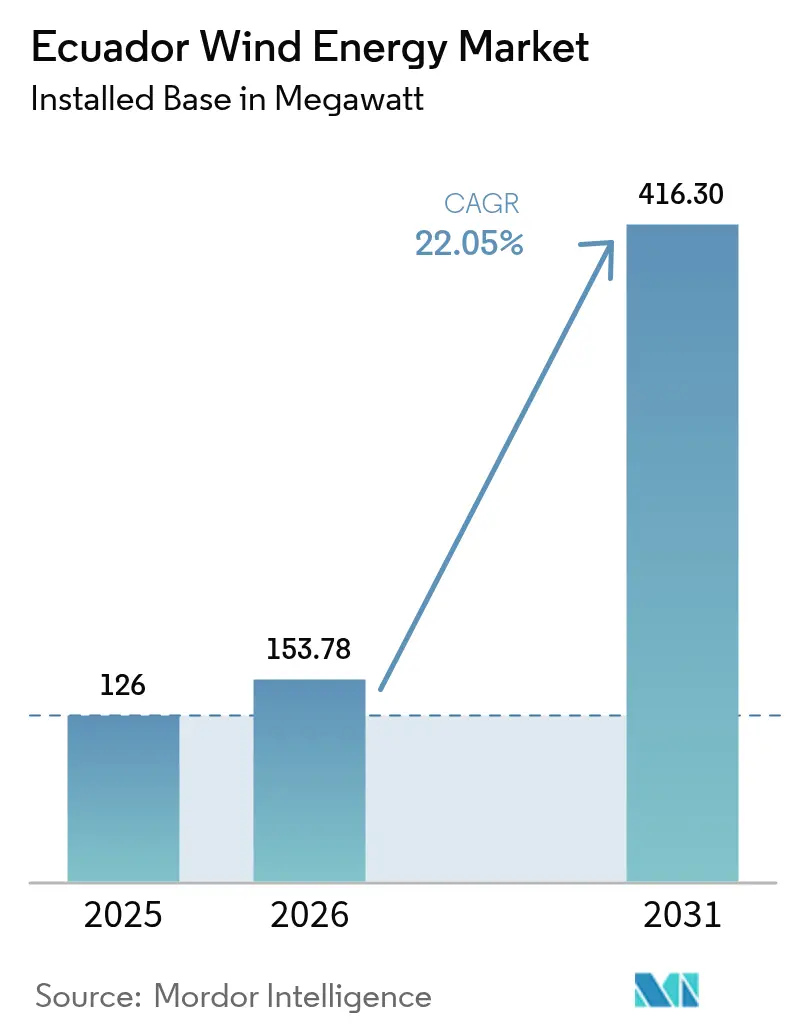

| Base Year Market Size (2025) | 126 megawatt |

| Market Volume (2026) | 153.78 megawatt |

| Market Volume (2031) | 416.3 megawatt |

| Growth Rate (2026 - 2031) | 22.05% CAGR |

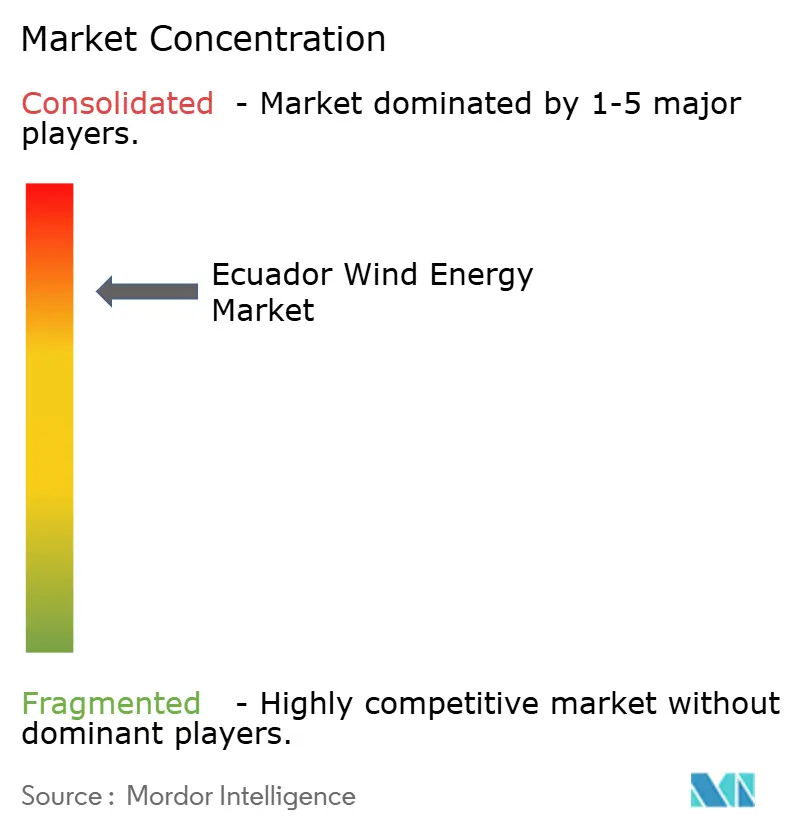

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ecuador Wind Energy Market Analysis by Mordor Intelligence

Ecuador Wind Energy Market size in 2026 is estimated at 153.78 megawatt, growing from 2025 value of 126 megawatt with 2031 projections showing 416.3 megawatt, growing at 22.05% CAGR over 2026-2031.

Growth is being propelled by the January 2024 Energy Competitiveness Law that lifted the private-project cap to 100 MW and extended generous feed-in tariffs through 2030, a policy combination that compresses development timelines and delivers bankable long-term offtake structures.[1]US Trade Administration, “Ecuador – Energy,” trade.gov Emergency procurement rounds launched during the 2023-2024 drought underscored the grid’s over-reliance on hydropower and opened a path for wind to diversify the generation mix. Grid-strengthening investments, multilateral credit guarantees, and accelerating turbine up-scaling toward 3-6 MW platforms are steadily lowering levelized costs, while state utility CELEC EP’s pivot to public-private partnerships is attracting foreign developers despite Ecuador’s shallow domestic capital markets. At the same time, community opposition around fishing-rights conflicts and transmission congestion in the Manabí–Santa Elena corridor remains a headwind that developers must navigate.

Key Report Takeaways

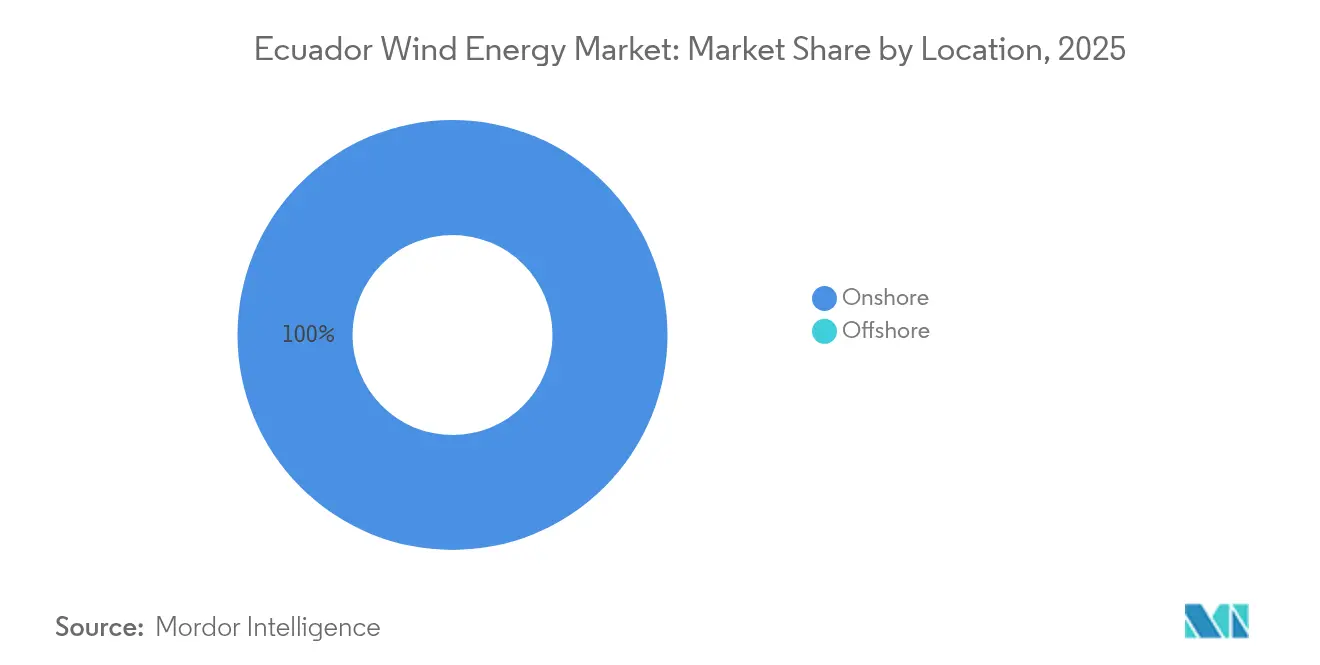

- By location, onshore installations represented 100.00% of capacity in 2025 and are advancing at a 22.03% CAGR through 2031.

- By turbine class, units rated up to 3 MW held 84.45% of Ecuador's wind energy market share in 2025, while the 3-6 MW segment is projected to expand at a 42.65% CAGR to 2031.

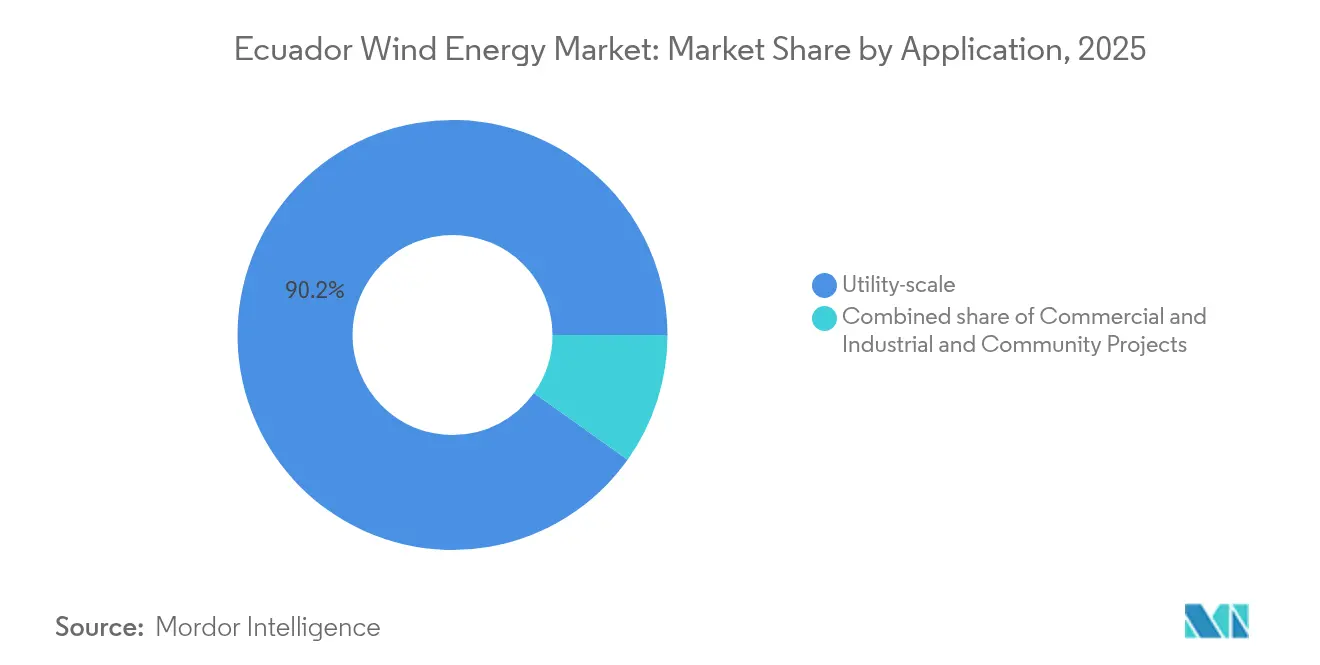

- By application, utility-scale projects commanded 90.15% of capacity in 2025 and are forecast to grow at 23.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ecuador Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generous feed-in tariff extension through 2030 | +5.7% | National, with early gains in Loja, Manabí, Santa Elena | Medium term (2-4 years) |

| Accelerated grid-interconnection program for coastal provinces | +4.5% | Manabí, Santa Elena, Guayas coastal corridor | Short term (≤ 2 years) |

| Falling levelized cost of energy for ≥5 MW turbines | +4.1% | Global, direct pass-through to Ecuador project economics | Long term (≥ 4 years) |

| Strong multilateral climate-finance pipeline | +3.4% | National, IDB and World Bank priority provinces | Medium term (2-4 years) |

| Port of Posorja nacelle-assembly free-trade zone incentives | +2.5% | Guayas province, with national supply-chain spillover | Long term (≥ 4 years) |

| Offshore wind pre-feasibility data-sharing pact with Peru & Colombia | +1.2% | Pacific coastal waters, Manabí and Santa Elena offshore zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generous Feed-in Tariff Extension Through 2030

The Energy Competitiveness Law locks in cost-reflective pricing for renewable generators to 2030 and raises the private-project size ceiling to 100 MW, allowing developers to avoid lengthy public tenders and secure bilateral power purchase agreements (PPAs) with mining and aquaculture offtakers.[2]US Trade Administration, “Ecuador – Energy,” trade.gov Fixed-price 25-year PPAs mitigate merchant-price risk in Ecuador’s shallow capital markets, unlocking the USD 500–700 million of private investment the World Bank expects will be needed to double non-hydro renewable capacity by 2028.[3]World Bank, “World Bank Approves $500 Million to Support Ecuador’s Energy Transition,” worldbank.org The Inter-American Development Bank (IDB) backs the tariff regime with a USD 77 million partial-credit guarantee that shields lenders from payment default, though credibility rests on the state’s ability to honor contracts after 500 MW of 2021 awards lapsed unsigned.[4]Inter-American Development Bank, “Partial Credit Guarantee for Non-Conventional Renewable Energy Projects,” iadb.org

Accelerated Grid-Interconnection Program for Coastal Provinces

CELEC EP earmarked USD 79 million in June 2025 to reinforce seven transmission projects that relieve the Manabí–Santa Elena bottleneck, currently curtailing wind dispatch during peak shrimp-farming demand. Complementing this, IDB Invest is financing a USD 56.5 million 500 kV Peru–Ecuador intertie slated for 2026 service, creating a southern export valve that reduces congestion risk. Because wind output peaks at dusk when hydropower reservoirs also flex, added transfer capacity is critical to integrate the forecast 279 MW of new wind by 2030.

Falling Levelized Cost of Energy for ≥5 MW Turbines

Global onshore wind LCOE averaged USD 0.033 kWh in 2023 after a 60% decline since 2010, driven by taller towers and longer blades that spread fixed costs across larger nameplates. In Latin America, costs remain modestly higher at USD 0.046 kWh, but Chinese original equipment manufacturers (OEMs) such as Goldwind and Mingyang price 5-6 MW platforms 15–20% below European competitors, improving project economics in Ecuador’s high-interest-rate environment. With diesel peakers topping USD 0.12 kWh during droughts, wind’s cost edge is material for a grid seeking to curb fuel-import exposure.

Strong Multilateral Climate-Finance Pipeline

IDB, World Bank, and the Development Bank of Latin America collectively commit more than USD 1 billion to Ecuador’s energy transition, supplying long-term debt that domestic banks cannot extend. The IDB partial-credit guarantee lets private lenders fund 10-15 year amortizations while offloading sovereign risk, replicating structures that underpinned USD 2–3 billion of renewable build-out in Colombia and Peru between 2020 and 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shallow domestic capital markets and high financing costs | -2.7% | National, affecting all utility-scale projects | Medium term (2-4 years) |

| Limited transmission capacity in Manabí-Santa Elena corridor | -2.3% | Manabí, Santa Elena, Guayas coastal provinces | Short term (≤ 2 years) |

| Community opposition tied to coastal fishing-rights conflicts | -1.8% | Coastal provinces with artisanal fishing activity (Manabí, Santa Elena, Esmeraldas) | Medium term (2-4 years) |

| Slow permitting for avian-migration impact assessments | -1.5% | National, particularly biodiverse coastal and highland zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shallow Domestic Capital Markets and High Financing Costs

Ecuadorian banks seldom lend beyond 10 years, forcing wind sponsors to raise 40–50% equity or seek offshore debt that carries currency-hedge costs despite dollarization. Sovereign risk perceptions widen spreads 200–300 basis points above regional averages, constraining financial close for utility-scale projects and capping the Ecuador wind energy market’s pace of build-out.

Limited Transmission Capacity in Manabí–Santa Elena Corridor

The coastal corridor operates near its thermal limit during shrimp-industry evening peaks, forcing curtailment or negative pricing for wind farms. CELEC EP’s seven-project reinforcement plan will unfold over 24–36 months, meaning congestion remains a short-term drag on the Ecuador wind energy market. Until the Peru–Ecuador 500 kV link relieves southbound flows in 2026, developers must assume higher curtailment risk in financial models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Onshore Monopoly Persists Through Forecast Horizon

Onshore projects accounted for 100.00% of 2025 capacity and will continue growing at 22.03% annually, keeping the Ecuador wind energy market squarely land-based through 2031. A tri-national offshore pre-feasibility pact with Peru and Colombia is collecting seabed data, yet floating foundations would carry 40–50% cost premiums and protract lead-times beyond 2032. Coastal onshore sites in Manabí and Santa Elena offer 7 m s-1 wind speeds at 80 m hub height and existing 230 kV substations, letting sponsors avoid submarine cables and expensive offshore logistics.

The Ecuador wind energy market size for onshore projects is projected to rise from 126 MW in 2025 to 416.3 MW in 2031 as permitting hurdles, not resource scarcity, set the cadence. Environmental baseline studies mandated under Ecuador’s Rights of Nature clause now extend impact-assessment timelines by 6–12 months, and recent referendums blocking extractive projects signal a politicized permitting environment that could lengthen schedules for wind farms near sensitive habitats.

By Turbine Capacity: Mid-Range Machines Capture Scale Shift

Turbines up to 3 MW represented 84.45% of the Ecuador wind energy market share in 2025, owing to legacy Villonaco units, yet the 3-6 MW class is growing 42.65% annually and will dominate utility-scale builds by 2031. Upscaling cuts balance-of-system costs 25–30% by slashing foundation counts, trenching, and O&M labor, advantages magnified in a capital-scarce market.

Ecuador wind energy market size for 3-6 MW turbines is forecast to eclipse the sub-3 MW fleet once 110 MW of Villonaco II & III capacity enters service after 2027. Above-6 MW machines remain improbable before 2030 because haul roads and cranes capable of lifting 100-ton nacelles are absent. The Port of Posorja free-trade zone could localize nacelle assembly, trimming logistics surcharges, but no OEM has yet committed capital.

By Application: Utility-Scale Projects Dominate Pipeline and Offtake

Utility-scale wind farms controlled 90.15% of installed capacity in 2025 and are set to increase at 23.3% annually, sustained by CELEC EP tenders and 25-year avoided-cost indexed PPAs that anchor bank financing. Net-metering gaps and the absence of community-ownership frameworks limit commercial-and-industrial (C&I) and cooperative penetration to under 10% of additions.

Ecuador's wind energy market size allocated to C&I users could improve if the 2024 draft net-billing regulation is enacted, letting surplus generation earn wholesale credits. Meanwhile, community projects under 10 MW are excluded from IDB guarantees, forcing higher equity shares that dilute returns. PPAs for utility-scale assets, therefore, remain the market's growth engine provided contract sanctity is upheld.

Geography Analysis

Wind capacity clusters in Loja’s Andean highlands and the Manabí–Santa Elena coastal belt, where trade winds average 7–8 m s-1 at 80 m. The coastal corridor should absorb 60–70% of new megawatts through 2031 due to substation proximity and co-location synergies with shrimp aquaculture off-takers. Yet congestion on the single-circuit line connecting both provinces caps dispatch until USD 79 million in scheduled upgrades are completed in 2027.

Loja, home to the pioneer 16.5 MW Villonaco wind farm, delivers high-elevation wind speeds but incurs 5–10% extra transport costs for 60-m blades over mountain passes. The province remains pivotal as Villonaco III proceeds, yet its 300 km distance from Guayaquil obliges long-haul transmission that elevates line-loss charges. The Peru–Ecuador 500 kV intertie landing near Loja will relieve those constraints by 2026, though hydro imports will compete for the same capacity.

Guayas province, anchored by the deep-water Port of Posorja, offers a manufacturing hub to cut Ecuador wind energy market logistics costs by 20–30% through in-country assembly. However, lacking domestic-content mandates in tenders diminishes OEM incentive to build locally. Draft 2024 regulations proposing 20–30% local-value thresholds face push-back from developers worried about cost inflation, leaving Guayas’ industrial promise unrealized.

Regulatory Landscape

Ecuador's wind power regulatory framework is anchored in the Organic Law of the Public Electric Power Service (LOSPEE) and reinforced by the January 2024 Energy Competitiveness Law, which increased the ceiling for private renewable projects to 100 MW and supported longer-tenor revenue structures through extended tariff provisions. Sector oversight and rulemaking sit with ARCERNNR/ARCONEL and the Ministry of Energy and Mines, while environmental licensing remains coordinated with the Ministry of Environment, Water and Ecological Transition, where Rights of Nature-related impact-assessment requirements have become more prominent.

For new wind projects, the key implementation layer is the set of technical and commercial rules for Non-Conventional Renewable Energy (NCRE) projects in the 10-100 MW range outside the Electricity Master Plan, complemented by ARCERNNR-008/23 for distributed generation interconnection and self-supply. Recent norms also codify a grid-integration requirement for intermittent NCRE, obliging projects such as wind to incorporate Battery Energy Storage Systems (BESS) at the connection point, shaping both permitting packages and bankability requirements for new capacity additions.

Competitive Landscape

Ecuador’s wind segment is highly concentrated. State-owned CELEC EP controls the only operating project and the largest pipeline asset, wielding first-mover advantage and grid-connection leverage. To accelerate build-out, the utility approved regulations in July 2024 permitting associative processes, effectively opening the Ecuador wind energy market to public-private partnerships while retaining state oversight.

Foreign developers such as Neoen, Total Eren, and EDP Renováveis are pre-qualifying for the 200 MW Pimo tender, but weigh sovereign counterparty risk after 2021 awards lapsed unsigned. OEM rivalry centers on unit price and financing. Chinese suppliers Goldwind and Mingyang undercut Siemens Gamesa and Vestas by 15–20%, yet European firms maintain share through embedded service fleets familiar with IDB procurement requirements.

Supply-chain ethics emerged as a differentiator after an October 2024 investigation linked balsa-wood sourcing for turbine blades to illegal logging in Yasuní indigenous territories. OEMs with certified plantation supply showcase environmental compliance, positioning competitively for tenders that now score non-price sustainability criteria. Storage integrators are additional disruptors, bundling 2–4 h lithium-ion systems with wind to firm capacity at declining battery prices of USD 150–180 kWh, an attractive hedge against curtailment during coastal congestion.

Ecuador Wind Energy Industry Leaders

CELEC EP

Neoen SA

Siemens Gamesa Renewable Energy, S.A.

Xinjiang Goldwind Science & Technology Co. Ltd.

Vestas Wind Systems A/S

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity centers on converting Ecuador's utility-scale wind pipeline into financed construction under public-private structures and development-finance-backed arrangements. A clear signal is Villonaco III in Loja, where an addendum to the project contract signed in January 2025 reactivated the development, and in June 2026 Cobra, through Villonacoenergy, pursued IDB Invest financing for the 112 MW project within a stated USD 200 million total investment. This financing-led pathway fits Ecuador's dependence on multilateral credit enhancement to offset shallow domestic tenors and support long-dated PPAs for wind.

A second opportunity involves new-build designs that treat grid and intermittency constraints as embedded requirements rather than external risks. The BESS requirement for intermittent NCRE projects, combined with the Manabi-Santa Elena corridor transmission congestion referenced in the report context, creates space for hybrid wind-plus-storage configurations that can improve dispatchability and reduce curtailment exposure at the interconnection point. On public procurement and planning, the Electricity Master Plan 2023-2032 provides the enabling backdrop for renewable additions to the National Interconnected System, while CELEC EP's Corporate Wind Plan activities and project-level feasibility work, including work around El Pimo, keeps a utility-scale pipeline active across provinces beyond the legacy Loja cluster.

Recent Industry Developments

- June 2026: Cobra, through Villonacoenergy, sought IDB Invest financing for the Villonaco III wind project in Loja, positioning the 112 MW development for financial close through development-finance channels. The financing push underscores the market's dependence on multilaterals to underwrite tenors and risk allocation that local lenders typically do not provide. It also moves the project pipeline referenced in the broader analysis beyond legacy sub-3 MW fleets toward larger utility-scale additions.

- February 2026: CELEC EP issued a request for quotations for a feasibility study for the El Pimo wind project, an estimated 150 MW facility in Azuay province. This step expands the state-led pipeline beyond the established Loja and coastal corridors and formalizes pre-investment work needed for bankable permitting and grid-connection design. The feasibility stage also sets expectations for early integration of environmental and interconnection requirements that can govern project timelines.

- October 2024: Ecuador's National Assembly passed the Organic Law to Promote Private Initiative in Electricity Generation, expanding incentives for renewables and easing pathways for private projects up to 100 MW. The legislation strengthened the commercial rationale for bilaterally contracted wind projects by reducing procedural friction and improving after-tax economics for developers. It also aligns with the report context shift toward public-private participation alongside CELEC EP's role in planning and grid access.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Ecuador wind energy market is defined as wind power capacity built and operating in the country, tracked in megawatts, along with the activity directly tied to developing, installing, and running wind farms.

Scope exclusions: We exclude broader power generation revenues, transmission and distribution investments, and non-wind renewables unless they are directly required to connect or operate wind projects.

Segmentation Overview

- By Location

- Onshore

- Offshore

- By Turbine Capacity

- Up to 3 MW

- 3 to 6 MW

- Above 6 MW

- By Application

- Utility-scale

- Commercial and Industrial

- Community Projects

- By Component (Qualitative Analysis)

- Nacelle/Turbine

- Blade

- Tower

- Generator and Gearbox

- Balance-of-System

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to pin down the fact base that sits under capacity additions, project timing, and operating status for Ecuador. We relied on public and official sources such as IRENA statistics, the Global Wind Energy Council, IEA power sector indicators, World Bank country energy data, and public releases from Ecuador energy authorities and regulators.

We also reviewed developer and utility press releases, project environmental filings where available, lender and multilateral announcements, and grid connection updates that help confirm whether a project is moving from pipeline to commissioning. In addition, we used a paid subscription for company financials and another paid subscription for patent and technology signals to support checks around turbine class shifts and supplier activity. The desk sources listed here are illustrative, and many other public documents were also used for data capture, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured questionnaires with developers, EPC and O&M participants, grid and permitting specialists, and large electricity offtakers. These discussions were used to confirm commissioning dates and translate what respondents said into utilization and curtailment assumptions, including how often plans shift due to permitting and grid readiness. That feedback then feeds back into the forecast model for Ecuador wind projects.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 44% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 33% |

| Smaller Players: 16% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down rebuild of Ecuador wind capacity using the installed base plus expected net additions, where project pipelines are filtered by permitting progress, financing readiness, and realistic grid interconnection timing. Once that backbone is set, selective bottom-up approximations are used as a check, such as summing known project MW, testing typical turbine nameplate ratings by site, and sanity-checking timelines through EPC and developer feedback.

Key inputs used in the model include installed capacity by project, expected commissioning schedule, turbine capacity bands used in new builds, typical capacity factor ranges by wind resource zone, curtailment and grid constraint expectations, and policy or auction signals that can change the pace of awards. For forecasting, scenario analysis is applied around the pipeline conversion rate and connection lead times, and then the final path is chosen based on what primary respondents see as the most likely build-out sequence over the next few years. Where project details are incomplete, assumptions are kept conservative and are only relaxed when multiple independent confirmations point in the same direction.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the model output and independent signals, such as published capacity totals, project commissioning announcements, and grid connection milestones in Ecuador. Outliers are reviewed in a second analyst pass, and we re-contact sources when a large variance shows up, such as a project moving dates, changing turbine class, or pausing due to permitting.

The report is refreshed annually, and material events are monitored in between so assumptions can be revisited when needed. Before delivery, a final review is completed to ensure the latest public updates and primary feedback are reflected in the sizing and forecast.

Mordor Intelligence's Ecuador Wind Energy Market Size Compared Against Other Published Estimates

Published market sizes for Ecuador wind energy can look far apart because the underlying unit and scope are not always the same, even when the titles sound similar. Differences also come from how pipeline projects are treated, how commissioning timing is handled, and whether the market is measured as installed MW or as revenue.

By tracking commissioning-linked installed MW and refreshing project status checks, Mordor Intelligence keeps the market total anchored to what is operating or credibly expected to enter operation in the stated year, which tends to diverge from revenue-based totals that also bundle equipment and service spending.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.15 B (2026) | |

| Global Consultancy A | USD 0.28 B (2023) | Uses revenue in USD as the main measure and appears to include broader value-chain spending, so the number is not directly comparable to an installed-capacity view, and the base year is earlier. |

| Industry Publisher B | USD 0.08 B (2026) | Presents a smaller 2026 value, which can happen when only near-term awarded or financed projects are counted and when grid-connection slippage is treated more conservatively in the pipeline conversion. |

The table shows that the spread is mostly explained by unit choice and pipeline treatment, rather than a disagreement on Ecuador moving toward more wind capacity. When the market boundary is held to installed MW by year and checked against project readiness signals, the sizing steps stay easy to repeat and easier to audit.

Key Questions Answered in the Report

How large is the Ecuador wind energy market today?

Installed capacity stood at 153.78 MW in 2026 and is set to reach 416.3 MW by 2031.

What CAGR is forecast for Ecuador’s wind build-out?

Capacity is projected to expand at 22.05% annually between 2026 and 2031.

Which province will add the most wind megawatts by 2031?

Manabí and Santa Elena together are expected to host 60–70% of new capacity once grid upgrades finish.

Who is the dominant player in Ecuador’s wind segment?

State-owned CELEC EP controls existing capacity and leads the largest pipeline projects.

What is the biggest barrier to wind investment in Ecuador?

High financing costs from shallow domestic capital markets remain the primary drag on project bankability.

How do larger 5–6 MW turbines affect project economics?

They cut balance-of-system costs by 25–30% versus older 2–3 MW units, sharply lowering levelized cost of energy.

Page last updated on: