Polyethylene Terephthalate (PET) Beverage Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

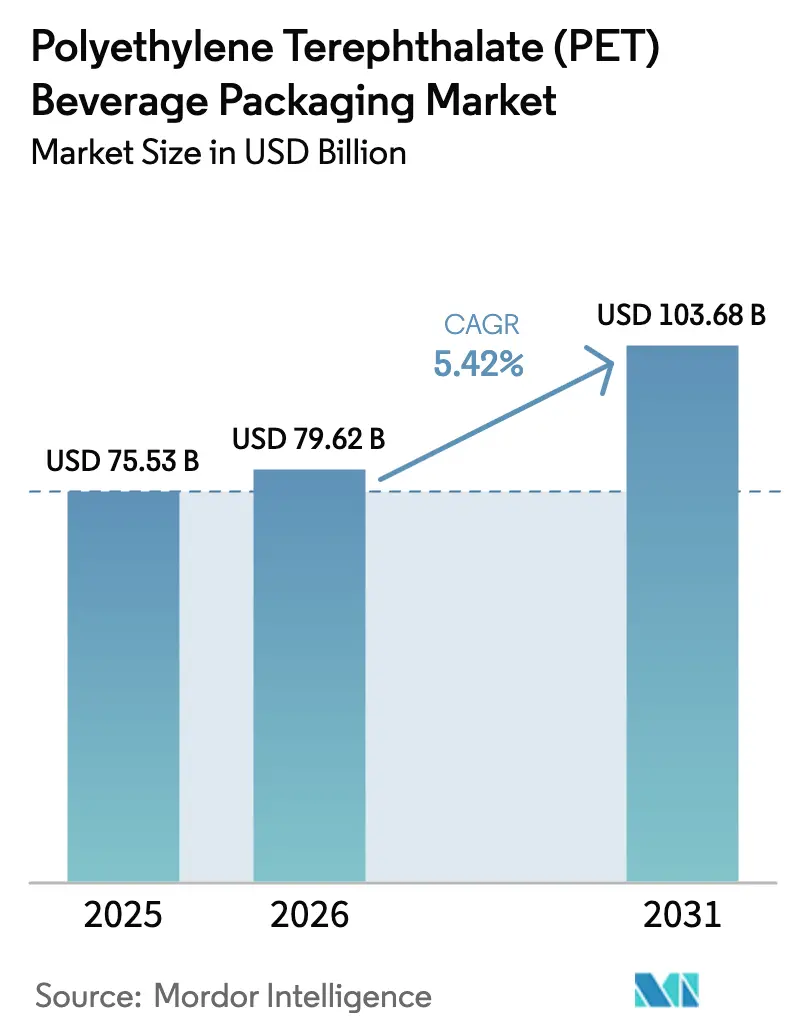

| Market Size (2026) | USD 79.62 Billion |

| Market Size (2031) | USD 103.68 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyethylene Terephthalate (PET) Beverage Packaging Market Analysis by Mordor Intelligence

The polyethylene terephthalate (PET) beverage packaging market size is expected to grow from USD 75.53 billion in 2025 to USD 79.62 billion in 2026 and is forecast to reach USD 103.68 billion by 2031 at 5.42% CAGR over 2026-2031. Robust demand comes from PET’s barrier performance, compatibility with high-speed filling lines, and recyclability advantages that help brand owners satisfy tightening environmental mandates. Lightweighting programs that cut gram weight while preserving carbonation retention keep material cost in check and reduce logistics emissions. Regulatory requirements for recycled content, especially in the European Union and India, stimulate rapid capacity additions in food-grade rPET. Consolidation among leading converters increases purchasing leverage for resin and funds investments in chemical recycling. Supply chain risk remains tied to feedstock volatility and geopolitical disruptions, but integrated players offset much of this pressure through long-term contracts and hedging strategies. Altogether, these forces sustain steady growth while positioning sustainability capabilities as the main source of competitive edge in the polyethylene terephthalate (PET) beverage packaging market.

Key Report Takeaways

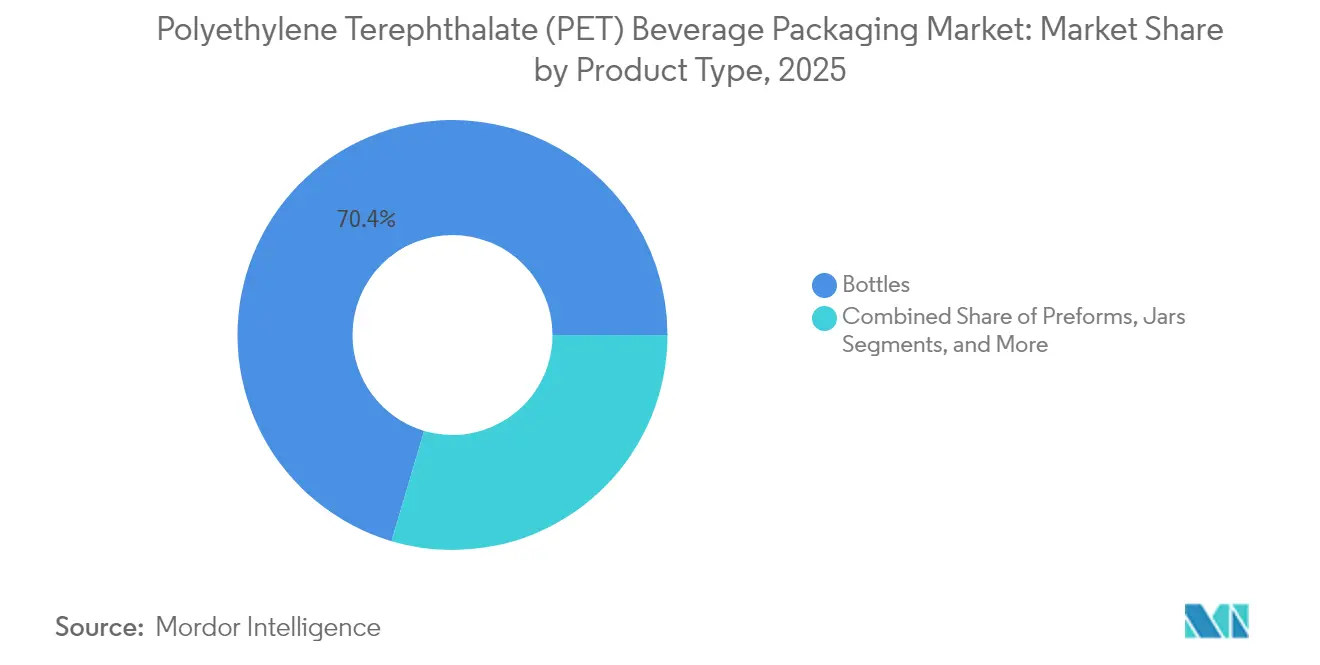

- By product type, bottles led with 70.42% revenue share in 2025; lids/caps and closures record the fastest 7.76% CAGR through 2031.

- By capacity, the 501-1,000 ml range held 38.44% of the polyethylene terephthalate (PET) beverage packaging market share in 2025, while containers ≤ 250 ml expand at a 6.93% CAGR to 2031.

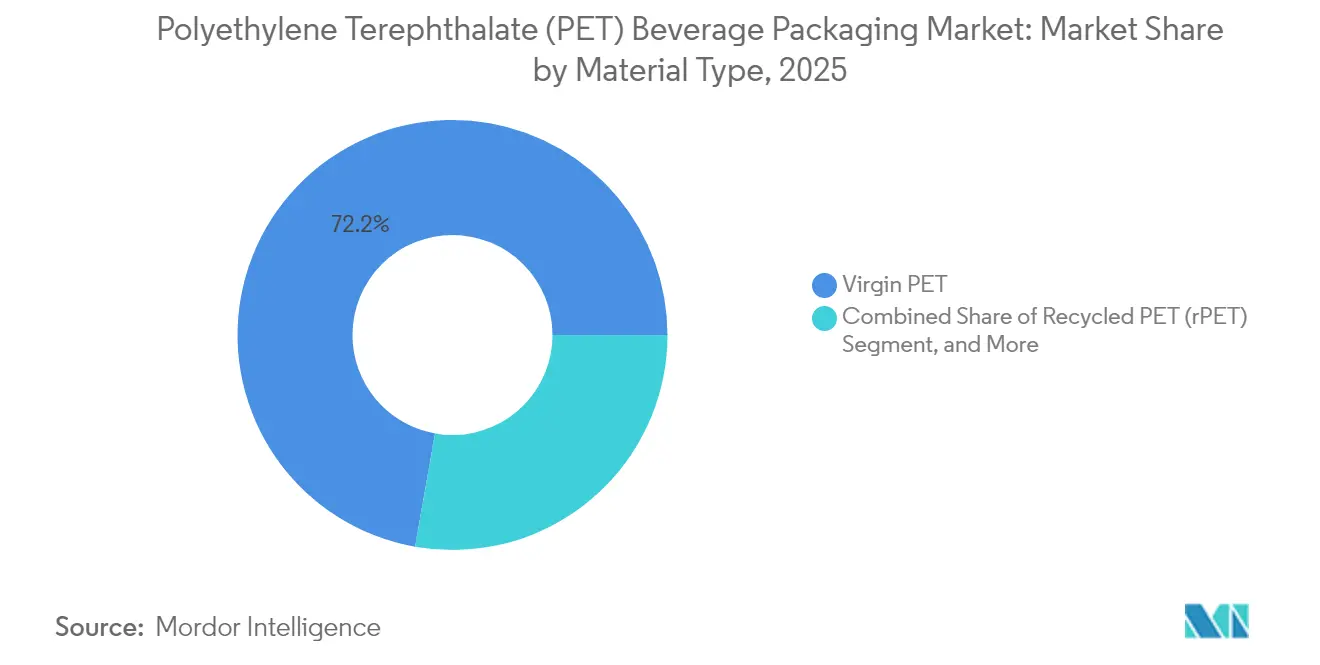

- By material, virgin PET captured 72.21% share in 2025; recycled PET grows at an 8.61% CAGR, the quickest among all materials.

- By end-user industry, water bottles accounted for 34.58% of the polyethylene terephthalate (PET) beverage packaging market size in 2025; energy and sports drinks rise at an 8.21% CAGR through 2031.

- By geography, Asia-Pacific commanded 42.63% share in 2025 and also posts the strongest 6.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyethylene Terephthalate (PET) Beverage Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Superior lightweight-to-strength ratio and clarity | +1.2% | Global, with strongest adoption in North America & Europe | Medium term (2-4 years) |

| Surging demand for recycled and rPET-content bottles | +1.8% | Global, led by EU mandates, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of bottled water and functional beverage categories | +1.1% | Asia-Pacific core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Bio-based PET capacity additions unlocking EPR credits | +0.7% | North America & EU, pilot programs in Japan | Long term (≥ 4 years) |

| EU tethered-cap directive accelerating bottle redesign | +0.5% | Europe primary, potential adoption in California by 2027 | Medium term (2-4 years) |

| On-premise refill programs pivoting to refillable PET | +0.3% | Europe and North America urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Superior lightweight-to-strength ratio and clarity

Coca-Cola’s lightweighting cut the 12–20 oz bottle from 21 g to 18.5 g, saving 3 million t of PET yearly and lowering haulage emissions while safeguarding carbonation standards.[1]Matt Reynolds, “Coke’s ‘First in Decades’ PET Lightweighting Project,” packworld.com Blow-molding refinements orient polymer chains for higher rigidity, letting converters lower resin use without risk of side-wall paneling. Ring Container’s Trimlite cut wide-mouth jar weight by 40% while keeping oxygen barrier, underlining PET’s cost-to-performance edge versus aluminum, which saw price swings during can shortages. Such advances help brands defend margins in markets where packaging can be 20% of delivered product cost. As emerging economies scale soft-drink output, lightweight PET unlocks volume growth without proportional resin demand, further stabilising the polyethylene terephthalate (PET) beverage packaging market.

Surging demand for recycled and rPET-content bottles

The EU’s 25% recycled content rule for 2025 and India’s 30% mandate from April 2025 are forcing brands to lock in supply contracts with recyclers or risk paying price premiums of up to 30%. Europe lifted collection rates to 75% in 2022, allowing average bottle rPET content of 24%.[2]Packaging Europe, “Where is Europe’s PET industry at in 2025?” packagingeurope.com DePoly’s USD 23 million Swiss plant and GR3N’s microwave depolymerisation add virgin-grade feedstock from contaminated waste, narrowing the deficit. Integrated converters that own recycling assets secure feedstock and strengthen negotiation power, fuelling growth in the polyethylene terephthalate (PET) beverage packaging market.

Expansion of bottled water and functional beverage categories

Sports and energy drinks posted 9% retail growth in 2023 as hydration shifted from sports-only to daily wellness, a trend amplified in Asia-Pacific where urban heat drives water purchases.[3]Jessica Jacobsen, “2024 State of the Beverage Industry: Sports Drinks Embrace Everyday Wellness,” bevindustry.com PET’s shatter resistance supports on-the-go consumption and e-commerce delivery, areas where glass breakage risk outweighs its premium perception. Keurig Dr Pepper’s USD 990 million move on GHOST Energy secures distribution heft in a high-margin niche. Portion-controlled high-protein drinks also choose PET for light weight and ease of labeling, pushing demand for specialty preforms and closures.

Bio-based PET capacity additions unlocking EPR credits

Indorama and Suntory commercialised bio-paraxylene bottles in Japan, producing 45 million units in 2024 and earning Extended Producer Responsibility offsets that cut compliance costs. Origin Materials’ biomass-derived PET shows carbon-negative life-cycle scores, turning packaging from emission source to carbon sink. Early adopters secure shelf space with sustainability claims and defend price premiums that shelter R&D payback. Limited supply grants scarcity value, nudging brands to long-term offtake deals and supporting strategic investment flows into the polyethylene terephthalate (PET) beverage packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic taxes and bans tightening globally | -1.4% | Global, with strictest enforcement in EU and select US states | Short term (≤ 2 years) |

| Volatility in PTA/MEG feedstock prices | -0.9% | Global, with highest impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Aluminum-can substitution in carbonated drinks | -0.6% | North America and Europe premium segments | Medium term (2-4 years) |

| Deposit-return schemes favouring glass in DACH and Nordics | -0.3% | Northern Europe, potential expansion to other EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-use plastic taxes and bans tightening globally

Oregon’s Bottle Bill now covers wine, adding a 10-cent deposit that raises handling cost and blunts PET’s lightweight economics. California is considering tethered-cap rules by 2027, nudging global brand lines toward standardised EU-compliant formats. Fragmented regulations force brands to manage multiple packaging variants, driving up inventory and tooling fees. Smaller beverage firms face disproportionate cost pressure, nudging market share toward large multinationals that can navigate compliance complexity.

Volatility in PTA/MEG feedstock prices

April 2025 PET prices rose 1–2 cents per pound even as feedstock costs softened 9% from 2024, illustrating how trade policy, tariffs and anti-dumping actions decouple resin from oil dynamics. Production cuts in China and Europe create artificial scarcity that keeps price floors high. European PET sits at EUR 1,130–1,170 t (USD 1,224–1,268 t). Currency gyrations and shipping disruptions linked to the Russia-Ukraine conflict complicate procurement planning, favouring converters with hedging sophistication and multi-regional plant networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bottles Dominate Despite Closure Innovation

Bottles accounted for 70.42% of 2025 revenue and remain the backbone of the polyethylene terephthalate (PET) beverage packaging market. The segment benefits from high tooling utilisation, global standardisation, and compatibility with carbonated and still beverages. Origin Materials’ all-PET tethered cap unlocks mono-material recycling, signalling eventual closure migration away from PP and HDPE. The polyethylene terephthalate (PET) beverage packaging market size for bottles is projected to rise alongside functional drinks that demand advanced oxygen barriers.

Closures record the fastest 7.76% CAGR, bolstered by EU legislation and the USD 65 billion opportunity in attached caps. Over 20 converters already qualified PET closure designs for Fortune 500 clients. Mono-material closures promise line-side simplification and remove mixed-polymer contamination, strengthening recycling economics and opening a new frontier of differentiation inside a previously commodity-like segment. Preforms retain importance as traded intermediates, especially in regions where bottle blowing happens close to filling lines, while jars stay niche for premium teas and kombucha.

By Capacity Type: Small Formats Drive Premiumisation

The 501–1,000 ml range held 38.44% polyethylene terephthalate (PET) beverage packaging market share in 2025 thanks to its versatility across water, soft drinks and ready-to-drink coffees. Yet containers not exceeding 250 ml show the highest 6.93% CAGR, mirroring portion-control and on-the-go consumption. The polyethylene terephthalate (PET) beverage packaging market size for these small formats is forecast to rise as brands deploy premium price points per ounce.

Small bottles help energy drinks and nutraceutical beverages capture impulse purchases at convenience stores. PET’s light weight improves pallet efficiency relative to glass miniatures, while clear walls showcase natural colourants in functional beverages. Larger formats above 1 L cater to family consumption but face refrigerator-door dimension constraints. Growth in e-grocery triggers interest in square cross-sections and handle-less jugs that maximise cube utilisation.

By Material Type: Recycled Content Mandates Reshape Supply

Virgin PET still controlled 72.21% of 2025 volume, supported by vast polymerisation capacity and predictable quality. Yet recycled PET clocks an 8.61% CAGR as brands race to hit 25% content targets in Europe by 2025 and 30% by 2030. The polyethylene terephthalate (PET) beverage packaging market size for rPET is expanding faster than collection growth, resulting in price premiums that can reach USD 350 t over virgin equivalents.

Food-grade rPET scarcity encourages chemical recycling investments that produce interchangeable polymer at lower impurity thresholds. Early movers secure offtake contracts and lock in margins, while converters without captive recycling build consortia to guarantee supply. Bio-based PET remains niche but commands price premiums due to carbon-negative credentials and EPR credits; its long-term adoption depends on scaling of bio-PX feedstock from waste cooking oil and lignocellulosic biomass.

By End-user Industry: Functional Categories Outpace Traditional

Water retained 34.58% volume share in 2025, reflecting basic hydration needs in markets with poor municipal supply. Functional, energy and sports drinks, though smaller in absolute litres, post the fastest 8.21% CAGR as consumers seek protein, electrolytes and caffeine on the move. Packaging must withstand low-pH formulations and preserve carbonation in high-pressure energy drinks, making PET the pragmatic choice for performance-oriented brands.

Higher-margin functional drinks support investment in smart closures and embossed designs that reinforce brand storytelling. Carbonated soft drinks face sugar-tax headwinds yet still generate significant PET demand in emerging economies. Alcoholic beverage use of PET is limited but rising for outdoor festivals and aviation, where weight, safety and quick recycling matter more than glass’s premium cues.

Geography Analysis

Asia-Pacific held 42.63% of global revenues in 2025 and expands at 6.29% CAGR. Rising middle-class incomes, rapid urbanisation and retail network penetration lift demand for packaged hydration. China’s anti-dumping duties protect domestic resin producers, while India’s 30% rPET rule from April 2025 accelerates backward integration among global bottlers. Japan and South Korea spearhead labelless bottles that minimise downstream delabelling costs, highlighting regional innovation strength.

North America remains the second-largest region with entrenched consumption habits and premium functional drink launches. California’s evolving recycled-content proposals and Oregon’s expanded bottle bill raise compliance complexity. Canada and Mexico supply resin at scale, balancing trade flows when US feedstock prices spike.

Europe is the most regulated landscape, featuring tethered caps and escalating recycled-content thresholds. Collection infrastructure allows 75% retrieval rates, yet rPET demand already overshoots supply, spurring plant investment in Spain, Poland and Germany. Nordic glass-favoured deposit systems present substitution risk, but lightweight refillable PET alternatives begin to appear in retail pilots.

Latin America, the Middle East and Africa contribute smaller shares but post solid growth as climate conditions and demographic profiles drive beverage uptake. Currency fluctuations and patchy recycling infrastructure shape entry strategies, prompting converters to partner with local collectors and NGOs to secure feedstock while building brand goodwill.

Competitive Landscape

Industry concentration is moderate and moving upward. Amcor’s USD 8.43 billion all-stock merger with Berry Global created a USD 24 billion packaging leader targeting USD 650 million synergy capture. The enlarged scale secures resin procurement discounts and funds technology such as molecular recycling. Silgan’s EUR 838 million (USD 907 million) takeover of Weener Packaging strengthens its closures portfolio, a high-margin segment poised for tethered-cap driven expansion.

Technological moats grow in importance. Origin Materials commercialised fully recyclable PET caps in early 2025, giving bottlers a mono-material solution that simplifies sorting and avoids HDPE contamination. Indorama’s bio-based PET launch ties renewable feedstock to strong brand sustainability narratives. Regional players such as ALPLA, Plastipak and Resilux defend share through proximity to customers, multi-continent plant footprints and agile custom-moulding services.

Strategic moves focus on recycling integration, lightweighting IP and geographic expansion. Companies announce joint ventures with chemical recyclers, sign multi-year offtake with rPET suppliers and retrofit lines for tethered cap production. Smaller converters specialise in short-run, design-heavy bottles serving craft brands, maintaining relevance in a consolidating polyethylene terephthalate (PET) beverage packaging market.

Polyethylene Terephthalate (PET) Beverage Packaging Industry Leaders

Resilux NV

Nampak Ltd

Amcor plc

Berry Global Group Inc.

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Alpek closed its Cedar Creek facility, removing 170,000 t of PET capacity and tightening North American supply.

- May 2025: Perstorp released Akestra polyester technology allowing 90% recycled content in heat-resistant PET trays designed for ready meals.

- April 2025: Amcor completed its combination with Berry Global, forming a USD 24 billion packaging group that targets USD 650 million synergies and bolsters sustainable material R&D.

- March 2025: Eastman Chemical secured up to USD 375 million from the US Department of Energy for a molecular recycling facility able to process 110,000 t of waste annually, underscoring federal support for circular PET feedstock.

Global Polyethylene Terephthalate (PET) Beverage Packaging Market Report Scope

The compound used for the manufacturing process of a wide variety of plastic bottles is polyethylene terephthalate or PET. In particular, it is important to point out that plastic containers of beverages are not the same as BPAbishenolA.

The study tracks the demand based on the consumption of PET beverage products globally across various end users listed in the study. The study factors in the impact of the Russia-Ukraine War on the overall supply chain of the market. The study factors the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The PET beverage packaging market is segmented by product (bottles, jars, lids/caps & closures), end-user industry (carbonated drinks, juices, water bottles, alcoholic beverages, energy drinks), and geography (North America (United States, Canada), Europe (France, Germany, Italy, Spain, United Kingdom, Rest of Europe), Asia-Pacific (China, India, Japan, Rest of Asia-Pacific), Latin America, Middle East & Africa). The report offers market forecasts and size in volume (tonnes) and value (USD) for all the above segments.

| Bottles |

| Preforms |

| Jars |

| Lids/Caps and Closures |

| Other Products |

| ≤ 250 ml |

| 251 – 500 ml |

| 501 – 1,000 ml |

| 1,001 – 2,000 ml |

| > 2,000 ml |

| Virgin PET |

| Recycled PET (rPET) |

| Bio-based PET |

| Other Material Types |

| Water Bottles |

| Carbonated Drinks |

| Juices and Nectars |

| Energy and Sports Drinks |

| Alcoholic Beverages |

| Functional and RTD Beverages |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | France |

| Germany | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| UAE | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Bottles | |

| Preforms | ||

| Jars | ||

| Lids/Caps and Closures | ||

| Other Products | ||

| By Capacity (Fill Volume) Type | ≤ 250 ml | |

| 251 – 500 ml | ||

| 501 – 1,000 ml | ||

| 1,001 – 2,000 ml | ||

| > 2,000 ml | ||

| By Material Type | Virgin PET | |

| Recycled PET (rPET) | ||

| Bio-based PET | ||

| Other Material Types | ||

| By End-user Industry | Water Bottles | |

| Carbonated Drinks | ||

| Juices and Nectars | ||

| Energy and Sports Drinks | ||

| Alcoholic Beverages | ||

| Functional and RTD Beverages | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the polyethylene terephthalate (PET) beverage packaging market?

The market is valued at USD 79.62 billion in 2026 and is projected to reach USD 103.68 billion by 2031, growing at a 5.42% CAGR.

Which product segment grows fastest through 2031?

Lids, caps and closures register the quickest 7.76% CAGR, driven by EU tethered-cap rules.

Why is rPET supply so tight?

Recycled content mandates in the EU and India outpace current food-grade rPET output, creating a supply gap that pushes price premiums and sparks investment in chemical recycling.

How does lightweighting benefit beverage brands?

Cutting bottle gram weight lowers resin costs, shrinks logistics emissions and improves profit margins without compromising performance.

Which region offers the highest growth potential?

Asia-Pacific combines the largest 42.63% revenue share with the strongest 6.29% CAGR, thanks to rising incomes and supportive recycling policies.

How are large converters responding to sustainability pressure?

They pursue acquisitions to gain scale, invest in chemical recycling facilities and launch mono-material closures to meet circular economy targets.

Page last updated on: