Dyspepsia Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.04 Billion |

| Market Size (2031) | USD 13.55 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

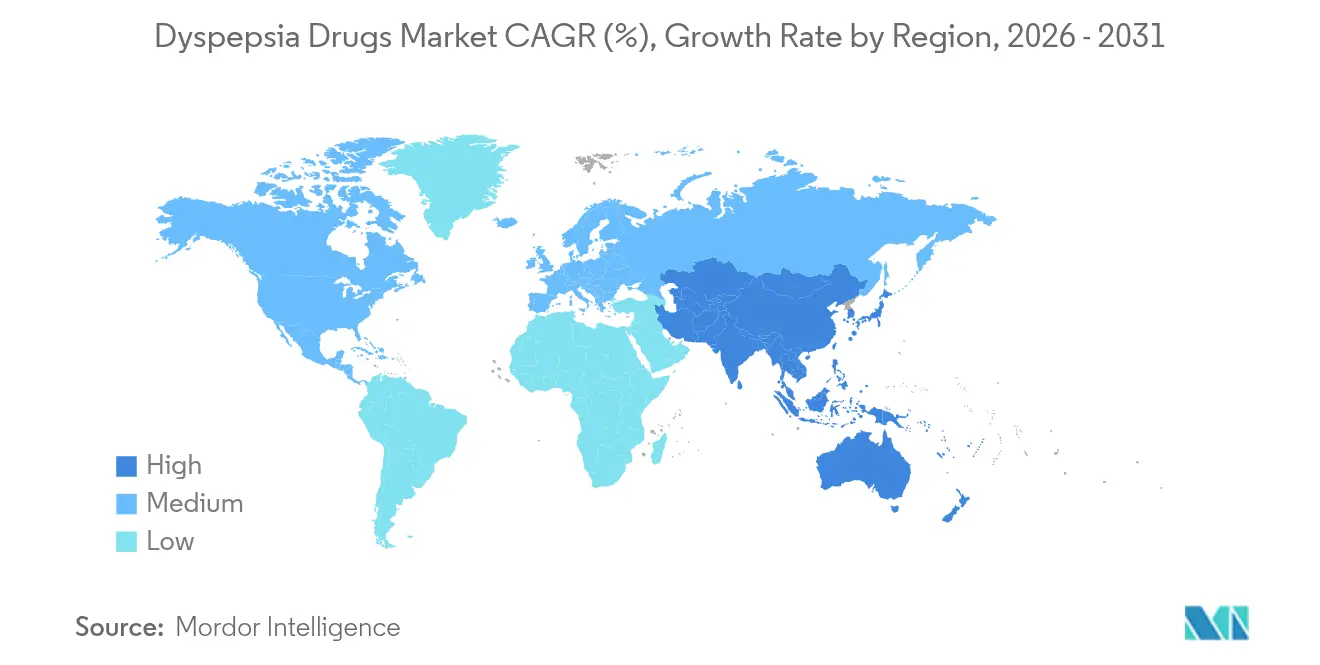

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

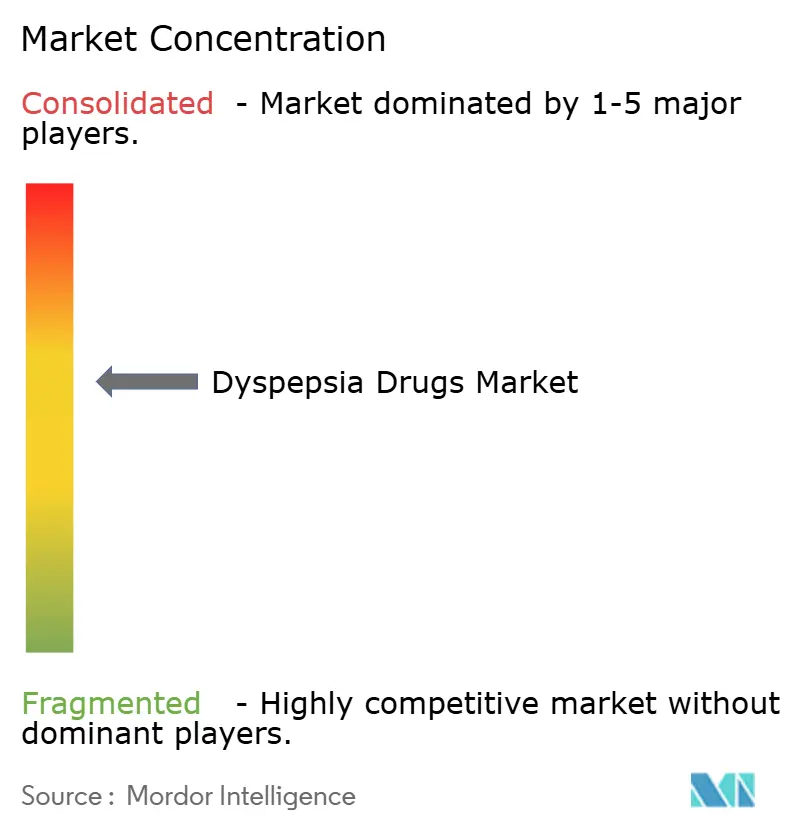

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dyspepsia Drugs Market Analysis by Mordor Intelligence

The dyspepsia drugs market size in 2026 is estimated at USD 11.04 billion, growing from 2025 value of USD 10.60 billion with 2031 projections showing USD 13.55 billion, growing at 4.18% CAGR over 2026-2031. The upward curve in the dyspepsia drugs market reflects an intricate mix of demographic ageing, technology-led drug innovation, and widening access channels that continue to shape therapy choices worldwide. Proton-pump inhibitors (PPIs) still underpin acid-suppression protocols, yet safety alarms are encouraging a rapid pivot toward potassium-competitive acid blockers (PCABs) and microbiome-modulating adjuvants that promise more targeted control of gastric acidity. Asia-Pacific tracks the fastest regional CAGR at 9.27% through 2030 as urban diets drive functional dyspepsia incidence, while North America retains the largest regional foothold due to early adoption of novel acid therapies and strong reimbursement scaffolds. Online and quick-commerce pharmacy models expand medicine access at 11.87% CAGR, signalling a structural redistribution of channel power previously held by brick-and-mortar outlets. Against this backdrop, API supply chain disruptions originating in China and tighter Western price-control mandates squeeze margins, meaning product differentiation and regulatory agility are now critical to preserve leadership in the dyspepsia drugs market.

Key Report Takeaways

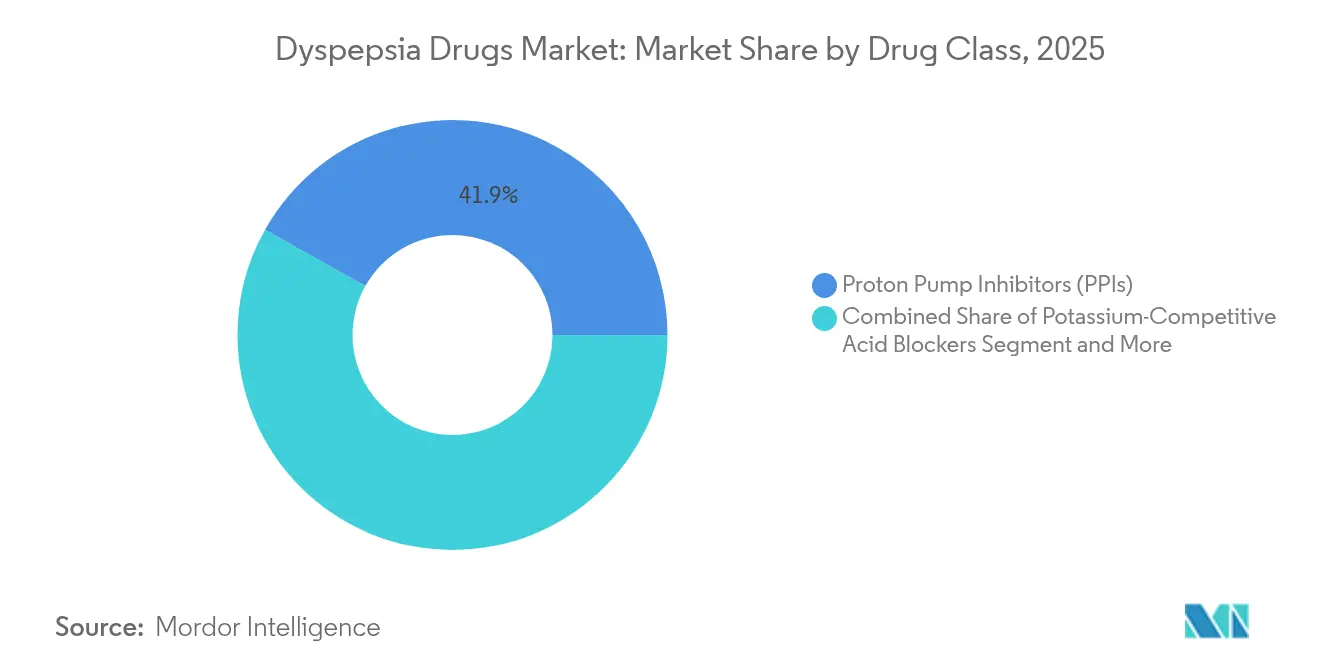

- By drug class, proton pump inhibitors led with 41.86% of the dyspepsia drugs market share in 2025, while PCABs are projected to compound at 11.90% CAGR to 2031.

- By route of administration, oral solid formulations accounted for 88.21% share of the dyspepsia drugs market size in 2025; oro-dispersible and sublingual formats are expected to climb at 10.67% CAGR through 2031.

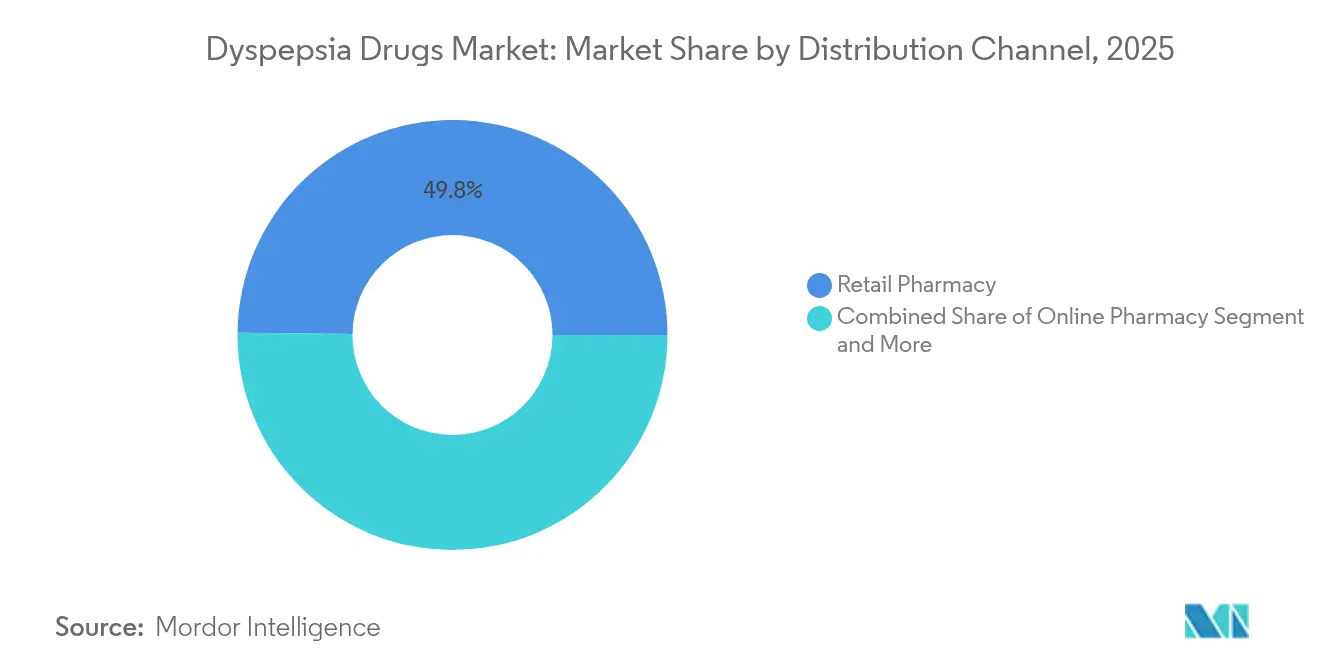

- By distribution channel, retail pharmacies held 49.83% revenue share in 2025, whereas online pharmacy platforms are forecast to grow at 11.68% CAGR between 2026 and 2031.

- By geography, North America commanded 37.92% of the dyspepsia drugs market in 2025; Asia-Pacific shows the fastest regional CAGR at 9.15% in the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dyspepsia Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTC Self-Medication Boom & E-Pharmacy Penetration | +1.2% | Global; strongest in North America & Asia-Pacific | Short term (≤ 2 years) |

| Growing Prevalence of Functional Dyspepsia in Aging Populations | +0.8% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Rapid Uptake of Potassium-Competitive Acid Blockers (PCABs) | +1.5% | North America & EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Drug-Repurposing Accelerating Pipeline Assets | +0.4% | North America & EU; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Post-Biotics & Microbiome Modulating Adjuvants Improving Drug Efficacy | +0.6% | Global; early adoption in North America & EU | Medium term (2-4 years) |

| Employer-Sponsored Digital Gut-Health Programs Amplifying Demand | +0.3% | North America primary; expanding to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OTC Self-Medication Boom & E-Pharmacy Penetration

Consumer tilt toward self-care and round-the-clock digital access is remapping prescription and OTC dispensing. Friction-free platforms combine price transparency, doorstep delivery within hours, and AI-driven symptom checkers that ease product selection, therefore broadening the dyspepsia drugs market[1]Eva Temkin, “FDA Finalizes Rule on ACNU Drugs,” Arnold & Porter, arnoldporter.com. The FDA’s ACNU rule widens the prescription-to-OTC pathway, allowing interactive apps to confirm safe use and further fuelling product switch momentum. Retail pharmacies respond by integrating teleconsultations and loyalty algorithms, yet foot-traffic leakage persists, signalling a likely convergence where omnichannel competence becomes a survival criterion in the dyspepsia drugs market.

Growing Prevalence of Functional Dyspepsia in Aging Populations

Functional dyspepsia now affects up to 25% of older adults, a proportion rising in tandem with global longevity gains. Age-linked gastric motility slowdown, polypharmacy, and comorbidity clustering increase demand for long-term symptom control, cementing a baseline expansion floor for the dyspepsia drugs market. Asia-Pacific feels this double burden most sharply, blending fast-ageing demographics with Westernised diets high in fat and processed sugar. Healthcare systems must therefore scale cost-effective regimens that lighten outpatient loads while sustaining quality-of-life metrics.

Rapid Uptake of Potassium-Competitive Acid Blockers (PCABs)

Vonoprazan’s 2024 FDA nod signalled the first new acid-suppression mode in three decades, propelling PCAB prescription counts beyond 390,000 in Q1 2025 in the United States alone. PCABs produce near-instant pH elevation without meal timing constraints, a compliance edge translating into visibly higher healing rates than legacy PPIs. Moreover, their metabolism bypasses CYP2C19 variability, reducing inter-patient response gaps that long plagued PPIs. Pipeline assets such as linaprazan glurate and fexuprazan portend a multi-asset class race likely to expand the dyspepsia drugs market well past 2030.

AI-Enabled Drug-Repurposing Accelerating Pipeline Assets

Machine-learning algorithms now compress indication-finding cycles from years to mere months, exemplified by ISM5411’s AI-directed pivot into gastrointestinal inflammation within a single development year. Repurposing curtails early-phase safety risk and trims R&D costs by up to 70%, freeing capital for market-access programmes. In dyspepsia, AI has flagged gabapentin analogues and serotonin modulators as potential visceral pain regulators, pushing big-data capability to the front line of future pipeline curation across the dyspepsia drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-Term Cardiovascular Safety Concerns of Chronic PPI Use | -0.9% | Global; strongest in North America & EU | Medium term (2-4 years) |

| Rising Price-Control Policies on OTC Antacids | -0.6% | North America & EU; expanding globally | Short term (≤ 2 years) |

| Consumer Shift Toward Clean-Label Acid Relief Nutraceuticals | -0.4% | North America & EU; emerging in Asia-Pacific | Medium term (2-4 years) |

| API Supply Bottlenecks for Vonoprazan & Other PCABs | -0.7% | Global; concentrated impact on PCAB availability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long-Term Cardiovascular Safety Concerns of Chronic PPI Use

Meta-analyses report hazard ratios of 1.36 for myocardial infarction and 1.14 for ischaemic stroke among chronic PPI users, especially diabetics. Such signals prompt guideline revisions favouring step-down or intermittent therapy and accelerate PCAB substitution, yet also shave volume from established blockbuster PPIs. Insurers scrutinise long-term scripts, linking reimbursement to documented indication renewals, thereby tempering growth in portions of the dyspepsia drugs market previously locked to repeat refills.

Rising Price-Control Policies on OTC Antacids Across Key Markets

Medicare’s inaugural negotiated discounts of up to 79% across selected drugs presage similar moves for high-volume antacids, pressuring manufacturers to rationalise SKU counts and streamline supply chains[2]Harshini Sadanala, “Which Price is Right: The Constitutionality of Lowering Drug Prices,” Columbia Undergraduate Law Review, culawreview.org. Cost squeezes crimp funds for marketing and line extensions, meaning brand equity alone can no longer guarantee shelf presence in the dyspepsia drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: PCABs Challenge PPI Dominance

PPIs controlled 41.86% of the dyspepsia drugs market share in 2025, underlining decades of clinical familiarity and broad insurance coverage. Yet incremental evidence linking chronic use with cardiovascular and renal events erodes prescriber confidence, shrinking refill frequency. Meanwhile, the dyspepsia drugs market size linked to PCAB uptake is forecast to compound at 11.90% CAGR, accelerated by vonoprazan’s once-daily schedule and stronger night-time pH control. Antacids remain the quick-relief choice for episodic symptoms, though commodity pricing reduces revenue potential. H2 antagonists serve a bridging role for patients tapering off PPIs, offering moderate symptom suppression with fewer long-term concerns.

Reinvestment tilts toward pipeline PCABs such as linaprazan glurate, now in late-stage trials, and fixed-dose combinations that pair proton pumps with prokinetics to address motility-driven dyspepsia. Antibiotic-based H. pylori eradication retains niche importance but faces rising clarithromycin resistance, prompting research into novel macrolide-sparing regimens. Competitive heft will hinge on blended portfolios able to address both acid and functional pain components across the dyspepsia drugs market.

By Route of Administration: Oral Innovation Drives Growth

Oral solid dosage forms delivered 88.21% of sales in 2025 as tablets and capsules dominate pharmacy shelves for convenience and cost-efficiency. The dyspepsia drugs market size for oro-dispersible formats is growing briskly, with 10.67% CAGR projected to 2031 thanks to melt-in-mouth strips that dissolve without water—an asset for elderly patients or those managing on-the-go lifestyles. Liquid suspensions secure a smaller but stable share among paediatric and dysphagic cohorts, while parenteral infusions reserve their use for hospitalised cases of severe upper-GI bleeding.

Formulation science prioritises rapid release matrices that reach therapeutic plasma levels within minutes, aiming to forestall rebound acidity that undermines compliance. Co-processed excipients extend shelf life under high humidity, vital for emerging tropical markets central to future expansion of the dyspepsia drugs market. Companies also explore micro-encapsulated probiotics co-packed with acid blockers, a strategy intended to differentiate products in crowded OTC aisles.

By Distribution Channel: Digital Disruption Accelerates

Retail pharmacies held 49.83% revenue in 2025 owing to trusted in-person advice and immediate product hand-over, yet online outlets accelerate at 11.68% CAGR, capturing chronic users who value doorstep refills. Teleconsultation tie-ins allow e-pharmacies to issue digital prescriptions inside the same customer journey, effectively collapsing the care pathway and reinforcing stickiness within the dyspepsia drugs market. Hospital pharmacies retain their role for acute presentation management, whereas mass merchandisers thrive on impulse antacid purchases linked to food courts and travel corridors.

E-pharmacies integrate AI engines that parse purchase history and overlay it with symptom logs, generating nudges for dosage optimisation—tools that physical outlets replicate more slowly. Such data-rich models produce up-sell pathways into personalised supplements, widening revenue streams and prompting traditional chains to invest in omnichannel dashboards to defend share in the dyspepsia drugs market.

Geography Analysis

North America controlled 37.92% of the dyspepsia drugs market in 2025, supported by robust reimbursement structures, early PCAB adoption, and high telehealth penetration. Net revenues for vonoprazan reached USD 28.5 million in Q1 2025, confirming clinician willingness to migrate from PPIs where sustained symptom clearance offers tangible quality-of-life gains. However, tightening price negotiations and pharmacovigilance scrutiny around chronic PPI cardiac risks are likely to moderate absolute value growth, nudging manufacturers toward real-world evidence programmes that showcase outcome superiority.

Asia-Pacific records the highest growth at 9.15% CAGR, combining swift urbanisation, ageing societies, and rising discretionary income. E-commerce-ready populations facilitate rapid uptake of OTC formats, a dynamic helped by smartphone-based symptom checkers packaged in local languages. Regulatory complexities persist, notably China’s heightened facility inspections that can stall API clearance for global export, but agile supply networks and regional manufacturing investments mitigate exposure, preserving headroom for the dyspepsia drugs market across the region.

Europe contributes steady incremental value, anchored by comprehensive universal care and stringent health-technology assessments that reward evidence-rich dossiers. PCAB launches are expected to secure premium reimbursement when head-to-head data substantiate both efficacy and safety advantages versus generics. Eastern European states add volume upside as their insurance pools expand, though currency fluctuations can complicate multinational pricing corridors. Middle East & Africa and South America remain nascent, yet infrastructure upgrades and branded-generic demand hint at double-digit percentage growth pockets that astute entrants can monetise in the wider dyspepsia drugs market.

Competitive Landscape

The dyspepsia drugs market presents moderate fragmentation: the top five firms command significant revenue, a level that leaves manoeuvring room for focused innovators yet still demands significant capital to scale. Takeda leverages long-tenured Dexilant and new-generation PCAB assets to anchor gastroenterology revenues, while AstraZeneca maintains Nexium’s residual strength via OTC line extensions. Sanofi fortifies its position through consumer-health bolt-ons, adding clean-label alginate syrups that meet evolving ingredient sentiment. Phathom Pharmaceuticals emerged as a challenger by focusing exclusively on vonoprazan’s US commercialisation and by running direct-to-consumer campaigns featuring high-visibility brand ambassadors.

Strategic pivots emphasise precision phenotyping and digital wraps that turn acute drug use into holistic gut-health journeys. Large players buy AI-first startups to embed computational chemistry inside discovery, evidenced by Ironwood’s 2025 buy-in to repurpose apraglutide for gastrointestinal restoration. Licensing deals focus on differentiated delivery—such as Dr. Falk Pharma’s naronapride IND green-light—aiming to address motility facets of dyspepsia that PPIs overlook.

M&A chatter concentrates on regional OTC portfolios where synergies can lift operating margins against looming price caps. Meanwhile, intellectual-property fences tighten around formulation know-how, particularly taste-masked melt-away tablets and shelf-stable post-biotics, defensive moves designed to extend lifecycle in a dyspepsia drugs market where chemical actives face generic drain.

Dyspepsia Drugs Industry Leaders

Eisai Co., Ltd.

Novartis AG

Sanofi SA

AstraZeneca PLC

Lupin Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Phathom Pharmaceuticals partnered with actor Kenan Thompson to raise awareness about gastroesophageal reflux disease and VOQUEZNA treatment options.

- January 2025: The FDA finalised the Additional Conditions for Nonprescription Use (ACNU) rule, opening a new pathway for OTC drugs that incorporate digital tools for safe use.

Global Dyspepsia Drugs Market Report Scope

As per the scope of the report, dyspepsia refers to indigestion or upset stomach that causes discomfort in the upper abdomen and leads to abdominal pain. Gastritis, peptic ulcers, gallstones, stomach cancer, constipation, and intestinal ischemia are gastrointestinal causes of dyspepsia. Diabetes, thyroid disorders, kidney problems, and the use of nonsteroidal anti-inflammatory drugs (NSAIDs such as ibuprofen) are examples of non-gastrointestinal causes. The dyspepsia drug market is segmented by drug class into antacids, proton pump inhibitors, H2 antagonists, antibiotics, and other drug classes. By route of administration, the market is segmented into oral and injectable. By distribution channel, the market is segmented into online pharmacy, retail pharmacy, and other distribution. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also offers the market size and forecasts for 17 countries across the region. The report offers the value (USD) for the above segments.

| Antacids |

| Proton Pump Inhibitors (PPIs) |

| H2 Receptor Antagonists |

| Potassium-Competitive Acid Blockers (PCABs) |

| Prokinetics & Neuromodulators |

| Antibiotics |

| Oral Solid |

| Oral Liquid |

| Oro-dispersible / Sublingual |

| Parenteral |

| Retail Pharmacy |

| Online Pharmacy / e-Pharmacy |

| Hospital & Clinic Pharmacy |

| Other Channels (Mass-merchandisers, Convenience Stores) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antacids | |

| Proton Pump Inhibitors (PPIs) | ||

| H2 Receptor Antagonists | ||

| Potassium-Competitive Acid Blockers (PCABs) | ||

| Prokinetics & Neuromodulators | ||

| Antibiotics | ||

| By Route of Administration | Oral Solid | |

| Oral Liquid | ||

| Oro-dispersible / Sublingual | ||

| Parenteral | ||

| By Distribution Channel | Retail Pharmacy | |

| Online Pharmacy / e-Pharmacy | ||

| Hospital & Clinic Pharmacy | ||

| Other Channels (Mass-merchandisers, Convenience Stores) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current market size of dyspepsia drugs and how fast is it growing?

The dyspepsia drugs market size is USD 11.04 billion in 2026 and is forecast to expand at a 4.18% CAGR to reach USD 13.55 billion by 2031.

Why are potassium-competitive acid blockers gaining traction?

PCABs such as vonoprazan offer faster, meal-independent acid suppression with fewer genetic metabolism issues than PPIs, driving 11.90% segment CAGR and physician adoption.

Which region shows the highest growth potential?

Asia-Pacific posts the fastest regional CAGR at 9.15% due to rapid urbanisation, dietary shifts, and larger ageing populations that heighten dyspepsia prevalence.

How are online pharmacies influencing the market?

Digital channels grow at 11.68% CAGR by providing 24/7 access, quick deliveries, and AI-guided product selection, steadily shifting share from traditional retail outlets.

What safety concerns affect long-term PPI use?

Studies link chronic PPI therapy to elevated cardiovascular and renal risks, prompting guideline revisions and encouraging uptake of alternative therapies such as PCABs.

Page last updated on: