Drilling Tools Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

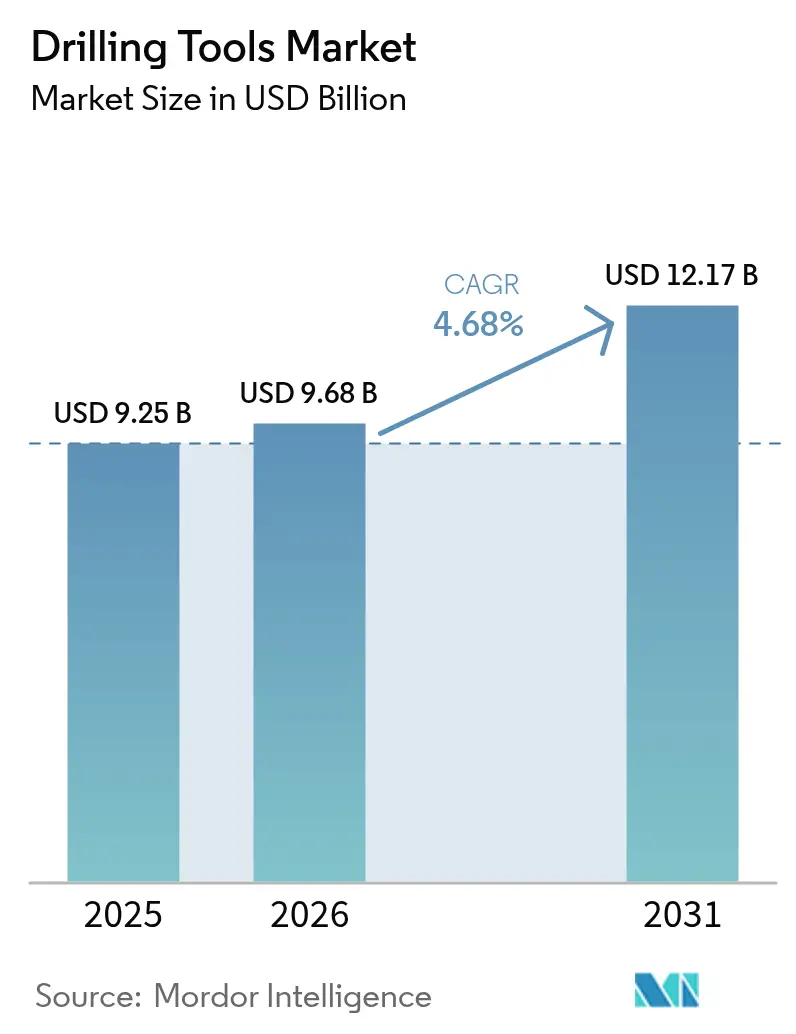

| Market Size (2026) | USD 9.68 Billion |

| Market Size (2031) | USD 12.17 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

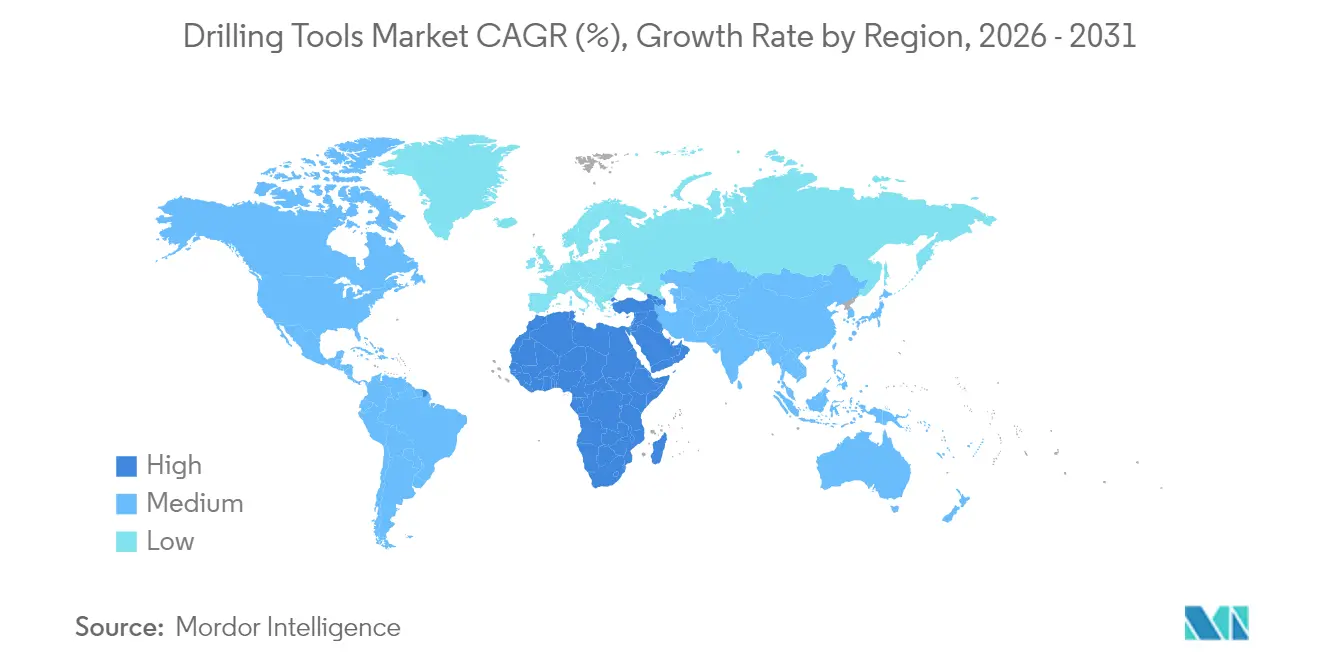

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drilling Tools Market Analysis by Mordor Intelligence

The Drilling Tools market size is expected to grow from USD 9.25 billion in 2025 to USD 9.68 billion in 2026 and is forecast to reach USD 12.17 billion by 2031 at 4.68% CAGR over 2026-2031.

The market’s forward momentum reflects selective reinvestment in high-return wells, improving access to advanced downhole technologies, and growing demand from geothermal and carbon-capture projects that diversify revenue streams away from purely hydrocarbon cycles. Operators are shifting capital toward efficiency-driven programs that shorten rig time and lift production reliability, a trend that rewards premium drill bits, rotary steerable systems, and high-specification mud motors. Momentum is further supported by final investment decisions on deep- and ultra-deepwater assets in Brazil, the US Gulf of Mexico, and West Africa, where elevated pressure and temperature ratings command purpose-built equipment. Meanwhile, supply-chain bottlenecks for specialty metals such as tungsten encourage long-term purchase agreements and foster vertical integration among service providers.

Key Report Takeaways

- By tool type, drill bits captured 31.98% of the drilling tools market share in 2025, while “Other Tools” led growth at an 7.72% CAGR through 2031.

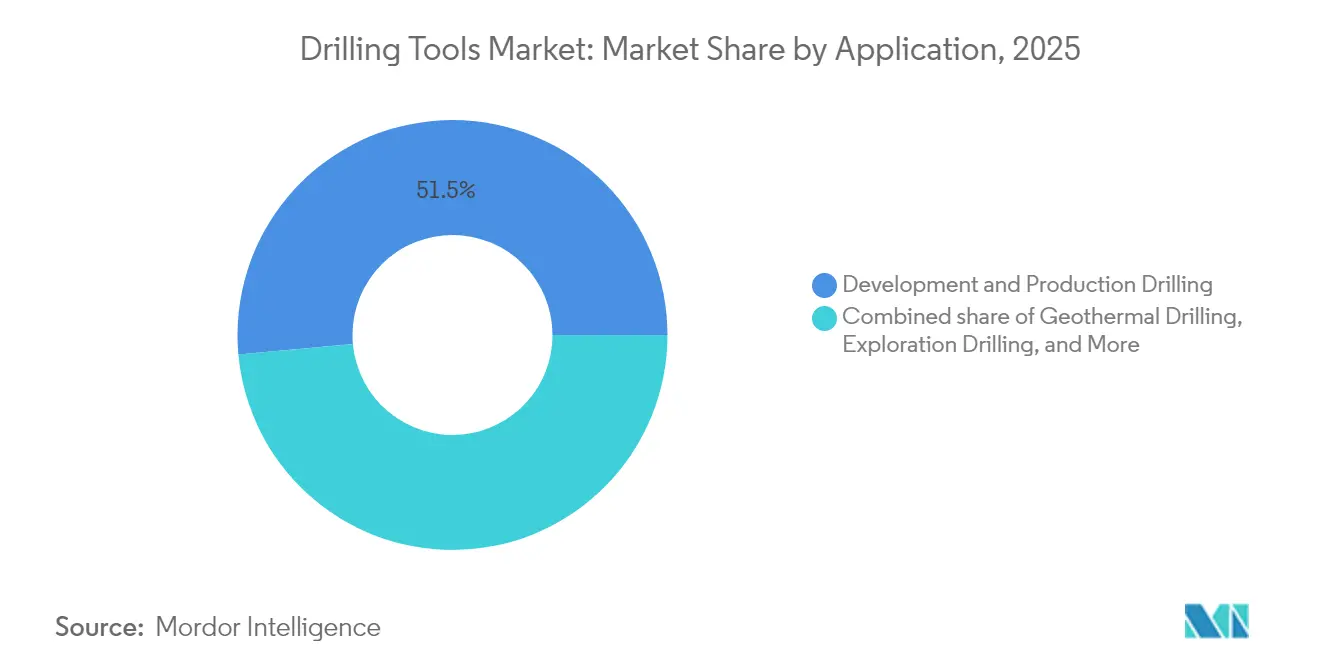

- By application, development and production drilling accounted for 51.45% of the drilling tools market size in 2025; geothermal drilling is set to expand at a 9.21% CAGR to 2031.

- By location of deployment, onshore activity held 67.92% of the drilling tools market share in 2025, whereas offshore applications are advancing at a 5.52% CAGR.

- By geography, North America generated 32.75% of the 2025 revenue, yet the Asia-Pacific region is forecast to post the fastest growth of 6.18% CAGR through 2031.

- SLB, Baker Hughes, Halliburton, NOV, and Weatherford collectively controlled more than 55% of 2024 revenue, underscoring the sector’s moderate concentration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drilling Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upstream CAPEX rebound post-pandemic | +1.2% | Global, with emphasis on North America & Middle East | Medium term (2-4 years) |

| Shale well complexity driving demand for advanced drill bits | +0.8% | North America core, expanding to Argentina & Australia | Long term (≥ 4 years) |

| Expansion of deep- and ultra-deepwater projects | +0.9% | Global offshore basins, led by Brazil, West Africa, Gulf of Mexico | Long term (≥ 4 years) |

| Increasing geothermal drilling investments | +0.6% | Global, with early gains in US, Europe, Indonesia | Medium term (2-4 years) |

| Carbon-capture & storage (CCS) injection well programs | +0.4% | North America & EU regulatory frameworks | Long term (≥ 4 years) |

| Rising demand for critical-mineral exploration drilling | +0.3% | APAC core, spill-over to Australia, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Upstream CAPEX Rebound Post-Pandemic

Global oil and gas investment is set to increase by 22% between 2025 and 2030, reversing three years of capital restraint and renewing demand for high-performance drilling tools, according to the International Energy Forum(1)International Energy Forum, “Growing Demand to Increase Upstream Oil & Gas Investment Needs 22% by 2030,” ief.org . In North America, Gulf of Mexico operators sanctioned multi-billion-dollar projects such as Chevron’s Anchor, which require 20,000 psi-rated equipment and validate the economic case for top-tier drill strings. Middle East national oil companies are likewise reviving infill drilling campaigns aimed at sustaining production quotas. This CAPEX upturn favors tools that deliver measurable rig-time savings, prompting suppliers to bundle rotary steerable systems with digital well-planning platforms. Service agreements are increasingly linking remuneration to improvements in penetration rates, a model that incentivizes continuous product upgrades. Taken together, an improving spend outlook, efficiency mandates, and contractual innovation provide sustained pull for the drilling tools market.

Shale Well Complexity Driving Demand for Advanced Drill Bits

Horizontal laterals now exceed 20,000 ft in premier US shale plays, subjecting drill bits to harsher vibration and cuttings-bed challenges AMERICAN OIL & GAS REPORTER. PDC cutters with advanced thermal-stable diamond and optimized face geometries extend run lengths under such regimes, enabling a single bit to drill multiple intervals NOV(2)NOV, “The Golden Era of Drill Bit Innovation,” nov.com . Meanwhile, AI-driven platforms, such as Halliburton’s LOGIX, analyze real-time torque data to preempt stick-slip, increasing lifting penetration rates by up to 30%. Argentina’s Vaca Muerta and Australia’s Cooper Basin replicate these design imperatives as they scale horizontal programs. Premium bit pricing, therefore, remains resilient, supporting the segment’s 32.3% revenue contribution to the drilling tools market.

Expansion of Deep- and Ultra-Deepwater Projects

The industry’s first 20,000 psi subsea systems entered service at Chevron’s Anchor and BP’s Kaskida, demonstrating commercial viability for fields once deemed uneconomic. Such projects require HP/HT drill pipes, collars, and jars certified to stringent metallurgical and fatigue limits, thereby increasing the average tool spend per well. Brazil and West Africa mirror this momentum with multi-well pre-salt developments that consolidate orders for rotary steerable systems capable of 60°/100 ft dog-leg severity. OEMs offering integrated BHAs and digital twin simulations gain a competitive edge, as operators prioritize full-package contracting to manage the risks associated with ultra-deepwater operations. The resulting premium lifts offshore’s CAGR ahead of onshore despite lower well counts.

Increasing Geothermal Drilling Investments

Enhanced geothermal systems funded by USD 200 million in US research grants adapt oil-field rotary steerable and insulated drill-pipe technologies to 300 °C reservoirs. NOV’s Phoenix PDC series and TK-340TC coatings mitigate thermal degradation and chloride corrosion, thereby lengthening bit life in superhot formations(3)Halliburton, “LOGIX®: precision drilling through intelligent automation,” halliburton.com . Europe supports similar pilots under the EU Innovation Fund, while Indonesia aims to add 17 GW of geothermal capacity by 2030. The crossover enables tool vendors to repurpose existing supply chains, thereby buffering revenue against fluctuations in hydrocarbon prices. As geothermal wells deepen beyond 15,000 ft, demand centers on high-torque mud motors and high-temperature elastomers, expanding the addressable drilling tools market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil prices impacting drilling budgets | -0.7% | Global, with highest sensitivity in North America shale | Short term (≤ 2 years) |

| Stringent environmental regulations on drilling operations | -0.5% | North America & EU, expanding to other regions | Medium term (2-4 years) |

| Supply-chain disruptions for high-spec drill pipes & bits | -0.4% | Global, with critical bottlenecks in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Skilled-labor shortage for digital drilling systems | -0.3% | Global, most acute in North America & Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil Prices Impacting Drilling Budgets

WTI spot prices slipped below USD 70/bbl in early 2025, prompting US independents to trim their planned spending to USD 60.1 billion, 4% lower than the prior guidance. When budgets tighten, non-core exploration wells are deferred, curbing near-term orders for standard drill pipe and collars. Conversely, operators continue to pay premiums for tools that shorten cycle times, sustaining top-end demand even in price troughs. Suppliers that diversify into geothermal or CCS projects gain partial insulation from oil-price swings, tempering but not eliminating the drag on the drilling tools market.

Stringent Environmental Regulations on Drilling Operations

EPA methane rules are expected to impose USD 22-31 billion in compliance costs through 2038, obliging operators to upgrade pneumatic controls and deploy continuous monitoring equipment. On the rig side, higher scrutiny extends to well control and HP/HT safety cases, adding engineering documentation and third-party certification requirements that lengthen procurement cycles. Smaller operators may exit marginal fields, reducing tool demand, while larger firms negotiate bundled contracts with service majors to manage compliance. This shift accelerates market consolidation, yet restricts overall well counts, thereby trimming the growth trajectory of the drilling tools market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: Premium Technologies Drive Market Evolution

Drill bits generated USD 2.96 billion in 2025, equal to 31.98% of the drilling tools market size, underscoring their pivotal role in well economics. Continued adoption of thermally stable PDC cutters and real-time imaging at the bit face allows operators to achieve single-run curves in interbedded formations, reducing connection time and NPT. OEMs capture price premiums by packaging bits with digital advisory software that recommends rotary speed and weight-on-bit adjustments in real time.

The “Other Tools” category—jars, shock subs, mud motors, and rotary steerable systems—will outpace overall growth at an 7.72% CAGR. Halliburton’s iCruise and Baker Hughes’ AutoTrak generate dynamic steering corrections that cut slide-rotate cycles, while SLB’s Suppressor dampening tool mitigates torsional oscillation by more than 60%. That performance edge justifies higher day rates, despite budget pressure, and anchors robust revenue expansion for full-suite providers.

By Application: Energy Transition Reshapes Demand Patterns

Development and production drilling accounted for 51.45% of 2025 revenue, reflecting operators’ focus on brownfield optimization and resource recovery. Multi-well pad designs and batch drilling intensify tool utilization, driving steady orders for drill pipe, reamers, and downhole vibration absorbers. Exploration drilling, although cyclical, gains strategic importance in frontier deepwater blocks sanctioned by major oil companies seeking to renew their portfolios.

Geothermal wells represent the fastest floor-count addition, advancing at a 9.21% CAGR as governments fund superhot rock pilots. Carbon-capture injection wells form a smaller but fast-scaling niche, where directional profiles require abrasion-resistant bottom-hole assemblies capable of handling dense CO₂ muds. The positive spill-over broadens the customer mix and offsets oil price-driven volatility, adding resilience to the drilling tools market.

By Location of Deployment: Offshore Premium Drives Value Creation

Onshore operations accounted for 67.92% of the 2025 turnover, driven by high-volume unconventional programs in the US, Canada, Argentina, and China. Standardized rig fleets, lower logistics costs, and shorter cycle times characterize this segment, tilting procurement toward cost-competitive drill strings and motors. Yet offshore activity, particularly ultra-deepwater, delivers stronger margin capture.

Offshore growth at 5.52% CAGR hinges on HP/HT discoveries such as Ballymore and Trion, where each well can require USD 20 million worth of specialized tools and services. Complex geomechanics drive the adoption of wired drill-pipe telemetry and remote steering consoles, allowing real-time trajectory correction from onshore centers. Suppliers with integrated surface-to-seabed portfolios hold a structural advantage, deepening the gulf between tier-one and regional competitors.

By End-User: Operator Consolidation Reshapes Procurement Patterns

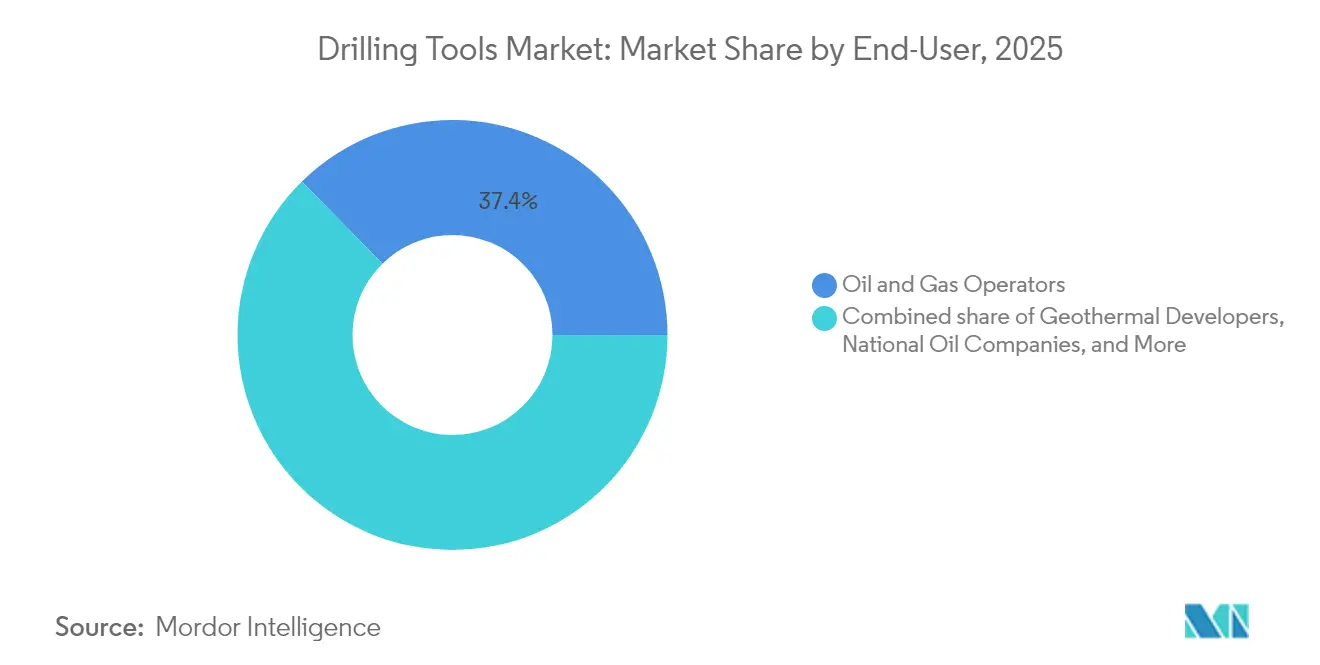

Oil and gas operators remained the single largest buyer group at 37.35% in 2025. Supermajors leverage global master service agreements to secure fleet-wide access to rotary steerable systems and high-torque motors, bundling them with analytics subscriptions that guarantee performance benchmarks. National oil companies, notably those in the Middle East, pursue local content targets by co-manufacturing drill bits and collars under technology transfer arrangements.

Geothermal developers are registering the quickest expansion, with a 9.21% CAGR driven by policy incentives and the technical similarity between geothermal and unconventional oil drilling. Independent E&Ps are increasingly outsourcing tool management to drilling contractors under lump-sum, turnkey deals, which is shrinking spot-purchase volumes but lengthening contract tenures. Mining exploration firms, though still niche, employ oil-field coring tools to accelerate critical-mineral discovery programs, adding breadth to the drilling tools market demand base.

Geography Analysis

North America generated 32.75% of 2025 revenue, driven by record Permian horizontal footage and resilient Gulf of Mexico deepwater campaigns. The region’s advanced logistics and digital drilling ecosystem keeps equipment utilization high, even as capital discipline tempers rig additions. Federal methane rules and state-level setback regulations pressure smaller operators, yet the supermajors’ adoption of triple-frac completion methods is increasing drill-pipe torque requirements and sustaining premium-tool demand.

Asia-Pacific leads growth at a 6.18% CAGR through 2031. China’s national firms drive deep onshore targets in the Tarim and Sichuan basins, demanding abrasion-resistant PDC bits and high-temperature mud motors. Indonesia pursues geothermal baseload projects, while Australia’s critical-mineral exploration creates a fresh pull for coring bits compatible with HP hard-rock drilling. Collectively, these trends expand the drilling tools market footprint across both hydrocarbon and renewable value chains.

Europe, anchored by Norway and the UK, maintains tooling demand via brownfield tie-backs and a surge of CCS wells under the North Sea Transition Deal. The Middle East and Africa capitalize on low breakeven reservoirs and state-sponsored capacity expansions, though political risk occasionally delays purchase orders. South America, buoyed by Brazil’s pre-salt, channels large integrated contracts to SLB and Baker Hughes, concentrating market share within a handful of vendors. The combined regional dynamics underscore a gradual shift from volume-led to efficiency-led purchasing.

Competitive Landscape

Consolidation defines the current competitive storyline. SLB’s USD 7.1 billion purchase of ChampionX fortifies its chemicals and artificial-lift offering, adding surface-production synergies to the downhole portfolio. Helmerich & Payne’s USD 1.97 billion acquisition of KCA Deutag quadruples its Middle East rig count, granting direct control over tool specification and procurement cycles. These moves illustrate how scale and integration help absorb R&D costs for AI-enabled drilling systems.

Technological differentiation remains the principal moat. Halliburton and Sekal achieved the world’s first automated on-bottom drilling system, uniting LOGIX and Drilltronics for closed-loop drilling parameter control. Baker Hughes invests in electrified surface units that cut emissions while synchronizing with high-speed downhole telemetry. NOV prioritizes high-temperature materials science to unlock geothermal revenues, collaborating with research labs on the stability of carbide matrices.

Disruption potential exists from software-native entrants developing reservoir-aware advisory engines, although safety certification requirements and incumbent bundling hamper acceptance. Regional toolsmiths coexist by specializing in reamers, stabilizers, or coring gear for hard-rock minerals; however, rising metallurgical standards are raising the capital barrier. The sector’s preference for performance-based contracts ultimately biases market share toward firms delivering integrated hardware-software packages.

Drilling Tools Industry Leaders

NOV Inc.

Halliburton Company

Schlumberger Limited

Baker Hughes Company

Weatherford International Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SLB completed its ChampionX acquisition for USD 7.1 billion, targeting USD 400 million annual synergies within three years.

- June 2025: Chevron and Halliburton deployed intelligent hydraulic fracturing using ZEUS IQ to automate stage execution.

- May 2025: SLB unveiled an at-bit imaging tool that enhances wellbore placement safety.

- April 2025: Baker Hughes released Hummingbird, an all-electric land cementing system, and SureCONTROL Plus valves to reduce emissions.

Global Drilling Tools Market Report Scope

The drilling tools market report includes:

| Drill Bit |

| Drill Pipe |

| Drill Collar |

| Drill Reamer and Stabilizer |

| Drill Swivel |

| Other Tools (Jars, Shock Subs, Mud Motors, RSS) |

| Exploration Drilling |

| Development and Production Drilling |

| Workover and Well Intervention |

| Geothermal Drilling |

| CCS and Injection Wells |

| Onshore |

| Offshore |

| Oil and Gas Operators |

| National Oil Companies |

| Independent EandP |

| Drilling Contractors |

| Geothermal Developers |

| Mining Exploration Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Tool Type | Drill Bit | |

| Drill Pipe | ||

| Drill Collar | ||

| Drill Reamer and Stabilizer | ||

| Drill Swivel | ||

| Other Tools (Jars, Shock Subs, Mud Motors, RSS) | ||

| By Application | Exploration Drilling | |

| Development and Production Drilling | ||

| Workover and Well Intervention | ||

| Geothermal Drilling | ||

| CCS and Injection Wells | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By End-User | Oil and Gas Operators | |

| National Oil Companies | ||

| Independent EandP | ||

| Drilling Contractors | ||

| Geothermal Developers | ||

| Mining Exploration Firms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the drilling tools market?

The drilling tools market size was USD 9.68 billion in 2026 and is forecast to reach USD 12.17 billion by 2031 on a 4.68% CAGR trajectory.

Which region leads global sales?

North America held 32.75% of 2025 revenue due to high unconventional activity and deepwater projects.

Which application segment is expanding fastest?

Geothermal drilling is projected to register the quickest 9.21% CAGR through 2031 as energy-transition funding accelerates.

How will offshore demand evolve?

Offshore wells—especially ultra-deepwater—are expected to grow at a 5.52% CAGR, supported by HP/HT project sanctions in Brazil, the Gulf of Mexico, and West Africa.

What technologies are shaping competitive advantage?

AI-enabled rotary steerable systems, at-bit imaging, and high-temperature PDC bits are central to performance-based contracting and margin expansion.

How do environmental rules affect tool demand?

Stricter methane and HP/HT regulations increase compliance costs, prompting operators to adopt premium, low-emission drilling tools that meet new safety standards.

Page last updated on: