Specialty Tapes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

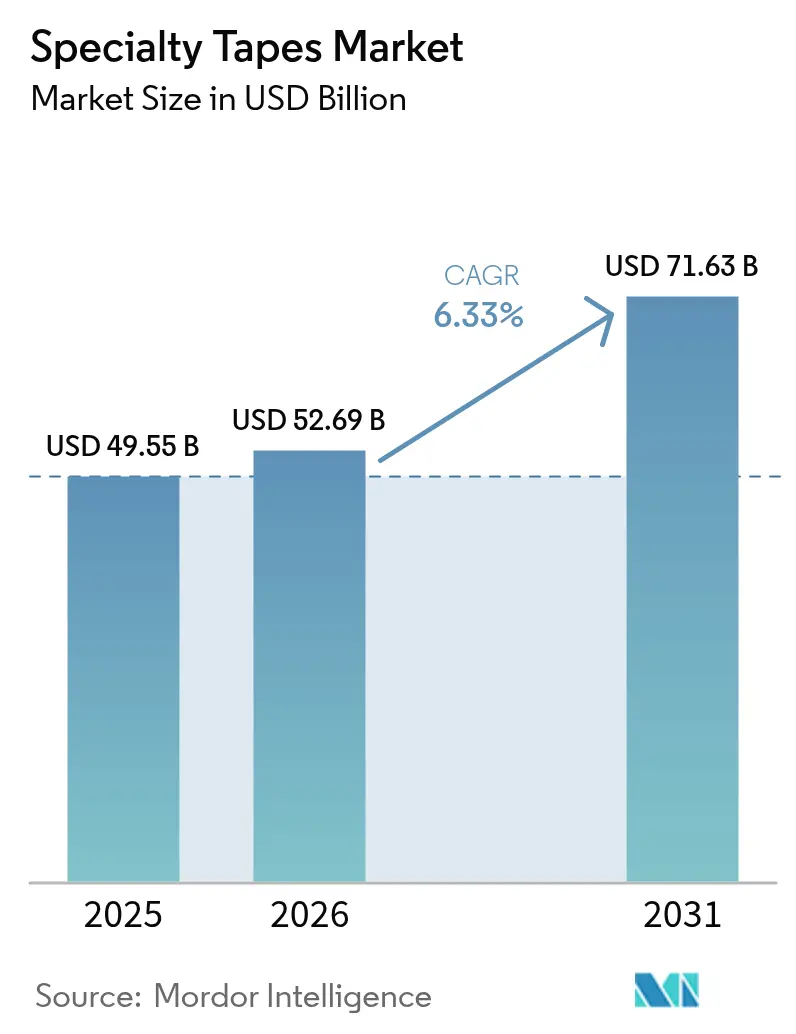

| Market Size (2026) | USD 52.69 Billion |

| Market Size (2031) | USD 71.63 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

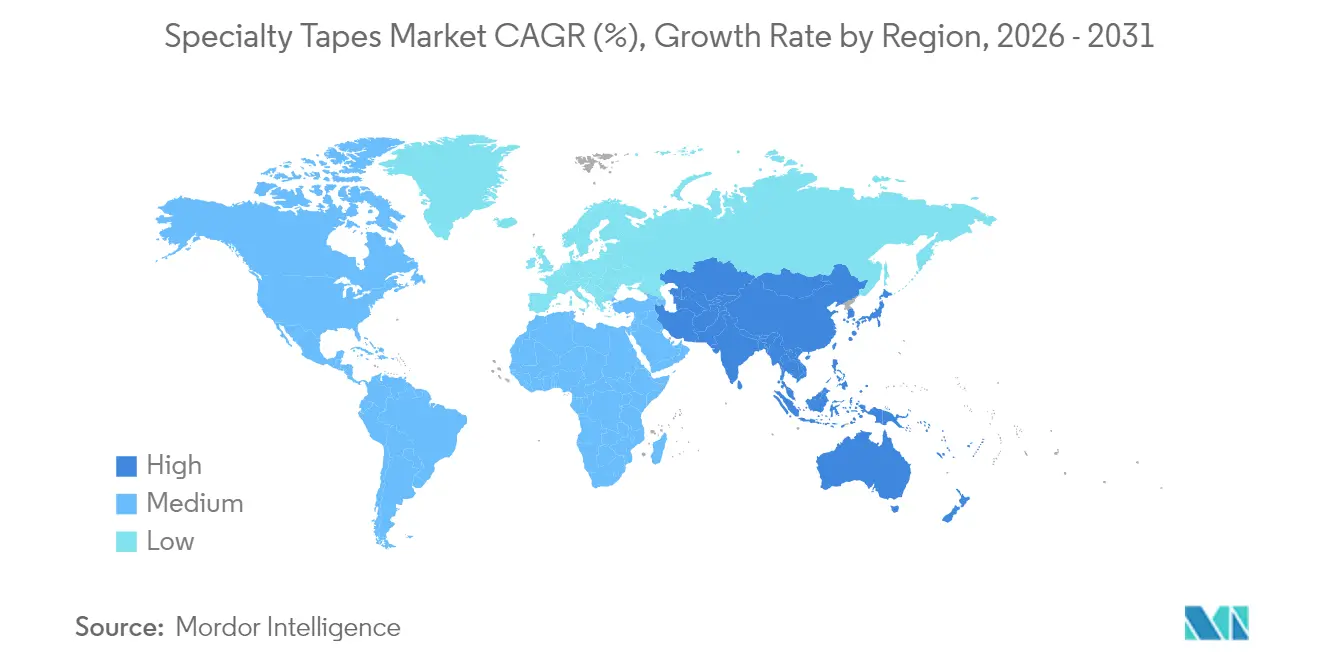

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Tapes Market Analysis by Mordor Intelligence

The Specialty Tapes Market size is expected to grow from USD 49.55 billion in 2025 to USD 52.69 billion in 2026 and is forecast to reach USD 71.63 billion by 2031 at 6.33% CAGR over 2026-2031. Strong demand from electronics, healthcare, and electric-vehicle manufacturing drives accelerated adoption of high-performance bonding, sealing, and protection solutions. Structural adhesive tapes continue to displace mechanical fasteners in weight-sensitive assemblies, while solvent-free chemistries support compliance with tightening emissions rules. Innovation in skin-friendly formulations for medical wearables and optically clear adhesives for foldable displays further increases product differentiation. Suppliers that combine vertical integration with sustainable material development capture rising orders as PFAS restrictions and VOC caps reshape customer specifications.

Key Report Takeaways

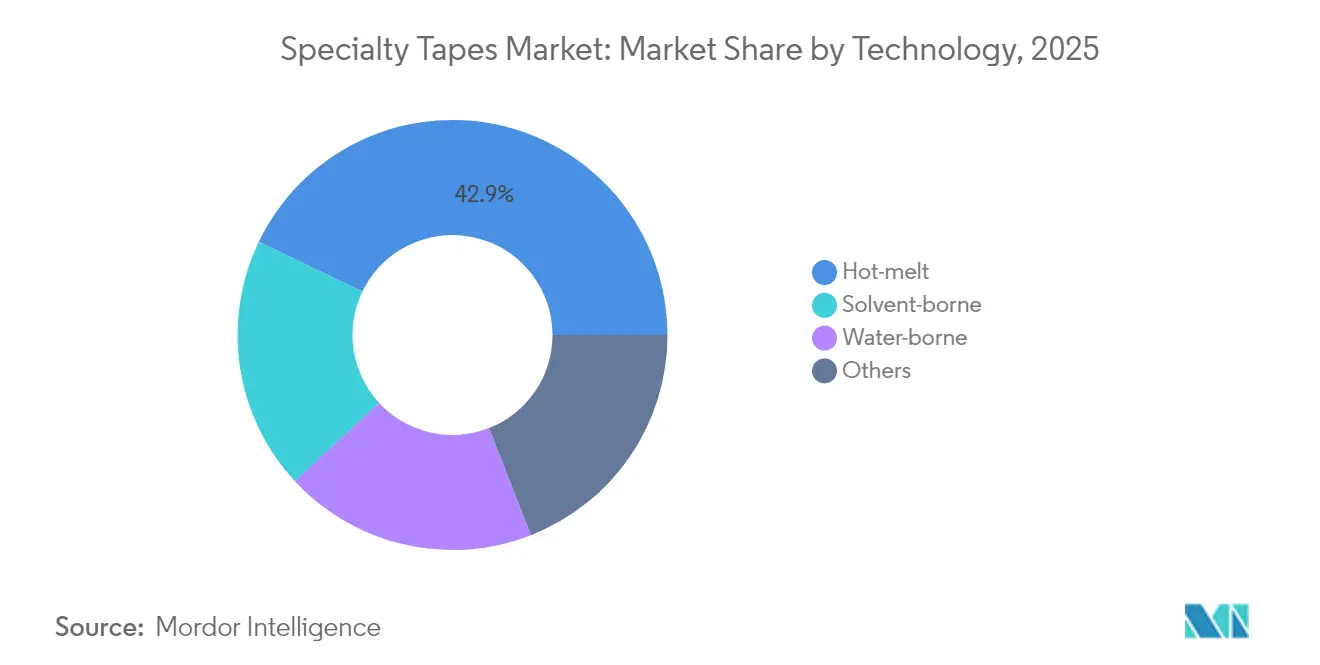

- By technology, hot-melt systems led with 42.85% of the specialty tapes market size in 2025 and are set to grow at a robust 6.98% CAGR.

- By adhesive resin, acrylics dominated with 46.75% revenue share in 2025; rubber-based formulations are poised for the highest 7.52% CAGR to 2031.

- By type, polyvinyl chloride accounted for 36.95% of specialty tapes market size in 2025, while woven/non-woven substrates will record the fastest 7.18% CAGR.

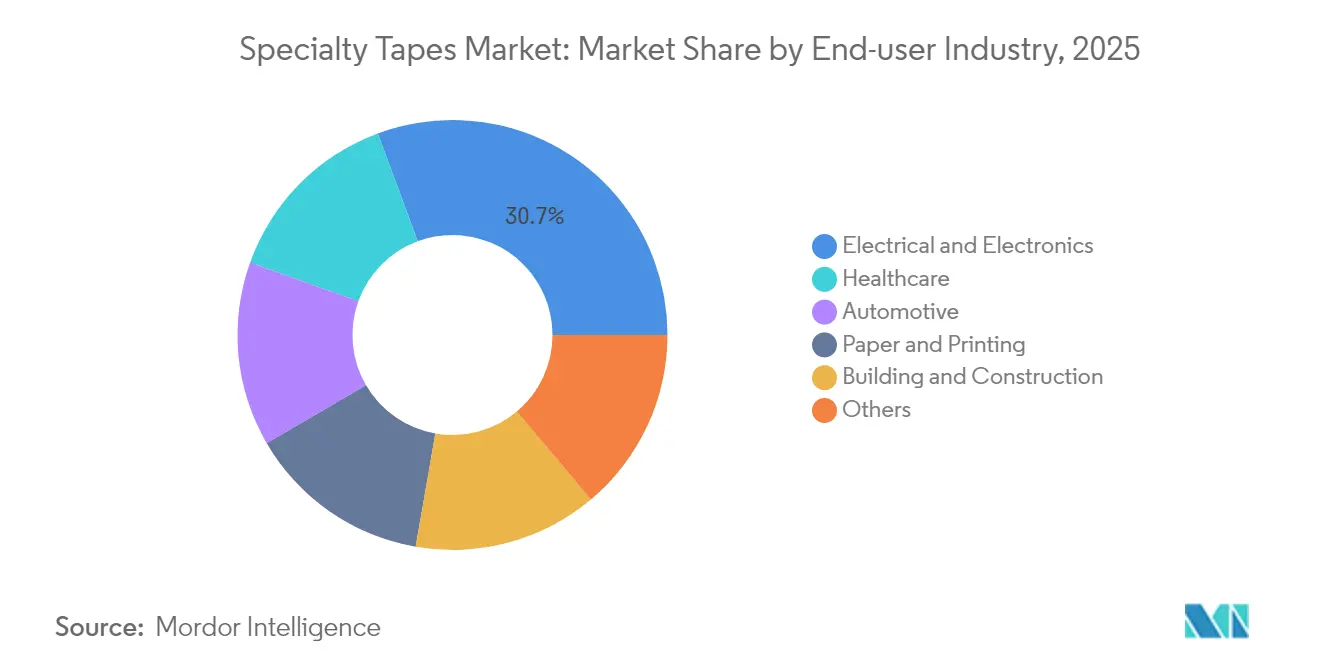

- By end-user industry, the electrical and electronics segment held 30.65% of specialty tapes market share in 2025, whereas healthcare is projected to expand at the fastest 7.35% CAGR through 2031.

- By geography, Asia Pacific captured 40.85% of specialty tapes market share in 2025 and is forecast to record the strongest 7.76% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specialty Tapes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding healthcare and wearable-device demand | +1.2% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Growth in flexible electronics and EV battery packs | +1.0% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Construction boom in Asia Pacific green buildings | +0.8% | APAC core, emerging in MEA | Medium term (2-4 years) |

| Lightweighting trend in auto and rail interiors | +0.7% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Emergence of thermal-management tapes for EV cells | +0.6% | Global, with concentration in China, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Healthcare and Wearable-Device Demand

Medical wearables such as continuous glucose monitors, smart bandages, and cardiac patches increasingly rely on skin-compatible tapes that combine strong initial tack with atraumatic removal. Growing adoption of remote patient monitoring accelerates demand for breathable, moisture-managing adhesives, with Avery Dennison Medical emphasizing long-term comfort in extended-wear devices[1]“Skin-Friendly Adhesive Platforms for Wearables,” medical.averydennison.com. Optically clear constructions that maintain transparency under dynamic skin movement enable advanced biosensor integration, shifting formulation priorities toward biocompatibility and low-trauma removal.

Growth in Flexible Electronics and EV Battery Packs

Foldable smartphones, rollable televisions, and ultra-thin displays require optically clear tapes that endure thousands of bend cycles without haze formation while safeguarding internal circuitry. Thermal interface tapes in EV battery modules mitigate cell-to-cell heat transfer, improving pack safety during thermal runaway. LINTEC Corporation’s focus on semiconductor packaging tapes targets reflow-resistant, EMI-shielding solutions for advanced chip designs. Structural adhesive tapes now replace screws in battery pack assembly, trimming weight while boosting vibration resistance.

Construction Boom in Asia Pacific Green Buildings

LEED-oriented regulations spur adoption of low-VOC specialty tapes in curtain-wall and building-envelope systems[2]“EPA Final Rule on Methylene Chloride,” adhesivesmag.com. tesa’s 2024 expansion in Mumbai and Bengaluru positions production close to India’s energy-efficient building market, including solar installations and modular construction. High-performance tapes enhance air- and water-sealing functions in prefabricated modules, supporting faster site assembly while maintaining weatherproofing integrity.

Lightweighting Trend in Auto and Rail Interiors

Automakers replace mechanical fasteners with pressure-sensitive tapes to reduce mass and improve noise, vibration, and harshness in EV cabins. Avery Dennison offers foam and fiber bonding adhesives that handle diverse substrates such as polyurethane foams and EPDM elastomers. Rail operators adopt tapes for panel attachment, leveraging stress-distribution and thermal-expansion benefits. Advanced adhesive lines allow reworkability during assembly while delivering enduring structural performance once vehicles enter service.

Restraints Impact Analysis*

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -0.9% | Global, with higher impact in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| Tight VOC/solvent-emission regulations | -0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| PFAS-related litigation and reformulation costs | -0.4% | North America and EU primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Price Volatility

Acrylic and rubber resin costs rise sharply when crude-oil-derived monomer prices spike, compressing margins for manufacturers unable to pass increases downstream. Ethylene volatility feeds through to polyvinyl chloride backings. European chemical producers report sustained energy-cost pressure, further tightening supply. Vertical integration and long-term supply contracts remain key hedges against cost swings.

Tight VOC/Solvent-Emission Regulations

The US EPA banned methylene chloride in consumer adhesives in 2024, accelerating migration to water-based and hot-melt lines. Europe’s Chemicals Strategy for Sustainability employs generic risk assessment to restrict solvent systems across industries, prompting multimillion-dollar reformulation programs. Smaller suppliers without research and development scale face exit or acquisition as compliance timelines shorten.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hot-Melt Dominance Continues

Hot-melt systems contributed 42.85% of specialty tapes market size in 2025, and their 6.98% CAGR indicates enduring preference for solvent-free, fast-setting options suitable for high-speed automated lines. Water-borne variants gain traction where substrates cannot tolerate 150 °C application temperatures, particularly in sensitive medical diagnostics.

Sustainability targets spur adoption of bio-sourced hot-melt resins based on tall-oil fatty acids and sugar-derived polyols. Henkel and Packsize demonstrated a 32% greenhouse-gas reduction with corn-based formulations in 2025 packaging trials. Equipment vendors broaden nozzle technology to apply patterns that cut adhesive use by up to 25%, aligning with both cost-reduction and ESG goals.

By Adhesive Resin: Acrylic Leadership Challenged

Acrylics commanded 46.75% specialty tapes market share in 2025 through balanced adhesion, UV stability, and cost profile. Specialty tapes market size for rubber-based formulations, however, is on track to expand 7.52% annually as OEMs seek flexibility under cold-temperature impact and rapid assembly adhesion. Silicone adhesives service high-temperature zones up to 260 °C, critical for electronics coupling and aerospace masking, yet their premium cost caps broader penetration. Hybrid chemistries that graft silicone blocks onto acrylic backbones emerge to balance temperature tolerance with price.

By Type: Woven Solutions Gain Traction

Polyvinyl chloride captured 36.95% specialty tapes market share in 2025, favored for chemical resistance, flame retardancy, and cost efficiency. Specialty tapes market size for woven and non-woven substrates, however, is forecast to expand at 7.18% CAGR, outpacing PVC as OEMs seek breathable, drapable materials for body-worn sensors and vehicle interior upholstery. Polyethylene terephthalate remains indispensable in flexible printed circuit board assembly owing to its dimensional stability under 260 °C reflow peaks. Paper and kraft backings serve masking, splicing, and easy-tear applications but face substitution risk where humidity exposure is high.

By End-User Industry: Healthcare Drives Innovation

The healthcare vertical accounted is projected to grow at 7.35% CAGR through 2031. Electrical and electronics still represent the largest revenue pool at 30.65%, reflecting entrenched reliance on thermal interface and EMI-shielding tapes for semiconductor packaging. Rising adoption of remote patient monitoring accelerates demand for breathable, skin-friendly constructions, prompting material suppliers to prioritize low-trauma removal and moisture management. The specialty tapes market continues to penetrate automotive assemblies, where lightweighting initiatives align with electrification goals by replacing clips and screws with advanced adhesive lines. Structural bonding in packaging machinery, paper converting, and printing maintains a steady baseline, cushioning cyclical downturns in discretionary sectors.

Geography Analysis

Asia Pacific’s 40.85% specialty tapes market share in 2025 underscores the region’s integration across electronics, construction, and mobility supply chains India’s Smart Cities Mission finances green-building retrofits that favor low-VOC window tapes capable of sustaining −10 °C to +70 °C service temperatures. In Japan, automotive OEMs source double-sided acrylic foam tapes for pillar trim, cutting assembly time by 30% relative to clip-based methods.

North America capitalizes on medical-grade demand from 6,000 hospitals and a rapidly expanding at-home diagnostics sector. Europe benefits from regional automotive electrification mandates that raise thermal-management tape consumption. The Middle East and Africa posts mid-single-digit growth as megaprojects like NEOM integrate high-performance façade sealing systems. South America’s share is anchored by Brazil’s white-goods and flexible-packaging output; domestic suppliers invest in acrylic monomer plants to curb import dependence. Across emerging regions, government subsidies for solar farms and wind turbines enlarge demand for UV-stable adhesive films that endure 25-year outdoor exposure.

Competitive Landscape

The market is moderately fragmented. Multinationals including 3M, Nitto Denko, and tesa steward broad portfolios spanning PVC electrical tapes to high-end optically clear and thermally conductive grades. Patent barriers remain significant. Regional specialists differentiate through converting agility and custom die-cutting services, especially for short-run medical and electronics programs where speed trumps scale.

Specialty Tapes Industry Leaders

3M

Avery Dennison Corporation

Nitto Denko Corporation

tesa SE

Intertape Polymer Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Berry Global agreed to sell its Specialty Tapes business to Nautic Partners for USD 540 million. The unit now operates as Vybond under Nautic ownership.

- August 2024: tesa SE announced plans to integrate green hydrogen into production, with the first hydrogen-enabled adhesive tapes slated for Hamburg-Hausbruch in 2027.

Global Specialty Tapes Market Report Scope

The specialty tapes market report includes:

| Solvent-borne |

| Water-borne |

| Hot-melt |

| Others |

| Acrylic |

| Rubber |

| Silicone |

| Others (Cyanoacrylate, Epoxy, PU) |

| Woven / Non-woven |

| Polyvinyl Chloride |

| Polyethylene Terephthalate |

| Paper |

| Polypropylene |

| Others |

| Healthcare |

| Electrical and Electronics |

| Automotive |

| Paper and Printing |

| Building and Construction |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Solvent-borne | |

| Water-borne | ||

| Hot-melt | ||

| Others | ||

| By Adhesive Resin | Acrylic | |

| Rubber | ||

| Silicone | ||

| Others (Cyanoacrylate, Epoxy, PU) | ||

| By Type | Woven / Non-woven | |

| Polyvinyl Chloride | ||

| Polyethylene Terephthalate | ||

| Paper | ||

| Polypropylene | ||

| Others | ||

| By End-user Industry | Healthcare | |

| Electrical and Electronics | ||

| Automotive | ||

| Paper and Printing | ||

| Building and Construction | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the specialty tapes market?

The specialty tapes market stands at USD 52.69 billion in 2026 and is on track to reach USD 71.63 billion by 2031.

Which end-user segment is growing the fastest?

Healthcare applications are expanding at a 7.35% CAGR, driven by wearables and advanced medical devices that require skin-friendly, breathable adhesives.

Why are hot-melt specialty tapes so dominant?

Hot-melt tapes combine solvent-free compliance with rapid processing, commanding 42.85% market share in 2025 and maintaining a 6.98% growth rate as VOC regulations tighten.

How significant is Asia Pacific in specialty tape consumption?

Asia Pacific captured 40.85% of global revenue in 2025 and is expected to post the strongest 7.76% CAGR through 2031 on the back of electronics and EV production.

What regulatory trends most affect specialty tapes producers?

Key pressures include VOC emission caps, PFAS restrictions, and escalating litigation tied to hazardous-substance designations, all driving costly reformulation initiatives.

Page last updated on: