Dosing Pumps Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

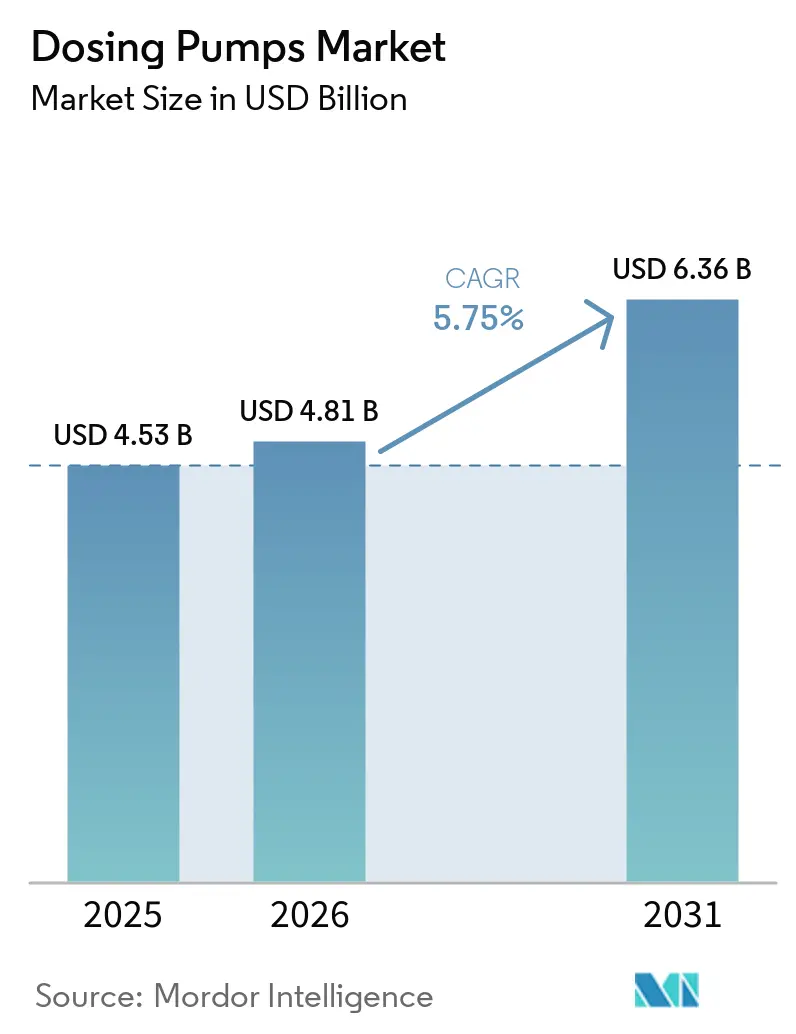

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 6.36 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dosing Pumps Market Analysis by Mordor Intelligence

The Dosing Pumps Market size was valued at USD 4.53 billion in 2025 and is estimated to grow from USD 4.81 billion in 2026 to reach USD 6.36 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031). Utility operators are shifting from reactive to predictive maintenance, pharmaceutical manufacturers are moving to continuous-flow production, and regulators are tightening nutrient-discharge limits. Precision metering, verifiable audit trails, and secure remote connectivity are now minimum procurement requirements. Peristaltic pumps gain momentum because they tolerate dry-run conditions, isolate fluids from moving parts, and cut unplanned downtime, while per-use digital twins help operators match chemical feed to real-time load. Cyber-secure controllers that support IEC 62443 and FDA 21 CFR Part 11 are drawing premium prices as end-users prepare for forthcoming cybersecurity audits.

Key Report Takeaways

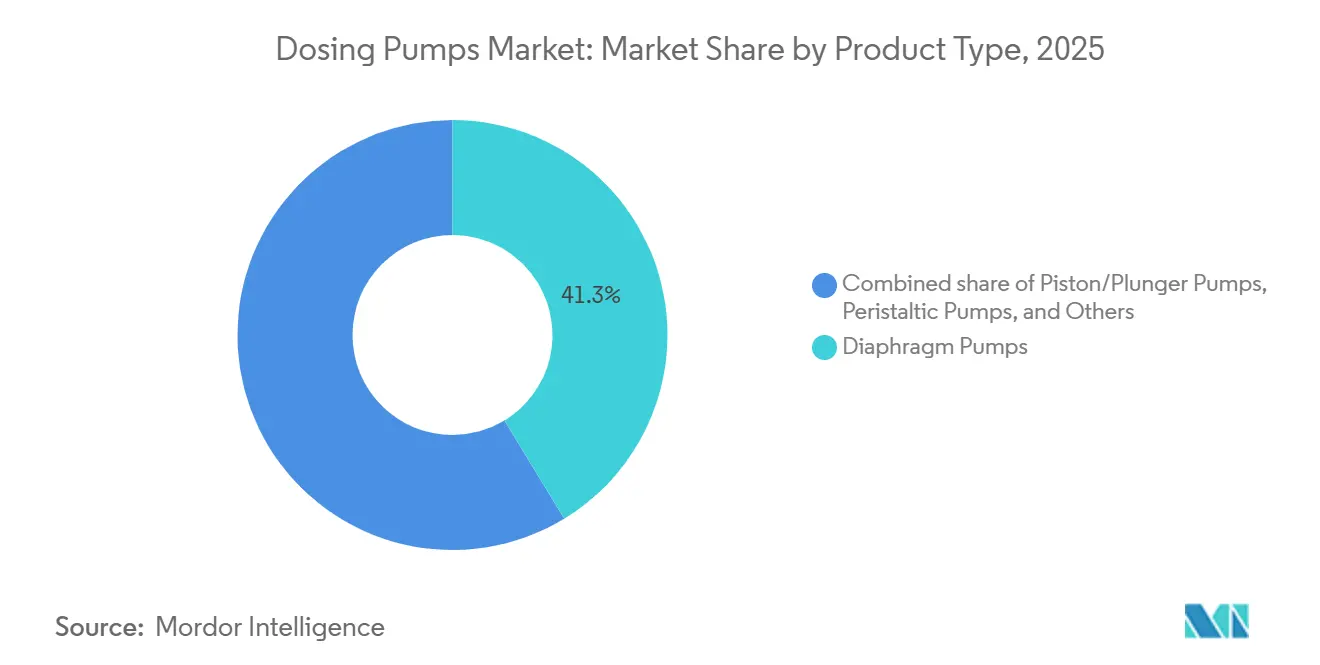

- By product type, diaphragm pumps led with 41.3% of dosing pumps market share in 2025; peristaltic variants are expanding at a 6.8% CAGR through 2031.

- By application, water and wastewater treatment accounted for a 33.9% slice of the dosing pumps market size in 2025, while pharmaceuticals and biotech are expected to advance at a 7.1% CAGR to 2031.

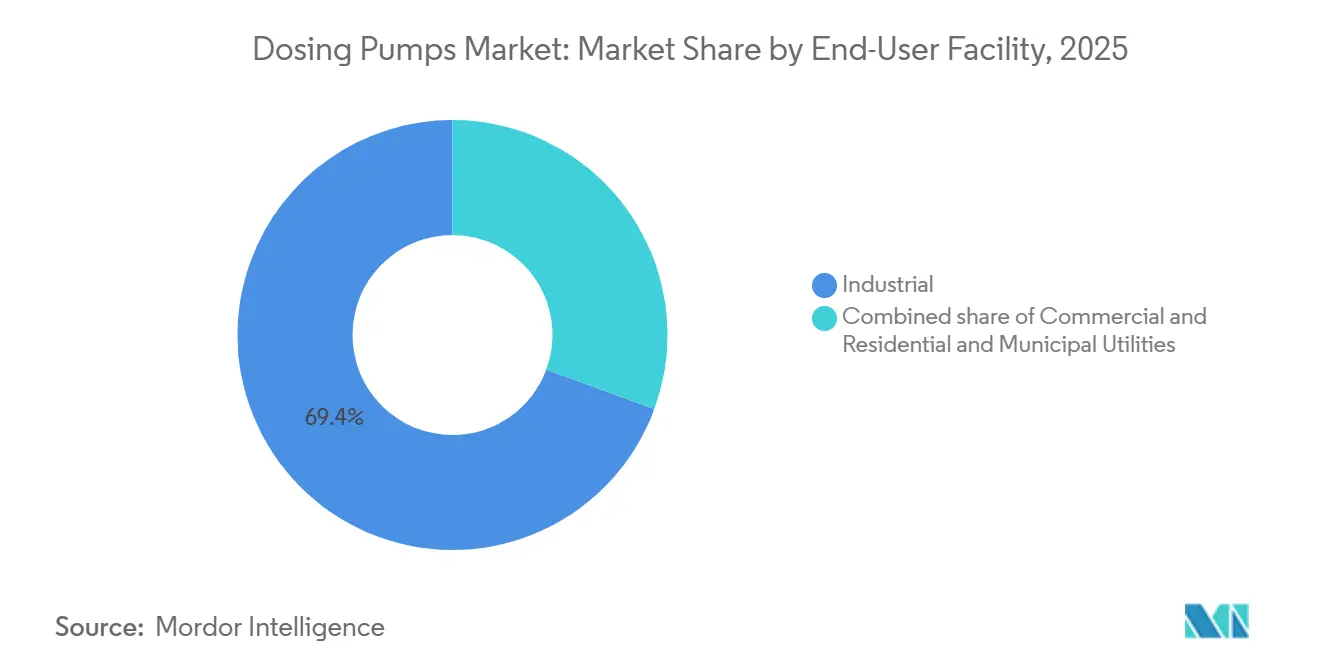

- By end-user facility, industrial sites held 69.4% of demand in 2025; residential and municipal utilities are forecast to grow at a 6.6% CAGR through 2031 as new EU rules capture plants down to 1,000 population equivalents.

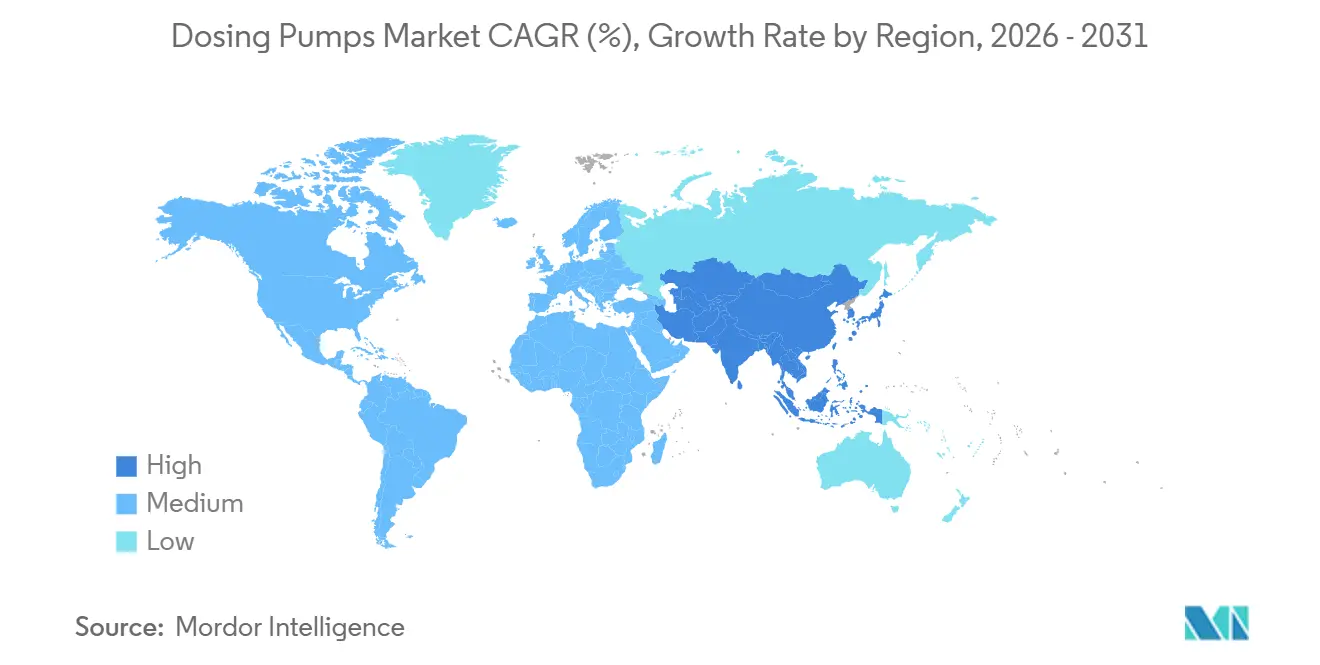

- By geography, Asia-Pacific commanded 40.8% of 2025 revenue and is set to post a 6.4% CAGR to 2031 on the back of India’s USD 6.7 billion wastewater-infrastructure grants and refinery expansions across China, India, and the Gulf.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dosing Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising water & wastewater infrastructure spend | +1.80% | Global, concentrated in North America, EU, India, Middle East | Medium term (2-4 years) |

| Stringent environmental dosing-accuracy norms | +1.20% | EU, North America, Asia-Pacific | Long term (≥ 4 years) |

| Oil & gas chemical-injection upswing | +0.90% | Middle East, Asia-Pacific, Latin America | Medium term (2-4 years) |

| AI-enabled remote-monitoring adoption | +0.70% | Global early adoption in North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Precision micro-dosing for continuous-flow biotech | +0.60% | North America, Western Europe, select Asia-Pacific | Medium term (2-4 years) |

| EU phosphorus-removal retrofit mandates | +0.50% | EU Member States, candidate countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Water & Wastewater Infrastructure Spend

Capital funding is accelerating. The U.S. Environmental Protection Agency earmarked USD 2.6 billion for clean-water projects and a further USD 800 million for emerging contaminants in FY 2025, with California, Texas, and New York receiving the largest state allocations.[1] U.S. Environmental Protection Agency, “National Water Program Guidance FY 2025-2026,” epa.gov India’s Finance Commission recommended INR 56,100 crore (USD 6.7 billion) of wastewater grants for mid-sized cities during 2026-2031 to lift treatment rates above 37.5%.[2]Swarajya Staff, “India’s Wastewater Infra Push,” swarajyamag.com Yorkshire Water’s USD 22.8 million Dewsbury upgrade exceeded 90% phosphorus-reduction targets and forms part of a USD 444 million program to retrofit 85 plants by 2030.[3]SmartWater Magazine, “Yorkshire Water Delivers Phosphorus Upgrade,” smartwatermagazine.com These outlays drive procurement of coagulation, pH-control, and disinfection skids that embed smart dosing pumps.

Stringent Environmental Dosing Accuracy Norms

The recast EU Urban Wastewater Treatment Directive lowered coverage to 1,000 population equivalents and set phosphorus limits of 0.5 mg/L for large plants, with quaternary treatment mandating 80% micropollutant removal by 2045.[4]European Parliament and Council, “Directive (EU) 2024/3019 concerning urban wastewater treatment,” eur-lex.europa.eu Extended Producer Responsibility shifts up to 80% of quaternary-treatment costs to pharmaceuticals and cosmetics producers, shrinking municipal funding gaps. Utilities, therefore, specify metering pumps that deliver ±1% flow accuracy and provide tamper-proof electronic records. IEC 62443 compliance is emerging as a bid-score differentiator, especially in Europe and North America.

Oil & Gas Chemical Injection Demand Upswing

OPEC’s 2025 World Oil Outlook foresees 19.5 million b/d of new refining capacity to 2050, with 70% in Asia-Pacific, Africa, and the Middle East. Secondary processing, carbon capture, and enhanced-oil-recovery projects all rely on high-pressure, corrosion-resistant dosing systems for amines, corrosion inhibitors, and catalysts. Certification to ATEX and IECEx remains essential, and vendors offering rugged plunger units rated above 16 bar retain a foothold in these harsh-duty niches.

AI-Enabled Remote-Monitoring Adoption

Utilities are embedding vibration, temperature, and flow sensors to support predictive maintenance. A German chemical site fitted LoRaWAN sensors on three river-water pumps and cut downtime by 70% while extending service life by 30%. Xylem’s majority stake in Idrica integrates analytics into Xylem Vue, halving non-revenue water in Hot Springs, Arkansas, and saving 17% network-wide consumption in Monterrey, Mexico. Remote firmware updates, OPC-UA interfaces, and dashboard-based alarm management now rank alongside hydraulic performance in tender evaluations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.80% | Global, acute in Asia-Pacific and India | Short term (≤ 2 years) |

| Low-cost Asian maker price pressure | -0.60% | Asia-Pacific, export spillovers | Medium term (2-4 years) |

| Cyber-security risk in networked pumps | -0.30% | North America, EU, Asia-Pacific metros | Medium term (2-4 years) |

| Skilled-maintenance labor shortages | -0.40% | Global, most acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Indian steel prices climbed more than 20% between late 2023 and Q1 2025 after safeguard tariffs of up to 15% on Chinese alloy imports, squeezing OEM margins and deferring tenders. Elastomer costs tied to petrochemical feedstocks remain elevated, and small manufacturers lack the scale to hedge, forcing specification downgrades or delivery deferrals in emerging-market projects.

Low-Cost Asian Maker Price Pressure

Domestic producers in China and India undercut multinational list prices by as much as 40% on standard diaphragm units, eroding margins. Regulated buyers in pharma, food, and drinking water segments still favor vendors with GMP documentation and IEC 62443 compliance, insulating premium brands in high-stakes applications. Multinationals respond by localizing assembly and emphasizing total cost-of-ownership savings from lower chemical consumption and predictive maintenance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Peristaltic Pumps Challenge Diaphragm Dominance

Diaphragm models controlled 41.3% of 2025 revenue, anchored in high-pressure chemical injection where API 675 conformity and PTFE diaphragms assure long service life. Yet peristaltic units are expanding at 6.8% CAGR through 2031 as utilities seek dry-run capability and 10-minute hose swaps that minimize downtime. A U.K. water utility eliminated vapor-locking in sodium-hypochlorite dosing after switching to peristaltic technology, trimming maintenance call-outs by two-thirds. In high-purity biotech filling, single-wear-part designs also lower cross-contamination risk. Piston and plunger pumps keep their stronghold in reverse-osmosis antiscalant and refinery catalyst dosing above 16 bar, where ceramic plungers and packed heads withstand abrasive fluids at elevated pressure. Specialty rotary designs, such as gear and screw pumps, occupy niche adhesive and resin duties but lack the growth momentum seen in peristaltic offerings.

By Application: Pharma & Biotech Lead Growth Curve

Water and wastewater projects represent 33.9% of the 2025 value and remain the largest single application, driven by the EU’s 30,354-plant retrofit program and U.S. State Revolving Fund grants. However, pharmaceutical and biotech facilities are forecast to post a 7.1% CAGR to 2031, the fastest among all segments. Continuous-flow reactors and single-use technologies demand dosing precision within ±1%, creating a pull for low-pulse pumps with electronic batch records. Oil & gas chemical injection rises on the back of new Middle-Eastern and Asian refineries, while food-and-beverage plants adopt hygienic peristaltic pumps for CIP-friendly ingredient metering. Power-generation, pulp, and mining uses add incremental but less dynamic demand.

By End-User Facility: Residential & Municipal Utilities Narrow the Gap

Industrial sites accounted for 69.4% of the dosing pumps market share in 2025, but residential and municipal utilities are projected to increase their slice of the dosing pumps market size at a 6.6% CAGR between 2026 and 2031. The revised EU Urban Wastewater Treatment Directive now covers plants serving as few as 1,000 population equivalents, compelling 30,354 facilities to invest in tertiary and quaternary nutrient-removal systems that rely on chemical-feed skids with integrated, cyber-secure controllers. In the United States, FY 2025 State Revolving Fund allocations deliver USD 5.2 billion in grants and low-interest loans, accelerating lead-service-line replacements, PFAS mitigation, and phosphorus-control retrofits that each specify precise metering equipment. India’s INR 56,100 crore (USD 6.7 billion) wastewater-infrastructure grants for 2026-2031 target cities of 1-4 million residents, where treatment coverage lags below 37.5%, unlocking thousands of new dosing points for coagulation, pH adjustment, and disinfection. Smaller utilities prefer packaged skids that arrive factory-tested with smart sensors, remote-monitoring dashboards, and auto-calibration routines, minimizing their dependence on scarce in-house technicians. Vendors that bundle pumps, controls, cloud analytics, and multi-year service contracts are therefore gaining traction, especially when they document IEC 62443 compliance to satisfy emerging cybersecurity audits.

Commercial buildings, including hospitals, hotels, and office complexes, add secondary growth by installing automated dosing systems for HVAC cooling-tower treatment, boiler feedwater conditioning, and on-site wastewater pretreatment, particularly in regions adopting green-building standards. Skilled-labor shortages remain a headwind: 38% of municipal operators worldwide lacked adequate training in automated chemical-control systems as of 2023, a gap suppliers address with color-touch HMIs, QR-coded maintenance guides, and subscription-based remote diagnostics. Across all non-industrial facilities, smart dosing upgrades have demonstrated chemical-use reductions of up to 18% and unplanned-maintenance cuts of 13%, a total-cost-of-ownership narrative that resonates with budget-constrained public buyers.

Geography Analysis

Asia-Pacific generated 40.8% of 2025 revenue, and the dosing pumps market size in the region is on track to expand at a 6.4% CAGR to 2031. India’s INR 56,100 crore wastewater-upgrade plan and refinery build-outs across China and the Gulf underpin long-term demand. North America and Europe form a replacement-driven landscape. The U.S. FY 2025 funding round allocates USD 5.2 billion to state revolving funds, accelerating lead-service-line replacement and PFAS treatment that each rely on precise chemical feed. Europe’s phosphorus-removal mandate stimulates multi-year dosing-skid orders, as seen in Yorkshire Water’s 90% phosphorus-reduction retrofit that exceeded national effluent quotas. South America and the Middle East & Africa show smaller baselines but attractive upside. Brazil’s deep-water projects and Oman’s USD 1.82 billion water-expansion program translate into chemical-injection and desalination dosing requirements, respectively.

Competitive Landscape

The dosing pumps market is moderately concentrated. Grundfos, IDEX, Xylem, Prominent, and Watson-Marlow combine manufacturing scale with digital-service portfolios. Grundfos’ 2025 acquisition of Newterra created a USD 350 million treatment unit that bundles pumps, controls, and packaged plants. Xylem’s USD 7.5 billion all-stock merger with Evoqua and its majority stake in Idrica integrate analytics that cut non-revenue water by up to 50% in pilot cities. Watson-Marlow opened a 14,000 m² cleanroom in Massachusetts to meet single-use bioprocess demand. Low-cost Chinese and Indian entrants keep commodity-segment margins thin, but stringent documentation and cybersecurity clauses shield premium vendors in regulated markets. Emerging software specialists retrofit legacy fleets with sensor kits and AI dosing optimization, capturing annuity-style service revenue without displacing hardware.

Dosing Pumps Industry Leaders

Grundfos Holding A/S

IDEX Corporation (Milton Roy, Pulsafeeder)

Prominent GmbH

SEKO S.p.A.

Watson-Marlow Fluid Technology (Spirax-Sarco)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: India’s Finance Commission endorsed INR 56,100 crore (USD 6.7 billion) of wastewater grants for 2026-2031, triggering a surge of municipal dosing-plant tenders.

- August 2025: Grundfos closed its acquisition of Newterra, expanding packaged treatment capabilities across Europe and North America.

- July 2025: OPEC released World Oil Outlook 2050, calling for 19.5 million b/d of new refining capacity, strengthening demand for high-pressure chemical-injection pumps.

- December 2024: Xylem acquired a majority stake in Idrica to embed data analytics into its Xylem Vue platform, doubling down on remote dosing optimization.

Global Dosing Pumps Market Report Scope

A dosing pump, also referred to as a metering pump, is a type of positive displacement pump engineered to deliver a specific, predetermined volume of liquid into a process or system at controlled intervals. Unlike standard transfer pumps, which emphasize bulk movement, dosing pumps prioritize precision, repeatability, and chemical compatibility.

The Dosing Pumps Market is segmented into product type, application, end-user facility, and geography. By product type, the market is segmented into diaphragm pumps, piston/plunger pumps, peristaltic pumps, and other product types. By application, the market is segmented into water and wastewater treatment, oil and gas, chemical processing, pharmaceuticals and biotech, food and beverages, power generation, and other applications. By end-user facility, the market is segmented into industrial, commercial, residential, and municipal utilities. The report also covers the market size and forecasts for the dosing pumps market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Diaphragm Pumps |

| Piston/Plunger Pumps |

| Peristaltic (Hose and Tube) Pumps |

| Others (Gear, Screw, etc.) |

| Water and Wastewater Treatment |

| Oil and Gas |

| Chemical Processing |

| Pharmaceuticals and Biotech |

| Food and Beverages |

| Power Generation |

| Others (Pulp and Paper, Mining) |

| Industrial |

| Commercial |

| Residential and Municipal Utilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Diaphragm Pumps | |

| Piston/Plunger Pumps | ||

| Peristaltic (Hose and Tube) Pumps | ||

| Others (Gear, Screw, etc.) | ||

| By Application | Water and Wastewater Treatment | |

| Oil and Gas | ||

| Chemical Processing | ||

| Pharmaceuticals and Biotech | ||

| Food and Beverages | ||

| Power Generation | ||

| Others (Pulp and Paper, Mining) | ||

| By End-User Facility | Industrial | |

| Commercial | ||

| Residential and Municipal Utilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the dosing pumps market expected to grow between 2026 and 2031?

The market is projected to expand at a 5.75% CAGR over the 2026-2031 period, reaching USD 6.36 billion by 2031.

Which segment is growing the quickest within dosing applications?

Pharmaceutical and biotech facilities show the highest momentum, advancing at a 7.1% CAGR as continuous-flow processes demand precise micro-dosing.

Why are peristaltic pumps gaining share against diaphragm models?

Peristaltic designs tolerate dry-run conditions, require only a hose change for maintenance, and deliver gentle, contamination-free flow, reducing downtime and lifecycle cost.

What regulations are driving pump upgrades in Europe?

The 2024 recast Urban Wastewater Treatment Directive lowers phosphorus limits to 0.5 mg/L and mandates 80% micropollutant removal, triggering widespread chemical-feed retrofits.

How are vendors addressing cybersecurity concerns in connected pumps?

Leading manufacturers now ship IEC 62443-compliant controllers with secure boot, signed firmware updates, and network-segmentation capabilities to prevent unauthorized dose changes.

Page last updated on: