Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.21 Billion |

| Market Size (2031) | USD 28.16 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Submersible Pumps Market Analysis by Mordor Intelligence

The Submersible Pumps Market size was valued at USD 15.59 billion in 2025 and estimated to grow from USD 17.21 billion in 2026 to reach USD 28.16 billion by 2031, at a CAGR of 10.36% during the forecast period (2026-2031).

Demand is scaling as utilities, energy companies, and construction firms prioritize energy-efficient equipment that performs reliably in harsh or flooded settings. Deeper well exploitation, large-scale flood-control programs, and rapid electrification of agricultural irrigation are reshaping procurement strategies, while smart monitoring tools are lowering lifetime operating costs and reinforcing the value proposition of premium systems. Competitive intensity remains moderate because globally diversified manufacturers and regional specialists now race to pair hydraulics expertise with digital diagnostics and renewable-ready powertrains. Supply-chain pressure on permanent-magnet motors and a shortage of advanced down-hole technicians raise execution risks, but they also open opportunities for modular motor platforms, automation, and local assembly partnerships.

Key Report Takeaways

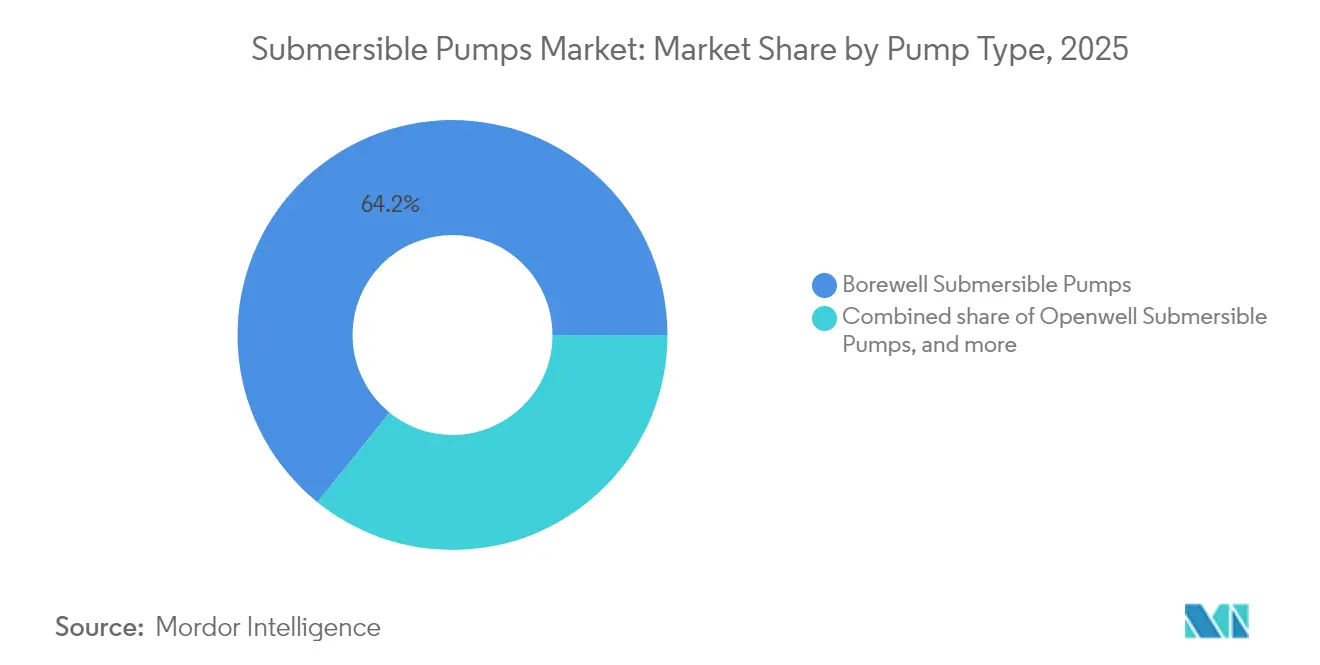

- By pump type, borewell units led with 64.18% revenue share in 2025; non-clog sewage pumps are forecast to expand at a 10.62% CAGR to 2031.

- By drive type, electric systems captured 77.65% of the submersible pump market share in 2025, while the same segment is expected to grow at a 10.89% CAGR through 2031.

- By head rating, above 100 m products accounted for 69.25% of the submersible pump market size in 2025 and are advancing at a 10.5% CAGR through 2031.

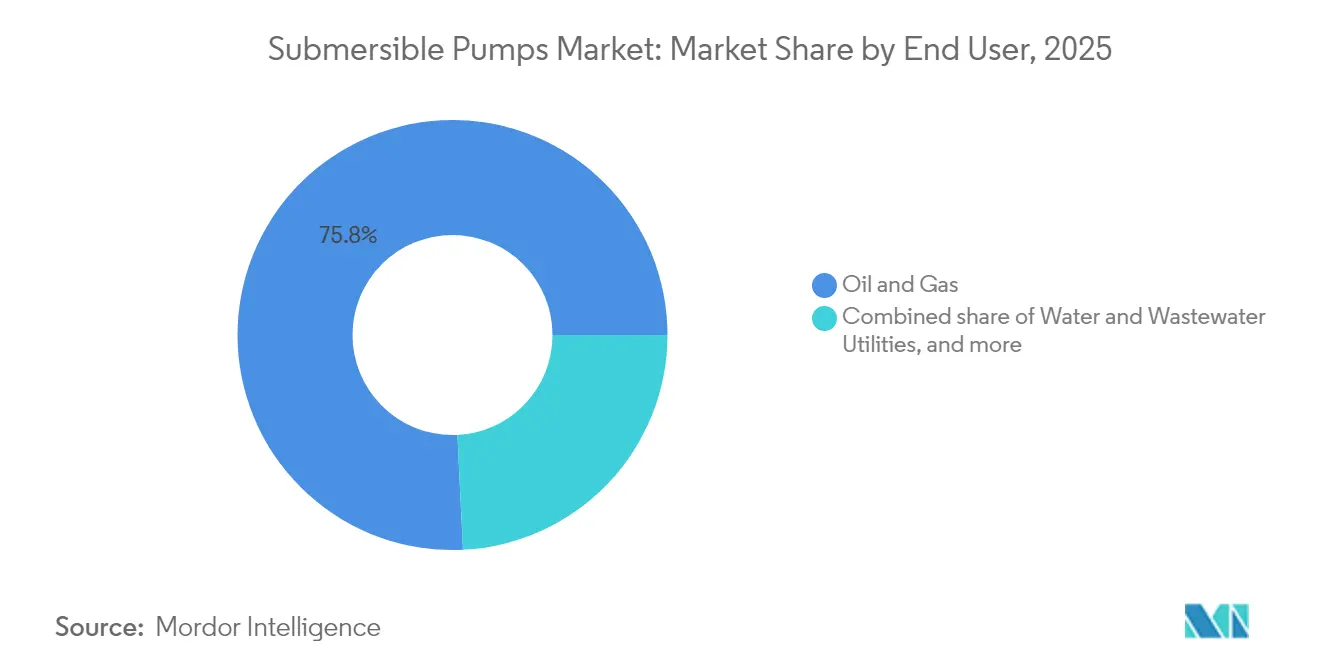

- By end user, oil and gas applications commanded 75.78% of demand in 2025, whereas water and wastewater utilities are recording the fastest projected CAGR at 11.05% through 2031.

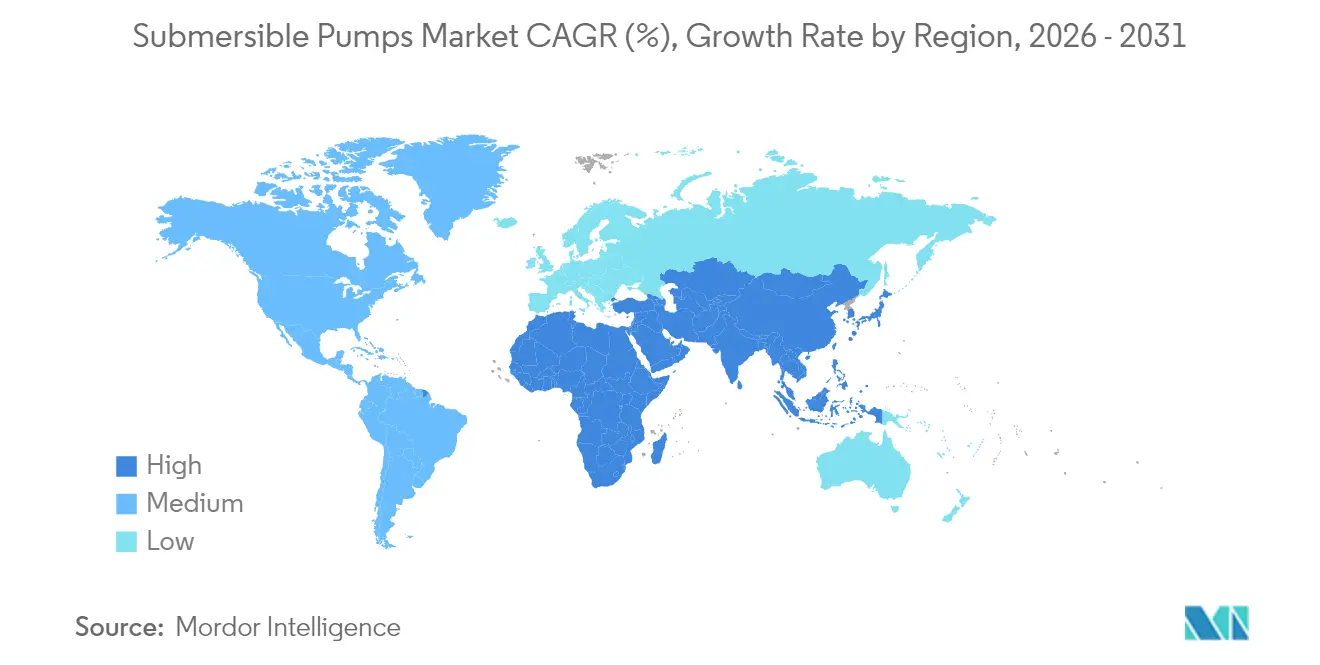

- By geography, Asia-Pacific dominates with 39.62% submersible pump market share in 2025 and is projected to expand at an 11.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Submersible Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery in oil & gas brown-field projects | +2.1% | Global, concentrated in North America, Middle East | Medium term (2-4 years) |

| Global construction boom & dewatering needs | +1.8% | APAC core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Climate-driven flood-control investments | +1.5% | Global, with early gains in UK, Netherlands, NYC | Medium term (2-4 years) |

| Rising municipal water-&-wastewater CAPEX | +1.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Electrification of African irrigation via solar pumps | +1.2% | Sub-Saharan Africa, expanding to South Asia | Long term (≥ 4 years) |

| AI-enabled predictive maintenance lowering OPEX | +0.8% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recovery in oil & gas brown-field projects

Brownfield optimization reshapes artificial-lift economics as operators redeploy capital toward mature wells requiring high-lift electric submersible pump (ESP) systems [1]Baker Hughes, “SOCAR Awards ESP Contract,” bakerhughes.com. A multi-year agreement to supply more than 150 ESP strings to Azerbaijan’s SOCAR illustrates how legacy reservoirs now depend on modern ESP technology to offset declining pressures and rising water cuts. SLB’s compact wide-range ESP series pursues similar goals, enabling deeper production zones while minimizing completion footprints. Subsea boosting contracts for projects such as BP’s Kaskida field further confirm that ESPs remain essential even when industry drilling budgets flatten, because maximizing recovery from existing assets protects cash flow and reduces exploration risk.

Global Construction Boom & Dewatering Needs

Accelerated infrastructure, tunneling, and underground transit programs boost demand for reliable site-dewatering pumps running continuously in abrasive conditions. The USD 1.1 billion Kensico-Eastview Connection Tunnel in New York requires high-capacity drainage systems to keep excavation dry. Manufacturers like Sulzer have expanded ranges, including portable site-drainage units and heavy-duty tunnel pumps, pairing rugged impeller materials with smart sensors to prevent unexpected downtime. Asia-Pacific civil works, pipelines, and mining exploration add additional momentum.

Climate-driven Flood-control Investments

More frequent extreme-rainfall events force municipalities to build large pump stations and mobile fleets that manage peak inflows. The UK budgeted GBP 2.65 billion for over 1,000 flood schemes requiring multiple high-throughput submersible pumps. New York City’s Bushwick sewer upgrade plans to lift capacity almost ninefold to 1.9 billion gallons per day, underscoring the scale of equipment required. Flowserve’s concrete-volute and vertical wet-pit pumps exceed 200,000 m³/h, setting new benchmarks for urban flood resilience.

Rising Municipal Water & Wastewater CAPEX

Regulatory mandates and aging assets drive North American and European utilities to spend hundreds of billions of dollars on pump replacement and treatment capacity expansion. The US Environmental Protection Agency projects more than USD 1 trillion in needed water infrastructure spending over two decades. San Francisco’s USD 4.8 billion Water System Improvement Program includes deep-well retrofits and variable-frequency drives that cut power draw and enable predictive maintenance. Nearly every surveyed operator plans to maintain or increase capital budgets in 2025, accelerating demand for connected and energy-efficient submersible systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High life-cycle energy costs vs. surface pumps | -1.4% | Global, particularly in energy-intensive applications | Long term (≥ 4 years) |

| Shortage of skilled down-hole service labor | -0.9% | North America, Middle East, offshore regions | Medium term (2-4 years) |

| Volatile rare-earth prices hitting PM motor BOM | -1.1% | Global, concentrated in high-performance applications | Short term (≤ 2 years) |

| Remote-area grid power-quality issues causing failures | -0.7% | Rural areas in developing markets, mining regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High life-cycle energy costs vs. surface pumps

Energy-intensive users often favor surface alternatives when shallow lift depths allow similar hydraulic performance at lower kilowatt-hours. Comparative ownership studies show submersible pump efficiency improves markedly only when paired with premium motors and variable-frequency drives such as Franklin Electric’s SubDrive series [2]Franklin Electric, “SubDrive Constant Pressure Systems,” franklin-electric.com. Manufacturers continue to refine impellers and insulation classes, yet inherent cooling losses impose an energy penalty in certain shallow settings.

Shortage of skilled down-hole service labor

Advanced ESP installations require technicians capable of handling high-voltage cables, fiber-optic sensors, and pressure-balanced seals. Talent pipelines have thinned as experienced workers retire faster than replacements are certified. Baker Hughes is responding with retrievable systems that minimize rig time and remote diagnostics that cut on-site visits. Automation alleviates some strain but does not fully substitute for field experience, making service capacity a gating factor in regions with accelerating artificial-lift projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Borewell leadership underpins irrigation expansion

Borewell units delivered 64.18% of 2025 revenue and are projected to log a 10.58% CAGR as acreage under electric or solar-assisted irrigation rises in India, China, and parts of Africa. The submersible pump market size for borewell applications is forecast to widen sharply because governments are issuing subsidies that defray initial hardware costs and incentivize farmers to swap diesel sets for efficient electric drives. Deep-well ESP systems occupy the premium tier, serving production rates above 150,000 barrels per day in oilfields with temperatures up to 250 °C. Urban growth supports non-clog sewage models, while open-well pumps remain viable where shallow aquifers enable simplified installations.

Growth momentum hinges on solar integration, with national schemes such as India’s PM-KUSUM awarding bulk orders for photovoltaic pump kits that cut electricity bills and reduce grid peak loads. Suppliers that combine corrosion-resistant metallurgy with maximum power-point tracking controllers stand to reinforce recurring revenue through replacement impellers and electronics upgrades. Conversely, inexpensive imports into price-sensitive farm markets heighten margin pressure for domestic fabricators.

By Drive Type: Electric dominance benefits from grid quality

Electric drives secured 77.65% market share in 2025 and are expanding at 10.89% CAGR as transmission upgrades improve voltage stability across emerging economies. Solar-ready inverters increasingly ship as standard, allowing the same motor to run on daytime photovoltaic arrays and night-time utility supply. Hydraulic drives persist in offshore and remote mineral projects where central power generation is impractical, but their lifecycle costs remain higher due to auxiliary equipment.

Innovations in permanent-magnet motors, active cooling jackets, and silicon-carbide power modules lift overall efficiency, mitigating one of the key restraints facing the submersible pump market. Short-term risks arise from rare-earth price swings that disrupt magnet supply; this is directing R&D toward ferrite or synchronous reluctance alternatives. Suppliers certifying products for low harmonic distortion also capture share in mining camps reliant on generator sets that exhibit uneven waveforms.

By Head Rating: Deep-lift systems command premium pricing

Pumps rated for heads above 100 m accounted for 69.25% of 2025 revenue and will post a 10.5% CAGR because oilfields, skyscrapers, and deep municipal wells all demand high differential pressures. The submersible pump market size at this head range grows faster than lower ranges because unit prices climb sharply with horsepower, metallurgy, and sensor options.

Engineering advances like multi-stage diffuser stacks and down-thrust compliant bearings extend run hours between pull-outs. Compact permanent-magnet motors reduce outside diameter so operators can fit larger flow stages within the same casing. Mid-range 50-100 m products target booster stations and small industrial parks, while sub-50 m centrifugal wet ends dominate private residential boreholes where a low purchase cost outweighs longevity.

By End User: Utilities begin to close gap with petroleum sector

Oil and gas held 75.78% of demand in 2025, yet water and wastewater utilities exhibit an 11.05% CAGR as federal grants flow into pipe renewal and flood-mitigation projects. Municipalities increasingly deploy online vibration and insulation monitoring that alerts crews before seal failures release effluent. Mining and construction represent steady niche revenues where dewatering remains mission-critical during excavation.

Thanks to solar pump kits that now approach grid parity in many sun-rich geographies, agricultural irrigation is the second-fastest rising use case. Farmers gravitate toward deeper borewell configurations as water tables decline, sustaining aftermarket demand for bowls, shafts, and thrust washers. Meanwhile, flood-control stations purchase very large axial-flow submersible propeller pumps, a specialized product family that only a handful of global OEMs currently build

Geography Analysis

Asia-Pacific contributed 39.62% of 2025 revenue and is tracking an 11.44% CAGR through 2031. China’s push to modernize rural water supply and India’s subsidy-backed irrigation electrification combine with Indonesia’s metro-rail expansion to keep tender volumes high. Regional suppliers such as Shakti Pumps and Kirloskar Brothers leverage cost-competitive casting capacity and local warranty networks, while multinationals source control electronics from regional contract manufacturers to reduce lead times.

North America remains a volume hub for high-horsepower ESP strings used in tight-oil basins, though a labor shortage of certified cable-splice and pull-crew technicians tempers installation pace. Substantial water infrastructure appropriations under the Infrastructure Investment and Jobs Act steer municipal bid specifications toward premium efficiency ratings and predictive-maintenance gateways. Canada’s remote mining districts adopt hybrid solar-diesel microgrids where variable-speed submersible pumps smooth station load profiles.

Europe prioritizes climate resilience and puts strict energy-efficiency labels on public procurement. The United Kingdom’s GBP 2.65 billion flood program adds a sizable project pipeline for high‐capacity stormwater stations. Germany, France, and the Benelux region deploy variable-speed borehole pumps in district heating and groundwater source-heat-pump loops, a market niche that values corrosion-resistant stainless alloys. Scandinavia’s focus on circularity drives refurbishment contracts over full replacements, favoring modular pump designs.

The Middle East invests in seawater desalination, where submersible turbine pumps withstand brine abrasion; a EUR 508 million plant in Taiwan secured SUEZ equipment orders that include corrosion-proof wet ends . African governments scale solar irrigation to curb diesel imports, while South America’s pre-salt fields award subsea boost systems that rely on long-step-out ESP modules rated for chemical exposure to CO₂-rich fluids.

Competitive Landscape

Competition is moderate because the five largest suppliers combine broad technology portfolios with installed-base service revenues, yet regional manufacturers successfully defend share in lower-price agricultural and building-services segments. Baker Hughes, SLB, and Grundfos lead R&D intensity, funneling capital toward digital twins, fiber-optic telemetry, and composite material research. Grundfos’ acquisition of Culligan’s European commercial unit tightens vertical integration into water treatment skids that ship with factory-programmed submersible pumps [4]Grundfos, “Acquisition of Culligan C&I Business,” grundfos.com.

Regional champions like Kirloskar Brothers and CRI Pumps secure government tenders by offering energy audits and on-site field service fleets. Shakti Pumps’ expansion into solar-ready controllers exemplifies how agile firms fill product gaps that global giants address more slowly. White-space entrants develop analytics platforms that layer machine learning onto vibration and insulation data, selling subscription services that boost mean-time-between-failure.

Strategic alliances revolve around electrification and lower emissions. Baker Hughes’ launch of all-electric cementing units and interval control valves illustrates the move toward integrated surface-and-subsurface electrification ecosystems. SLB’s planned acquisition of ChampionX adds specialty chemicals that extend ESP run life by mitigating scale and corrosion. Capital allocation patterns indicate sustained investment in automating diagnostics and precertifying components for hydrogen and ammonia compatibility.

Submersible Pumps Industry Leaders

Grundfos Holding A/S

Xylem Inc.

Sulzer AG

Flowserve Corporation

Baker Hughes Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The UK committed GBP 2.65 billion for more than 1,000 flood-protection schemes, driving procurement of very large stormwater pumps.

- February 2025: SLB obtained antitrust clearance to close its ChampionX acquisition by early Q2 2025, strengthening its artificial-lift portfolio.

- October 2024: Frontier-Kemper Constructors secured a USD 1.1 billion contract for New York’s Kensico-Eastview Connection Tunnel, specifying high-capacity dewatering pumps

- March 2024: INTECH secured a project from a major oil company in the Middle East to automate power supply skids for electric submersible pump (ESP) applications. As part of the agreement, INTECH will automate over 10 ESP power skids.

Global Submersible Pumps Market Report Scope

A submersible pump is a type of pump that is an air-tight sealed motor close-coupled to the pump body. The main advantage of a submersible pump is that a problem associated with a high elevation difference between the pump and fluid surface prevents pump cavitation. This type of pump never requires priming because the whole assembly is submerged in the fluid.

The submersible pumps market is segmented by type, drive type, head, end-use and geography. By type, the market is segmented into borewell submersible pump, open-well submersible pump, and non-clog submersible pump. By drive type, the market is segmented into electric, hydraulic, and other drive types. By head, the market is segmented into below 50 m, between 50 m to 100 m, and above 100 m. By end user, the market is segmented into water and wastewater, oil and gas industry, mining and construction industry, and other end users. The report also covers the market size and forecasts for the submersible pumps market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Pump Type

| Borewell Submersible Pumps |

| Openwell Submersible Pumps |

| Non-clog/Sewage Submersible Pumps |

| Deep-well Electric Submersible Pumps (ESPs) |

| Submersible Turbine Pumps |

By Drive Type

| Electric |

| Hydraulic |

| Solar-powered |

By Head Rating

| Below 50 m |

| 50 to 100 m |

| Above 100 m |

By End User

| Water and Wastewater Utilities |

| Oil and Gas (Artificial-Lift) |

| Mining and Construction Dewatering |

| Agriculture and Irrigation |

| Municipal Flood Control |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Pump Type | Borewell Submersible Pumps | |

| Openwell Submersible Pumps | ||

| Non-clog/Sewage Submersible Pumps | ||

| Deep-well Electric Submersible Pumps (ESPs) | ||

| Submersible Turbine Pumps | ||

| By Drive Type | Electric | |

| Hydraulic | ||

| Solar-powered | ||

| By Head Rating | Below 50 m | |

| 50 to 100 m | ||

| Above 100 m | ||

| By End User | Water and Wastewater Utilities | |

| Oil and Gas (Artificial-Lift) | ||

| Mining and Construction Dewatering | ||

| Agriculture and Irrigation | ||

| Municipal Flood Control | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the submersible pump market?

The market stands at USD 17.21 billion in 2026 and is projected to reach USD 28.16 billion by 2031.

Which segment is growing fastest within the submersible pump market?

Water and wastewater utilities are expanding at an 11.05% CAGR, outpacing other end-user groups.

Why are electric drive systems so dominant?

Electric drives hold a 77.65% share because grid reliability, renewable power integration and variable-speed electronics lower operating costs relative to hydraulic or diesel alternatives.

How will flood-control spending influence demand?

Climate-driven investments such as the UK’s GBP 2.65 billion program require high-capacity pumps, boosting orders for large axial-flow models over the forecast horizon.

Which region offers the highest growth potential?

Asia-Pacific leads with a 39.62% share and an 11.44% CAGR due to accelerating urban infrastructure and irrigation electrification projects.

What restraints could slow market expansion?

Elevated life-cycle energy costs for shallow lifts and shortages of skilled down-hole technicians may curb uptake unless efficiency improvements and automation close the gap.

Page last updated on: