Distribution Voltage Regulator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.56 Billion |

| Market Size (2031) | USD 3.29 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Distribution Voltage Regulator Market Analysis by Mordor Intelligence

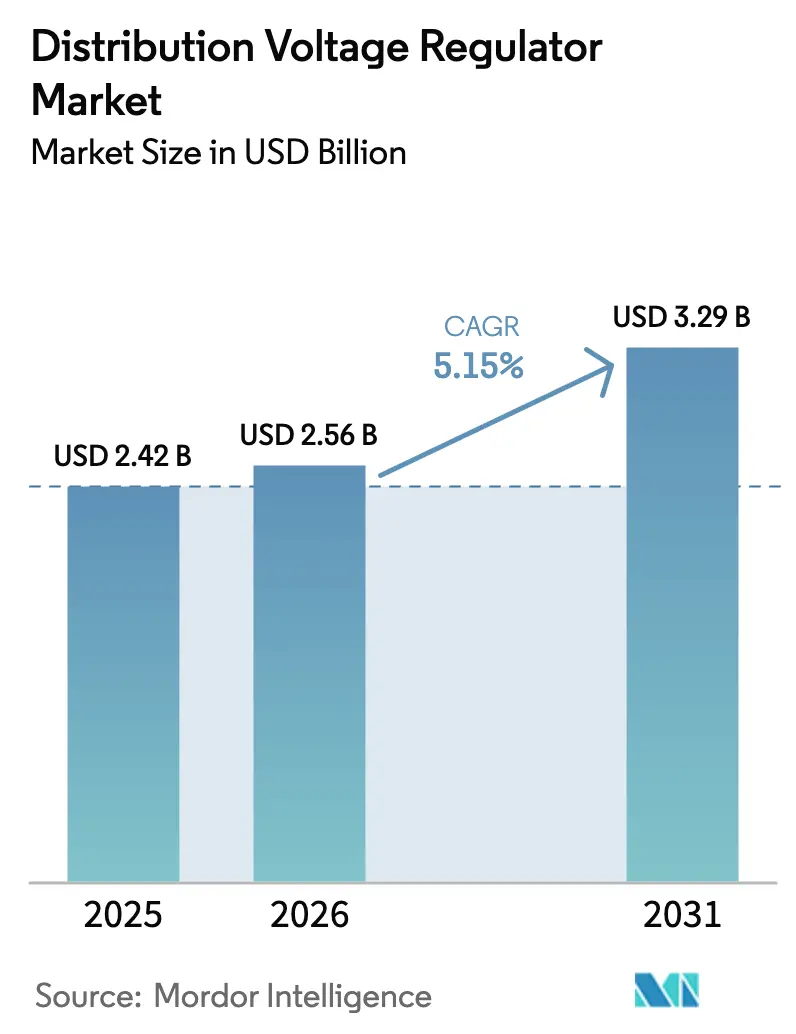

The Distribution Voltage Regulator Market size is expected to increase from USD 2.42 billion in 2025 to USD 2.56 billion in 2026 and reach USD 3.29 billion by 2031, growing at a CAGR of 5.15% over 2026-2031.

A structural pivot is underway as grid operators replace reactive asset management with predictive voltage control to absorb hyperscale data-center clusters, EV fast-charging hubs, and gigawatt-scale renewable additions. Asia-Pacific drives both scale and momentum, powered by China’s State Grid modernization and India’s Central Electricity Authority mandates, while high-voltage (over 40 kV) units emerge as a premium niche because offshore-wind HVDC links require voltage support at transmission–distribution interfaces.[1]ISO New England, “2025 Regional System Plan,” iso-ne.com Automatic and smart regulators dominate new builds as utilities embed SCADA-ready devices that execute millisecond tap changes and stream diagnostics to cloud ADMS platforms.[2]Eaton, “Eaton begins production at newly expanded Texas manufacturing facility,” eaton.com Converging cybersecurity and domestic-content rules are tilting procurement toward suppliers with regional manufacturing footprints, evidenced by recent capacity additions in Texas and Tennessee. Simultaneously, copper at USD 12,758 per ton and silicon-carbide supply swings are squeezing margins, pushing vendors toward hybrid STATCOM-regulator skids that consolidate reactive compensation and voltage adjustment in one enclosure.[3]KME, “Metal Prices,” kme.com

Key Report Takeaways

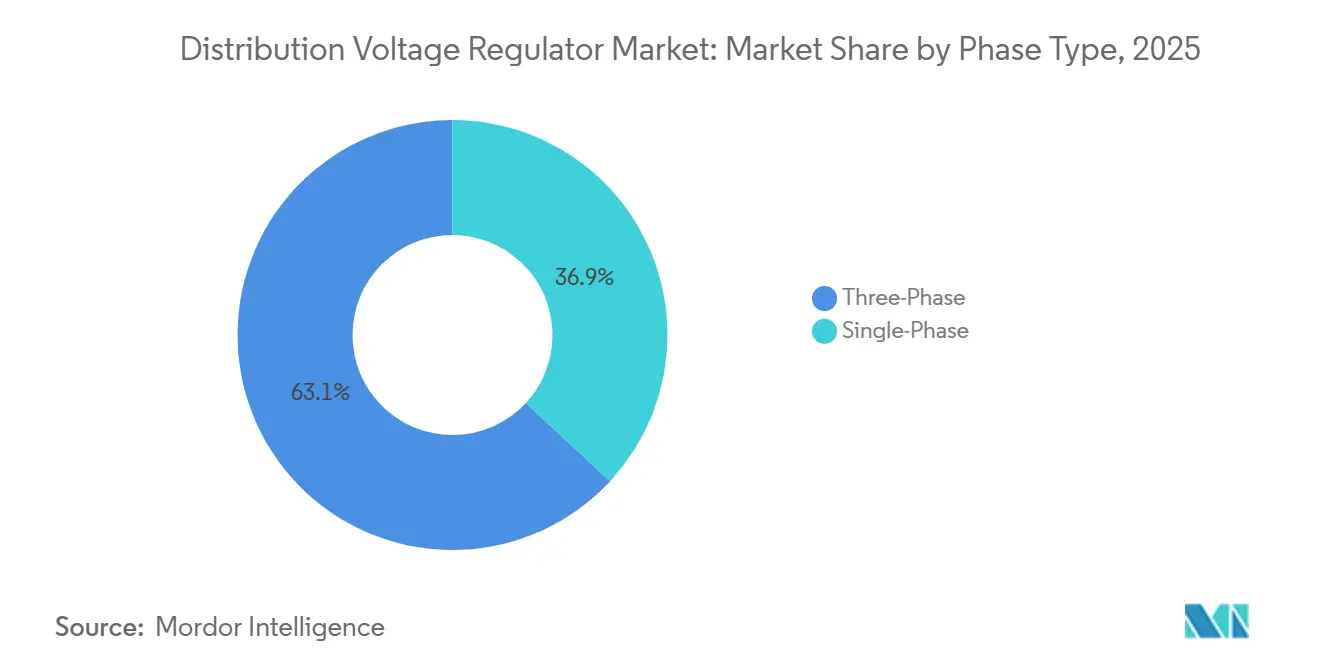

- By phase type, three-phase regulators held 63.1% of the distribution voltage regulator market share in 2025, while single-phase units are projected to advance at a 7.2% CAGR through 2031.

- By mounting, pole-mounted units represented 54.5% of 2025 deployments, but substation-mounted installations are set to expand at a 7.6% CAGR, reflecting a shift toward centralized, cyber-secure voltage control.

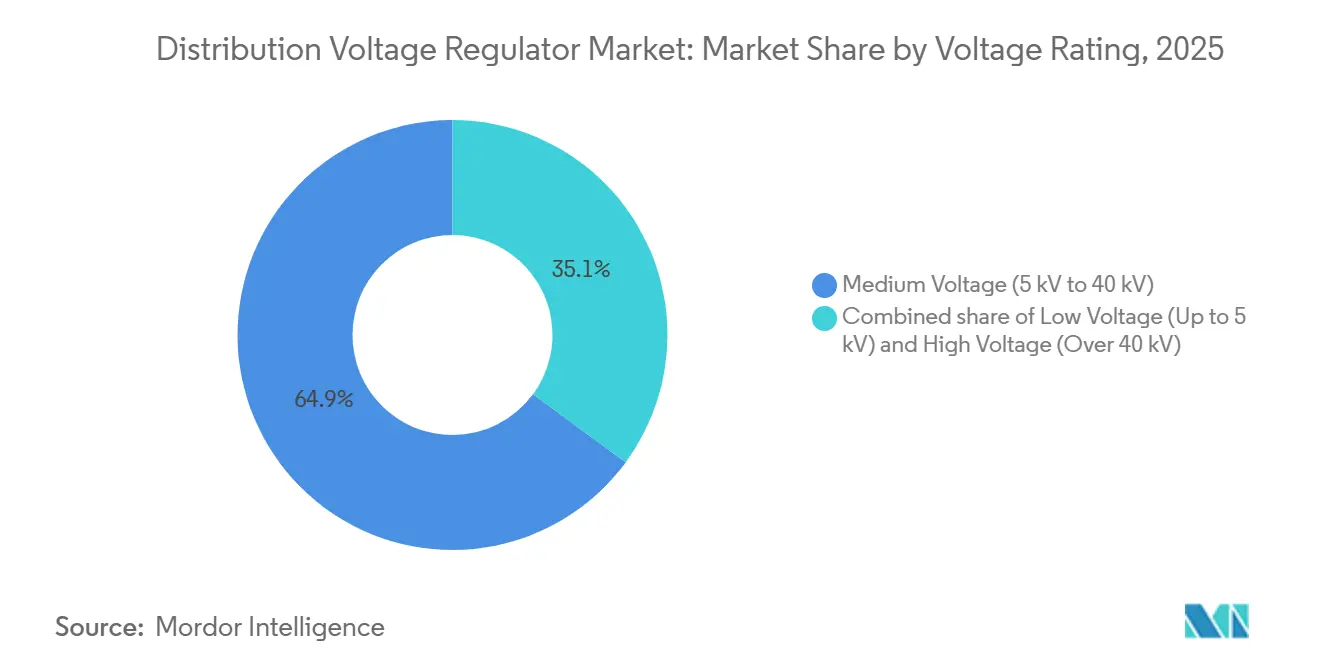

- By voltage rating, medium-voltage devices retained 64.9% of the distribution voltage regulator market size in 2025, yet high-voltage regulators are forecast to grow fastest at a 7.9% CAGR on the back of offshore-wind interconnections.

- By control type, automatic and smart regulators captured 65.3% share in 2025 and are poised for a 5.7% CAGR through 2031 as utilities pivot toward firmware-defined functionality.

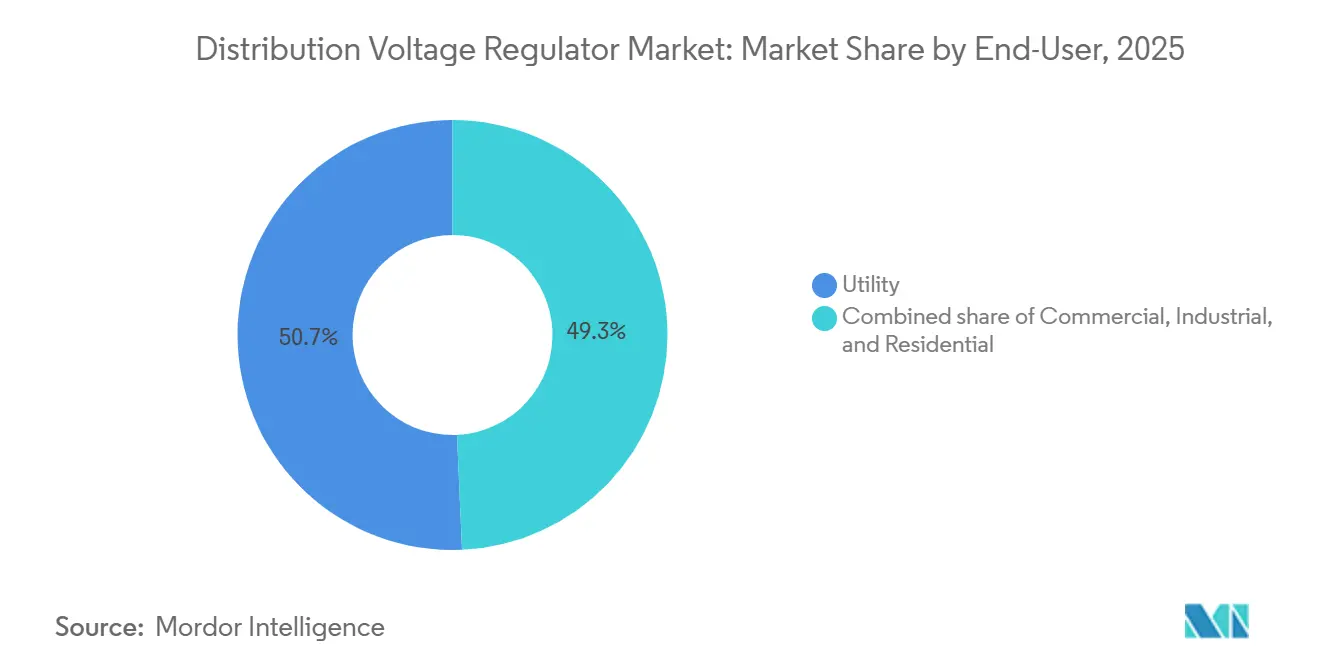

- By end-user, utilities accounted for 50.7% of 2025 demand, expanding at a 5.9% CAGR as feeder automation budgets rise under DER ride-through mandates.

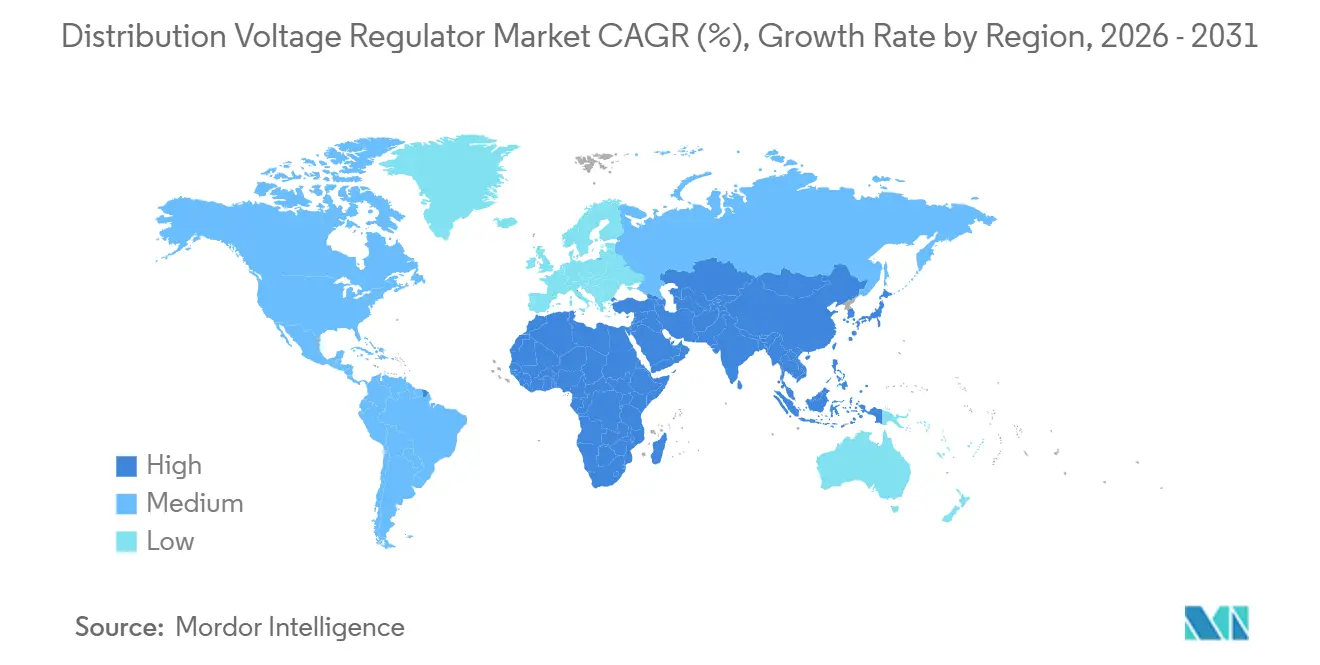

- By geography, Asia-Pacific commanded 43.0% of 2025 revenue and is projected to maintain leadership with a 5.7% CAGR driven by China and India's grid-modernization programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Distribution Voltage Regulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-grid build-out & feeder automation | +1.2% | North America, Europe, China | Medium term (2-4 years) |

| Renewable-penetration pressure | +1.4% | Europe (offshore wind), Asia-Pacific (solar), North America (utility PV) | Long term (≥ 4 years) |

| Power-quality demand from data centers | +0.9% | U.S., Ireland, Netherlands, Singapore, India | Short term (≤ 2 years) |

| Rise of EV fast-charging hubs | +0.7% | North America, Europe, China | Medium term (2-4 years) |

| AI-optimized self-healing feeders | +0.5% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Emerging DER ride-through mandates | +0.6% | India, ASEAN, Brazil, Chile, Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart-grid Build-out & Feeder Automation

Utilities are migrating from time-based tap schedules to real-time, SCADA-driven adjustments that align voltage setpoints with cloud load forecasts, DER output, and weather models.[4]ISO New England, “2025 Regional System Plan,” iso-ne.com ISO New England earmarked USD 11.4 billion for asset-condition projects, including STATCOMs and advanced regulators that mitigate inverter-driven volatility. Alberta’s Electric System Operator has tendered 692–834 MW of fast frequency response, opening parallel demand for substation-mounted regulators in weak-grid zones. Georgia Power forecasts 2,065 MW of battery storage by 2031, pairing smart regulators with storage dispatch algorithms. The transition from electromechanical to microprocessor-based tap changers shortens replacement cycles because legacy units lack DNP3 and IEC 61850 interfaces.

Renewable-Penetration Pressure on Distribution Networks

High solar and wind penetration is forcing regulators to perform 10–20 tap changes daily, accelerating mechanical fatigue and driving adoption of solid-state designs with no moving parts. India’s Khavda Phase-IV project leverages 765 kV switchgear and shunt reactors that complement high-voltage regulators for gigawatt-scale renewables. Offshore wind export cables funnel fluctuating power onto weak coastal feeders, spurring demand for above 40 kV regulators integrated into HVDC converter yards. Field trials with RWE AG in Germany confirmed that ABB’s new line regulator curbs rooftop-solar voltage spikes by ±10% within two seconds. Europe’s 50Hertz awarded GE Vernova the 2 GW Ostwind 4 HVDC link, signaling a move toward converter-integrated regulation that compresses balance-of-plant footprints.

Power-quality Demand from Hyperscale Data Centers

Hyperscale campuses cap voltage excursions at ±1% to avoid server shutdowns and GPU throttling during AI training bursts. Reinhausen’s Tennessee plant will ship ETOS MD-IV regulators offering sub-cycle response tailored for 200 MW clusters. Alberta’s Transmission-Connected Data Center code restricts ramp rates and fault ride-through, pushing operators to finance on-site regulators rather than depend solely on the utility. Eaton’s Nacogdoches facility began shipping three-phase regulators to Oncor in October 2025, shrinking lead times for Texas data-center feeders. This bifurcates demand: utilities buy pole-mounted units for bulk feeders, while cloud providers specify substation regulators with redundant control paths and cybersecurity hardening.

Rise of EV Fast-charging Hubs Requiring Dynamic Voltage Control

Fast chargers drawing ≥350 kW induce voltage dips that spread along feeders, compelling regulators to shift taps in seconds to protect adjacent loads. ISO-NE forecasts net energy use climbing from 117,262 GWh in 2025 to 130,665 GWh by 2034 as winter peaks rival summer loads. Georgia Power schedules 500 MW of storage RFPs to smooth EV peaks, integrating battery-linked regulators at substations. Machine-learning models embedded in smart regulators parse traffic and weather data to anticipate charging surges, but utilities still lack feeder-end voltage telemetry, limiting predictive accuracy. Vendors are embedding edge analytics and 5G modems to close that visibility gap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front capex vs alternative devices | –0.8% | India, Southeast Asia, Africa | Short term (≤ 2 years) |

| Copper & power-semiconductor volatility | –0.6% | North America, Europe | Medium term (2-4 years) |

| Cybersecurity certification burden | –0.4% | North America, Europe, Australia | Medium term (2-4 years) |

| Shift to hybrid STATCOM-regulator platforms | –0.5% | Europe, North America, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-front Capex Versus Alternative Power-quality Devices

Cost-sensitive utilities in Asia, Africa, and Latin America prefer capacitor banks priced at USD 30,000–50,000 over smart regulators costing USD 80,000–120,000 despite lower precision. ISO-NE’s asset-condition backlog illustrates capital shifting toward transmission, while Georgia Power diverts funds to coal-to-gas conversions for EPA compliance. Where tariff structures do not reward voltage quality, regulators face slower payback than reactive-only devices. Vendors are countering with leasing models and performance-based contracts, but uptake remains slow.

Copper & Power-Semiconductor Supply-Chain Volatility

Copper at USD 12,758 per ton lifts material costs for windings that form up to 50% of a regulator BOM. Silicon-carbide overcapacity pushed device-line utilization to 70 % in 2025, delaying next-gen solid-state regulator launches until 2027–2028. Redesigns triggered by DDR4 shortages add 6–9 months to control-board schedules. Export-control skirmishes between the Netherlands and China fracture single-source supply chains, prompting utilities to demand multi-vendor qualification, which fragments component volumes and erodes scale economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase Type: Single-phase Gains on Rural Solar

Single-phase units cornered 36.9% of the distribution voltage regulator market size in 2025 and will log a 7.2% CAGR to 2031 as rural electrification and rooftop solar overload unbalanced feeders. Programs in India and ASEAN finance single-phase laterals that serve dispersed houses and farms, while U.S. cooperatives retrofit suburban feeders where PV backfeed raises phase-to-neutral voltages. Manufacturers respond with modular 250 kVA line regulators and ganged banks that allow utilities to add capacity per conductor, easing capex phasing.

Three-phase regulators retained 63.1% distribution voltage regulator market share in 2025, underpinning industrial parks, data centers, and utility substations that require phase balance. Georgia Power’s nuclear uprates and combustion-turbine additions rely on three-phase regulators for generator interconnections. Yet even in these applications, vendors now offer split-core designs enabling hot-swap maintenance, acknowledging operators’ intolerance for downtime during AI-era computing peaks.

By Mounting: Substation Installations Accelerate

Substation-mounted units accounted for 30.5% of 2025 deployments but will outpace other formats with a 7.6% CAGR as utilities centralize cybersecurity compliance and maintenance. Alberta’s Medicine Hat strength project illustrates the trend: regulators and synchronous condensers co-located at grid nodes for rapid fault support. Data-center campuses prefer substation units with redundant controllers to meet ±1% voltage windows.

Pole-mounted regulators still dominate numerical shipments because overhead feeders remain ubiquitous, but growth slips below 3% as aging wood poles raise wildfire risk and visual concerns escalate in suburbs. Pad-mounted formats serve underground networks; costs run 20–30% higher owing to sealed enclosures and ventilation, yet urban utilities accept the premium for aesthetics and pedestrian safety. Hitachi Energy’s compact pad regulator, fitting a secondary-substation footprint, seeks to unlock replacement demand where excavations are infeasible.

By Voltage Rating: High-voltage Segment Surges

High-voltage (over 40 kV) regulators represented 13.2% of 2025 revenue yet carry a 7.9% CAGR as offshore wind and inter-regional renewables push voltage control into HVDC yards. Germany’s Ostwind 4 and India’s 765 kV corridors typify projects where regulators must withstand elevated BIL ratings and coordinate with converter valves. Premium pricing per MVA is 1.5–2 times medium-voltage equivalents, improving vendor margins despite lower unit volumes.

Medium-voltage (5 to 40 kV) equipment remains the backbone, commanding 64.9% of 2025 revenue, serving 12 kV and 34.5 kV feeders common across North America and Europe. Low-voltage (up to 5 kV) devices inhabit a niche, gradually displaced by customer-sited UPS and power electronics. ABB’s ReliaHome Flex showcases the pivot toward behind-the-meter regulation, bundling EV chargers and water heaters under a 250 A controller.

By Control Type: Smart Regulators Dominate Growth

Automatic and smart devices claimed 65.3% of the 2025 volume and will broaden with a 5.7% CAGR as firmware-defined capabilities let utilities roll out features via over-the-air updates. GE Vernova’s GridBeats Device Management enables fleet-wide visibility, predictive diagnostics, and auto-provisioning, cutting O&M costs by up to 30%.

Conventional electromechanical units fade in developed grids but linger in low-capex regions lacking SCADA. Even there, vendors introduce plug-in communication cards to future-proof purchases. Software licensing models emerge, allowing utilities to unlock harmonic-filter or EV-forecast modules later, aligning expenses with benefit realization.

By End-user: Utilities Lead Amid DER Complexity

Utilities held 50.7% of 2025 shipments and will expand faster than commercial and industrial buyers as the distribution voltage regulator market growth tracks DER volatility. Asset-condition backlogs and renewable mandates drive the replacement of legacy regulators unable to communicate with ADMS platforms.

Commercial and industrial customers, notably data centers and semiconductor fabs, specify regulators with ±1% tolerances and redundant controls to shield mission-critical loads. Reinhausen’s ETOS MD-IV targets this segment with fiber-optic sensors and self-healing firmware. Residential penetration remains minimal, yet rooftop-solar feeders may trigger utility programs that subsidize customer-sited regulators as non-wire alternatives.

Geography Analysis

Asia-Pacific generated 43.0% of 2025 revenue and is forecast to retain leadership with a 5.7% CAGR as China’s State Grid ramps ultra-high-voltage AC/DC projects and India accelerates renewable corridors under its 500 GW non-fossil target. Domestic SiC device fabrication reaching volume scale in China mitigates semiconductor volatility for regional suppliers. ASEAN nations, especially Vietnam and Indonesia, adopt single-phase regulators to stabilize rural feeders, while Japan and South Korea pilot AI-driven self-healing feeders that demand microprocessor-based tap changers.

North America ranks second, buoyed by U.S. infrastructure spending and Canadian system-strength initiatives. Eaton’s USD 100 million Texas expansion doubled national capacity, aligning with domestic-content incentives under the Infrastructure Investment and Jobs Act. Alberta’s fast-frequency-response auctions integrate battery and regulator packages for weak-grid areas. Mexico’s progress is constrained by regulatory uncertainty, yet cross-border HVDC links drive sporadic high-voltage regulator orders.

Europe shows steady but slower expansion as IEC 62351 cybersecurity certification prolongs purchase cycles. GE Vernova’s Ostwind 4 underscores the continent’s tilt toward converter-integrated regulation. Germany’s “Networks of the Future” pilot with ABB validated ±10% voltage swings suppression on solar-heavy feeders ABB.COM. South America and the Middle East progress from smaller bases; Brazil’s ANEEL and Saudi Arabia’s regulators embed ride-through clauses that push utilities toward smart regulators, though copper price shocks slow purchase timing.

Competitive Landscape

The distribution voltage regulator market is moderately concentrated: ABB, Siemens, Eaton, GE Vernova, and Schneider Electric command roughly 55–60% combined share through integrated hardware-plus-software portfolios. ABB’s Electrification orders hit USD 4.5 billion in Q3 2025, buoyed by medium-voltage protection gear. Eaton’s and Reinhausen’s U.S. capacity buildups signal that localized factories now sway tender awards where utilities demand short lead times and trade-compliant steel.

Asian challengers TBEA, Daihen, and Toshiba leverage cost advantages to clinch Southeast Asian and Middle-Eastern bids but face hurdles in North America and Europe because of stringent cybersecurity audits. Hubbell’s USD 600 million acquisition of DMC Power widens its portfolio to include high-voltage connectors, enabling bundled offers for renewable interconnections.

Strategic white spaces revolve around hybrid STATCOM-regulator skids and software-defined functionality. GE Vernova’s collaboration with German TSOs on 525 kV DC breakers positions the firm at the interface of transmission and distribution. Hitachi Energy’s compact regulator shows how transformer-integrated designs unlock retrofit projects where space is limited. Niche players like G&W Electric and Beckwith Electric court municipal utilities needing rapid delivery and bespoke logic schemes.

Distribution Voltage Regulator Industry Leaders

ABB Ltd.

Schneider Electric SE

Siemens AG

Eaton Corporation plc

GE Grid Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: GE Vernova won a contract from Power Grid Corporation of India to refurbish the Chandrapur 2×500 MW HVDC link, upgrading converter valves and controls.

- October 2025: Eaton completed a USD 100 million expansion in Nacogdoches, Texas, doubling U.S. voltage-regulator output and shipping first units to Oncor.

- October 2025: Hubbell Incorporated finalized the USD 600 million acquisition of DMC Power, adding high-voltage connector technology.

- June 2025: Hitachi Energy introduced the Compact Line Voltage Regulator at CIRED 2025 for space-constrained retrofit projects.

Global Distribution Voltage Regulator Market Report Scope

The Distribution Voltage Regulator Market encompasses the global industry focused on the design, production, deployment, and maintenance of voltage regulation equipment. These devices are essential for stabilizing and maintaining consistent voltage levels within electrical distribution networks. Distribution voltage regulators automatically adjust voltage to safeguard distribution lines, ensure reliable power delivery, minimize technical losses, and support modern grid operations, particularly with the growing integration of distributed energy resources (DERs), rooftop solar installations, and electric vehicle (EV) charging demands.

The distribution voltage regulator market is segmented into phase type, mounting, voltage rating, control type, end-user, and geography. By phase type, the market is segmented into single-phase and three-phase. By mounting, the market is segmented into pole-mounted, pad-mounted, and substation-mounted. By voltage rating, the market is segmented into low voltage (Up to 5 kV), medium voltage (5 kV to 40 kV), and high voltage (Over 40 kV). By control type, the market is divided into automatic/smart regulators and conventional/electromechanical. By end-user, the market is segmented into commercial, residentials, industrial, and utility. The report also covers the market size and forecasts for the distribution voltage regulator market across each region. The market sizes and forecasts for the market are provided in terms of value (USD).

| Single-Phase |

| Three-Phase |

| Pole-Mounted |

| Pad-Mounted |

| Substation-Mounted |

| Low Voltage (Up to 5 kV) |

| Medium Voltage (5 kV to 40 kV) |

| High Voltage (Over 40 kV) |

| Automatic/Smart Regulators |

| Conventional/Electromechanical |

| Commercial |

| Residential |

| Industrial |

| Utility |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Phase Type | Single-Phase | |

| Three-Phase | ||

| By Mounting | Pole-Mounted | |

| Pad-Mounted | ||

| Substation-Mounted | ||

| By Voltage Rating | Low Voltage (Up to 5 kV) | |

| Medium Voltage (5 kV to 40 kV) | ||

| High Voltage (Over 40 kV) | ||

| By Control Type | Automatic/Smart Regulators | |

| Conventional/Electromechanical | ||

| By End-user | Commercial | |

| Residential | ||

| Industrial | ||

| Utility | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the distribution voltage regulator market?

It is estimated at USD 2.56 billion, part of a trajectory toward USD 3.29 billion by 2031.

Which region contributes the most revenue?

Asia-Pacific generated 43% of global sales in 2025 and continues to expand fastest.

Why are high-voltage regulators gaining attention?

Offshore-wind HVDC links and long-distance renewables require above 40 kV voltage support, driving a 7.9% CAGR for the segment.

How are copper prices influencing device costs?

Copper at USD 12,758 per ton raises material expenses for windings, squeezing supplier margins and extending lead times.

What role do data centers play in demand?

Hyperscale campuses impose ±1 % voltage windows, prompting substation-mounted smart regulator installations with millisecond response.

Are hybrid STATCOM-regulator solutions replacing standalone units?

Yes, many utilities now specify integrated skids that combine reactive power injection with voltage regulation to cut footprint and control complexity.

Page last updated on: