Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 9.64% CAGR |

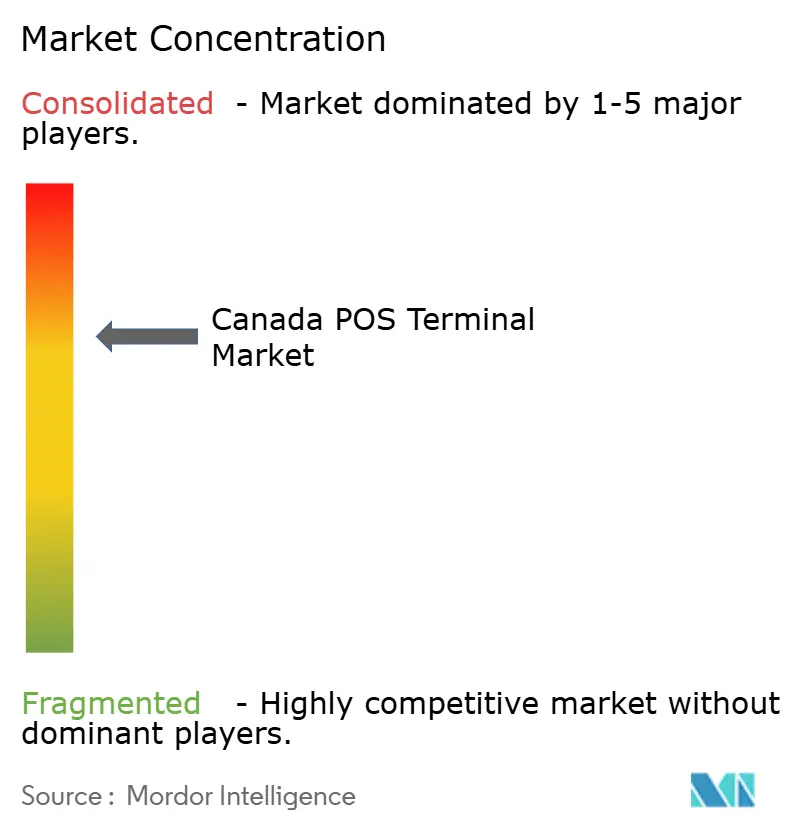

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada POS Terminal Market Analysis by Mordor Intelligence

Canada POS Terminal Market size in 2026 is estimated at USD 1.49 billion, growing from 2025 value of USD 1.36 billion with 2031 projections showing USD 2.36 billion, growing at 9.64% CAGR over 2026-2031. Contactless transactions already account for 63% of all in-store payments, up 17 percentage points from 2024, underscoring a structural pivot toward tap-to-pay behavior. The Retail Payment Activities Act (RPAA) drives a compliance-led refresh cycle as all payment service providers must register by November 2024 and meet operational standards by September 2025.[1]Source: Morrow, Ron, “Laying bare the evolution of payments in Canada,” Bank of Canada, bankofcanada.ca Competitive differentiation is shifting from hardware alone to software-rich ecosystems that embed AI fraud analytics, real-time reporting, and omnichannel orchestration capabilities. Meanwhile, persistent semiconductor shortages and elevated cybersecurity concerns temper momentum but are offset by interchange-fee reductions of up to 27% for small businesses and the anticipated launch of open banking legislation in 2025, which together lower the cost and complexity of electronic acceptance

Key Report Takeaways

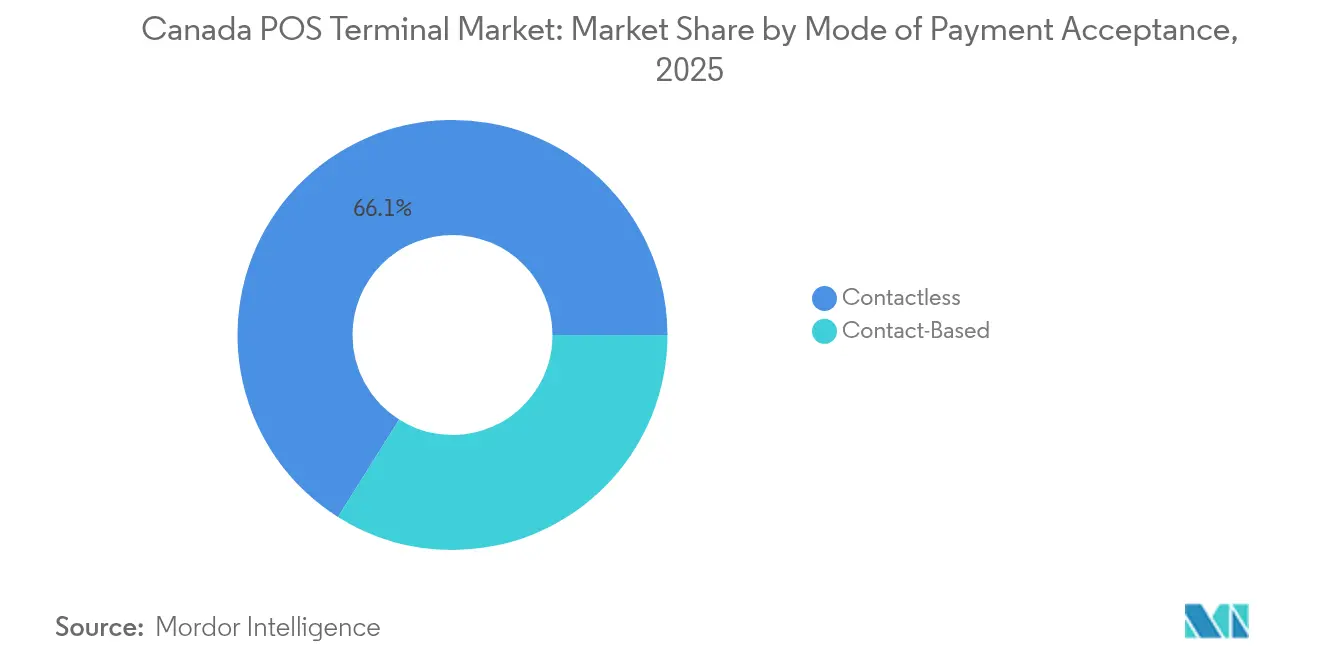

- By mode of payment acceptance, contactless solutions led with a 66.05% of the Canada POS terminal market revenue share in 2025 and are forecast to expand at an 11.12% CAGR through 2031.

- By POS type, mobile and portable systems held 54.25% of the Canada POS terminal market share in 2025, while the segment is projected to grow at a 10.45% CAGR to 2031.

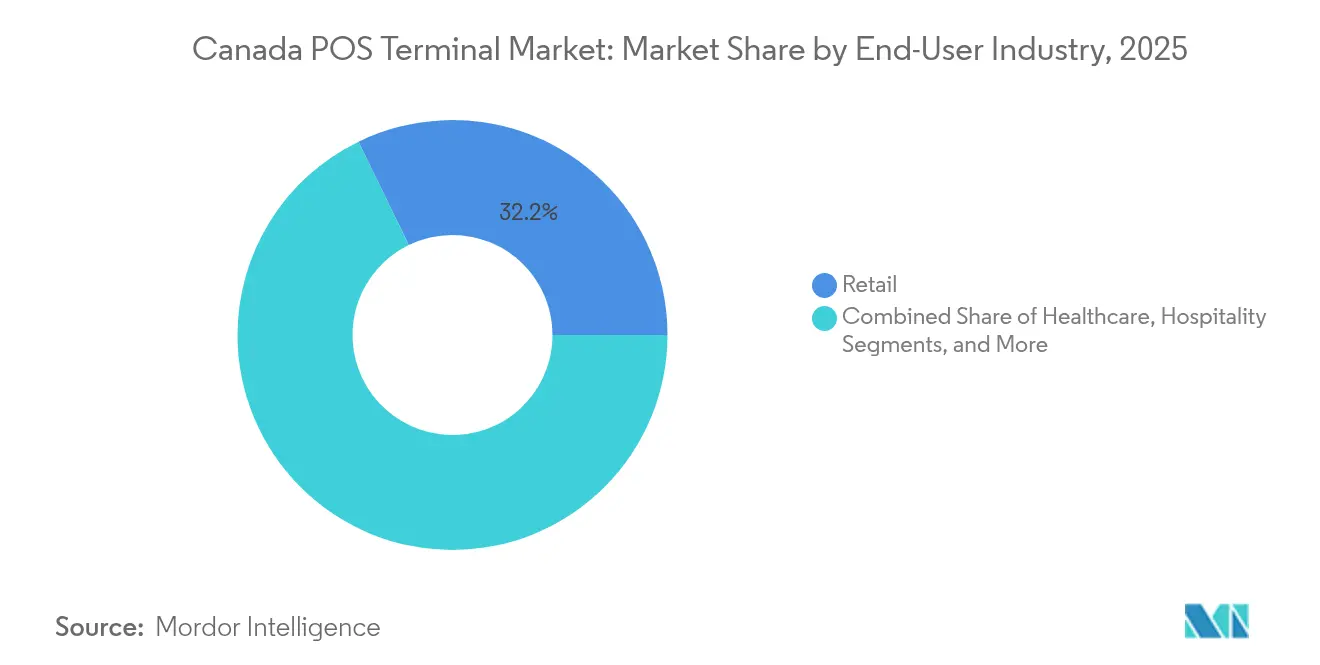

- By end-user industry, retail accounted for a 32.20% share of the Canada POS terminal market size in 2025 and healthcare is advancing at a 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Total Cost of Ownership vs Other Payment Channels | +1.8% | National, with early gains in Toronto, Montreal, Vancouver | Medium term (2-4 years) |

| Surging Demand for Contactless and mPOS Solutions | +2.4% | National, accelerated adoption in urban centers | Short term (≤ 2 years) |

| Regulatory Push toward Cashless Economy | +1.5% | National, with RPAA compliance requirements | Medium term (2-4 years) |

| Expansion of SaaS-Based POS Platforms for SMBs | +2.1% | National, concentrated in SMB-dense regions | Medium term (2-4 years) |

| 5G and Edge-Enabled Real-Time Analytics at Checkout | +1.2% | Major urban centers, expanding to secondary markets | Long term (≥ 4 years) |

| Rise of POS-as-a-Service Subscription Models | +1.6% | National, particularly attractive to cash-constrained SMBs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Contactless and mPOS Solutions

Contactless usage is reshaping checkout strategies as in-store mobile contactless payments surged 42% year-over-year in 2024 to represent 23% of all tap-to-pay volume. Wearables generated 44 million transactions worth CAD 1.1 billion, reflecting deepening consumer trust in tokenized NFC credentials.[2]Interac Corp., “Get ahead of the curve with data-driven trends,” interac.ca Gen Z adoption fuels the change, with 70% using mobile wallets and 63% comfortable leaving physical wallets behind. Merchants respond by deploying NFC-ready devices that enable staff-assisted or self-checkout flows anywhere on the sales floor. Public transit rollouts, such as tap-to-pay across the Toronto Transit Commission, showcase large-scale viability and build consumer familiarity with touchless fare collection.

Expansion of SaaS-Based POS Platforms for SMBs

Cloud POS subscriptions lower entry barriers, illustrated by Moneris Go Retail POS at CAD 10 per month for software plus CAD 34.95 for terminal rental. This operating-expense model resonates with Canada’s 1.2 million SMBs, 53% of whom feel overwhelmed by manual finance workflows.[3]Plooto Money Team, “The state of SMB finances,” plooto.com SaaS offers continuous feature delivery and automatic compliance updates, vital under rapidly evolving RPAA rules. Integrated inventory, CRM, and loyalty functions add value beyond payment processing, encouraging merchants to consolidate their tech stack with a single vendor. Third-party solution providers also gain from easier API integrations and revenue-sharing opportunities.

Low Total Cost of Ownership vs Other Payment Channels

Contactless debit dominates POS activity, representing 62% of tap transactions and generating materially lower interchange versus credit rails. Lower per-transaction fees, coupled with durable solid-state hardware, reduce lifetime costs compared with cash handling or legacy chip-and-PIN terminals. Cloud management cuts on-premises server spend, while over-the-air updates mitigate technician dispatch costs. These factors raise ROI for merchants and widen the addressable base for the Canada POS terminal market. Vendor finance programs further spread out capital expenditure and support faster refresh cycles among cost-sensitive verticals.

Regulatory Push toward Cashless Economy

The RPAA imposes mandatory registration and risk frameworks on payment providers, effectively institutionalizing digital rails as the standard for Canadian commerce. Concurrently, interchange reductions up to 27% on sub-CAD 300,000 annual Visa volumes enhance card economics for small firms. Looming open banking legislation promises real-time account-to-account settlement within POS flows, potentially bypassing card networks for certain use cases. Pandemic-era declines in cash use have become structural, reinforcing the policy-driven shift. Vendors offering compliance-ready software enjoy a first-mover edge as merchants seek turnkey solutions that satisfy audits without major hardware swaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Payment-Data Security Concerns | -1.4% | National, heightened in sectors handling sensitive data | Short term (≤ 2 years) |

| High Up-Front Hardware Cost for Micro-Merchants | -0.9% | National, concentrated in rural and low-margin businesses | Medium term (2-4 years) |

| Supply-Chain Chipset Volatility Post-COVID-19 | -1.1% | National, with manufacturing delays affecting all regions | Short term (≤ 2 years) |

| Legacy Integration Complexities in Tier-1 Retail | -0.8% | Major urban centers, concentrated in established retail chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Payment-Data Security Concerns

High-profile breaches heighten anxiety among healthcare and financial-services merchants that handle sensitive data. Many believe personal information is more exposed today than ever, yet feel current safeguards remain inadequate. Compliance with PCI DSS, provincial privacy statutes, and forthcoming AI governance rules adds complexity and cost. Security fears delay refresh cycles, especially for niche verticals that store medical or biometric data. Vendors that obtain PCI P2PE certification and embed tokenization, as Moneris has done across its Go devices, convert risk management into a selling point.

High Up-Front Hardware Cost for Micro-Merchants

Micro-merchants operating on thin margins struggle to justify advanced terminals once processing fees, software licenses, and integration labor are factored in. Inflation pressures and limited cash flow amplify the challenge. Rural operators often lack wired broadband, necessitating cellular or satellite connectivity that drives costs higher. To counteract sticker shock, providers now push SoftPOS, turning Android smartphones into tap-to-pay endpoints, and subscription models that bundle hardware, support, and settlement services. Payroc’s partnership with Moneris exemplifies such semi-integrated packages that lower entry thresholds for independent software vendors serving small merchants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Dominance Accelerates

Contactless transactions held a 66.05% slice of the Canada POS terminal market in 2025 and are projected to post an 11.12% CAGR through 2031, far outpacing chip-and-PIN volumes. This trajectory positions tap-to-pay as the de facto consumer expectation at checkout, especially as debit-card limits rise and mobile wallet penetration deepens. Debit’s 62% share of contactless volume underscores the importance of immediate fund access and budget control for Canadian shoppers. Merchants therefore prioritize NFC-enabled devices with real-time debit rails and one-tap wallet compatibility, reshaping procurement criteria.

Contact-based acceptance remains relevant for high-ticket or regulated scenarios that still demand signature or PIN verification, yet its share continues to erode. Regulatory frameworks now grant lower PCI scope to tokenized contactless environments, further tipping the scales toward tap adoption. The total contactless Canada POS terminal market size for debit alone is forecast to exceed USD 1.06 billion by 2031, reinforcing hardware and software roadmaps centered on NFC, tokenization, and biometric validation features.

By POS Type: Mobile Solutions Drive Market Evolution

Mobile and portable devices captured 54.25% of the Canada POS terminal market in 2025 and are advancing at a 10.45% CAGR to 2031 as retailers pivot from queue-based checkout to in-aisle engagement. Tablets and purpose-built handhelds enable line-busting, proactive sales assistance, and tableside ordering, thereby monetizing store real estate more efficiently. Restaurants top the priority list: 89% plan technology investments with mobile POS at the forefront for integrating order, pay, and loyalty workflows.

Fixed units still dominate high-volume lanes where cash drawers, receipt printers, and conveyor belts remain critical. Yet their growth lags as portable form factors inherit cashier functions at a lower footprint cost. The Canada POS terminal market size tied to mobile formats is expected to reach USD 1.33 billion by 2031, spurred by 5G connectivity, cloud API ecosystems, and declining battery prices. Vendors now emphasize modular docks and unified OS stacks so merchants can fluidly combine countertop and roaming experiences without duplicating software spend.

By End-User Industry: Healthcare Emerges as Growth Leader

Retail preserved its historical leadership with a 32.20% share of the Canada POS terminal market in 2025 due to sheer store count and high transaction frequency. However, healthcare is registering the fastest expansion at a 10.05% CAGR through 2031 as clinics move away from invoices and checks toward instant card or wallet settlement. Rising patient cost-sharing, telehealth adoption, and the need for HIPAA-compliant payment flows drive hospital investments in secure, tokenized devices.

Hospitality follows closely, pairing reservation, menu, and payment data into unified dashboards that streamline staff workflows and elevate guest experiences. Transportation and logistics firms increasingly deploy ruggedized mobile units for proof-of-delivery and on-the-spot payments. Collectively, non-retail verticals account for roughly 48% of Canada POS terminal market share, a balance that diffuses vendor risk across multiple industry cycles and regulatory regimes.

Geography Analysis

Ontario and Quebec command the largest provincial shares, leveraging dense merchant populations, well-developed fiber and 5G networks, and early-adopter cultures that embrace digital commerce. The Greater Toronto Area alone processes more than 25% of national card volumes, making it a bellwether for hardware upgrades and software feature rollouts. Montreal’s vibrant SMB scene accelerates SaaS POS uptake, particularly among bilingual retailers seeking localized support.

British Columbia, anchored by Vancouver, posts strong demand in hospitality, driven by tourism and an expanding tech workforce. Alberta and Saskatchewan exhibit growing adoption tied to resource-sector diversification and agri-business modernization, with mobile devices enabling remote, seasonal, and pop-up operations. Atlantic provinces progress at a steadier pace, though Halifax retailers increasingly integrate tap-to-pay with loyalty platforms to compete for visitor spend.

Nationwide payment rails, Real-Time Rail and ISO 20022 messaging, assure consistent settlement speeds and data depth regardless of geography, unlocking advanced analytics for even rural merchants. Government small-business grants targeting digital transformation further stimulate hardware refresh outside major metros. The result is a broadening Canada POS terminal market footprint that balances urban scale with regional niche opportunities, sustaining double-digit growth despite economic unevenness.

Competitive Landscape

The market is moderately fragmented: global hardware giants Ingenico, Verifone, and PAX vie with domestic software-first players such as Moneris, Lightspeed, and Square Canada. Hardware commoditization pushes vendors toward platform strategies bundling payment processing, business software, and data services. Moneris leverages deep Canadian regulatory insight to tailor RPAA-compliant tools, while Square scales on seamless e-commerce-brick-and-mortar convergence.

M&A signals maturation. Shift4’s CAD 200 million purchase of Givex extended its reach into gift-card and loyalty data, adding 100,000-plus Canadian endpoints. Paystone’s CAD 21 million acquisition of Ackroo boosted its cloud loyalty stack, illustrating appetite for value-added software to offset interchange compression. SoftPOS entrants threaten the low-end hardware tier, prompting incumbents to release smartphone-based solutions or flexible rental models.

Strategic partnerships amplify distribution. Square’s 2025 alliances with TouchBistro and Vend embed its payment rails within specialized vertical software, broadening exposure to restaurants and independent retailers. Integrated ecosystems increasingly decide vendor selection as merchants seek fewer vendors and unified support agreements. The combined share of the top five providers hovers near 55%, indicating healthy competition yet meaningful scale advantages for rule-of-three leaders.

Canada POS Terminal Industry Leaders

HP Development Company LP

Panasonic Corporation

NEC Corporation

Samsung Electronics Co., Ltd.

Ingenico Group SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Square Canada partnered with TouchBistro and Vend to extend integrated payment capabilities across restaurant and retail platforms.

- December 2024: Paystone acquired Ackroo for CAD 21 million to strengthen its loyalty and cloud POS offerings.

- October 2024: PSP Services agreed to buy NCR Atleos’ Canadian debit card production and processing business, enhancing its HLX commerce stack.

- August 2024: Shift4 Payments purchased Givex for CAD 200 million, uniting payment processing with gift-card and loyalty programs.

Canada POS Terminal Market Report Scope

The POS Terminals market includes revenues generated from hardware, software, and services, managing the transaction during the sale of a product or a service. It helps collect, save, share, and report data regarding sales transactions.

The system eases the shopping experience, helping expedite the checkout process, and implying customer satisfaction. Inventory management, product availability, stock in hand, and pricing information are primary data acquired from the systems.

The various end-user industries include entertainment, retail, healthcare, and hospitality. The impact of COVID-19 on the market and affected segments are also covered under the scope of the study.

By Mode of Payment Acceptance

| Contact-Based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable POS Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-user Industries |

| By Mode of Payment Acceptance | Contact-Based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable POS Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the Canada POS terminal market?

The Canada POS terminal market is valued at 1.49 billion USD in 2026 and is set to reach 2.36 billion USD by 2031.

How fast is the contactless segment growing?

Contactless payment acceptance is expanding at an 11.12% CAGR, outpacing all other modes through 2031.

Which POS type leads adoption in Canada?

Mobile and portable terminals lead with 54.25% market share as merchants favor flexible, in-aisle checkout.

Which industry vertical is the fastest-growing user of POS terminals?

Healthcare is advancing at a 10.05% CAGR as clinics digitize patient billing and copay collection.

How does regulation affect POS investment?

The Retail Payment Activities Act compels merchants to adopt compliant terminals by September 2025, fueling upgrade cycles.

Page last updated on: