Digital Holography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.58 Billion |

| Market Size (2031) | USD 11.03 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

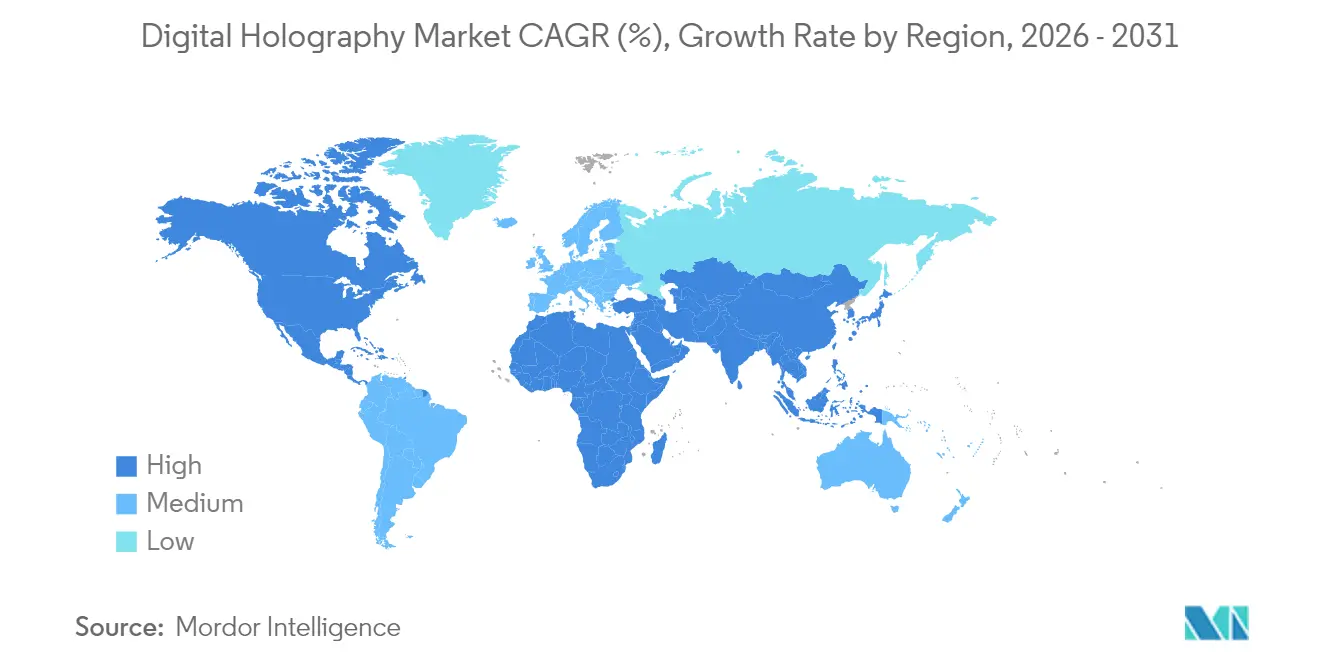

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Holography Market Analysis by Mordor Intelligence

The digital holography market size is expected to grow from USD 4.87 billion in 2025 to USD 5.58 billion in 2026 and is forecast to reach USD 11.03 billion by 2031 at 14.62% CAGR over 2026-2031. A sequence of defense, medical and automotive roll-outs has raised adoption far above the broader imaging-technology field. U.S. programs funding holographic LiDAR for military intelligence, Japanese and South Korean grants supporting label-free cell analysis, and German premium-vehicle head-up-display (HUD) design wins have converged to create a powerful pull for commercial deployments. Bandwidth barriers that once constrained real-time 3D meetings receded after Versatile Video Coding (H.266/VVC) cut data loads by 40%, enabling nationwide U.S. 5G telepresence pilots. Simultaneously, Chinese tier-1 malls proved that volumetric advertising can lift featured-product sales 40%, attracting retailers across Southeast Asia to the digital holography market.

Key Report Takeaways

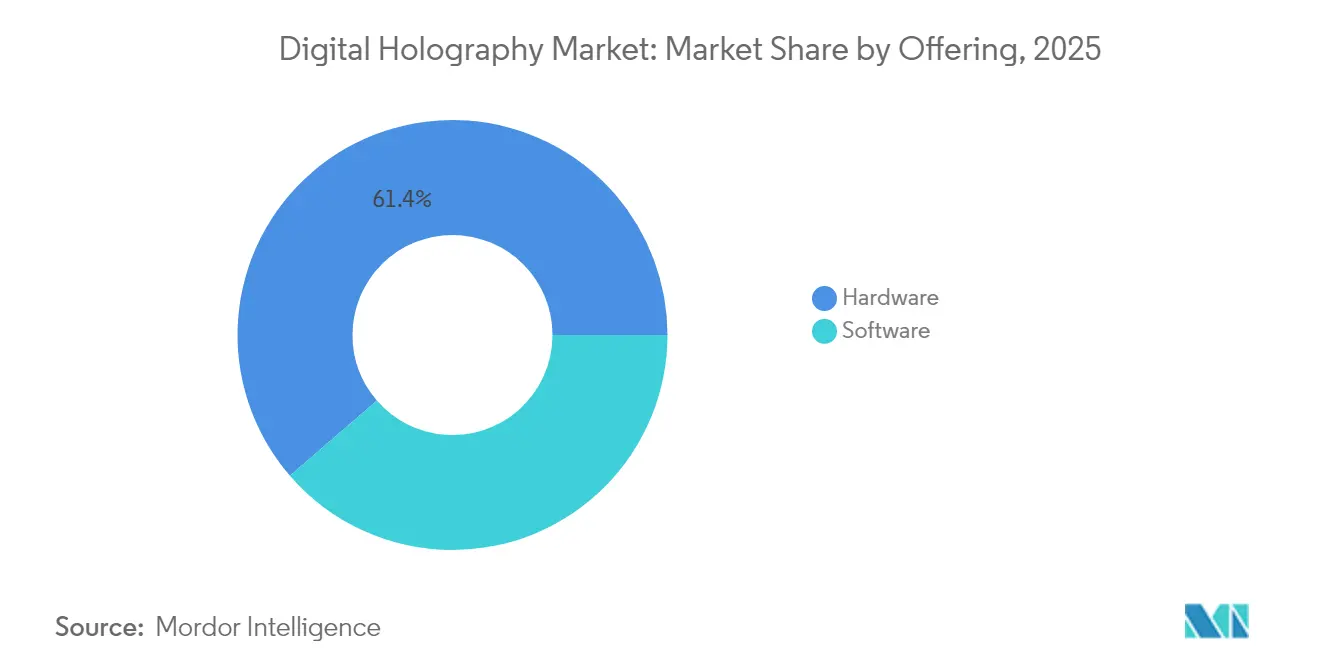

- By offering, hardware held 61.35% of digital holography market share in 2025, whereas software is advancing with a 14.73% CAGR through 2031.

- By technique, off-axis holography led with 68.50% revenue share in 2025; synthetic-aperture methods are rising fastest at a 16.42% CAGR to 2031.

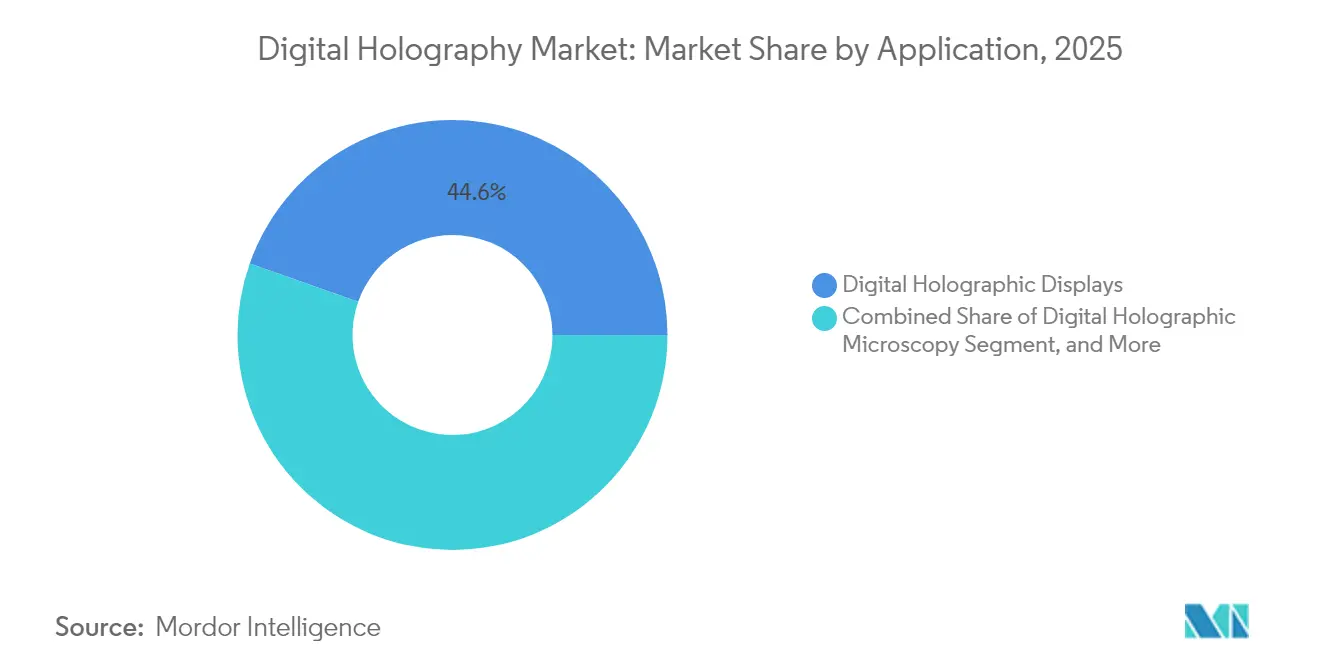

- By application, digital holographic displays accounted for 44.60% share of the digital holography market size in 2025, while telepresence solutions are forecast to expand at 15.22% CAGR.

- By end-user vertical, medical and life sciences captured 31.10% of digital holography market share in 2025; the automotive sector is projected to grow at 15.56% CAGR.

- By region, North America dominated with 41.70% share in 2025, yet Asia–Pacific is projected to rise at a 15.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Holography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Label-free quantitative phase imaging in regenerative-medicine trials | +2.2% | Japan and South Korea with spillover to US/EU | Medium term (2-4 years) |

| Holographic HUD adoption by premium German OEMs | +2.3% | Germany; expansion across Europe and North America | Short term (≤ 2 years) |

| H.266/VVC codec enabling bandwidth-light telepresence | +2.3% | United States with global implications | Medium term (2-4 years) |

| Defense funding for holographic LiDAR ISR payloads | +2.5% | Israel and UAE; technology transfer to US | Medium term (2-4 years) |

| Edge-rendered volumetric ads on Chinese 5G-Advanced | +2.4% | China; early roll-outs in SE Asia | Short term (≤ 2 years) |

| AI-assisted reconstruction algorithms boosting image fidelity | +2.1% | Global research labs and OEM toolchains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in label-free quantitative phase imaging demand in regenerative medicine trials

Japanese and South Korean regenerative-medicine investigators increasingly relied on digital holographic microscopy to study living cells without stains, supported by Japan’s USD 215 million grant program in 2025. The ability of digital holography to capture both amplitude and phase information simultaneously enables researchers to analyze living cells with unprecedented detail, revealing cellular morphology and dynamics that remain invisible to conventional microscopy.[1]Frontiers in Physiology, “Cell Image Reconstruction Using Digital Holography With an Improved GS Algorithm,” frontiersin.org Phase Holographic Imaging reported a strategic expansion into the Spanish and Portuguese markets in Q1 2024, specifically targeting regenerative medicine applications. The resulting ability to monitor morphology and cell-cycle kinetics in real time sharpened trial design, shortened discovery timelines and reinforced Asia’s first-mover status in precision cell therapy. Spillover demand appeared in U.S. cancer-research centers adopting the same quantitative-phase workflows.

Adoption of holographic HUDs in premium German automotive OEM 2026 line-ups

German automotive manufacturers are at the forefront of integrating holographic head-up displays (HUDs) into their premium vehicle models, with production implementations scheduled for 2026. BMW Group, Mercedes-Benz and Audi confirmed 2026 model-year launches using windshield-embedded holographic HUDs that maintain 5 000-nit brightness and remain visible through polarized sunglasses.[2]MotorTrend, “Are You Not Infotained?! New In-Car Screen Tech Is Jaw-Dropping at CES 2025,” motortrend.com Eastman, Ceres Holographics and Covestro supplied Holographic In-Plane Transparent Display (HIPTD) films that anchor the solution.[3]Eastman, “Eastman, Ceres Holographics and Covestro Partner to Advance Holographic Transparent Display HUD Technology,” saflex-vanceva.eastman.com By relocating speed, navigation and ADAS alerts into the driver’s line of sight, OEMs targeted higher Euro NCAP scores and reduced distraction-related incidents.

Standardization of H.266/VVC enabling bandwidth-light holographic telepresence on U.S. 5G networks

The finalization of the H.266/Versatile Video Coding (VVC) standard represents a watershed moment for holographic telepresence applications, reducing bandwidth requirements by approximately 40% compared to previous codecs. This efficiency gain is critical for holographic communication, which traditionally demands massive data transmission capabilities. U.S. telecommunications providers are leveraging this advancement to enable real-time holographic telepresence over 5G networks, with commercial deployments beginning in major metropolitan area.[4]Telecom Review Asia, “The Emergence of Holographic Communication in Asia-Pacific Telecommunications,” telecomreviewasia.com Enterprises began evaluating remote-training and executive-briefing applications that promise travel-cost savings and carbon-footprint reductions.

Defense funding for long-range holographic LiDAR ISR payloads in Israel and UAE

Israeli and Emirati ministries of defense awarded multi-year contracts for drone-borne holographic LiDAR able to map 10 km targets with millimeter accuracy, enhancing ISR reach while shrinking sensor weight by 30% compared with scanning-mirror systems. These systems utilize digital holography to achieve unprecedented range and resolution in target identification while maintaining compact form factors suitable for drone and vehicle-mounted deployments. The technology enables 3D mapping of terrain and structures with millimeter-level precision at distances exceeding 10 kilometers, representing a significant advancement over conventional LiDAR systems. Lockheed Martin highlighted the integration of holographic technologies in space and defense applications, noting that these systems enhance situational awareness while reducing size, weight, and power requirements.[5]Lockheed Martin, “Space Technology Trends 2025,” lockheedmartin.com U.S. primes licensed the architecture under export agreements, anticipating integration into next-generation under-30 kg reconnaissance drones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse supply of high-efficiency 4K spatial-light modulators | -0.8% | Global, acute for North America and Europe | Short term (≤ 2 years) |

| Prohibitive clean-room CAPEX (> USD 80 million) for phase-only SLMs | -0.9% | Global, highest for emerging entrants | Long term (≥ 4 years) |

| Lack of volumetric-video standards among LATAM broadcasters | -0.7% | Latin America; secondary global effects | Medium term (2-4 years) |

| Clinician scepticism absent multi-centre RCT evidence | -0.8% | EU and North American healthcare markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse supply of high-efficiency 4K spatial light modulators from APAC foundries

The digital holography market faces significant supply constraints for high-efficiency 4K spatial light modulators (SLMs), a critical component in holographic display systems. APAC foundries, particularly in Japan and South Korea, are struggling to meet growing demand due to production capacity limitations and competing priorities for semiconductor manufacturing lines. This supply shortage is exacerbated by the specialized nature of SLM production, which requires expertise in both semiconductor fabrication and optical engineering. Recent research has explored alternative approaches, such as digital micromirror devices (DMDs), which offer advantages including higher resolution and faster switching speeds compared to traditional liquid crystal SLMs. Spot prices for phase-only devices spiked 18% in 2025.

Prohibitive clean-room CAPEX (> USD 80 m) for phase-only SLM fabrication

The establishment of new production facilities for phase-only spatial light modulators requires capital expenditures exceeding USD 80 million, primarily for clean-room environments that meet the stringent requirements for optical-grade component manufacturing. This substantial investment barrier is deterring new entrants and limiting expansion of existing production capacity. The high costs are driven by the need for Class 10 or better clean rooms, specialized lithography equipment, and precision optical testing facilities. A study published in Photonics highlighted the challenges in fabricating SLMs with the necessary pixel density and phase modulation capabilities for advanced holographic applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Solutions Accelerate Transformation

Hardware captured 61.35% of digital holography market share in 2025, anchored by lasers, cameras and spatial-light modulators that convert optical interference into raw holograms. Cameras now exceed 100 MP at sub-3 µm pixel pitches, lifting system-level resolution. Meanwhile, software revenue is on course to add USD 1.58 billion through 2031 as iterative-phase retrieval, neural up-scaling and compression modules become indispensable for turnkey deployments. UCLA researchers demonstrated a recurrent-neural-network reconstruction that lifted structural-similarity metrics 40% and shortened compute time fifteen-fold, underscoring software’s role in unlocking latent value. Industrial original-equipment buyers have shifted to subscription models that bundle firmware upgrades, cloud render pipelines and on-premises debugging utilities in multi-year service-level agreements. These shifts point toward a future in which vendors package complete stacks, compressing integration timelines and amplifying switching costs-thereby raising the digital holography market size in recurring-revenue terms.

Second-generation application-programming interfaces link hologram generation engines with AR/VR design packages, removing barriers that previously fragmented content pipelines. Medical imaging labs exploit open-source Python plug-ins to automate phase-unwrap workflows, cutting experiment-setup times from hours to minutes. Automotive dashboard suppliers license proprietary calibration algorithms that align laser modulators to curved windshields, simplifying field-service logistics and protecting margin. Collectively, these dynamics confirm that software, though representing the smaller top-line slice today, will deliver disproportionate long-term profitability inside the digital holography industry.

By Technique: Synthetic-Aperture Methods Raise Resolution

Off-axis holography retained 68.50% of revenue in 2025 owing to robust photolithography-mask inspection and aerospace metrology installations. Users appreciate its single-exposure acquisition and inherent noise rejection, which preserve data integrity on vibrating factory floors. Yet synthetic-aperture and hybrid approaches are projected to climb at a 16.42% CAGR, propelled by multiview registration algorithms that chain sequential captures into one ultra-high-numerical-aperture composite. UCLA, Beihang University and Fraunhofer teams each reported > 57° viewing angles derived from synthetic-aperture assembly, tearing down the field-of-view wall that once limited commercial viability.

In-line holography, a workhorse for label-free microscopy, maintains a niche in cost-sensitive university labs that favor simpler alignments over maximal resolution. Touchable-holography prototypes from the Public University of Navarra added tactile feedback via ultrasonic phased arrays in April 2025, prompting museum and ed-tech pilots. The confluence of decreasing laser-diode pricing, precision-servo advances and AI reconstruction now positions hybrid systems to usurp legacy interferometers in inspection lines, potentially redirecting another 5% share toward synthetic-aperture architectures by 2028. If spatial-light-modulator supply stabilizes, the digital holography market share of these techniques could accelerate faster than forecast.

By Application: Telepresence Momentum Continues Post-Pandemic

Digital holographic displays accounted for 44.60% of 2025 revenue, serving flagship retail windows, medical theatres and defense planning cells. Brands such as Louis Vuitton reported 30% foot-traffic lifts when volumetric showcases rotated augmented bags in Shanghai malls. Concurrently, telepresence applications chart the quickest 15.22% CAGR. Early adopters in legal arbitration and surgical consulting validated productivity gains when remote participants interacted with life-size holograms rather than two-dimensional video tiles. The IEEE 1918.1.1 working group is drafting content-stream specifications expected to be ratified by 2026, smoothing cross-vendor interoperability.

Microscopy remains indispensable for live-cell biomechanics, corrosion-growth tracking and additive-manufacturing process control. Automotive HUD packages, now shipping in pilot fleets, are slated to enter mid-market trims once cost curves break USD 500 per windshield. Digital-holography-based data-vaults that store interference patterns in photopolymer discs reached 2-terabyte density demonstrations in 2024 and will target sensitive defense archives first. Authentication tags etched as nano-scale phase-gratings onto high-value documents surpassed 1 billion units shipped, illustrating how diversified the digital holography market size has become across use cases.

By End-User Vertical: Automotive Adoption Curve Steepens

Medical and life-science institutions commanded 31.10% of digital holography market share in 2025, financing turnkey microscopes that deliver quantitative-phase videos at 30 fps for stem-cell characterization. Hospitals in Germany and the United States trialed real-time holographic overlays during minimally invasive procedures, using gesture controls to pivot organ models without breaking sterile fields. In parallel, the automotive sector is poised to register a 15.56% CAGR as HUD penetration rises from niche luxury packages to mainstream ADAS platforms. Hyundai Mobis and Zeiss introduced holographic optical elements (HOEs) that refract light for sunlight-readable dashboards, trimming energy budgets versus LCD clusters.

Aerospace defense integrators integrate holographic sensors into small-satellite payloads for Earth-observation data cubes. Retail deploys volumetric ad walls in experiential flagships, and education ministries in South Korea equip classrooms with interactive holography kits to stimulate STEM enrollment. Semiconductor-inspection vendors use sub-nanometric phase mapping to quantify overlay errors, driving metrology tool upgrades on every lithography-node shrink. As these deployments converge, the automotive vertical’s incremental spend acts as a bellwether for consumer-facing holography, further broadening the overall digital holography market.

Geography Analysis

North America captured 41.70% of global revenue in 2025, driven by Pentagon R&D allocations and Silicon Valley enterprise pilots. U.S. telecom carriers fast-tracked city-center telepresence studios after H.266/VVC proved bandwidth-viable, turning Chicago, Dallas and San Francisco into early hubs. Canada emerged as a HUD-design incubator, leveraging provincial tax credits to lure optical-component start-ups that feed Detroit and Munich supply chains. Venture funding exceeded USD 300 million in 2025 for Montreal-based sensor firms.

Asia–Pacific, already the fastest-growing region with a 15.92% CAGR, benefited from Beijing’s 5G-Advanced footprint that streams real-time product holograms to high-street boutiques, advancing the digital holography market size for retail. Japanese life-science complexes adopted high-throughput phase-imaging rigs for regenerative-medicine assays, while South Korean automakers synchronized HOE tooling with HUD electronics to shorten ramp-up cycles. India’s e-waste challenge repurposed obsolete LCD backlights into holography-ready light-engines, diverting 500 tons of landfill in 2025.

Europe sustained momentum through Germany’s auto-tech partnerships and the UK’s National Health Service pilots. Horizon Europe earmarked EUR 95 million for advanced photonics projects in 2025, with phase-only SLM and polymer-film waveguide research receiving first-round grants. Israel and the UAE advanced defense LiDAR adoption, while Turkey initiated smart-city holographic-mapping bids. Latin America trailed due to volumetric-video standard gaps; Brazil’s broadcasters postponed 3D studio renovations pending specification clarity. Notwithstanding, Mexican architectural firms used holographic walk-throughs to win offshore contracts, hinting at latent demand growth once standards mature.

Competitive Landscape

Market concentration remained moderate: the top five suppliers controlled roughly 35% revenue in 2024, leaving space for vertical-specific entrants. Incumbents pursued joint ventures that fuse optics, materials and computation. The Eastman-Ceres-Covestro MoU established a complete windshield-display stack under one roof, reducing OEM validation burdens. RealView Imaging expanded its holographic cardiac-navigation suite, enabling catheter-lab teams to manipulate floating anatomy with ungloved hands. Lyncee TEC shipped interferometric microscopes calibrated for semiconductor front-end lines, tripling Swiss export revenue.

Start-ups targeted whitespace: WayRay delivered proof-of-concept holographic navigation for ride-hale fleets, and Light Field Lab sealed a USD 50 million Series C to miniaturize solid-state emitter arrays for gaming monitors. Component makers hedged supply risk by dual-sourcing phase-shifting backplanes from Taiwanese foundries. AI-centric algorithm suppliers moved upstream, bundling source code with FPGA reference designs to lock in silicon-level dependencies. Collectively these maneuvers intensified the fight for digital holography market share yet also expanded the total addressable market by bundling complementary offerings.

Niche applications remain ripe for first movers. Pharmaceutical simulation suites that visualize protein docking in volumetric space could shave months from drug-discovery cycles. Construction firms piloted on-site holographic blueprints that overlay wiring paths on bare studs, cutting rework costs. As defense, healthcare and mobility leaders validate such use cases, expect sustained M&A as conglomerates assemble capability portfolios, inching concentration upward over the forecast horizon.

Digital Holography Industry Leaders

RealView Imaging Ltd.

Lyncee TEC SA

Leia Inc

Holoxica Limited

EON Reality Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Phase Holographic Imaging expanded into Spain and Portugal via partnerships with Altium and Paralab to supply HoloMonitor systems for regenerative-medicine labs.

- April 2025: Researchers at the Public University of Navarra unveiled touchable hologram technology allowing users to manipulate 3D images without special gloves.

- March 2025: Stanford engineers developed a lightweight augmented-reality headset overlaying full-color holograms on standard eyewear, addressing comfort issues seen in earlier devices.

- January 2025: Ceres Holographics and Appotronics announced a joint program aiming to commercialize transparent HUD technology for 2028 vehicle platforms.

- December 2024: Eastman, Ceres Holographics and Covestro signed a Memorandum of Understanding to co-develop holographic windshield displays.

- October 2024: Holoconnects introduced Hologrid interactive walls, enhancing retail event engagement.

Global Digital Holography Market Report Scope

A wavefront diffracted from an object is captured using the holographic technique. By applying the theory of light diffraction, a hologram can be used to rebuild a three-dimensional (3D) image. An object's wavefront is recorded on a digital hologram using the process known as "Digital Holography," and then a computer is used to reconstruct both quantitative phase pictures and 3D images of the object.

The Digital Holography Market is Segmented by Offering (Hardware and Software), Application (Digital Holographic Displays, Digital Holographic Microscopy, and Holographic Telepresence), End-user Vertical (Medical, Aerospace and Defense, Commercial, Education, Automation, and Other End-user Verticals), and Geography. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Lasers |

| CCD/CMOS Image Sensors | |

| Spatial Light Modulators | |

| Beam Splitters and Optics | |

| Processors and Memory | |

| Software | Reconstruction Algorithms |

| Visualization/Rendering Engines | |

| Compression and Transmission Software |

| Off-Axis Holography |

| In-Line Holography |

| Synthetic Aperture and Hybrid Techniques |

| Touchable Holography |

| Digital Holographic Displays |

| Digital Holographic Microscopy |

| Holographic Telepresence and Communication |

| Head-Up Displays (Automotive and Aviation) |

| Data Storage and Security Authentication |

| Manufacturing and Metrology Inspection |

| Medical and Life Sciences |

| Aerospace and Defense |

| Automotive |

| Commercial and Retail |

| Education and Research Institutes |

| Industrial Automation |

| Media and Entertainment |

| Consumer Electronics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Gulf Cooperation Council Countries |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Hardware | Lasers |

| CCD/CMOS Image Sensors | ||

| Spatial Light Modulators | ||

| Beam Splitters and Optics | ||

| Processors and Memory | ||

| Software | Reconstruction Algorithms | |

| Visualization/Rendering Engines | ||

| Compression and Transmission Software | ||

| By Technique | Off-Axis Holography | |

| In-Line Holography | ||

| Synthetic Aperture and Hybrid Techniques | ||

| Touchable Holography | ||

| By Application | Digital Holographic Displays | |

| Digital Holographic Microscopy | ||

| Holographic Telepresence and Communication | ||

| Head-Up Displays (Automotive and Aviation) | ||

| Data Storage and Security Authentication | ||

| Manufacturing and Metrology Inspection | ||

| By End-User Vertical | Medical and Life Sciences | |

| Aerospace and Defense | ||

| Automotive | ||

| Commercial and Retail | ||

| Education and Research Institutes | ||

| Industrial Automation | ||

| Media and Entertainment | ||

| Consumer Electronics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Gulf Cooperation Council Countries | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What core factors are propelling the digital holography market?

Automotive HUD roll-outs, defense spending on long-range LiDAR and rising hospital demand for quantitative phase imaging collectively drive a 14.62% CAGR toward 2031.

Which region is growing fastest and why?

Asia–Pacific is expanding at a 15.92% CAGR, boosted by Chinese retail holography, Japanese regenerative-medicine grants and South Korean industrial deployments.

How does the H.266/VVC codec influence market adoption?

H.266/VVC trims volumetric-stream bandwidth by about 40%, enabling real-time holographic telepresence over existing 5G networks without infrastructure upgrades.

Why is spatial-light-modulator supply a constraint?

High-efficiency 4K SLMs require specialized fabs; limited capacity in Japan and South Korea has raised lead times and costs, hindering new product launches.

Which vertical commands the largest share of revenue?

Medical and life-science users held 31.10% of 2025 revenue because holography delivers non-invasive, high-resolution imaging vital for cell therapy and surgical planning.

How are leading companies strengthening competitive positions?

They form alliances that integrate optics, materials and AI-such as Eastman, Ceres Holographics and Covestro-shortening time-to-market and securing incremental digital holography market share.

How large is the Digital Holography market in 2026?

The digital holography market is expected to grow from USD 4.87 billion in 2025 to USD 5.58 billion in 2026 and is forecast to reach USD 11.03 billion by 2031 at 14.62% CAGR over 2026-2031

Page last updated on: