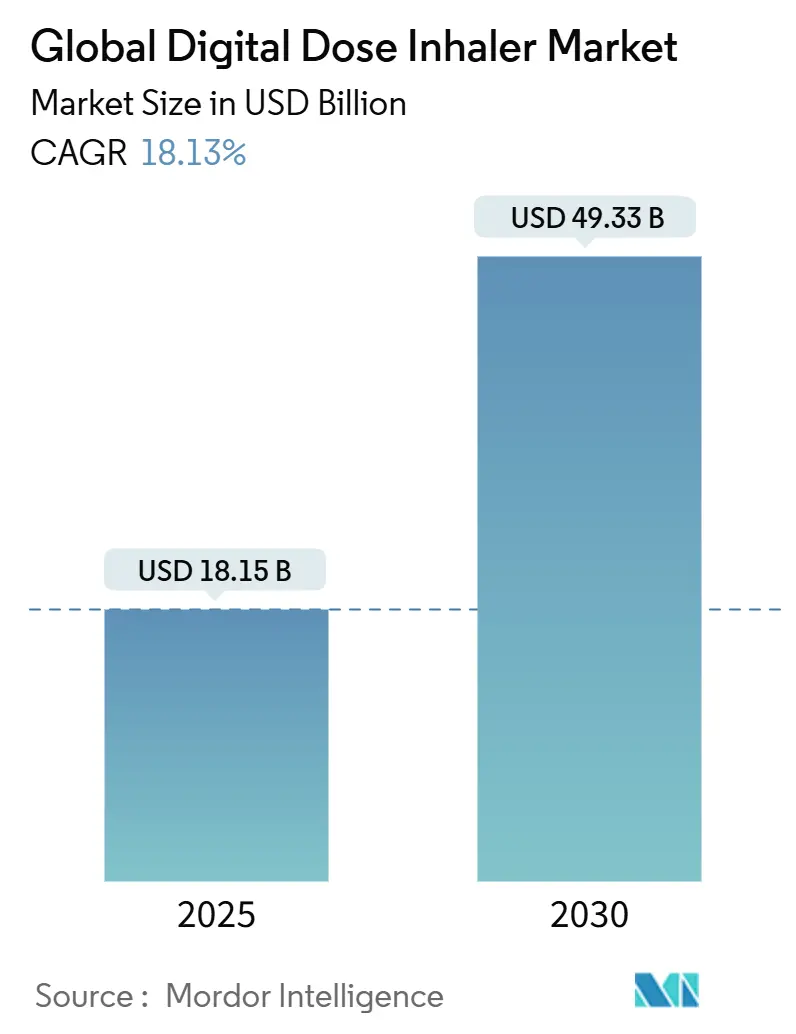

Global Digital Dose Inhaler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 18.15 Billion |

| Market Size (2030) | USD 49.33 Billion |

| Growth Rate (2025 - 2030) | 18.13% CAGR |

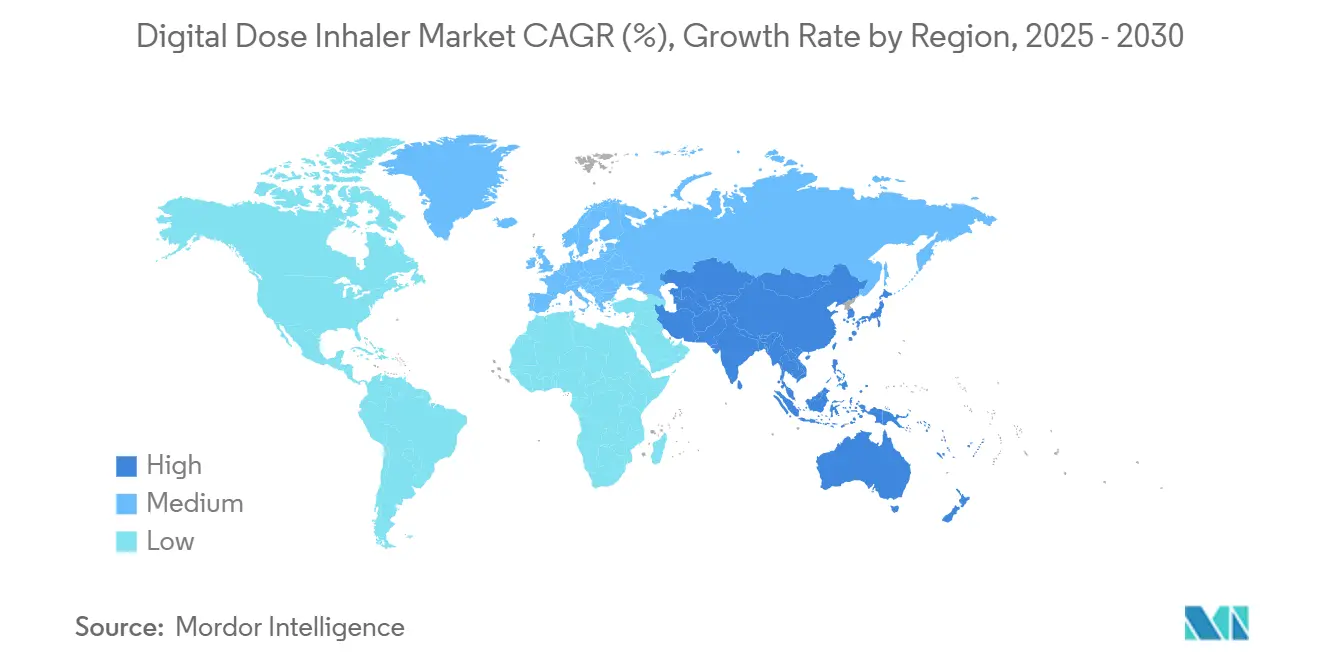

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Digital Dose Inhaler Market Analysis by Mordor Intelligence

The digital dose inhaler market is valued at USD 18.15 billion in 2025 and is projected to reach USD 49.33 billion by 2030, reflecting an 18.13% CAGR. Robust growth is linked to rising respiratory disease prevalence, rapid uptake of connected therapeutics, and stringent environmental regulations that are forcing propellant innovation. Real-time data capture from Internet of Things–enabled inhalers is giving physicians objective adherence evidence, while artificial intelligence is beginning to predict exacerbations before they occur. Capital inflows into digital respiratory care start-ups continue to climb, strengthening the competitive landscape and expanding patient access to sensor-equipped devices. Environmental legislation in Europe is accelerating the switch to low-GWP propellants, prompting major suppliers to overhaul meter-dose inhaler portfolios well ahead of 2030 compliance deadlines.

Key Report Takeaways

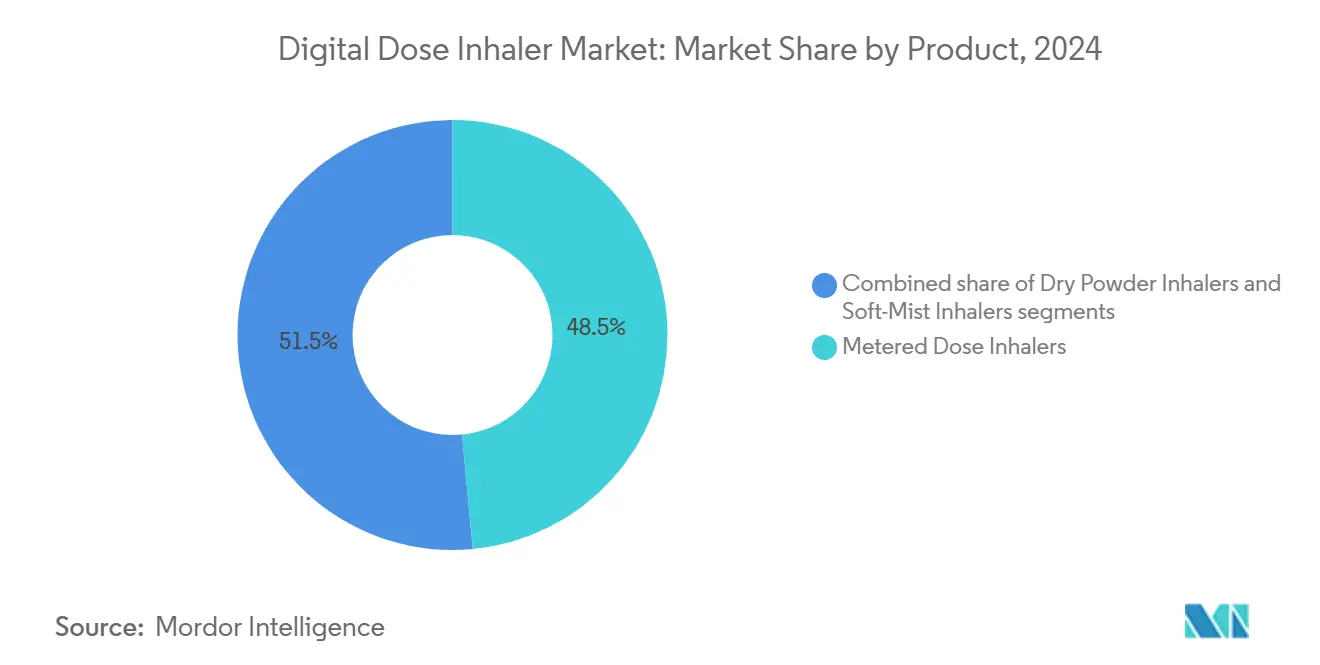

- By product, metered dose inhalers led with 48.54% of digital dose inhaler market share in 2024, while soft-mist inhalers are advancing at a 20.34% CAGR to 2030.

- By indication, asthma accounted for 41.48% share of the digital dose inhaler market size in 2024; cystic fibrosis is projected to expand at a 19.45% CAGR through 2030.

- By type, branded products captured 60.45% revenue share in 2024, whereas generics exhibit the highest projected CAGR at 19.86% to 2030.

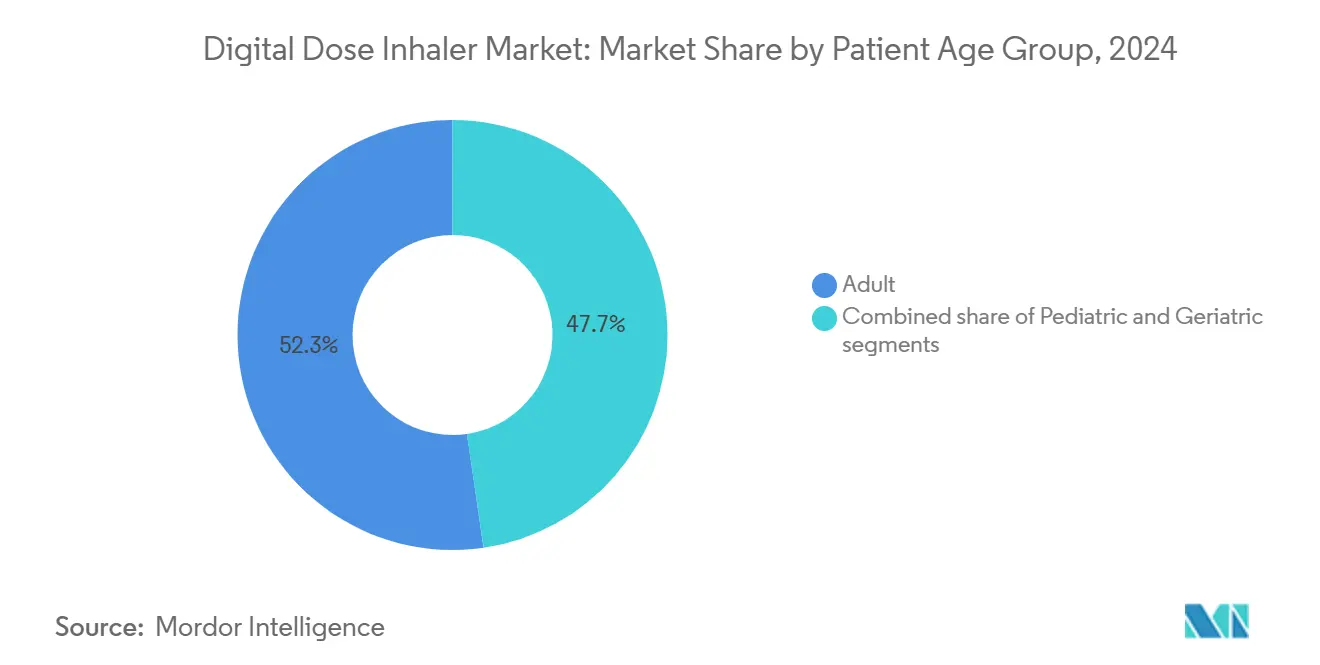

- By patient age, adults held 52.34% share of the digital dose inhaler market size in 2024, and pediatrics is growing at 18.67% CAGR to 2030.

- By distribution channel, retail pharmacies dominated with 46.78% of digital dose inhaler market share in 2024, while online pharmacies are forecast to post a 20.56% CAGR through 2030.

- By geography, North America controlled 43.45% revenue in 2024; Asia-Pacific is the fastest-growing region at a 19.45% CAGR to 2030.

Global Digital Dose Inhaler Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Respiratory Disease Burden | +4.2% | Highest in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Expanding Geriatric Patient Pool | +3.1% | North America & Europe; rising in Asia-Pacific | Long term (≥ 4 years) |

| Technological Advancements In Smart Inhaler Platforms | +5.8% | North America & Europe lead; Asia-Pacific catching up | Medium term (2-4 years) |

| Transition Toward Digital Therapeutics And Remote Monitoring | +3.7% | Global, with regulatory variations | Medium term (2-4 years) |

| Integration Of Data Analytics And Value-Based Care Models | +2.9% | Primarily North America & Europe | Medium term (2-4 years) |

| Environmental Compliance And Low-Gwp Propellant Adoption | +2.1% | European Union now; global roll-out expected | Short term (≤ 2 years) |

Source: Mordor Intelligence

Escalating Global Respiratory Disease Burden

Chronic respiratory diseases affected 213.39 million people in 2021, sustaining demand for connected inhalers that objectively record adherence. Studies show 44% adherence improvement among COPD patients using behavior-change programs linked to smart devices[1]Ravi Patel, “Behavior-Change Programs Boost COPD Adherence,” Expert Review of Pharmacoeconomics & Outcomes Research, tandfonline.com. Integration of artificial intelligence is enabling early exacerbation alerts, moving digital devices from passive trackers to proactive disease-management tools.

Expanding Geriatric Patient Pool

The geriatric cohort is the fastest-growing user group at an 18.67% CAGR through 2030 as age-related dexterity limitations make intuitive breath-activated devices attractive. Simplified interfaces and larger displays improve usability, while Medicare payment pilots are experimenting with sensor reimbursement, although national coverage remains uneven.

Technological Advancements in Smart Inhaler Platforms

The ProAir Digihaler became the first FDA-cleared inhaler with embedded monitoring, and real-world data from 360 patients captured 53,083 inhalations over 12 weeks, demonstrating granular insight into technique and frequency. Emerging wearables like AI Asthma Guard extend analytics beyond the device to ambient environment and physiology, creating closed-loop management frameworks.

Transition Toward Digital Therapeutics and Remote Monitoring

The FDA Digital Health Center of Excellence is shortening review cycles for combination products, and telemedicine infrastructure built during the COVID-19 pandemic remains in place, allowing inhaler data to flow directly into virtual visits. Real-time dashboards alert clinicians to non-adherence, reducing emergency visits and inpatient days, though high device costs and patient-education needs temper universal deployment[2]Anna Smith, “Artificial Intelligence Enhances Digital Inhaler Adherence,” Frontiers in Digital Health, frontiersin.org.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing Of Connected Inhaler Devices | -2.8% | Greatest in price-sensitive markets worldwide | Short term (≤ 2 years) |

| Complex Regulatory And Reimbursement Pathways | -1.9% | Most challenging in EU and emerging economies | Medium term (2-4 years) |

| Stringent Data Privacy And Cybersecurity Requirements | N/A | Global; strongest where data laws are strict | Medium term (2-4 years) |

| Semiconductor Supply Chain Constraints | N/A | Global | Short term (≤ 2 years) |

Source: Mordor Intelligence

Premium Pricing of Connected Inhaler Devices

Smart inhalers cost substantially more than conventional units, and total ownership expenses include data plans and software subscriptions. Economic evaluations find clinical benefits but question cost-effectiveness when pharmacy margins are narrow. Tiered pricing and payer partnerships are evolving, yet the lack of consistent reimbursement, especially in public systems, limits penetration in developing regions.

Complex Regulatory and Reimbursement Pathways

Digital inhalers are regulated as drug-device combinations, requiring simultaneous conformity with pharmaceutical and medical-device standards. Manufacturers navigate 510(k) clearances for sensors while maintaining NDA or ANDA status for formulations, prolonging timelines and inflating costs[3]FDA, “Digital Health Center of Excellence Guidance,” U.S. Food and Drug Administration, fda.gov. Data-protection statutes such as GDPR add cybersecurity obligations, and value-based payment models demand extensive real-world evidence before premium price approval.

Segment Analysis

By Product: Metered Dose Inhalers Lead Despite Environmental Pressures

Metered dose inhalers retained 48.54% of digital dose inhaler market share in 2024, underscoring user familiarity and mature manufacturing economics. The digital dose inhaler market size for this segment is projected to rise at a 14.2% CAGR as companies transition to ultra-low-GWP propellants. Environmental mandates are accelerating formulation re-engineering, with AstraZeneca’s HFO-1234ze(E) rollout reducing broad environmental impact by 99.9%.

Soft-mist inhalers provide higher lung deposition and need no propellant, fueling a 20.34% CAGR that outpaces the broader digital dose inhaler market. Device miniaturization and embedded sensors allow real-time flow measurement, appealing to providers seeking precise dose verification. Dry-powder inhalers remain relevant in regions with cooler climates and robust inspiratory flow among adult users, yet high humidity limits uptake in tropical geographies.

Note: Segment shares of all individual segments available upon report purchase

By Indication: Asthma Dominance Faces COPD Growth Acceleration

Asthma accounted for 41.48% of revenue in 2024, buoyed by large pediatric and young-adult cohorts and plentiful clinical evidence supporting connected adherence solutions. The digital dose inhaler market size for COPD is expanding faster at 18.9% CAGR as aging populations lengthen disease duration and payers seek cost offsets through fewer hospitalizations. HealthPrize RespiPoints documented a 44% adherence increase among tiotropium users, translating to material cost savings.

Cystic fibrosis growth at 19.45% CAGR demonstrates willingness of caregivers to invest in premium monitoring to optimize high-value medication regimens. AI algorithms now differentiate disease-specific inhalation patterns, personalizing coaching for each indication and raising the clinical relevance of connected platforms.

By Type: Branded Segment Maintains Premium Position

Branded products commanded 60.45% revenue in 2024 as physicians place a premium on consistent aerosol performance and integrated apps. One example is Novartis’ Enerzair Breezhaler, which received European Commission clearance bundled with a sensor and reminder app. Generic entrants are gaining momentum, though duplicating sophisticated digital ecosystems strains development budgets. As exclusivity cliffs appear, partnerships between generic manufacturers and software specialists may narrow the feature gap.

Regulators demand bioequivalence for both medicine and device, further complicating generic smart inhaler launches. Nevertheless, price pressure in public systems is likely to produce hybrid models whereby low-cost device shells pair with subscription-based digital overlays.

By Patient Age Group: Adult Segment Leadership with Pediatric Growth

Adults held 52.34% share in 2024 thanks to expansive insurance coverage and established clinic pathways. Seniors face dexterity challenges, driving refresh cycles toward breath-triggered units with wider mouthpieces and visual dose counters. Pediatric adoption is accelerating at 18.67% CAGR, propelled by child-specific trials such as INHALE-1 evaluating inhaled insulin delivery for young diabetes patients.

User-interface gamification boosts engagement among children, while parental dashboards enable dose confirmation. Withdrawal of certain age-specific corticosteroids in early 2024 illuminated supply vulnerabilities, supporting policy arguments for diversified pediatric portfolios.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Retail Pharmacy Dominance Faces Online Disruption

Retail pharmacies sold 46.78% of units in 2024 because inhaler technique training often happens in person. Chain-pharmacy pilots now incorporate Bluetooth-enabled teaching stations that sync with patient smartphones for later self-assessment. Online pharmacies are set to post a 20.56% CAGR as telehealth legitimacy grows, particularly for chronic-disease refills.

Regulatory reform permitting e-prescriptions for controller inhalers underpins channel migration. Direct-to-consumer storefronts for attachable sensors reinforce cross-sell opportunities, though regulators still require pharmacy fulfilment for medicated canisters.

Geography Analysis

North America generated 43.45% of revenue in 2024 on the back of sophisticated payer systems, high COPD prevalence, and early FDA approvals of digital therapeutics. GSK and Propeller Health broadened their collaboration to ship sensor-enabled Ellipta inhalers nationwide, demonstrating the commercial viability of integrated prescription-tech bundles. Canada benefits from single-payer purchasing leverage, while Provincial formularies are piloting outcome-based procurement tied to adherence reports. Mexico’s growing middle class and digital-health incentives open gateways for mid-priced devices.

Asia-Pacific is the fastest-growing region at 19.45% CAGR through 2030 as urban air pollution and smoking contribute to rising COPD cases. China’s population-level burden pressures policymakers to adopt preventive tools; public hospitals are trialling cloud dashboards that integrate inhaler data with electronic medical records. India’s expanding 4G coverage and revised telemedicine guidelines underpin online pharmacy distribution of sensor kits, yet affordability gaps persist. Japan couples rapidly aging demographics with a mature technology culture, making it a fertile market for premium soft-mist inhalers bundled with AI coaching.

Europe remains a mature but innovative market where environmental regulation sets global precedents. The F-Gas Regulation 2024/573 bans new HFC-filled inhalers outside of quota allocations from 2025, accelerating low-GWP adoption schedules. Germany’s DiGA framework reimburses certified digital health apps, positioning inhaler companion software for rapid uptake. The United Kingdom maintains a pragmatic stance, reimbursing devices that demonstrate hospital-admission avoidance. Middle East & Africa and South America are nascent yet promising, limited by infrastructure, clinician training, and consumer purchasing power. Donation programs and tiered pricing models aim to bridge these gaps.

Competitive Landscape

The digital dose inhaler market shows moderate consolidation, with incumbents acquiring specialized design firms to lock in end-to-end capabilities. Molex finalized its purchase of Vectura Group through Phillips Medisize, combining component miniaturization expertise with large-scale manufacturing. Altaris merged Kindeva Drug Delivery with Meridian Medical Technologies to create a hybrid CDMO spanning inhalers, autoinjectors, and transdermal patches, signaling a trend toward platform-agnostic drug-delivery contractors.

Technology alliances are equally influential. Teva collaborated with Amazon Web Services to analyze inhalation flow data, improving predictive algorithms for asthma attack risk. Start-ups offer disruptive innovation: Aevice Health raised USD 7 million to commercialize a wearable stethoscope that pairs with inhaler data streams to validate symptom-dose relationships. Intellectual-property filings in closed-loop vapor delivery and acoustic technique analysis are proliferating, indicating competitive differentiation is shifting from formulation to data science.

Regulatory expertise has emerged as a competitive asset. Firms with established quality-management systems and cybersecurity certifications secure faster approvals, shortening time-to-market. Market entry for new players is possible but resource-intensive, encouraging collaboration over direct confrontation.

Global Digital Dose Inhaler Industry Leaders

-

Teva Pharmaceutical Industries

-

GlaxoSmithKline plc

-

AstraZeneca plc

-

Boehringer Ingelheim

-

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AstraZeneca filed in the EU, UK, and China for HFO-1234ze(E) pressurized metered-dose inhalers—propellant cuts global warming impact by 99.9% and supports 2030 transition targets.

- February 2025: Molex closed the acquisition of Vectura Group through Phillips Medisize, enlarging its drug-device CDMO footprint in inhalation technologies.

- February 2025: Altaris combined Kindeva Drug Delivery with Meridian Medical Technologies to create a diversified complex-drug-delivery CDMO.

- January 2025: EU F-Gas Regulation 2024/573 became effective, banning HFC-filled medical inhalers outside quota systems.

- August 2024: Aevice Health secured USD 7 million seed-plus funding to scale its wearable respiratory monitoring platform in the US, Japan, and Singapore.

Global Digital Dose Inhaler Market Report Scope

As per the scope of the report, digital dose inhalers are devices that deliver a specific amount of medication to the lungs in the form of aerosolized medicine or dry powder. The Digital Dose Inhaler Market is Segmented by Product (Dry Powder Inhalers and Metered Dose Inhalers), Application (Chronic Obstructive Pulmonary Disease, Asthma and Others), Type (Branded and Generic), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Product | Dry Powder Inhalers | ||

| Metered Dose Inhalers | |||

| Soft-Mist Inhalers | |||

| By Indication | COPD | ||

| Asthma | |||

| Cystic Fibrosis | |||

| Other Respiratory Disorders | |||

| By Type | Branded | ||

| Generic | |||

| By Patient Age Group | Pediatric | ||

| Adult | |||

| Geriatric | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Dry Powder Inhalers |

| Metered Dose Inhalers |

| Soft-Mist Inhalers |

| COPD |

| Asthma |

| Cystic Fibrosis |

| Other Respiratory Disorders |

| Branded |

| Generic |

| Pediatric |

| Adult |

| Geriatric |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current digital dose inhaler market size?

The market stands at USD 18.15 billion in 2025 and is forecast to reach USD 49.33 billion by 2030.

Which product type leads the digital dose inhaler market?

Metered dose inhalers hold 48.54% market share due to clinical familiarity, although soft-mist inhalers are growing fastest.

How do environmental regulations influence inhaler design?

The EU F-Gas Regulation 2024/573 bans high-GWP propellants, prompting rapid adoption of alternatives like HFO-1234ze(E).

Which region is expected to grow most rapidly?

Asia-Pacific shows the highest CAGR at 19.45% through 2030, driven by rising disease incidence and expanding digital health infrastructure.

What are the main barriers to smart inhaler adoption?

Premium device pricing and complex regulatory-reimbursement pathways limit widespread uptake, especially in price-sensitive markets.

How do smart inhalers improve patient outcomes?

Sensors provide real-time adherence data, AI predicts exacerbations, and remote monitoring reduces emergency visits and hospitalizations.

Page last updated on: June 19, 2025