Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

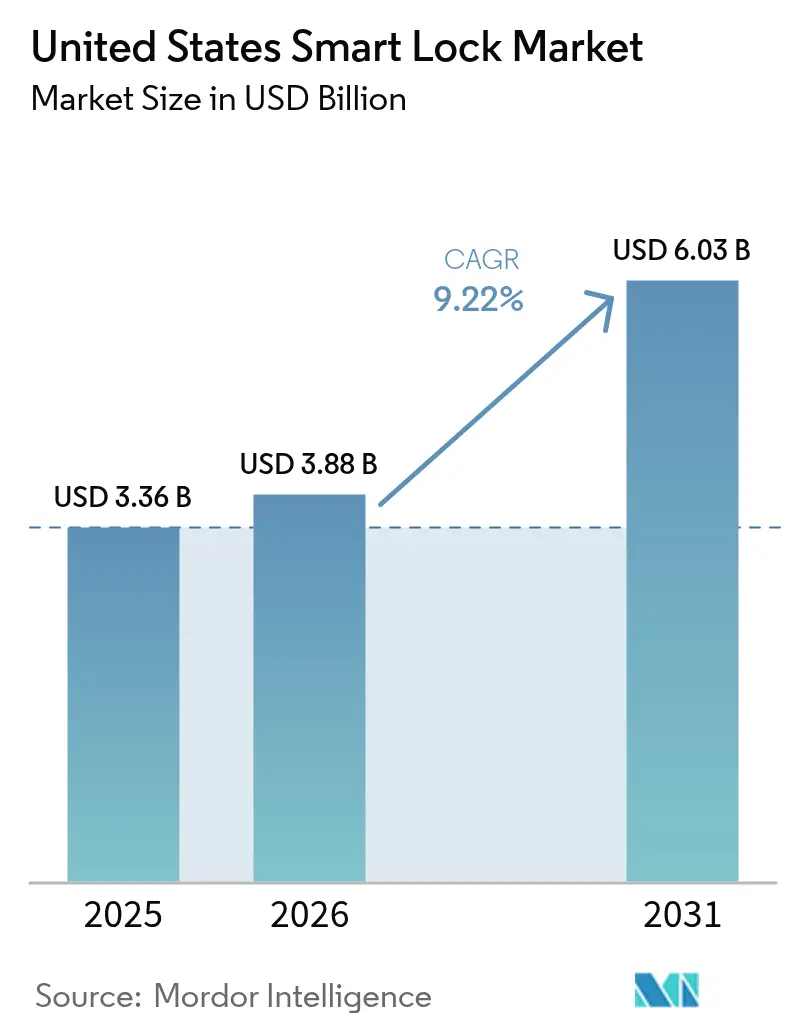

| Base Year Market Size (2025) | USD 3.36 Billion |

| Market Size (2026) | USD 3.88 Billion |

| Market Size (2031) | USD 6.03 Billion |

| Growth Rate (2026 - 2031) | 9.22% CAGR |

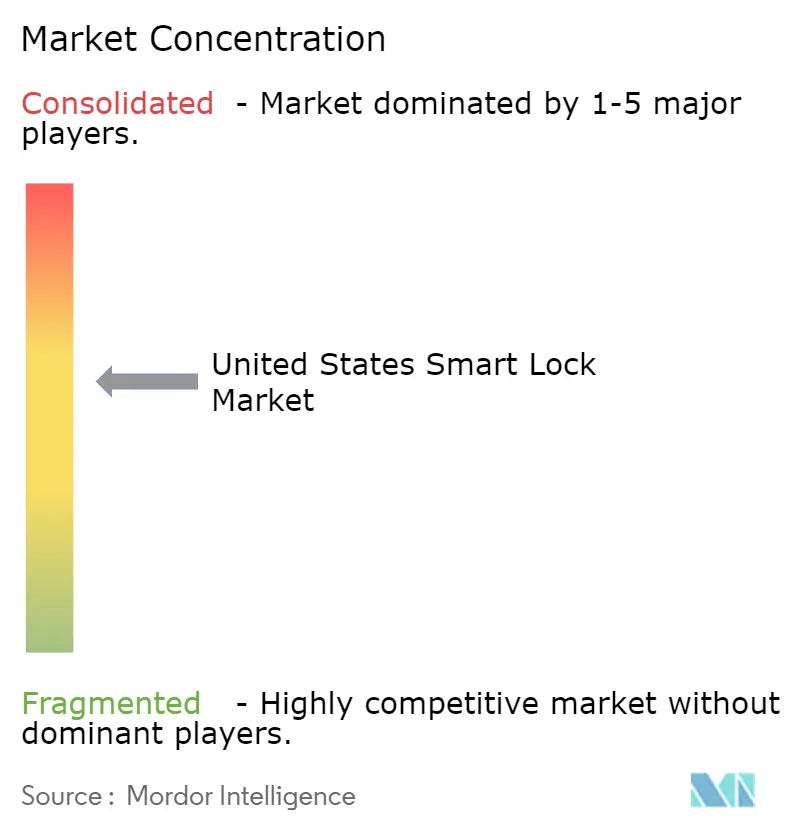

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Smart Lock Market Analysis by Mordor Intelligence

The United States smart lock market size was valued at USD 3.36 billion in 2025 and estimated to grow from USD 3.88 billion in 2026 to reach USD 6.03 billion by 2031, at a CAGR of 9.22% during the forecast period (2026-2031). Across the forecast horizon, demand is being pulled from mechanical deadbolts toward networked locks that authenticate smartphones, voice assistants, and property-management platforms in a unified credential ecosystem. Deadbolt formats still dominate shipments but the share of mortise, lever, and rim designs is climbing because commercial developers in hospitality, healthcare, and office real estate require ANSI/BHMA Grade 1 durability and fire-door compliance. Institutional landlords accelerating build-to-rent projects in Sunbelt states specify connected locks during the design phase, which removes retrofit complexity and cuts truck-roll costs after residents move in. Growth is further supported by insurance carriers that grant 2%5% premium discounts when policyholders verify smart-security installations.

Key Report Takeaways

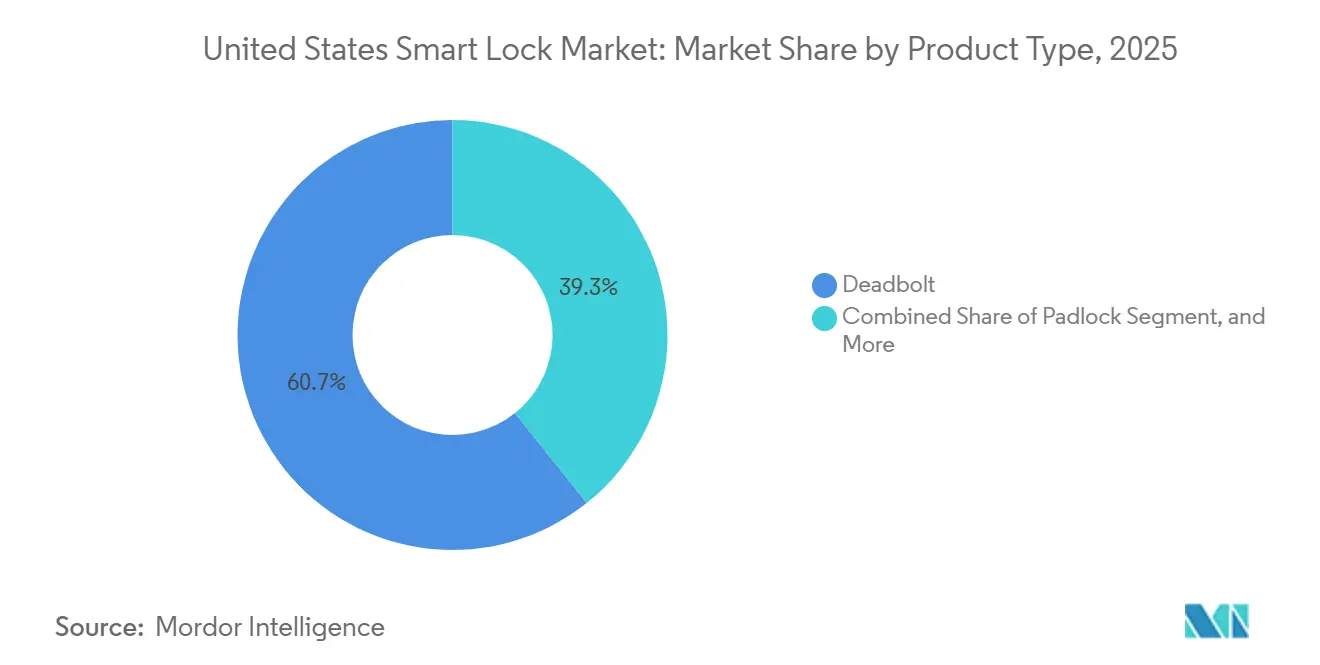

- By product type, deadbolts led with 60.73% of the United States smart lock market share in 2025, while mortise, lever, and rim locks are advancing at a 10.37% CAGR to 2031.

- By end-user, residential applications accounted for 88.39% of the US smart lock marketshare in2025 revenue, whereas commercial deployments are forecast to post an 11.12% CAGR through 2031.

- By installation type, retrofit solutions captured 57.88% share in 2025, yet new-construction integrated systems are projected to expand at a 10.61% CAGR between 2026 and 2031.

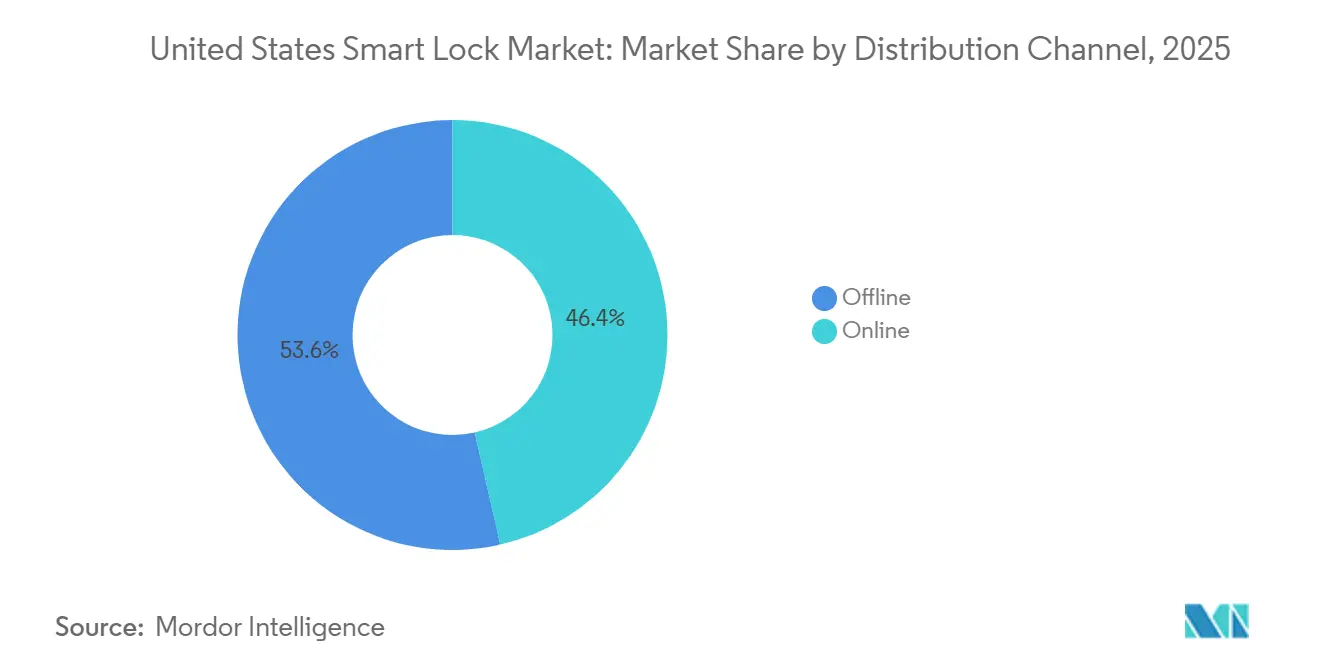

- By distribution, offline retail and pro-installer channels held 53.57% of the US smart lock marketshare in 2025, but online sales are projected to grow at a 9.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Smart Lock Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UWB Passive-Entry Capabilities Embedded in Smartphones | +2.1% | National, Strongest in Metros With High iPhone and Samsung Galaxy Penetration | Medium Term (2–4 Years) |

| Integration with Smart-Home Hubs and Voice Assistants | +1.8% | National, Accelerated in Regions With High Amazon Echo and Google Nest Adoption | Short Term (≤ 2 Years) |

| Build-to-Rent Single-Family Developments Adopting Smart Locks at Scale | +1.5% | Sunbelt States (TX, FL, AZ, GA, NC) | Medium Term (2–4 Years) |

| Rising Package-Theft Incidents Boosting Entryway Security Demand | +1.3% | National, Most Acute in Urban and Suburban Delivery Corridors | Short Term (≤ 2 Years) |

| Insurance Premium Discounts for Smart-Security Installations | +0.9% | National, Dependent on State Regulations and Carrier Participation | Long Term (≥ 4 Years) |

| ESG and LEED Incentives for Connected Access Solutions | +0.6% | Urban Markets With Green-Building Mandates (CA, NY, WA) | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Integration With Smart-Home Hubs and Voice Assistants

Matter 1.3 certification, ratified in late 2024, lets locks interoperate across Apple Home, Google Home, Amazon Alexa, and Samsung SmartThings without proprietary bridges, eliminating a major adoption barrier.[1]onnectivity Standards Alliance, “Matter 1.3 Specification,” csa-iot.org Thread mesh networking replaces Bluetooth Low Energy as the default radio for battery-powered locks, cutting latency and improving range inside multistory residences. Schlage’s Encode Plus debuted Apple Home Key support in early 2025, and Kwikset’s Halo Select Plus matched the feature set by August 2025, reinforcing competitive parity on credential options.[2]Schlage Lock Company LLC, “Encode Plus Product Sheet,” schlage.com Voice assistants now trigger compound routines, such as locking the door, arming the alarm, and adjusting the thermostat, through a single spoken command, which lowers the technical threshold for first-time buyers. The resulting rise in ease of use is broadening the United States smart lock market beyond early adopters into mass-market households. Continued firmware updates that bring Matter certification to older devices further protect consumer investment and encourage ecosystem stickiness.

Rising Package-Theft Incidents Boosting Entryway Security Demand

An estimated 250 000 parcels were stolen every day in 2025, driving USD 15 billion in annual losses across U.S. households according to aggregated carrier claims and retailer surveys. Smart locks paired with doorbell cameras allow owners to create one-time or time-bounded codes so delivery drivers can leave packages inside vestibules or garages. Amazon’s Key In-Garage Delivery program expanded to 15 additional metros in 2025, prompting lock vendors to pursue “Key-compatible” certification to tap that channel. Higher parcel volume in suburban single-family neighborhoods, combined with lower camera density than urban cores, intensifies demand for access-controlled drop-off points. The functional convergence of video verification, temporary credentials, and cloud logging has therefore repositioned entry doors as critical nodes in the last-mile logistics chain, lifting unit sales within the United States smart lock market.

Build-to-Rent Single-Family Developments Adopting Smart Locks at Scale

Institutional landlords managed roughly 750 000 rental homes in 2025, and most have standardized smartphone-controlled locks to remove physical key exchanges during tenant turnover.[3]Invitation Homes Inc., “Smart Homes in SFR,” invitationhomes.com When specified during construction, smart locks eliminate retrofit labor, reduce door damage risk, and integrate natively with property-management software, allowing automatic credential provisioning at lease signing. Invitation Homes reports that automated re-keying shrinks vacant-unit days and cuts locksmith expenses by 60%, demonstrating clear operational savings that reinforce adoption. Sunbelt projects benefit most because horizontal site plans allow builders to pre-stage Wi-Fi and power infrastructure that supports Wi-Fi-enabled deadbolts and hardwired mortise locks alike. These efficiencies push institutional investors to factor smart-access infrastructure into pro-forma underwriting, reinforcing multi-year tailwinds for the United States smart lock market.

UWB Passive-Entry Capabilities Embedded in Smartphones

Ultra-wideband chips inside every flagship iPhone and Android handset sold since 2025 enable centimeter-level ranging, letting doors unlock automatically as the user approaches. The Connectivity Standards Alliance finalized the Aliro protocol in 2024 to govern credential exchange for UWB-enabled locks, ensuring a phone credential issued by one brand can be read by another’s hardware. Aqara shipped the first Aliro-certified U400 lock in early 2025 and Schlage and Yale both announced mid-2026 launches. Eliminating the Bluetooth wake-up delay addresses a core user-experience pain point and brings electronic access parity with a mechanical key in perceived speed. As handset penetration climbs, passive entry is poised to become the default unlock method on premium models, lifting average selling prices in the United States smart lock market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Cyber-Security Vulnerabilities and Public Hacks | -1.4% | National, With Heightened Scrutiny in Tech-Savvy Metros | Short Term (≤ 2 Years) |

| Multi-Family Building Code Restrictions on Retrofit Devices | -1.1% | Urban Multifamily Markets Subject to IBC and NFPA Codes | Medium Term (2–4 Years) |

| Chip-Set Supply Constraints for Secure SoCs | -0.7% | National, All Manufacturers That Depend on Secure-Element Foundry Capacity | Short Term (≤ 2 Years) |

| Consumer Privacy Concerns Over Data Sharing | -0.6% | National, Amplified in CA and VA Where Stringent Privacy Laws Apply | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Persistent Cyber-Security Vulnerabilities and Public Hacks

Demonstrations at DEF CON 32 in 2024 showed cloning of hotel-lock RFID cards in under 60 seconds, while CVE disclosures during 2024-2025 exposed hard-coded keys and replay flaws in several consumer brands.[4]DEF CON Communications, “Cloning Hotel RFID Locks,” defcon.org Absent a mandatory federal certification regime, unlike the European ETSI TS 103 815 baseline, U.S. buyers rely on media reports and brand reputation to gauge device security. Each breach temporarily suppresses retail demand, especially among tech-savvy homeowners who fear door-unlock exploits. Manufacturers have responded with secure boot loaders and hardware-backed encryption, but SoC updates lengthen product cycles and raise bill-of-materials costs. Continued negative headlines therefore subtract momentum from the United States smart lock market even as feature innovation accelerates.

Multi-Family Building Code Restrictions on Retrofit Devices

International Building Code and NFPA 101 require that apartment entry doors retain 20- or 90-minute fire ratings verified through UL 10C tests, standards many battery-powered retrofits fail because plastic housings melt at elevated temperatures.[5]National Fire Protection Association, “NFPA 101 2024 Edition,” nfpa.org High-rise property managers instead specify hardwired electrified mortise locks that maintain mechanical failsafe egress during outages, limiting the addressable retrofit base in dense urban markets. ANSI/BHMA endurance tests further constrain low-cost hardware that cannot sustain 500 000 open-close cycles.[6]American National Standards Institute, “ANSI/BHMA A156.5,” ansi.org Consequently, retrofit vendors such as Wyze and SimpliSafe focus on single-family housing and smaller walk-up apartments exempt from stringent code oversight. This bifurcation caps retrofit volume growth and slows overall expansion of the United States smart lock market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mortise and Lever Formats Gain Commercial Traction

Deadbolts commanded 60.73% of United States smart lock market share in 2025, reflecting their ubiquity on single-family exterior doors. Mortise and lever formats, however, are forecast to grow at a 10.37% CAGR through 2031 as hotels, offices, and healthcare facilities prioritize Grade 1 mechanical robustness and code-compliant panic egress. The United States smart lock market size attributed to mortise platforms is projected to expand from USD 0.70 billion in 2026 to USD 1.15 billion by 2031, outpacing unit growth because commercial buyers accept higher average selling prices for durability and warranty coverage. Manufacturers now ship modular chassis that accept interchangeable trims, finishes, and credential modules, Wi-Fi, Thread, or Zigbee, reducing SKU count and smoothing installer logistics.

Lever-handle locks satisfy Americans with Disabilities Act clearance angles and one-hand egress rules, increasing adoption in elder-care facilities and public schools where building inspectors demand accessible hardware. Padlock-style smart locks remain a niche but resilient sub-segment, especially among logistics yards that need audit logs without drilling permanent holes into container doors. Meanwhile, rim locks attract multifamily renters who cannot alter door hardware, yet their surface-mount profile limits penetration into higher-income owner-occupied homes. Across every format, rapid iteration on battery-life optimization and Matter-over-Thread upgrades is blurring historical boundaries between commercial and consumer feature sets, sustaining momentum for product diversification inside the United States smart lock market.

By End-User: Commercial Hospitality and Corporate Segments Accelerate

Residential buyers generated 88.39% of 2025 revenue, but commercial deployments, in hospitality, retail, corporate campuses, education, and healthcare, are projected to post an 11.12% CAGR to 2031, twice the residential rate. Hotel chains migrating from RFID cards to mobile credentials show clear ROI: front-desk bypass improves guest satisfaction scores while reducing plastic card costs. Dormakaba’s Ambiance Cloud on-boarded over 500 hotels in 2025, and Vingcard’s VConnect added Apple and Google Wallet keys to legacy installations, confirming broad ecosystem uptake.

Corporate offices pivoting toward hot-desking rely on credentialed locks for office suites, phone booths, and lockers, linking access logs to occupancy analytics that inform real-estate consolidation decisions. Retail big-box stores deploy smart padlocks on warehouses and point-of-sale cash drawers, replacing manual key sign-outs. In healthcare, smart locks secure medication rooms to improve narcotics auditing under HIPAA, while universities integrate student ID systems to dormitory locks, automatically revoking credentials upon graduation or disciplinary action. This mosaic of commercial use cases captures higher recurring SaaS revenue per door than residential channels, lifting the blended average selling price and reinforcing revenue diversification across the United States smart lock industry.

By Installation Type: New-Construction Integration Reduces Retrofit Friction

Retrofit solutions represented 57.88% revenue share in 2025, leveraging an installed base of 100 million legacy doors nationwide. Yet builders now integrate locks during framing, allowing factory-milled bores, hidden wiring chases, and seamless integration with alarm and fire-panel circuits. The United States smart lock market size for new-construction deployments is projected to rise from USD 1.45 billion in 2026 to USD 2.40 billion by 2031, underscoring a 10.61% CAGR that outpaces retrofit growth. Installation labor falls from 45 minutes to below 10 minutes when doors arrive pre-drilled with strike plates aligned, which in turn reduces warranty claims for misaligned latches.

Build-to-rent single-family communities spearheaded by Lennar and DR Horton standardize locks across hundreds of homes, simplifying credential management for property managers and boosting take-rates for bundled smart-home service packages. Multifamily developers specify hardwired mortise locks that meet UL 10C fire ratings and tie into centralized credential platforms, avoiding the compliance pitfalls of battery-only retrofits. This divergence creates distinct go-to-market strategies: value-priced brands concentrate on DIY retrofit kits sold online, while enterprise-grade vendors court architects and general contractors during preconstruction design review, each reinforcing separate but parallel revenue flywheels inside the United States smart lock market.

By Distribution Channel: Direct-to-Consumer Brands Pressure Traditional Retail

Brick-and-mortar retail and professional installer networks retained 53.57% share in 2025, anchored by big-box chains such as Home Depot and Lowe’s that offer live product demos and in-aisle locksmith services. However, online channels are projected to grow at a 9.76% CAGR through 2031 as brands reduce wholesale margins and reinvest the spread into paid-search and influencer marketing. Amazon occupies a uniquely strategic position: it sells competing devices, certifies “Key-compatible” models for in-garage delivery, and cross-sells Ring doorbells and cloud storage, deepening platform lock-in.

Direct-to-consumer challengers, including Level Home, Lockly, and Wyze, eschew store shelves altogether, leveraging social media and unboxing videos to compress the awareness-to-purchase funnel. The approach trades physical trial for rapid iteration on firmware updates delivered over Wi-Fi, allowing these firms to roll out Matter or UWB features months ahead of brick-and-mortar cycles and sustain buzz among enthusiasts. Professional alarm installers such as ADT and Vivint protect their turf by bundling locks with monitoring contracts, effectively transforming hardware into a customer-acquisition subsidy. As online market penetration crosses 40%, retailers respond by offering installation add-ons and extended financing, blurring the historical distinctions between offline, online, and professional channels yet again inside the United States smart lock market.

Geography Analysis

Commercial research indicates that Sunbelt states, Texas, Florida, Arizona, Georgia, and North Carolina, generate the highest unit growth because build-to-rent developers cluster in regions with favorable land prices and year-round construction calendars. In these areas, new rental communities pre-install smart locks and bundle Wi-Fi, accelerating first-time purchases and inflating regional penetration rates above the national average. Insurance discounts offered by carriers such as Allstate and State Farm further amplify adoption in weather-exposed coastal zones, where storm-related claims can be mitigated by connected door sensors that verify secure closure during evacuations.

The Northeast registers slower volume growth because housing stock skews older and retrofits must comply with stringent municipal fire codes. Nonetheless, rising package theft in densely populated New York and Massachusetts suburbs is nudging homeowners toward keypad-enabled deadbolts that log delivery events, sustaining moderate replacement demand. The Midwest sits between these extremes: sprawling single-family lots reduce neighbor surveillance, so consumers value smartphone alerts and auto-locking features that compensate for longer police response times. Local utilities in Illinois and Minnesota also pilot demand-response programs that integrate thermostats with door-lock status, indirectly boosting the United States smart lock market by bundling energy rebates with security upgrades.

On the West Coast, California’s Title 24 energy-efficiency mandates encourage integrated home-automation packages that include locks, lighting, and HVAC control. Builders adopt smart-access products to accumulate LEED points, while tech-savvy consumers in Silicon Valley skew toward premium models with UWB passive entry. Wildfire evacuation zones in Northern California have also seen municipalities promote connected locks that can be remotely verified as unlocked for firefighter entry, although adoption remains niche. Across all regions, federal infrastructure spending on broadband improves rural connectivity, removing one of the last technical roadblocks to nationwide penetration of the United States smart lock market.

Competitive Landscape

ASSA ABLOY and Allegion jointly captured an estimated 45%-50% of United States smart lock market revenue in 2025, a level that creates moderate but not dominant concentration. ASSA ABLOY’s September 2024 acquisition of Level Home added an invisible, internal-mount technology that appeals to design-focused buyers unwilling to replace exterior hardware, expanding Yale’s target demographic. Allegion countered by spending USD 30 million on Gatewise in July 2025, gaining a cloud credential platform that resonates with multifamily operators seeking door-to-cloud integrations without on-premises servers. Both incumbents pursue patent portfolios around UWB ranging, filing more than 20 applications combined in 2024 to shield passive-entry intellectual property.

Price-disruptive challengers such as Wyze and SwitchBot set retail tags below USD 100, forcing premium brands to clarify value propositions around security certifications and ecosystem breadth. Lockly differentiates via 3-D fingerprint readers and offline encrypted PIN codes, catering to privacy-sensitive buyers wary of cloud dependence. Aqara and Anker’s Eufy round out the challenger cohort by bundling locks with hubs, contact sensors, and robot vacuums at 30%-40% lower price points than incumbents, leveraging vertical integration to squeeze gross margins.

Technology leadership continues to define competitive advantage: manufacturers race to ship Matter-over-Thread firmware updates, advertise Aliro certification for UWB credentials, and integrate Apple, Google, and Samsung wallets in a single SKU. Simultaneously, public vulnerability disclosures make cyber-security a marketing necessity; brands now tout penetration-test reports and bug-bounty programs to rebuild consumer trust. Component shortages for secure elements have narrowed SKU breadth since 2024, but supply normalization expected in 2026 should let firms re-engage in feature differentiation rather than rationing. These dynamics collectively sustain innovation velocity and support healthy rivalry within the United States smart lock market.

United States Smart Lock Industry Leaders

August Home Inc. (ASSA ABLOY AB)

Yale Home (ASSA ABLOY AB)

Kwikset (ASSA ABLOY AB)

Schlage (Allegion Company)

Level Home Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Allegion expanded the Schlage Encode Plus line with a mortise variant that supports Apple Home Key and Google Wallet and offers hardwired power for UL 10C-compliant multifamily deployments.

- December 2025: Yale unveiled the Assure Lock 3 featuring Matter-over-Thread networking and local storage for 250 user codes, shifting data control to the edge in response to privacy scrutiny.

- October 2025: Kwikset introduced the Zentra lock with NFC and UWB passive entry, earning the first Aliro certification in the residential category.

- August 2025: Kwikset launched Halo Select Plus and Aura Reach, both Matter-certified; Aura Reach adds an embedded Wi-Fi radio that eliminates separate bridges.

United States Smart Lock Market Report Scope

A smart lock is an electromechanical device used for locking that facilitates users in various industries to access and unlock the device remotely to enter the premises. Smart locks allow remote authentication to be verified and authorized users by providing access to smartphone connections and other smart devices through various communication technologies, like Wi-Fi, Bluetooth, Zigbee, or Z-Wave. The United States smart lock market is segmented on the basis of End-users that cover Residential as well as Commercial users and by Type of lock that covers Deadbolt, Padlock, and other types of locks such as Lever Handles and Mortise.

The United States Smart Lock Market Report is Segmented by Product Type (Deadbolt, Padlock, Mortise, Lever, Rim, Other Product Types), End-User (Residential (Single-Family, and Multi-Family), Commercial (Hospitality, Retail, Corporate Offices, Healthcare, Education and More)), Installation Type (Retrofit, New-Construction Integrated), and Distribution Channel (Online (Direct from Manufacturer, Marketplaces), Offline (Retailers, Professional Installers)). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Deadbolt |

| Padlock |

| Other Product Types (Mortise, Lever, Rim, etc.) |

By End-User

| Residential | Single-Family |

| Multi-Family | |

| Commercial | Hospitality |

| Retail | |

| Corporate Offices | |

| Healthcare | |

| Education and More |

By Installation Type

| Retrofit |

| New-Construction Integrated |

By Distribution Channel

| Online | Direct from Manufacturer |

| Marketplaces | |

| Offline | Retailers |

| Professional Installers |

| By Product Type | Deadbolt | |

| Padlock | ||

| Other Product Types (Mortise, Lever, Rim, etc.) | ||

| By End-User | Residential | Single-Family |

| Multi-Family | ||

| Commercial | Hospitality | |

| Retail | ||

| Corporate Offices | ||

| Healthcare | ||

| Education and More | ||

| By Installation Type | Retrofit | |

| New-Construction Integrated | ||

| By Distribution Channel | Online | Direct from Manufacturer |

| Marketplaces | ||

| Offline | Retailers | |

| Professional Installers | ||

Key Questions Answered in the Report

What is the forecast CAGR for the United States smart lock market between 2026 and 2031?

The market is projected to expand at a 9.22% CAGR from 2026 to 2031, rising from USD 3.88 billion in 2026 to USD 6.03 billion by 2031.

Which product configuration generated the highest revenue in 2025?

Deadbolt smart locks led with 60.73% share in 2025, reflecting their dominance on single-family exterior doors.

How fast are commercial installations growing compared with residential ones?

Commercial deployments in hospitality, retail, offices, and healthcare are forecast to post an 11.12% CAGR through 2031, roughly double the residential growth rate.

Why are Sunbelt states seeing especially strong adoption?

Institutional build-to-rent projects in Texas, Florida, Arizona, Georgia, and North Carolina install connected locks during construction, cutting retrofit labor and accelerating first-time purchases.

What does Matter 1.3 certification add to a smart lock?

Matter 1.3 lets locks work across Apple Home, Google Home, Amazon Alexa, and Samsung SmartThings without proprietary bridges, reducing complexity for new buyers.

Can installing a smart lock lower my homeowners-insurance premium?

Yes. Major carriers such as State Farm and Allstate offer premium discounts of about 2%-5% when policyholders verify the presence of qualified smart-security devices.

Page last updated on: