Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

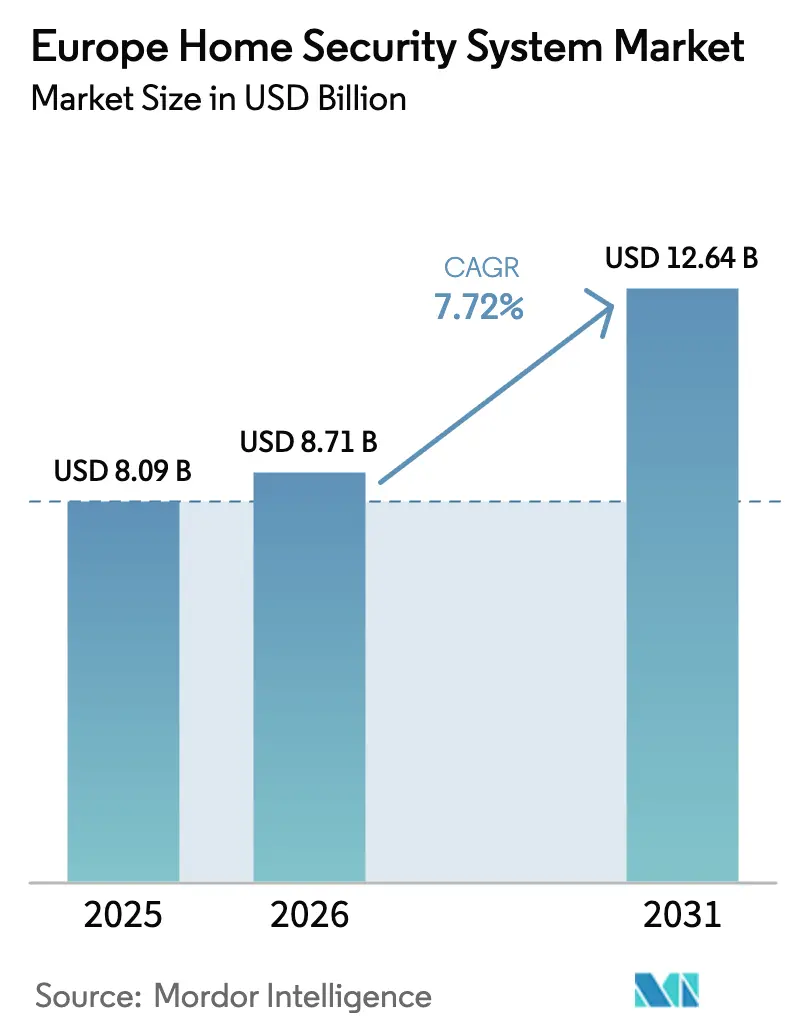

| Base Year Market Size (2025) | USD 8.09 Billion |

| Market Size (2026) | USD 8.71 Billion |

| Market Size (2031) | USD 12.64 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

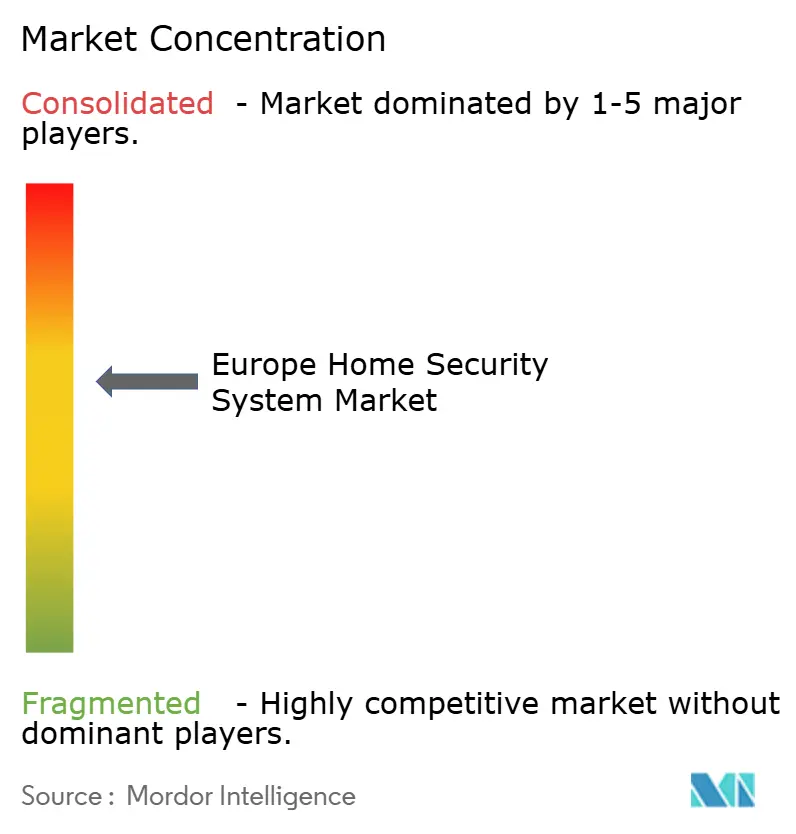

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Security System Market Analysis by Mordor Intelligence

Europe home security system market size in 2026 is estimated at USD 8.71 billion, growing from 2025 value of USD 8.09 billion with 2031 projections showing USD 12.64 billion, growing at 7.72% CAGR over 2026-2031. The market’s expansion is underpinned by mandatory insurance incentives, fast-rising adoption of IP cameras, and the growing preference for wireless, battery-powered devices that simplify retrofits across diverse European building stocks.[1]Verisure, “Annual Report 2024,” verisure.com Consumers increasingly value unified ecosystems that merge intrusion detection, video analytics, fire protection, and smart-home automation into a single, app-based interface. Hardware remains the revenue anchor, yet service revenues are accelerating as providers transition toward recurring monitoring and cloud analytics contracts that lock in long-term customer relationships. Competitive momentum favors vendors able to bundle equipment, software, and professional monitoring under subscription plans that align with European purchasing habits. Meanwhile, upcoming EU cyber-resilience regulations and carbon-monoxide alarm mandates are reshaping product roadmaps and pushing manufacturers to certify robust cybersecurity stacks and life-safety functions by mid-2026.

Key Report Takeaways

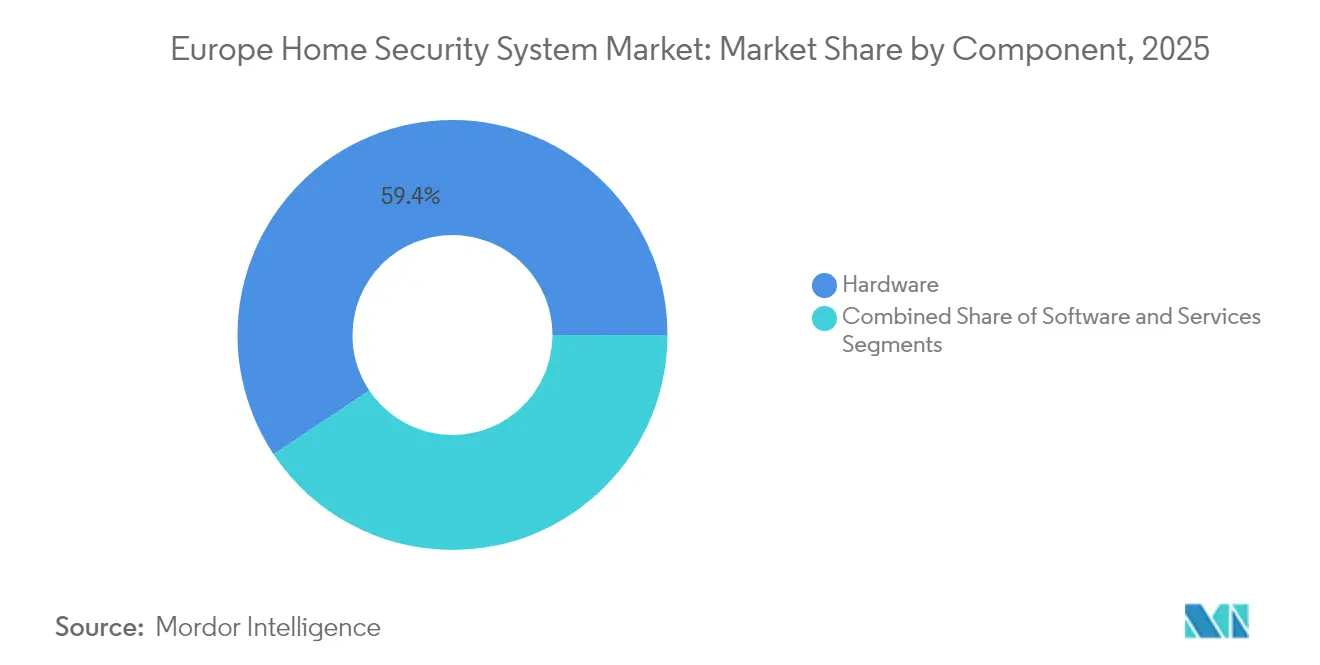

- By component, hardware accounted for 59.35% revenue share of the European home security system market in 2025; services are forecast to expand at a 8.67% CAGR through 2031.

- By system type, video surveillance systems led with 42.25% revenue share of the European home security system market in 2025; access-control systems are projected to grow at a 8.88% CAGR to 2031.

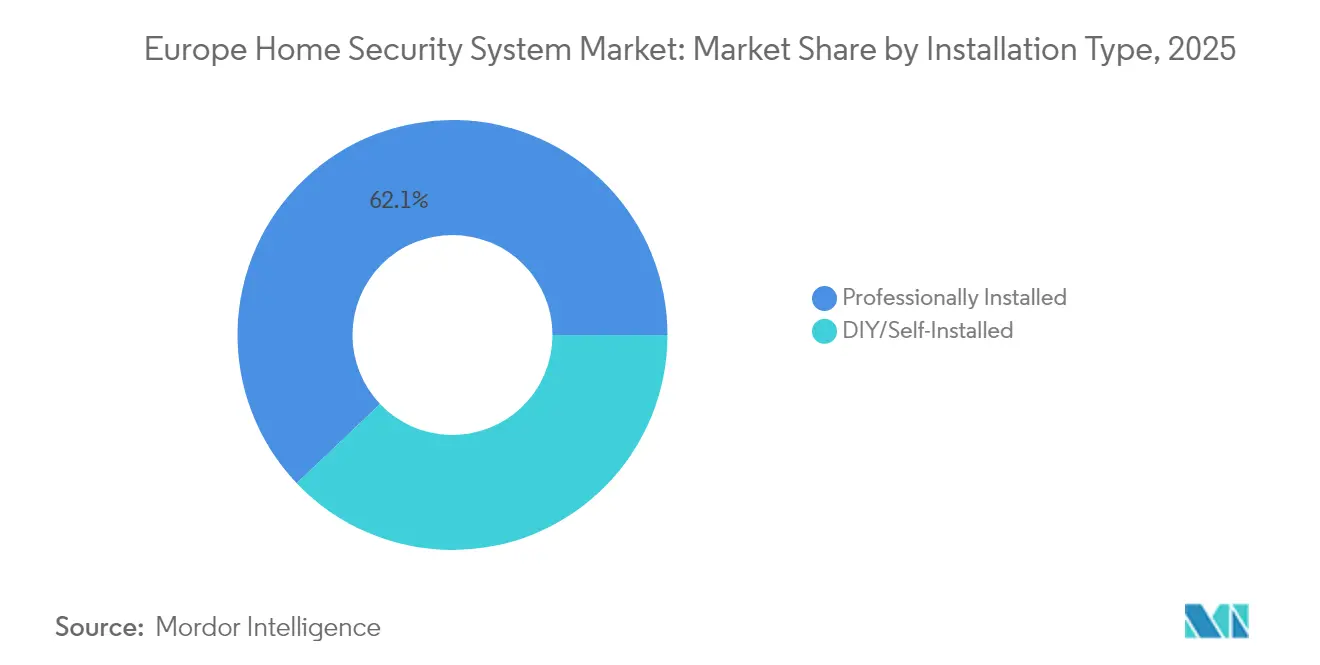

- By installation type, professionally installed solutions captured 62.10% share of the European home security system market in 2025; DIY/self-installed systems are expected to register an 8.55% CAGR over the forecast period.

- By communication technology, wireless deployments dominated with 63.55% share of the European home security system market in 2025; wireless also represents the fastest-growing segment at an 8.46% CAGR through 2031.

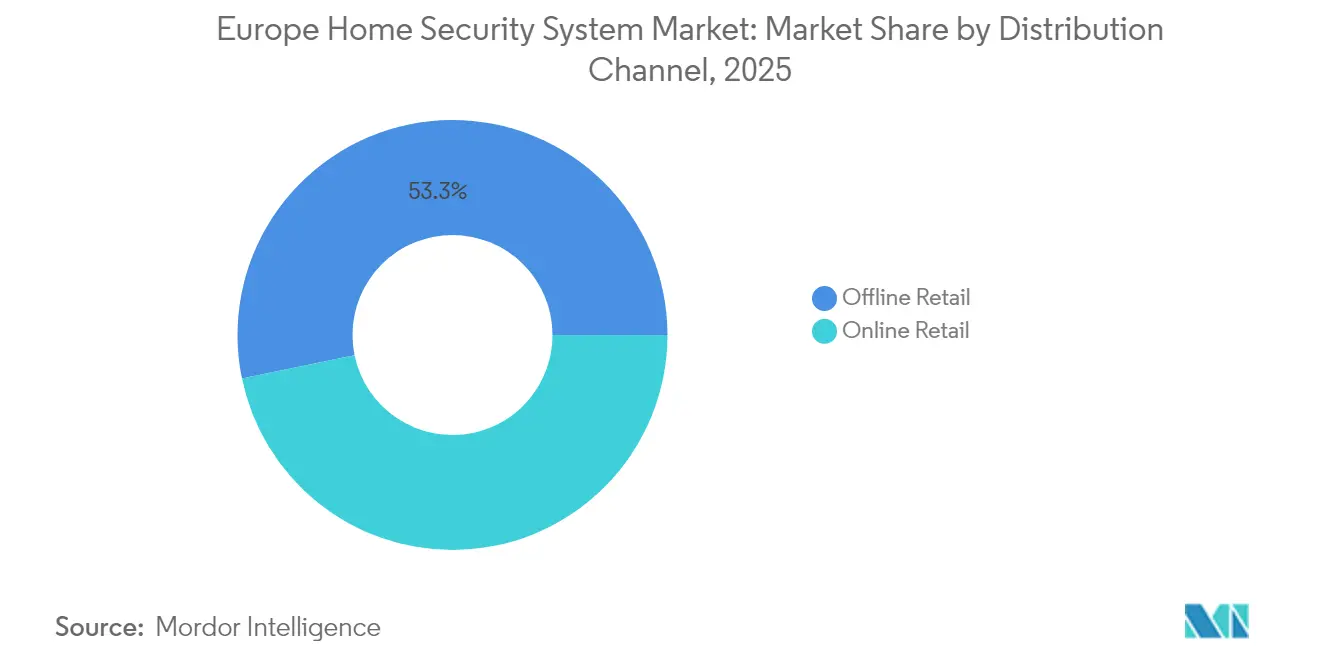

- By distribution channel, offline retail outlets held 53.25% revenue share of the European home security system market in 2025; online retail sales are anticipated to post a 8.79% CAGR to 2031.

- By end user, single-family homes generated 55.85% of the 2025 revenue of the European home security system market; multi-family apartments are set to record a 8.96% CAGR during the forecast window.

- By geography, Germany led with 30.15% market share of the European home security system market in 2025; Italy is poised to deliver the highest growth at a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Home Security System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid migration to IP-based cameras | +1.8% | Germany and the UK | Medium term (2-4 years) |

| Growing adoption of VSaaS | +1.5% | Core EU, expanding East | Long term (≥ 4 years) |

| Tightening insurance discounts for connected-home policies | +1.2% | Germany, France, Netherlands | Short term (≤ 2 years) |

| Smart-home bundling by telecom operators | +1.4% | Western Europe | Medium term (2-4 years) |

| Shift to wire-free multisensor hubs | +0.9% | Nordics and rural Europe | Long term (≥ 4 years) |

| Mandatory carbon-monoxide alarm mandates (EU 2026) | +0.7% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Migration to IP-Based Cameras

European households are decisively replacing analog CCTV with IP cameras that stream 4 MP-plus HDR video, offer AI-powered human and vehicle classification, and integrate seamlessly with cloud analytics engines. Ajax Systems’ launch of its IndoorCam Wi-Fi line illustrates this shift; the camera falls back to the firm’s proprietary radio protocol if Wi-Fi is lost, ensuring continuous alarm signaling.[2]Ajax Systems, “IndoorCam Product Sheet,” ajax.systems Insurance carriers in Germany and France now grant premium discounts of up to 15% on properties fitted with certified IP cameras that support video verification, accelerating adoption and reinforcing a virtuous cycle of increasing penetration.

Growing Adoption of Video-Surveillance-as-a-Service (VSaaS)

VSaaS converts large one-off equipment purchases into predictable monthly fees that bundle hardware, software, storage, and expert monitoring. European telecom operators have capitalized on this model by integrating cameras and analytics into broadband packages, thereby lifting average revenue per user and reducing churn. Property managers appreciate centralized administration of multi-unit buildings, while residents gain professional-grade security without high upfront costs. The recurring-revenue framework entices investors, as evidenced by Verisure’s planned initial public offering aimed at funding expansion in fragmented European territories.

Tightening EU Insurance Discounts for Connected-Home Policies

Insurers have demonstrated that connected alarm systems cut burglary claims by roughly 60%. As a result, leading German underwriters grant tiered premium reductions that scale with system sophistication from basic intrusion detection to fully monitored, AI-verified composite solutions. Similar models are rolling out in France and the Netherlands, pushing homeowners toward professional installations that satisfy both insurer and EU data-protection criteria.

Smart-Home Bundling by European Telecom Operators

Telecom players are packaging security hardware, monitoring, broadband, and television into single invoices, turning security into a sticky, high-margin add-on. SFR in France and Telefónica in Spain highlight this strategy, promoting turnkey installations completed by certified technicians and supported by nationwide service centers. Customers gain a unified bill, while operators defend market share against over-the-top competitors by deepening household lock-in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented wireless-protocol ecosystem | -0.8% | EU-wide | Medium term (2-4 years) |

| End-user privacy litigation risk | -1.1% | Germany, France, Nordics | Long term (≥ 4 years) |

| Low retrofit budgets in multi-family dwellings | -0.6% | Western European cities | Long term (≥ 4 years) |

| Skilled-installer shortage in rural Europe | -0.9% | Eastern and Southern rural regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Wireless-Protocol Ecosystem

European projects frequently juggle Wi-Fi, Zigbee, Z-Wave, Bluetooth Low Energy, Thread, and proprietary frequencies, forcing integrators to deploy multiple hubs or invest in complex bridges. Compatibility headaches inflate labor hours and complicate after-sales support, eroding installer margins. While the Matter standard promises relief, many major security OEMs prioritize proprietary stacks that preserve system lock-in and subscription revenue.

End-User Privacy Litigation Risk

GDPR enforcement has intensified, and homeowners can face fines if outdoor cameras capture public sidewalks without explicit signage. Vendors must offer privacy masking, on-device encryption, and short retention periods to reduce liability. Larger players can absorb compliance costs, but start-ups often struggle with the legal overhead associated with multi-country data-protection audits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Infrastructure Investment

Hardware held 59.35% of the Europe home security system market share in 2025, underscoring consumers’ desire for tangible assets cameras, locks, sirens, and sensors that physically protect property. The European home security system market size for hardware reached USD 4.80 billion in 2025 and is forecast to climb at a 7.26% CAGR, supported by the rapid replacement of analog cameras with IP models and heightened demand for multi-sensor hubs. Services remain the fastest-growing element, expected to add USD 1.21 billion in incremental value by 2031 as subscription models gain favor.

Heightened software sophistication is driving hardware design; AI modules embedded in edge devices now deliver object recognition and early-warning analytics locally, reducing cloud bandwidth requirements. Providers increasingly package hardware, firmware updates, and lifetime monitoring into five-year leasing contracts, reshaping revenue pools toward predictable annuities.

By System Type: Video Surveillance Leadership Reflects Consumer Priorities

Video surveillance accounted for 42.25% of 2025 revenue, equal to USD 3.42 billion of the European home security system market size, illustrating homeowners’ preference for visual verification to deter break-ins and facilitate insurance claims. Access-control solutions, smart locks, biometric pads, and video doorbells are poised to record a 8.88% CAGR as regulations encourage keyless entry for multi-family dwellings.

Alarm systems remain foundational, integrating magnetic contacts and PIR sensors that deliver instant alerts. Fire-protection platforms are benefiting from EU-wide life-safety legislation and the shift toward multi-threat detectors that monitor smoke, heat, and carbon monoxide in a single enclosure.

By Installation Type: Professional Services Maintain Market Leadership

Professionally installed products represented 62.10% of the Europe home security system market in 2025, largely because German and French insurers require certified placements for premium reductions. The European home security system market size tied to professional installation is projected to rise to USD 7.61 billion by 2031 at a 7.18% CAGR.

DIY penetration continues climbing in Scandinavia and the UK, where tech-savvy consumers appreciate quick, adhesive-mounted devices shipped directly from manufacturers. Hybrid models are emerging in which homeowners self-install entry-level kits, then upgrade to professional monitoring plans that layer on video analytics and cellular backup.

By Communication Technology: Wireless Solutions Drive Market Evolution

Wireless links captured 63.55% of 2025 revenue, equating to USD 5.14 billion of the European home security system market size, and should expand at an 8.46% CAGR through 2031 as battery life exceeds five years and RF range grows beyond 2 km in open air. Wired Ethernet remains crucial for high-bit-rate NVRs in luxury villas, yet overall momentum favors cable-free deployments in urban apartments where drilling is restricted.

Cellular fallback modules that pivot to Cat-M1 or NB-IoT during broadband outages are now standard on Grade 2 and Grade 3 panels. Next-generation LTE routers with embedded eSIMs deliver dual-SIM redundancy, meeting stringent EN 50136 signaling requirements for monitored alarms.

By Distribution Channel: Offline Retail Leadership Reflects Service Requirements

Specialty security shops and mass-merchandise retailers retained a 53.25% share because European buyers still prize in-store demos, expert advice, and installer referrals. Nevertheless, online revenues are compounding at 8.79% CAGR as brands such as Ajax Systems shift to D2C e-commerce storefronts across Germany, Italy, and the UK.

Marketplace platforms simplify cross-border sales inside the Schengen Area, while localized fulfillment centers cut delivery times to under 48 hours in most EU capitals.

By End User: Single-Family Homes Drive Primary Demand

Single-family residences generated 55.85% of revenue in 2025, supported by ample installation space and strong insurance incentives. Multi-family apartments, however, will post the fastest growth at 8.96% CAGR as developers pre-wire new towers for integrated video intercoms and cloud-connected access-control cores.

Small businesses, especially retail stores below 50 employees, rely on residential-grade solutions to satisfy EN 62676 video standards at cost-effective price points. Providers therefore design modular panels that scale from a two-door shop to a 32-zone estate without hardware change.

Geography Analysis

Germany led the European home security system market with a 30.15% share in 2025, propelled by high disposable incomes, rigorous EN 50131 certification norms, and insurance models rewarding monitored alarms with double-digit premium cuts. Strong professional-installer networks and familiarity with Grade 3 wireless systems fuel uptake of multi-sensor packages that merge burglary, fire, and medical monitoring.

Italy is the region’s momentum outlier, forecast at a 9.18% CAGR through 2031 as digitalization grants and urban densification lift demand for integrated access control in condominium complexes. Telecom operators there are bundling security subscriptions with FTTH contracts, enabling same-day installation across major metropolitan areas. Spain and France exhibit middle-single-digit growth anchored by telecom bundling and favorable insurer partnerships. The United Kingdom is leveraging its mature alarm monitoring infrastructure to accelerate cloud migrations, while the Netherlands and Sweden champion sustainable, low-power devices that dovetail with national carbon-neutrality goals. In Eastern Europe, Poland and Hungary are moving from rudimentary PIR-only systems toward full IP camera portfolios as GDP per capita climbs and EU cyber-resilience funding becomes available. Providers must therefore tailor product catalogs and price points to each country’s regulatory environment, average dwelling size, and installer density.

Competitive Landscape

Verisure, Securitas Direct, and ADT spearhead the market, collectively servicing more than 9 million European accounts through 24-hour monitoring centers and vertically integrated field-service teams. Verisure reported EUR 3.408 billion in 2024 revenue and intends to float shares publicly to finance pan-regional acquisitions, reflecting the capital intensity of scaling subscription platforms.[4]Verisure, “IPO Intent Statement,” verisure.com

Up-and-coming challenger Ajax Systems has captured share by offering wireless hubs, cloud-backed analytics, and five-minute self-install workflows that appeal to both consumers and underserved rural installers. The firm recently tapped UK distributor Eurotech to widen channel reach, strengthening its presence in a market that values BS EN 50131 compliance combined with stylish industrial design.

Technological differentiation centers on AI-assisted object recognition, sub-GHz mesh networks, and integrated cyber-hardening features that pre-empt 2026 EU mandates. Competitive intensity is rising as telecom operators cross-sell security bundles, while smaller manufacturers may exit or merge because of mounting compliance costs. Overall, the top five players account for roughly 45% of revenue, indicating a moderately consolidated field open to strategic partnerships and roll-ups.

Europe Home Security System Industry Leaders

Honeywell International Inc.

ADT Inc.

ASSA ABLOY AB

Bosch Service Solutions GmbH

Vivint Smart Home, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ajax Systems launched its AI-powered DoorBell, featuring 4 MP HDR imaging, a six-meter IR range, and on-device object recognition that cuts false alarms by segregating people, vehicles, and animals.

- March 2025: Ajax Systems introduced SIM cards optimized for alarm transmission, providing direct cellular routing independent of subscriber broadband.

- February 2025: Origin AI and Verisure partnered to embed Wi-Fi Sensing motion detection into Verisure’s platform, leveraging existing routers to add radar-like coverage without new sensors.

- February 2025: Investors LRM NV and Apixa injected capital into Secury360 to accelerate disruptive camera technology for European deployments.

- January 2025: Ajax Systems appointed Eurotech as its official UK distributor, augmenting the firm’s European network and local support footprint.

Europe Home Security System Market Report Scope

The home security system integrates software and hardware devices intended to detect an intrusion or unauthorized access if a secured zone is breached. There are many home security systems ranging from light sensors or security cameras to fully integrated smart home solutions. The market studied briefs about the ongoing technological trends in the region and provided key information regarding the regional companies.

By Component

| Hardware | Electronic Locks |

| Security Cameras | |

| Fire Sprinklers | |

| Window Sensors | |

| Door Sensors | |

| Other Hardware | |

| Software | |

| Services |

By System Type

| Video Surveillance Systems |

| Alarm Systems |

| Access-Control Systems |

| Fire-Protection Systems |

By Installation Type

| Professionally Installed |

| DIY/Self-Installed |

By Communication Technology

| Wired | |

| Wireless | Wi-Fi |

| Zigbee and Z-Wave | |

| Bluetooth LE | |

| Cellular / LTE |

By Distribution Channel

| Offline Retail | Specialty Stores |

| Mass Merchandisers | |

| Online Retail |

By End User

| Single-Family Homes |

| Multi-Family Apartments |

| Small Businesses (<50 employees) |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Rest of Europe |

| By Component | Hardware | Electronic Locks |

| Security Cameras | ||

| Fire Sprinklers | ||

| Window Sensors | ||

| Door Sensors | ||

| Other Hardware | ||

| Software | ||

| Services | ||

| By System Type | Video Surveillance Systems | |

| Alarm Systems | ||

| Access-Control Systems | ||

| Fire-Protection Systems | ||

| By Installation Type | Professionally Installed | |

| DIY/Self-Installed | ||

| By Communication Technology | Wired | |

| Wireless | Wi-Fi | |

| Zigbee and Z-Wave | ||

| Bluetooth LE | ||

| Cellular / LTE | ||

| By Distribution Channel | Offline Retail | Specialty Stores |

| Mass Merchandisers | ||

| Online Retail | ||

| By End User | Single-Family Homes | |

| Multi-Family Apartments | ||

| Small Businesses (<50 employees) | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will the Europe home security system market be by 2031?

It is projected to reach USD 12.64 billion, growing at a 7.72% CAGR from 2026.

Which component segment is expanding the fastest?

Services are forecast to post a 8.67% CAGR as subscriptions for monitoring and cloud analytics proliferate.

Which country leads the region today?

Germany holds 30.15% of 2025 revenue thanks to strict insurance incentives and mature installer networks.

Why are IP cameras displacing analog models?

Homeowners prefer higher-resolution video, AI event filtering, and cloud access; insurers also reward IP deployments with premium discounts.

How will EU regulations influence future product design?

The 2026 Cyber Resilience Act will require hardened cybersecurity and extensive vulnerability reporting, advantaging manufacturers with strong R&D budgets.

Page last updated on: