Digital Asset Custody Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.7 Trillion |

| Market Size (2031) | USD 2.12 Trillion |

| Growth Rate (2026 - 2031) | 24.67% CAGR |

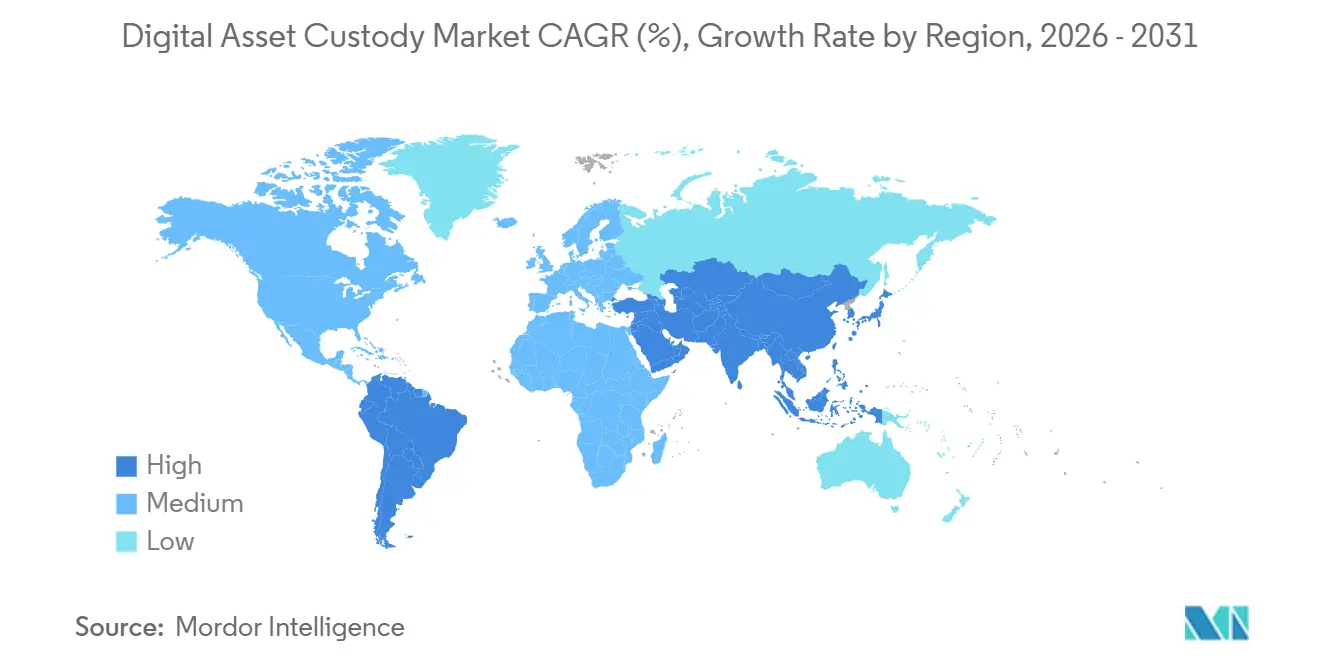

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

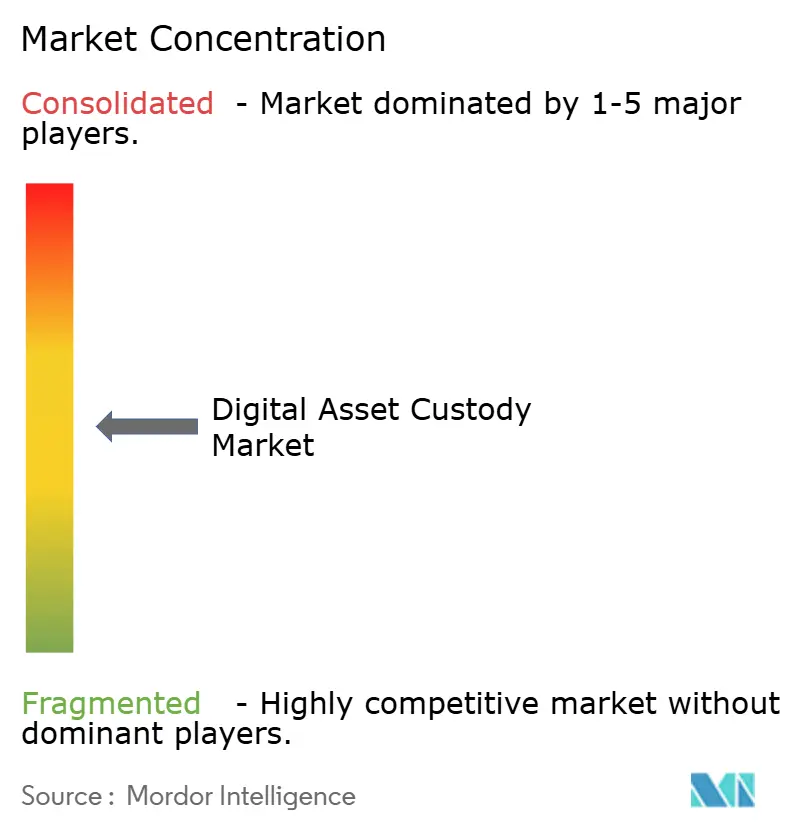

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Asset Custody Market Analysis by Mordor Intelligence

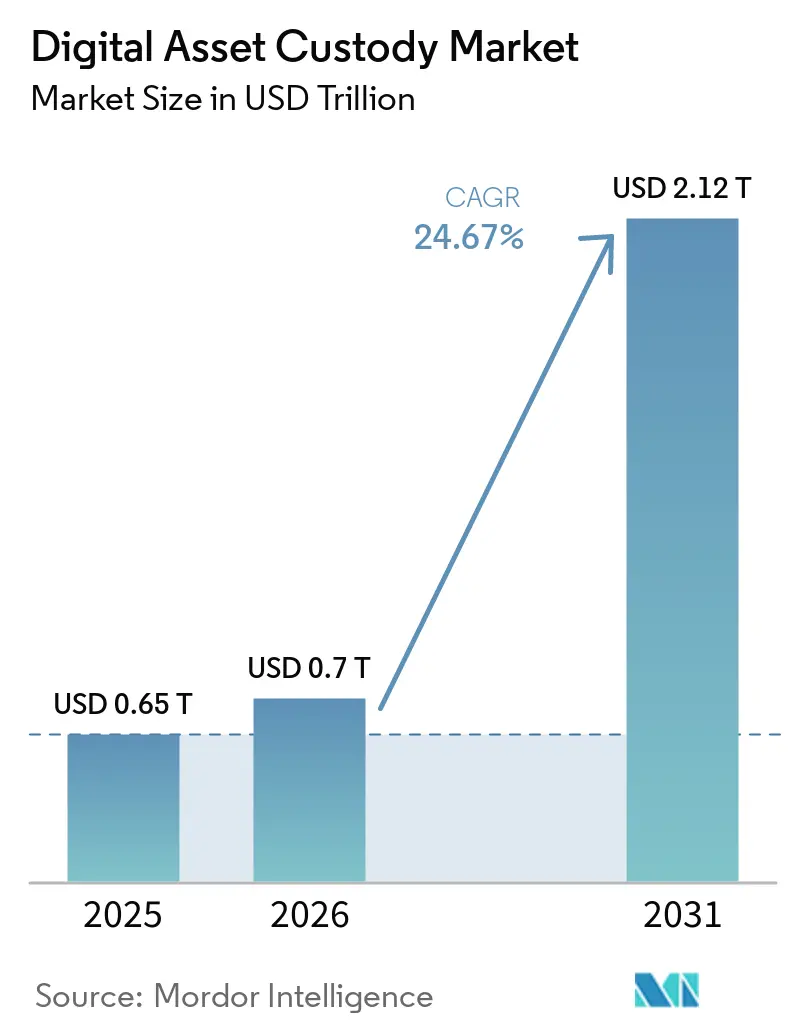

The Digital Asset Custody Market size is expected to increase from USD 0.65 trillion in 2025 to USD 0.70 trillion in 2026 and reach USD 2.12 trillion by 2031, growing at a CAGR of 24.67% over 2026-2031.

The digital asset custody market is expanding because regulated financial institutions can now participate more directly after the Securities and Exchange Commission (SEC) rescinded SAB 121, replaced by Staff Accounting Bulletin 122 in January 2025, which removed a major accounting barrier for bank-led custody models. The GENIUS Act, enacted in July 2025, also expanded the role of custody by setting federal standards for stablecoin reserve management, tying the digital asset custody market not only to crypto ownership but also to payment infrastructure and reserve safeguarding. BNY Mellon’s USD 59.4 trillion in assets under custody as of March 2026 shows how much the established custody scale can now move toward digital assets as regulation becomes clearer. The digital asset custody market is also benefiting from settlement modernization, as tokenized money and atomic settlement models are integrating custody into transaction execution rather than treating it as a separate back-office function. Competitive activity is rising at the same time, as banks, crypto-native custodians, and hybrid providers are all expanding into staking, collateral management, governance, and reporting layers to protect client relationships and improve fee capture in the digital asset custody market.

Key Report Takeaways

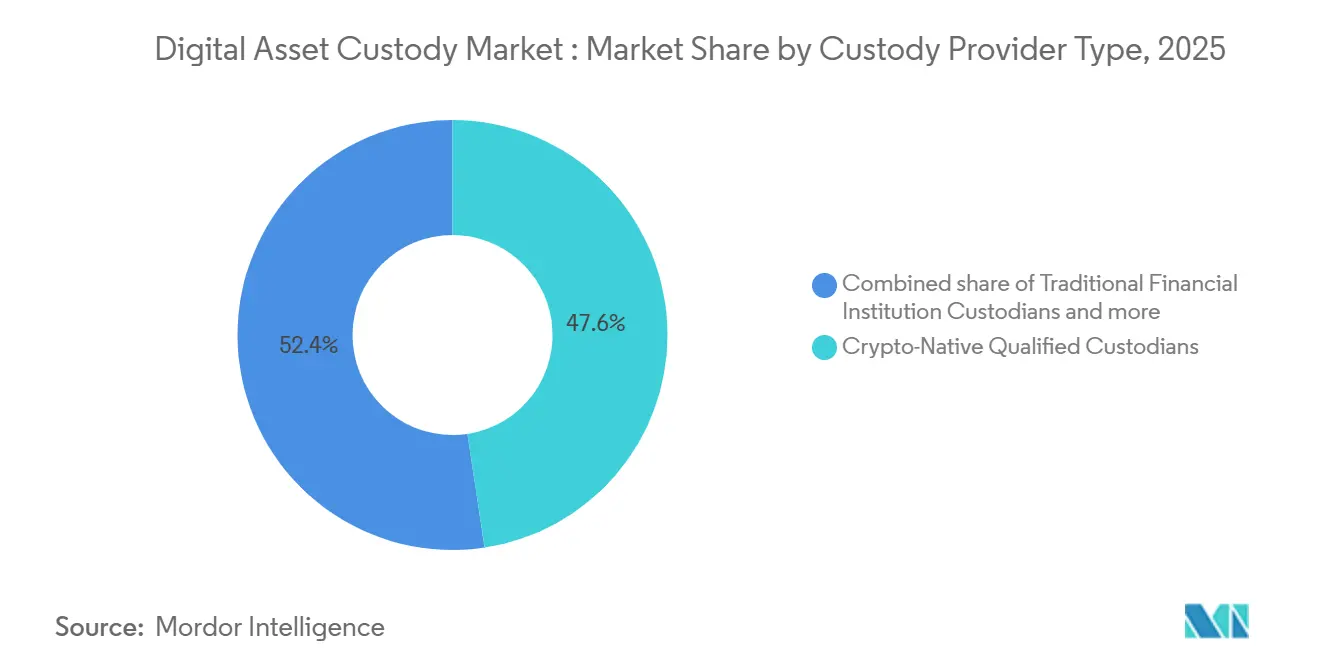

- By custody provider type, crypto-native qualified custodians held a 47.62% of the digital asset custody market share in 2025, while traditional financial institution custodians are projected to grow at a 27.87% CAGR through 2031.

- By asset class, cryptocurrencies captured 77.25% of the digital asset custody market share in 2025, while tokenized real-world assets and digital securities are projected to grow at 32.09% CAGR through 2031.

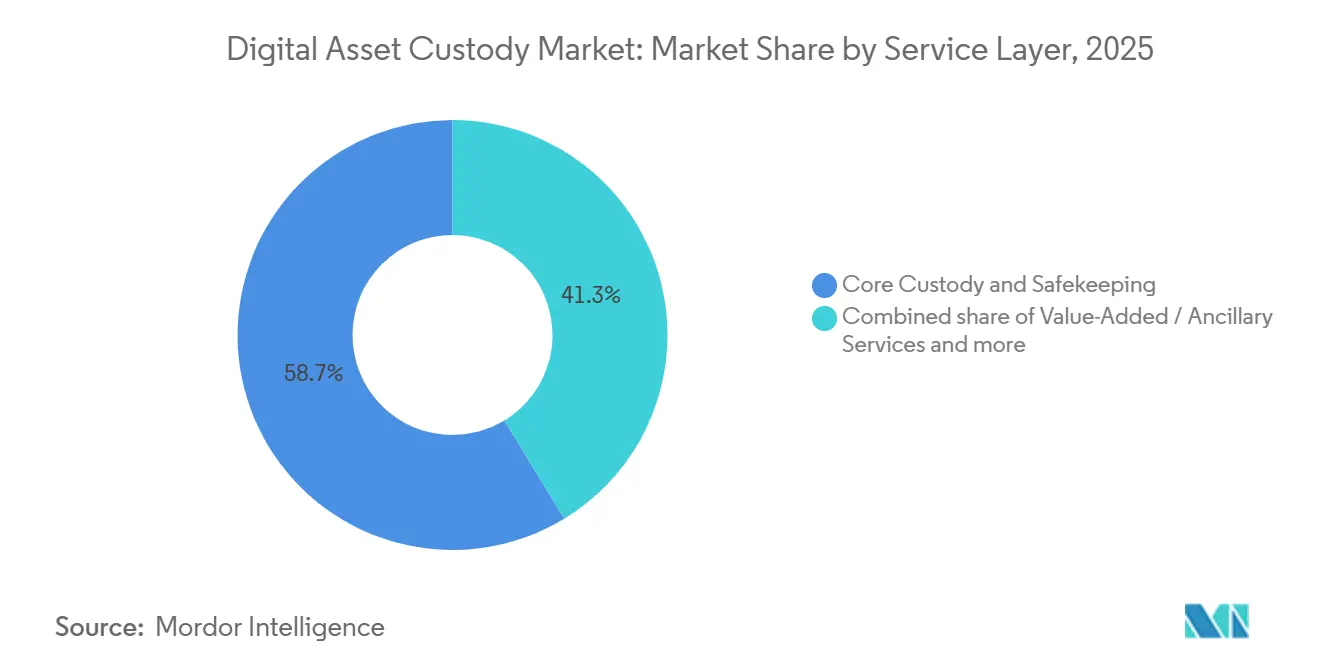

- By service layer, core custody and safekeeping accounted for 58.69% of the digital asset custody market share in 2025, while value-added and ancillary services are projected to grow at a 29.37% CAGR through 2031.

- By end user, traditional financial institutions held a 33.53% of the digital asset custody market share in 2025, while corporates and treasuries are projected to grow at a 28.47% CAGR through 2031.

- By geography, North America captured 45.77% of the digital asset custody market size in 2025, while Asia-Pacific is projected to grow at 27.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Asset Custody Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Institutional Allocation to Tokenized and Crypto Assets | +5.2% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Regulatory Recognition of Qualified Custody Models | +4.8% | North America and EU core, with spill-over to Asia-Pacific | Short term (≤ 2 years) to Medium term (2-4 years) |

| Insurance-Backed and Auditable Key Management Demand | +3.2% | Global | Medium term (2-4 years) |

| T+0 and Near-Real-Time Settlement Requirements for Tokenized Markets | +2.9% | Global, early gains in North America, Japan, and Singapore | Medium term (2-4 years) |

| Cross-Chain Asset Support and Interoperability Needs | +2.4% | Global, Asia-Pacific, and the EU leading infrastructure build-out | Medium term (2-4 years) to Long term (≥ 4 years) |

| Staking, Governance, and Asset Utilization Within Custody Rails | +2.1% | Asia-Pacific core, spill-over to North America and the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Institutional Allocation to Tokenized and Crypto Assets

Institutional demand remains one of the clearest growth engines for the digital asset custody market. In the United States, spot Bitcoin ETF mandates created a large and durable custody requirement because each product needs qualified safekeeping of the underlying assets. Coinbase Prime alone custodies assets for over 80% of the United States' Bitcoin and Ether ETFs, indicating that the digital asset custody market is increasingly tied to regulated fund channels rather than solely to direct token ownership[1]COINDESK.COM Coinbase's John D’Agostino says crypto platform stands alone as industry's full-service prime broker. This matters because custody relationships often remain in place even when trading activity or asset prices fluctuate, which makes the revenue base more durable than exchange volumes. The digital asset custody market is therefore moving closer to the behavior of institutional fund servicing, where infrastructure decisions are sticky and replacement risk is lower once operating, legal, and audit processes are established.

Regulatory Recognition of Qualified Custody Models

Regulatory recognition is reshaping the competitive landscape in the digital asset custody market. The OCC confirmed in 2025 that national banks may provide and outsource crypto asset custody and execution services, while the SEC’s SAB 122 restored ordinary fiduciary treatment instead of forcing bank custodians to carry client crypto as a balance-sheet liability. In Europe, MiCA established one of the clearest formal rule sets for custody providers and required client asset segregation on distributed ledgers, raising the operating standard for firms serving institutional mandates[2]State Street Corporation, “Digital Asset Regulation Accelerates in 2026,” State Street, statestreet.com. These changes not only reduce friction. They also increase the advantage of firms that already have capital, audit, reporting, and legal infrastructure in place. The digital asset custody market is therefore seeing a shift from open participation to a more filtered model where regulated scale matters much more than it did in earlier crypto cycles.

Insurance-Backed and Auditable Key Management Demand

Insurance and audit readiness are now central buying criteria in the digital asset custody market. Institutional clients want custody arrangements that can withstand operational reviews, cyber controls testing, and policy underwriting requirements, which makes key management architecture a commercial issue as much as a technical one. Liminal Custody’s HSM Vaults and Ledger’s enterprise hardware approach demonstrates how providers are aligning custody design with the certified hardware security requirements that large institutions increasingly require[3]Liminal Custody, “Liminal HSM Vaults, How Banks and Enterprises Can Secure Digital Assets with Certified HSM and MPC Technology,” Liminal Custody, liminalcustody.com. As more mandates move through regulated banks, asset managers, and treasury teams, the digital asset custody market is placing greater value on providers that can demonstrate documented controls rather than rely solely on broad security claims. This raises the barrier for smaller operators and supports a market structure where trust, certification, and process evidence matter as much as wallet functionality.

T+0 and Near-Real-Time Settlement Requirements for Tokenized Markets

Settlement expectations are rising, widening the role of the digital asset custody market. BIS Project Agorá showed in May 2026 that atomic settlement of wholesale cross-border transactions using tokenized central bank reserves and tokenized commercial bank deposits is technically workable, signaling that custody will increasingly sit within real-time settlement flows on[4]Bank for International Settlements, “Project Agorá Shows How Tokenization Can Improve Wholesale Cross-Border Payments,” BIS, bis.org. When assets, cash, and collateral all move on programmable rails, the custodian is no longer only a storage provider. It becomes a control point for transaction finality, asset movement, and risk management. The digital asset custody market, therefore, has an opportunity to capture more value from settlement-linked services, especially when clients want tokenized deposits, stablecoins, and securities workflows to operate together. That shift also favors providers with direct network connectivity and stronger institutional operating models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory Treatment Across Jurisdictions | -1.8% | Global, most acute for cross-border custody mandates spanning the United States, the EU, and Asia-Pacific | Medium term (2-4 years) |

| High Cost of MPC, HSM, Audit, and Insurance Infrastructure | -1.5% | Emerging markets, mid-tier custodians globally | Long term (≥ 4 years) |

| Limited Bankability of Non-Standard Assets and Protocol Risk Exposure | -1.2% | Global | Medium term (2-4 years) |

| Liability Ambiguity in Hybrid and Multi-Party Custody Structures | -1.0% | North America and the EU | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Treatment Across Jurisdictions

Cross-border inconsistency remains a real constraint on the digital asset custody market. Europe is moving under MiCA, the United States still operates through a combined SEC, OCC, and FDIC framework, and Asia-Pacific continues to rely on separate national models, which means multinational custody mandates often need jurisdiction-specific structures. ESMA highlighted uneven transitional arrangements across the EU in late 2025, and Canada’s OSFI added its own 2026 capital and liquidity treatment for crypto-asset exposures, which adds another layer of country-level compliance for banks active in custody. This raises legal, operational, and audit costs for any provider serving institutions across several markets. It also slows product rollout because firms often have to build separate entities, segregation, and reporting structures rather than one global model. The digital asset custody market will continue to grow, but regulatory fragmentation will favor larger providers that can absorb this complexity.

High Cost of MPC, HSM, Audit, and Insurance Infrastructure

The cost base of a qualified custodian remains high, which limits the depth of competition in the digital asset custody market. Providers must invest in multi-party computation, hardware security modules, audits, reporting systems, insurance coverage, and operational controls before scale economics fully emerge. BitGo’s 2026 post-quantum MPC transaction simulation shows that the investment cycle is not ending with today’s infrastructure, as security standards are already moving toward another generation of mandatory upgrades. These requirements weigh more heavily on mid-tier firms and regional operators than on large banks or well-funded crypto-native specialists. As a result, the digital asset custody market is likely to continue consolidating around firms that can spread compliance and security costs across a larger asset base and broader service revenue streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Custody Provider Type: TradFi Institutions Narrowing the Structural Gap

Crypto-native qualified custodians held 47.62% of the digital asset custody market in 2025, supported by early infrastructure development, wider token coverage, and strong relationships with funds, exchanges, and trading desks. They remain deeply embedded in ETF workflows and multi-chain asset handling, where execution speed and protocol access are critical. Firms like Anchorage Digital illustrate how this segment is moving beyond basic safekeeping into settlement and operating infrastructure. Their advantage also comes from faster product development and broader support for institutional use cases. Even as regulation becomes more favorable to banks, crypto-native custodians still retain a large installed base. That makes their position especially strong in workflows where flexibility and speed matter most. They are now defending that position by embedding more deeply into client operations rather than relying only on wallet security.

Traditional financial institution custodians are the fastest-growing provider type, with a projected CAGR of 27.87% from 2026 to 2031. This shift reflects the removal of key legal and accounting barriers and the need for banks to retain institutional clients within a single operating environment. The OCC’s 2025 guidance and SEC SAB 122 have improved banks’ ability to provide or outsource these services at client direction. Citigroup’s custody buildout shows that large financial institutions now see digital asset custody as a client retention issue rather than a side business. As these providers scale, blended offerings will become more common across fund administration, collateral, reporting, and safekeeping. Hybrid providers such as Fireblocks Trust bridge crypto-native and bank models by combining technology-led architecture with regulated custody frameworks. The market is increasingly rewarding firms that can offer both secure infrastructure and direct regulatory accountability.

By Asset Class: Cryptocurrencies Anchoring Revenue While RWAs Reshape the Mandate

Cryptocurrencies accounted for 77.25% of the digital asset custody market in 2025, making them the core revenue base across most custody models. Bitcoin and Ether remain central because institutional demand is deepest in those assets. ETF mandates, institutional trading, and cold storage programs all continue to route significant demand toward cryptocurrency custody. The legal, audit, and compliance ecosystems around major crypto assets are also more established than those for newer tokenized instruments. That lowers operational complexity for custodians and supports standardization of policies and controls. As a result, cryptocurrencies should remain the dominant source of custody revenue over the medium term. Even so, the market is gradually moving beyond this base as tokenized finance gains traction.

Tokenized real-world assets and digital securities are the fastest-growing asset class, with a projected CAGR of 32.09% from 2026 to 2031. These assets require custody models that support ownership records, transfer controls, and compliance rules that differ from open cryptocurrency networks. Tokenized funds, repo transactions, deposits, and treasury-linked instruments are pushing the market closer to securities-style servicing. BIS and IMF are working on tokenized finance, reinforcing the view that settlement and ownership infrastructure will continue to move toward the mainstream of wholesale finance. This creates more demand for providers with traditional securities backgrounds. It also increases the role of bank-affiliated custodians and hybrid firms in the segment. NFTs remain the smallest category because legal classification, transfer rights, and valuation treatment are still inconsistent across jurisdictions.

By Service Layer: Core Safekeeping Commoditizing as Value-Added Services Define Differentiation

Core custody and safekeeping held 58.69% of the market in 2025, which shows that secure storage still accounts for the largest share of current revenue. Institutions first need qualified safekeeping, private key control, segregation, and audit readiness before they can adopt higher-value services. Hardware-backed security, MPC design, and cold storage controls remain essential features for large mandates. However, the market is beginning to treat core safekeeping as a baseline capability rather than the sole reason to choose a provider. That means the service remains vital even as differentiation shifts elsewhere. Pure storage is still important, but it is no longer enough on its own to win institutional preference. Providers now need to show how custody connects with broader workflows.

Value-added and ancillary services are projected to grow at a CAGR of 29.37% between 2026 and 2031, making them the fastest-growing service layer. These services include staking, governance participation, collateral management, and off-exchange settlement. Sygnum’s Protect platform and Komainu’s CORE launch show how custody is becoming active infrastructure rather than passive storage. Institutions are increasingly willing to pay for models that keep assets productive while preserving control standards. Compliance, reporting, and risk management are also gaining ground because regulated clients need audit trails and regulator-ready outputs. This makes reporting infrastructure a revenue layer rather than just an internal support function. Providers that can combine custody with controls and workflow support are likely to gain the strongest institutional mandates.

By End User: Corporate Treasury Adoption Accelerating from Discretionary to Structural

Traditional financial institutions held 33.53% of the market in 2025, making them the largest end-user group. Their scale in ETFs, asset management, and institutional servicing creates strong repeat demand for custody services. These users also impose the strictest requirements around segregation, reporting, and compliance. That helps shape market standards across the broader industry. Other important users include hedge funds, family offices, and crypto-native platforms. Each group has different needs, ranging from active trading integration to custom control structures. The market, therefore, remains segmented by operating model rather than offering one uniform custody product.

Corporates and treasuries are the fastest-growing end-user segment, with a projected CAGR of 28.47% from 2026 to 2031. Digital assets are increasingly being folded into cash management, collateral, and treasury workflows. Ripple’s acquisition of GTreasury and the integration of XRP and RLUSD into treasury systems reflect this shift. Stablecoin reserve structures also support broader adoption because compliant reserves require regulated custody of underlying assets. That expands demand beyond speculative or investment-led use cases. It also pushes custody closer to core enterprise finance systems. Over time, custody is likely to become a standard treasury control rather than a specialist digital asset function.

Geography Analysis

North America held 45.77% of the digital asset custody market share in 2025, maintaining its leading regional position. The region benefited from a sharp change in regulatory posture after SAB 122, OCC Interpretive Letter 1184, and the GENIUS Act improved the framework for bank-affiliated and institutional custody services. The United States also remains the center of spot Bitcoin ETF custody activity, which strengthens the role of a small number of large providers in the regional digital asset custody market. Canada is also relevant because OSFI’s 2026 crypto-asset exposure guideline aligned domestic supervision more closely with Basel-style treatment for banks active in this field. South America remains a smaller part of the digital asset custody market. Still, inflationary pressures and demand for Bitcoin and stablecoin holdings continue to support interest among corporates and wealthy investors, as institutional frameworks are still developing.

Europe remains the most prescriptive regulatory environment in the digital asset custody market, and that has created both a growth base and a concentration filter. MiCA’s segregation requirements and the end of the transitional period for CASPs by July 1, 2026, raised the compliance threshold for firms serving institutional clients across the region. Luxembourg’s Blockchain Law IV also added flexibility for tokenized securities structures, which supports custody requirements for funds and structured financial products. As a result, the European digital asset custody market is likely to favor fully licensed operators with stronger legal control and reporting capabilities over smaller firms with narrower operating models.

Asia-Pacific is the fastest-growing region in the digital asset custody market and is forecast to expand at a 27.41% CAGR between 2026 and 2031. Japan’s finalized custody and stablecoin guidelines, effective July 2026, and Hong Kong’s move toward a dedicated virtual asset custodian licensing regime are providing the region with a more formal operating structure for institutional participation. In the Middle East and Africa, BNY Mellon’s strategic collaboration in Abu Dhabi Global Market shows that large global custodians are beginning to treat the Gulf as a meaningful location for regulated digital asset servicing. The digital asset custody market is therefore widening geographically, but growth is strongest where licensing, reserve rules, and tokenized finance frameworks are moving from consultation to operational implementation.

Competitive Landscape

The digital asset custody market is moderately concentrated, with a few very visible leaders in specific institutional channels. However, it is still broader and more fragmented once the field moves beyond top ETF and bank mandates. Coinbase Prime’s role across the United States Bitcoin and Ether ETF structures, and BNY Mellon’s existing global custody scale, illustrate how large incumbents can dominate high-profile institutional flows even as the full market still includes many smaller participants. Below that top tier, the digital asset custody market includes crypto-native custodians, bank-affiliated units, and hybrid infrastructure firms that compete on charter status, asset support, reporting quality, and value-added services. This means competitive intensity is high, but it is not uniform across all client types or asset classes. Some providers are strongest in ETFs, others in off-exchange collateral, and others in tokenized finance workflows.

Strategic moves in 2025 and 2026 show how providers are expanding their roles. BitGo expanded qualified custody support for Canton Network CIP-56 assets, positioning it more directly within permissioned institutional blockchain ecosystems rather than solely in open-network crypto custody. Komainu launched Komainu CORE to support collateral-as-a-service, which moves custody further into active trading and default management workflows. BNY Mellon also expanded its digital asset position through a strategic collaboration in Abu Dhabi, which shows how incumbent custody banks are linking digital assets to broader cross-border infrastructure expansion. These examples show that the digital asset custody market is no longer competing only on safekeeping. It is competing on where custody sits inside settlement, collateral, and regulated product infrastructure.

Security architecture is another major competitive line in the digital asset custody market. BitGo’s post-quantum MPC simulation in 2026 set a clear marker for future-proof custody design. It signaled that firms will need to prepare for another cycle of security investment even as current systems mature. Fireblocks Trust and other hybrid models show that infrastructure providers are also moving closer to the regulated custody edge rather than remaining solely back-end technology vendors. At the same time, the digital asset custody market still has room for improvement in multi-chain collateral mobility, as clients want assets to move across networks without creating separate compliance, bridge, or counterparty risks. Providers that can combine regulated status, chain interoperability, and institutional operating controls are likely to improve their position fastest over the next few years.

Digital Asset Custody Industry Leaders

Coinbase Global, Inc.

BitGo, Inc.

Anchorage Digital Bank N.A.

Fidelity Digital Asset Services, LLC

The Bank of New York Mellon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: BNY Mellon announced a strategic collaboration with Finstreet and ADI Foundation to deliver regulated institutional-grade digital asset custody anchored in the Abu Dhabi Global Market, initially for Bitcoin and Ether, with planned expansion to stablecoins and tokenized assets. BNY oversees USD 59.4 trillion in assets under custody as of March 2026, making this the most significant Tier-1 custodian commitment to MEA digital asset infrastructure to date.

- May 2026: BitGo extended its Canton Network infrastructure to support CIP-56 token-standard assets, including USDCx and cBTC, enabling qualified custody and management of institutional financial assets built on this standard. BitGo first launched Canton Coin custody in October 2025, expanding the ecosystem to the full institutional asset class within six months.

- April 2026: Komainu launched Komainu CORE, a Collateral-as-a-Service offering that positions Komainu as an independent custodian for asset safeguarding and liquidation facilitation, targeting institutional trading firms and asset managers that require regulated collateral infrastructure.

- February 2026: BitGo and Silence Laboratories completed the first post-quantum MPC transaction simulation by a regulated custodian, using MPC-based wallet infrastructure aligned with post-quantum security standards. The companies plan continued development with select financial institutions as NIST post-quantum standards mature.

Global Digital Asset Custody Market Report Scope

| Traditional Financial Institution Custodians |

| Crypto-Native Qualified Custodians |

| Hybrid / Advanced Key Management Providers |

| Cryptocurrencies |

| Tokenized Real-World Assets (RWAs) and Digital Securities |

| Non-Fungible Tokens (NFTs) and Unique Digital Assets |

| Core Custody and Safekeeping |

| Value-Added / Ancillary Services |

| Compliance, Reporting and Risk Management |

| Traditional Financial Institutions |

| Alternative Asset Managers and Hedge Funds |

| Family Offices and HNWI / UHNWI |

| Crypto-Native Platforms & Exchanges |

| Corporates & Treasuries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Custody Provider Type | Traditional Financial Institution Custodians | |

| Crypto-Native Qualified Custodians | ||

| Hybrid / Advanced Key Management Providers | ||

| By Asset Class | Cryptocurrencies | |

| Tokenized Real-World Assets (RWAs) and Digital Securities | ||

| Non-Fungible Tokens (NFTs) and Unique Digital Assets | ||

| By Service Layer | Core Custody and Safekeeping | |

| Value-Added / Ancillary Services | ||

| Compliance, Reporting and Risk Management | ||

| By End User | Traditional Financial Institutions | |

| Alternative Asset Managers and Hedge Funds | ||

| Family Offices and HNWI / UHNWI | ||

| Crypto-Native Platforms & Exchanges | ||

| Corporates & Treasuries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in digital asset custody through 2031?

Growth is being supported by clearer regulation, stablecoin reserve custody requirements, ETF-related asset safekeeping, and the move toward tokenized settlement infrastructure. The market is projected to rise from USD 702.62 billion in 2026 to USD 2,116.07 billion by 2031 at a 24.67% CAGR.

Which region leads today and which one is growing fastest?

North America led with 45.77% share in 2025 because of United States regulatory progress and ETF custody activity. Asia-Pacific is the fastest-growing region with a forecast CAGR of 27.41% between 2026 and 2031.

Which asset category is expected to grow the fastest?

Tokenized Real-World Assets and Digital Securities are forecast to grow the fastest at a 32.09% CAGR during 2026-2031. Cryptocurrencies still led in 2025 with 77.25% share.

Why are banks becoming more active in this space now?

Banks gained a clearer path after the SEC rescinded SAB 121 through SAB 122 and after the OCC confirmed that national banks may provide or outsource crypto custody. This is helping Traditional Financial Institution Custodians become the fastest-growing provider type at 27.87% CAGR.

How is custody shifting beyond basic safekeeping?

Providers are adding collateral management, staking, governance, and off-exchange settlement services. That is why Value-Added and Ancillary Services are projected to grow at 29.37% CAGR, faster than core safekeeping.

Why are corporates and treasury teams becoming important clients?

Stablecoin reserve rules and treasury software integration are making digital assets more relevant to finance teams. Corporates and Treasuries are therefore the fastest-growing end-user segment, with a 28.47% CAGR through 2031.

Page last updated on: