United Kingdom Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

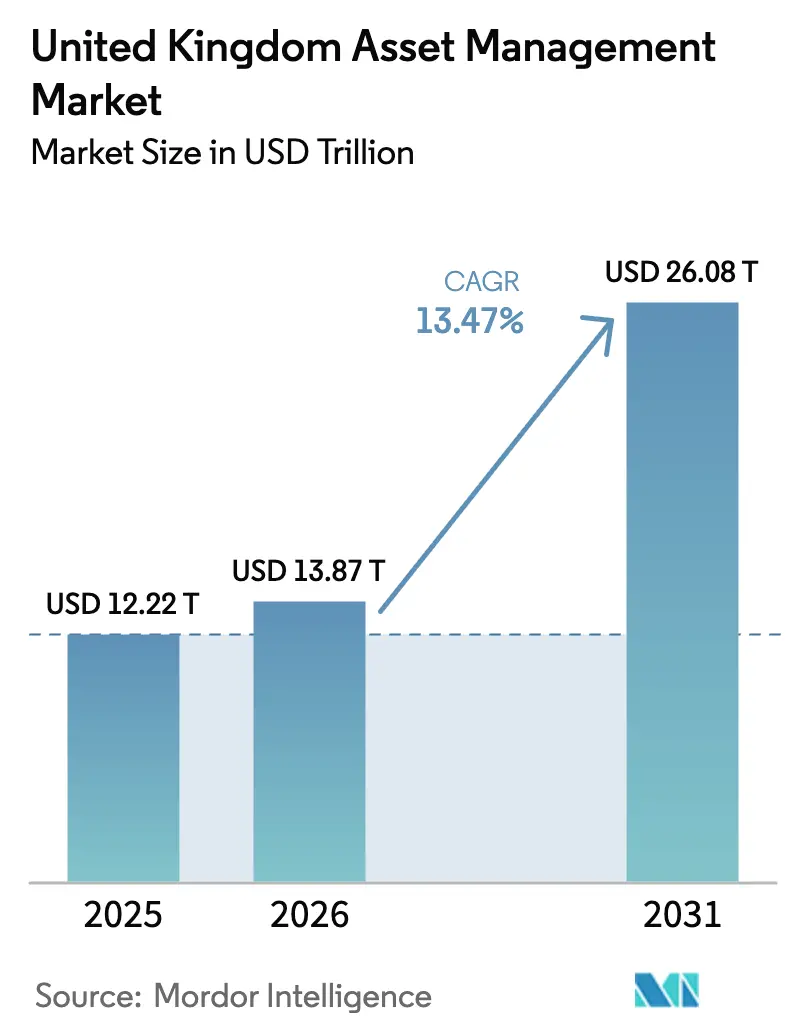

| Base Year Market Size (2025) | USD 12.22 Trillion |

| Market Size (2026) | USD 13.87 Trillion |

| Market Size (2031) | USD 26.08 Trillion |

| Growth Rate (2026 - 2031) | 13.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Asset Management Market Analysis by Mordor Intelligence

The United Kingdom Asset Management Market size was valued at USD 12.22 trillion in 2025 and is estimated to grow from USD 13.87 trillion in 2026 to reach USD 26.08 trillion by 2031, at a CAGR of 13.47% during the forecast period (2026-2031).

The United Kingdom asset management market is experiencing strong growth driven by a structural shift in client composition and investment preferences. Increasingly, institutional investors are rotating toward private markets and illiquid strategies, seeking inflation-adjusted returns and diversification beyond traditional portfolios. Retail investors are also playing a larger role, fueled by the rapid adoption of digital-first investing platforms that make market access easier and more engaging. Overseas mandates are taking up a growing share of assets, integrating the United Kingdom more closely with global capital flows and attracting cross-border investments. Regulatory reforms, including changes to the ISA framework and the Long-Term Asset Fund regime, are opening new pathways for retail and defined contribution investors to access alternative investments. The industry has stabilized after previous market shocks, with improved governance and liquidity safeguards reinforcing investor confidence. Wealth advisory firms and hybrid robo-advisory models are expanding rapidly, capturing market share from traditional banks by catering to evolving investor needs. Private markets and alternative assets are increasingly popular as investors seek long-term growth and diversified exposure. Strategic partnerships between United Kingdom managers and global asset originators are enabling access to new opportunities and innovative investment products.

Key Report Takeaways

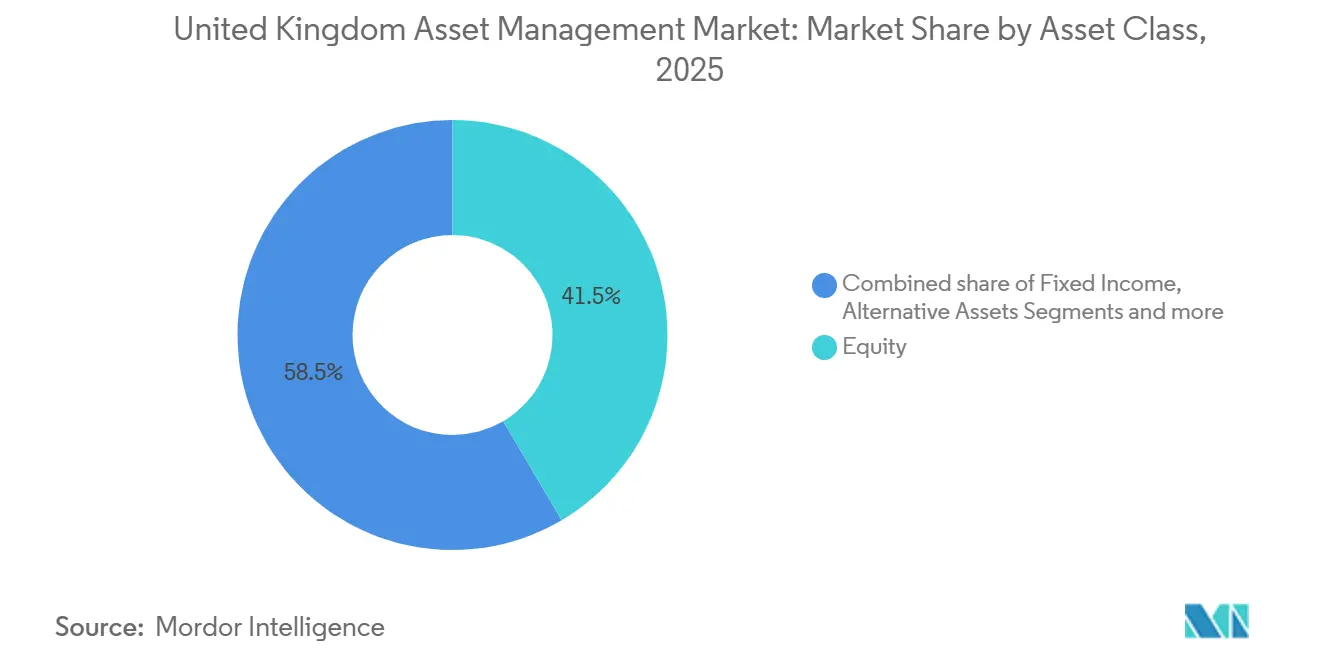

- By asset class, equity led with 41.52% of the United Kingdom asset management market share in 2025, while alternative assets are projected to expand at a 15.44% CAGR through 2031.

- By firm type, banks held 39.83% of the United Kingdom asset management market share in 2025, and wealth advisory firms and RIAs are projected to grow at a 14.96% CAGR through 2031.

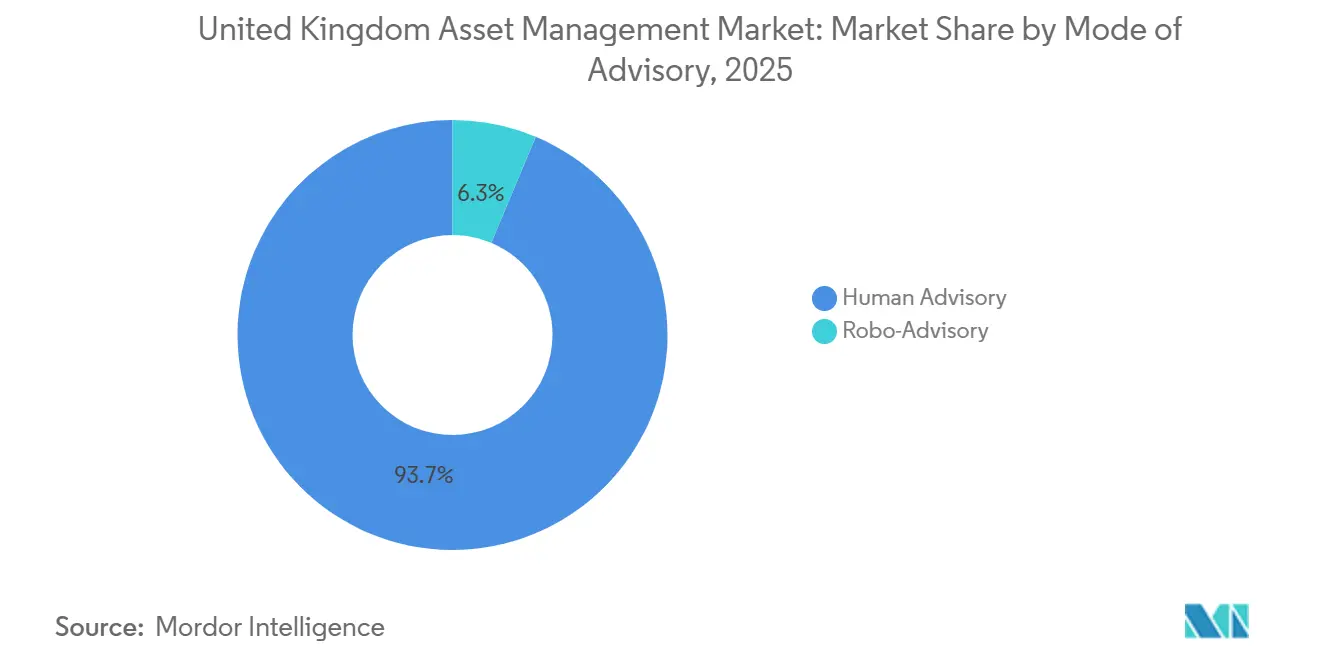

- By mode of advisory, human advisory accounted for 93.67% of the United Kingdom asset management market share in 2025, while robo-advisory is projected to grow at a 20.63% CAGR through 2031.

- By client type, institutional investors controlled 73.52% of the United Kingdom asset management market share in 2025, and retail is projected to grow at a 17.89% CAGR through 2031.

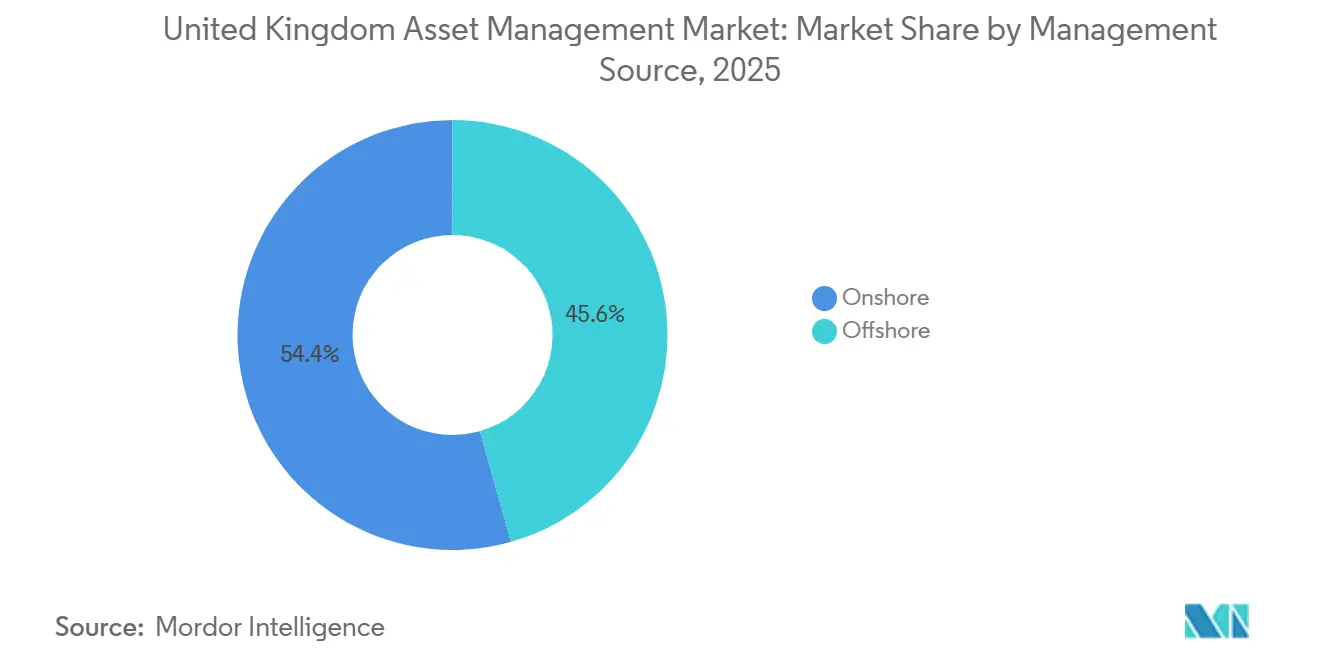

- By management source, onshore-managed assets held 54.39% of the United Kingdom asset management market share in 2025, and offshore-delegated assets are projected to grow at a 14.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Overseas Mandates Drive United Kingdom Asset Management Growth | +2.8% | Global, with concentration in Europe and emerging Asia Pacific markets | Medium term (2-4 years) |

| Rise of private markets & alternatives allocations | +3.1% | Global core institutional; APAC core with spillover to United Kingdom DC schemes via LTAFs | Medium term (2-4 years) |

| Digital-first retail investing & fractional shares | +1.9% | National, with early gains in London, Manchester, and Edinburgh, fintech hubs | Short term (≤ 2 years) |

| Accelerating ESG / SDR-labelled fund inflows | +1.4% | Europe and the United Kingdom, with regulatory alignment between the European SFDR and the United Kingdom SDR frameworks | Long term (≥ 4 years) |

| Tokenised fund structures are gaining FCA sandbox slots | +0.9% | The national pilot stage focused on the City of London and Edinburgh fintech clusters | Long term (≥ 4 years) |

| LTAF regime unlocking DC access to illiquids | +2.4% | National, with policy focus on the United Kingdom allocations per Mansion House Accord | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Overseas Mandates Drive United Kingdom Asset Management Growth

In 2024, international client assets surpassed domestic assets for the first time, reaching a majority share of United Kingdom-managed assets and signaling a structural shift in the market. This change has prompted United Kingdom asset managers to rethink client servicing, pricing strategies, and regulatory navigation to cater to a more global investor base. European mandates rebounded strongly, reflecting renewed confidence in United Kingdom-based managers to oversee continental portfolios. Strategic collaborations are reinforcing this trend, such as M&G’s multi-year partnership with Dai-ichi Life and Legal & General’s expansion of its global real estate platform through acquisitions and minority stakes. These initiatives demonstrate how United Kingdom managers are increasingly linking with European and Asian pools of capital while leveraging the country’s operational hubs and professional talent. Policy developments, including upcoming AIFM reforms and Europe’s AIFMD II timetable, are shaping delegation models and cross-border market access, influencing how international mandates are structured[1]The Investment Association, “Investment Management Survey 2024–2025,” The Investment Association, theia.org.

Rise of Private Markets & Alternatives Allocations

Private markets and alternative assets are increasingly central to institutional investment strategies, as investors seek long-term, inflation-adjusted returns and portfolios aligned with their liquidity and liability requirements. Leading United Kingdom managers are scaling capabilities across private equity, infrastructure, private debt, and real estate, reflecting strong resilience in evolving market conditions. The Long-Term Asset Fund regime is enabling both retail and defined contribution investors to access diversified private strategies. Enhanced governance, oversight, and fund design are making these investments more secure and accessible for long-term savers. Institutional demand is driving innovation in fund structures and investment approaches to meet evolving investor needs. This trend is reshaping portfolio allocation, with private markets taking a larger role relative to traditional public market strategies. United Kingdom managers are leveraging their expertise and operational hubs to capture this growing demand.

Digital-First Retail Investing & Fractional Shares

Fintech upgrades and regulatory changes are lowering entry barriers to retail investing and laying the foundation for steady participation growth. The FCA enabled the holding of fractional interests in Stocks and Shares ISAs, Junior ISAs, and Child Trust Funds from October 2024, removing a constraint that had previously limited the tax efficiency of fractional investing for many households[2]HM Government, “Individual Savings Account and Child Trust Funds (Amendment No 2) Regulations 2024,” GOV.UK. Building on this, HSBC launched a new solution in 2025 that enables fractional dealing and custody for all LSE-listed ETFs, making it easier for retail investors to access ETFs on a fractional basis through platforms and wealth managers[3]ETF Express, “HSBC launches fractional shares offering for all LSE‑listed ETFs,” etfexpress.com. The offering supports more efficient execution for smaller transactions, addresses challenges such as cash drag and unit rounding, and targets millions of United Kingdom ETF investors. The United Kingdom retail investing pool is substantial, and policy initiatives such as the Leeds Reforms and the FCA’s Targeted Support regime aim to help households move idle cash into diversified investments. Together, these developments create a durable retail tailwind for the United Kingdom asset management market. Managers can capitalize on this by providing simple, intuitive investing journeys, clear guidance, and risk-aligned guardrails.

Accelerating ESG / SDR-labelled Fund Inflows

The introduction of the United Kingdom Sustainability Disclosure Requirements has established voluntary labels and anti-greenwashing standards, creating clear criteria for Focus, Improvers, Impact, and Mixed Goals funds. By late 2025, a significant number of funds had secured SDR labels, reflecting a strong commitment to transparency and credibility in sustainability claims. The FCA’s phased approach, which delayed the application of SDRs to portfolio and wealth managers, allowed the fund channel to lead adoption while firms developed robust internal controls. Investor interest in climate and sustainability-focused outcomes remains strong, shaping product design and encouraging the integration of measurable ESG objectives. Enhanced reporting and stewardship requirements are reinforcing trust in sustainability-labelled products. These developments are driving inflows into ESG strategies, supporting the growth of the United Kingdom asset management market. Firms are increasingly focused on demonstrating impact and accountability, making ESG offerings a key structural growth driver[4].

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression in passive & model-portfolio channels | -2.1% | National, with acute pressure in London wealth management hubs | Short term (≤ 2 years) |

| Post-Brexit regulatory divergence/friction costs | -1.3% | National cross-border operations; Europe-facing firms in Edinburgh and London | Medium term (2-4 years) |

| Talent drain from rapid M&A consolidation waves | -0.8% | National, concentrated in Edinburgh, Manchester, and London | Medium term (2-4 years) |

| Gilt-market volatility exposing LDI liquidity risks | -1.6% | National, affecting DB pension schemes and insurance-linked portfolios | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fee Compression in Passive & Model-Portfolio Channels

Intense competition across both active and passive products is putting pressure on fees, which has constrained operating margins and driven pricing down in several mainstream investment categories. Passive trackers continue to attract strong inflows, while active funds are experiencing outflows, reinforcing the dominance of large, low-cost index platforms. Rising operating costs further challenge mid-sized firms that lack scale, making it difficult to maintain profitability without efficiency improvements. Extremely low fee levels in broad-market offerings, such as flagship ETFs, have anchored investor expectations, particularly across digital and model-portfolio channels. As a result, asset managers are increasingly focused on scalable operating models, streamlining product ranges, and selectively differentiating offerings where research or active oversight supports higher fees. This environment of fee compression acts as a restraint on revenue growth for the broader United Kingdom asset management market, especially for firms competing outside the largest platforms.

Post-Brexit Regulatory Divergence/Friction Costs

Reforms in the United Kingdom designed to strengthen market competitiveness have created a regulatory framework that diverges from the European one, resulting in dual-track obligations for cross-border asset managers. The United Kingdom AIFM rules are implementing a tiered approach based on fund size, which differs from the European AIFMD II framework and affects delegation, marketing, and operational processes. With the European marketing passport no longer available to United Kingdom managers, firms must rely on National Private Placement Regimes while leveraging the Overseas Funds Regime for UCITS recognition in the United Kingdom. This regime includes application fees and specific disclosure requirements, such as clarifying that these funds are not covered by the United Kingdom compensation scheme, adding complexity and cost. While regulators are accelerating authorization timelines to encourage innovation, firms still face friction as they transition to the new system. These regulatory divergences increase operational burdens, raise compliance costs, and create potential barriers to efficient cross-border management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Alternatives Rising as Equity Dominance Fades

Equity strategies held a 41.52% share in 2025, while Alternative Assets are projected to grow at a 15.44% CAGR through 2031 as institutions seek diversified sources of returns. Private markets, including private equity, private debt, infrastructure, and real estate, are becoming increasingly important, with large managers expanding their capabilities to meet growing demand. Long-Term Asset Funds are providing a channel for retail and defined contribution investors to access multi-asset private exposures under strengthened valuation and governance frameworks. Fixed income remains essential for liability matching and duration management, even as shifts in interest rates have influenced income and hedging strategies.

Allocators are broadening global equity exposure as domestic equity allocations decline, while other asset classes, such as commodities and currencies, are used tactically for diversification rather than as core holdings. The increasing role of private markets is prompting a rethink of traditional portfolio constructions, moving away from conventional models toward allocations that better align with inflation and growth objectives. Overall, portfolios in the United Kingdom asset management market are becoming more diversified, with a more balanced mix of listed and unlisted exposures. This evolution reflects the market’s adaptation to changing risk, return, and liquidity dynamics.

By Firm Type: Wealth Advisory Firms Closing the Gap on Banks

Banks held a 39.83% share in 2025 and continue to benefit from strong distribution and balance sheet linkages. Wealth advisory firms and RIAs are forecasted to grow at a 14.96% CAGR to 2031, supported by policy moves like the Leeds Reforms and the FCA’s forthcoming Targeted Support regime, which is designed to scale simple, guided pathways for millions of consumers. Many households hold substantial cash balances, and shifting even a portion of these into diversified investments is driving sustained inflows for advisory channels. Advisors are responding by expanding simplified model portfolios, guided onboarding processes, and transparent fee structures that align with clients’ risk profiles. The market is also seeing greater integration of advisory services within workplace savings schemes and digital platform interfaces, making investing more accessible.

Regulatory measures, such as the upcoming Targeted Support regime, will enable firms to provide ready-made investment recommendations based on limited client information while maintaining appropriate safeguards. Platforms and firms are also enhancing fractional ETF capabilities, clearer cost disclosures, and plain-language content to help investors make recurring contributions with confidence. Collectively, these trends are fostering multi-year growth for wealth advisory channels and strengthening their role in the broader United Kingdom asset management market.

By Mode of Advisory: Hybrid Models Leading Robo-Advisory’s Ascent

Human Advisory held a 93.67% share in 2025, and Robo-Advisory is projected to grow at a 20.63% CAGR to 2031 as hybrid models become the default in many consumer channels. Hybrid models combine algorithm-driven portfolio allocation and rebalancing with human oversight for suitability checks, coaching, and complex financial planning. Regulatory reforms, including enhanced consumer disclosures and the introduction of the Consumer Composite Investments regime, are reshaping how firms communicate costs, risks, and performance, supporting simpler, more intuitive onboarding experiences. These changes make it easier for first-time investors to make recurring contributions while maintaining advisor support for more complex needs.

Robo solutions are gaining ground among younger, price-sensitive investors who favor automated plans and fractional investing, while human advisors continue to play a key role in retirement, estate, and tax planning. Firms are increasingly offering modular services through omnichannel journeys, including video, messaging, and digital platforms. Simplified product shelves and clearer risk signaling are reducing friction at the decision point, helping investors stay committed through market cycles. As hybrid advisory models mature, they strengthen the long-term growth potential of retail channels within the United Kingdom asset management market.

By Client Type: Retail Ascending While Institutional Rebalances

Institutional investors accounted for 73.52% in 2025, but the Retail segment is forecast to grow at a 17.89% CAGR through 2031, supported by workplace pension expansion and simple guided investing journeys. Broader participation is being encouraged as more individuals plan to make regular contributions, while retirees are increasingly engaging with decumulation solutions such as annuities and drawdown strategies. At the same time, Long-Term Asset Funds and private market access are being integrated into default strategies and workplace schemes, driving diversified long-term portfolios for savers.

Institutional activity is evolving alongside improved funding levels and pension risk transfers, which are shifting assets from defined benefit schemes to insurers’ balance sheets. Regulatory measures, including enhanced liquidity and collateral rules following prior market stress, have strengthened risk management for institutional investors. Insurance allocations are rising, influencing core fixed income demand and overall market flows. Together, these dynamics are creating a more balanced flow mix in the United Kingdom asset management market, combining institutional de-risking, insurer participation, and expanding retail contributions.

By Management Source: Offshore Mandates Gaining Ground on Onshore Dominance

Onshore management accounted for 54.39% in 2025, while Offshore-delegated assets are projected to grow at a 14.28% CAGR to 2031 as managers secure more mandates from Europe and Asia. Policy frameworks, including the Overseas Funds Regime, support cross-border fund recognition, enabling United Kingdom-based managers to attract mandates from Europe and Asia. Strategic partnerships allow managers to access origination channels in private credit and real assets abroad, which are then incorporated into United Kingdom-managed multi-asset portfolios. This approach strengthens diversification, resilience, and operational flexibility, as managers balance currency, liquidity, and regulatory exposures across different jurisdictions.

Multi-domicile platforms are increasingly used to serve clients across regions, deepening global linkages while maintaining a strong United Kingdom regulatory foundation. Firms are leveraging partnerships and alliances to expand private market capabilities and deliver international flows into United Kingdom-managed products. The expansion of offshore-delegated management is creating a more versatile allocation model and supporting sustainable growth in the United Kingdom asset management market. These developments highlight the market’s integration with global capital while preserving its domestic oversight and compliance standards.

Geography Analysis

Leading global platforms dominate index and ETF segments, while United Kingdom-headquartered firms defend leadership in retirement and private market capabilities. Strategic partnerships and alliances are increasingly used to accelerate capability expansion, provide access to private credit origination, and optimize operational efficiency. Fee compression, post-Brexit regulatory divergence, and investor demand for sustainable and tokenized products are driving innovation and strategic differentiation. Overall, the United Kingdom asset management market is evolving into a more diversified, digitally enabled, and globally connected ecosystem, where scale, expertise, and technology adoption define competitive advantage.

Competitive Landscape

The United Kingdom asset management market is experiencing strong growth driven by shifts in client demand, asset allocation, and digital adoption. Institutional investors are increasingly allocating to private markets and alternative assets to seek inflation-adjusted returns and diversify portfolios beyond traditional models. Retail investors are gaining greater access to diversified strategies through Long-Term Asset Funds, fractional shares, and simplified, guided investment journeys. Fintech solutions and regulatory reforms, such as the FCA’s guidance on fractional holdings, are lowering entry barriers and enabling recurring contributions from households previously holding idle cash. Together, these trends are creating a broader, more inclusive investor base and expanding the market’s total assets under management.

Market segmentation reveals evolving dynamics across asset classes, firm types, and advisory modes. Equity and fixed income remain core exposures, but private equity, private credit, and multi-asset alternatives are growing in prominence, supported by LTAFs and enhanced governance frameworks. Wealth advisory firms and registered investment advisers are closing the gap with banks by offering simplified portfolios, guided onboarding, and transparent fees tailored to mass-affluent investors. Hybrid advisory models combining algorithmic portfolio construction with human oversight are expanding access, particularly for younger and price-sensitive clients, while human advisors remain essential for complex retirement, estate, and tax planning. At the same time, onshore-managed assets are complemented by offshore-delegated mandates, allowing managers to tap international flows while balancing currency, liquidity, and regulatory considerations.

United Kingdom Asset Management Industry Leaders

Legal & General Investment Management

Insight Investment

Schroders

Aviva Investors

M&G Investments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Aberdeen Investments has agreed to acquire the management of closed-end fund assets from MFS, consolidating multiple funds into larger municipal and multi-sector fixed income vehicles. The deal strengthens Aberdeen’s position among global closed-end fund managers and is expected to be income accretive.

- July 2025: HSBC launched integrated fractional dealing and custody for all LSE-listed ETFs, offering value-based orders for retail investors with a zero-execution-cost approach for platform partners.

- May 2025: M&G and Daiichi Life Holdings announced a long-term strategic partnership under which Daiichi Life intends to acquire approximately a 15 % shareholding in M&G plc, and the deal is expected to generate at least USD 6 billion of new business flows for M&G over the next five years.

- April 2025: State Street Global Advisors announced a strategic partnership and equity investment in Ethic Inc., a technology‑driven asset management platform focused on personalized, values‑aligned, and tax‑smart investing for institutional and intermediary clients. The collaboration aims to deliver customized investment solutions at scale, enhancing portfolio personalization and client engagement.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom asset management market as the total value of client assets held in segregated mandates, pooled vehicles, and investment funds managed by firms whose portfolio management decisions are taken inside the UK, regardless of the investor's domicile.

Scope exclusion: One-off advisory fees, custodial services, and sales of asset management software are outside this market.

Segmentation Overview

- By Asset Class

- Equity

- Fixed Income

- Alternative Assets

- Other Asset Classes

- By Firm Type

- Broker-Dealers

- Banks

- Wealth Advisory Firms

- Other Firm Types

- By Mode of Advisory

- Human Advisory

- Robo-Advisory

- By Client Type

- Retail

- Institutional

- By Management Source

- Offshore

- Onshore

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed portfolio managers at leading insurers, pension trustees, wholesale distributors, and fintech platforms across England, Scotland, and the Channel Islands. The conversations validated offshore mandate growth rates, average fee compression, adoption of Long-Term Asset Funds, and retail digital channel penetration, filling data gaps left by desk work.

Desk Research

We built the evidence base first by compiling publicly available datasets from authorities such as the Bank of England, the Financial Conduct Authority, the Office for National Statistics, and The Investment Association, which collectively track flows, fund authorizations, and pension contributions. Complementary insight came from tier-1 journals and trade bodies (EFAMA, OECD), company filings, and press archives retrieved through D&B Hoovers and Dow Jones Factiva. These sources establish historic AUM levels, client mix, and regulatory milestones that shape addressable wealth. This list is illustrative; many other documents and portals were reviewed before numbers were frozen.

Market-Sizing & Forecasting

A top-down construct starts with reported AUM from regulated firms, which are then reconciled with pension inflows, net overseas mandates, and market performance to derive a 2024 base. Select bottom-up checks, sampled manager roll-ups and average fee times asset ratios, test the plausibility of the aggregate before results are locked. Key variables include net defined contribution contributions, FCA fund launch pipeline, Bank Rate movements, UK equity market cap shifts, and sterling volatility. We forecast through multivariate regression combined with scenario analysis, allowing GDP growth and real yield paths to flex the model. When bottom-up checks diverge beyond 5%, assumptions are iterated with fresh interviews.

Data Validation & Update Cycle

Every draft passes a two-stage peer review where anomalies versus external yardsticks are flagged. Only after reconciliation and sign-off do we publish. Reports refresh each year, with mid-cycle updates triggered by material policy or market events; the analyst repeats key checks days before delivery so clients receive the newest view.

Why Mordor's UK Asset Management Baseline Proves Dependable

Published figures often differ because firms mix revenue metrics with asset pools, apply varying currency conversions, or refresh models on different calendars.

Our framework fixes a single market definition, aligns inputs to authoritative regulators, and re-checks fee and flow assumptions with practitioners, giving decision-makers a figure they can trace and replicate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.22 trn (2025) | Mordor Intelligence | |

| GBP 10 trn (2024) | Industry Association A | Captures only member firms; omits boutique managers and applies sterling without PPP adjustment |

| USD 12.46 bn (2023) | Global Consultancy B | Tracks software and services revenue, not assets; radically narrower scope |

| USD 12.30 bn (2024) | Research Boutique C | Technology-centric segmentation; excludes institutional asset pools |

The comparison shows that scope definition and metric selection, not simple data error, drive most gaps. By anchoring to regulated AUM, refreshing annually, and cross-checking with both top-down and bottom-up signals, Mordor Intelligence delivers a balanced baseline that clients can trust.

Key Questions Answered in the Report

What is the size and growth outlook for the United Kingdom asset management market?

The United Kingdom asset management market size is USD 13.87 trillion in 2026 and is expected to reach USD 26.08 trillion by 2031 at a 13.47% CAGR.

Which segments lead in share and growth within the United Kingdom asset management market?

Equity holds the largest share at 41.52% in 2025, while Alternative Assets are projected to grow fastest at a 15.44% CAGR through 2031.

How are regulatory changes shaping the United Kingdom asset management market?

SDR labeling is raising disclosure integrity, LTAFs are expanding DC and retail access to private markets, and the FCA’s tokenization roadmap could materially lower fund operating costs.

What are the main risks and constraints in the United Kingdom asset management market?

Fee compression in passive channels, post-Brexit regulatory divergence, and LDI-related liquidity safeguards are the notable near-term constraints on margins and product design.

How is retail participation changing in the United Kingdom asset management market?

Retail is set to expand at a 17.89% CAGR supported by Targeted Support guidance, fractional ETF access, and workplace pension defaults that integrate diversified multi-asset exposures.

Where are the top growth opportunities in the United Kingdom asset management market over the next five years?

Growth is likely in tokenised funds, retail private markets via LTAFs, and sustainable strategies meeting SDR label standards, complemented by cross-border offshore mandates.

Page last updated on: