Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Bauxite Market Report is Segmented by Application (Alumina for Metallurgical Purposes, Cement, Refractories, Abrasives, and Other Applications), Grade (Metallurgical, Chemical, Refractory, and Abrasive), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

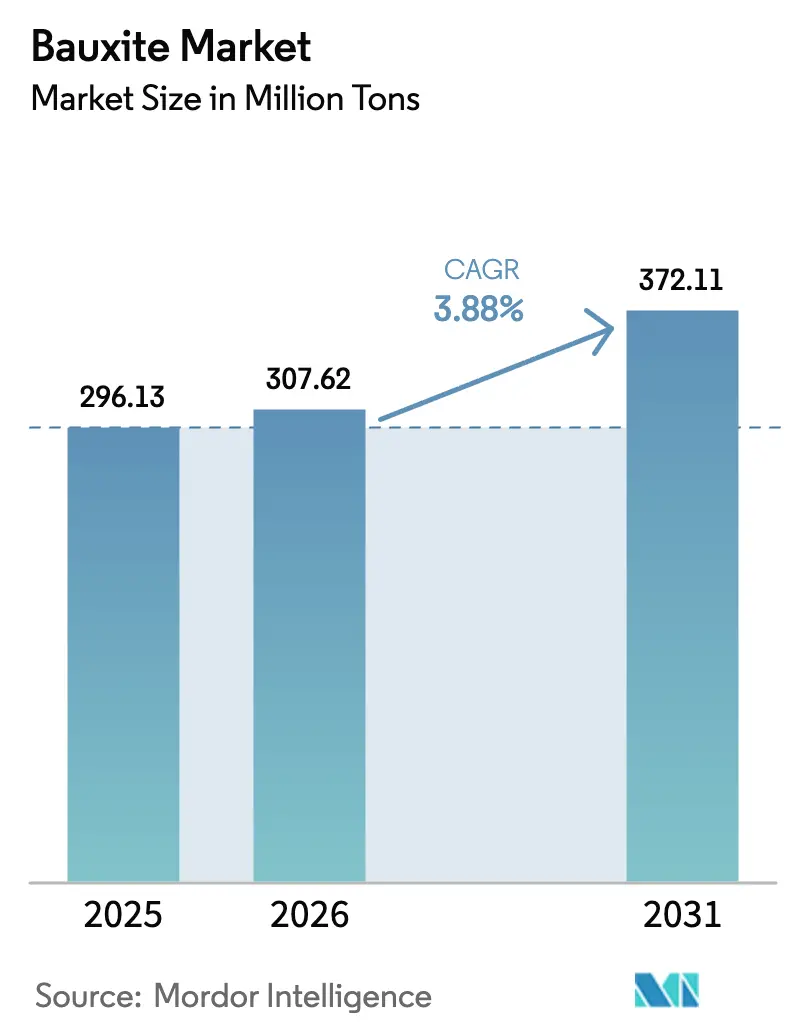

| Market Volume (2026) | 307.62 Million tons |

| Market Volume (2031) | 372.11 Million tons |

| CAGR | 3.88 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Bauxite Market size is projected to expand from 296.13 million tons in 2025 and 307.62 million tons in 2026 to 372.11 million tons by 2031, registering a CAGR of 3.88% between 2026 to 2031. Decarbonization policies, especially the EU's Carbon Border Adjustment Mechanism, are pushing aluminum supply chains to prioritize traceable low-carbon ore, which fetches premium prices. With the rise of electric-arc furnaces, there is an escalating demand for refractory-grade materials, amplifying the need for high-purity alumina bricks capable of withstanding intense heat cycles. The trend of mine-to-mill integration is gaining momentum, as demonstrated by Rio Tinto's 2024 acquisition of a stake in Compagnie des Bauxites de Guinée, ensuring a captive supply and marking a strategic pivot from traditional spot procurement. Similarly, initiatives in India and Europe are transforming red mud, a mining byproduct, into valuable rare-earth elements and construction materials, thereby prolonging mine viability and enhancing financial returns.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shift toward alumina-based refractory bricks in steel

mini-mills

Shift toward alumina-based refractory bricks in steel

mini-mills

| +0.60% | Global - strongest in India, ASEAN, Eastern Europe | Medium term (2-4 years) | (~) % Impact on

CAGR Forecast:

+0.60%

|

Geographic

Relevance

:

Global - strongest in India, ASEAN, Eastern Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Government-backed infrastructure stimulus in India and

ASEAN

Government-backed infrastructure stimulus in India and

ASEAN

| +0.90% | India, Indonesia, Vietnam, Thailand, Philippines | Short term (≤ 2 years) | |||

Supply-security programs by OEMs (captive mine

investments)

Supply-security programs by OEMs (captive mine

investments)

| +0.50% | Global, led by Australia-China and Guinea-Europe corridors | Long term (≥ 4 years) | |||

Plasma-based red-mud valorization unlocking waste

stockpiles

Plasma-based red-mud valorization unlocking waste

stockpiles

| +0.30% | India, Europe, Australia | Long term (≥ 4 years) | |||

Blockchain-enabled traceability premiums for low-carbon

bauxite

Blockchain-enabled traceability premiums for low-carbon

bauxite

| +0.40% | Europe, North America, Japan, South Korea | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Shift Toward Alumina-Based Refractory Bricks in Steel Mini-Mills

In 2024, the global installation of electric-arc furnaces (EAF) surged. Each new EAF unit, pivotal in crude steel production, now relies on high-alumina bricks, marking a departure from traditional magnesia-carbon linings. In 2025, JSW Steel's refractories tender highlighted a preference for bauxite with less than 2% reactive silica, emphasizing the industry's focus on purity. Modular mini-mills in the Southeast Asia region are now consuming refractories at a higher rate per ton of output than their integrated counterparts. This increased demand has driven spot prices for high-alumina ore above those of metallurgical variants. With fewer than a dozen qualified mines worldwide, the constrained supply has tightened trade dynamics and spurred beneficiation upgrades. As a result, miners focusing on refractory-grade concentrates are achieving significant gross-margin premiums over bulk ore.

Government-Backed Infrastructure Stimulus in India and ASEAN

India's National Infrastructure Pipeline, with its ambitious vision extending to 2030, has allocated substantial funds for transportation, energy, and urban projects. This initiative has prompted an upward revision in domestic aluminum demand forecasts for the FY 2025-26 budget[1]Press Information Bureau, “Union Budget 2025-26 Infrastructure Outlay,” pib.gov.in . Concurrently, ASEAN's connectivity blueprint, with its focus on vital rail, port, and grid connections, is set to reroute annual bauxite. Once destined for export terminals, this bauxite will now flow into regional refining hubs. Highlighting the surging demand, Vietnam's Long Thanh airport is sourcing its aluminum cladding from Malaysian alumina. Additionally, Indonesia's prohibition on raw-ore exports has triggered a surge of domestic refinery projects. These refineries, now processing local bauxite, have significantly reduced seaborne volumes. Collectively, these initiatives are streamlining supply chains, amplifying regional premiums, and enhancing demand visibility in the Bauxite market.

Supply-Security Programs by OEMs (Captive Mine Investments)

Alcoa's expansion at Kwinana, Hindalco's upgrade at Utkal, and Tianshan Aluminum's strategic investment in Guinea's Boffa project signal a pronounced industry shift towards captive ore. This shift has increased captive ore's presence in the seaborne trade. By consolidating operations, producers are effectively navigating the volatility of quarterly spot prices and securing alumina-indexed pricing. This strategy has compressed margins for third-party refineries. While this upstream consolidation poses challenges for independent miners, it promises a more stable long-term ore flow in the Bauxite market.

Plasma-Based Red-Mud Valorization Unlocking Waste Stockpiles

As global red-mud inventories swell, the associated environmental liabilities are becoming increasingly burdensome. However, there is a beacon of hope. India's CSIR has unveiled a plasma-torch technology capable of extracting a significant percentage of valuable oxides from red mud at a cost well below the economic threshold[2]Centre for Scientific and Industrial Research, “Plasma Valorization Breakthrough,” csir.res.in . Vedanta is piloting a project targeting rare-earth revenue by 2027 while concurrently reducing tailing loads. Norsk Hydro, on the other hand, is innovating with a hydrogen-reduction technique, converting Brazilian red mud into iron pellets. This approach not only mitigates dam deposits but also capitalizes on coproduct sales. Such innovations not only prolong mine lifespans but also reduce Scope 1 emissions and ease feedstock pressures in the Bauxite market.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |||

|---|---|---|---|---|---|---|

Volatile energy costs inflating calcination margins

Volatile energy costs inflating calcination margins

| -0.80% | Europe, North America, Japan | Short term (≤ 2 years) |

(~) % IMPACT ON CAGR FORECAST

:

-0.80%

|

GEOGRAPHIC RELEVANCE

:

Europe, North America, Japan

|

IMPACT TIMELINE

:

Short term (≤ 2 years)

|

ESG-driven capital rationing for new greenfield mines

ESG-driven capital rationing for new greenfield mines

| -0.50% | Global; acute in Australia, Brazil, West Africa | Medium term (2-4 years) | |||

Geostrategic resource nationalism and export-levy

volatility

Geostrategic resource nationalism and export-levy

volatility

| -0.40% | Guinea, Indonesia, Malaysia | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Energy Costs Inflating Calcination Margins

Alumina refining is energy-intensive, consuming an amount of electricity per ton. By late 2025, European spot power prices increased significantly compared to 2023 levels. This rise reduced profit margins, resulting in capacity shutdowns in Germany and France. Alcoa’s Kwinana plant experienced a significant increase in energy costs in 2025, negatively impacting its EBITDA. Producers struggling with elevated costs and lacking renewable Power Purchase Agreements (PPAs) face the risk of permanent closure. As a result, trade is shifting toward low-tariff refineries in the Middle-East, while liquidity in the European Bauxite market tightens.

ESG-Driven Capital Rationing for New Greenfield Mines

In Western Australia, project approvals now take longer than pre-2023 durations due to stricter biodiversity and heritage evaluations. In 2025, Brazil, citing tailings concerns, suspended multiple licenses in Pará, stalling substantial capital. Investors are now seeking higher project Internal Rate of Returns (IRRs) compared to 2022 levels. This shift in expectations is redirecting investments toward brownfield expansions and constraining supply elasticity in the Bauxite market.

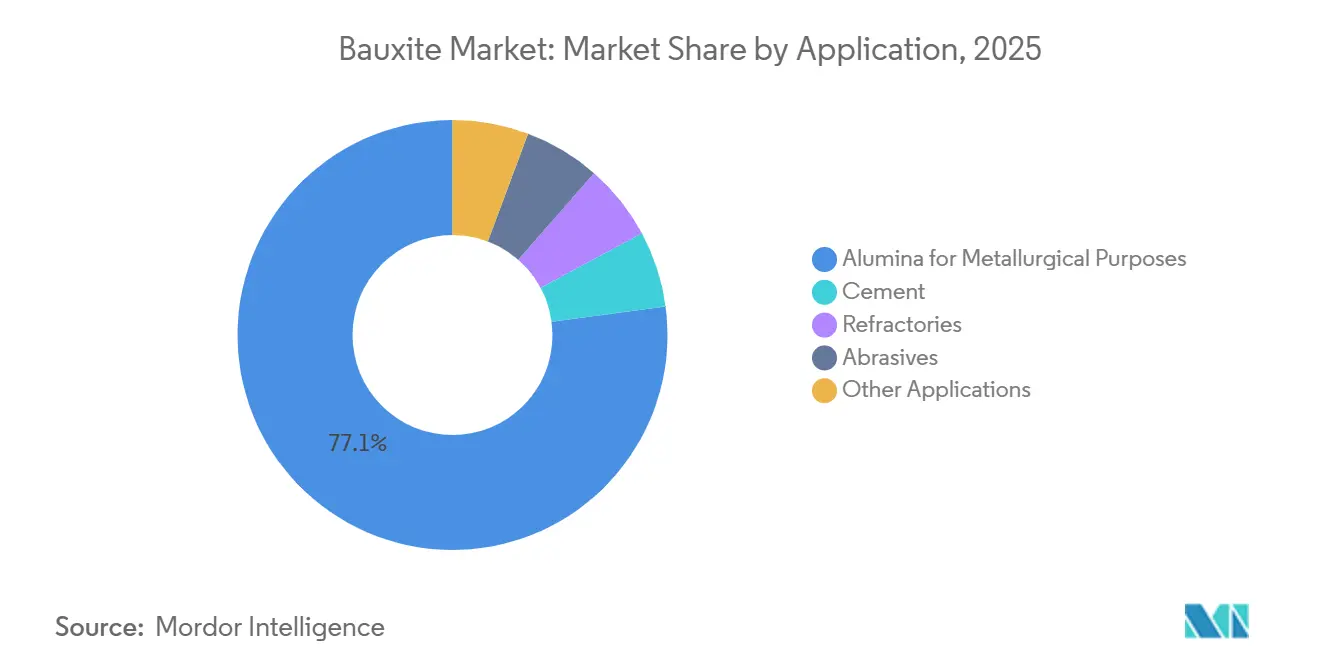

By Application: Refractories Capture Margin Upside

Refractory demand is projected to grow at a CAGR of 4.72% during the forecast period of 2026-2031. Metallurgical alumina, which held a dominant 77.12% of the volume, experienced a deceleration in its growth rate, a consequence of China's phased retirement of its high-cost smelting capacities. Refractories, especially those with high Al₂O₃ bricks, command a premium. This premium is justified as these bricks extend the lifespan of Electric Arc Furnaces (EAFs), leading to fewer costly operational stoppages. A constrained supply of qualified materials has stabilized profit margins. While cement and abrasives hold niche positions, they benefit from rising demands: rapid-setting Calcium Aluminate Cement (CAC) in cement and semiconductor polishing in abrasives, driving modest growth.

By 2031, the Bauxite market's share for metallurgical use is set to wane, with refractories and specialty chemicals increasingly claiming the volumes. In response, suppliers are channeling significant capital expenditures towards upgrading to refractory-grade materials. This strategic pivot highlights a broader industry trend: a shift in focus from quantity to quality across diverse application segments, deepening the price divergence in the Bauxite market.

Note: Segment shares of all individual segments available upon report purchase

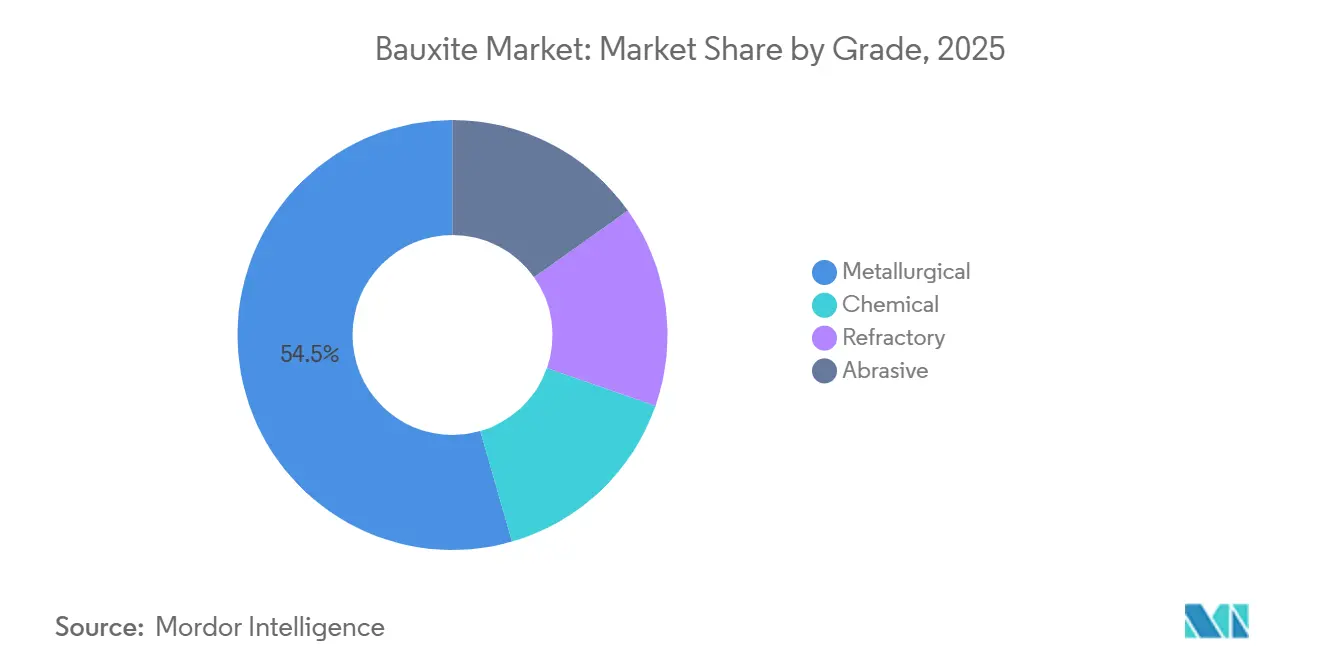

By Grade: Metallurgical Dominance, Refractory Margin Leadership

In 2025, metallurgical-grade Bauxite accounted for 54.46% of the market volume. Yet, it was the refractory grade that surged the quickest, boasting a 4.41% CAGR during the forecast period of 2026-2031. The chemical-grade, mainly utilized for flame-retardant Aluminum Trihydrate (ATH), capitalized on stricter European fire-safety regulations, securing a commendable market share and consistent growth. Though the abrasive-grade represented a smaller slice of the overall volume, it closely mirrored automotive production trends and commanded the highest price among all grades.

Notable shifts in gross-margin spreads indicate evolving economic dynamics. For example, Metro Mining pivoted a substantial portion of its 2024-2025 output towards the refractory grade, reaping a significant year-over-year gross margin uplift without any increase in tonnage. In Europe and Japan, compliance with ISO 4009 standards and third-party assays is becoming paramount. This compliance necessitates investments in technologies like X-ray fluorescence (XRF) and automated sorting, posing a financial challenge for smaller miners. Given that these certifications can command price premiums, integrated producers are poised for substantial gains, highlighting the pronounced two-speed dynamic in the Bauxite market.

Note: Segment shares of all individual segments available upon report purchase

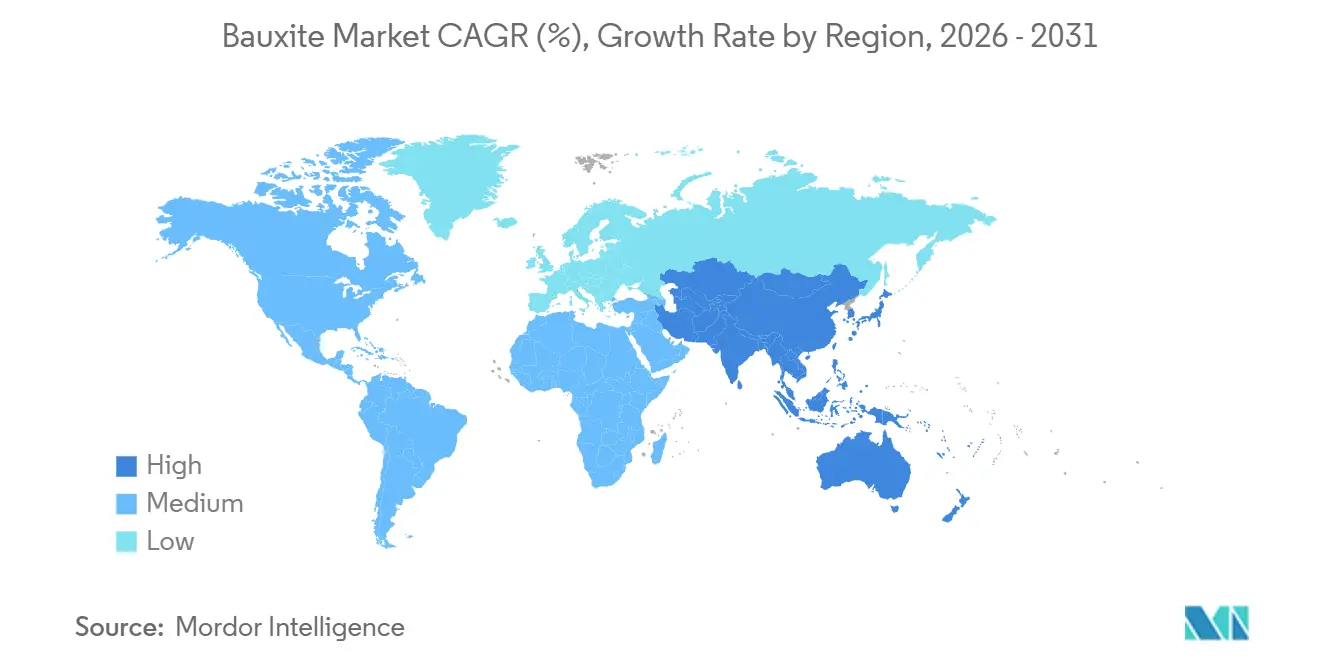

Asia-Pacific, accounting for 54.44% of global volume in 2025, is set to grow at a 4.32% CAGR through the forecast period of 2026-2031. This growth is fueled by China's robust alumina output and rising aluminum demand, largely driven by infrastructure initiatives in India. China, which heavily relies on imports, sourced a significant volume of bauxite, predominantly from Guinea. However, following a ban, Indonesia's contribution saw a sharp decline. India's expanded Panchpatmali, now with increased capacity, has notably lessened the nation's dependence on imports, signaling a regional pivot towards domestic ore.

North America also made its mark in the 2025 demand landscape. The United States leaned on imports, mainly from Jamaica and Brazil, to bolster its refining capacity. Canada's Vaudreuil refinery, reliant on Australian ore, and Mexico's extrusion sector, which brought in alumina, highlight the region's trend towards near-shoring.

Meanwhile, Europe's influence is waning. Rising energy costs led to capacity closures in Germany and France, causing a shift of raw ore to more economically viable plants in the Middle-East. The European Union's Carbon Border Adjustment Mechanism (CBAM) is advocating for certified low-carbon imports. A noteworthy uptick from 2023, a large segment of 2025's bauxite acquisitions came with third-party carbon verification.

South America, spearheaded by Brazil, played a pivotal role in the seaborne trade, primarily directing shipments to China and North America. Norsk Hydro's expanded Paragominas is at the forefront, championing solar power endeavors with an ambitious goal of carbon-neutral mining by 2028. Argentina, with Chinese financial backing, is setting its sights on ramping up output at the Sierra de Bahoruco project by 2029.

The Middle-East and Africa, with Guinea making significant contributions in 2025, are key players in the global supply chain. Yet, with new levy hikes and domestic processing mandates, the dynamics are evolving. The UAE's Al Taweelah refinery, processing Guinean ore, boasts gas-linked cash costs that outpace European rates, propelling the region's growth.

Market Concentration

The bauxite market is moderately consolidated. While the top five miners dominate output, their grip on refining remains limited. This gap paves the way for mid-tier toll processors. Rio Tinto's Guinea investment not only secures a steady feedstock but also highlights a cost-plus vertical integration approach, bolstering profit margins. Metro Mining's shift to refractory grade materials has reaped rewards, showcasing a marked gross-margin increase in FY 2024-2025.

Digital traceability is becoming a cornerstone for market share growth. EGA's blockchain venture stands out, attracting green bonds that offer cost advantages over conventional debt. The Aluminium Stewardship Initiative's certification made waves in 2025, with European stakeholders advocating for broader coverage by 2027. Miners lacking ESG credentials are facing challenges, with margin pressures leading to a spike in asset divestitures to integrated majors.

A rising trend in technology is focusing on waste monetization. Vedanta's red-mud pilot project eyes profitable rare-earth sales, while Norsk Hydro's hydrogen-reduction innovation is converting tailings into lucrative iron pellets. Players that adeptly weave in circular-economy revenue streams and spotlight low-carbon intensity data are set to draw in cheaper capital and command premium prices in the bauxite market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Volume)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Bauxite is a reddish clay-based rock that is most commonly found in tropical and subtropical regions. Bauxite is majorly composed of aluminum oxide compounds (alumina), silica, iron oxides, and titanium dioxide.

The Bauxite Market is segmented by application, grade and geography. alumina for metallurgical purposes, cement, refractories, abrasives, and other applications. By grade, the market is segmented into metallurgical, chemical, refractory, and abrasive. The report also covers the market size and forecasts for bauxite in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.