Dolomite Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 198.63 Million tons |

| Market Volume (2031) | 239.24 Million tons |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dolomite Market Analysis by Mordor Intelligence

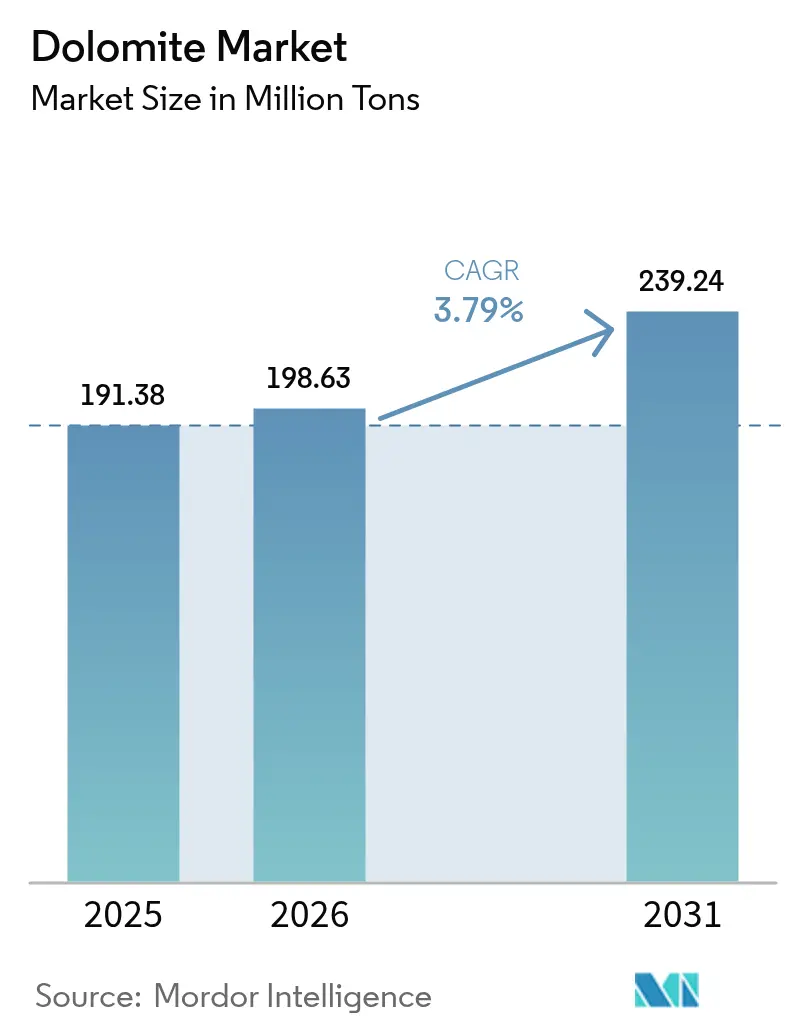

Dolomite market size in 2026 is estimated at 198.63 Million tons, growing from 2025 value of 191.38 Million tons with 2031 projections showing 239.24 Million tons, growing at 3.79% CAGR over 2026-2031. The expansion underscores the mineral’s entrenched role as a dual-oxide material that supplies calcium and magnesium for steelmaking fluxes, construction aggregates, and next-generation water treatment media. Asia-Pacific continues to set the consumption tone, helped by China’s large crude steel output, India’s infrastructure build-out, and ASEAN’s multitrillion-dollar financing gap for roads, ports, and power plants. Industrial users favor dolomite when high-temperature resilience, slag-forming efficiency, or pH buffering are essential, giving the material cost and performance advantages over single-oxide substitutes. Ongoing decarbonization across glass, cement, and hydrogen-ready steel operations adds another structural layer of demand by calling for refractory formulations and flux chemistries that withstand harsher thermal cycles.

Key Report Takeaways

- By mineral type, calcined dolomite led with 46.21% of dolomite market share in 2025, while sintered dolomite is projected to grow at the fastest 4.53% CAGR through 2031.

- By end-user industry, mining and metallurgy accounted for 34.87% of the dolomite market size in 2025, while water treatment is expected to post the highest 4.29% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded 53.39% of overall volume in 2025 and is forecast to expand at a 4.62% CAGR through 2031, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dolomite Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Construction Spending in Asia-Pacific | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Expanding Global Steel and Iron Production | +0.9% | Global, concentrated in China, India, ASEAN | Long term (≥ 4 years) |

| Environmental Regulations Boosting Soil Conditioning Demand | +0.7% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising Glass and Ceramics Capacity Expansions | +0.5% | Global, emphasis on Asia-Pacific and Europe | Short term (≤ 2 years) |

| Waste-Water PFAS Removal Pilots Using Dolomite Adsorbents | +0.4% | North America and EU regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Construction Spending in Asia-Pacific

Asia-Pacific’s infrastructure investment pipeline requires USD 26 trillion through 2030, driving sustained consumption of dolomite-derived cement additives and construction aggregates[1]Asian Development Bank, “ASEAN Infrastructure Financing Gap,” adb.org . China’s urban redevelopment programs and India’s National Infrastructure Pipeline widen the market for flux-grade dolomite in clinker production, where magnesium oxide improves concrete durability. Logistics advantages encourage contractors in ASEAN’s archipelagic settings to substitute locally quarried dolomite for imported limestone, tightening regional supply and lifting prices. Producers with quarry proximity to coastal megacities gain higher margins thanks to shorter hauling distances. Sustainability certification programs that promote low-carbon, locally sourced inputs further entrench regional suppliers.

Expanding Global Steel and Iron Production

Electric arc furnace investments in India and Southeast Asia continue to raise demand for calcined dolomite, which combines with silica to form low-viscosity slag. The growth path is reinforced by hydrogen-based steel trials that run at higher operating temperatures and need refractory linings enriched with sintered dolomite grains. Dual-oxide composition trims raw-material inventories because a single feedstock supplies both CaO and MgO. As mini-mills proliferate near scrap sources, their operators prefer fluxes that arrive pre-calcined and quality-certified, creating premium niches for integrated miners that also own rotary kilns.

Environmental Regulations Boosting Soil Conditioning Demand

U.S. EPA soil-health guidance and the European Union’s Farm-to-Fork strategy elevate the place of dolomite in precision agriculture, especially for magnesium-deficient soils. Regulators stipulate tighter tolerance bands for pH and nutrient release, nudging growers toward higher-purity, low-impurity products. The same rulebooks raise red flags about microplastic fragments in bulk lime, prompting audits that favor operators with traceable supply chains and covered storage systems. Premium certification unlocks price differentials and encourages continued process investments at grind-and-screen plants.

Rising Glass and Ceramics Capacity Expansions

Technical glass producers in Asia and Europe have proven that dolomite lowers melt viscosity and cuts furnace energy inputs, aligning with net-zero roadmaps that seek double-digit reductions in CO₂ per ton of product. Meanwhile, advanced ceramics makers use fine-grind dolomite as a magnesium source that enhances thermal shock resistance in substrates for automotive exhaust sensors and consumer electronics. Oxy-fuel furnace retrofits favor dolomite-infused refractory bricks because they resist accelerated oxidation in high-oxygen atmospheres. Producers positioned in regions with strong renewables penetration can promote the low-carbon story further by citing greener electricity mixes at their calcination sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution With Cheaper Igneous Rock Fillers | -0.8% | Global, particularly cost-sensitive applications | Short term (≤ 2 years) |

| Stricter Land-Use and Mining Permitting Hurdles | -0.6% | North America and EU, expanding globally | Medium term (2-4 years) |

| Agricultural Liming Scrutiny Over Micro-Plastic Contamination | -0.3% | EU and North America regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution With Cheaper Igneous Rock Fillers

Price-sensitive users in aggregate and low-spec refractory markets often switch to olivine or basalt when dolomite premiums widen. Olivine’s higher magnesium content and its availability from coastal Norway and Turkey add competitive tension in Europe. Growth of recycled concrete aggregates in public works further caps virgin dolomite demand. Suppliers respond by differentiating on chemical consistency and by bundling technical support that documents slag-forming efficiency.

Agricultural Liming Scrutiny Over Micro-Plastic Contamination

The European Food Safety Authority is reviewing pathways for microplastics in soil-amendment products, including dolomite lime[2]European Food Safety Authority, “Microplastics in Food and Feed,” efsa.europa.eu . New lab testing protocols could disqualify lower-grade material containing polymer fragments from conveyor belting or packaging. High-purity producers that already operate enclosed crushing lines gain a first-mover advantage and can capture premium market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Type: Calcined Grades Anchor Steel and Refractory Demand

Calcined variants captured 46.21% of dolomite market share in 2025 as steelmakers demanded reactive oxides to bind silica and alumina at 1,700 °C furnace temperatures. The dolomite market size for calcined grades is forecast to expand in step with EAF capacity additions and decarbonization retrofits that rely on slag-forming efficiency. Sintered forms are set to outpace other products at a 4.53% CAGR because hydrogen-ready furnaces require bricks that endure higher heat fluxes. In that context, the dolomite market creates pricing tiers linked to bulk density and residual CO₂ levels.

Technological strides such as vertical shaft kilns with oxygen-enriched combustion improve calcination yield while trimming fuel intensity. Producers also accelerate roll-outs of automated optical sorters to guarantee low-silica feed. Agglomerated pellets remain niche yet strategic in water treatment where controlled dissolution prevents overdosing. As municipalities standardize on PFAS remediation systems, pellet suppliers can quote higher prices than for raw fines, enhancing margin profiles.

By End-User Industry: Water Treatment Breaks Away From Traditional Core

Mining and metallurgy retained 34.87% of volume in 2025, supported by steady molten-steel flux demand and refractory consumption. However, the dolomite market size allocated to water treatment is projected to grow fastest at 4.29% CAGR, reflecting regulatory urgency to tackle legacy contaminants. Utilities appreciate dolomite’s dual-function chemistry—adsorption plus pH buffering—over single-purpose media. Pilot adoption has already shifted purchasing from occasional spot loads to multiyear offtake commitments.

Agriculture remains a resilient baseline, yet future growth rests on value-added micronized powders with certified low contamination. The cement sector benefits from clinker optimization that uses dolomite to balance MgO and reduce CO₂ intensity, dovetailing with carbon-capture retrofits at integrated plants. Meanwhile, glass and ceramics customers request tighter particle-size distributions to ensure melting homogeneity in advanced technical products, sustaining a reliable mid-single-digit demand uptick through 2030.

Geography Analysis

Asia-Pacific commanded 53.39% of global volume in 2025 and will add capacity at a 4.62% CAGR as mega-projects such as India’s high-speed rail corridors and Indonesia’s new capital city consume flux-grade aggregates. Chinese consolidation across upstream magnesite and dolomite mines stabilizes supply quality, enabling refractory firms to meet hydrogen furnace specifications without importing European feedstock. Japan’s leading steelmakers test higher-purity dolomite bricks in pilot hydrogen direct-reduction modules, reinforcing the region’s technological gravity.

North America shows balanced dynamics: legacy demand from integrated steelworks in the Great Lakes coexists with new opportunities in PFAS removal systems mandated by the U.S. EPA. Canadian miners leverage rail links to ship premium sintered material to U.S. Midwest mini-mills, while Mexico’s automotive growth spurs ceramic substrate production that requires finely milled dolomite.

Europe maintains steady pull from glass decarbonization and organic farming regulations. German furnace rebuilds favor low-CO₂ dolomite flux, whereas France and Italy continue to value soil conditioners that release magnesium slowly. Nordic smelters turn to high-density sintered bricks sourced from domestic quarries, reducing import reliance and shortening lead times.

Competitive Landscape

The global dolomite market hosts a moderately fragmented lineup in which the top five players hold an estimated 45-55% combined share. Carmeuse and Lhoist capitalize on extensive quarry networks and captive kilns to supply both lump flux and milled powders across continents. Imerys pursues higher-margin niches such as technical ceramics by integrating customer laboratories within its R&D centers. Nordkalk leverages Baltic Sea shipping lanes to deliver consistent chemistry to Northern European steel plants, lowering delivered cost compared with inland rivals.

Strategic activity centers on energy-efficient calcination, digital mine scheduling, and downstream granulation lines that target fertilizer and filtration customers. Omya’s 2024 expansion of specialty fertilizer granulation in Kansas typifies moves into agriculture that fetch premium pricing. RHI Magnesita’s July 2025 cost-containment plan underscores vulnerability to cyclical steel demand yet also spotlights the upside of proprietary refractory grades for hydrogen furnaces. Smaller regional operators defend share by offering just-in-time delivery within 200 km radii, mitigating freight costs that often exceed run-of-quarry ore value.

Dolomite Industry Leaders

Calcinor

Lhoist

Carmeuse

Imerys

Omya AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: RHI Magnesita acquired U.S.-based Resco Group for USD 430 million, strengthening its North American market presence and expanding its dolomite-based refractories portfolio. The transaction enhances the company's capabilities to serve the steel and cement industries with high-performance materials for industrial applications.

- March 2023: REFRACTARIOS KELSEN S.A., part of Calcinor established a new dolomite-fired brick manufacturing facility in Aduna (Guipúzcoa), strengthening its European leadership position. The plant features advanced automation systems and environmentally sustainable production processes for refractory dolomite manufacturing.

Global Dolomite Market Report Scope

Dolomite is an anhydrous carbonate mineral high in magnesium, calcium, and some amount of iron. Dolomite mining is a non-metallic mineral that can be used to produce ceramics, composites, glass, and refractory materials. Dolomite is used in mining, manufacturing, refining, and construction, among other things.

The dolomite market is segmented by mineral type, end-user industry, and geography. By mineral type, the market is segmented into agglomerated, calcined, and sintered. By end-user industry, the market is segmented into agriculture, ceramics and glass, cement, mining and metallurgy, pharmaceuticals, water treatment, and others (animal feed, etc.). The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Calcined |

| Agglomerated |

| Sintered |

| Mining and Metallurgy |

| Agriculture |

| Cement |

| Ceramics and Glass |

| Water Treatment |

| Pharmaceuticals |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Mineral Type | Calcined | |

| Agglomerated | ||

| Sintered | ||

| By End-user Industry | Mining and Metallurgy | |

| Agriculture | ||

| Cement | ||

| Ceramics and Glass | ||

| Water Treatment | ||

| Pharmaceuticals | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of dolomite market?

The dolomite market is estimated at 198.63 million tons in 2026 and forecast to reach 239.24 million tons by 2031.

Which region leads global consumption?

Asia-Pacific holds the top position with 53.39% share in 2025 and the fastest 4.62% CAGR outlook.

Which end-use industry is growing fastest?

Water treatment industry is expected to post the highest 4.29% CAGR through 2031.

Why are sintered dolomite grades gaining attention?

Hydrogen-ready steel furnaces and advanced ceramics need sintered products for enhanced thermal shock resistance.

Page last updated on: