DevOps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.57 Billion |

| Market Size (2031) | USD 51.43 Billion |

| Growth Rate (2026 - 2031) | 21.33% CAGR |

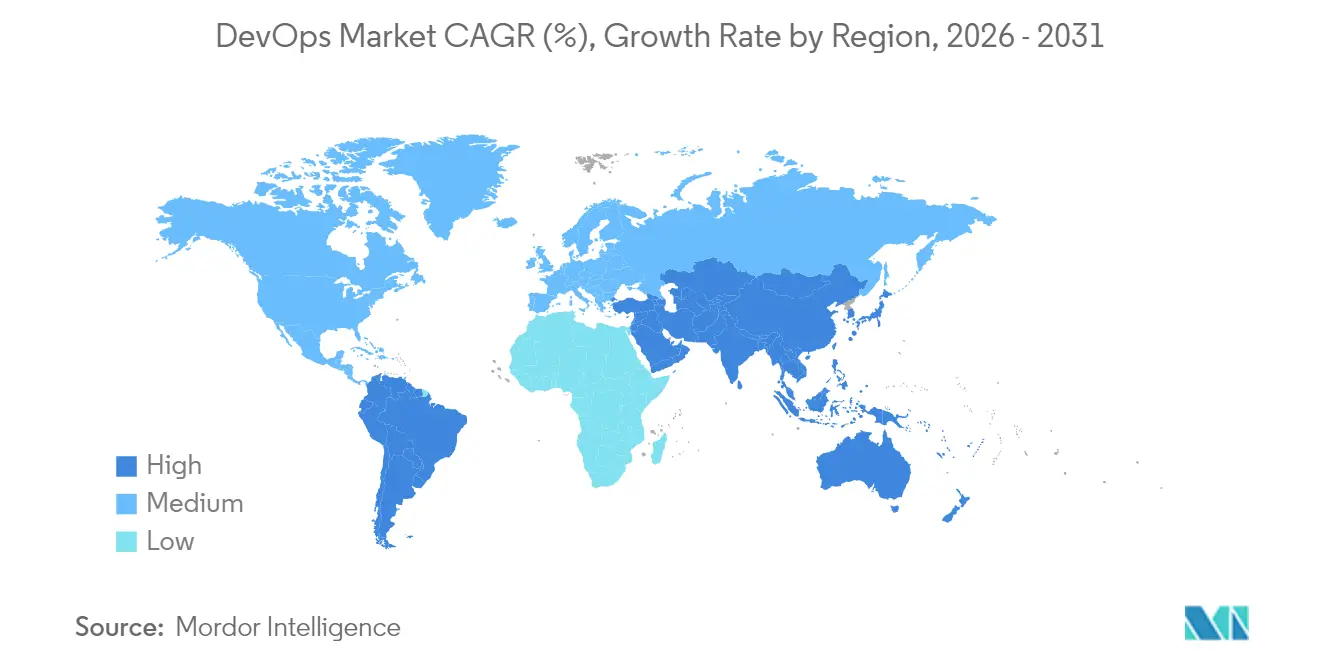

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

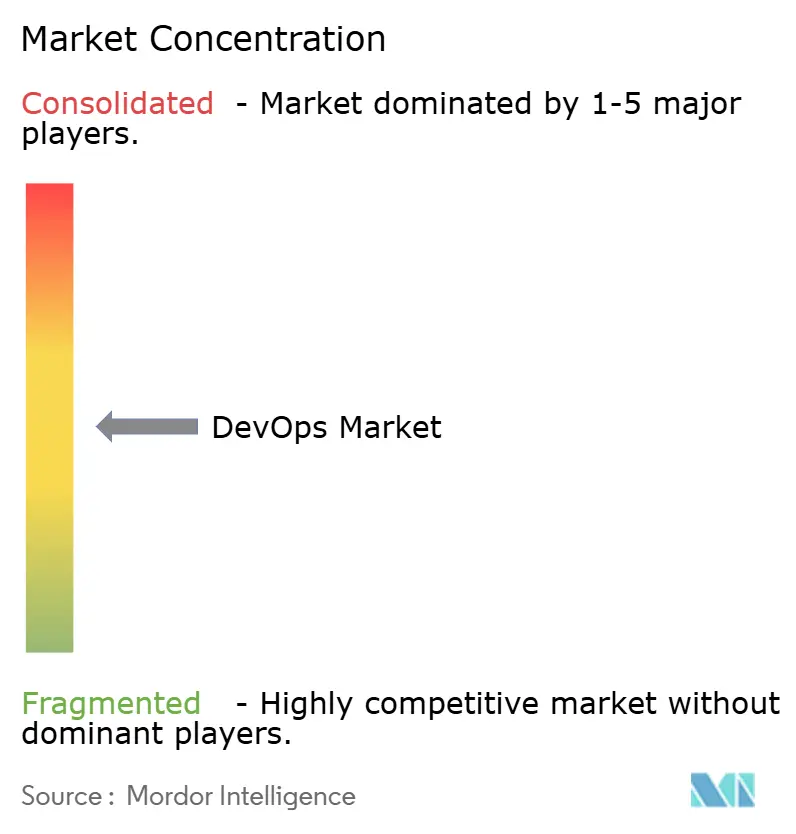

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DevOps Market Analysis by Mordor Intelligence

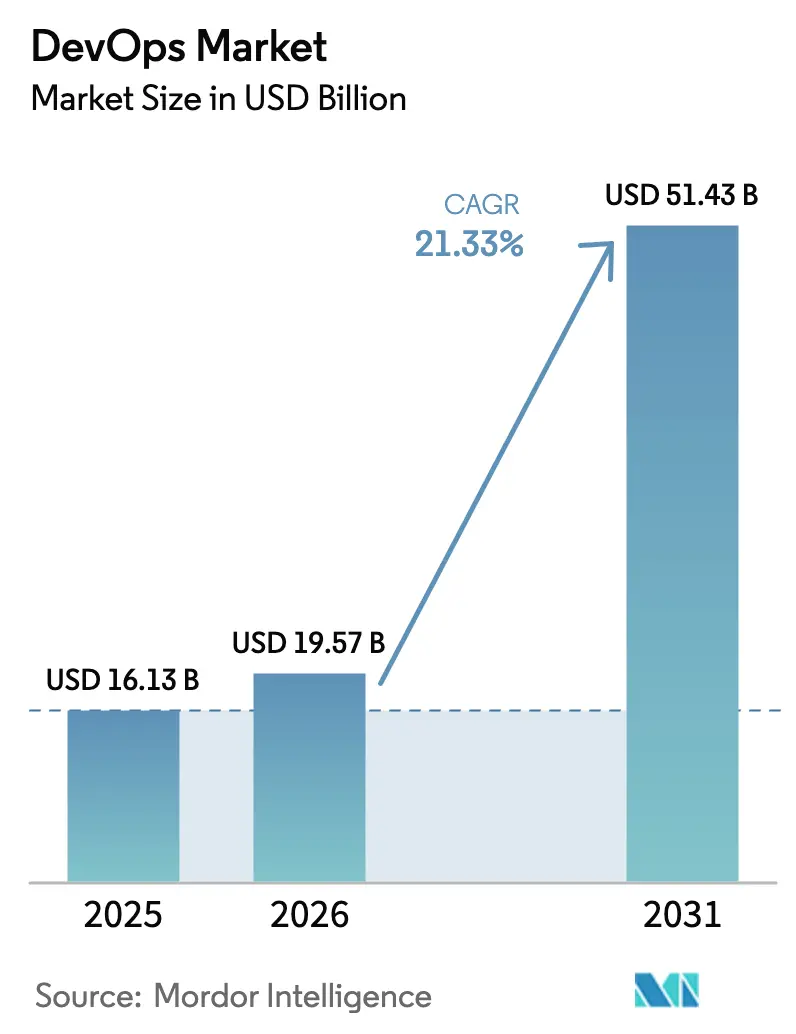

The DevOps market size is expected to grow from USD 16.13 billion in 2025 to USD 19.57 billion in 2026 and is forecast to reach USD 51.43 billion by 2031 at 21.33% CAGR over 2026-2031. Intensifying demand for shorter software delivery cycles, rising enterprise-wide automation, and the mainstreaming of artificial-intelligence-assisted workflows are accelerating adoption rates. North America leads early uptake owing to a mature cloud ecosystem, while Asia-Pacific’s rapid digitalization is shaping the fastest growth runway. Toolchains are evolving toward integrated DevSecOps platforms as security moves “left” in the development lifecycle. Hybrid-cloud strategies, skills shortages, and the pivot from monoliths to microservices are defining the competitive battleground and creating service-led growth opportunities.

Key Report Takeaways

- By component, solutions held 59.65% of DevOps market share in 2025; services are projected to expand at a 23.1% CAGR to 2031.

- By deployment model, the public-cloud segment accounted for 44.70% of the DevOps market size in 2025, while the hybrid cloud is advancing at a 24.1% CAGR through 2031.

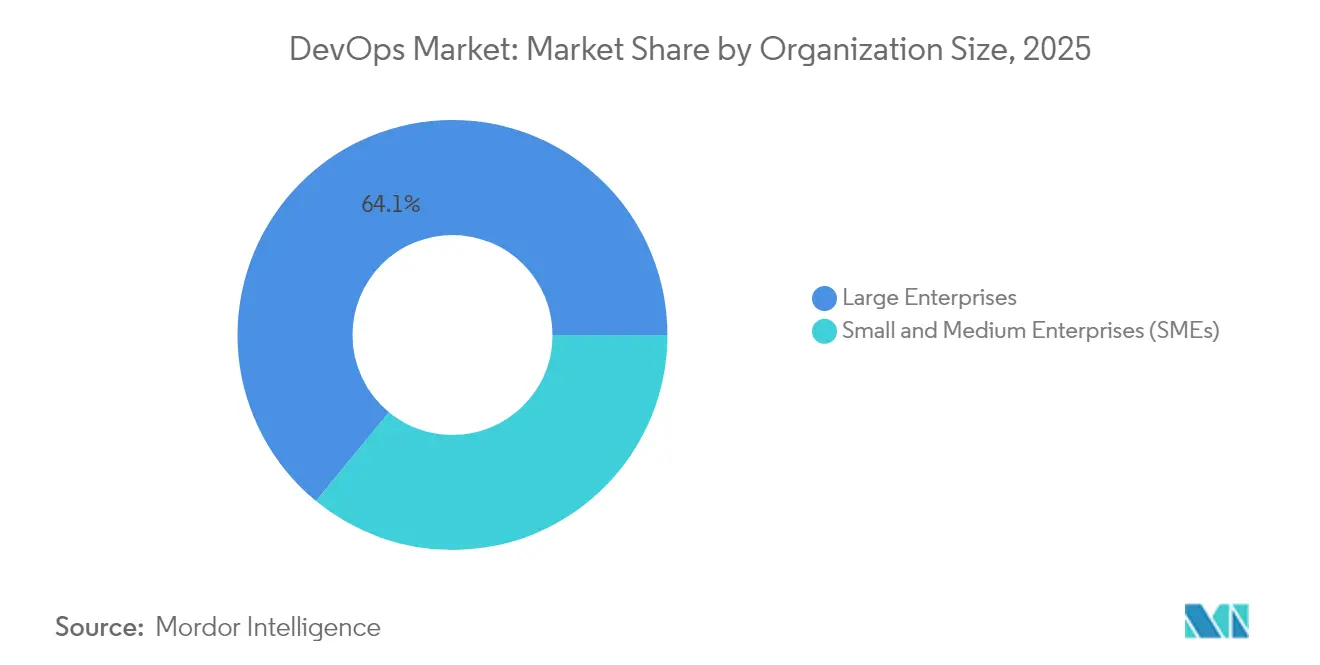

- By organization size, large enterprises led with 64.05% revenue share in 2025; SMEs post the highest expected CAGR of 21.2% between 2026-2031.

- By end-user industry, IT and telecommunications commanded 25.05% of DevOps market size in 2025, whereas healthcare and life sciences are forecast to grow at 28.1% CAGR to 2031.

- By geography, North America captured 37.85% of the DevOps market share in 2025; Asia-Pacific is set to grow at a 25.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global DevOps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need to shorten software development lifecycle | +5.2% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Growing enterprise adoption of automation and CI/CD | +4.8% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Cloud-native and micro-services proliferation | +4.3% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Large-scale digital-transformation and agile uptake | +3.7% | Global, with higher impact in APAC and Europe | Medium term (2-4 years) |

| AI/ML-centred predictive DevOps (AIOps) | +2.9% | North America, Europe, and advanced APAC economies | Long term (≥ 4 years) |

| Mandatory shift to DevSecOps for zero-trust compliance | +2.6% | North America, Europe, and regulated industries globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Need to shorten software development lifecycle

Organizations using mature DevOps practices report a 200% rise in deployment frequency and a 50% fall in time-to-market. [1]Continuous Delivery Foundation, “State of CI/CD Report,” linuxfoundation.org Regulated sectors such as healthcare see 83% of developers engaged in DevOps to keep pace with compliance-driven release schedules. Earlier defect detection through continuous testing cuts quality-related costs by 60%. Cross-functional teams replace siloed structures to sustain faster iteration, and demand for platform tooling that simplifies governance is climbing.

Growing enterprise adoption of automation and CI/CD

Seventy percent of enterprises intend to deploy Infrastructure-as-Code by end-2025, cutting deployment failures 40%. Manufacturing firms report lower factory downtime and swifter innovation cycles, while 93% of financial institutions drive rapid service delivery with embedded security. [2]Microsoft Corp., “FY25 Second Quarter Earnings Call,” microsoft.comAutomation improves code quality 30% and trims mean-time-to-recovery 25%, shifting staff focus from repetitive tasks to innovation.

Cloud-native and micro-services proliferation

Cloud services are used by 94% of enterprises to heighten scalability. [3]IEEE Computer Society, “How DevOps and Cloud-Native Architecture Go Hand-in-Hand,” computer.org Banks anticipate that 75% will adopt hybrid strategies by 2026, allowing sensitive workloads on-premises while exploiting cloud elasticity for development. DevOps aligned with microservices supports frequent feature releases and limits systemic failure risk. Talent demand now favors engineers fluent in both cloud-platform tooling and DevOps methodologies.

Large-scale digital-transformation and agile uptake

Digital-transformation spending in BFSI stood at USD 93.04 billion in 2024 and is set to reach USD 108.51 billion in 2025. DevOps integration with agile programs yields 29% faster releases and 20% higher customer satisfaction. Industry 4.0 in manufacturing counts on Industrial DevOps for synchronized IT and OT delivery cycles. Skills-based hiring is rising as 81% of organizations widen candidate pools to secure DevOps talent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy–to–micro-services migration complexity | -2.1% | Global, with higher impact in industries with significant legacy systems | Medium term (2-4 years) |

| Multi-cloud security and compliance risks | -1.8% | Global, with higher impact in highly regulated industries | Medium term (2-4 years) |

| Shortage of skilled DevOps engineers and cultural inertia | -2.5% | Global, with varying impact based on regional talent pools | Short term (≤ 2 years) |

| Toolchain sprawl causing observability blind-spots | -1.6% | Global, with higher impact in large enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy-to-micro-services migration complexity

Sixty percent of firms deem DevSecOps adoption technically challenging. [4]Zscaler Inc., “Q2 FY2025 Results,” sec.gov Financial institutions face cost overruns exceeding 30% due to unforeseen integration hurdles. SMEs with limited budgets experience amplified risk, prompting vendors to offer automated refactoring and data-integrity safeguards to ease transitions.

Multi-cloud security and compliance risks

Fifty-three percent of APAC organizations encounter high-impact outages each week. Governance gaps raise vulnerability exposure as 73% of enterprises struggle with policy consistency across clouds. Zero-trust frameworks gain traction, and DevSecOps spending is projected to reach USD 41.66 billion by 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead, Services Accelerate

Solutions accounted for 59.65% of 2025 revenue, anchoring automation, integration, and collaboration workflows across the DevOps market. Source-control management and CI/CD attracted the highest deployment rates, delivering 40% higher release throughput and 25% lower error incidence. Vendors are layering AI modules that predict pipeline failures and optimize resource use, improving operational resilience.

The services segment is forecast to record a 23.1% CAGR to 2031. Enterprises rely on consulting, training, and managed offerings to bridge skills gaps and handle complex toolchains. Demand spikes for managed DevSecOps platforms that combine advisory and execution. Average US DevSecOps engineer compensation of USD 140,000 illustrates talent scarcity, channeling budget toward external providers.

By Deployment Model: Hybrid Cloud Ascendancy

Public cloud captured 44.70% of 2025 revenue, reflecting ease of access to native tool ecosystems. Mature marketplaces from AWS, Microsoft, and Google let teams onboard DevOps pipelines with reduced integration overhead. Yet regulated workloads often remain on private infrastructure.

Hybrid-cloud adoption will post a 24.1% CAGR through 2031, creating the largest incremental opportunity for the DevOps market. Financial services institutions anticipate 75% hybrid utilization by 2026, balancing sovereignty with scalability. Organizations deploy unified policy engines and observability layers to preserve a consistent experience across on-premises and cloud assets.

By Organization Size: Enterprise Dominance, SME Momentum

Large enterprises generated 64.05% of 2025 sales, supported by cross-business mandates and capital for end-to-end platform rollouts. DevOps centers of excellence embed standardized practices, governance, and talent pipelines. This scale lowers per-unit tooling costs and accelerates innovation.

SMEs will expand at a 21.2% CAGR, narrowing capability gaps with larger peers. Cloud-based starter kits reduce upfront investment, and pay-as-you-grow pricing aligns with constrained budgets. Successful SME pilots report 200% deployment-frequency gains and 50% faster time-to-market, driving peer adoption. Methodologies tailored for SME constraints, such as lean DevOps frameworks, are gaining traction.

By End-User Industry: Healthcare Acceleration

IT & telecom firms held 25.05% of 2025 revenue as early adopters and creators of core DevOps tooling. Telecommunications operators lean on pipeline automation to roll out network functions and customer-facing apps reliably.

Healthcare and life sciences will be the fastest segment at 28.1% CAGR to 2031, propelled by telehealth growth, AI diagnostics, and stringent uptime needs. Continuous deployment enables rapid clinical software updates while sustaining compliance. Emerging use cases such as connected medical devices demand stable, repeatable deployment models.

Geography Analysis

North America contributed 37.85% of 2025 revenue. A dense concentration of hyperscale cloud providers, venture-backed software vendors, and early adopter enterprises underpins regional leadership. The IT sector produced 39% of regional DevOps market revenue in 2024, and AI-enabled tool launches maintain the innovation cycle.

Asia-Pacific will post the highest regional CAGR of 25.4% through 2031. India, China, and ASEAN economies accelerate cloud spending to support digital objectives. In India, 65% of organizations report high-impact outages, raising urgency for resilient DevOps practices. South Korea records the highest outage cost bracket, exceeding USD 1 million per hour for 92% of firms, reinforcing adoption impetus.

Europe is scaling rapidly under tightening regulations. Germany is projected to log USD 1.13 billion in cloud-based DevOps tools revenue by 2031. GDPR drives DevSecOps implementation for data-protection alignment. Consolidation is visible; Eficode’s acquisition of Solidify strengthens GitHub services across the region, mirroring a trend toward specialist consultancies.

Competitive Landscape

The DevOps market shows moderate concentration as cloud hyperscalers, integrated-platform specialists, and niche innovators vie for share. AWS, Microsoft, and Google bundle infrastructure with pipeline tooling, lowering entry friction and locking in workloads. GitLab’s integrated DevSecOps platform recorded USD 759.2 million revenue in FY 2025, up 31% year over year.

Consolidation is intensifying. Eficode’s Solidify takeover broadens GitHub consulting depth and AI capabilities. Strategic alliances, such as JFrog’s partnership with Hugging Face, embed ML model management within secure pipelines and broaden platform stickiness. Vendors differentiate by automating security scans, dependency checks, and policy enforcement to meet zero-trust mandates.

White-space opportunities include AI-driven observability, verticalized solutions for regulated industries, and simplified packages for SMEs. Providers able to fuse low-code, security, and compliance in an integrated experience are poised to capture incremental DevOps market demand.

DevOps Industry Leaders

Google LLC

Microsoft Corporation

IBM Corporation

Oracle Corporation

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Eficode acquired Solidify to bolster GitHub, Azure DevOps, and AI expertise across EMEA, aligning with its 70% four-year CAGR growth trajectory.

- May 2025: JFrog Ltd. posted 22% Q1 2025 revenue growth to USD 122.4 million and launched JFrog ML, partnering with Hugging Face to integrate AI asset management.

- May 2025: L&T Technology Services and Tennant Company created an offshore development center to advance IoT-enabled industrial cleaning technologies.

- March 2025: GitLab recorded USD 211.4 million Q4 revenue and introduced Duo Self-Hosted to enhance data-residency controls for enterprises.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the DevOps market as the global spend generated when organizations buy software platforms and related services that integrate software development and IT operations to automate continuous integration, delivery, testing, and infrastructure provisioning. Revenues flowing from one-time license, subscription, and managed support contracts tied to DevOps toolchains, orchestration layers, and advisory or implementation services are counted by Mordor Intelligence.

Scope exclusion: we leave out pure-play security-only (DevSecOps) tools sold as standalone offerings, as well as generic cloud infrastructure services that do not directly enable DevOps workflows.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- On-Premises

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- BFSI

- Retail and eCommerce

- Government and Public Sector

- Manufacturing

- IT and Telecommunications

- Healthcare and Life Sciences

- Media and Entertainment

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed senior DevOps engineers, cloud architects, and procurement managers across North America, Europe, Asia-Pacific, and the Gulf to validate price bands, typical seat counts, and toolchain mix. Follow-up surveys with platform vendors and system integrators clarified renewal cycles, service attach rates, and regional discounting practices.

Desk Research

We began with macro data sets from entities such as the World Bank, OECD ICT accounts, and national statistics portals that track enterprise software outlays. Sector-level adoption cues were drawn from industry associations like the Cloud Native Computing Foundation, IEEE, and regional IT services trade bodies, complemented by public 10-K filings, earnings transcripts, and patent analytics pulled through Questel and Dow Jones Factiva. Selected shipment-level insights from Volza and tender notices on Tenders Info helped us triangulate regional project momentum. The sources cited are illustrative; our analysts referred to many additional open datasets for cross checks and context.

Market-Sizing & Forecasting

A combined top-down build (enterprise software spending reconstructed from government ICT tables and enterprise adoption ratios) is reconciled with selective bottom-up checks such as average selling price times active user seats reported in supplier interviews. Key model inputs include: 1) cloud migration rate, 2) average CI/CD pipeline penetration inside target verticals, 3) share of hybrid versus public cloud deployments, 4) developer headcount growth, and 5) median DevOps tool ASP decline. We forecast each driver with multivariate regression and apply scenario analysis for currency shifts and macro shocks before rolling totals into a 2019-2030 view. Gaps in granular bottom-up data are bridged through ratio benchmarks agreed with interviewed experts.

Data Validation & Update Cycle

Outputs undergo variance checks against secondary indicators, peer benchmarks, and prior editions. An internal reviewer signs off after anomaly resolution. The model is refreshed annually, with interim updates when material events, such as major M&A or pricing resets, distort the baseline.

Why Our Devops Baseline Commands Reliability

Published estimates differ because firms pick distinct scopes, refresh cadences, and conversion methods. By anchoring numbers to verifiable enterprise software spend and substantiating tool usage through field interviews, Mordor Intelligence offers a balanced, repeatable baseline decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.13 B (2025) | Mordor Intelligence | - |

| USD 13.16 B (2024) | Global Consultancy A | Excludes professional services revenue and uses 2023 FX rates |

| USD 12.66 B (2024) | Industry Association B | Relies on historical install base without adjusting for cloud-first seat growth |

| USD 12.54 B (2023) | Regional Consultancy C | Older base year and narrower definition limited to DevOps software licenses only |

In sum, our disciplined scope selection, transparent variable mapping, and annual refresh underpin a dependable market view while explaining why other published values trend lower or diverge on different timelines.

Key Questions Answered in the Report

What is the current value of the DevOps market and its growth outlook?

The DevOps market stands at USD 19.57 billion in 2026 and is projected to reach USD 51.43 billion by 2031, reflecting a 21.33% CAGR.

Which region is growing the fastest in DevOps adoption?

Asia-Pacific is forecast to grow at a 25.4% CAGR through 2031, supported by large-scale digital-transformation projects and expanding cloud investments.

Why is hybrid cloud important to DevOps strategies?

Hybrid cloud blends public-cloud scalability with private-infrastructure control, supporting consistent DevOps practices while meeting data-sovereignty and regulatory requirements.

What challenges do organizations face when migrating from legacy systems to micro-services?

Key hurdles include integration complexity, budget overruns, and compliance constraints, with 60% of firms labeling DevSecOps implementation technically difficult.

How are security concerns influencing DevOps tool selection?

The shift toward DevSecOps embeds automated vulnerability scanning and zero-trust principles directly into pipelines, driving demand for unified platforms that address security and compliance by design.

Which industry vertical is expected to adopt DevOps the fastest?

Healthcare and life sciences are projected to record a 28.1% CAGR to 2031 as telehealth, AI diagnostics, and data analytics heighten the need for agile, reliable software delivery.

Page last updated on: