Deep Fryers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

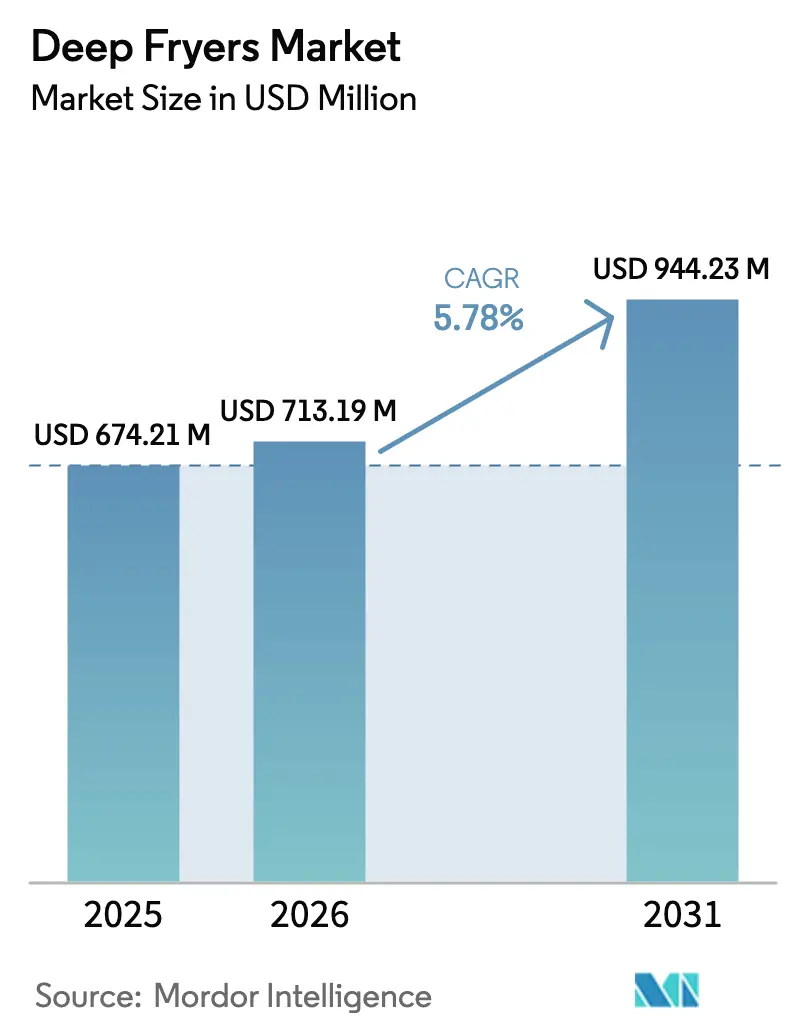

| Market Size (2026) | USD 713.19 Million |

| Market Size (2031) | USD 944.23 Million |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

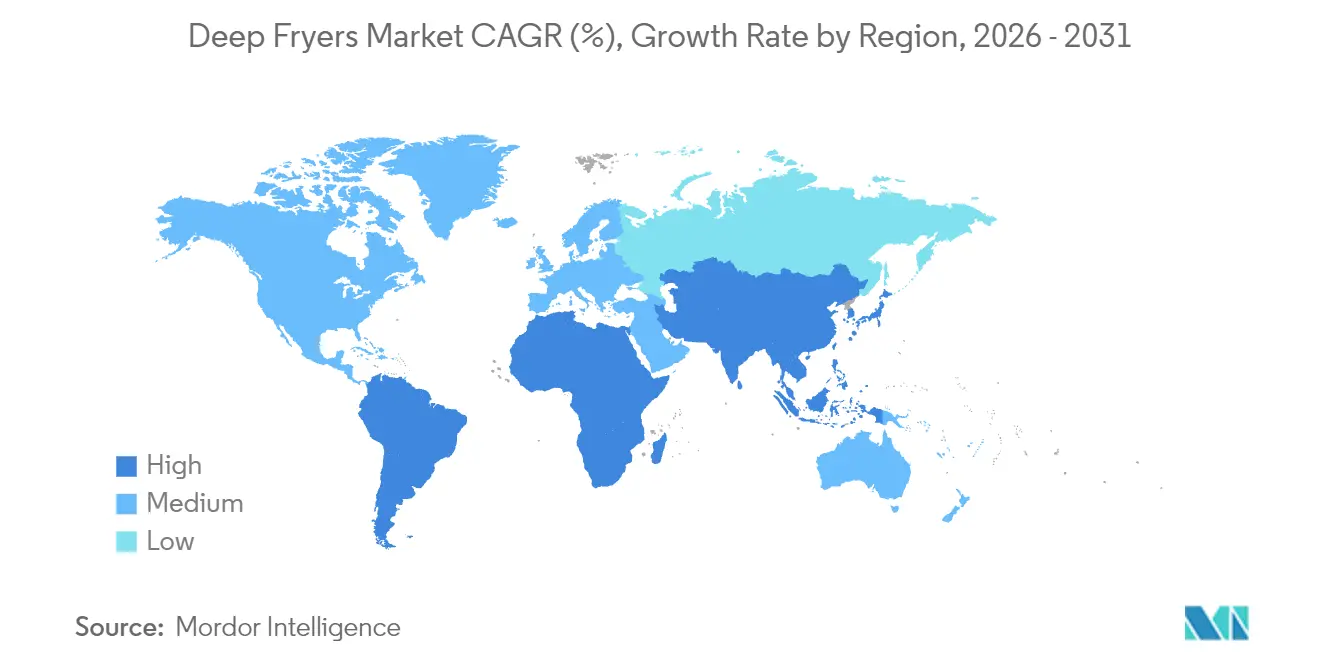

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

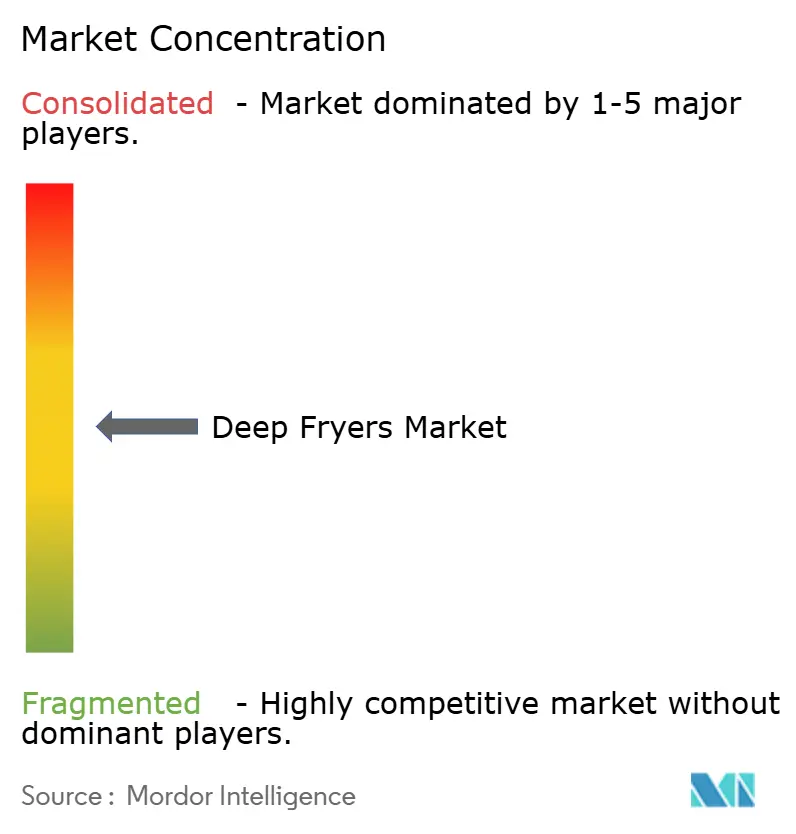

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deep Fryers Market Analysis by Mordor Intelligence

The deep fryers market size is projected to be USD 674.21 million in 2025, USD 713.19 million in 2026, and reach USD 944.23 million by 2031, growing at a CAGR of 5.78% from 2026 to 2031. The global deep fryer market is experiencing significant growth, driven by increasing demand for quick and convenient cooking methods, particularly in fast food and commercial kitchens. The rise of foodservice industries, including restaurants, cafes, and food chains, has substantially increased the demand for commercial deep fryers. Additionally, the growing popularity of fried food products globally, combined with innovations in oil filtration and energy-efficient models, has further spurred market expansion. In terms of trends, the shift towards healthier cooking options, such as air fryers, is a notable development, with consumers seeking alternatives that reduce oil usage. The market is also witnessing advancements in smart fryer technologies, incorporating IoT features for improved efficiency and ease of use.

Key Report Takeaways

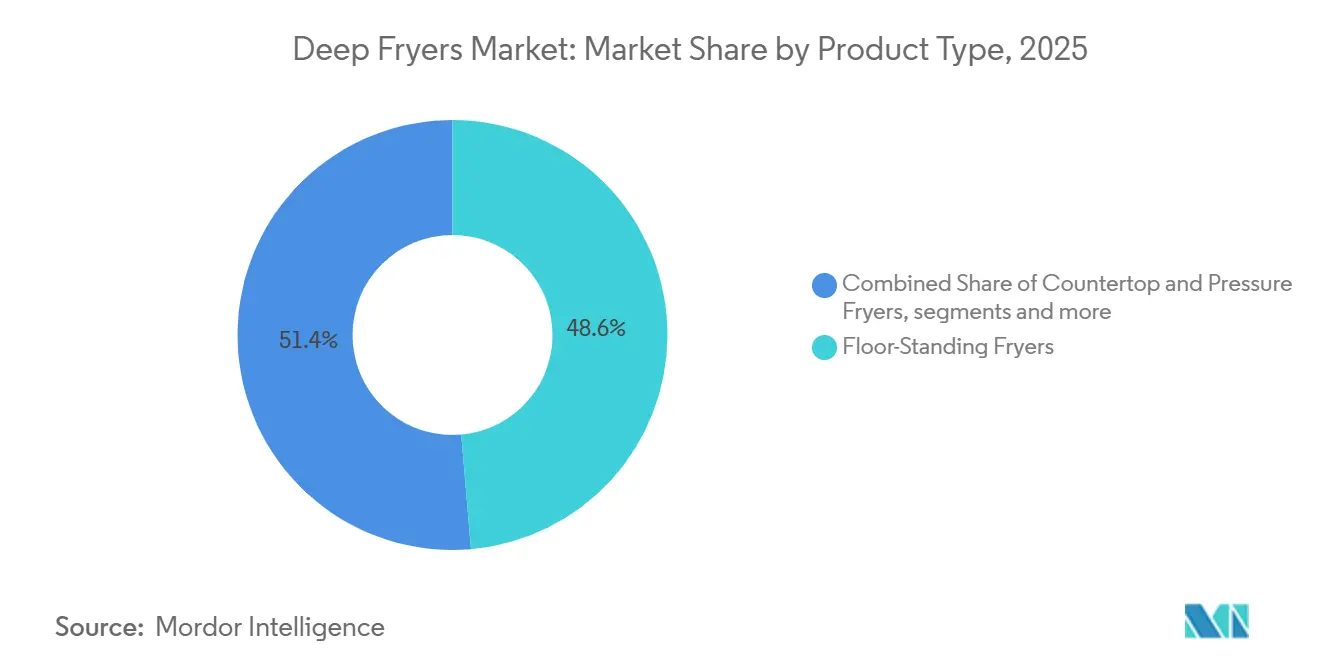

- By product type, floor-standing units led with 48.62% shares of the deep fryers market in 2025; ventless models are forecast to grow at a 9.36% CAGR through 2031.

- By heating source, gas units captured 57.83% of the deep fryers market share in 2025; induction platforms are projected to expand at an 11.05% CAGR through 2031.

- By end-user, QSR and FSR restaurants accounted for 42.10% of the deep fryers market in 2025 demand; food trucks and cloud kitchens are set to grow at a 12.10% CAGR through 2031.

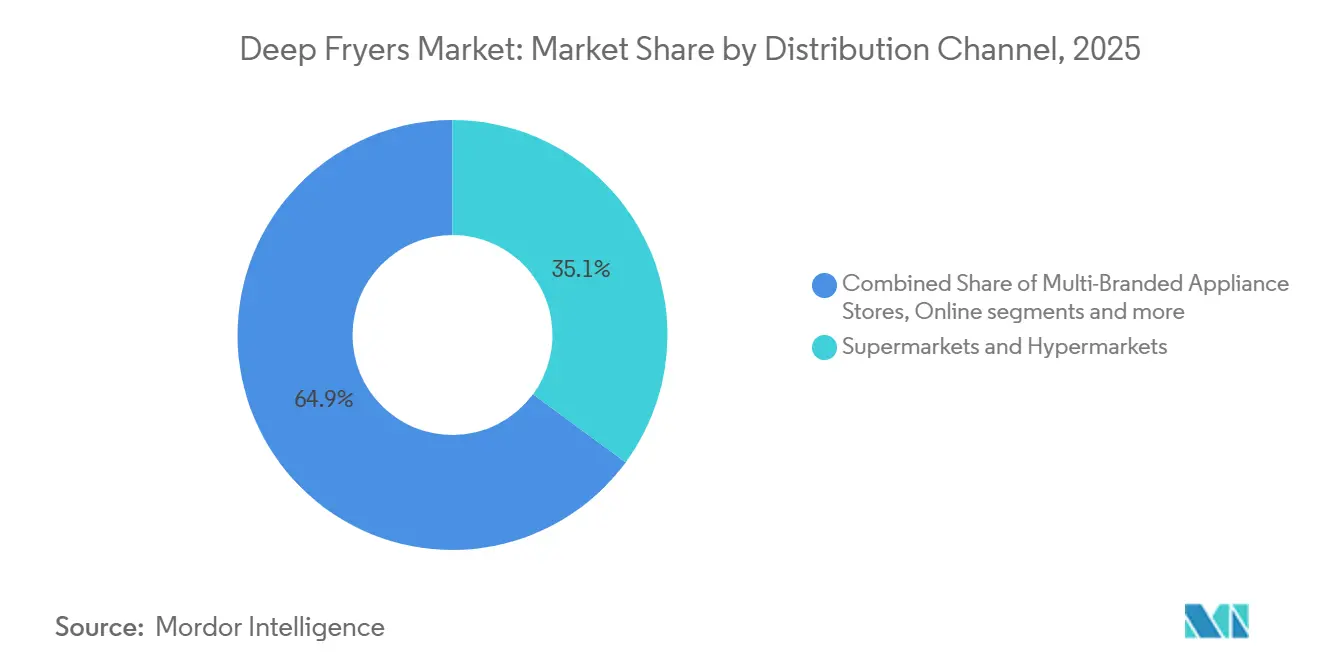

- By distribution channel, supermarkets and hypermarkets commanded 35.05% of sales in 2025; online marketplaces are expected to grow at a 9.78% CAGR through 2031.

- By geography, North America held 32.05% of demand in 2025; Asia-Pacific is the fastest-growing region with an 8.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Deep Fryers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| QSR/FSR New-Unit Growth and Remodeling, Sustaining Fryer Replacement Cycles | +1.2% | Global, with early gains in North America, Asia-Pacific metropolitan clusters | Medium term (2-4 years) |

| Cloud Kitchens and Food Trucks Are Expanding Demand for Compact, High-Throughput Fryers | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa, urban clusters in North America, and the European Union | Medium term (2-4 years) |

| Energy-Efficiency and Electrification Policies Are Accelerating The Adoption of Electric/Induction | +0.8% | North America, the European Union, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Advances In Oil Filtration and Automated Oil Management Are Reducing The Total Cost of Ownership | +0.7% | Global | Short term (≤ 2 years) |

| Induction Fryers Lowering Heat Load And HVAC Requirements in Micro-Kitchens | +0.6% | North America and the European Union | Medium term (2-4 years) |

| Allergen Segregation Is Driving Dedicated or Specialty Fryers | +0.5% | North America and the European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

QSR/FSR New-Unit Growth and Remodeling Sustaining Fryer Replacement Cycles

Aggressive chain expansion and standardized back-of-house specifications continue to translate into steady fryer procurement and predictable replacement cycles averaging 7 to 10 years for high-volume stores. Operators use remodels and kitchen refresh projects to lock in higher-efficiency equipment that reduces energy and maintenance costs while meeting corporate sustainability targets. This behavior benefits the deep fryers market as multi-unit brands negotiate fleet-wide specifications across floor-standing, filtration-equipped, and hood-compatible models. The strategy also supports the adoption of ENERGY STAR-style performance thresholds where available and aligns procurement with electrification roadmaps in priority jurisdictions. The continued cadence of store openings and remodels helps smooth quarterly order cycles for OEMs and dealers and sustains an installed base that feeds aftermarket services.

Cloud Kitchens and Food Trucks Expanding Demand for Compact, High-Throughput Fryers

Urban delivery formats and mobile operations are prioritizing compact, ventless, and modular fryers that bypass local ventilation constraints and reduce permitting risk. Ventless fryers that integrate catalytic filtration enable installation in non-traditional sites and support quick commissioning for delivery-only kitchens and small-footprint units. Food truck operators select countertop models with rapid recovery and small oil volumes, typically under 30 inches wide and priced from USD 500 to USD 2,000 for mainstream configurations. Retailers have reported growing interest in ventless platforms since late 2025, signaling broader acceptance of infrastructure-light solutions for constrained real estate. Specification choices in these formats often emphasize ease of cleaning, built-in filtration, and short preheat times to support throughput within tight labor windows.

Energy-Efficiency and Electrification Policies Accelerating Adoption of Electric/Induction Platforms

Proposed commercial fryer standards in California target 56% minimum cooking efficiency and 8,000 Btu per hour idle-energy rates for standard-vat gas models and are under active consideration for implementation milestones beginning in 2025. The European Union’s Energy Efficiency Directive requires annual end-use savings that step up from 2026 to 2030 and drives energy audits for large users, which strengthens the case for high-efficiency equipment upgrades in foodservice. Switzerland implemented minimum energy-efficiency requirements for commercial fryers in 2024 as part of a broader push to improve performance in professional kitchens[1]Federal Office of Energy Editorial Team, “Minimum Energy Performance for Professional Kitchen Appliances,” Swiss Federal Office of Energy, bfe.admin.ch. Induction platforms deliver high thermal efficiency compared with open-flame gas and can materially reduce waste heat in the cookline, which lowers HVAC tonnage requirements in compact stores. Together, these policies and performance gains favor higher-velocity adoption of electric and induction fryers in new builds and electrification-focused retrofits.

Advances in Oil Filtration and Automated Oil Management: Reducing Total Cost of Ownership

Automated filtration and oil-quality monitoring can extend oil life and reduce purchase frequency, which lowers recurring costs for chains with high fryer utilization. Frymaster’s FilterQuick Infinity system is designed to automate top-off and filtration tasks and can extend usable oil life compared with manual routines, improving consistency and food quality. Mobile filtration units and plumbed-in solutions reduce labor needed for oil handling and can produce a return on investment within months when oil savings and time savings are accounted for[2]Solutions Team, “Commercial Kitchen Parts and Filtration ROI Notes,” PartsFe, partsfe.com. Manufacturers are also embedding connectivity to enable alerts for filtration cycles and oil changes that minimize downtime and support food safety records. These savings compound when paired with efficient heating systems that limit thermal degradation of oil and stabilize cook temperature under heavy load.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-Driven Menu Shifts and Consumer Perception Limiting Deep-Fried Demand | -0.60% | North America and Western Europe | Long term (≥ 4 years) |

| High Energy Costs and HVAC Loads Raising Operating Expenses for Legacy Vented or Gas Kitchens | -0.50% | Global, most acute in North America and the European Union | Medium term (2-4 years) |

| Ventilation and Fire-Suppression Permitting Complexity Delaying Installations | -0.40% | North America and the European Union | Medium term (2-4 years) |

| Robust Refurbished Equipment Supply Lengthening Replacement Cycles for Independents | -0.30% | Global, most acute in Latin America, and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health-Driven Menu Shifts and Consumer Perception Curbing Deep-Fried Category Growth

Menu innovation has favored lower-oil preparations and stricter control of process contaminants, which moderates growth in traditional deep-fried lines over time. European Union Regulation 2017/2158 requires food businesses to apply acrylamide mitigation measures during frying, including temperature control below 175°C for specific products, blanching where relevant, and maintaining oil quality through proper filtration and change-out procedures. This framework has increased process discipline and raised the bar for fryer temperature accuracy and oil-management features in equipment procurement. Allergen management has also encouraged the use of dedicated fryers to separate gluten-containing foods from gluten-free items, which affects planning and capital footprints in chains with broad menus. The regulatory and consumer context continues to nudge operators toward equipment with tight temperature control, filtration, and documentation capability to support food safety and labeling requirements[3]Center for Food Safety and Applied Nutrition, “Food Allergen Labeling and Guidance,” U.S. Food and Drug Administration, fda.gov.

High Energy Costs and HVAC Loads Increasing Operating Expenses for Legacy Vented/Gas Kitchens

Legacy gas installations radiate significant waste heat into the kitchen, which increases HVAC loads and can elevate refrigeration energy consumption in busy restaurants. Induction platforms reduce ambient heat by up to 10°C and can lower cooling tonnage requirements, which helps control utility costs and improve worker comfort in compact kitchens. Proposed efficiency standards in California and emerging electrification policies raise expected performance for new fryers and favor efficient electric and induction options over low-efficiency legacy designs. Conversion to electric or induction can require an upfront premium versus baseline gas units, which may slow adoption among capital-constrained independents despite favorable total cost of ownership for many sites. Over the medium term, operators that standardize efficient electric platforms and pair them with disciplined oil management are positioned to blunt energy volatility and stabilize back-of-house costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Floor Units Anchor Volume, Ventless Models Capture Retrofit Wave

Floor-standing fryers accounted for 48.62% of shipments in 2025 and remain the primary specification among high-throughput quick-service and full-service operators. This configuration supports large oil capacities and rapid recovery, which is essential for peak-hour output and consistent food quality across chain menus. Ventless models are expanding at a 9.36% CAGR through 2031 as operators retrofit in sites where hood installation is impractical or cost-prohibitive, and where speed to open is a priority. The deep fryers market benefits from broader acceptance of self-contained filtration and catalytic systems that enable compliance and reduce build-out complexity in malls, food courts, and micro-formats. Countertop fryers address cafés, delis, and mobile units with compact footprints and lower absolute purchase cost, with mainstream models ranging from USD 500 to USD 2,000.

NFPA 96 requirements for Type I hoods and UL 300-compliant wet-chemical suppression continue to shape equipment selection and site design, which sustains demand for models validated for integration with certified suppression systems. Specialty and pressure fryers serve niche menus such as bone-in chicken or donuts, where pressure cooking and unique vat geometries enhance product texture and moisture retention. As the deep fryers industry focuses on ease of cleaning, oil lifecycle, and filtration automation, OEMs are adding features that reduce downtime and labor while supporting food safety records. These features align with large operators’ needs to standardize service protocols and maximize uptime across wide networks. With space and permitting constraints more visible across urban footprints, ventless and countertop models extend the addressable base for the deep fryers market.

By Heating Source: Gas Incumbency Faces Induction’s Efficiency Surge

Gas units held 57.83% of 2025 demand, reflecting legacy infrastructure and fast heat-up and recovery that have historically favored gas specifications in many chain fleets. At the same time, induction platforms are projected to expand at an 11.05% CAGR through 2031 due to electrification policies and to lower HVAC loads associated with reduced radiant heat in compact or ventless configurations. High thermal efficiency for induction compared to open-flame gas reduces wasted energy and supports tighter temperature control, which helps stabilize product quality at peak. Proposed California standards for cooking efficiency and idle rates further support energy-optimized designs and sharpen the case for electric or induction across retrofits and new builds. For sites that rely on propane, conversion kits allow fuel flexibility, and policy developments increasingly weigh on the trajectory of new gas installations.

Across many geographies, procurement teams are writing specifications that anticipate future electrification rules and energy audits, which press operators to evaluate lifecycle costs beyond initial purchase price. In this context, energy performance, ambient heat reduction, and oil-management compatibility are rising as selection criteria for the deep fryers market. Operators also consider utility rates and site electrical capacity alongside hood requirements and make-ready costs to determine optimal heating source by location. As restrictions on open flame cooking expand in dense urban cores, induction systems and efficient electric vats gain traction in micro-kitchens and in venues with strict ventilation rules. These adoption patterns are reinforcing momentum behind connected, energy-efficient models in the deep fryers industry.

By End-User: QSR/FSR Dominance Coexists with Double-Digit Cloud-Kitchen Growth

QSR and FSR restaurants accounted for 42.10% of demand in 2025 as large chains sustained replacement cycles and standardized on specification-grade equipment to protect uptime and food quality. Kitchen refresh programs are an important catalyst for upgrading to efficient, filtration-integrated vats that align with brand sustainability and cost objectives. Food trucks and cloud kitchens are projected to grow at a 12.10% CAGR through 2031 and are favoring compact, ventless, and stackable configurations that improve installation agility across constrained buildings. These formats often require small oil capacities, quick preheat and recovery, and easy-to-service filtration to support high-turnover menus and tight prep areas. Hotels and resorts continue to rely on floor-standing and pressure units to support banquets and buffets where consistent batch output is essential.

Institutional and catering buyers, including education and healthcare, are centralizing on easy-to-clean designs and documented allergen segregation, supported by dedicated fryers where menus require it. Investment decisions in these segments refer to energy performance and noise and heat profiles, especially in facilities that have modern HVAC systems with strict thresholds installed. Ventless options are attractive when hood installation is challenging or when commissioning speed and site flexibility matter more than absolute peak throughput. The deep fryers market also sees steady retrofit interest among independents that prioritize lifecycle costs and reliability over initial list price. Over time, the end-user mix continues to shift toward flexible, electrification-ready equipment that balances performance with compliance obligations.

By Distribution Channel: Offline Leads, Yet E-commerce Captures B2B Procurement Digitization

Supermarkets and hypermarkets accounted for 35.05% of sales in 2025 as small businesses and households sourced countertop models through retail aisles and local dealer partners. Multi-brand appliance stores give operators a side-by-side view of vat sizes, filtration features, and control systems while enabling same-week installation and in-person service options. Online marketplaces are projected to grow at a 9.78% CAGR through 2031 as procurement digitizes, and manufacturers expand direct-to-operator models that include warranty registration and configuration tools. Direct sales and dealer networks remain the backbone for multi-unit chains that need custom specifications and coordinated rollouts with technician training and connected-kitchen integration. As operators compare lifecycle economics, channel partners that bundle financing, filtration consumables, and service contracts can gain share in the deep fryers market.

Refurbished equipment ecosystems extend replacement cycles among cost-sensitive independents and small operators, which can temper new-unit growth in some local markets. For OEMs and dealers, pre-owned channels also serve as trade-in paths that support upgrades to energy-efficient models in high-usage stores. E-commerce platforms play a larger role in spare parts, filtration media, and accessories, reinforcing value across the installed base. Over time, omnichannel approaches that match product complexity and service intensity to the right route to market will shape share dynamics across regions. These shifts keep the deep fryers market competitive while improving buyer access to specification-grade products and service capabilities.

Geography Analysis

North America held 32.05% of global demand in 2025, supported by dense QSR penetration and mature replacement cycles that average 7 to 10 years in high-volume chain locations. Growth in the region is projected at 3.50% CAGR through 2031 as remodeling programs emphasize energy compliance and as ventless retrofits expand in older sites without modern hoods. Proposed California standards for gas fryer efficiency and idle rates and broader electrification initiatives in key metros are steering new projects toward electric and induction platforms. Building codes and fire-safety frameworks that include NFPA 96 and UL 300 have long anchored specification decisions and continue to shape equipment integration and service schedules.

Asia-Pacific is the fastest-growing region with an 8.42% CAGR through 2031 as QSR networks scale and as urbanization and rising incomes increase spending on limited-service formats. Online marketplaces are an important route to market for small operators and are contributing to faster access to specification-grade products, training materials, and consumables. In several dense metropolitan areas, standards are favoring electric and induction as compliance paths for new installations, which strengthens the case for induction-ready and ventless models. These dynamics support sustained demand for equipment that balances throughput, compact footprints, and energy performance as the deep fryers market expands in the region.

Europe, excluding Russia, is projected to grow at a 3.00% CAGR through 2031, with replacement and modernization cycles tied to efficiency mandates and acrylamide mitigation rules set under European Union Regulation 2017/2158. The European Union’s Energy Efficiency Directive requires annual energy savings and energy audits for large users beginning in 2026, which guide procurement toward higher-performance models and systematic energy management. Switzerland moved first with minimum energy-efficiency requirements for commercial fryers in 2024, offering a policy reference for neighbors that plan efficiency regulations for professional kitchens. Russia’s segment is projected at 2.00% CAGR, while South America is at 3.80% and Western Asia at 4.00%, with Africa at 3.50% and Oceania at 2.80%, anchored by a strong local OEM presence supplying floor-standing and countertop portfolios.

Competitive Landscape

The deep fryers market remains moderately concentrated, with top players like Ali Group and Middleby holding substantial shares in the market. Ali Group’s 2022 acquisition of Welbilt expanded its scale and product breadth across commercial foodservice equipment, including top fryer brands and connected-kitchen capabilities. Middleby completed the sale of a 51% stake in its Residential Kitchen business to 26North Partners in February 2026 to sharpen its focus as a commercial foodservice leader[4]Investor Relations Team, “Company Overview and Portfolio,” Middleby, middleby.com. Both companies continue to invest in filtration, controls, and service networks that support fleet standardization among large chains.

Innovation priorities include automated filtration, oil lifecycle management, and IoT-enabled remote diagnostics to reduce downtime and improve food quality consistency. Frymaster’s FilterQuick Infinity automates top-off and filtration workflows to extend oil life and reduce manual handling risk, while connected platforms alert teams to maintenance events and compliance schedules. Welbilt’s KitchenConnect has worked with ecosystem partners to integrate secure connectivity for back-of-house assets, improving data visibility and enabling energy-management use cases. Henny Penny expanded international distribution in 2025 and has continued to invest in service infrastructure, including a new Global Services Center to support global customers.

Strategic emphasis among leading players spans retrofit electrification packages for legacy kitchens, filtration media, and oil recycling partnerships to lower cost and waste, and compact high-throughput fryers for mobile and micro-format sites. Compliance with NFPA 96 and UL 300 remains a barrier that protects established brands with certified integrations and technician networks. Regional OEMs and value brands compete on price and localized service, although dealer reach and after-sales capabilities often determine adoption in fragmented markets. As procurement digitizes, connected equipment and data-rich service models are shaping differentiation and long-term customer retention in the deep fryers market.

Deep Fryers Industry Leaders

Ali Group

The Middleby Corporation

ITW Food Equipment Group

Electrolux Professional AB

Henny Penny Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Middleby completed the sale of a 51% stake in its Residential Kitchen business to 26North Partners for USD 540 million in cash and a USD 135 million seller note, focusing the company on commercial foodservice systems.

- January 2025: The California Energy Commission proposed enhanced efficiency standards for commercial fryers, including 56% cooking efficiency and 8,000 Btu per hour idle-energy limits for standard-vat gas models.

- January 2025: Henny Penny appointed six new master dealers to strengthen its international distribution footprint.

- December 2024: Electrolux Professional outlined a strategic roadshow, citing operations in 110 countries and a target professional-equipment market of USD 31 billion.

Global Deep Fryers Market Report Scope

A deep fryer is an electronic appliance used in the kitchen to cook various food products. Gas and electric deep fryers are available for domestic and commercial purposes. Deep fryers are available in nest baskets, ventilation systems, and electronic temperature controls.

A deep fryer's market is segmented into product type (floor-standing fryers, countertop fryers, pressure fryers, ventless fryers, and specialty fryers (donut, fish, etc.)), heating sources (gas fryers, electric fryers and induction fryers), end-user (households, quick-service, hotel and resorts, food truck & cloud kitchen and others), distribution channel (supermarket & hypermarket, multibrand store, online marketplace and direct sales), and geography (North America (United States, Canada, Mexico, and Rest of North America), Asia-Pacific (India, China, Japan, Australia, and Rest of Asia-Pacific), South America (Brazil, Argentine, and Rest of South America), Europe (United Kingdom, Germany, Italy, and Rest of Europe), and Middle East and Africa (South Africa, United Arab Emirates, and Rest of Middle East and Africa)). The report offers market size and forecasts for the deep fryers market in value (USD) for all the above segments.

| Floor-Standing Fryers |

| Countertop Fryers |

| Pressure Fryers |

| Ventless Fryers |

| Specialty Fryers (Donut, Fish, etc.) |

| Gas Fryers |

| Electric Fryers |

| Induction Fryers |

| Household |

| Quick-Service (QSR) and Full-Service Restaurants (FSR) |

| Hotels & Resorts |

| Food Trucks & Cloud Kitchens |

| Others (Institutional & Catering etc) |

| Supermarkets & Hypermarkets |

| Multi-Branded Appliance Stores |

| Online Marketplaces |

| Direct Sales |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Floor-Standing Fryers | |

| Countertop Fryers | ||

| Pressure Fryers | ||

| Ventless Fryers | ||

| Specialty Fryers (Donut, Fish, etc.) | ||

| By Heating Source | Gas Fryers | |

| Electric Fryers | ||

| Induction Fryers | ||

| By End User | Household | |

| Quick-Service (QSR) and Full-Service Restaurants (FSR) | ||

| Hotels & Resorts | ||

| Food Trucks & Cloud Kitchens | ||

| Others (Institutional & Catering etc) | ||

| By Distribution Channel | Supermarkets & Hypermarkets | |

| Multi-Branded Appliance Stores | ||

| Online Marketplaces | ||

| Direct Sales | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the deep fryers market size and growth outlook to 2031?

The deep fryers market size was USD 674.21 million in 2025 and is projected to reach USD 944.23 million by 2031, with a 5.78% CAGR over 2026 to 2031.

Which product and heating-source segments lead the deep fryers market?

Floor-standing units led 2025 shipments at 48.62% and gas-fired models held 57.83% share, while ventless and induction platforms show the fastest growth into 2031.

Which end-user segments are expanding fastest in deep fryers?

QSR and FSR restaurants dominated in 2025, while food trucks and cloud kitchens are projected to grow at a 12.10% CAGR through 2031.

What are the top regulatory factors shaping fryer specifications?

Proposed California efficiency standards, European Union Energy Efficiency Directive requirements, and European Union acrylamide mitigation rules drive adoption of efficient electric and induction platforms with stronger oil-management capabilities.

Which regions drive demand and which grow fastest in deep fryers?

North America held 32.05% of the 2025 demand with steady replacement cycles, while Asia-Pacific is the fastest-growing region with an 8.42% CAGR through 2031.

How are rising oil prices impacting fryer design choices?

Volatile oil prices are pushing operators toward models with advanced filtration and low-volume vats that reduce consumption and extend oil life, helping offset input-cost swings.

Page last updated on: