Dairy Herd Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.98 Billion |

| Market Size (2031) | USD 8.32 Billion |

| Growth Rate (2026 - 2031) | 10.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dairy Herd Management Market Analysis by Mordor Intelligence

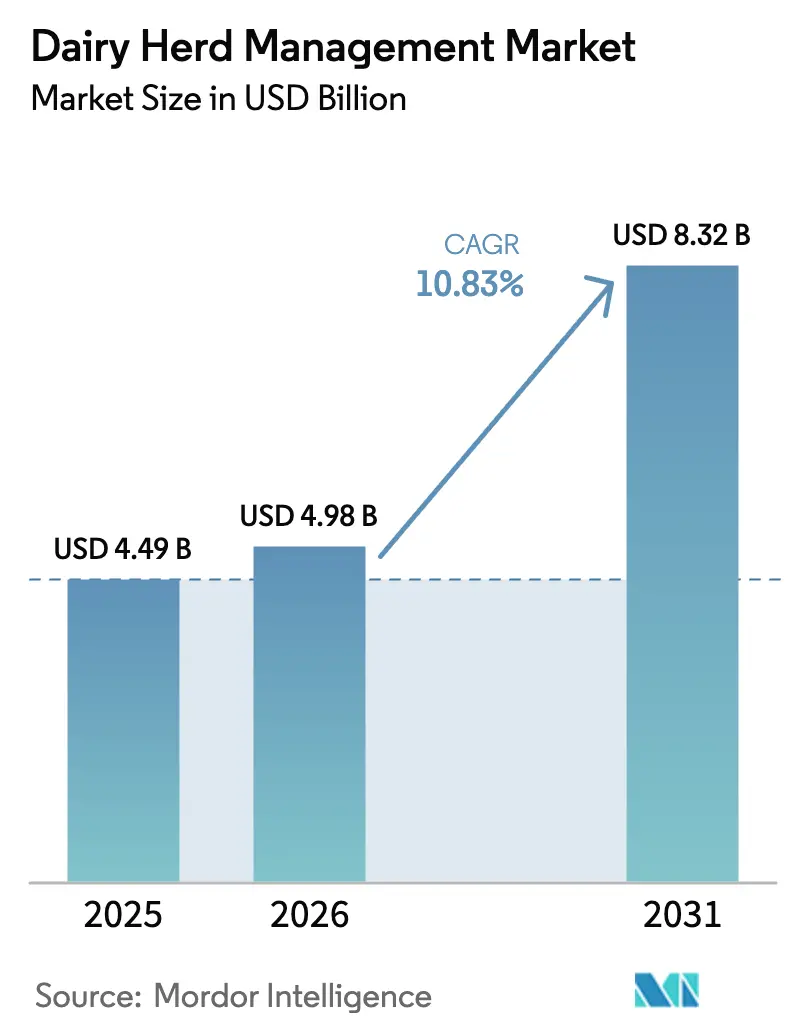

The dairy herd management market size is expected to grow from USD 4.49 billion in 2025 to USD 4.98 billion in 2026 and is forecast to reach USD 8.32 billion by 2031 at 10.83% CAGR over 2026-2031. Rising labor shortages, new methane-emission reporting requirements, and expanding insurance incentives for data-rich farms underpin this growth as producers pivot toward precision livestock farming systems that combine automation with real-time analytics. North America remains the largest adopter, while China’s push for dairy self-sufficiency propels Asia-Pacific as the fastest-growing region. Hardware still represents the bulk of spending, yet software is gaining momentum as farms seek actionable insights that stretch existing capital assets. Medium-sized operations are emerging as technology pace-setters because they can justify selective innovation without committing to fully robotic suites.

Key Report Takeaways

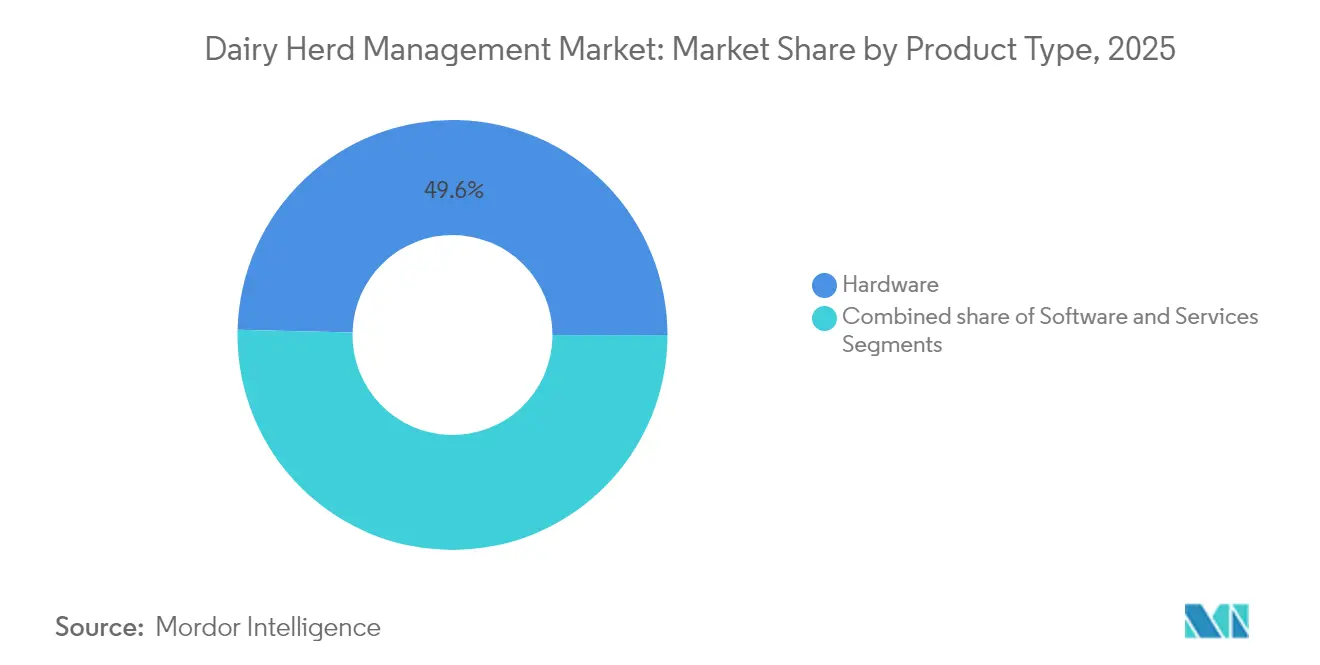

- By product type, hardware led with 49.62% of the dairy herd management market share in 2025, while software is advancing at an 11.05% CAGR through 2031.

- By application, milk harvesting and parlour automation commanded 36.44% share of the dairy herd management market size in 2025, whereas feeding and nutrition solutions are tracking a 11.82% CAGR to 2031

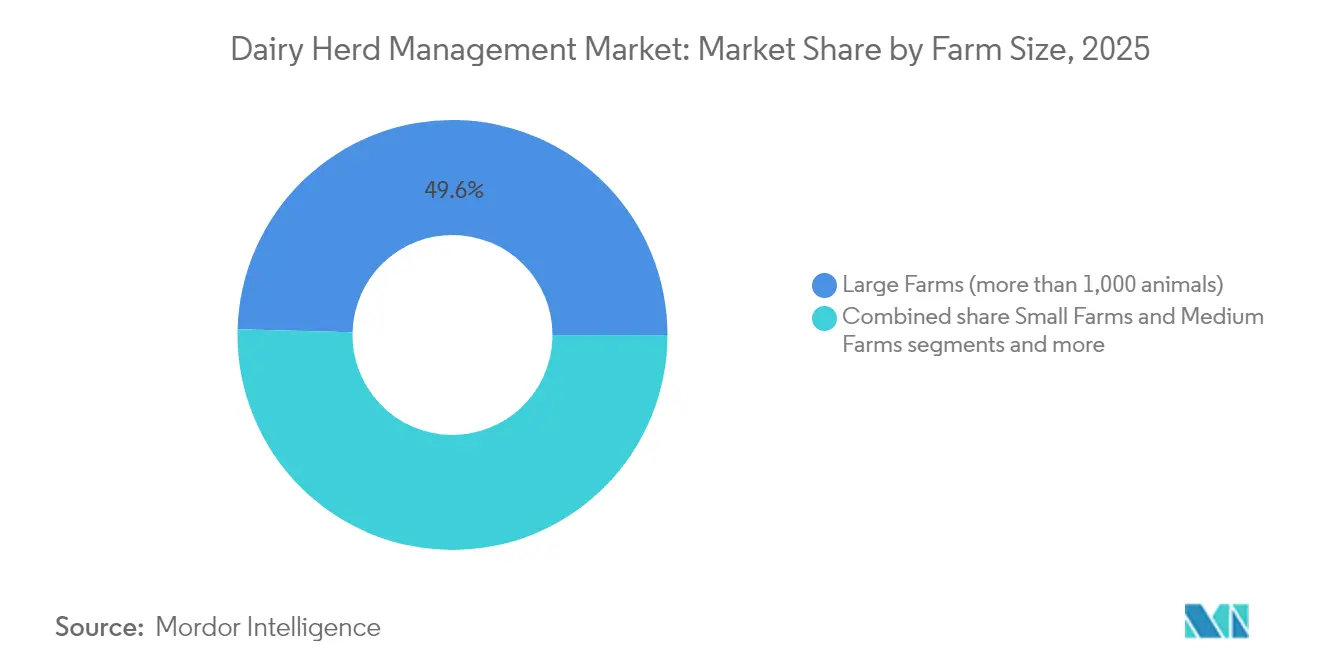

- By farm size, large operations held 49.58% share of the dairy herd management market size in 2025; medium farms are the fastest-growing segment at 12.83% CAGR.

- By deployment mode, on-premise systems accounted for 59.78% share in 2025, but cloud-based platforms are expanding at an 11.01% CAGR through 2031 .

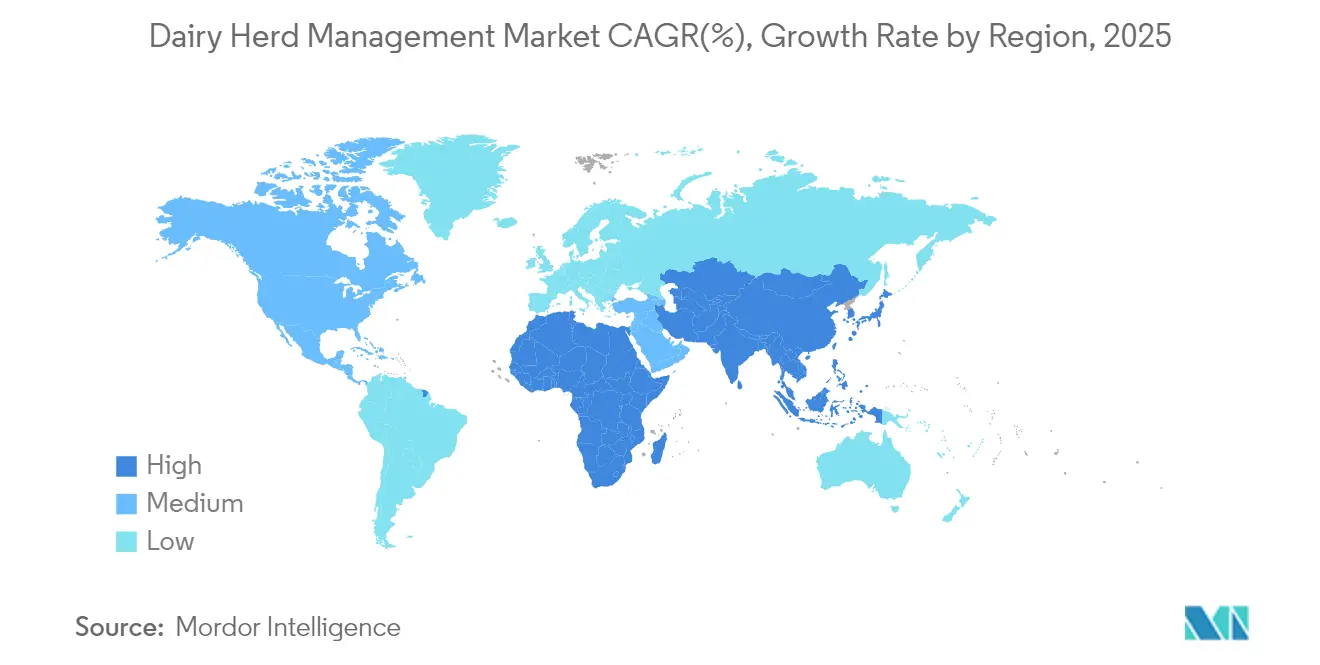

- Regionally, North America captured the largest revenue share in 2025, while Asia-Pacific is projected to post the highest CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dairy Herd Management Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising herd sizes & milk demand | 2.80% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Labor shortages accelerating automation | 3.20% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| IoT-enabled real-time health monitoring | 2.10% | Global, led by developed markets | Medium term (2-4 years) |

| Government productivity & traceability mandates | 1.70% | EU, North America, Australia/New Zealand | Long term (≥ 4 years) |

| Methane-emission reporting driving analytics | 0.90% | EU, California, New Zealand | Long term (≥ 4 years) |

| Insurers tying premiums to granular herd data | 0.80% | North America, expanding to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Herd Sizes & Milk Demand

Intensifying demand for dairy-based nutrition in China and other emerging economies is moving the dairy herd management market toward ever-larger, highly efficient operations. U.S. census data show that 65% of national dairy cattle now reside on farms with more than 1,000 cows, concentrating technology adoption where economies of scale are strongest. As mega-dairies require granular oversight, they prioritize advanced monitoring platforms and thereby accelerate supplier innovation cycles. Continuous growth expectations—80% of global dairy executives forecast volume expansion above 3%—reinforce a technology arms-race orientation among producers[1]Source: Tom Bailey, “Global Dairy Outlook 2025,” mckinsey.com . The resulting feedback loop positions automated tools as non-negotiable, pushing overall system integration deeper into standard operating procedures within the dairy herd management market.

Labor Shortages Accelerating Automation

Average foreign-born dairy workers in the United States are now 42 years old, six years older than their U.S.-born peers, widening succession gaps across daily farm tasks . Automated milking systems, priced between USD 150,000 and USD 275,000 per unit, are gaining traction, with 18% of producers considering short-term adoption plans Hoards. Europe leads penetration, yet North American uptake is climbing as visa constraints tighten labor supply. Far from displacing staff entirely, automation reallocates human labor toward higher-value oversight and data interpretation roles, raising productivity per worker in the dairy herd management market.

IoT-Enabled Real-Time Health Monitoring

Cloud-linked sensor suites such as Merck’s SenseHub now track more than 1 million North American cows, producing behavioural and physiological data that detect health events with 88% accuracy. Scientific studies show 50% reductions in antibiotic usage and 6% yield gains when automated lameness detection enables faster treatment decisions. Computer vision is merging with accelerometers, temperature tags, and rumination monitors to offer predictive health insights that support both regulatory audits and welfare benchmarks. As insurance carriers begin pricing policies based on such data, system adoption delivers direct financial paybacks, solidifying demand within the dairy herd management market.

Government Productivity & Traceability Mandates

Mandatory RFID tagging for interstate cattle movement in the United States takes effect in November 2024, embedding digital traceability into routine management workflows [2]Source: U.S. Department of Agriculture, “RFID Transition Timeline for Cattle Identification,” usda.gov. Australia’s National Agricultural Traceability Strategy invests more than USD 100 million in interoperable data systems, while the EU’s Farm-to-Fork program stresses transparent supply chains. Denmark’s graduated livestock emissions tax begins at 120 kroner per ton in 2030, compelling farms to quantify methane outputs with certified tools. These measures turn comprehensive data collection into a regulatory baseline, expanding addressable demand for integrated platforms in the dairy herd management market

Restraint Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for automated systems | -2.10% | Global, most acute in developing markets | Short term (≤ 2 years) |

| Shortage of skilled tech operators | -1.40% | Global, particularly rural areas | Medium term (2-4 years) |

| Data ownership & cybersecurity concerns | -1.30% | EU and privacy-conscious markets | Medium term (2-4 years) |

| Farm consolidation shrinking small-farm customer base | -0.70% | North America & EU primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Automated Systems

Comprehensive automation packages can cost USD 2 million–USD 4 million for a 600-cow operation, stretching debt ratios for smaller businesses. Developing economies face even tougher credit access barriers despite strong demand growth, slowing global rollout in the dairy herd management market. Leasing models and outcome-based contracts are emerging but remain a fraction of total install volumes.

Data Ownership & Cybersecurity Concerns

Cloud platforms require producers to share granular operational data that some fear could be misused by competitors or regulators. European privacy rules heighten complexity, forcing vendors to invest heavily in encryption and permissioning frameworks before producers will entrust mission-critical datasets to third-party clouds in the dairy herd management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hardware Dominance Faces Software Disruption

Hardware delivered 49.62% of 2025 revenue inside the dairy herd management market, thanks to capital-intensive assets such as automated parlours, smart feeders, and barn-climate controllers. Yet farm priorities are shifting toward data-rich platforms that synthesize sensor outputs, explaining why software subscriptions are advancing at an 11.05% CAGR through 2031. MA Series, which overlays conventional parlour gear with advanced control modules, illustrates this tight coupling of physical machinery and predictive intelligence.

The hardware-to-software pivot parallels broader smart-factory trends: once automation removes labor bottlenecks, returns hinge on making better decisions from the expanded data exhaust. Vendors now position unified dashboards that integrate feed, fertility, and milk-quality records, allowing managers to benchmark performance against regional peers. Predictive maintenance scheduling cuts unplanned downtime, and AI-guided feeding algorithms enhance feed-to-milk conversion ratios. Over the forecast window, suppliers that bundle ruggedized devices with evergreen software updates are expected to capture larger recurring revenue streams, locking farms into brand ecosystems and reshaping competitive boundaries in the dairy herd management market.

By Application: Automation Drives Core Operations

Milking and parlour solutions delivered 36.44% of 2025 revenue, cementing their role as gateway technologies inside the dairy herd management market Topcon. High adoption stems from direct impacts on daily cash flow: every percentage-point in milking efficiency flows straight to the bottom line. Precision feeding platforms, supported by computer-vision bunk scanners and ear-tag rumination sensors, are growing at 11.82% CAGR and will narrow the revenue gap over the next five years. Early disease detection modules, built on accelerometer and thermal data fusion, accelerate treatment and limit milk discard days, offering annual savings above USD 45,000 for a 200-cow herd.

Reproduction monitoring has evolved from basic heat-detection ear tags to AI-enabled algorithms that triangulate activity, temperature, and rumination for >90% estrus detection accuracy. Calf management tools are gaining prominence as farms recognise lifetime productivity links to early-life nutrition and immune status. Manufacturers increasingly bundle multi-application suites, reflecting producer preference for unified interfaces that cut cross-platform data silos. This consolidation trend highlights that long-term value inside the dairy herd management market arises not from stand-alone devices but from full-lifecycle herd visibility.

By Farm Size: Medium Operations Drive Growth

Large herds exceeding 1,000 cows represented 49.58% of global revenue in 2025 as they can amortize automation over greater milk volumes AgProud. Yet medium operations, defined as 200-999 cows, are expanding fastest at 12.83% CAGR, pushing vendors to design modular products scaled to mid-tier budgets. The dairy herd management market size allocated to medium farms is projected to more than double by 2031, reflecting their strategic role in regional milk supply resilience Mordor Intelligence. Mid-scale producers typically adopt technology piecemeal—starting with feeding or health modules—before graduating to robotic parlours once ROI is proven.

This incremental pathway demands interoperable architectures: sensor tags that read into multiple software ecosystems; feeding controls that integrate flawlessly with mastitis detection alerts. Vendors that force lock-in risk pushback from this influential cohort, whereas those offering open APIs and staged payment plans are gaining share. The segment’s trajectory signals that future revenue diversity in the dairy herd management market will correlate with vendor flexibility as much as with technical prowess.

By Deployment Mode: Cloud Adoption Accelerates

On-premise installations still command 59.78% of total sales because inconsistent rural broadband and data-sovereignty fears dominate purchasing logic. Rapid fiber rollouts combined with telecom 5G coverage are, however, spurring an 11.01% CAGR for SaaS-based offerings through 2031. Hybrid models—local data buffering with cloud analytics—bridge the reliability gap and satisfy cybersecurity audits led by larger enterprises.

Cloud deployment amplifies value through remote expert advisory services, cross-farm benchmarking, and machine-learning models trained on aggregated multi-regional datasets. Yet fear of ransomware attacks and data misappropriation remains material: solution providers are investing in end-to-end encryption, on-farm edge devices that isolate critical controls, and blockchain-anchored audit trails. Those efforts aim to reassure producers that the benefits of anywhere-anytime decision support outweigh residual data risks in the dairy herd management market.

Geography Analysis

North America generated the greatest absolute revenue in 2025 as large-scale barns, deep capital pools, and government sustainability grants converged to encourage full-stack adoption of monitoring and automation suites. Recent USD 8 billion in processing investments create downstream demand for consistent milk quality, reinforcing sensor-based oversight from farm to plant. Canada’s satellite-enabled methane tracking pilots underscore how policy incentives and technology maturity intersect to keep regional growth resilient .

Europe follows closely, distinguished by stringent welfare statutes and carbon-intensity targets that embed data capture into compliance workflows. The planned Arla-DMK cooperative merger will unify technology standards across 12,000 farms, potentially accelerating scale economics for new digital tools. Denmark’s phased livestock emissions tax elevates methane analytics to strategic priority status, driving additional platform purchases over the long term.

Asia-Pacific records the highest CAGR as China’s mega-operations integrate UCOWS NB-IoT tags across 1.26 million animals, Indonesia channels subsidies into heat-resilient barn retrofits, and India meshes AI advisory apps with its vast cooperative network Huawei. New builds rather than retrofits dominate spending, letting operators embed cloud connectivity, robotic parlours, and feed-intake cameras from day one. The region’s expanding middle class, plus self-sufficiency policies, ensures sustained momentum in the dairy herd management market.

Competitive Landscape

Fragmentation persists: global leaders DeLaval, GEA, and Lely compete with niche innovators that target methane capture, lameness analytics, or predictive breeding. Hardware incumbents are layering AI software atop proven mechanics; DeLaval’s collaboration with John Deere integrates agronomic and animal data into the Milk Sustainability Center, delivering cross-discipline dashboards that traditional stand-alone solutions cannot match DeLaval. GEA’s Space-Time computer-vision module for hoof health illustrates how incremental add-ons defend installed bases by embedding new value in established parlours.

Start-ups exploit regulatory white space: Windfall Bio deploys methane-eating microbes that transform emissions into high-value fertilizer, carving out an environmental-compliance niche. Athian monetizes verified Scope 3 reductions by channeling USD 9 million in payouts to participating U.S. farms, creating external revenue streams that justify deeper sensor penetration. Traditional suppliers respond with in-house carbon modules or acquisition pipelines aimed at back-filling sustainability gaps in their portfolios.

Consolidation is accelerating: BouMatic’s purchase of SAC Group expanded global distribution reach, while Lactalis’ USD 2.1 billion acquisition of General Mills’ U.S. yogurt brand extends downstream leverage. Economies of scale in R&D and data infrastructure encourage roll-ups, yet the demand for region-specific services limits how concentrated the dairy herd management market can become. Vendors able to couple ruggedized equipment, AI insight, and sustainability monetization mechanisms stand best positioned to lead the next competitive cycle.

Dairy Herd Management Industry Leaders

Delaval

Merck and Company

Afimilk

Boumatic

Inc. GEA Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lactalis acquired General Mills’ U.S. yogurt business for USD 2.1 billion after regulatory approval, expanding its North American footprint.

- May 2025: Arla Foods and DMK Group announced a merger to form Europe’s largest farmer-owned cooperative, representing 12,000 members and USD 20.8 billion in projected revenue.

- March 2025: Godrej Agrovet moved to acquire full control of Creamline to deepen its Indian dairy presence and bolster technology offerings

- February 2025: Athian disclosed USD 9 million in payments to producers from certified Scope 3 emission cuts on U.S. farms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dairy herd management market as all on-farm hardware, software, and service tools that dairy farmers apply to record, automate, and optimize milk yield, reproduction, feeding, and herd health.

We exclude generic livestock equipment built for beef animals or mixed-species monitoring.

Segmentation Overview

- By Product Type (Value)

- Hardware

- Software

- Services

- By Application (Value)

- Milk Harvesting & Parlour Automation

- Reproduction & Fertility Management

- Feeding & Nutrition Management

- Health & Disease Monitoring

- Calf & Young-stock Management

- By Farm Size (Value)

- Small Farms (less than 200 animals)

- Medium Farms (200-999 animals)

- Large Farms (more than 1,000 animals)

- By Deployment Mode (Value)

- On-premise

- Cloud-based / SaaS

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured calls with veterinarians, nutritionists, equipment dealers, and large-farm managers across North America, Europe, and Asia that tested secondary assumptions, benchmarked average selling prices, and sized latent demand pools.

Desk Research

Our desk work started with FAO milk-output tables, USDA and Eurostat herd inventories, and International Dairy Federation cost curves, which together created national baselines for herd numbers, yields, and cost structure.

We then drew on company 10-Ks, cooperative annual reports, and patent trends captured through D&B Hoovers, Dow Jones Factiva, and Questel to refine vendor revenues and technology roll-outs, while peer-reviewed journals and open trade magazines filled remaining data gaps. This list is illustrative, and many other open sources were also reviewed.

Market-Sizing & Forecasting

After official milk output and average yield build regional spending pools, the pools are adjusted for farm size mix and technology penetration, and only then does the model arrive at the expenditure. Supplier shipment tallies and sampled SaaS fees provide a bottom-up cross-check that trims outliers. A multivariate regression weighing herd expansion, labor-cost inflation, methane-emission mandates, and robotic milking uptake drives the forecast, while scenario ranges handle thin data points.

Data Validation & Update Cycle

Our Mordor analysts run variance checks against trade data, import filings, and price trackers, and any anomaly triggers rapid expert re-contact before final sign-off. Models refresh each year, with interim updates after major policy or disease shocks, and only after these steps is the file released to clients.

Why Mordor's Dairy Herd Management Baseline Commands Reliability

We observe that published values often diverge because firms stretch scope, pick different base years, or assume identical pricing in all regions.

Many external numbers blend beef automation or ignore smallholder investment, while Mordor restricts scope to dairy-only tools, applies country-level price ladders, and refreshes figures every twelve months, which yields a balanced midpoint that decision makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.49 bn (2025) | Mordor Intelligence | |

| USD 4.16 bn (2024) | Global Consultancy A | Dairy and beef devices combined, flat ASP |

| USD 4.19 bn (2024) | Industry Research B | Older base year, single region growth factor |

The comparison shows that clear scope rules, current data, and multi-source checks make Mordor's baseline the most dependable reference for strategic planning.

Key Questions Answered in the Report

What is the current size of the dairy herd management market and how fast is it growing?

The market is valued at USD 4.98 billion in 2026 and is expected to reach USD 8.32 billion by 2031, expanding at a 10.83% CAGR.

Which region offers the highest growth potential for dairy herd management solutions?

Asia-Pacific shows the fastest expansion as nations such as China invest in large-scale, tech-enabled dairies to boost self-sufficiency.

What farm segment is adopting technology the quickest?

Medium-sized operations with 200-999 cows are growing adoption at a 12.83% CAGR because modular systems let them compete with mega-dairies at lower capital risk.

Which region has the biggest share in Dairy Herd Management Market?

In 2025, the North America accounts for the largest market share in Dairy Herd Management Market.

Why are software platforms gaining momentum over hardware in this market?

Although hardware still holds 49.62% revenue share, software subscriptions are rising at an 11.05% CAGR because analytics extract more value from existing sensors and machinery.

What are the biggest obstacles to wider technology adoption in dairy herd management?

High upfront capital needs—often USD 2–4 million per mid-size farm—and ongoing data-ownership and cybersecurity worries remain primary barriers.

Page last updated on: