Cattle Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.42 Billion |

| Market Size (2030) | USD 12.43 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

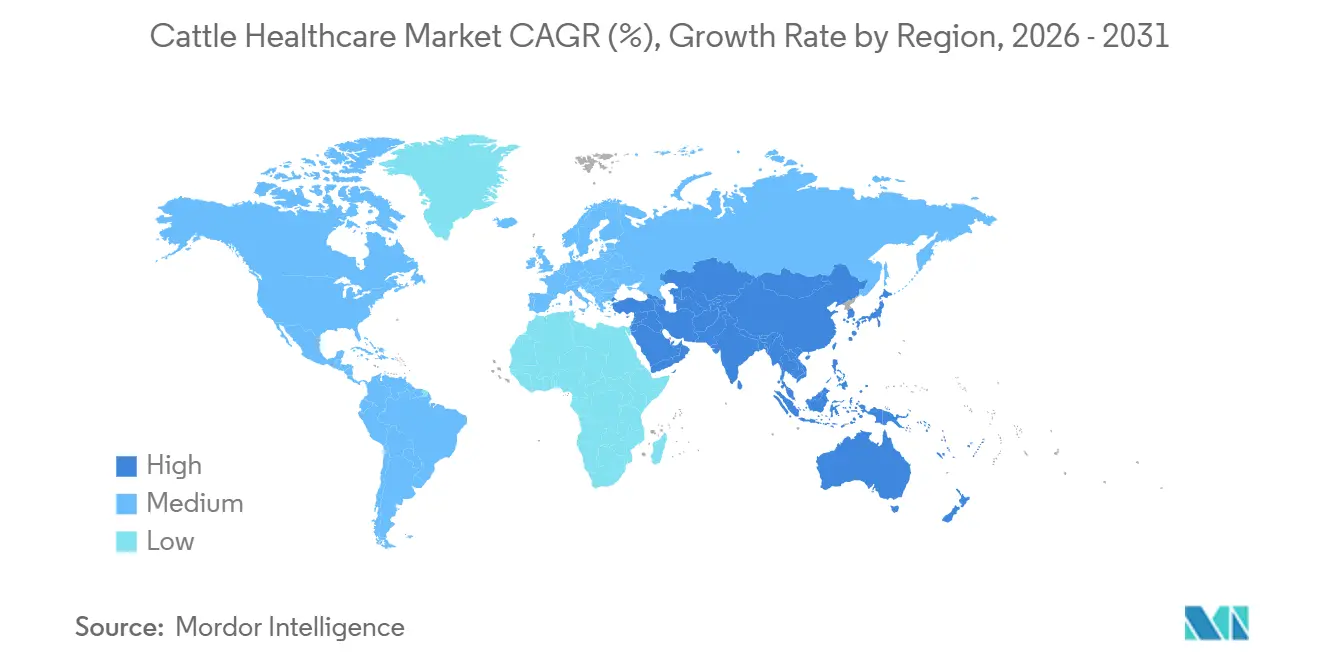

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cattle Healthcare Market Analysis by Mordor Intelligence

The Cattle Healthcare Market size is projected to expand from USD 8.91 billion in 2025 and USD 9.42 billion in 2026 to USD 12.43 billion by 2030, registering a CAGR of 5.71% between 2026 to 2030.

Rising global demand for safe beef and dairy is pushing producers to shift from episodic treatment toward data-enabled herd-management systems that integrate diagnostics, biologics and real-time monitoring. Wearables that flag abnormal activity, modular mRNA vaccines that shorten strain-update cycles and carbon-credit programs that reward low-methane herds are giving suppliers new revenue streams even as regulators tighten oversight of antibiotics. North America anchors the cattle healthcare market because large U.S. dairies and feedlots deploy precision tools to meet retailer sustainability metrics, while Asia-Pacific sets the growth pace as China and India modernize smallholder herds through cooperative models [1]Animal and Plant Health Inspection Service, “2025 Matching Grants,” U.S. Department of Agriculture, aphis.usda.gov. Competitive intensity remains moderate; four multinational biologics groups command the majority of global revenue, yet regional generics flourish in parasiticides and off-patent vaccines.

Key Report Takeaways

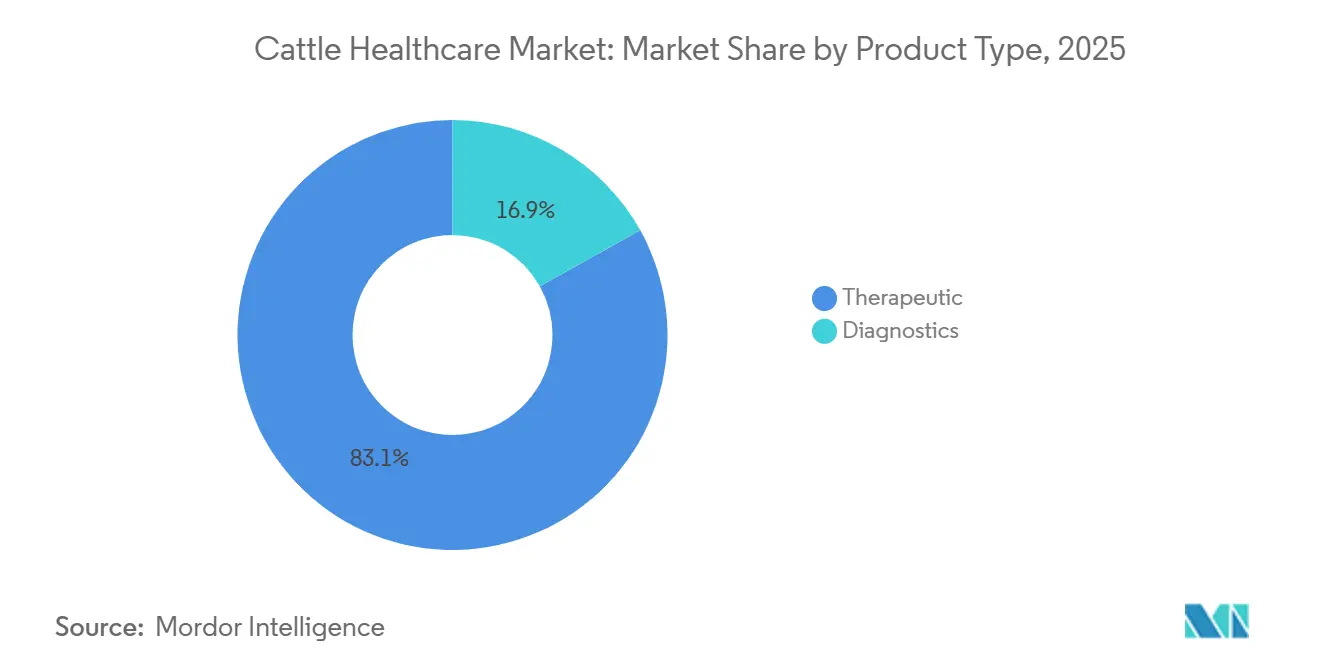

- By product type, therapeutics led with 83.1% cattle healthcare market share in 2025, whereas diagnostics are forecast to deliver a 7.22% CAGR to 2031.

- By disease, bovine respiratory disease accounted for 28.65% of 2025 spending, while lumpy skin and other vector-borne conditions are set to grow at 6.54% through 2031.

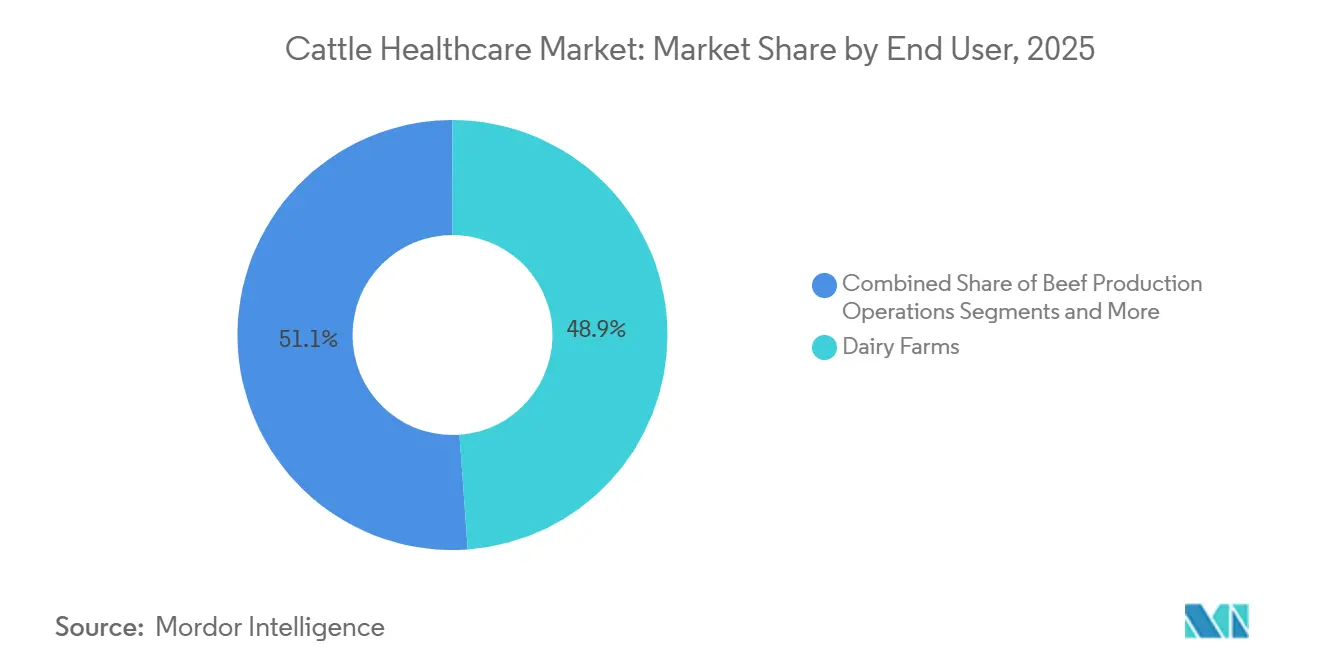

- By end user, dairy farms represented 48.87% of 2025 expenditure, yet beef feedlots are projected to register a 7.11% CAGR to 2031.

- By geography, North America captured 41.2% revenue share in 2025; Asia-Pacific is expected to be fastest-expanding region with an 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cattle Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global consumption of animal protein | +1.2% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Expansion of preventive-care subsidies | +0.8% | North America, Europe, Brazil, India | Short term (≤ 2 years) |

| Adoption of AI-based wearables | +0.9% | North America, EU, urban China and India | Medium term (2-4 years) |

| mRNA & nanoparticle vaccine breakthroughs | +0.7% | United States, EU, Australia, global export markets | Long term (≥ 4 years) |

| Carbon-credit premiums for low-methane herds | +0.5% | North America, Europe, New Zealand, Brazil | Long term (≥ 4 years) |

| Blockchain-verified provenance schemes | +0.4% | Europe, North America, premium South American export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Global Consumption of Animal Protein

Beef intake in Asia-Pacific rose 3.2% in 2025, far above the world average, reinforcing the need to lift per-animal productivity through preventive health protocols [2]OECD-FAO, “Agricultural Outlook 2025,” oecd.org. Middle Eastern buyers now demand veterinary certificates that exceed OIE baselines, obliging exporters to invest in rapid diagnostics and traceability. India added 2.1 million milking cows in 2025, yet subclinical mastitis still erodes yields by up to 20%, creating clear headroom for point-of-care immunodiagnostics. Urban Chinese consumers are paying 12% more for milk labeled low in antibiotic residues, nudging cooperatives toward prophylactic biologics. Altogether, demand growth is less about herd expansion and more about squeezing higher, residue-free output from existing cattle through precision health investments.

Expansion of Preventive-Care Subsidies

USDA matching grants worth USD 180 million in 2025 covered automated vaccination, surveillance networks, and on-farm biosecurity upgrades, lowering producer payback periods to under two years. Common Agricultural Policy payments now reimburse up to 60% of the cost of integrated herd-health plans that meet animal-welfare and methane targets, effectively bundling climate goals with disease prevention. Brazil piloted a 40% vaccine subsidy for foot-and-mouth disease in transitioning states, spiking short-term biologics demand before the program sunsets. Once producers experience lower morbidity and cull losses under subsidized regimes, they rarely revert, creating a ratchet effect that locks in structural demand for vaccines and diagnostics.

Adoption of AI-Based Wearables

Collar sensors flagged respiratory distress 2.3 days earlier than visual checks in a 1,200-head Wisconsin feedlot trial, cutting treatment costs by 28% and deaths by 35%. Dutch dairies deployed ear-tag biosensors covering 22% of national herds by end-2025, linking automated alerts to milk-robot data for instant mastitis detection. Boehringer Ingelheim now integrates sensor streams with vaccine schedules so producers can time shots to individual stress profiles, boosting efficacy and reducing wastage. The upside is a shift of decision-making from barn to algorithm, elevating demand for rapid-acting biologics deployable within hours of an alert. Connectivity gaps and data-literacy barriers still exclude smaller farms, widening the productivity divide

mRNA & Nanoparticle Vaccine Breakthroughs

Zoetis filed the first bovine mRNA respiratory vaccine in late 2025, showing 92% efficacy versus roughly 72% for conventional live strains. The modular platform updates strains in under 10 weeks, a critical advantage as antigens drift. Merck Animal Health’s nanoparticle vaccine for lumpy skin disease achieved 14-month immunity in African trials, halving annual booster costs. FDA issued draft guidance for veterinary mRNA biologics in early 2026, but the EMA is still setting equivalency rules, delaying EU launches [3]Center for Veterinary Medicine, “Draft Guidance on Veterinary mRNA Products,” fda.gov. Early movers will enjoy premium pricing and extended patent tails, while generics face steep technology adoption curves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain & formulation costs for next-gen biologics | -0.6% | Emerging Asia-Pacific, Africa, rural South America | Medium term (2-4 years) |

| Acute shortage of large-animal veterinarians | -0.5% | Rural North America, Australia, selected EU areas | Short term (≤ 2 years) |

| Producer push-back on data ownership | -0.3% | North America, Europe, parts of Latin America | Medium term (2-4 years) |

| Tariff volatility on antigen inputs | -0.3% | South America, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cold-Chain & Formulation Costs for Next-Gen Biologics

mRNA products demand -20 °C to -70 °C storage, yet majority of distributors in India and in sub-Saharan Africa lacked ultra-cold equipment in 2025. Spoilage reached 18% in Southeast Asia, forcing manufacturers to overship by up to 25% and lifting landed costs. Ceva reported that lyophilized mRNA prototypes last six months at room temperature but raise per-dose cost by 35%, a trade-off that limits adoption in price-sensitive areas. The result is a two-tier cattle healthcare market where advanced biologics stay locked in temperate, well-capitalized regions while emerging markets rely on older, less effective options.

Acute Shortage of Large-Animal Veterinarians

Only 3.2% of U.S. veterinary graduates entered food-animal practice in 2025, down from 5.1% five years earlier, as debt averaging USD 183,000 steered talent toward companion-animal clinics. Rural Great Plains counties saw large-animal capacity fall 22% between 2020 and 2025, delaying diagnostics and encouraging producers to self-medicate cattle with over-the-counter drugs. Australia’s AUD 15 million rural-placement subsidy under-recruited, highlighting lifestyle hurdles. These gaps multiply the value of producer-operated diagnostics and tele-veterinary services, but also raise biosecurity risks when complex cases go unmanaged.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostics Gain Momentum on Preventive Focus

Therapeutics maintained an 83.1% share of the cattle healthcare market in 2025, reflecting enduring reliance on vaccines, parasiticides, and anti-infectives that underpin basic biosecurity. Diagnostics, however, are forecast to grow 7.22% annually to 2031 as point-of-care PCR devices and on-farm biosensors compress result times to under 30 minutes. Molecular platforms captured a significant share of diagnostic revenue in 2025, buoyed by Neogen’s USDA-approved handheld BVD detector priced at USD 4,200. Immunodiagnostics still dominate unit volumes, yet growth slows in saturated developed markets. Within therapeutics, vaccine demand outperforms anti-infectives as retailers and regulators clamp down on antibiotic use.

The tilt toward diagnostics underscores a strategic shift: preventing outbreaks delivers higher returns than treating sick animals, particularly as antimicrobial resistance attracts policy scrutiny. Mobile ultrasound and rapid chemistries remain niche but gain traction in breeding herds where early pregnancy confirmation tightens calving intervals. As uptake widens, diagnostics are set to boost the cattle healthcare market size for ancillary data-analytics services that benchmark herd performance.

By Disease: Respiratory Disorders Dominate While Vector Threats Escalate

Bovine respiratory disease (BRD) absorbed 28.65% of disease-related outlays in 2025, driven by feedlot commingling stress and multi-agent pathogen loads. Lumpy skin and other vector-borne conditions are growing 6.54% to 2031 as climate change expands mosquito habitats into temperate zones, triggering emergency vaccination across Southeast Europe. Mastitis held a significant share of dairy herds, while foot-and-mouth disease spending stays regionally concentrated in South America and parts of Asia.

Strong BRD prevalence anchors therapeutic spending, yet rising vector-borne incidence draws R&D toward thermostable vaccines deployable in warm climates. Parallel investment in fast diagnostic panels for BRD, mastitis, and BVD aims to shorten isolation windows and protect the broader cattle healthcare market size. Precision analytics now quantify pathogen load and environmental stress simultaneously, allowing producers to pre-empt disease spikes rather than chase symptoms.

By End User: Feedlots Accelerate Technology Adoption

Dairy farms commanded 48.87% of 2025 spend, justified by high-yield cows where slight health dips slash milk output and margin. Each clinical mastitis case costs USD 444 in treatment, dumped milk, and lost yield, validating robust prophylaxis budgets. Beef feedlots are on a 7.11% CAGR track as consolidation drives pen sizes above 10,000 head, a scale at which algorithmic sensors, auto-dosing, and real-time diagnostics pay off.

Breeding operations funnel resources into reproductive vaccines and persistent-infection testing, whereas veterinary hospitals are losing relative share as over-the-counter rules loosen. Ranches in extensive systems still lag due to low stocking density and distance from labs, yet mobile diagnostic vans and telehealth may shrink that gap. Government institutes and research farms, while small in spending, remain pivotal by underwriting surveillance trials that de-risk private-sector innovation, reinforcing resilience across the cattle healthcare market.

Geography Analysis

North America held 41.2% of 2025 revenue as U.S. mega-dairies and feedlots invested in robotics, AI-based monitoring and proprietary biologics to hit retailer sustainability metrics. Canada’s supply-managed dairy sector reinvested an average CAD 142 (USD 105) per cow in preventive care, 18% above the continental mean. Mexican feedlot expansion, buoyed by foreign capital, boosts respiratory vaccine sales, although counterfeit therapeutics and regulatory gaps temper growth.

Asia-Pacific rides a 6.98% CAGR as India’s 303 million-head herd digitizes under National Livestock Mission subsidies, and China targets half of milk output from 1,000-plus-cow dairies by 2030. Japan and South Korea post world-leading per-head spend due to strict residue standards, while Australia’s export-oriented graziers demand tick and vector vaccines for disease-free status. Southeast Asian cold-chain limitations restrain uptake of next-gen biologics, keeping older killed vaccines in rotation.

Europe accounts for a significant share of the cattle healthcare market, with antibiotic-reduction policies driving vaccine substitution and alternative therapies. German and French herds invest heavily in diagnostics that document low-residue status for premium retailers. South America leverages Brazil’s 224 million-head herd yet sees cyclical demand swings tied to antigen tariffs and credit access. The Middle East and Africa remain smallest by value; however, GCC climate-controlled dairies and sub-Saharan disease-eradication campaigns are niche engines of higher-margin biologics demand.

Competitive Landscape

The cattle healthcare market remains moderately concentrated. Zoetis, Boehringer Ingelheim, Merck Animal Health, and Elanco together controlled the majority of global sales in 2025, leaving ample share for regional generics, diagnostics specialists, and start-ups. Zoetis generated USD 2.1 billion from cattle products, with diagnostics and digital subscriptions at 14% of that tally, up from 9% two years earlier. Boehringer Ingelheim’s 2025 purchase of a precision-livestock analytics firm signals a pivot toward bundled data-plus-biologics offerings.

White-space prospects focus on point-of-care diagnostics for emerging markets, thermostable vaccine formulations that bypass cold chains, and digital platforms that monetize herd data through benchmarking. Smaller innovators pursue bacteriophage mastitis therapies and autogenous vaccines, products that sidestep antibiotic resistance and regulatory delays. Patent filings for cattle healthcare technologies rose significantly between 2024 and 2025, especially in adjuvants that lengthen immunity and cut booster frequency. Regulatory shifts such as the U.S. Veterinary Feed Directive favor companies offering integrated veterinary consulting, raising the entry bar for pure generic drug makers.

Cattle Healthcare Industry Leaders

Boehringer Ingelheim

Elanco Animal Health

Zoetis Inc.

Qiagen

Merck Animal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Merck Animal Health won conditional FDA approval for EXZOLT CATTLE-CA1 fluralaner topical to treat New World screwworm and cattle fever ticks.

- March 2025: The EMA approved this vaccine for Epizootic Hemorrhagic Disease Virus (EHDV) in cattle, addressing the spread of vector-borne diseases in Europe.

- February 2025: Elanco entered a joint venture to launch methane-reducing feed supplements targeting herds in carbon-credit schemes.

Global Cattle Healthcare Market Report Scope

As per the scope of the report, cattle healthcare includes the products that are used for the treatment and diagnosis of cattle against various medical conditions and diseases.

The cattle healthcare market is segmented by products, disease, end users, and geography. By product, the market is segmented into therapeutics (vaccines, parasiticides, anti-infectives, anti-inflammatories, medical feed additives, and other therapeutics) and diagnostics (immunodiagnostics, molecular diagnostics, diagnostic imaging, point-of-care devices & biosensors, clinical chemistry, and other diagnostics). By disease, the market is segmented into bovine respiratory disease, mastitis, bovine viral diarrhea, foot & mouth disease, parasitic infestations, metabolic & reproductive disorders, lumpy skin & other vector-borne diseases. By end users, the market is segmented into Dairy Farms, Beef Feedlots, breeding operations, veterinary hospitals & clinics, government & research institutes, and ranches.

Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-infectives | |

| Anti-inflammatories | |

| Medical Feed Additives | |

| Other Therapeutics | |

| Diagnostics | Immunodiagnostics |

| Molecular Diagnostics | |

| Diagnostic Imaging | |

| Point-of-Care Devices & Biosensors | |

| Clinical Chemistry | |

| Other Diagnostics |

| Bovine Respiratory Disease (BRD) |

| Mastitis |

| Bovine Viral Diarrhoea (BVD) |

| Foot & Mouth Disease (FMD) |

| Parasitic Infestations |

| Metabolic & Reproductive Disorders |

| Lumpy Skin & Other Vector-borne |

| Dairy Farms |

| Beef Feedlots |

| Breeding Operations |

| Veterinary Hospitals & Clinics |

| Government & Research Institutes |

| Ranches |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-infectives | ||

| Anti-inflammatories | ||

| Medical Feed Additives | ||

| Other Therapeutics | ||

| Diagnostics | Immunodiagnostics | |

| Molecular Diagnostics | ||

| Diagnostic Imaging | ||

| Point-of-Care Devices & Biosensors | ||

| Clinical Chemistry | ||

| Other Diagnostics | ||

| By Disease | Bovine Respiratory Disease (BRD) | |

| Mastitis | ||

| Bovine Viral Diarrhoea (BVD) | ||

| Foot & Mouth Disease (FMD) | ||

| Parasitic Infestations | ||

| Metabolic & Reproductive Disorders | ||

| Lumpy Skin & Other Vector-borne | ||

| By End User | Dairy Farms | |

| Beef Feedlots | ||

| Breeding Operations | ||

| Veterinary Hospitals & Clinics | ||

| Government & Research Institutes | ||

| Ranches | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the cattle healthcare market?

The cattle healthcare market size reached USD 9.42 billion in 2026.

How fast will the market grow through 2031?

It is projected to register a 5.71% CAGR from 2026 to 2031.

Which product type is expanding quickest?

Diagnostics are forecast to advance at 7.22% per year through 2031 as producers prioritize early detection.

Why is bovine respiratory disease so costly?

BRD accounted for 28.65% of 2025 disease spending because feedlot stress and multi-agent infections drive high morbidity and treatment costs.

Which region leads in spending today?

North America held 41.2% of the 2025 market revenue due to large, technology-enabled U.S. dairies and feedlots.

Page last updated on: