Cytokine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

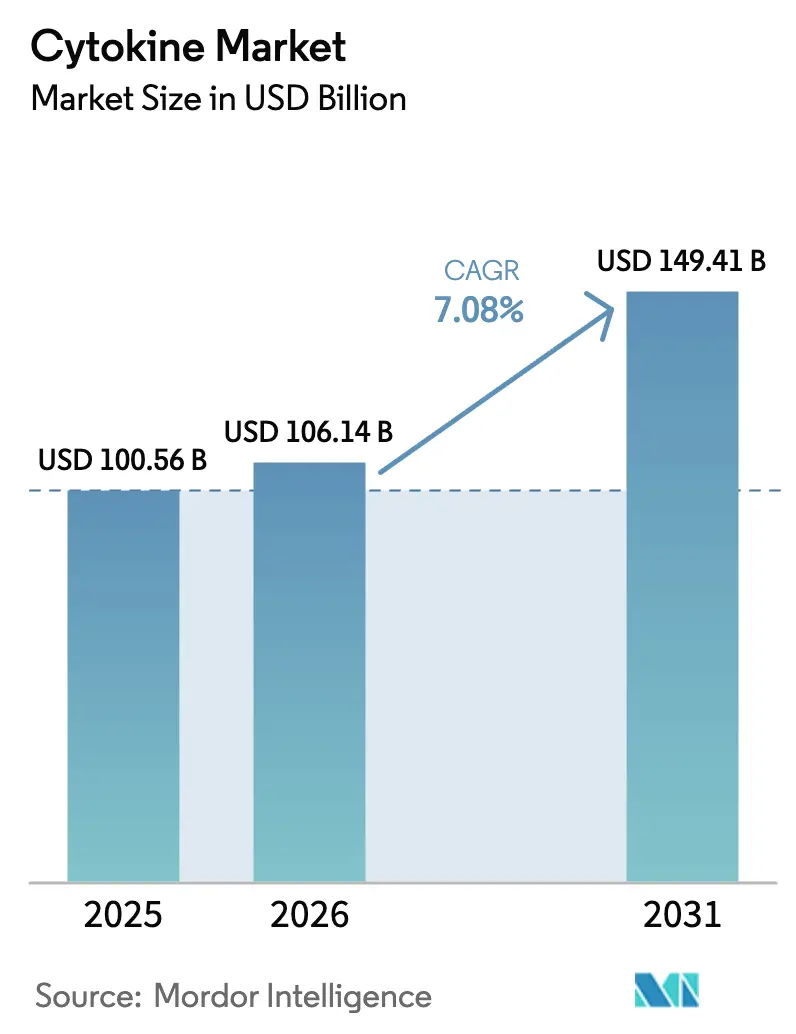

| Market Size (2026) | USD 106.14 Billion |

| Market Size (2031) | USD 149.41 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

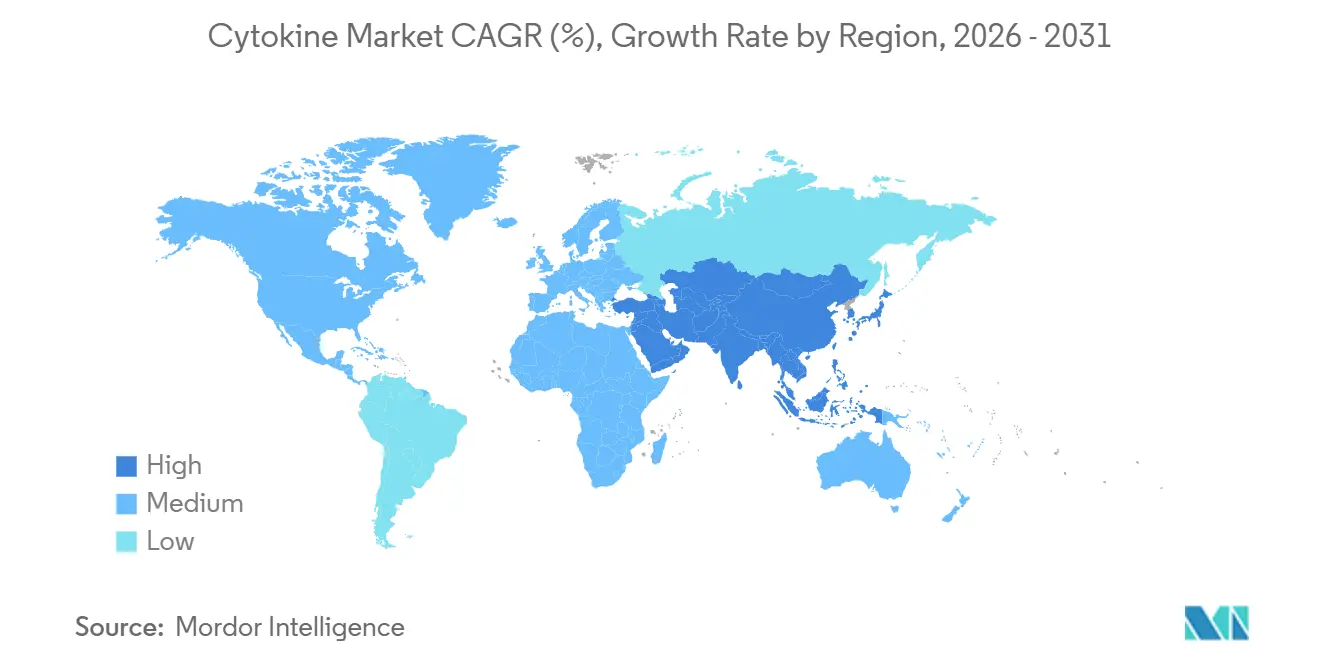

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

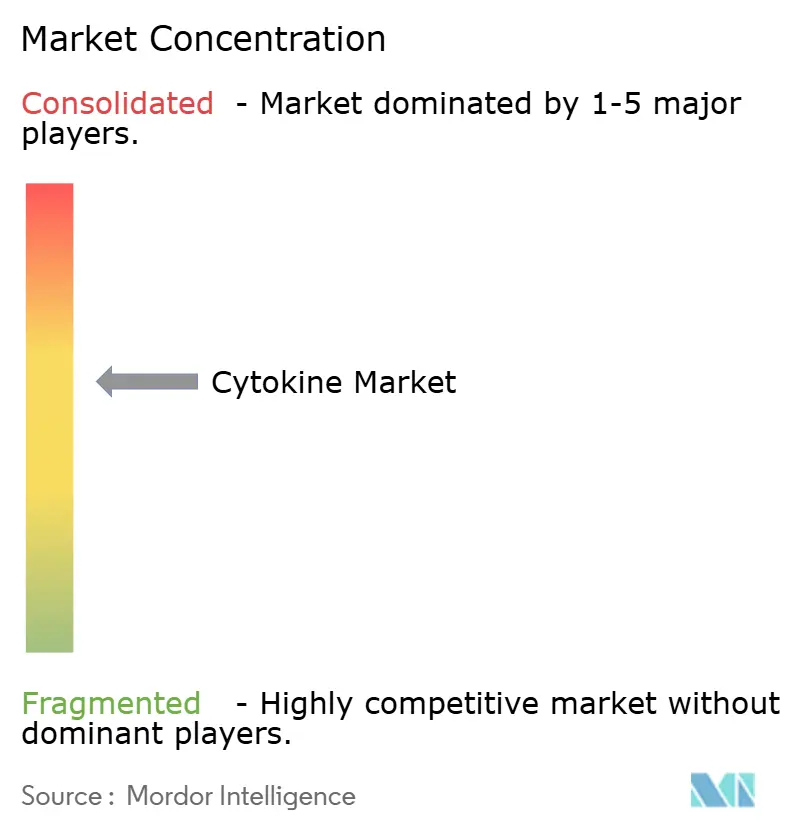

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cytokine Market Analysis by Mordor Intelligence

The Cytokine Market size is projected to be USD 100.56 billion in 2025, USD 106.14 billion in 2026, and reach USD 149.41 billion by 2031, growing at a CAGR of 7.08% from 2026 to 2031.

Three forces underpin this momentum: rising chronic–disease incidence, rapid uptake of cytokine-based cancer immunotherapies, and growing demand for GMP-grade cytokines in cell and gene therapy manufacturing. Biologics that neutralize tumor necrosis factor (TNF) still dominate revenue, yet next-generation interleukins are capturing clinical attention as they tackle refractory autoimmune and rare inflammatory disorders.[1]Food and Drug Administration, “Drugs@FDA: FDA-Approved Drugs,” Food and Drug Administration, fda.gov Biosimilar erosion of legacy TNF inhibitors, vertical integration by large biopharma to secure cytokine supply, and a pivot toward digitally enabled home-delivery channels are reshaping competitive dynamics. At the same time, novel mRNA-encoded cytokine constructs promise faster manufacturing and localized immune activation, though durability and regulatory classification remain open questions.

Key Report Takeaways

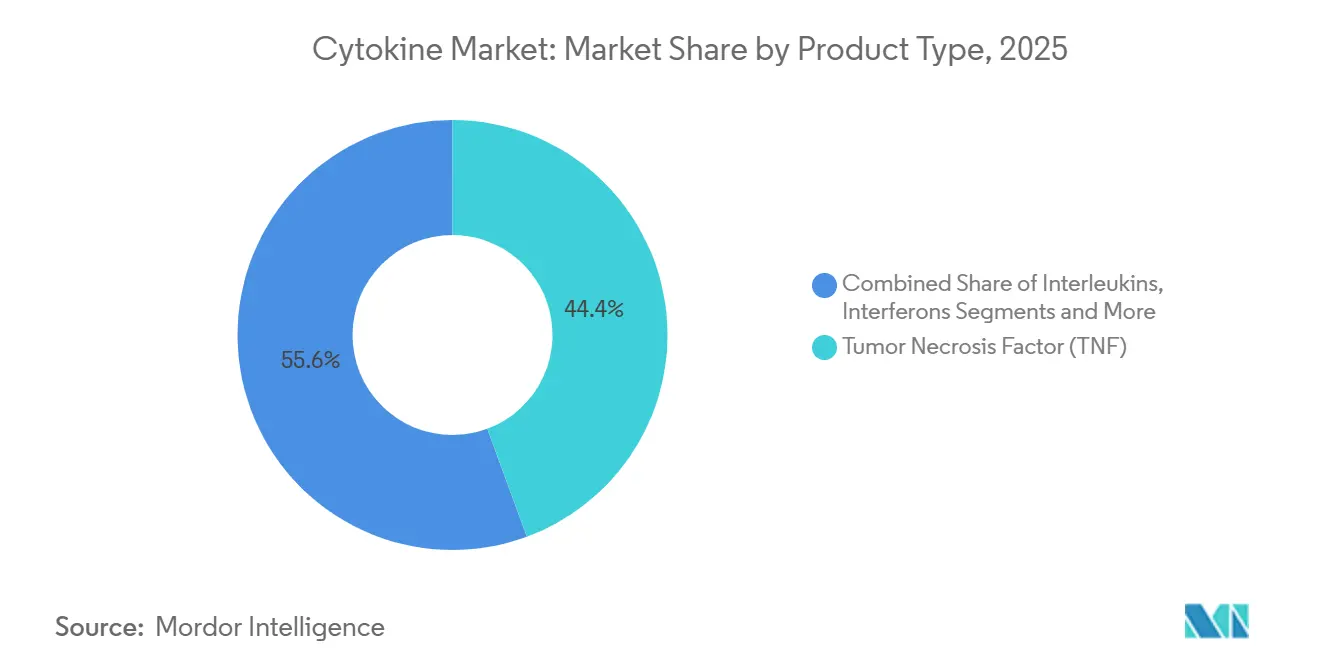

- By product type, TNF agents held 44.36% of the cytokine market share in 2025, while interleukins are projected to expand at a 9.84% CAGR through 2031.

- By therapeutic application, cancer and malignancies commanded 49.78% of 2025 revenue; autoimmune disorders post the fastest outlook at a 9.54% CAGR to 2031.

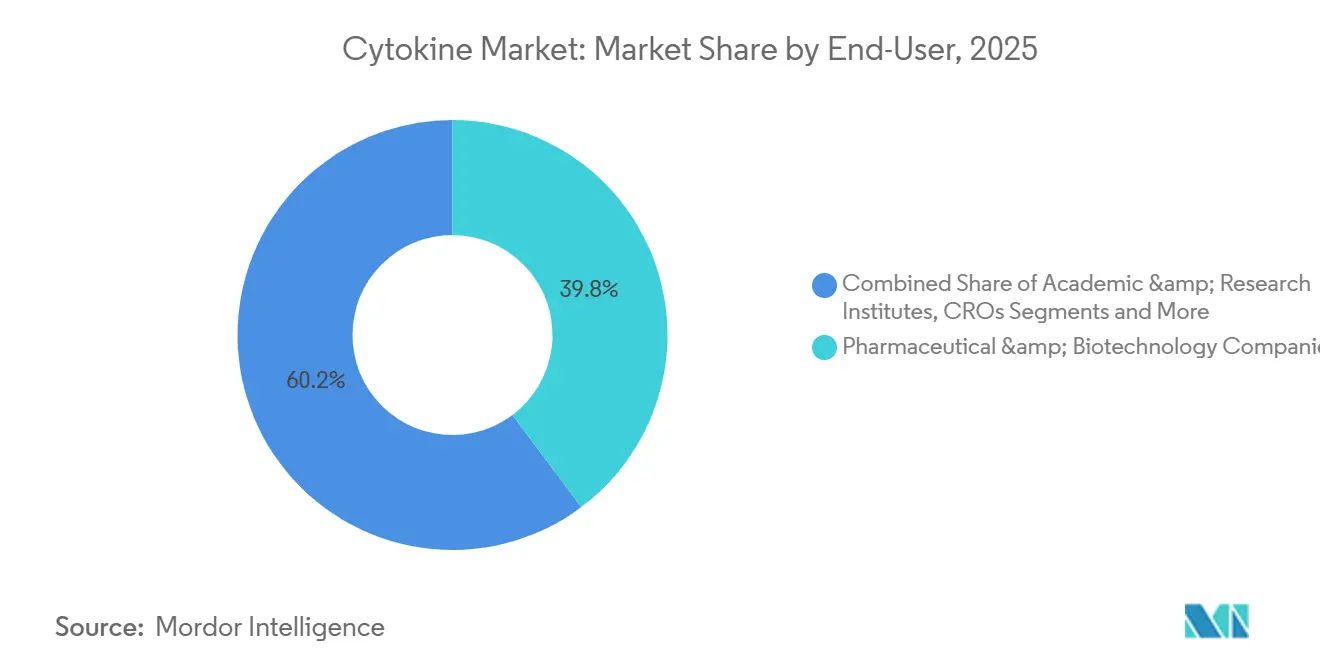

- By end user, pharmaceutical and biotechnology companies generated 39.77% of 2025 demand, whereas contract research organizations will rise at a 10.56% CAGR during the forecast.

- By function, pro-inflammatory cytokines contributed 46.24% of 2025 value, but growth and differentiation factors are set to climb at a 10.13% CAGR.

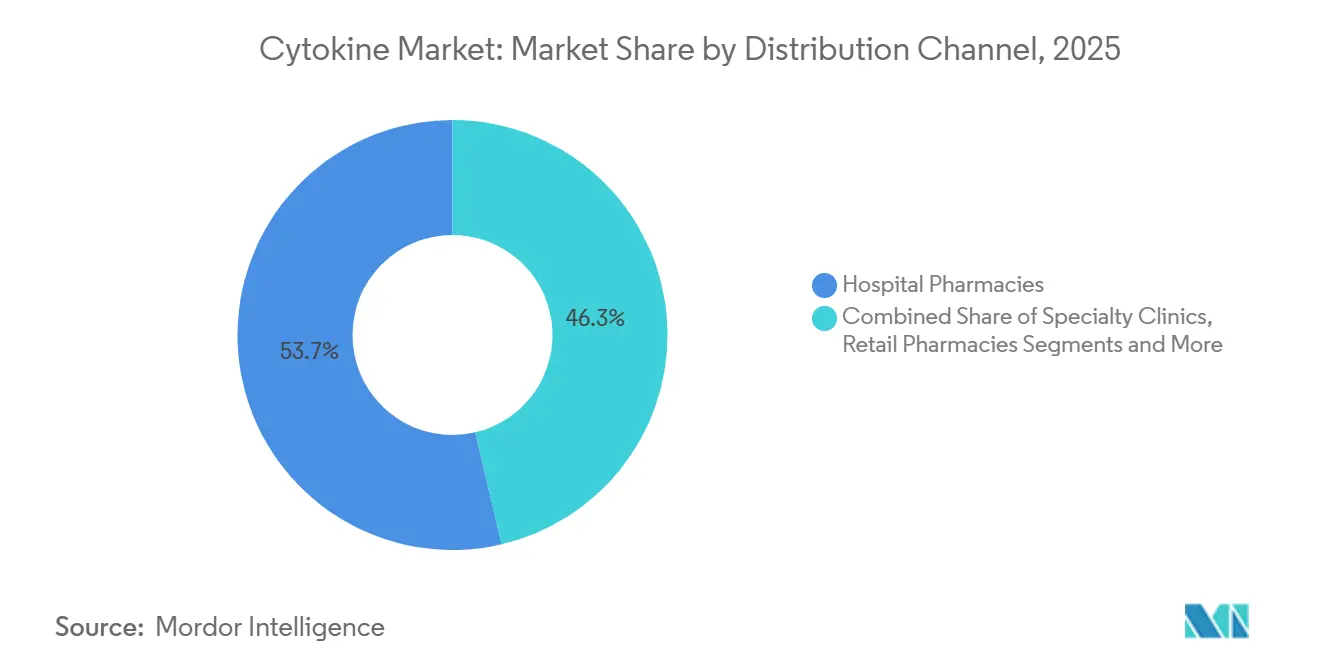

- By distribution channel, hospital pharmacies dispensed 53.66% of cytokines in 2025; online pharmacies are on track for an 11.34% CAGR to 2031.

- North America contributed 41.53% of 2025 sales, while Asia-Pacific is predicted to post a 10.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cytokine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic and autoimmune diseases | +1.2% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Expanding oncology pipeline using cytokine-based immunotherapies | +1.5% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Advances in recombinant engineering and bioprocessing technologies | +0.9% | Global, led by North America and Europe | Medium term (2–4 years) |

| mRNA-encoded, locally delivered cytokine adjuvants gaining traction | +0.7% | North America and Europe, early Asia-Pacific adoption | Long term (≥ 4 years) |

| GMP-grade cytokine demand for cell and gene therapy manufacturing | +1.3% | North America and Europe, expanding Asia-Pacific | Medium term (2–4 years) |

| Recent FDA/EMA approvals for first-in-class cytokine therapeutics | +0.8% | North America and Europe with Asia-Pacific spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Autoimmune Diseases

Escalating autoimmune prevalence is fueling steady cytokine prescribing, especially agents that block interleukin-17, interleukin-23, and TNF pathways. Dupilumab added three new U.S. indications in 2024, lifting revenue expectations above USD 13 billion and highlighting the strategy of extending established antibodies into adjacent diseases.[2] Investor Relations, “Dupilumab Label Expansions,” Regeneron Pharmaceuticals, investor.regeneron.com Rheumatoid arthritis, psoriasis, and inflammatory bowel disease affect over 30 million diagnosed U.S. patients, yet injection-site reactions and immunogenicity still curb adherence. Long-acting formulations and subcutaneous devices aim to ease this gap, encouraging payers to authorize at-home use. The cytokine market therefore benefits from both a widening patient pool and therapeutic refinements that improve convenience, creating a virtuous cycle of uptake.

Expanding Oncology Pipeline Using Cytokine-Based Immunotherapies

Cytokines are moving from supportive care to frontline oncology, often paired with checkpoint inhibitors or CAR-T therapies. BNT152 encodes interleukin-2 mRNA inside lipid nanoparticles for intratumoral delivery, limiting systemic exposure while activating local immune cells. Moderna’s mRNA-2752 combines interleukin-2 with an OX40 ligand to broaden T-cell activation and entered Phase I trials in 2024. These approaches bypass recombinant protein manufacturing, shortening production cycles from months to weeks. Early data show transient expression of 48–72 hours, so optimal dosing remains uncertain. Nonetheless, positive safety profiles could position these assets to take share from protein-based cytokines in solid tumors by 2030.

Advances in Recombinant Engineering & Bioprocessing Technologies

Single-use bioreactors and continuous perfusion systems are trimming cycle times by 40% and boosting volumetric yields.[3] Investor Relations, “Thermo Fisher Scientific Q4 2025 Update,” Thermo Fisher Scientific, ir.thermofisher.com Embedded process-analytical technology lets operators fine-tune pH, oxygen, and nutrients in real time, improving lot consistency—a key regulator focus. Chromatography innovations from Sartorius and Pall have cut purification steps from seven to four, lowering cost-of-goods by roughly 25% while meeting ICH-Q6B quality norms. For GMP-grade cytokines used in cell therapy expansion, these gains accelerate batch release and free working capital. Sponsors that integrate continuous processing therefore gain both margin upside and supply-security advantages, reinforcing competitive position in the cytokine market.

mRNA-Encoded, Locally Delivered Cytokine Adjuvants Gaining Traction

mRNA constructs deliver transient cytokine pulses inside tumors, aiming to boost antitumor immunity without the systemic toxicity tied to high-dose proteins. CureVac’s CV8102—a Toll-like receptor 7/8 agonist—induced interferon-gamma within melanoma lesions in early testing and avoided the flu-like symptoms common with recombinant interferon-alpha. Gritstone’s GRANITE platform splices neoantigen mRNA with interleukin-12 and interleukin-15 adjuvants to expand tumor-specific T cells, an approach now in Phase I trials. Regulatory pathways are still evolving; sponsors often file dual biologic and gene-therapy designations to hedge. This ambiguity lengthens IND lead times by 6–12 months but, once clarified, could unlock rapid follow-on approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing cost and complex purification requirements | -0.8% | Global, most acute in emerging markets | Medium term (2–4 years) |

| Dose-limiting toxicities driving stringent regulatory scrutiny | -0.6% | North America and Europe, Asia-Pacific spillover | Short term (≤ 2 years) |

| Patent cliffs and biosimilar competition compressing margins | -1.0% | North America and Europe, expanding Asia-Pacific | Short term (≤ 2 years) |

| Supply-chain bottlenecks for single-use bioprocess consumables | -0.5% | Global, acute in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Cost and Complex Purification Requirements

Recombinant cytokines rely on costly mammalian expression systems that demand serum-free media priced at USD 500–1,200 per liter, while multi-step chromatography pushes cost-of-goods for interleukin-2 to USD 8,000–12,000 per gram. Contract manufacturers impose 50 kg minimum orders, requiring upfront commitments exceeding USD 600,000 before clinical proof-of-concept. Smaller sponsors often lack the capital to meet these thresholds, concentrating innovation among cash-rich firms. Emerging markets face added challenges from import tariffs on filtration resins and resupply delays, widening the cost gap and slowing local cytokine market growth. While continuous processing lowers expenses, adoption remains limited to large facilities with robust quality-systems infrastructure.

Dose-Limiting Toxicities Driving Stringent Regulatory Scrutiny

Cytokine release syndrome (CRS) and capillary leak are the principal safety hurdles in high-intensity cytokine therapy. Tocilizumab rescue is now mandatory for each CAR-T infusion, adding USD 3,000–5,000 per patient and limiting administration to roughly 150 certified U.S. centers. High-dose interleukin-2 still causes severe hypotension in up to 20% of recipients, pushing inpatient costs above USD 100,000 per course. Stringent Risk-Evaluation-and-Mitigation requirements delay community-site adoption and shrink addressable volumes. Innovators are testing lower doses and tumor-targeted fusion proteins, but regulators remain anchored to historical safety databases, making change incremental.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Interleukins Drive Next-Generation Growth

Interleukins are set to outpace all categories, expanding at a 9.84% CAGR as sponsors pivot from mature TNF franchises to address rare inflammatory disorders. Tumor necrosis factor agents retained 44.36% of 2025 revenue, but biosimilars now pressure prices, pulling AbbVie’s Humira down from USD 21.2 billion in 2022 to USD 14.4 billion in 2023. The cytokine market size for interleukins is therefore expected to widen its gap over interferons, whose sales have contracted below USD 500 million as oral antivirals dominate hepatitis care.

Colony-stimulating factors serve a stable supportive-oncology niche, with Zarxio and Nivestym securing 40% of U.S. volume by 2025. Growth factors beyond CSFs, erythropoietin, PDGF, and VEGF, will rise at a 10.13% CAGR (2026-2031), aided by a 35%-cheaper darbepoetin biosimilar approved in 2024. Chemokines remain largely pre-commercial, though CXCR4 antagonists show promise in stem-cell mobilization. Overall, innovators target interleukin-23 and interleukin-6 pathways for their dual autoimmune and oncology potential, injecting fresh momentum into the cytokine market.

By Therapeutic Application: Autoimmune Disorders Accelerate

Cancer still generated 49.78% of cytokine prescriptions in 2025, reflecting entrenched use of colony-stimulating factors and CAR-T manufacturing cytokines. Yet autoimmune disorders will log the fastest expansion at a 9.54% CAGR, thanks to label extensions for guselkumab, dupilumab, and other interleukin-targeted drugs. The cytokine market size for autoimmune care could surpass oncology by 2031 if current trajectories persist.

Infectious-disease cytokine use is contracting as curative antivirals displace interferon regimens, while inflammatory respiratory disorders converge mechanistically with autoimmune pathways, opening cross-indication leveraging of IL-4, IL-5, and IL-13 blockers. Oral Janus-kinase inhibitors add competitive pressure but often serve as bridge therapy when biologic access is delayed, indirectly supporting ongoing biologic sales.

By End User: Contract Research Organizations Surge

Pharma and biotech firms consumed 39.77% of cytokine output in 2025, but demand from contract research organizations (CROs) is projected to grow at 10.56% as outsourcing of complex protein production rises. The cytokine market share flowing through CRO suites is expected to reach double-digit territory by 2031.

Charles River and WuXi each invested more than USD 250 million in GMP cytokine capacity since 2024, banking on cell-therapy developers lacking internal plants. Academic labs represent a quarter of current volume for research-grade cytokines, while hospitals and diagnostics labs adopt cytokine panels for immune profiling. As clinical-stage companies prioritize capital-light models, CRO partnerships will remain critical to scaling the cytokine market.

By Function: Growth Factors Gain Momentum

Pro-inflammatory cytokines accounted for 46.24% of functional demand in 2025, yet growth and differentiation factors are poised for a 10.13% CAGR as biosimilar epoetin and filgrastim broaden access. That shift signals a gradual rebalance within the cytokine market.

Anti-inflammatory cytokines still play a niche role in transplant tolerance and wound repair because of infectious-risk concerns. Mechanistic overlap—such as IL-6 acting pro- or anti-inflammatory depending on context—encourages combination regimens that complicate trial design but can unlock synergistic efficacy. The functional landscape will therefore become more blended, making clear categorization challenging.

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies dispensed 53.66% of cytokine units in 2025, driven by inpatient CAR-T and high-dose IL-2. Online pharmacies, however, are forecast to post an 11.34% CAGR on the back of expanding cold-chain logistics from distributors like McKesson Specialty Health. Home delivery aligns with payer goals to shift infusion costs away from hospitals, boosting at-home adherence.

Specialty clinics retained roughly 20% share by providing on-site infusion services reimbursed at higher rates, while retail pharmacies lost ground due to limited refrigeration upgrades and branch closures by CVS and Walgreens. As e-commerce platforms mature, patient preference and insurer mandates will steer more biologic volume online, reshaping the cytokine market.

Geography Analysis

North America generated 41.53% of 2025 cytokine revenue, sustained by FDA Fast-Track and Priority Review pathways that cut median approval times to nine months. Medicare’s 2024 decision to reimburse outpatient CAR-T saved each patient USD 50,000 and widened access beyond academic hospitals. Canada’s pan-Canadian Pharmaceutical Alliance forced 25–40% price reductions for biosimilar TNF blockers, accelerating switch rates in Ontario and British Columbia. Mexico approved its first locally made filgrastim biosimilar in 2025, trimming import reliance by 30%.

Asia-Pacific is forecast to post a 10.79% CAGR through 2031, led by China’s 18 cytokine biosimilar approvals in 2024 under relaxed rules that allow foreign data and waive local Phase III trials. India earmarked USD 200 million to expand cytokine manufacturing for export, courting Western clients facing supply bottlenecks. Japan aligned its biosimilar review to ICH guidelines, cutting timelines to 16 months and attracting Samsung Biologics and Celltrion investments worth USD 1.2 billion. South Korea’s national insurance now covers all approved biosimilars, driving originator-to-biosimilar switching above 60% in hospitals. Australia’s 2025 interchangeability rule permits pharmacists to auto-substitute biosimilars, expected to save AUD 300 million (USD 195 million) per year.

Europe accounted for 28% of 2025 sales, concentrated in Germany, France, and the United Kingdom. EMA guidance lets one biosimilarity study unlock approvals across all indications, easing multi-label entry for adalimumab and infliximab copies. Germany enforces 80% prescribing quotas for TNF biosimilars, slashing originator share to 18% by 2025. France now demands clinical superiority for price premiums, squeezing legacy biologics. NICE ties reimbursement to cost-effectiveness thresholds that favor biosimilars below GBP 10,000 per QALY, nudging prescribers away from originators. Brazil, South Africa, and Gulf states round out the landscape as emerging buyers; Brazil’s volume-based contracts halved cytokine prices, widening public-system coverage.

Competitive Landscape

Consolidated Market with Strong Regional Leaders

The top five players, including AbbVie, Amgen, Novartis, and Pfizer, hold a roughly major share of 2025 revenue, giving the cytokine market a moderate concentration profile. Biosimilar entry is fragmenting share, particularly in TNF and IL-6 segments, prompting incumbents to invest in subcutaneous, high-concentration, and combination formats to extend lifecycles. Rare inflammatory disorders with populations under 100,000 represent high-value niches because expedited approvals allow premium pricing despite small volumes.

mRNA platforms from BioNTech and Moderna could capture 10–15% of oncology cytokine demand by 2030 if Phase II data validate safety and efficacy, potentially redrawing competitive lines. Amgen’s 2024 Teneobio deal added a heavy-chain-only antibody platform that simplifies manufacturing and supports convenient dosing. Regeneron’s VelocImmune mouse technology cuts antibody discovery timelines by 18 months, giving it a speed edge in interleukin-4 receptor blockade.

Roche filed 14 patents in 2024 for bispecific cytokines that tether IL-2 to tumor antigens, aiming to confine activation to malignant tissue. Manufacturing comparability remains a hurdle; FDA guidance demands analytic proof that single-use bioreactor transitions do not alter glycosylation profiles, favoring firms with deep process-development capabilities. As biosimilar pressure grows, differentiation will hinge on delivery technology, safety enhancements, and manufacturing agility, shaping future cytokine market trajectories.

Cytokine Industry Leaders

AbbVie Inc

Novartis AG

Johnson & Johnson

Amgen

F. Hoffmann La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Bristol Myers Squibb’s Breyanzi won FDA approval for relapsed or refractory marginal zone lymphoma as a one-time CD19 CAR-T infusion.

- October 2025: The FDA accepted an expedited-review sBLA for Tzield to delay stage 3 type 1 diabetes progression under the Commissioner’s National Priority Voucher pilot.

- August 2025: Celltrion gained FDA approval to extend AVTOZMA IV (tocilizumab-anoh) into cytokine release syndrome for adults and children aged ≥2 years.

- July 2025: Regeneron secured accelerated FDA approval for Lynozyfic in heavily pre-treated multiple myeloma, contingent on confirmatory evidence.

Global Cytokine Market Report Scope

As per the scope of the report, cCytokines are small signaling proteins that act as messengers between cells, regulating immune responses, inflammation, and cell growth and development. Produced by immune cells (e.g., T cells, macrophages) and others (e.g., fibroblasts, endothelial cells), they bind to cell surface receptors to trigger specific actions such as activating immune cells, inducing inflammation, or coordinating tissue repair. They function through autocrine (self), paracrine (nearby), or endocrine (distant) signaling mechanisms.

The Cytokine Market is segmented by product type, therapeutic application, end user, function, distribution channel, and geography. The Product Type market is segmented into Interleukins, Tumor Necrosis Factor, Interferons, Colony-Stimulating Factors, Chemokines, and Growth Factors. By Therapeutic Application, the market is segmented into cancer and malignancies, Autoimmune Disorders, Infectious Diseases, Inflammatory Disorders, and Others. By End User, the market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, hospitals and diagnostic laboratories, and Contract Research Organizations. By Function, the market is segmented into Pro-inflammatory Cytokines, Anti-inflammatory Cytokines, Growth & Differentiation Factors. By Distribution Channel, market is segmented into Hospital Pharmacies, Specialty Clinics, Retail Pharmacies, Online Pharmacies. By Geography, market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Interleukins |

| Tumor Necrosis Factor (TNF) |

| Interferons |

| Colony-Stimulating Factors (CSFs) |

| Chemokines |

| Growth Factors |

| Cancer & Malignancies |

| Autoimmune Disorders |

| Infectious Diseases |

| Inflammatory Disorders |

| Others |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Hospitals & Diagnostic Laboratories |

| Contract Research Organizations (CROs) |

| Pro-inflammatory Cytokines |

| Anti-inflammatory Cytokines |

| Growth & Differentiation Factors |

| Hospital Pharmacies |

| Specialty Clinics |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Interleukins | |

| Tumor Necrosis Factor (TNF) | ||

| Interferons | ||

| Colony-Stimulating Factors (CSFs) | ||

| Chemokines | ||

| Growth Factors | ||

| By Therapeutic Application | Cancer & Malignancies | |

| Autoimmune Disorders | ||

| Infectious Diseases | ||

| Inflammatory Disorders | ||

| Others | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Hospitals & Diagnostic Laboratories | ||

| Contract Research Organizations (CROs) | ||

| By Function | Pro-inflammatory Cytokines | |

| Anti-inflammatory Cytokines | ||

| Growth & Differentiation Factors | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Clinics | ||

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the cytokine market in 2026?

The cytokine market size reached USD 106.14 billion in 2026 and is projected to grow at a 7.08% CAGR to USD 149.41 billion by 2031.

Which segment is expanding fastest within cytokines?

Interleukin products are expected to post a 9.84% CAGR through 2031, the quickest among product categories.

Why is Asia-Pacific attracting attention for cytokine manufacturing?

Streamlined biosimilar pathways in China, new Indian incentives, and Korean reimbursement all contribute to a 10.79% forecast CAGR in the region.

What is driving growth in online pharmacy distribution?

Improved cold-chain logistics and payer preference for home delivery support an 11.34% CAGR for online channels.

How are mRNA platforms affecting cytokine development?

MRNA-encoded cytokines shorten production timelines and localize immune activation, potentially winning 10–15% oncology share by 2030 if trials succeed.

Page last updated on: