Cyclopentane Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

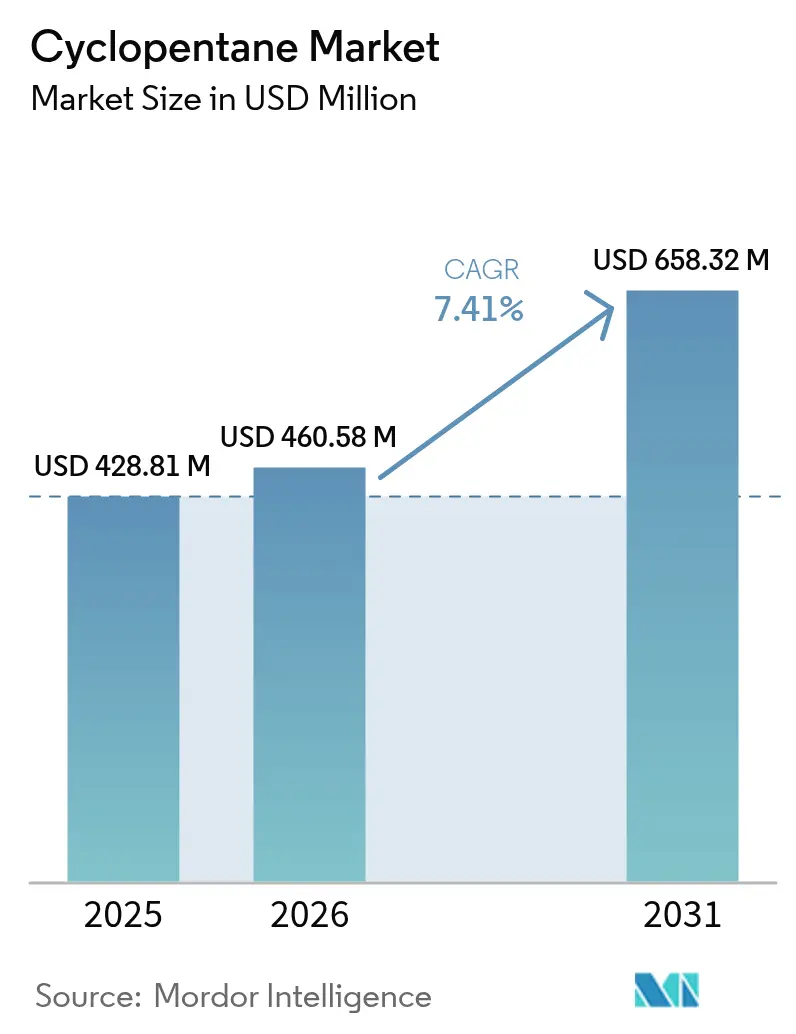

| Market Size (2026) | USD 460.58 Million |

| Market Size (2031) | USD 658.32 Million |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cyclopentane Market Analysis by Mordor Intelligence

The Cyclopentane Market size was valued at USD 428.81 million in 2025 and estimated to grow from USD 460.58 million in 2026 to reach USD 658.32 million by 2031, at a CAGR of 7.41% during the forecast period (2026-2031). Regulatory accelerators—most notably the Kigali Amendment’s stepped-down HFC quotas—have elevated cyclopentane from a niche hydrocarbon to a mainstream compliance pathway for appliance, construction and cold-chain manufacturers. Producers are simultaneously confronting constrained feedstock supply, limited global capacity and rising transportation costs, prompting investments in on-site blending and high-purity processing assets. Competitive strategies now hinge on balancing volume-driven foam markets with higher-margin specialty end uses such as vacuum insulated panels (VIPs) and electric-vehicle battery modules, where tighter chemical specifications command premium prices. While raw-material volatility and stricter hydrocarbon safety codes weigh on margins, the cyclopentane market continues to benefit from multi-industry decarbonization mandates, widening its application footprint across emerging and mature economies alike.

Key Report Takeaways

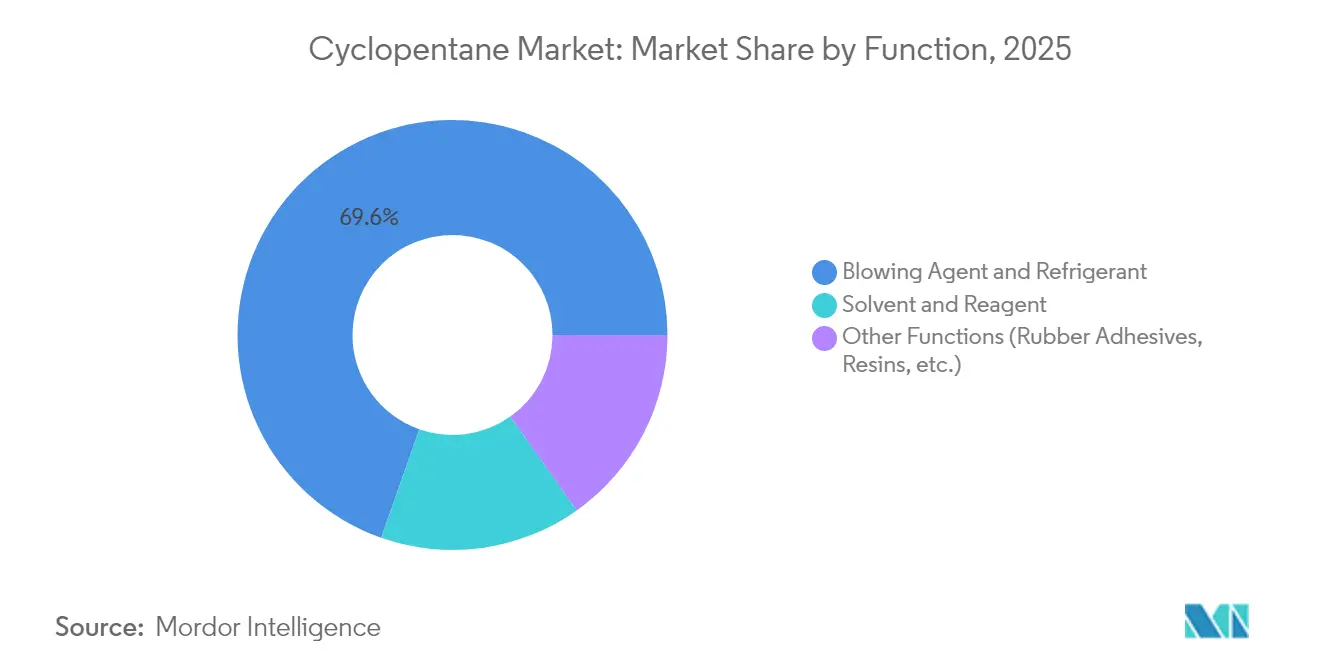

- By function, blowing agents and refrigerants captured 69.62% of cyclopentane market share in 2025, whereas solvents and reagents are forecast to grow at an 7.98% CAGR through 2031.

- By purity grade, ≥98% cyclopentane led with 54.71% revenue share in 2025; this grade is advancing at a 7.75% CAGR to 2031.

- By application, refrigeration accounted for a 61.62% share of the cyclopentane market size in 2025, yet insulation applications are expected to expand at 7.99% CAGR over 2026-2031.

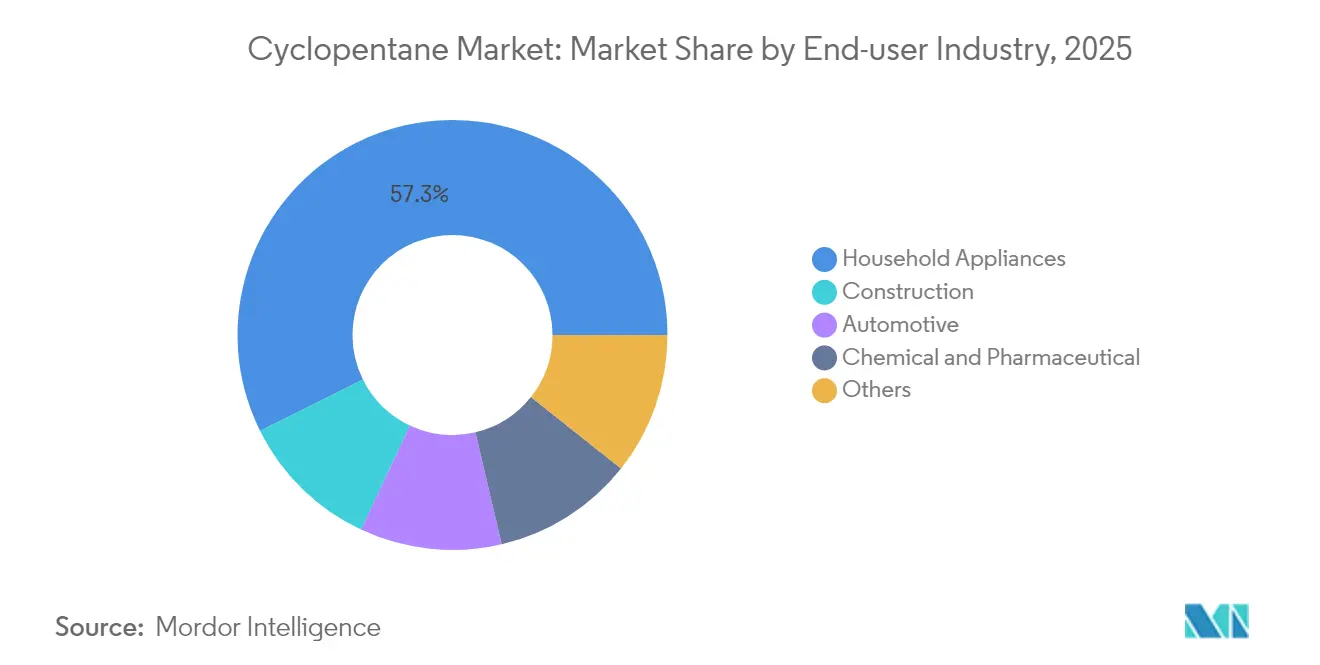

- By end-use industry, household appliances commanded 57.34% of the cyclopentane market in 2025, while construction is projected to post the fastest 8.04% CAGR to 2031.

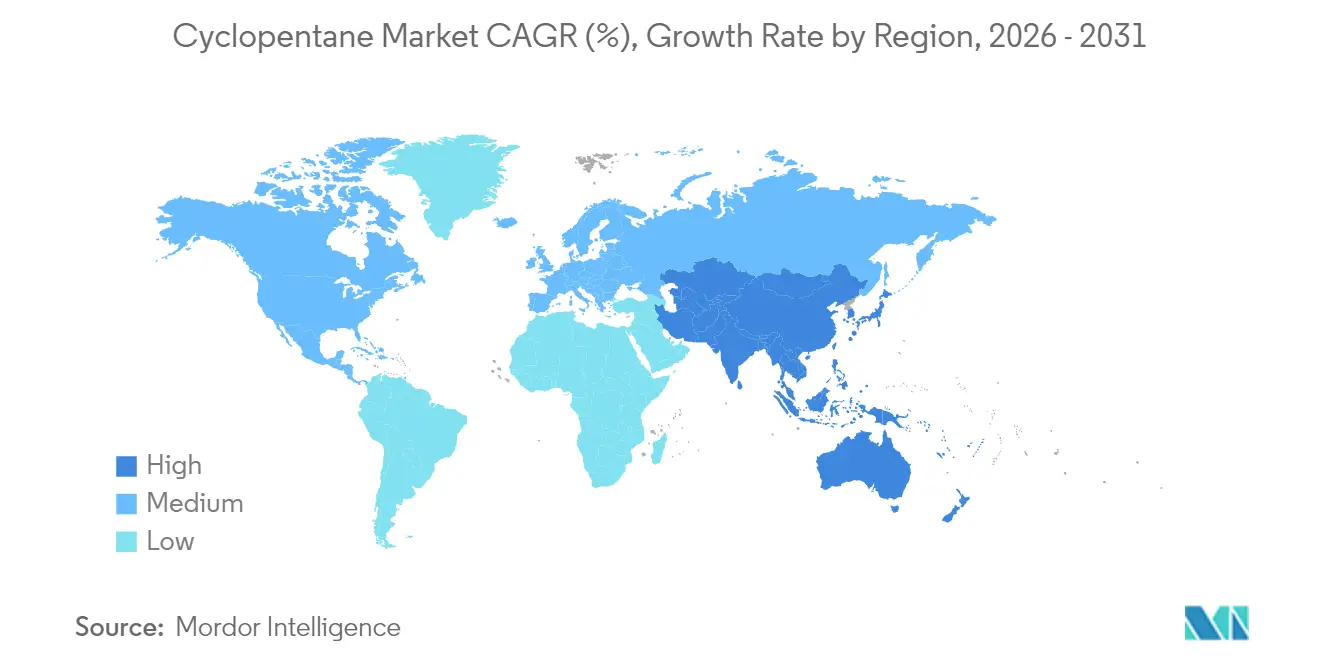

- By geography, Asia-Pacific held 45.22% of the global cyclopentane market in 2025 and is set to grow at an 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cyclopentane Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of cyclopentane VIP blowing agents | +1.2% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Kigali Amendment-driven HFC phase-down | +2.1% | EU, North America, global | Short term (≤2 years) |

| Cold-chain demand for eco-refrigerants | +1.8% | Asia-Pacific core; MEA & Latin America spill-over | Medium term (2-4 years) |

| EV battery pack lightweight foams | +0.9% | China, EU, North America | Long term (≥4 years) |

| On-site pentane blending cost savings | +0.7% | High-volume manufacturing hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cyclopentane Blowing Agents in High-Performance Vacuum Insulated Panels

Cyclopentane-based VIP cores enable refrigerator and building-panel producers to achieve top-tier thermal resistance while slimming wall thickness, freeing interior volume and cutting energy use. Studies show that substituting 40% of fumed silica with cyclopentane foam maintains λ-values below 4 mW/m·K, lowering material costs without performance sacrifice. Premium appliance makers are leveraging the thinner-wall advantage to boost storage capacity within fixed external dimensions, a key differentiator in tightly regulated efficiency tiers. Haltermann Carless’s incremental debottlenecking in Germany is directed at these high-specification batches, reflecting the price premium VIP grades fetch[1]Haltermann Carless, “Expanding High-Purity Pentane Capacities for VIP Applications,” haltermann-carless.com. Rising electricity tariffs worldwide further strengthen the value proposition, making VIP adoption a cost-effective route to compliance and consumer savings.

Regulations Phasing-Down HFC Blowing Agents Under Kigali Amendment

Europe’s F-Gas Regulation drops HFC quotas to 9 Mt CO2-eq by 2030, triggering immediate shortages that amplify cyclopentane uptake in foam and refrigeration lines. Parallel rules in the United States, where the EPA approved additional hydrocarbon substitutes under SNAP in December 2024, remove lingering adoption barriers and streamline permitting[2]Environmental Protection Agency, “SNAP Rule 26—Acceptable Substitutes for Refrigeration and Air-Conditioning,” epa.gov. UNIDO-backed conversions in Chinese appliance factories demonstrate scalable, incident-free transitions when robust safety protocols are applied. As a result, board-room investment ranking now classifies cyclopentane capacity as an essential permit-to-operate, not an optional sustainability upgrade.

Demand for Eco-Friendly Refrigerants in Expanding Cold-Chain Logistics Across Emerging Economies

Emerging economies are racing to build temperature-controlled warehousing to meet booming demand for perishable foods and vaccines. The zero-ODP, low-GWP profile of cyclopentane satisfies multinational retail and pharma corporate governance codes while meeting local efficiency mandates. Operators in Indonesia, Vietnam and Nigeria report energy cost ratios up to 30% of operating expenses, making high-performance insulation critical for profitability. Asia-Pacific governments increasingly embed HFC phase-down clauses in bilateral trade deals, accelerating timelines for substitution and reinforcing growth for the cyclopentane market.

Lightweight Composite Insulating Foams for EV Battery Packs

Organic Rankine cycle tests confirm that cyclopentane achieves 72% heat-transfer efficiency at stable pressures suited to automotive systems. Automakers integrating pack-level thermal shields gain dual benefits of weight reduction and consistent battery temperature, supporting range extension and safety compliance. Composite suppliers are co-developing thermoplastic skins with embedded cyclopentane foams, offering recyclability advantages over epoxy-based alternatives. The electrification wave therefore unlocks a long-tail growth curve beyond legacy white-goods demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock (naphtha/crude) price volatility | -1.4% | Net-import regions in Asia & Europe | Short term (≤2 years) |

| Stricter safety codes for flammable HC gases | -0.8% | Developed markets first, global rollout | Medium term (2-4 years) |

| Limited capacity & unplanned outages | -1.1% | Regions lacking indigenous production | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Feedstock (Naphtha/Crude) Price Volatility

Cyclopentane’s synthesis from cracker-grade streams exposes producers to propylene and naphtha price spikes. Argus forecasts show Northwest Europe propylene contracts climbing on planned refinery rationalizations, compressing foam-grade margins. Integrated refiners partially shield earnings by channeling co-product streams into captive cyclopentane units, but such scale remains unattainable for many standalone formulators. Smaller firms lack the credit lines to hedge multi-month feedstock swings, propelling sector consolidation as they seek balance-sheet relief within larger portfolios.

Stricter Safety Codes for Flammable Hydrocarbons Raise Compliance Costs

The U.S. Pipeline and Hazardous Materials Safety Administration’s October 2024 rulemaking adds tank-car design reviews and facility registration, projecting USD 97.3 million in net benefits, yet requiring significant upfront capex. OSHA’s May 2024 HazCom revision mandates pictogram-rich labeling and extended training, elevating administrative spend. EPA’s concurrent Risk Management Program amendments cover 11,740 facilities and introduce third-party audits, driving annual costs of USD 256.9 million. Compliance disproportionately affects sub-10 ktpa producers, intensifying exit or acquisition decisions and heightening the cyclopentane market’s consolidation trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Blowing Agents Drive Market Leadership

Blowing agents and refrigerants held 69.62% of cyclopentane market share in 2025, as appliance and panel producers adopted the hydrocarbon to satisfy HFC-phase-down quotas. This mainstream volume anchors cash flow for suppliers; nevertheless, the solvent and reagent niche, though representing modest tonnage, is charted to grow at 7.98% CAGR, reflecting diversification into pharmaceutical synthesis and specialty polymerization lines. Developers targeting these chemistries must guarantee ultra-low benzene content and sub-20 ppm sulfur, characteristics that fetch a 20-30% price premium. Future revenue therefore hinges on balancing scale economics with niche customization—a dual-track strategy increasingly evident across the cyclopentane industry.

By Purity Grade: High-Purity Specifications Command Premium

≥98% purity grades captured 54.71% of 2025 demand, buoyed by VIPs and high-efficiency refrigerator walls where off-spec impurities jeopardize λ-performance. The segment is forecast to widen its lead at a 7.75% CAGR, supported by expanded distillation columns in Singapore and the U.S. Gulf Coast. The mid-tier 95-98% bracket services conventional rigid-foam boards, while technical grades (<95%) retreat to solvent duty as regulatory baselines tighten. EPA sets a 95% minimum purity for SNAP-approved cyclopentane, embedding a compliance floor that squeezes low-grade production economics. Investors therefore prioritize debottlenecking purity towers rather than green-field technical-grade assets.

By Application: Refrigeration Dominance Faces Insulation Growth

Refrigeration lines accounted for 61.62% of the cyclopentane market size in 2025, reflecting decades-long brand familiarity in refrigerator foams. Insulation boards and VIP cores, however, are slated for 7.99% CAGR, boosted by net-zero building codes and retro-fit subsidies in the EU and South Korea. Chemical solvent usage remains steady at single-digit share, limited by alternative hydrocarbon blends. Strategic focus is shifting toward building-sector procurement, where public-sector tender volumes incentivize locked-in supply contracts, shielding suppliers from spot volatility.

By End-Use Industry: Household Appliances Lead Amid Construction Growth

Household appliances absorbed 57.34% of global cyclopentane volumes in 2025, a reflection of refrigerator and freezer output in China, Turkey and Mexico. Construction is the brightest growth pocket at 8.04% CAGR, riding stringent insulation requirements under Europe’s EPBD recast and India’s Eco-Niwas Samhita code. Automotive uptake, though presently niche, gains momentum via battery thermal barriers and lightweight interior panels. Chemical and pharmaceutical users favor cyclopentane for reaction control in select syntheses, though volumes stay modest. Producers tailoring additive packages for construction foams stand to capture outsized margins as architects specify lower λ-values for tall-building façades.

Geography Analysis

Asia-Pacific’s 45.22% market hold, coupled with 8.21% CAGR to 2031, is driven by rising appliance penetration and government-funded cold-chain nodes. China, backed by UNIDO technical training, retrofitted 140+ refrigerator lines to cyclopentane without incident, underscoring scalable safety viability. Japan’s Top-Runner efficiency mandate fuels continuous VIP innovation, while India’s PLI scheme incentivizes localized foam-grade production, curbing import reliance. North America and Europe focus on high-purity cycles and stringent occupational-safety audits, commanding price premiums that offset slower volume growth. EPA SNAP revisions and Europe’s quota cliff accelerate HFC exit, making cyclopentane the default drop-in across foams. MEA and Latin America trail yet present latent upside once logistics corridors and regulatory clarity mature.

Sub-regional dynamics reveal intra-Asia shifts: Southeast Asian contract packagers increasingly source cyclopentane from Singapore and South Korea to mitigate Chinese port congestion. In Europe, importers balance Russian feedstock risk by diversifying to U.S. Gulf Coast supply. North American blenders co-locate with polyurethane panel plants across Mexico’s Bajío corridor, curtailing hazardous-goods haulage miles. Altogether, the cyclopentane market landscape intertwines regulatory cadence, logistics elasticity and purity demands, shaping divergent regional strategies over the forecast horizon.

Competitive Landscape

The cyclopentane market exhibits moderate concentration: the top five suppliers hold an estimated 55-60% output, while niche formulators address specialty applications. Chevron Phillips Chemical leverages integrated ethylene crackers to stabilize feedstock and is upgrading C5 splitter capacity in Cedar Bayou for high-purity throughput. INEOS capitalizes on its European refinery footprint, enabling backward integration that insulates margins during crude spikes. Haltermann Carless focuses on specialty purification, launching ISCC PLUS mass-balance certified cyclopentane in 2023 to tap circular-economy premiums. Regional independents install on-site blending skids to serve captive foam plants, a strategic hedge against maritime delays.

Consolidation is poised to continue as regulatory compliance costs and feedstock volatility strain under-scale operators, opening acquisition runways for cash-rich majors aiming to broaden geographic coverage.

Cyclopentane Industry Leaders

-

INEOS

-

Haltermann Carless Group GmbH

-

SK Geo Centric Co., Ltd.

-

Chevron Phillips Chemical Company LLC

-

Maruzen Petrochemical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: HCS Group’s acquisition by International Chemical Investors Group closed, creating a new hydrocarbon specialties platform within ICIG.

- February 2023: Haltermann Carless launched ISCC PLUS-certified mass-balance n-/iso- and cyclopentanes, offering reduced carbon footprints for insulation customers.

Global Cyclopentane Market Report Scope

Cyclopentane is a flammable hydrocarbon used in the manufacture of synthetic resins and rubber adhesives. It is also used as a blowing agent in the production of polyurethane insulating foam. It is used in a variety of household appliances like refrigerators and freezers, replacing environmentally harmful substitutes like CFC-11 and HCFC-141b.

The cyclopentane market is segmented into function, application, and geography. Based on function, the market is segmented into blowing agents & refrigerants, solvents & reagents, and other functions (rubber adhesives, resins, etc.). The market is segmented by applications into refrigeration, insulation, chemical solvent, and other applications (personal care, fuel additives, etc.). The report also covers the market size and forecasts for the cyclopentane market in 15 countries across major regions. For each segment, the market sizing and forecasts are done on the basis of Revenue (USD).

| Blowing Agent and Refrigerant |

| Solvent and Reagent |

| Other Functions (Rubber Adhesives, Resins, etc.) |

| ≥ 98 % Purity |

| 95 - 98 % Purity |

| < 95 % Purity (Technical grade) |

| Refrigeration |

| Insulation |

| Chemical Solvents |

| Other Applications (Personal Care, Fuel Additives) |

| Household Appliances |

| Construction |

| Automotive |

| Chemical and Pharmaceutical |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Function | Blowing Agent and Refrigerant | |

| Solvent and Reagent | ||

| Other Functions (Rubber Adhesives, Resins, etc.) | ||

| By Purity Grade | ≥ 98 % Purity | |

| 95 - 98 % Purity | ||

| < 95 % Purity (Technical grade) | ||

| By Application | Refrigeration | |

| Insulation | ||

| Chemical Solvents | ||

| Other Applications (Personal Care, Fuel Additives) | ||

| By End-use Industry | Household Appliances | |

| Construction | ||

| Automotive | ||

| Chemical and Pharmaceutical | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current cyclopentane market size and projected growth?

The cyclopentane market size is USD 460.58 million in 2026 and is forecast to reach USD 658.32 million by 2031, growing at a 7.41% CAGR.

Which region dominates the cyclopentane market?

Asia-Pacific leads with 45.22% share in 2025 and is also the fastest-growing region at an 8.21% CAGR through 2031.

Why are vacuum insulated panels important for cyclopentane demand?

VIPs require high-purity cyclopentane to achieve ultra-low thermal conductivity, enabling thinner walls and higher energy efficiency, a segment growing at 7.75% CAGR.

How are regulations influencing cyclopentane adoption?

Kigali Amendment HFC phase-downs and EPA SNAP approvals are accelerating the shift to cyclopentane, especially in foams and refrigeration, adding an estimated +2.1% to forecast CAGR.

What are the key restraints on cyclopentane market growth?

Feedstock price volatility, stricter flammable-gas safety codes and limited global capacity together subtract around 3.3% from potential CAGR.

Which end-use industry is growing fastest outside appliances?

Construction uses of cyclopentane-based insulation are expanding at an 8.04% CAGR, driven by stringent building-energy codes worldwide.

Page last updated on: