Cushing's Syndrome Diagnostics And Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

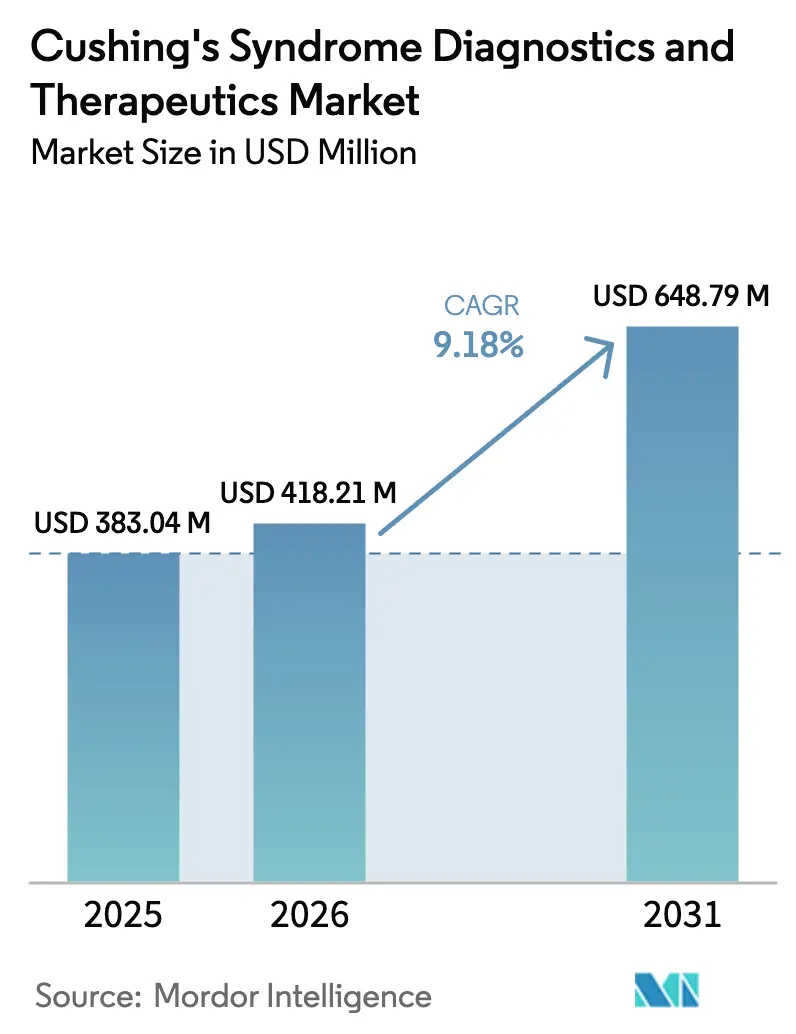

| Market Size (2026) | USD 418.21 Million |

| Market Size (2031) | USD 648.79 Million |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

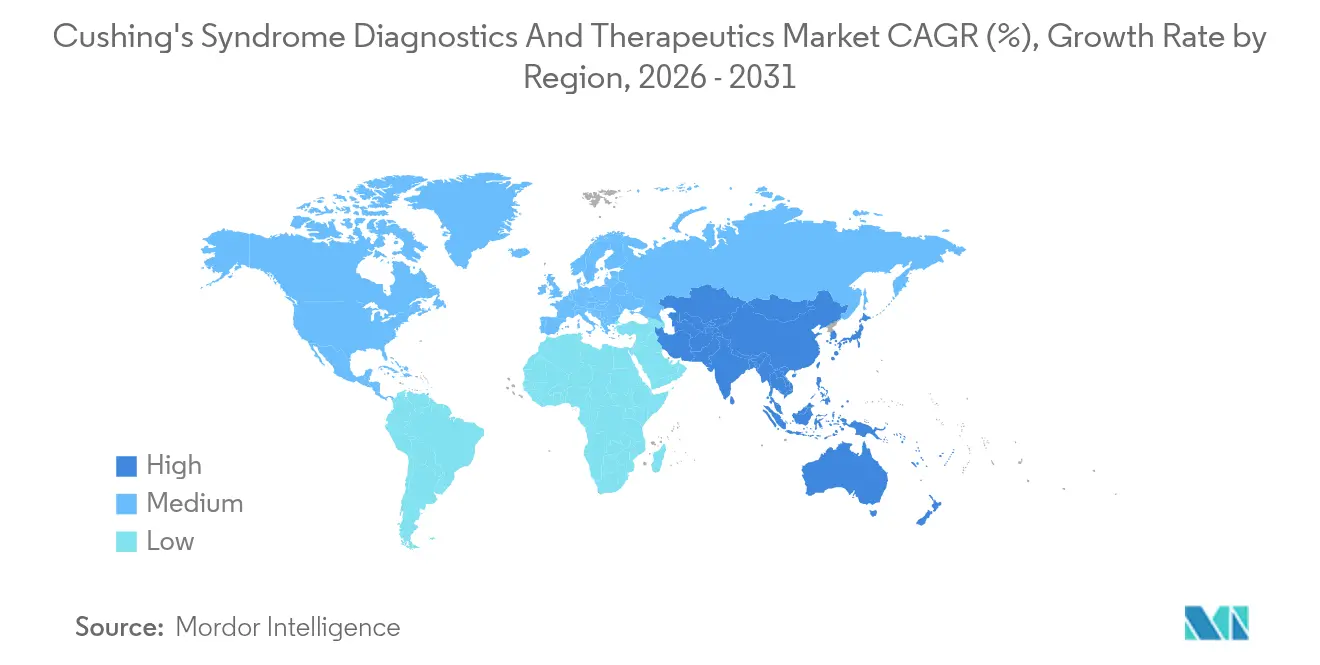

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cushing's Syndrome Diagnostics And Therapeutics Market Analysis by Mordor Intelligence

The Cushing's syndrome diagnostics and therapeutics market size was valued at USD 383.04 million in 2025 and estimated to grow from USD 418.21 million in 2026 to reach USD 648.79 million by 2031, at a CAGR of 9.18% during the forecast period (2026-2031). Broader screening in diabetology clinics, multiple late-stage pipeline assets, and digital distribution channels are combining to expand access, while favorable orphan-drug regulations and precision biomarker panels continue to shorten development cycles. Intensifying competition among selective cortisol modulators, notably relacorilant and osilodrostat, is expected to keep innovation high and prices under watch. Added momentum comes from stereotactic radiosurgery advances that are lifting radiation therapy uptake, and from online pharmacies that are making chronic-care refills easier for patients spread across wide geographies. Yet the market still contends with high treatment costs, diagnostic complexity, and payer prior-authorization hurdles that slow therapeutic starts.

Key Report Takeaways

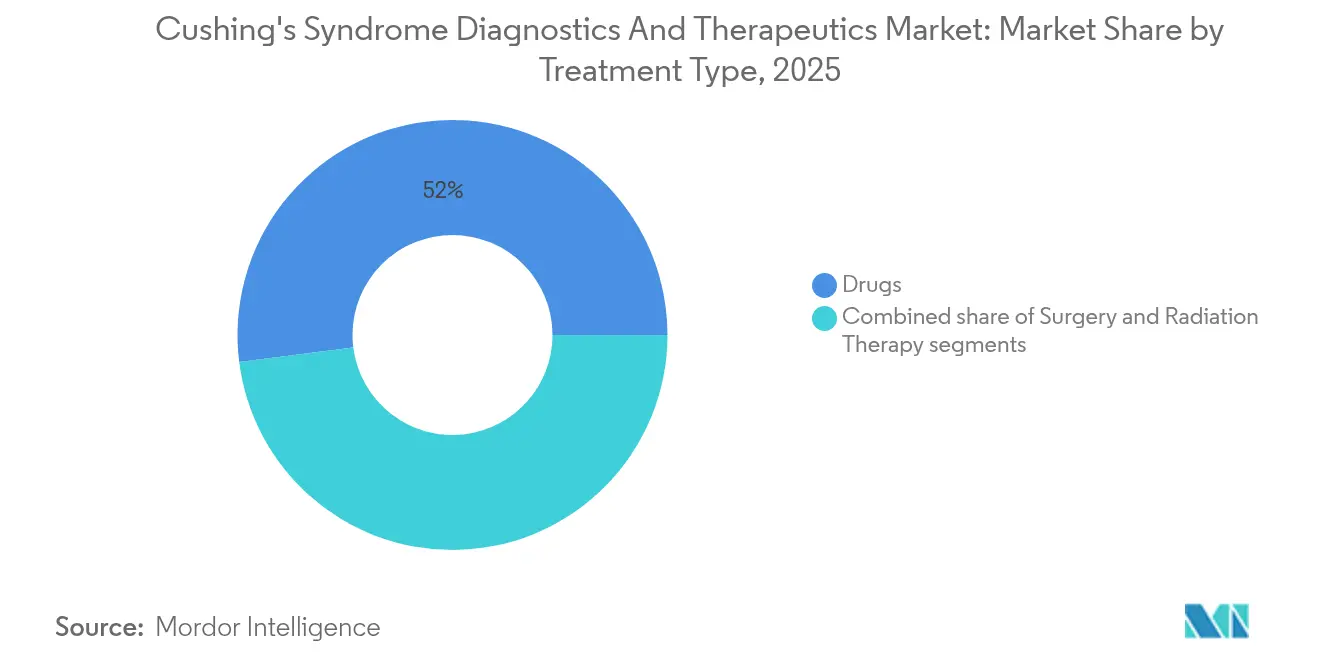

- By treatment type, drugs held 52.01% of the Cushing's syndrome diagnostics and therapeutics market share in 2025, while radiation therapy is projected to advance at an 11.12% CAGR between 2026 and 2031.

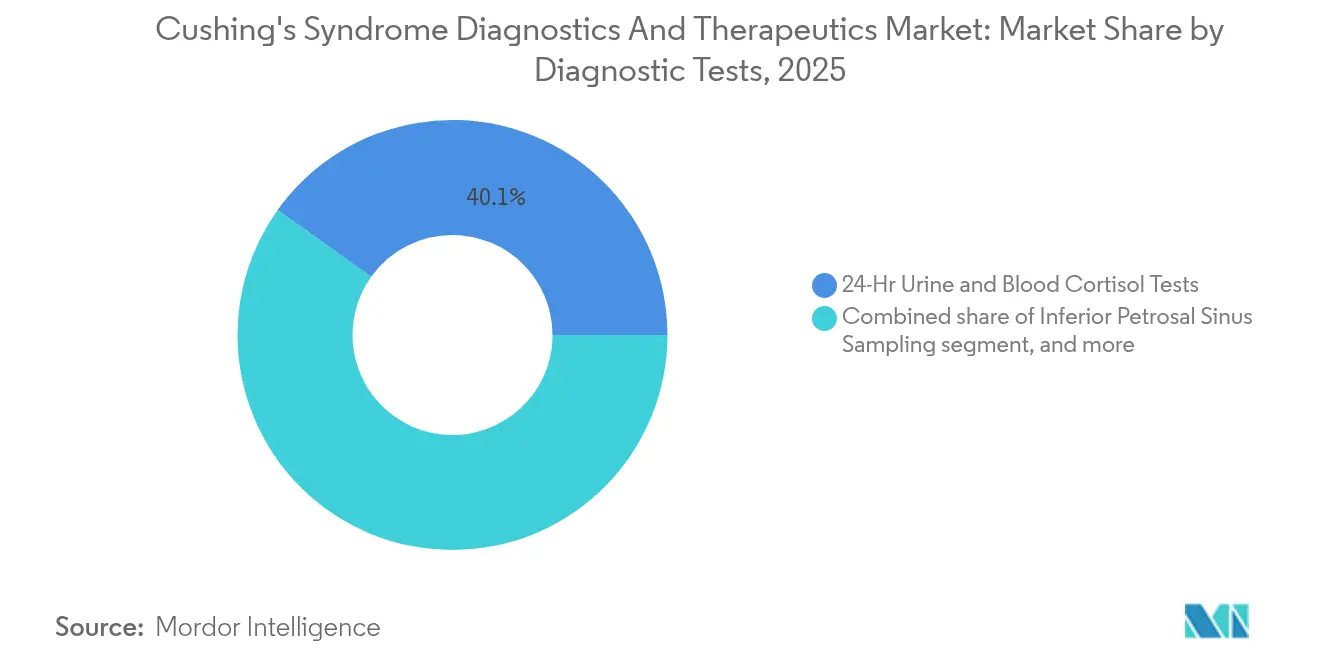

- By diagnostic test, 24-hour urine and blood cortisol panels accounted for 40.12% of the Cushing's syndrome diagnostics and therapeutics market size in 2025; hair-based and LC-MS/MS assays are expanding at an 11.35% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 53.88% of the Cushing's syndrome diagnostics and therapeutics market size in 2025, whereas online pharmacies are forecast to post a 12.08% CAGR to 2031.

- By geography, North America led with 41.02% revenue share in 2025; Asia-Pacific is on track for a 10.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cushing's Syndrome Diagnostics And Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of Cushing's syndrome | +2.1% | Global, stronger effect in North America & EU | Medium term (2-4 years) |

| Increasing R&D investments | +1.8% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Advances in diagnostic technologies | +1.5% | Global, early uptake in developed markets | Short term (≤ 2 years) |

| Expansion of orphan drug designations | +1.3% | North America & EU regulatory environments | Medium term (2-4 years) |

| Adoption of tele-endocrinology platforms | +0.9% | Global, accelerated post-pandemic | Short term (≤ 2 years) |

| Growing availability of compassionate-use programs | +0.7% | Primarily North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cushing's Syndrome

Routine screening of difficult-to-control type 2 diabetes has uncovered a 24% prevalence of hypercortisolism, instantly broadening the Cushing’s syndrome diagnostics and therapeutics market. As primary-care physicians incorporate low-cost salivary and urinary cortisol checks into annual check-ups, thousands of previously undiagnosed patients are being funneled toward confirmatory testing and long-term therapy. Machine-learning classifiers trained on routine laboratory panels now offer non-invasive case-finding tools that bypass inferior petrosal sinus sampling, thus reducing both cost and patient risk. Collectively, these measures lift patient volumes, extend treatment duration, and reinforce the business case for new diagnostic disposables and modular sensor platforms.

Increasing Research and Development Investments

Selective cortisol modulators with no progesterone-receptor binding such as relacorilant have emerged from more than 1,000 proprietary analogs, creating a defensible IP moat for Corcept Therapeutics. Spill-over from adjacent adrenal disorders, highlighted by the atumelnant Phase 2 success in congenital adrenal hyperplasia, is broadening therapeutic pipelines and adding new label-extension targets. In parallel, academic centers are sequencing corticotroph adenomas to uncover USP8 and USP48 mutations that correlate with surgical outcomes, opening precision-medicine opportunities for target-specific adjuvants. Capital continues to flow toward combination regimens that pair steroidogenesis inhibitors with ACTH antagonists, aided by rare-disease grants and tax credits.

Advances In Diagnostic Technologies

Point-of-care LC-MS/MS cartridges now quantify cortisol, cortisone, and dexamethasone in one 20-µL finger-stick sample, trimming turnaround time to 15 minutes and raising confidence in overnight suppression tests. Hair-strand assays, validated at 90% diagnostic accuracy, supply a three-month cortisol exposure history, thereby helping clinicians differentiate chronic endogenous hypercortisolism from transient stress responses. Real-time electrochemical biosensors embedded in smartwatch bands provide continuous cortisol readouts that alert both patients and physicians to post-surgical recurrences. Integration of AI into full-blood-count analysis further enables early flagging of mild cases, improving chances of organ-sparing interventions.

Expansion Of Orphan Drug Designations

Recent FDA orphan designations for clofutriben and crinecerfont secure seven-year U.S. exclusivity, creating predictable cash-flow horizons that draw mid-cap biotech interest. Harmonized EMA procedures now offer a similar 10-year window in Europe, while mutual-recognition treaties trim duplicative studies and regulatory friction[1]EMA, “Orphan Drug Designation Procedures,” ema.europa.eu. As more pipeline assets benefit from priority review vouchers, overall phase-III attrition risk falls, shortening average time-to-market by nearly 18 months. The result is faster therapy rollout, stronger company valuations, and a more competitive Cushing's syndrome diagnostics and therapeutics market landscape.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs | -1.9% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Diagnostic complexity and delayed detection | -1.4% | Global, pronounced in resource-limited settings | Medium term (2-4 years) |

| Limited endocrinologist workforce | -0.8% | Emerging markets and rural regions | Medium term (2-4 years) |

| Stringent post-marketing safety monitoring requirements | -0.6% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs

A full-year Korlym course costs insurers more than USD 150,000 and has driven strict prior-authorization protocols that slow time-to-therapy by up to 11 weeks in U.S. managed-care settings. Even when coverage is granted, dose-titration caps and six-month re-authorizations create administrative drag and spark occasional therapy discontinuations. In lower-middle-income nations, where out-of-pocket spending is decisive, many patients defer care until invasive surgery becomes unavoidable, constraining addressable demand despite rising prevalence.

Diagnostic Complexity and Delayed Detection

Current algorithms call for at least two positive first-line tests followed by imaging and, often, site-of-origin sampling, elongating diagnostic pathways beyond 18 months in many health systems. Non-specific symptomatology—obesity, hypertension, glucose intolerance—means primary physicians frequently pursue common metabolic causes first, losing critical windows for early, organ-sparing interventions. Disparities persist: Black patients present with larger macroadenomas and more hypopituitarism, pointing to diagnostic-pathway bias that still awaits correction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Drugs Maintain Dominance Despite Surgical Innovation

Drug-based regimens captured 52.01% of the Cushing's syndrome diagnostics and therapeutics market share in 2025 as lifelong management needs favored oral and IV therapies, while radiation therapy is projected to record an 11.12% CAGR to 2031 on the back of precision radiosurgery roll-outs. Initial trans-sphenoidal surgery succeeds in 90% of small adenomas but up to 30% of cases relapse, steering clinicians toward adjuvant relacorilant or osilodrostat courses. Advances in gamma-knife protocols, delivering submillimeter accuracy, are keeping peri-pituitary tissue damage low and widening eligibility for frail elderly patients. Biomarker-guided selection—particularly USP8 mutation status—is further refining postoperative regimens and lengthening drug therapy duration, strengthening the long-run dominance of pharmaceuticals within the wider Cushing's syndrome diagnostics and therapeutics market.

Precision-medicine pipelines emphasize specificity: relacorilant avoids progesterone-receptor cross-reactivity, potentially cutting gynecologic adverse events by 70% relative to mifepristone. ACTH antagonists such as atumelnant add mechanistic variety, promising combinational logic that may counter resistance seen in long-term monotherapy. With several entrants eyeing 2026-2028 launches, drug portfolios look primed for steady growth, cushioning revenue even as surgery and radiation maintain their frontline status.

By Diagnostic Tests: Traditional Methods Face Innovation Pressure

The 24-hour urine and serum battery still accounts for 40.12% of Cushing's syndrome diagnostics and therapeutics market size, but hair-based and LC-MS/MS panels now exhibit the fastest uptake at 11.35% CAGR through 2031. Point-of-care cartridges shrink lab wait times from days to minutes, allowing real-time surgical decision-making and earlier therapy starts. Salivary late-night cortisol, while convenient, sees assay-to-assay variability, nudging labs toward mass-spec confirmation workflows that are less prone to false positives.

Emerging AI-guided pattern recognition of routine blood tests has entered primary-care toolkits, flagging patients whose cortisol trajectories sit outside normative diurnal patterns. In resource-limited regions, urinary cortisol/creatinine ratios—showing 88.3% sensitivity and 91.7% specificity—offer an inexpensive alternative, amplifying case identification and routing more patients into the Cushing's syndrome diagnostics and therapeutics market funnel.

By Distribution Channel: Digital Transformation Accelerates Access

Hospital pharmacies commanded 53.88% of the 2025 Cushing's syndrome diagnostics and therapeutics market size due to initial dosing supervision requirements, yet online pharmacies are sprinting ahead with a 12.08% CAGR to 2031 as chronic-care refills migrate to mail-order models. Specialty portals integrate financial-assistance bots, appointment booking, and remote nursing, simplifying adherence for geographically dispersed patients. COVID-era telemedicine normalized virtual endocrine consults, and integrated e-prescription platforms now push drug orders directly to accredited online dispensaries, trimming average refill time by 37%.

Retail pharmacies hold the middle ground, convenient for stable maintenance but constrained by limited stock-keeping of niche orphan drugs. As wearable cortisol sensors feed dosing algorithms to physicians in real time, hospital-based IDNs are setting up centralized specialty-pharmacy hubs, preserving share against pure-play e-commerce entrants.

Geography Analysis

North America retained 41.02% of 2025 revenue on the strength of academic medical centers, a mature payer system that reimburses orphan drugs, and multiple active late-stage trials that channel patients straight into commercial therapy once approvals arrive. The FDA continues to run point on expedited pathways, making the region the preferred launch pad for premium-priced selective cortisol modulators. Large managed-care organizations, despite rigid prior-authorization templates, furnish structured reimbursement once criteria are met, underpinning overall adoption.

Asia-Pacific, advancing at a projected 10.11% CAGR, is seeing rapid diagnostic uptake as governments expand rare-disease lists and introduce partial reimbursement for imports. Thailand’s 15-year registry points to a higher prevalence of ACTH-independent disease, steering surgical protocols toward adrenalectomy and bolstering demand for postoperative cortisol blockers. China’s centralized procurement of LC-MS/MS analyzers and Japan’s early embrace of hair-cortisol assays are shrinking diagnosis lag times and broadening the therapeutic base.

Europe maintains steady mid-single-digit expansion, thanks to a harmonized orphan-drug framework that rewards symmetrical launches across the bloc. ERCUSYN’s pancontinental registry fuels evidence-based guideline updates, while cross-border treatment programs help smaller states access high-cost drugs. South America and parts of the Middle East still trail, hampered by import tariffs and currency volatility that drive retail prices beyond patient reach, but aid agencies are piloting risk-sharing schemes to narrow the gap.

Competitive Landscape

The competitive field shows moderate concentration, with the top five companies estimated to command about 55% of revenue, leaving meaningful room for pipeline challengers. Corcept Therapeutics leverages Korlym’s established cash-flow to finance relacorilant and a deeper bench of selective cortisol modulators. Recordati’s ISTURISA extension into broader hypercortisolemia indications signals a push to secure share before newer modulators arrive.

Novartis, via pasireotide, uses its endocrinology franchise to cross-promote next-generation products, while emerging biotechs such as Crinetics and Sparrow emphasize novel mechanisms—ACTH antagonism and HSD-1 inhibition—that could re-segment the drug landscape.

Technology partnerships are multiplying: Ubie’s AI symptom checker funnels potential patients into clinician networks, boosting diagnostic throughput and indirectly driving drug sales[3]Pharmaphorum, “Ubie Partners with Cushing’s Foundation,” pharmaphorum.com. Specialty-pharmacy tie-ups add longitudinal data streams that inform pay-for-performance negotiations with payers. Pediatric and combination-therapy white spaces remain underexploited, positioning agile biotechs for substantial upside if safety hurdles are cleared.

Cushing's Syndrome Diagnostics And Therapeutics Industry Leaders

Corcept Therapeutics Inc.

Perrigo Co. Plc

Recordati S.p.A

Xeris Biopharma Holdings Inc.

Crinetics Pharmaceuticals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Corcept Therapeutics released CATALYST data showing a 1.47% HbA1c decline with Korlym versus 0.15% for placebo, and a 24% hypercortisolism prevalence in refractory diabetes cohorts.

- April 2025: FDA broadened ISTURISA’s label to all endogenous hypercortisolemia forms, enlarging Recordati’s target pool.

- March 2025: Relacorilant NDA accepted with a December 2025 action date after trials showed improvements in blood pressure and glucose homeostasis.

- March 2025: Ubie and the Cushing’s Support and Research Foundation launched an AI-driven symptom checker aimed at cutting diagnostic lag times.

- February 2025: Corcept posted record Korlym revenue, adding new prescribers while funding multi-indication trials.

- January 2025: Crinetics reported positive atumelnant Phase 2 results in congenital adrenal hyperplasia, underscoring spill-over potential for Cushing-related ACTH disorders.

Global Cushing's Syndrome Diagnostics And Therapeutics Market Report Scope

As per the scope of the report, Cushing's syndrome occurs when the body produces an excessive amount of the hormone cortisol over a prolonged period. Some of the symptoms that arise in CS patients are a fatty hump between the shoulders, a rounded face, and pink or purple stretch marks on the skin.

The Cushing's syndrome diagnostics and therapeutics market is segmented into treatment type, diagnosis, distribution channel, and geography. By treatment type, the market is segmented into surgery, radiation therapy, and drugs. By diagnostic tests, the market is segmented into petrosal sinus sampling, saliva tests, urine and blood tests, and imaging tests. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across significant global regions. The report offers the value (USD) for the above segments.

| Surgery | Trans-Sphenoidal Surgery |

| Adrenalectomy | |

| Radiation Therapy | |

| Drugs | Pituitary-Directed Drugs |

| Adrenal Steroidogenesis Inhibitors | |

| Glucocorticoid-Receptor Antagonists |

| Inferior Petrosal Sinus Sampling | |

| Late-Night Saliva Cortisol Test | |

| 24-Hr Urine & Blood Cortisol Tests | |

| Imaging Tests | MRI |

| CT | |

| PET/CT | |

| Emerging Assays (Hair Cortisol, LC-MS/MS Panels) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Surgery | Trans-Sphenoidal Surgery |

| Adrenalectomy | ||

| Radiation Therapy | ||

| Drugs | Pituitary-Directed Drugs | |

| Adrenal Steroidogenesis Inhibitors | ||

| Glucocorticoid-Receptor Antagonists | ||

| By Diagnostic Tests | Inferior Petrosal Sinus Sampling | |

| Late-Night Saliva Cortisol Test | ||

| 24-Hr Urine & Blood Cortisol Tests | ||

| Imaging Tests | MRI | |

| CT | ||

| PET/CT | ||

| Emerging Assays (Hair Cortisol, LC-MS/MS Panels) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the Cushing's syndrome diagnostics and therapeutics market growing through 2031?

The market's value is expected to climb from USD 418.21 million in 2026 to USD 648.79 million by 2031, representing a 9.18% CAGR.

Which treatment category currently commands the largest revenue?

Drug therapy holds 52.01% of 2025 revenue, reflecting chronic disease management and an expanding portfolio of selective cortisol modulators.

What diagnostic innovations are making the biggest impact?

Hair-strand cortisol assays and point-of-care LC-MS/MS panels are gaining ground thanks to faster turnaround times and 90% diagnostic accuracy levels.

Which region offers the quickest revenue upside for new entrants?

Asia-Pacific, growing at an anticipated 10.11% CAGR, pairs expanding insurance cover with growing diagnostic capacity, making it the most dynamic regional opportunity.

What is the main hurdle for therapy adoption in emerging markets?

High drug prices and limited reimbursement infrastructure pose the largest access barriers, dampening uptake despite increased disease recognition.

Page last updated on: