Curing Agent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

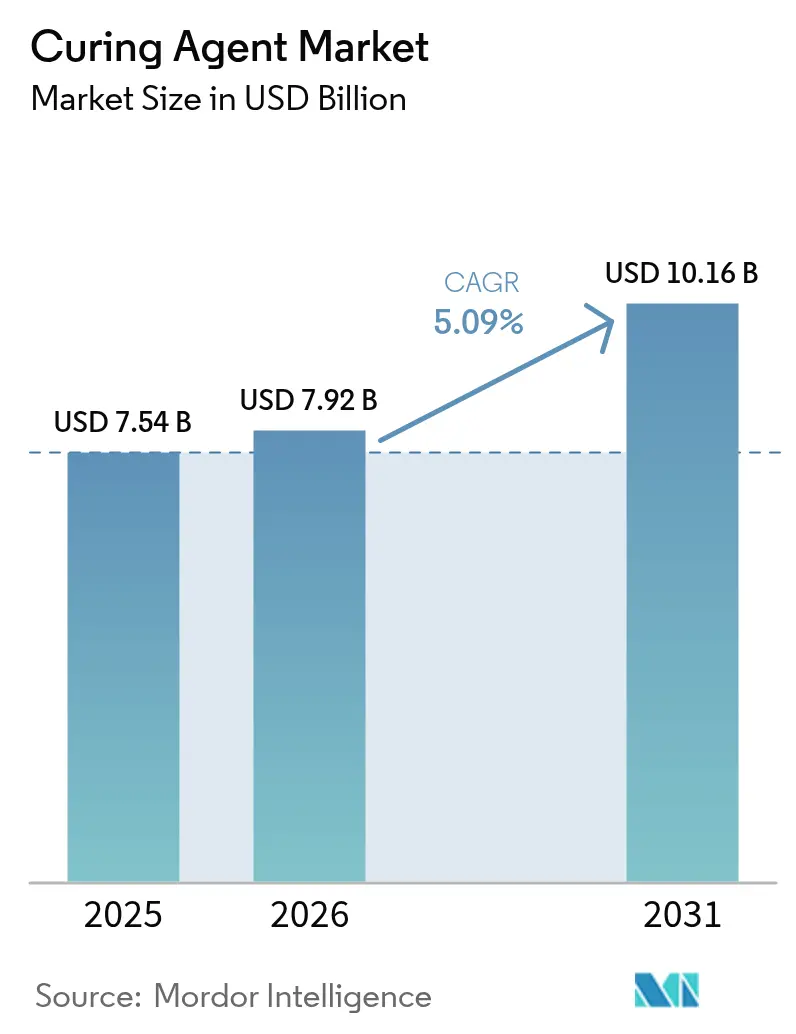

| Market Size (2026) | USD 7.92 Billion |

| Market Size (2031) | USD 10.16 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Curing Agent Market Analysis by Mordor Intelligence

The curing agent market size is expected to grow from USD 7.54 billion in 2025 to USD 7.92 billion in 2026 and is forecast to reach USD 10.16 billion by 2031 at 5.09% CAGR over 2026-2031. Robust construction spending, wind-energy buildouts, and a decisive pivot toward bio-based chemistries keep demand resilient even as regulatory barriers tighten. Manufacturers benefit from expanding infrastructure budgets, electrification of transport, and the need for durable, low-VOC coating systems that meet global environmental mandates. Wind-turbine blade production, battery potting, and 3D-printing resins provide high-value outlets, while supply-chain integration in Asia Pacific continues to influence raw-material availability and pricing. Competitive pressure centers on faster cure cycles, lower emissions, and life-cycle recyclability, pushing incumbents to accelerate research and devlopment and scale up renewable feedstocks to defend margins in the curing agent market.

Key Report Takeaways

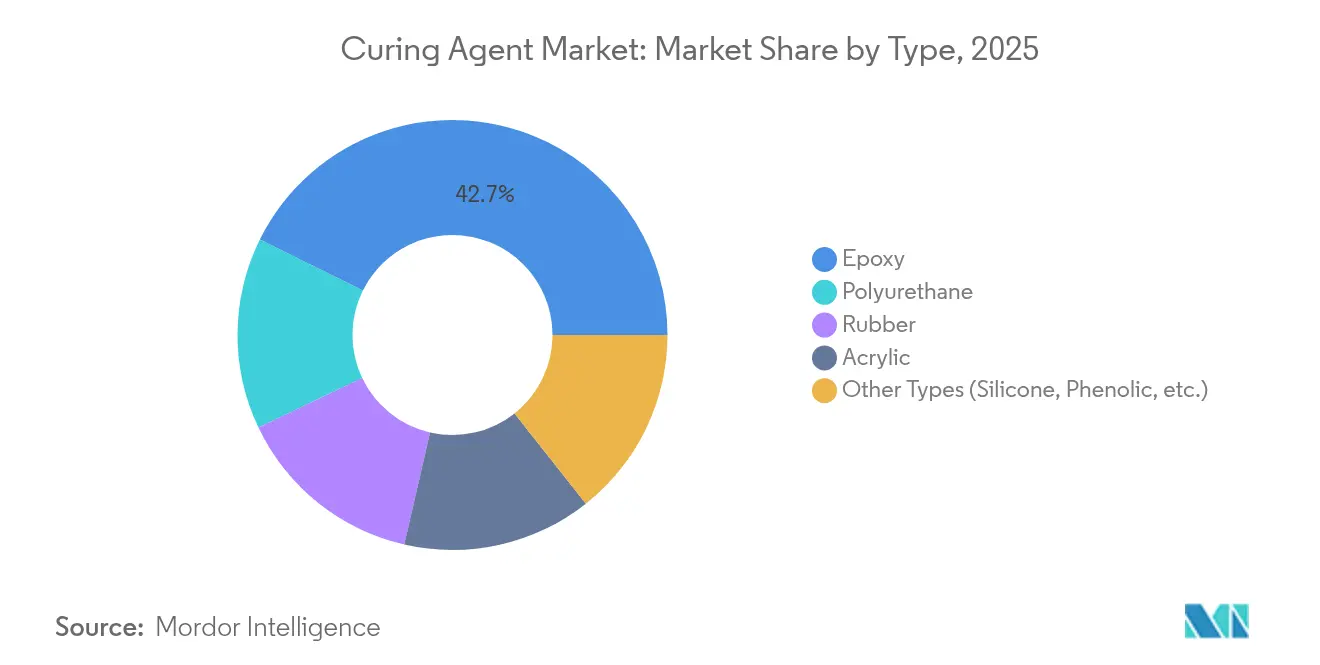

- By type, epoxy curing agents captured 42.68% of the curing agent market share in 2025 and are expanding at a 6.29% CAGR to 2031.

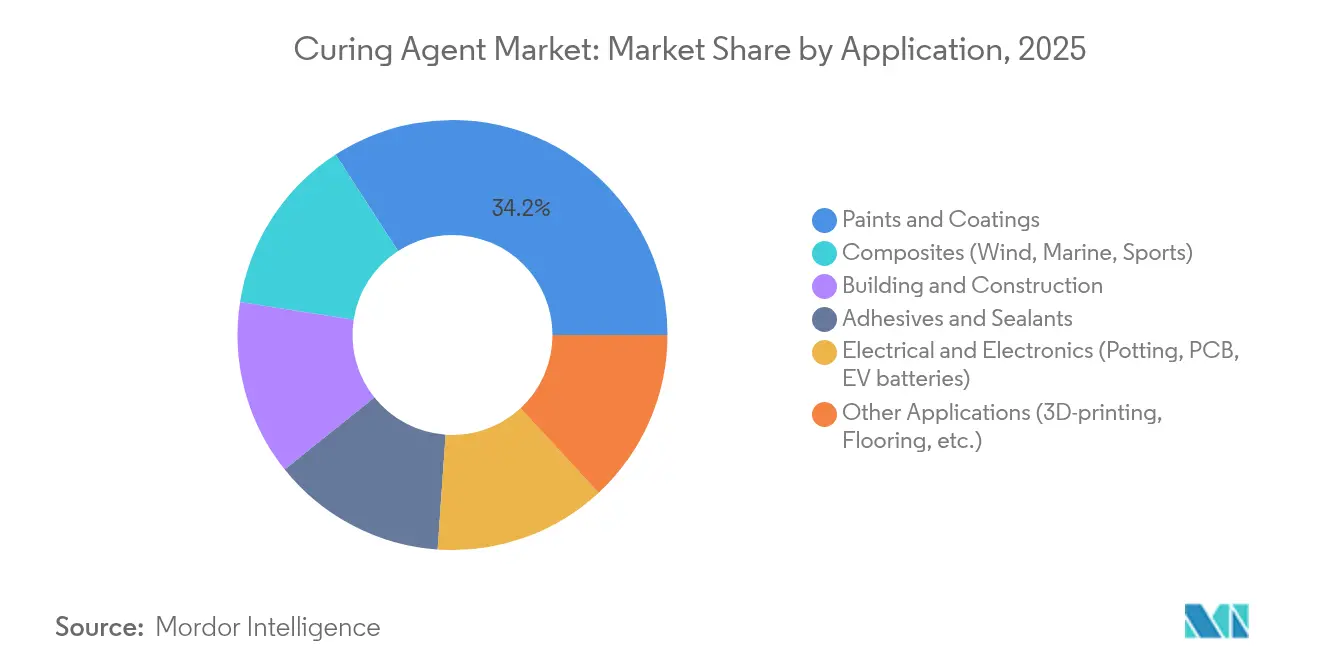

- By application, paints and coatings led with 34.15% of the curing agent market size in 2025, while composites are projected to post the highest 6.12% CAGR through 2031.

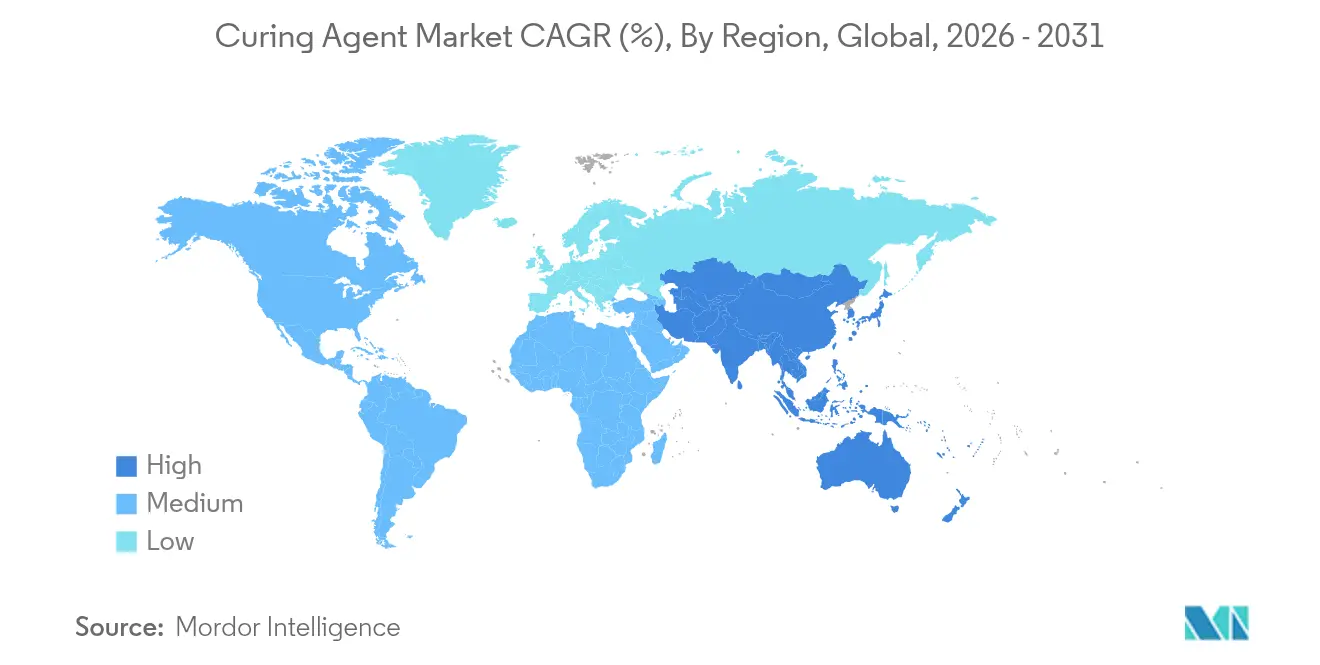

- By geography, Asia Pacific accounted for 44.75% revenue share of the curing agent market in 2025 and is advancing at a 6.46% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Curing Agent Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from paints and coatings | +1.2% | Global, APAC leading growth | Medium term (2-4 years) |

| Infrastructure boom driving building and construction composites | +1.4% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Rapid expansion of wind-energy blade production | +0.9% | Global, concentrated in China, Europe, and North America | Medium term (2-4 years) |

| Shift to bio-based CNSL and lignin curing chemistries | +0.7% | North America and EU leading, APAC following | Long term (≥ 4 years) |

| Ultra-fast curing agents enabling 3D-printing resins | +0.5% | North America and EU innovation hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Paints and Coatings

Low-VOC and waterborne coatings now dominate procurement specifications for architectural and protective layers, prompting formulators to specify curing agents that deliver hardness, UV resistance, and corrosion protection without breaching emission caps. New waterborne polyamide chemistries like EPIKURE 6874-WZ-50 simplify dispersion stability while maintaining salt-spray performance[1]Westlake Corporation, “Westlake Epoxy Introduces EpoVIVE™ Waterborne Portfolio,” westlakelive.com. Infrastructure refurbishment raises volumes for anti-corrosion primers, and IoT-enabled surface diagnostics accelerate renovation cycles, driving additional throughput. Growing consumer awareness of sustainability pushes resin producers to leverage bio-based hardeners that match mechanical performance. These factors continue to lift demand across the global curing agent market.

Infrastructure Boom Driving Building and Construction Composites

Government-backed megaprojects in Asia Pacific favor fiber-reinforced polymers for bridge decks, façades, and rebar, as these materials reduce installation labor and mitigate corrosion costs. In the United States, bipartisan infrastructure funding has opened grants for composite girder replacement, increasing purchase orders for reactive amine systems optimized for high-humidity cure schedules. India’s push for USD 300 billion chemical output by 2025 strengthens the domestic supply of specialty amines and accelerators, reinforcing regional self-sufficiency. Rapid urbanization sustains consumption of structural adhesives, further lifting the curing agent market.

Rapid Expansion of Wind-Energy Blade Production

Global onshore and offshore wind capacity additions are raising blade lengths beyond 100 meters, necessitating curing agents that extend pot-life yet develop green strength fast enough for takt-time targets. Huntsman’s polyetheramines permit room-temperature infusion cycles of 90 minutes for 120-meter molds, shortening fabrication bottlenecks. Dow’s polyurethane-carbon fiber spar cap system achieves more than 90% conversion in minutes while hiking modulus, illustrating premium niches inside the curing agent market. Digital twins optimize exotherm profiles, helping blade makers reduce scrap and resin waste. As wind installations accelerate, turbine manufacturers lock in long-term supply contracts, anchoring multi-year volume visibility for curing agent suppliers.

Ultra-Fast Curing Agents Enabling 3D-Printing Resins

Additive manufacturing demands snap-cure photoinitiators to sustain high print throughput and fine resolution. Lawrence Livermore National Laboratory validated microwave volumetric AM that cures centimeter-thick epoxy composites within seconds, lifting productivity for aerospace tooling[2]Lawrence Livermore National Laboratory, “Microwave Volumetric Additive Manufacturing Breakthrough,” llnl.gov. Titania quantum-dot catalysts widen the usable spectrum for outdoor-stable photopolymer resins. Renewable lipoate-based systems enable closed-loop recyclability, addressing sustainability checkpoints in the curing agent market. Collectively, ultra-fast solutions expand resin vendor margins and shorten prototyping cycles, enhancing market pull for specialty hardeners.

Restraints Impact Analysis of Curing Agent Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and REACH regulations on amines and anhydrides | -0.8% | EU primary impact, global compliance ripple effects | Medium term (2-4 years) |

| Volatility in petro-derived raw-material costs | -0.6% | Global, APAC manufacturing is most exposed | Short term (≤ 2 years) |

| Supply chain concentration of specialty amines in Asia | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and REACH Regulations on Amines and Anhydrides

Europe’s 2025 REACH revision extends PFAS curbs and lowers emission thresholds, compelling formulators to redesign epoxy and polyurethane systems around safer accelerators. Diisocyanate training mandates add indirect cost, and the January 2025 SVHC update tightens documentation for amine derivatives. Similar moves by the U.S. EPA on NMP heighten complexity for coatings exporters. Downstream, automotive OEMs now screen full material disclosures, elevating switching pressure toward bio-based or ultra-low-odor alternatives. Compliance expenses weigh on smaller producers, but integrated majors with green portfolios gradually consolidate share inside the curing agent market.

Volatility in Petro-Derived Raw-Material Costs

Cracker shutdowns across Southeast Asia in 2024 underscored susceptibility to naphtha price swings, shocking spot values for ethyleneamines and phthalic anhydride. Political tensions and freight rate increases exacerbate landed-cost variability, urging procurement teams to lock multi-year index-linked contracts or develop dual sourcing. Some multinationals respond with backward integration into propylene derivatives, while others fast-track bio-route pilots to sidestep crude exposure. The unpredictability compresses margins, yet it also accelerates innovation in renewable feedstocks, adding impetus to structural change in the curing agent market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Curing Agent Market Segment Analysis

By Type:

Epoxy Dominance Accelerates Through InnovationEpoxy systems generated the largest revenue within the curing agent market in 2025, and their 6.29% CAGR through 2031 outpaces every other chemistry category. Within this segment, aliphatic amine blends enable thin-film cure at temperatures below 10 °C, while polyamides contribute moisture tolerance for marine primers. Huntsman, BASF, and Evonik combine backward-integrated amine chains with regional mixing plants, sustaining their cost edge and technical support.

Polyurethane hardeners continue to hold strong positions in flexible flooring and spray foams, yet isocyanate regulation encourages hybrid epoxy-polyurethane routes with blocked functionality that releases under heat. Silicone and phenolic curing agents remain indispensable for aerospace and high-temperature electronics, where dielectric stability is critical. Rubber and acrylic formulations address niche sealing, tire, and UV-cure needs, contributing steady but slower growth.

By Application:

Composites Growth Outpaces Traditional SegmentsComposites are forecast to expand at 6.12% through 2031. The steep trajectory reflects surging wind-turbine blade needs, electrified vehicle platforms, and lightweight urban mobility structures. Longer blades necessitate resin systems that remain in workable form for 4 hours while curing overnight at 60 °C, stimulating demand for innovative amine adducts. Battery potting applications require thermally conductive yet electrically insulating epoxies that dissipate heat spikes without compromising dielectric properties. At the same time, paints and coatings keep their top spot in revenue terms, driven by monumental upkeep cycles in infrastructure, maritime shipping decarbonization, and universal incentives for low-solvent architectural finishes.

Electrical and electronics usage rises on the back of 5G rollouts and high-density semiconductor packaging that demands filler-rich, low-CTE epoxy encapsulants. 3D-printing resins, though currently a small slice, post a significant volume growth thanks to digital spare-part programs and on-site construction trials. Collectively, these diverse outlets balance cyclical swings and broaden the demand base for the curing agent market.

Geography Analysis

APAC Curing Agent Market

Asia Pacific dominates on both volume and value, holding 44.75% of global sales in 2025 and riding a 6.46% CAGR to 2031. Regional supply chains feature integrated amine synthesis, competitive labor, and proximity to downstream users, giving local producers agility in pricing and lead time. China’s Made-in-China 2025 initiative upgrades domestic output from commodity epoxy diluents toward specialty crosslinkers, supporting local turbine and semiconductor customers simultaneously. India’s production-linked incentive framework attracts multinational capital into polyetheramine and phenalkamine facilities, cutting import dependency and propelling the curing agent market in South Asia.

North America and Europe Curing Agent Market

North America benefits from shale gas feedstock and high wind-capacity additions, yet stricter VOC proposals and PFAS scrutiny raise research and development outlays. Leading formulators move toward mass-balance bio-attribution models and circular end-of-life options to maintain differentiation and secure grants. Europe confronts elevated electricity prices and evolving REACH thresholds, compelling operators to migrate toward high-margin custom solutions while scaling green hydrogen-powered plants to lower Scope 2 emissions.

Competitive Landscape

The curing agent market remains moderately fragmented. BASF secures scale advantages from backward-integrated isophorone diamine and has formalized an exclusive North American Baxxodur distribution deal with Univar, enhancing customer reach. Smaller innovators scale cardanol refining and lignin amination, partnering with turbine OEMs and EV start-ups to validate performance.

Curing Agent Industry Leaders

Evonik Industries, AG

BASF

Hexion Inc.

Huntsman International LLC

Mitsubishi Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Curing Agent Market Companies Covered in this Report

- Alfa Chemicals

- Atul Ltd.

- BASF

- Cardolite Corporation

- DIC Corporation

- Evonik Industries, AG

- Hexion Inc.

- Huntsman International LLC

- Incorez Ltd.

- Kukdo Chemical Co.

- Mitsubishi Chemical Corporation

- Olin Corporation

- Palmer International

- Supreme Polytech Pvt Ltd.

- Wanhua Chemical Group

Recent Industry Developments in Curing Agent Market

- November 2024: Evonik Industries, AG broke ground on a specialty amines expansion in Nanjing, deepening its commitment to epoxy and polyurethane curing systems.

- September 2024: Evonik Industries, AG introduced Ancamide 2853 and 2865 polyamide-based curing agents for the Americas, broadening sustainable options for coating formulators.

Curing Agent Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the curing agent market as the global sales value of chemical hardeners, principally amine, polyamide, anhydride, polyurethane, rubber, acrylic, and select bio-based chemistries, used to cross-link resins across paints and coatings, construction compounds, adhesives and sealants, composites, and electrical and electronics. According to Mordor Intelligence analysts, the scope captures only new commercial-grade agents supplied in bulk or formulated blends; recycled or reclaim streams are outside the estimate.

Scope exclusion: products marketed solely as curing accelerators or thinners without reactive functionality are not covered.

Segments Covered in This Report

- By Type

- Epoxy

- Polyurethane

- Rubber

- Acrylic

- Other Types (Silicone, Phenolic, etc.)

- By Application

- Paints and Coatings

- Building and Construction

- Adhesives and Sealants

- Composites (Wind, Marine, Sports)

- Electrical and Electronics (Potting, PCB, EV batteries)

- Other Applications (3D-printing, Flooring, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed raw-material producers, regional distributors, coating formulators, and composite fabricators across Asia-Pacific, North America, and Europe. Conversations probed average selling prices, cure-speed preferences, wind-blade resin uptakes, and the shift toward low-VOC chemistries, allowing us to reconcile secondary cues, refine penetration ratios, and test early model outputs.

Desk Research

We compiled baseline demand indicators from open sources such as United States International Trade Commission import codes, Eurostat PRODCOM output, China Customs HS-2916 lines, industry association whitepapers from ACA and JEC Composites, patent filings from Questel, and listed company 10-K disclosures. Additional volume, price, and end-use split clues were extracted from D&B Hoovers screened supplier financials and Dow Jones Factiva news archives. These sources provide shipment trends, typical unit prices, and capacity additions that ground the initial data grid; however, they are illustrative and not exhaustive, as many other public records supported our assessment.

Market-Sizing & Forecasting

We apply a top-down construct in which global epoxy, polyurethane, and other resin consumption volumes are reconstructed from production and trade data, then multiplied by validated curing-agent-to-resin dosage factors. Select bottom-up checks, supplier revenue roll-ups, and channel ASP times sample volume are run to sense-check totals. Key variables include regional infrastructure spending, wind-turbine blade installations, coatings output indices, average dosage rates, and agent ASP progression. A multivariate regression combined with scenario analysis projects these drivers forward to 2030; gaps for niche uses are bridged through expert consensus ranges.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst critique, and senior sign-off. We revisit models annually, triggering interim refreshes for material capacity additions, regulatory shifts, or price shocks, ensuring clients receive the latest vetted view before report delivery.

How Mordor Intelligence's Curing Agent Market Size Compares to Other Published Estimates

Published estimates often differ because firms select dissimilar product baskets, conversion ratios, and refresh cadences.

Key gap drivers arise when other publishers (i) limit inclusion to epoxy agents only, (ii) anchor models on earlier base years without mid-cycle price resets, or (iii) assume single uniform ASPs across regions, whereas our team factors Asia-Pacific discounting, specialty bio-based premiums, and quarterly FX updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.54 B (2025) | Mordor Intelligence | - |

| USD 7.02 B (2024) | Global Consultancy A | excludes polyurethane and rubber agents; earlier base year, biennial updates |

| USD 6.30 B (2024) | Industry Association B | relies on single global ASP assumption, limited primary validation |

| USD 5.90 B (2023) | Trade Journal C | narrower end-use capture and no currency normalization to 2025 USD |

These comparisons show that, by selecting the full reactive agent set, refreshing data annually, and cross-checking with end-user interviews, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to clear drivers and repeatable steps.

Key Questions Answered in the Report

What is the current size of the curing agent market?

The curing agent market stands at USD 7.92 billion in 2026 and is projected to reach USD 10.16 billion by 2031.

Which curing agent type holds the largest share?

Epoxy curing agents lead with 42.68% of curing agent market share in 2025, growing at a 6.29% CAGR through 2031.

Why is Asia Pacific pivotal for curing agent suppliers?

Asia Pacific commands 44.75% of global revenue thanks to integrated supply chains, lower production costs, and expanding construction and wind-energy sectors.

How are regulations influencing product development?

Stricter VOC and REACH rules push manufacturers toward bio-based, low-odor chemistries and accelerate research and development for PFAS-free and low-hazard accelerators, reshaping portfolios.

Which application segment is growing fastest?

Composites applications, especially wind-turbine blades and lightweight automotive parts, register the highest 6.12% CAGR through 2031.

Page last updated on: