Antiknock Agents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

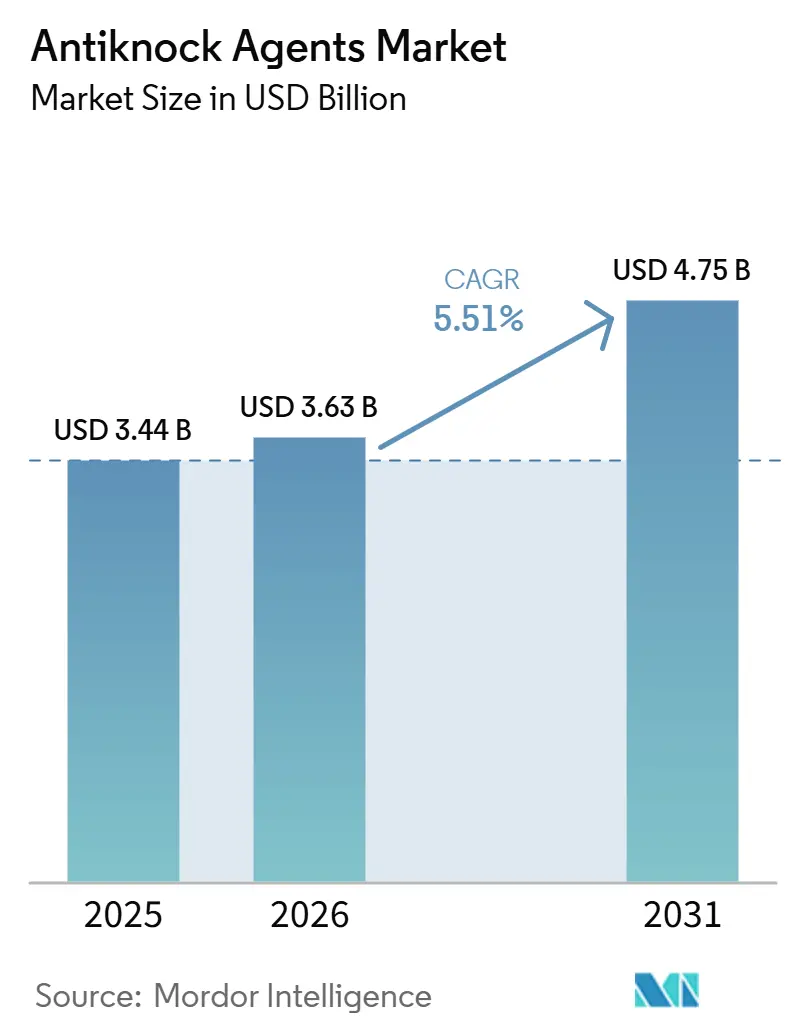

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 4.75 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antiknock Agents Market Analysis by Mordor Intelligence

The Antiknock Agents Market size is expected to increase from USD 3.44 billion in 2025 to USD 3.63 billion in 2026 and reach USD 4.75 billion by 2031, growing at a CAGR of 5.51% over 2026-2031. Turbocharged gasoline direct-injection engines, relaxed aromatic ceilings in Southeast Asia, and the European Union's Renewable Energy Directive III are collectively driving the adoption of premium-grade oxygenate blending. Automakers are increasing octane specifications beyond 95 Research Octane Number (RON) to mitigate the risk of low-speed pre-ignition. This trend is encouraging refiners to prioritize Methyl Tertiary-Butyl Ether (MTBE), Ethyl Tertiary-Butyl Ether (ETBE), and ethanol over benzene-based aromatics. Simultaneously, pilot projects for synthetic fuels (e-fuels) in Germany, Japan, and Chile are creating opportunities for drop-in boosters. These boosters enhance RON levels without disrupting paraffinic synthetic gasoline streams. In the Asia-Pacific region, refinery upgrades and flexible fuel standards are supporting the demand for toluene and MTBE. Additionally, the European Union's 29% renewable transport fuel mandate is directing investments toward bio-ETBE production units, which provide double credit toward compliance targets. While North America and Europe anticipate a reduction in total gasoline volumes due to the increasing adoption of battery-electric vehicles, premium-grade gasoline consumption is expected to grow. This growth is attributed to the requirements of turbo-hybrid powertrains, which necessitate an octane rating of 93 RON or higher.

Key Report Takeaways

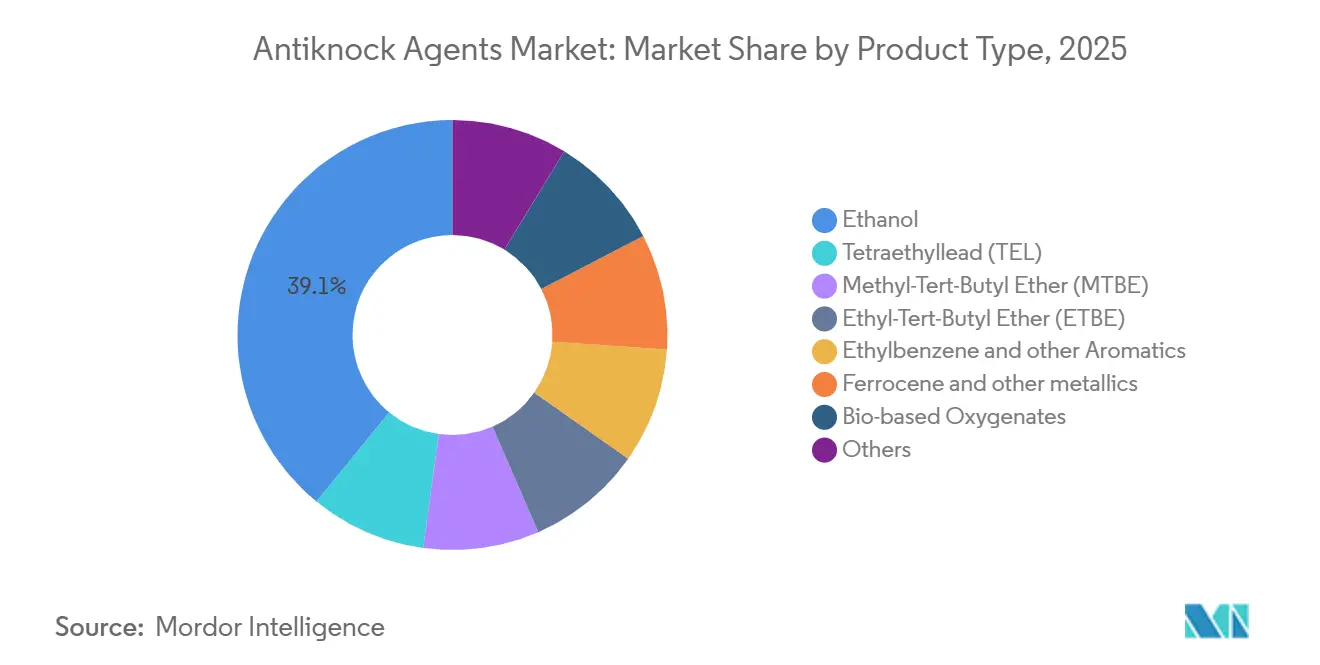

- By product type, ethanol held 39.11% of the antiknock agents market share in 2025, while bio-based oxygenates are set to advance at a 6.17% CAGR through 2031.

- By form, liquid formulations captured 62.14% of the anti-knock agents market share in 2025 and will rise at 5.88% CAGR to 2031.

- By distribution channel, bulk terminal injection led with 44.78% revenue share in 2025; the retail aftermarket is projected to expand at a 6.12% CAGR to 2031.

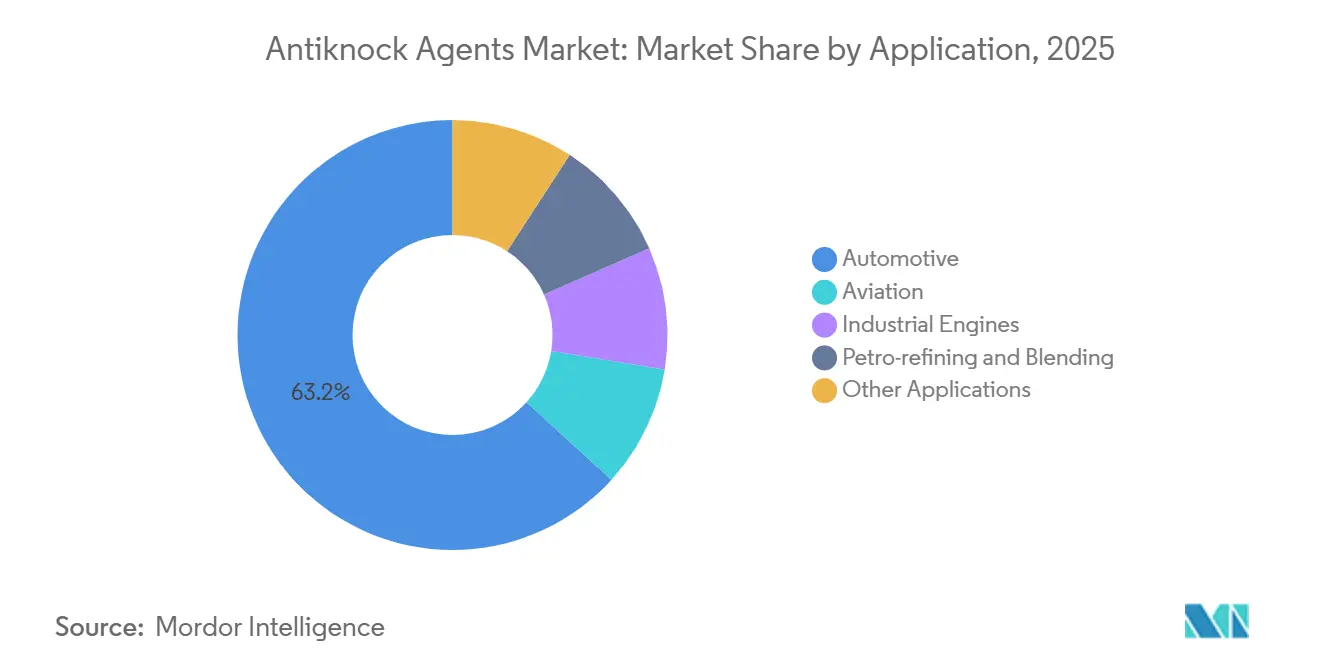

- By application, automotive accounted for 63.24% of the antiknock agents market size in 2025, while petro-refining and blending are advancing at a 5.93% CAGR through 2031.

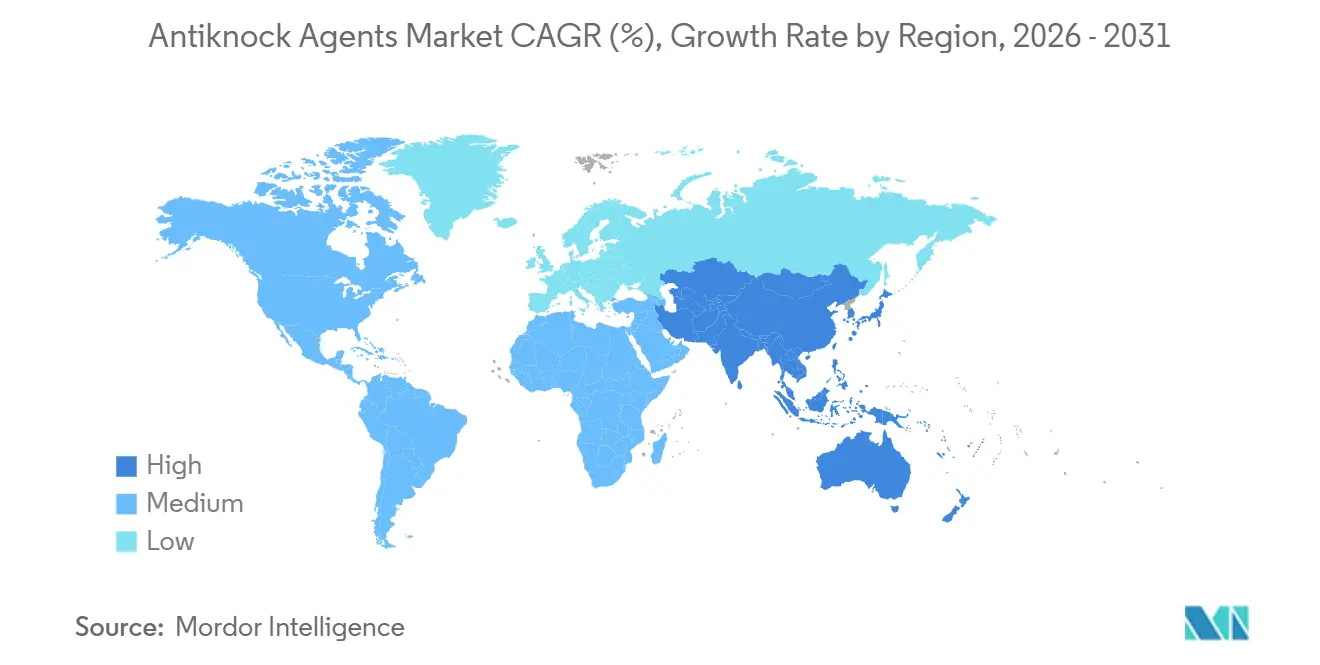

- By geography, Asia-Pacific commanded 46.11% of the antiknock agents market size in 2025 and is projected to grow at 6.28% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antiknock Agents Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Turbocharged downsizing requiring higher octane fuels | +1.2% | EU, China, India, United States | Medium term (2-4 years) |

| Rapid motorization in Southeast Asia with lax aromatic limits | +1.4% | Indonesia, Vietnam, Thailand, Malaysia | Short term (≤ 2 years) |

| Bio-MTBE and bio-ETBE adoption to meet EU renewable targets | +0.9% | EU-27, led by France, Germany, Netherlands | Long term (≥ 4 years) |

| E-fuel pilot projects creating drop-in octane demand | +0.6% | Germany, Japan, Chile, Saudi Arabia | Long term (≥ 4 years) |

| SAF off-gas integration enabling co-produced bio-ethers | +0.4% | United States, Finland, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Turbocharged Downsizing Requiring Higher Octane Fuels

With compression ratios of 11:1 or higher, 1.2 to 2.0 liter turbocharged engines operate near the limits of 91 Research Octane Number (RON) fuel. In 2025, 14 Original Equipment Manufacturers (OEMs) adopted the TOP TIER standard, mandating five times the Environmental Protection Agency's (EPA) detergent baseline to address injector deposits and low-speed pre-ignition[1]TOP TIER, “Fuel Standard and Requirements,” TOPTIERGAS.COM. Research from Argonne National Laboratory indicates that increasing ethanol content from E10 to E15 reduces particulate number emissions by 18%. However, RON improvements plateau beyond E20 due to charge-cooling effects on flame speed. Consequently, premium fuel blenders are incorporating 10–12 volume percent (vol%) Ethyl Tertiary Butyl Ether (ETBE) into E10, achieving 95+ RON while adhering to the 7 pounds per square inch (psi) Reid vapor-pressure limit.

Rapid Motorization in Southeast Asia With Lax Aromatic Limits

Indonesia's Euro 4-equivalent regulations permit 45% aromatics and 1.5% benzene. This regulatory framework enables Pertamina to efficiently supply reformate-rich 92 RON gasoline. In 2025, gasoline consumption in Vietnam increased by 8.2%. However, with its refineries lacking Fluid Catalytic Cracking (FCC) upgrades, importers rely on aromatic naphtha from Korea and Singapore. While E20 has been introduced in Thailand, it accounts for only 12% of retail sales due to concerns about reduced mileage. Conversely, luxury hybrids require 95 RON or higher, creating a premium market for Methyl Tertiary Butyl Ether (MTBE) and ethanol.

Bio-MTBE and Bio-ETBE Adoption to Meet EU Renewable Targets

Under Renewable Energy Directive III (RED III), the transport renewable quota is set to increase to 29% by 2030, with advanced bio-ETBE receiving double credit[2]European Commission, “Renewable Energy Directive – Targets and Rules,” ENERGY.EC.EUROPA.EU. France is already blending 6.8 vol% bio-ETBE, enabling refiners to meet mandates without additional investments in Hydrotreated Vegetable Oil (HVO). Evonik has developed a zeolite-based process that converts waste ethanol into isobutylene with 82% selectivity, reducing dependence on fossil C4 streams.

E-Fuel Pilot Projects Creating Drop-In Octane Demand

Porsche's Haru Oni pilot project is converting e-methanol into gasoline, which requires the addition of 8-10 vol% ETBE to achieve 95 RON. Meanwhile, Japan's New Energy and Industrial Technology Development Organization (NEDO) consortium is enhancing Fischer-Tropsch synthetic naphtha from 78 to 93 RON using Innospec's non-metallic additive package. Saudi Aramco's upcoming 50,000 barrels per day (kbpd) e-fuel plant plans to implement on-site alkylation instead of relying on imported oxygenates, ensuring alignment with its petrochemical integration strategy.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethanol price volatility and US blend-wall constraints | -0.7% | United States, Brazil, EU importers | Short term (≤ 2 years) |

| Electric vehicle penetration eroding gasoline demand base | -1.1% | China, EU, California, Norway | Medium term (2-4 years) |

| Next-gen engine controls reducing octane requirement | -0.6% | Global, concentrated in premium OEM segments (Germany, Japan, US) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ethanol Price Volatility and US Blend-Wall Constraints

In January 2025, corn-ethanol prices increased from USD 1.85 per gallon to USD 2.62 by August, driven by a 14% yield reduction due to Midwestern droughts. Although the Environmental Protection Agency (EPA) approved year-round E15 at 3,800 stations, the E10 blend wall continues to limit additional demand. Rotterdam import prices rose to EUR 720 (USD 0.47) per m³ as Brazil redirected ethanol to domestic hydrous use.

Electric Vehicle Penetration Eroding Gasoline Demand

In 2025, battery electric vehicle (BEV) sales reached 18.2 million, reducing gasoline demand by 420 thousand barrels per day (kbpd), with China accounting for 60% of this decline. In Norway, gasoline demand decreased by 11%, leading to service station closures and a shift toward premium-only offerings. California's Advanced Clean Cars II regulation is expected to further reduce gasoline demand, with a projected annual decline of 2.8% through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Oxygenates Break Out Behind Ethanol’s Lead

Ethanol accounted for 39.11% of the antiknock agents market share in 2025, driven by Brazil's E27–E30 policy and the United States Renewable Fuel Standard, which supported demand. However, bio-based oxygenates are projected to experience the fastest growth in the antiknock agents market, with a CAGR of 6.17% through 2031. This growth is attributed to the Renewable Energy Directive III (RED III) double-counting of bio-ethyl tertiary-butyl ether (bio-ETBE) and the integration of sustainable aviation fuel (SAF) off-gas, which provides cost-effective isobutylene.

By Form: Liquids Dominate, Additive Packages Gain Appeal

Liquid formulations accounted for 62.14% of the antiknock agents market share in 2025 and are projected to grow at a CAGR of 5.88%. This growth is attributed to their compatibility with pipelines and the convenience they offer in terminal dosing processes. Additionally, Chevron's inline analyzers contributed to operational efficiency by reducing octane giveaway by 0.4 points, which resulted in cost savings of USD 3.2 million in oxygenate expenses. These factors highlight the significant role of liquid formulations in the antiknock agents market.

By Distribution Channel: Bulk Injection Steady, Aftermarket Accelerates

Bulk-terminal blending accounted for 44.78% of the projected 2025 revenue, primarily due to its effectiveness in ensuring regulatory traceability for Renewable Fuel Standard (RFS) credit generation. This method is widely adopted for its ability to meet compliance requirements efficiently and maintain consistency in fuel quality.

The retail aftermarket segment is the fastest-growing, with a compound annual growth rate (CAGR) of 6.12%. This growth is driven by increasing consumer demand for ferrocene-based fuel additives, which are readily available through online platforms. Companies like Lucas Oil have contributed to this growth by reformulating their products, replacing manganese with ferrocene, which led to an 18% increase in 2025 sales.

By Application: Automotive Large, Petro-Refining Fastest

The automotive sector accounted for 63.24% of the projected 2025 volume. This significant share highlights the continued reliance on automotive applications for gasoline consumption. On the other hand, the petro-refining and blending segment is the fastest-growing application, with a CAGR of 5.93%. This growth is driven by the adoption of inline octane systems, which allow refiners to adjust gasoline properties as needed. Sinopec's Zhenhai alkylation startup has contributed to this growth by increasing the 95 Research Octane Number (RON) pool yield. This development aligns with the implementation of China VII regulations, which restrict aromatics to 35%.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.11% of the antiknock agents market revenue and is projected to grow at a CAGR of 6.28% through 2031. China's 300 million-vehicle fleet, along with its transition to 95 Research Octane Number (RON), is driving Methyl Tertiary Butyl Ether (MTBE) demand. In India, the implementation of Bharat Stage VII is leading to upgrades in Fluid Catalytic Cracking (FCC) catalysts, with BASF's Fourtiva supporting aromatic control. Japan's hybrid vehicles, requiring a 100 RON premium, have contributed to a 6% increase in high-octane sales, despite a decline in overall gasoline consumption.

North America's antiknock agents market is experiencing stable volumes but an increase in octane intensity. The region's year-round E15 adoption and Canada's Clean Fuel Regulations are supporting the use of ethanol and bio-MTBE. In Mexico, reduced tariff barriers have facilitated higher MTBE imports. While electric vehicle penetration is reducing U.S. gasoline consumption by 1.1% annually, the growth of turbo-hybrids is maintaining strong demand for premium-grade fuels.

Europe is progressing due to renewable mandates. France has increased its bio-MTBE usage to 6.8 vol%, while Germany is targeting a 12-15% blend for carbon dioxide (CO₂) compliance. The United Kingdom's E10 baseline still allows for a 97+ RON premium, which grew by 9% in 2025. Norway, with a 92% share of battery electric vehicles (BEVs), has reduced gasoline consumption by 11%, indicating a future shift in antiknock agents market demand toward premium segments.

Competitive Landscape

The antiknock agents market is moderately concentrated. BASF’s Keropur TOP TIER+ addresses detergent, octane, and warranty protection requirements. Innospec’s manganese-free Octaburn suite complies with China VI metal restrictions. LyondellBasell has increased its Channelview methyl tert-butyl ether (MTBE) production to 620 kilotons per year (kt/y), supporting exports from the Gulf Coast to Latin America. Evonik and Braskem are advancing bio-isobutylene pathways that secure Renewable Energy Directive III (RED III) double credits and address fossil C4 shortages.

Strategic initiatives include Chevron Oronite’s planned 2024 launch of gasoline additive platforms tailored for e-fuel blends. TotalEnergies is upgrading its Gonfreville facility to produce an additional 150 kt/y of bio-ethyl tert-butyl ether (bio-ETBE), and Phillips 66 is collaborating with Chevron Richmond on an off-gas MTBE connection. The focus on technology is shifting toward inline analyzers and artificial intelligence (AI)-driven blending controls. These advancements have reduced octane giveaways to below 0.2 at refineries such as Marathon Galveston Bay, resulting in annual savings of USD 4.8 million.

Antiknock Agents Industry Leaders

Innospec

Chevron Oronite Company LLC

Afton Chemical

BASF

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: BASF introduced Keropur TOP TIER+ detergent-octane concentrate, which increases Research Octane Number (RON) by 1.5. This product, linked to the Antiknock Agents market, enabled the company to secure a 12% share of the U.S. market within six months.

- August 2024: Indian Oil Panipat contracted BASF to introduce its Fourtiva Fluid Catalytic Cracking (FCC) catalyst to enhance octane levels, aligning with Bharat Stage VII standards. This development is linked to the use of antiknock agents in improving fuel quality.

Global Antiknock Agents Market Report Scope

Antiknock agents, chemical compounds added to gasoline, increase its octane rating. This prevents premature ignition, also known as engine knocking, and enhances fuel efficiency in high-compression engines. By allowing gasoline to withstand higher temperatures and pressures before ignition, these additives reduce engine wear and minimize pinging sounds.

The antiknock agents market is segmented by product type, form, distribution channel, application, and geography. By product type, the market is segmented into ethanol, tetraethyllead (tel), methyl-tert-butyl ether (mtbe), ethyl-tert-butyl ether (etbe), ethylbenzene and other aromatics, ferrocene and other metallics, bio-based oxygenates, and others. By form, the market is segmented into liquid, solid, and additive packages/concentrates. By distribution channel, the market is segmented into bulk terminal injection, OEM supply, and retail aftermarket. By application, the market is segmented into automotive, aviation, industrial engines, petro-refining and blending, and other applications. The report also covers the market size and forecasts for antiknock agents in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Ethanol |

| Tetraethyllead (TEL) |

| Methyl-Tert-Butyl Ether (MTBE) |

| Ethyl-Tert-Butyl Ether (ETBE) |

| Ethylbenzene and other Aromatics |

| Ferrocene and other metallics |

| Bio-based Oxygenates |

| Others |

| Liquid |

| Solid |

| Additive Packages/Concentrates |

| Bulk Terminal Injection |

| OEM Supply |

| Retail Aftermarket |

| Automotive |

| Aviation |

| Industrial Engines |

| Petro-refining and Blending |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Ethanol | |

| Tetraethyllead (TEL) | ||

| Methyl-Tert-Butyl Ether (MTBE) | ||

| Ethyl-Tert-Butyl Ether (ETBE) | ||

| Ethylbenzene and other Aromatics | ||

| Ferrocene and other metallics | ||

| Bio-based Oxygenates | ||

| Others | ||

| By Form | Liquid | |

| Solid | ||

| Additive Packages/Concentrates | ||

| By Distribution Channel | Bulk Terminal Injection | |

| OEM Supply | ||

| Retail Aftermarket | ||

| By Application | Automotive | |

| Aviation | ||

| Industrial Engines | ||

| Petro-refining and Blending | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Antiknock Agents Market?

The Antiknock Agents Market size is expected to increase from USD 3.44 billion in 2025 to USD 3.63 billion in 2026 and reach USD 4.75 billion by 2031, growing at a CAGR of 5.51% over 2026-2031.

Which region leads to demand for antiknock agents?

Asia-Pacific held 46.11% of 2025 revenue and is projected to grow at 6.28% CAGR through 2031.

Which product will grow fastest through 2031?

Bio-based oxygenates, notably bio-MTBE and bio-ETBE, are expected to expand at 6.17% CAGR.

Why are turbocharged engines important to octane demand?

Small turbocharged GDI engines need 95 RON or higher to avoid knocking, raising demand for premium antiknock blends.

Page last updated on: