Epoxy Curing Agent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.70 Billion |

| Market Size (2031) | USD 5.97 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

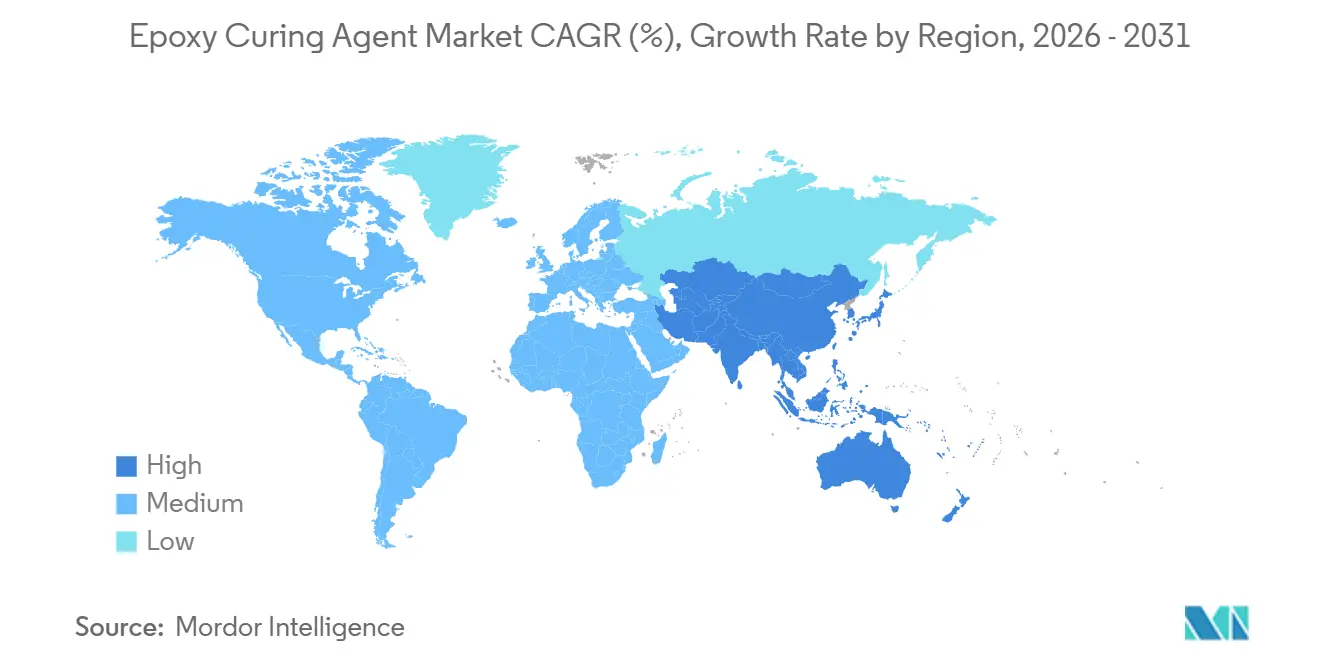

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

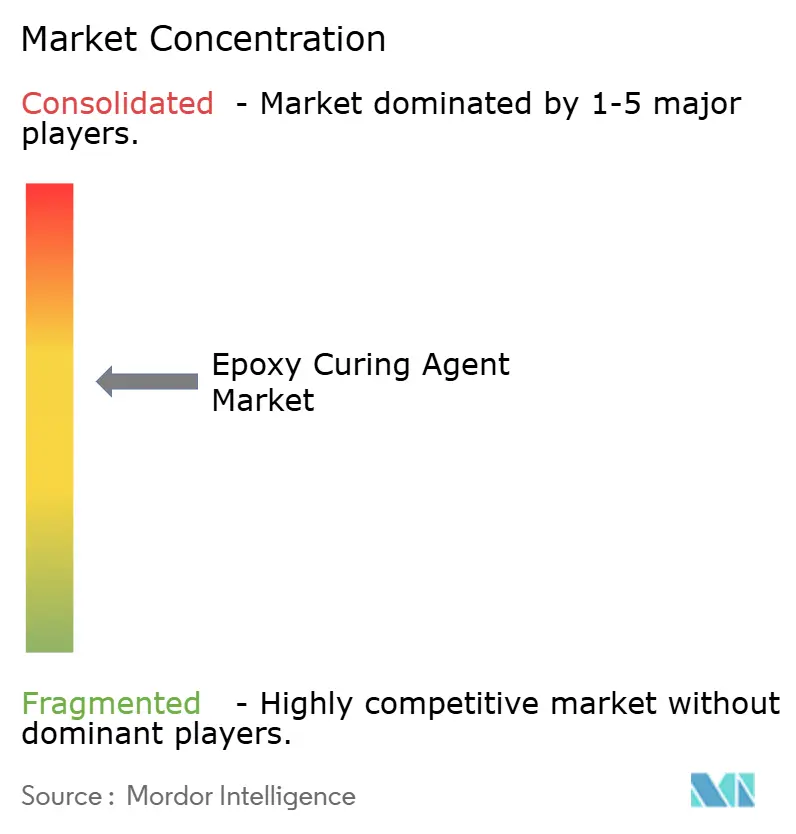

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epoxy Curing Agent Market Analysis by Mordor Intelligence

The Epoxy Curing Agent Market size is expected to increase from USD 4.5 billion in 2025 to USD 4.70 billion in 2026 and reach USD 5.97 billion by 2031, growing at a CAGR of 4.87% over 2026-2031. Rapid migration from commodity protective coatings to high-performance composites, electronics encapsulants, and 3-D printed thermosets underpins the expansion. Amines remain the volume leader, but cycloaliphatic variants are setting new benchmarks in cure speed and ultraviolet stability. Regional demand is diverging: Europe and North America continue to favor maintenance coatings, while Asia-Pacific drives incremental volume through semiconductor packaging, wind-turbine blades, and infrastructure flooring. Supply security for low-void encapsulants, recyclable epoxy matrices, and bio-based phenalkamines is becoming a dominant competitive theme.

Key Report Takeaways

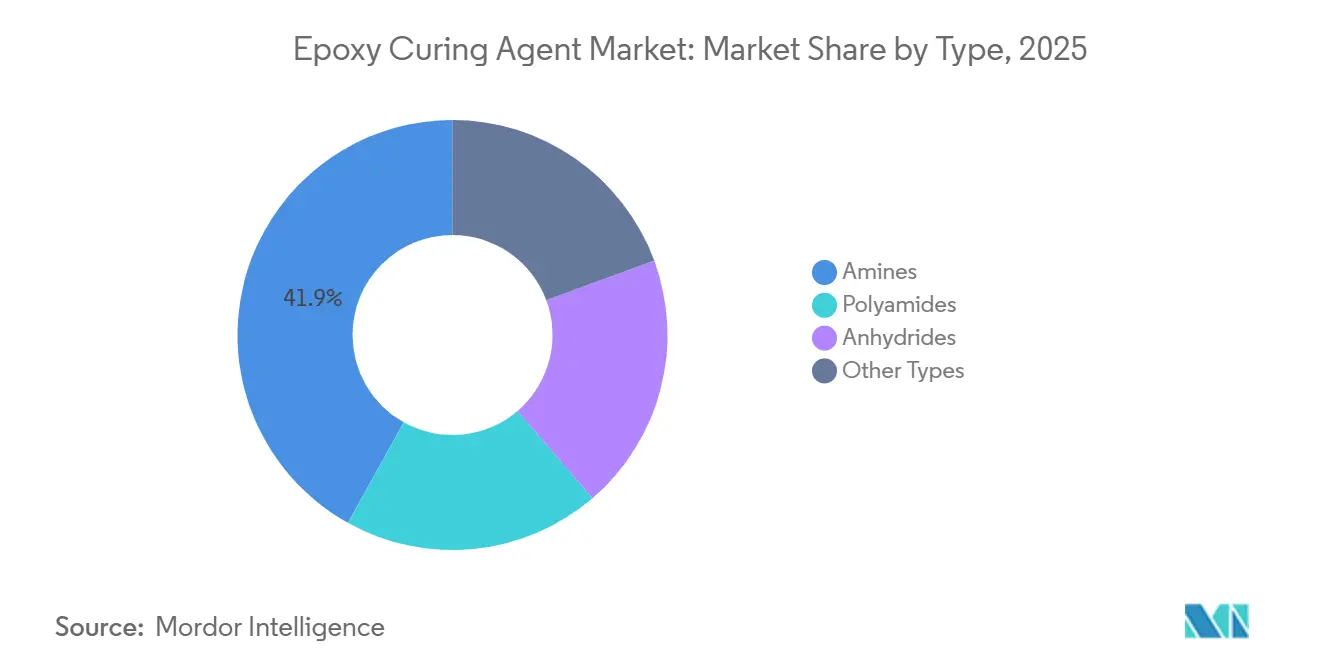

- By type, amines led with a 41.91% share in 2025, and polyetheramine subtypes are advancing at a 5.21% CAGR through 2031.

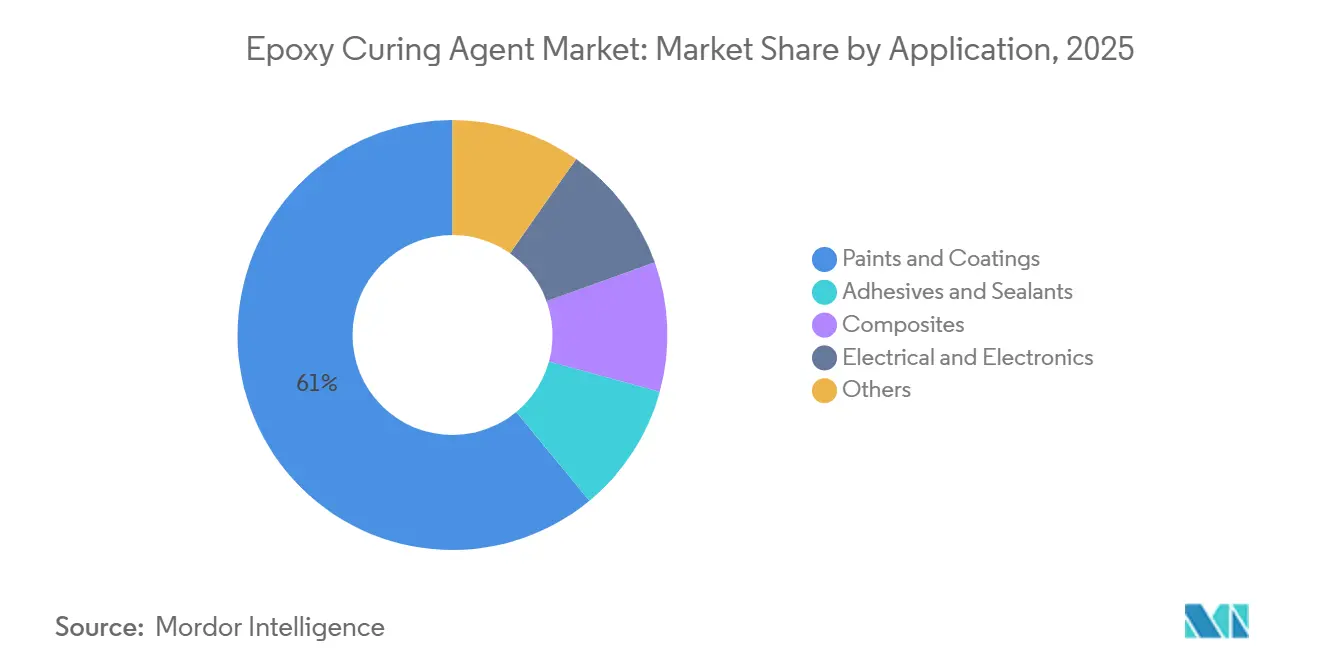

- By application, paints and coatings contributed 60.97% of revenue in 2025, and are projected to log the fastest 5.08% CAGR to 2031.

- By geography, Asia-Pacific accounted for 35.51% of global demand in 2025 and is on course to expand at a 5.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Epoxy Curing Agent Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure boom driving demand for high-performance floor coatings | +1.2% | APAC core, Middle East | Medium term (2-4 years) |

| Wind-turbine blade production surge | +1.0% | APAC, Europe | Long term (≥ 4 years) |

| Miniaturization of electronics requiring ultra-low-void encapsulants | +1.4% | Japan, South Korea, Taiwan, India | Short term (≤ 2 years) |

| Lightweight CFRP adoption in automotive & aerospace | +0.9% | Global | Long term (≥ 4 years) |

| Ultra-fast latent systems enabling 3-D printing | +0.6% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom Driving Demand for High-Performance Floor Coatings

Rising logistics, pharmaceutical, and data-center construction across China, India, and Gulf Cooperation Council countries is lifting solvent-free and high-solids epoxy flooring volumes. Authorities in China have set volatile organic compound (VOC) limits below 80 g/L, prompting formulators to adopt waterborne polyamide adducts despite humidity-sensitivity trade-offs. India’s cleanroom standards cap VOC emissions at 50 g/L, accelerating solvent-free epoxy mortars. GCC mega-projects specify cycloaliphatic amine systems that cure at ambient temperatures above 40°C, ensuring rapid turnaround and chemical resistance.

Wind-Turbine Blade Production Surge in APAC & Europe

Installed wind capacity rose to 241.7 GW in the European Union during 2024, while blade manufacture is concentrating in China and India, where resin and labor costs are lower[1]European Composites Industry Association, “Wind Energy Composites Statistics 2024,” eucia.eu. Medium-reactivity amines offering 80-120 minute pot life dominate vacuum infusion of 80 m-plus blades. End-of-life waste, forecast at 350,000 t by 2030 in the EU, is accelerating the adoption of cleavable hardeners such as Swancor’s EzCiclo that allow solvolysis recovery of carbon fiber.

Miniaturization of Electronics Requiring Ultra-Low-Void Encapsulants

Advanced semiconductor packaging demands epoxy molding compounds with void content below 0.01% and glass-transition temperatures above 180°C. Japan controls 40% global share in sealing materials, led by Sumitomo Bakelite, while India’s new assembly and test facilities in Gujarat and Gujarat’s Dahej chemical hub are spurring domestic demand for cycloaliphatic amine systems that reduce import lead times and tariffs.

Lightweight CFRP Adoption in Automotive & Aerospace

European Union fleet CO₂ targets of 93.6 g/km by 2025 compel greater carbon-fiber reinforced polymer use. Aerospace OEMs shift from autoclave to vacuum-bag-only prepregs cured at 120°C, favoring modified aromatic amines with long pot life. The EU’s EuReComp program highlights recyclable amine chemistries that depolymerize at the end of life while retaining fiber performance[2]European Commission, “Directive 2004/42/EC VOC Limits,” ec.europa.eu.

Restraints Impact Analysis of Epoxy Curing Agent Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC caps on solvent-borne amine systems | -0.8% | Europe, North America, China | Short term (≤ 2 years) |

| Volatile epichlorohydrin & benzyl-amine feedstock prices | -0.6% | Global | Medium term (2-4 years) |

| Supply crunch in cashew-derived phenalkamine feedstock | -0.3% | India, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter VOC Caps on Solvent-Borne Amine Systems

Volatile organic compound regulations are compressing margins for solvent-borne polyamide and amine hardeners, forcing reformulation toward waterborne and high-solids alternatives that often sacrifice pot life or film build. EU Directive 2004/42/EC limits VOCs to 40 g/L in one-pack and 65 g/L in multi-pack coatings, rendering legacy polyamide hardeners obsolete. Similar caps are pending in North America and China, steering demand toward waterborne polyamide adducts and polyaspartic hybrids despite higher raw-material costs.

Volatile Epichlorohydrin & Benzyl-Amine Feedstock Prices

Feedstock price volatility for epichlorohydrin and benzyl amine is eroding profitability for vertically integrated producers and forcing smaller formulators to pass costs to end users or absorb margin compression. Epichlorohydrin tracks propylene, experiencing 20–30% quarterly swings, while benzyl amine supply remains concentrated among five producers, heightening price shock risk. Integrated suppliers hedge volatility, whereas smaller formulators face margin compression and reduced R&D spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Epoxy Curing Agent Market Segment Analysis

By Type:

Cycloaliphatic Variants Redefine Amine DominanceAmines captured 41.91% revenue in 2025, and their share of the epoxy curing agents market is projected to expand at a 5.21% CAGR to 2031. Cycloaliphatic amines command 30–50% price premiums because they deliver ultraviolet stability and low viscosity essential for thick-section composites. Polyamides remain preferred for contaminated surfaces, but cannot match the two-hour overcoat readiness offered by polyaspartic hybrids. Anhydrides dominate electrical laminates thanks to glass-transition temperatures above 200°C, though their 150°C cure requirement limits field application. Phenalkamines, derived from cashew nutshell liquid, are winning niche marine and offshore jobs due to superior salt-fog performance and flexibility, while amidoamines offer a low-temperature cure for winter pipeline projects.

The epoxy curing agents market share of “Other Types” is set to climb as customers accept 20–40% upcharges for lifecycle cost savings. Adoption hinges on local availability because import lead times of eight weeks and tariffs of 7.5–10% erode project schedules. Patent activity in encapsulated imidazoles signals impending latent amine introductions that promise a six-month shelf life without refrigeration, a game-changer for additive manufacturing and field repair kits.

By Application:

Composites & Electronics Outpace Coatings GrowthPaints and coatings still represent 60.97% of the epoxy curing agents market size, yet their 5.08% growth lags behind composites and electronics. Protective floor systems in logistics centers require cycloaliphatic amines that cure under four hours, displacing slower polyamide systems. Marine coatings now specify phenalkamine hardeners capable of 300 µm dry film in one pass to cut dry-dock downtime.

Composites, adhesives, and electronics are set for faster expansion. Wind-turbine blades need medium-reactivity amines with 80–120 minute pot life, and semiconductor underfills demand phenolic-modified cycloaliphatic amines delivering void levels below 0.01%. Thermal-conductive adhesives for battery packs favor anhydrides to reach 2 W m-K while holding dielectric integrity. Industrial flooring is pivoting to waterborne systems to meet VOC mandates, penalizing commodity hardeners but opening niches for high-solids adducts with reduced odor.

Geography Analysis

APAC Epoxy Curing Agent Market

Asia-Pacific held 35.51% of the epoxy curing agents market in 2025 and is set to post a 5.77% CAGR through 2031. China continues to dominate floor coatings for logistics hubs and data centers, despite property-sector headwinds, while the Ministry of Ecology and Environment rules cap VOCs, boosting waterborne demand. India’s semiconductor expansion, Tata’s 300 mm fab, and Micron’s USD 2.75 billion assembly plant, will require domestic low-void encapsulants to avoid 10% tariffs and 60-day imports. Japan and South Korea retain technology leadership in sealing materials, but localization efforts in China and India are narrowing the gap.

North America Epoxy Curing Agent Market

North America benefits from aerospace composites and infrastructure upgrades funded by the Infrastructure Investment and Jobs Act. Aerospace OEMs increasingly specify vacuum-bag-only prepregs cured at 120°C, favoring modified aromatic amines. Offshore wind projects along the Atlantic demand cleavable hardeners to enable blade recycling mandates. Mexico’s vehicle output pushes adhesive volumes higher, yet reliance on imported curing agents adds USD 0.15 kg freight cost.

Europe, South America and GCC Epoxy Curing Agent Market

Europe shows steady demand from offshore wind and automotive lightweighting, but stricter VOC caps erode margins for solvent-borne hardeners. Wind-blade manufacturing is migrating toward Asia, leaving European suppliers focused on recyclable epoxy matrices to meet the Union’s 350,000 t end-of-life blade waste challenge. South America is led by Brazil’s protective-coating needs, while Gulf Cooperation Council construction, valued at USD 4.3 trillion over the next decade, requires amines that can cure in 40°C ambient conditions.

Value Chain Analysis

The epoxy curing agent value chain starts with petrochemical and bio-based feedstocks for amines, polyamides, and anhydrides (for example, epichlorohydrin-linked epoxy systems and benzyl-amine type intermediates on the amine side, plus cashew nutshell liquid for phenalkamines). Core manufacturing is concentrated among integrated and specialty chemical producers that convert these inputs into curing-agent families (aliphatic/cycloaliphatic amines, polyamide adducts, anhydrides, and latent systems), then package them into standardized forms for coatings, composites, and electronics formulators. Sustainability and process footprint are increasingly embedded in production operations, illustrated by Evonik transitioning its Crosslinkers epoxy curing agent production plants (Marl, Clayton, Isehara, Los Angeles, and Singapore) to renewable electricity.

Downstream, distributors and direct-to-formulator channels feed paint and coating producers, composite resin system houses, and electronics materials suppliers, where qualification cycles, VOC compliance, and application performance (pot life, low-void encapsulation, cure speed, and chemical resistance) shape supplier selection. Supply security and localization remain central, supported by capacity investments and regional manufacturing positioning that improve lead times and resilience, including Evonik expanding specialty amines capacity in Nanjing, China to support epoxy-related demand. Key bottlenecks include feedstock price volatility, qualification time in electronics and aerospace, and constrained availability of certain bio-based inputs such as phenalkamine feedstocks, which raises the value of backward integration, multi-site networks, and differentiated chemistries.

Competitive Landscape

The Epoxy Curing Agent market is moderately consolidated. Large players invest in backward integration into epichlorohydrin and benzyl amine, cushioning feedstock swings. Cardolite capitalizes on renewable feedstocks to supply phenalkamines for marine and offshore coatings. Technology competition centers on VOC-compliant waterborne systems, cleavable amines for recyclable composites, and latent catalysts for additive manufacturing.

Epoxy Curing Agent Industry Leaders

Evonik Industries AG

Huntsman International LLC

BASF

Cardolite Corporation

Olin Corporation

- *Disclaimer: Major Players sorted in no particular order

Epoxy Curing Agent Market Companies Covered in this Report

- Aditya Birla Group

- Air Products Inc.

- Atul Ltd.

- BASF

- Cardolite Corporation

- DIC Corporation

- Evonik Industries AG

- Huntsman International LLC

- KUKDO CHEMICAL CO., LTD.

- Kumho P&B Chemicals Inc.

- Mitsubishi Chemical Group Corporation

- Olin Corporation

- Shandong Deyuan Epoxy Resin Co. Ltd

- Toray Industries Inc.

- Westlake Corporation

Market Opportunities and Future Outlook

A clear whitespace is emerging around low-emission and low-temperature curing systems that help coatings users meet tightening VOC limits while maintaining productivity in marine and protective applications. Product activity in 2026 reflects this shift: Evonik introduced Ancamine 2873 as an ultra-low-emission curing agent designed for application at temperatures as low as 5 degrees C, which targets cold-weather windows where conventional systems struggle. Demand drivers linked to industrial flooring and infrastructure build-outs also point toward solvent-free and fast-turnaround systems, supporting cycloaliphatic and modified amine packages that balance cure speed, odor reduction, and moisture tolerance.

A second opportunity area is recyclable and circular epoxy networks for composites and high-temperature electronics, where end-of-life constraints coincide with high performance requirements. The market is seeing parallel pushes from industry and research into cleavable or reworkable hardeners and bio-based chemistries, including 2026 academic reports on bio-based latent curing agents for one-component epoxies and formaldehyde-free, bio-based phenalkamine routes for adhesives. On the supply side, investments that add regional amines capacity, such as Evonik starting operation of expanded specialty amine production in Nanjing in 2026, support localization strategies in Asia-Pacific where semiconductor packaging and infrastructure flooring are expanding, and where shorter lead times and stable supply can matter in qualification-driven segments.

Recent Industry Developments in Epoxy Curing Agent Market

- April 2026: Evonik introduced Ancamine 2873 as an ultra-low-emission epoxy curing agent for protective and marine coatings designed to enable application at temperatures as low as 5 degrees C. The launch reinforces the move toward VOC- and odor-reduced formulations while preserving field-season flexibility in colder climates. It also raises performance benchmarks for low-temperature cure systems in maintenance coatings.

- July 2025: Evonik transitioned epoxy curing agent production plants in its Crosslinkers business line to operate using 100% renewable electricity across sites including Marl, Clayton, Isehara, Los Angeles, and Singapore. This embeds lower-carbon manufacturing into the curing-agent supply base and supports customers that screen suppliers on Scope 1 and 2 emissions. Multi-site implementation also signals a standardized approach to decarbonizing production for globally supplied specialty hardeners.

- February 2024: DIC Corporation announced development of core technology for an epoxy resin curing agent that delivers heat resistance above 200 degrees C and enables recycling through remolding. This addresses a longstanding barrier in thermoset epoxy use cases where reworkability and end-of-life options have been limited. The development aligns with growing interest in reprocessable epoxy systems for high-temperature electrical and industrial applications.

Epoxy Curing Agent Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues generated from epoxy curing agents used to cure epoxy resins, which then support final performance in coatings, adhesives, composites, and electrical applications. We size demand based on where curing agents are sold as part of epoxy systems across major end-use industries.

Scope exclusions: Excluded items include epoxy resins themselves, non-epoxy hardeners, and finished epoxy formulated products sold without a separable curing-agent value.

Segments Covered in This Report

- By Type

- Amines

- Polyamides

- Anhydrides

- Other Types (Phenalkamines, Amidoamines, etc.)

- By Application

- Paints and Coatings

- Adhesives and Sealants

- Composites

- Electrical and Electronics

- Others (Industrial Flooring and Repairs, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research sets the factual base for the model so the inputs are not built on guesswork. We reviewed public sources such as USGS minerals data where relevant for feedstocks, US International Trade Commission trade statistics for chemical flows, OECD industrial indicators for downstream activity signals, and safety and regulatory references such as the US EPA and ECHA for substance and use restrictions that can shift product mix.

Along with that, we used company annual reports, investor presentations, and product technical literature to map curing-chemistry families, typical use rates, and where pricing moves up or down. Patent databases were also scanned to track new curing-agent development directions, including bio-based and low-VOC systems, and to sanity check whether adoption is still early or already scaled. For company-level revenue context and fast-moving announcements, we also used paid subscriptions focused on company financials and news. These desk sources are illustrative, and additional public references were also used during data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions, especially around application share splits, typical curing-agent loading, and how average selling prices change by chemistry and region. We spoke with participants across the value chain, including raw material suppliers, formulators, distributors, and downstream users in coatings, adhesives, composites, and electronics, and we covered major demand centers across APAC, EMEA, and the Americas to confirm what is actually purchased and used.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 42% |

| Mid tier: 44% | Functional/Unit leaders: 43% | EMEA: 33% |

| Smaller Players: 17% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

The market is first built using a top-down approach where epoxy end-use demand signals are reconstructed and then translated into curing-agent consumption using typical formulation ratios and application penetration. For epoxy curing agents, we tracked practical inputs such as epoxy coatings and flooring activity, infrastructure and construction spend linked to protective coatings, composites output indicators (including wind blades), and electronics and electrical encapsulation demand. We also tracked mix shifts between amines, anhydrides, and polyamides, since this changes both the price and the loading profile.

Once the demand pool is formed, results are corroborated through selective bottom-up approximations so totals stay realistic. This includes sampling supplier revenues where disclosures exist, checking distributor channel feedback on volume movement, and validating implied average selling prices against ranges seen in technical grades and regional supply conditions. Where visibility is weaker, such as for smaller local formulators, we apply conservative share bands and then re-check implied per-application volumes with interview guidance. Forecasts use scenario analysis anchored to end-use outlooks, followed by simple regression checks between key drivers like construction coatings activity, industrial production, and composites growth. We then adjust outcomes based on expected product mix and pricing.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number does not rely on one data stream. We compare modeled totals against independent signals like epoxy resin consumption direction, trade movement for relevant chemical categories, and downstream activity patterns, and then review outliers until the variance has a clear explanation.

Before sign-off, the model and assumptions go through step-by-step analyst review, including consistency checks across regions, type shares, and implied pricing. If a material event occurs, such as a capacity change, regulation shift, or sharp feedstock swing, respondents are re-contacted to determine whether the impact is temporary or structural. Reports are refreshed annually, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Epoxy Curing Agent Market Size Measured Against Other Published Estimates

Different published market sizes can disagree even when the same product name is used, because scope lines and counting rules are not the same, and the update timing also varies. The biggest differences usually show up when a study blends adjacent epoxy product value into the total, or when it applies a single price curve to different curing chemistries.

Finished epoxy formulated products sold as a bundled system are kept outside Mordor Intelligence's epoxy curing agent scope, which is why some broader chemical totals look higher when they include full formulation value instead of the curing-agent component only. Another common gap driver is how demand is tied to end uses: some estimates start from resin production, while others start from coatings, adhesives, composites, and electronics activity and then convert to curing-agent need using loading factors. Currency timing and inflation assumptions also matter, especially when feedstock-linked pricing moves quickly and a report is not refreshed close to the current year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.70 B (2026) | |

| Global Consultancy A | USD 5.73 B (2024) | Uses an earlier base year and a broader definition that can roll in additional epoxy system value across end users, and then applies a higher long-run growth profile that lifts the current-year equivalent. |

| Industry Publisher B | USD 5.80 B (2025) | Likely assumes faster mix shift and pricing progression across curing chemistries, and the longer forecast window can encourage optimistic adoption assumptions that are not always reconciled to near-term demand signals. |

The spread in the table mainly comes from what is being counted in the revenue pool, and how pricing and mix are carried forward from the base year. When inputs are tied back to clear end-use activity, chemistry-level mix, and realistic loading factors, the estimate stays traceable and easier to replicate in internal planning discussions.

Key Questions Answered in the Report

What is the forecast revenue for the epoxy curing agents market in 2031?

The market is projected to reach USD 5.97 billion by 2031.

Which region shows the fastest growth for epoxy curing agents?

Asia-Pacific leads, advancing at a 5.77% CAGR through 2031.

Why are cycloaliphatic amines gaining popularity?

They offer ultraviolet stability and rapid cure, meeting outdoor coating and composite needs.

How are VOC regulations influencing product development?

Stricter caps in the EU, North America, and China are shifting demand toward waterborne and high-solids hardeners.

Which application segment is expanding beyond protective coatings?

Composites and electronics encapsulation are outpacing traditional coatings growth.

Page last updated on: