Coalescing Agents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

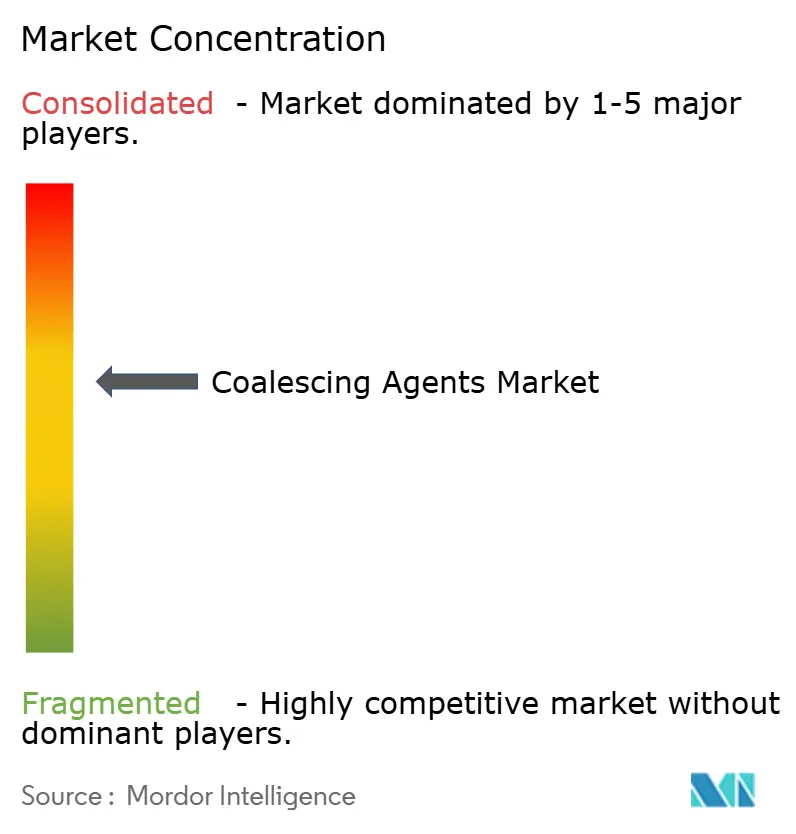

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coalescing Agents Market Analysis by Mordor Intelligence

The Coalescing Agent market size is expected to grow from USD 1.18 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.57 billion by 2031 at 4.86% CAGR over 2026-2031. Current demand is anchored in water-borne architectural, industrial, and specialty coating systems that must balance performance with strict environmental rules. Tightening volatile-organic-compound (VOC) limits, wider adoption of low-temperature curing, and growth in personal care emulsions jointly elevate consumption of next-generation additives. Manufacturers continue to relocate capacity to Asia-Pacific in response to favorable feedstock economics and large-scale coating line investments. At the same time, price spikes in glycol-ether intermediates and pending EPA aerosol-coating deadlines compel formulators to diversify raw-material portfolios and accelerate zero-VOC innovation.

Key Report Takeaways

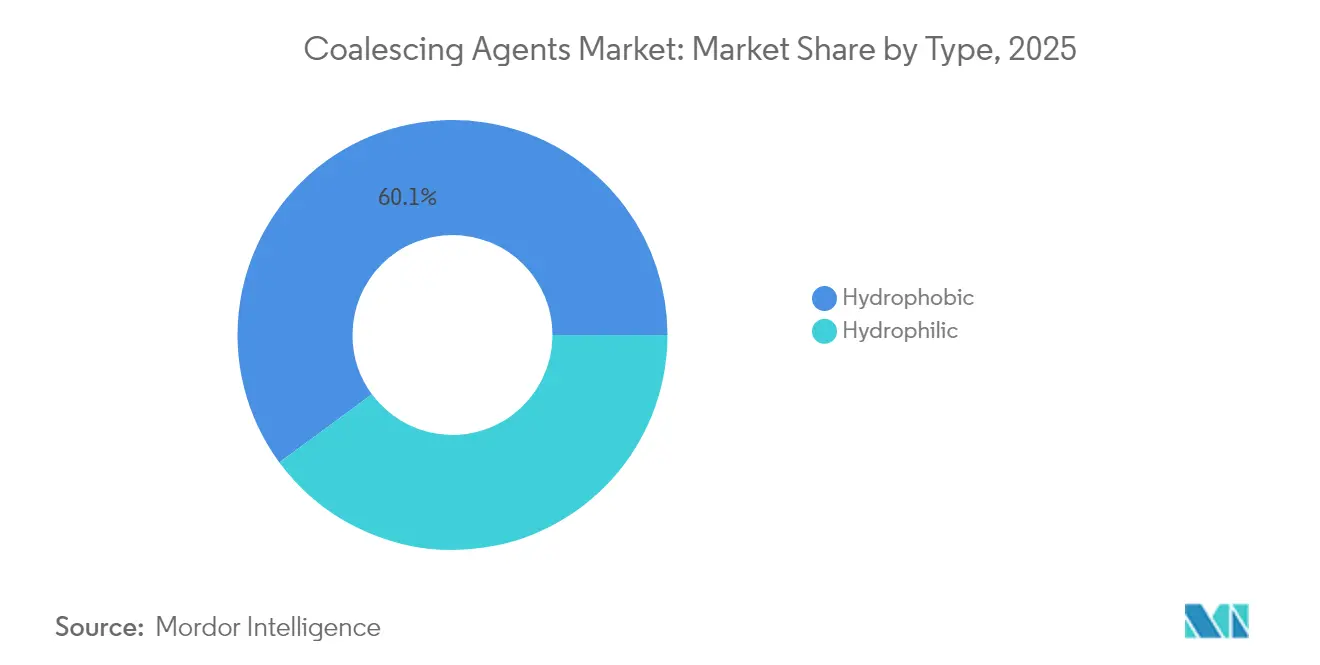

- By type, hydrophobic agents led with 60.10% of the coalescing agents market share in 2025, while hydrophilic agents are projected to expand at a 5.51% CAGR to 2031.

- By chemistry, alcohols accounted for 40.88% share of the coalescing agents market size in 2025, while esters are set to advance at a 5.34% CAGR through 2031.

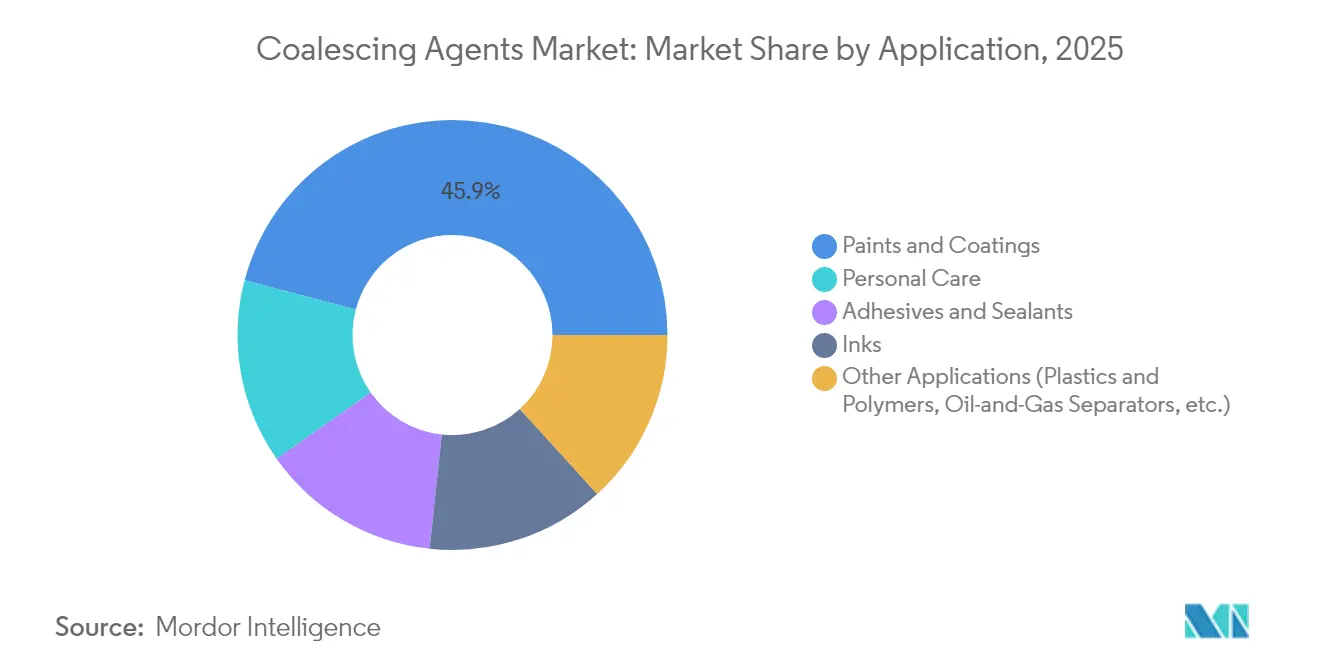

- By application, paints and coatings commanded 45.90% of 2025 demand within the coalescing agents market, while personal care is forecast to grow at a 5.72% CAGR up to 2031.

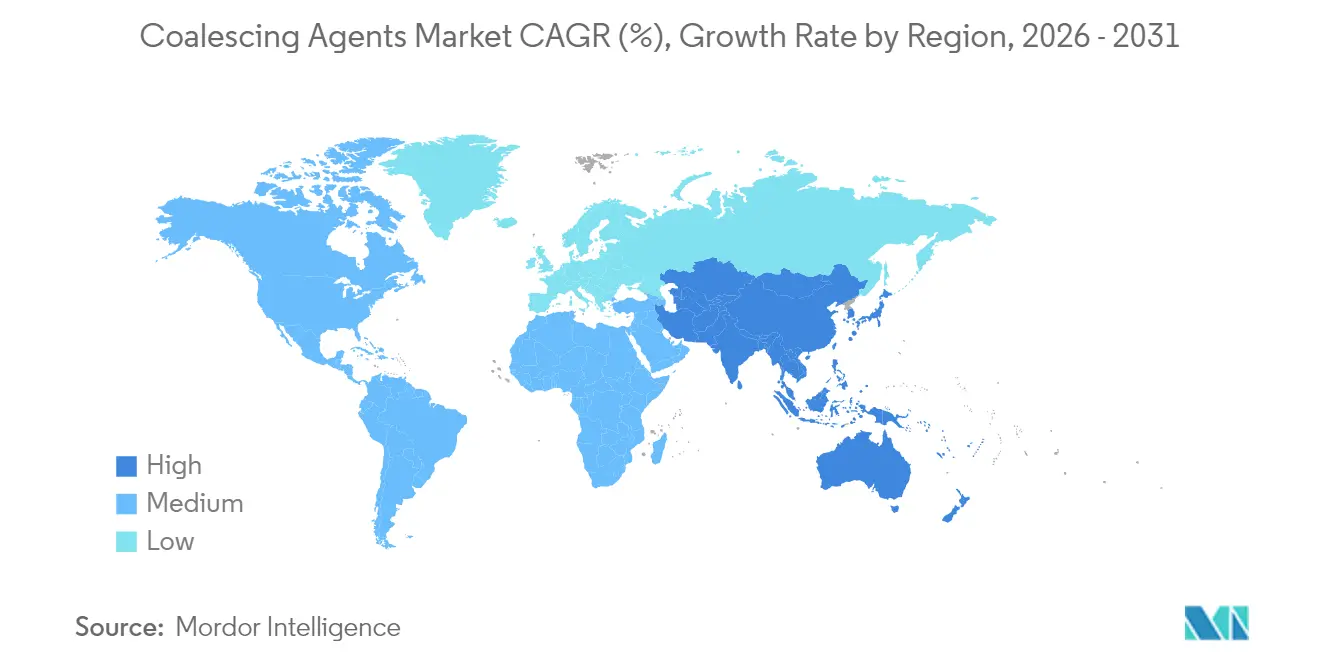

- By geography, Asia-Pacific captured 38.40% of the coalescing agents market size in 2025 and is expected to post the fastest 5.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coalescing Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Industrial Coating Lines in Developing Economies | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Uptake of Low-Temperature Film-Formation Additives in Automotive Refinish | +0.8% | Global, with concentration in North America and EU | Short term (≤ 2 years) |

| Tightening Indoor-Air-Quality Norms in Building Codes | +0.6% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Commercialization of Reactive (Zero-VOC) Coalescing Agents | +0.7% | Global | Medium term (2-4 years) |

| Commercialization of Reactive (Zero-VOC) Coalescing Agents | +0.5% | Global, with focus on North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Industrial Coating Lines in Developing Economies

Record infrastructure outlays across China, India, and Southeast Asia are lifting industrial coating throughput and creating a volume pull for the coalescing agents market. New ethylene and propylene crackers, such as SABIC’s USD 6.4 billion Fujian project with 1.8 million t/y capacity, guarantee backward integration for acrylic esters and glycol-ether derivatives essential to additive production. As water-borne formulations become mandatory in factory-applied metal, plastic, and wood coatings, demand concentrates on hydrophobic grades that accelerate film formation at ambient humidity. Regional petrochemical self-sufficiency also curbs import dependency, enabling local suppliers to shorten lead times while tailoring products to divergent national VOC caps. Collectively, these factors improve supply security and strengthen APAC’s positional advantage within the broader coalescing agents market.

Uptake of Low-Temperature Film-Formation Additives in Automotive Refinish

Electric-vehicle platforms and stringent air-district rules push refinish shops toward lower bake profiles to conserve energy and protect sensitive battery components. The South Coast Air Quality Management District’s revised Rule 1151, effective May 2025, tightens VOC ceilings across primer, base-coat, and clear-coat systems, accelerating the switch to high-boiling, low-odor coalescing agents that deliver proper film coalescence below 60 °C. Large refinish paint makers are incorporating ester blends that remain in the film long enough to promote latex fusion yet volatilize before service, helping body shops meet cycle-time KPIs. Global uptake is rapid because identical low-temperature needs exist in plastics finishing, aerospace touch-ups, and composite repair. This cross-sector adoption enlarges the coalescing agents market and mitigates cyclical swings tied solely to automotive volumes.

Tightening Indoor-Air-Quality Norms in Building Codes

Since 2024, multiple U.S. federal agencies and green-building programs have synchronized guidance that elevates indoor-air-quality benchmarks, disallowing high-VOC paint ingredients. Europe follows suit by revising EN 16516 to mandate lower emissions from decorative coatings. Architects therefore specify interior paints containing zero-VOC or chemically reactive coalescing agents that polymerize into the film. Suppliers who certify emissions through UL GREENGUARD quickly capture premium positions, especially in commercial and education projects where occupant-health metrics factor into funding decisions. Over the forecast period, the driver adds incremental growth to the coalescing agents market by stimulating formulation redesign across both renovation and new-build segments.

Commercialization of Reactive (Zero-VOC) Coalescing Agents

Reactive coalescent technology covalently integrates additive molecules into the polymer backbone, eliminating evaporative emissions and enabling compliance ahead of pending 2027 EPA aerosol-coating limits. BASF’s 2024 bio-based ethyl acrylate, which delivers 40% certified renewable content and a 30% smaller carbon footprint, represents a first mover in this category[1]BASF, “BASF Introduces Bio-based Ethyl Acrylate,” basf.com . Parallel academic research into polyurea-acrylic hybrids confirms viability for scratch-resistant clear-coat markets. Cost hurdles persist, but early adopters in electronics and luxury cosmetics signal that premium pricing is acceptable when paired with a demonstrable green label. Widespread scale-up is expected during the medium term, adding technology-rich sales to the coalescing agents market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| REACH and EPA Restrictions on High-VOC Ester Alcohols | -0.9% | North America and EU, expanding globally | Short term (≤ 2 years) |

| Volatility in Glycol-Ether Feedstock Pricing | -0.6% | Global | Short term (≤ 2 years) |

| Self-Coalescing Polymer Dispersion Technologies | -0.4% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

REACH and EPA Restrictions on High-VOC Ester Alcohols

EU REACH dossiers and the U.S. National VOC Emission Standards are progressively blacklisting high-reactivity ester alcohols, obliging formulators to re-screen raw materials and re-qualify end-use coatings Compliance timelines consume R&D budgets and slow product launches, especially for SMEs. Because acceptable substitutes often cost more and may require additional surfactant packages to stabilize latex particles, overall formulation economics tighten. Regional rule deviations further limit economies of scale, fragmenting inventories and adding logistics complexity that restrains the coalescing agents market.

Volatility in Glycol-Ether Feedstock Pricing

Dow’s January 2025 notice of USD 0.05/lb hikes on several glycol-ether grades highlights a trend of supply tightness triggered by propylene outages and robust demand from hair-care surfactants. Price swings compress margins for additive blenders that lack backward integration. Contract indexation offers partial relief, yet frequent negotiations disrupt customer relations. Smaller producers, particularly in Latin America, struggle to hedge and may withdraw from tender bids, tempering growth within the coalescing agents market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hydrophobic Dominance Faces Hydrophilic Innovation

The hydrophobic category retained 60.10% of the coalescing agents market share in 2025, benefiting from proven adhesion and water-resistance properties in heavy-duty coatings. Construction equipment, offshore platforms, and marine topcoats all specify hydrophobic blends due to prolonged exposure to moisture and solvents. Yet formulators increasingly complement these agents with ancillary wetting aids to manage gloss uniformity at higher solid contents. Margins remain attractive because large-volume paint makers favor long-term contracts that guarantee steady off-take.

Hydrophilic grades, while smaller today, log a 5.51% CAGR through 2031 on the back of stringent indoor-air-quality targets. Their molecular affinity to water packages allows use levels 10–15% lower than hydrophobic counterparts, trimming total VOC grams per liter. Cosmetic emulsion producers leverage these agents to stabilize oil-in-water formulations, improving sensory attributes without synthetic surfactants. As R&D refines film-formation profiles, uptake will accelerate in interior latex paints and next-generation adhesives, further diversifying the coalescing agents market.

By Chemistry: Alcohols Hold Leadership while Esters Accelerate

Alcohol-based products captured 40.88% of 2025 global demand thanks to cost-effective synthesis routes and balanced evaporation rates ideal for architectural latexes. Their supply chain is tightly linked to propylene oxide and acetaldehyde derivatives, which benefits integrated majors. Nonetheless, odor and toxicity considerations limit maximum inclusion levels in confined-space applications.

Ester chemistries post the fastest 5.34% CAGR through 2031. They offer lower odor thresholds, improved block resistance, and compatibility with bio-resins. Producers capitalize on glycerol and fatty-acid feedstocks, aligning with brand net-zero roadmaps. For example, reactive glycerol formal esters provide dual coalescing and cross-linking functionality, cutting additive count in high-performance floor finishes. With regulatory momentum squarely favoring low-VOC profiles, esters will expand their share of the coalescing agents market size for premium interior finishes and high-end packaging.

By Application: Paints and Coatings Anchor Demand while Personal Care Surges

Architectural, industrial, and OEM paints together consumed 45.90% of 2025 volume. Urbanization across Asia drives new construction, while North American renovation cycles sustain aftermarket demand. Water-borne epoxy primers and polyurethane finishes rely on carefully tailored coalescing packages to meet mechanical and corrosion-resistance targets, reinforcing the centrality of this segment within the coalescing agents market.

Personal care registers a 5.72% CAGR through 2031, the highest among all applications. Natural emulsifiers, such as saponins, require auxiliary coalescence aids to optimize viscosity, texture, and active-ingredient delivery. Clean-beauty brands highlight low-VOC claims to differentiate products on retail shelves, granting additive suppliers pricing latitude. Growth is also visible in functional skin transfer films used in long-wear color cosmetics. As indie brands scale globally, their procurement footprints enlarge, channeling incremental revenue into the coalescing agents market.

Geography Analysis

Asia-Pacific commanded 38.40% of coalescing agents market size in 2025. New ethylene and acrylic ester capacity clusters in China’s coastal provinces and in Vietnam’s Long Son complex assure raw-material supply and reduce freight expense. Regional governments continue to harmonize VOC measures with OECD benchmarks, propelling water-borne coating adoption. This policy push, combined with consumer upgrading and e-commerce packaging growth, yields a 5.29% CAGR through 2031, the fastest worldwide.

North America accounts for roughly one-quarter of demand, underpinned by mature but innovation-rich coatings and personal-care sectors. The EPA’s aerosol-coating deadline extension to January 2027 offers breathing room for formulation trials, stabilizing near-term offtake. Meanwhile, the shift to electric vehicle assembly lines raises consumption of low-temperature coalescing blends in refinish and plastic interior parts. Feedstock pricing volatility remains the primary regional headwind, prompting downstream users to negotiate shorter contracts.

Europe mirrors North American technology adoption yet grapples with elevated natural-gas costs that feed into acrylic-acid and glycol-ether production. Producers offset cost inflation by emphasizing zero-VOC innovations and bio-feedstock chain-of-custody certifications. Regulatory clarity on post-consumer plastic recycling targets stimulates R&D partnerships that position European firms at the vanguard of circular chemistry, maintaining steady contributions to the coalescing agents market.

Latin America, the Middle East, and Africa together represent a high-growth frontier. Petrochemical build-outs in Saudi Arabia and Abu Dhabi underpin resin-grade solvent availability, inviting downstream additive ventures. In Brazil and Mexico, housing rebound and export-oriented appliance manufacturing add diverse consumption points. Multinationals deploy technical service teams in these regions to tailor products to tropical climate performance norms, thereby expanding the addressable coalescing agents market over the long term.

Competitive Landscape

The coalescing agents market is moderately consolidated. Leading diversified chemical majors—BASF, Dow, Eastman, and Arkema—draw on integrated feedstocks and broad additive lines to serve global paint giants under multi-year supply accords. BASF’s 90% localized production footprint in Europe and North America insulates customers from cross-border freight disruptions. Dow leverages its propylene-oxide and epoxy chains to bundle solvents with related rheology modifiers, driving wallet share.

Strategic M&A remains lively. Milliken’s 2025 purchase of Borchers Group deepens know-how in cobalt-free driers and low-VOC dispersants, strengthening the combined entity’s hand in sustainability-focused coatings[2]Milliken & Company, “Milliken Completes Acquisition of Borchers,” milliken.com . Regional specialists in Japan and South Korea compete on niche performance, emphasizing electrolyte-stable esters for battery-pack coatings and anti-fog films.

Disruption risk stems from emergent self-coalescing binders that reduce additive loading. To hedge, incumbents co-develop binder-plus-additive packages with resin suppliers, embedding performance synergies difficult for stand-alone challengers to replicate. Digital formulation platforms, where predictive algorithms recommend optimal coalescent blends, further differentiate suppliers able to invest in data science.

Regulatory mastery evolves into a core competency. Companies conducting life-cycle analysis and providing third-party verified product carbon footprints enjoy accelerated vendor-of-choice status as paint makers align with corporate net-zero pledges. The converging trends of sustainability, digitalization, and specialty differentiation will shape competitive ranking inside the coalescing agents market during the next decade.

Coalescing Agents Industry Leaders

Eastman Chemical Company

Dow

BASF SE

Arkema

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Dow introduced a coalescing agent in its EcoDry product line for water-based paints and coatings. The product reduces volatile organic compound (VOC) emissions while maintaining coating performance.

- October 2023: BASF SE partnered with a research institution to develop coalescing agents for scratch-resistant automotive coatings. The collaboration focuses on improving the performance and durability of automotive coatings, specifically in scratch and mar resistance.

Global Coalescing Agents Market Report Scope

Coalescing agents are used in dispersion paints to optimize the film formation process of the polymeric binder particles. Coalescing agents help soften the polymer and form a solid, continuous film as the paint dries. They are stabilizers or temporary plasticizers that provide an even dispersion for polymer or resin.

The coalescing agents market is segmented by type, application, and geography. By type, the market is segmented into hydrophilic and hydrophobic. By application, the market is segmented into adhesives & sealants, paints & coatings, inks, personal care, and others (decoloring, polymer, etc.). The report also covers the market size and forecasts for the market in 27 countries across the globe.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Hydrophilic |

| Hydrophobic |

| Esters |

| Ketones |

| Alcohols |

| Diols and Glycol-ethers |

| Other Chemistries (Lactates, Citrates, Siloxanes) |

| Paints and Coatings |

| Adhesives and Sealants |

| Inks |

| Personal Care |

| Other Applications (Plastics and Polymers, Oil-and-Gas Separators, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Hydrophilic | |

| Hydrophobic | ||

| By Chemistry | Esters | |

| Ketones | ||

| Alcohols | ||

| Diols and Glycol-ethers | ||

| Other Chemistries (Lactates, Citrates, Siloxanes) | ||

| By Application | Paints and Coatings | |

| Adhesives and Sealants | ||

| Inks | ||

| Personal Care | ||

| Other Applications (Plastics and Polymers, Oil-and-Gas Separators, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the coalescing agents market?

The coalescing agents market size stands at USD 1.24 billion in 2026.

How fast is the coalescing agents market expected to grow?

The market is forecast to expand at a 4.86% CAGR, reaching USD 1.57 billion by 2031.

Which region holds the largest share of the coalescing agents market?

Asia-Pacific leads with 38.40% of global revenue and is also the fastest-growing region.

Which product type dominates the coalescing agents market?

Hydrophobic coalescing agents command 60.10% market share, while hydrophilic grades show the highest growth momentum.

What is driving demand for coalescing agents in personal care applications?

Innovations in sustainable cosmetic emulsions and texture-enhancing formulations are propelling personal care demand at a 5.72% CAGR.

Page last updated on: