Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 38.84 Billion |

| Market Size (2026) | USD 39.63 Billion |

| Market Size (2031) | USD 43.82 Billion |

| Growth Rate (2026 - 2031) | 2.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Processed Meat Market Analysis by Mordor Intelligence

The European processed meat market size in 2026 is estimated at USD 39.63 billion, growing from 2025 value of USD 38.84 billion with 2031 projections showing USD 43.82 billion, growing at 2.03% CAGR over 2026-2031. In Europe, the processed meat market is experiencing slower growth, mirroring a shift in consumer values. Concerns over health, sustainability, and ethics increasingly challenge traditional meat preferences. While pork, with its deep cultural roots, continues to dominate, beef is carving out a niche, especially among those seeking premium, high-protein options. Chilled products are favored for their freshness and convenience, yet frozen items are gaining traction due to their longer shelf life and versatility. Innovations in packaging, particularly vacuum solutions, are on the rise, emphasizing shelf-life, hygiene, and sustainability. These advancements not only cater to consumer demand for longer-lasting products but also address environmental concerns by reducing food waste and incorporating eco-friendly materials. Supermarkets and retail outlets still lead in sales channels, but restaurants and hospitality venues are witnessing a significant rebound, fueled by a resurgence in tourism and a renewed dining-out culture.

Key Report Takeaways

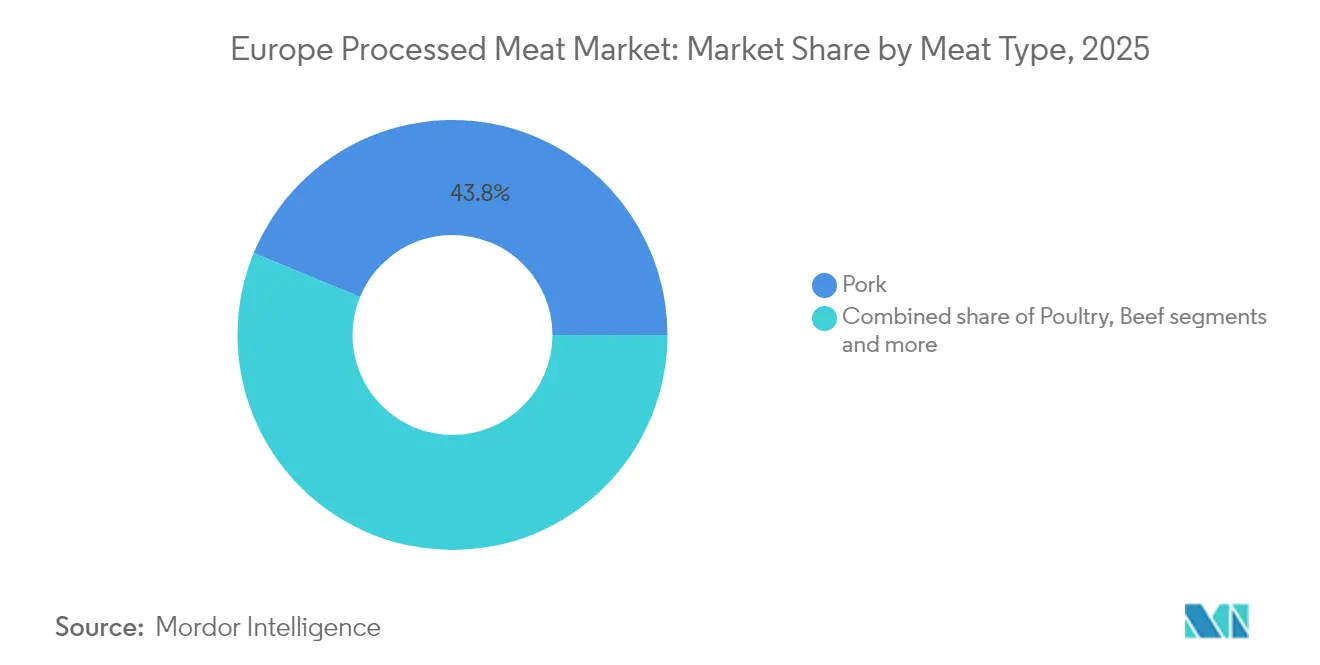

- By meat type, pork led with 43.78% of the Europe processed meat market share in 2025, whereas beef is projected to post the quickest 4.48% CAGR during 2026-2031.

- By product type, chilled items captured 60.72% revenue share in 2025; frozen products are forecast to expand at a 5.35% CAGR to 2031.

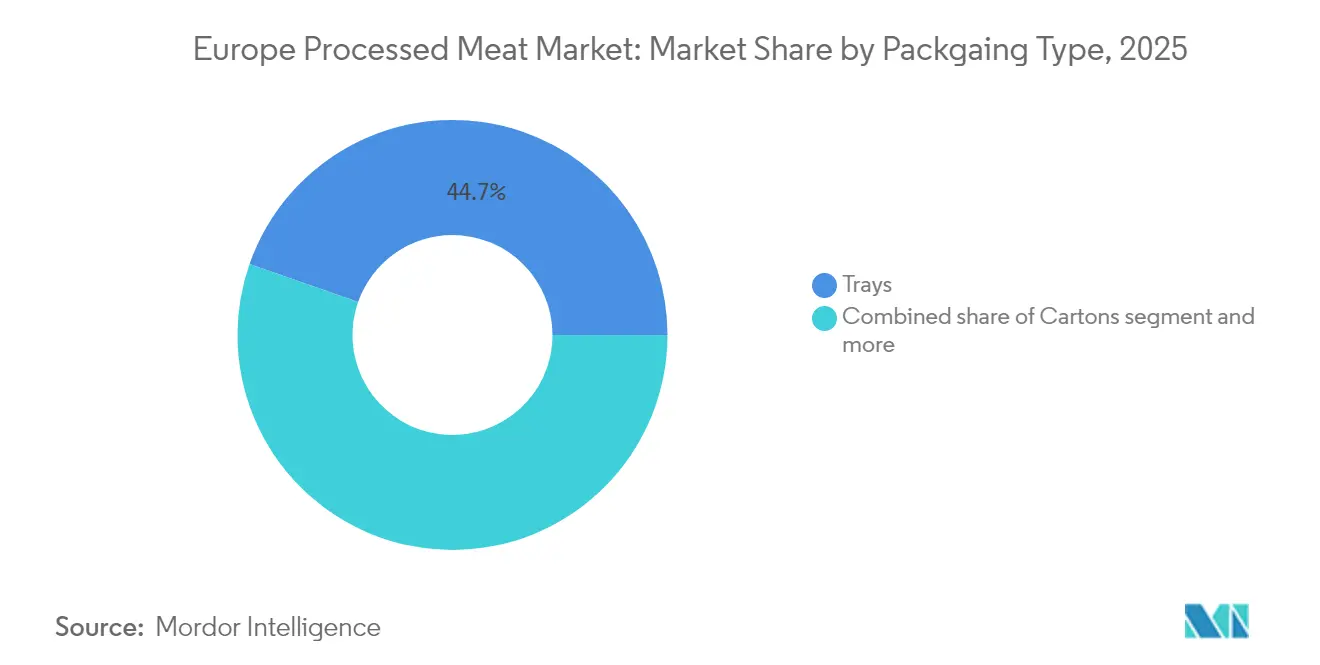

- By packaging, trays held 44.65% of the market in 2025, while vacuum-pack solutions are advancing at a 4.34% CAGR through 2031.

- By distribution channel, off-trade accounted for 61.74% share of the Europe processed meat market in 2025; on-trade is the fastest-growing segment, rising at 6.92% CAGR.

- By geography, Germany commanded 23.85% of the market in 2025, whereas Spain is set to grow the quickest at 3.67% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Processed Meat Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer demand for convenient and ready-to-eat meat products drives market growth | +0.5% | Germany, United Kingdom, France, Spain, Italy | Short term (≤ 2 years) |

| Advancements in food processing technologies improve product quality and shelf life | +0.3% | Germany, Netherlands, Denmark, United Kingdom | Medium term (2-4 years) |

| Rising awareness about protein's role in health and fitness supports product demand | +0.2% | United Kingdom, Germany, Sweden, Netherlands | Medium term (2-4 years) |

| Increasing demand for ethnic and flavored processed meat varieties stimulates market innovation | +0.4% | United Kingdom, France, Germany, Spain | Short term (≤ 2 years) |

| Growing tourism and hospitality sector boosts consumption in foodservice channels | +0.4% | Spain, Italy, France, Greece | Short term (≤ 2 years) |

| Growing popularity of international cuisines increases demand for diverse processed meat products | +0.3% | United Kingdom, Germany, France, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer demand for convenient and ready-to-eat meat products drives market growth

Surging consumer appetite for convenient, ready-to-eat meat products fuels market expansion. In Europe, the growing preference for processed meat products such as sausages, salami, bacon, ham, and pre-cooked chicken is a significant driver. For instance, the increasing adoption of ready-to-eat meals among working professionals and urban households highlights the demand for convenience. The working population, in particular, plays a crucial role in driving this demand, as busy schedules and long working hours leave limited time for meal preparation, making processed meat products an attractive option. According to the European Commission, approximately 65.4% of all parents in the EU were in active employment in 2023 [1]Source: European Commission, “Household Consumption Statistics,"ec.europa.eu. Countries like Germany, Spain, and Italy have witnessed a notable rise in the consumption of processed meat due to their strong culinary traditions and the growing number of employed individuals seeking quick meal solutions. Additionally, the rise of retail chains and online platforms offering a wide variety of processed meat options further supports market growth. For example, supermarket chains such as Tesco, Carrefour, and Lidl have expanded their processed meat product ranges to cater to evolving consumer preferences.

Advancements in food processing technologies improve product quality and shelf life

Food processing technology advancements enhance product quality and extend shelf life, driving the growth of the Europe processed meat market. For instance, technologies like high-pressure processing (HPP) and vacuum packaging are widely adopted to preserve the freshness and nutritional value of processed meat products. HPP effectively eliminates pathogens without compromising the taste or texture, while vacuum packaging minimizes oxidation, thereby extending shelf life. Additionally, innovations such as automated slicing and portioning systems ensure consistent product quality, meeting consumer demand for convenience and reliability. Furthermore, the adoption of modified atmosphere packaging (MAP) has gained traction, as it helps maintain the color, flavor, and overall quality of processed meat for longer durations. Advanced freezing techniques, such as cryogenic freezing, are also being utilized to retain the texture and moisture content of meat products. These advancements not only improve product appeal but also support manufacturers in reducing waste, optimizing supply chain efficiency, and complying with stringent food safety regulations.

Rising awareness about protein's role in health and fitness supports product demand

In Europe, the processed meat market is witnessing a surge in demand, largely driven by a growing awareness of the health and fitness benefits associated with protein. Consumers are increasingly gravitating towards high-protein processed meat options to meet their dietary and fitness goals. Health-conscious individuals are showing a marked preference for products such as protein-enriched sausages, turkey bacon, and lean ham. The rising popularity of fitness trends, from gym memberships to home workout routines, has intensified the demand for processed meats, especially those marketed as high in protein and low in fat. Additionally, the shift towards healthier lifestyles has encouraged manufacturers to innovate and introduce products that cater to these evolving consumer preferences. The market is also witnessing a rise in collaborations between fitness influencers and processed meat brands to promote protein-rich products. Furthermore, the growing popularity of clean-label and organic processed meat options, which prioritize natural ingredients and boast high protein content, is bolstering market growth. These trends underscore the pivotal role of protein in shaping Europe's processed meat landscape.

Growing tourism and hospitality sector boosts consumption in foodservice channels

Europe's tourism and hospitality boom is propelling a surge in processed meat consumption, particularly through foodservice channels. According to Eurostat, in 2024, the EU recorded 2.99 billion nights in tourist accommodations, a notable rise from 2.8 billion in 2022 [2]Source: Eurostat, "EU sees bigger share of tourists from outside Europe,"ec.europa.eu. This uptick in tourism has spurred a heightened appetite for dining out, bolstering the foodservice sector. Moreover, in 2024, the EU's Travel & Tourism industry injected nearly EUR 1.8 trillion into the region's GDP, underscoring its economic significance [3]Source: World Travel and Tourism Council, "France Set to Maintain Unmatched 2024 Growth in Travel & Tourism,"wttc.org. As tourist numbers surge, quick-service restaurants, cafes, and upscale dining venues are increasingly turning to processed meat to satisfy their patrons. Processed meat offers convenience, consistency, and versatility, making it a preferred choice for foodservice operators aiming to meet diverse consumer preferences. Additionally, the growing trend of dining out and the increasing popularity of international cuisines further drive the reliance on processed meat. With the hospitality sector expanding alongside this tourist influx, the demand for processed meat in foodservice channels is set to grow even more in the years ahead.

Restraints Impact Analysis of Europe Processed Meat Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to high fat, salt, and preservative content limit consumer demand | -0.3% | United Kingdom, Germany, Netherlands, Sweden | Medium term (2-4 years) |

| Increasing shift towards vegetarian and vegan diets restrains market growth | -0.2% | Germany, United Kingdom, Netherlands, Sweden | Long term (≥ 4 years) |

| Strict regulations on food safety and additives increase production costs and complexity | -0.4% | Europe-wide, particularly Germany, France, Italy | Medium term (2-4 years) |

| Rising raw material costs increase production expenses and affect pricing | -0.3% | Europe-wide, particularly affected by global commodity markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns related to high fat, salt, and preservative content limit consumer demand

Growing scientific evidence linking processed meat consumption to various health conditions is creating significant headwinds for market growth across Europe. Concerns about nitrites and nitrates, commonly used as preservatives in processed meats, have prompted regulatory responses, with the European Commission implementing stricter limits on these additives in animal-origin products. Denmark has pioneered more stringent national provisions, allowing for lower maximum added amounts of nitrites (60 mg/kg for many products) compared to broader EU standards (up to 150 mg/kg). Consumer awareness of these health implications is growing, with a study across multiple European countries revealing that many consumers view processed meats as unhealthy, associating them with high levels of harmful chemicals, fat, and salt. This perception challenge is particularly acute among health-conscious demographics, with women consistently demonstrating greater concern about processed meat consumption than men. The industry is responding with reformulation efforts to reduce salt, fat, and preservative content, though these modifications often present technical challenges for maintaining traditional flavor profiles and shelf stability.

Increasing shift towards vegetarian and vegan diets restrains market growth

Plant-based diets are gaining traction across Europe, posing a significant challenge to the processed meat market, especially in Northern European nations. This shift towards plant-based eating is fueled by health, environmental, and ethical considerations, putting consistent pressure on traditional meat consumption. According to the European Commission's Agricultural Outlook Report 2024-2035, EU pork consumption is set to decline by 0.4% annually until 2035, with projections hitting 30 kg per capita. This decline is largely attributed to rising sustainability concerns and evolving consumer preferences. The market for plant-based meat alternatives is on the rise, bolstered by substantial investments and innovations. A testament to this momentum, the European Investment Bank extended a EUR 20 million loan to Heura Foods, a Spanish startup at the forefront of plant-based meat alternatives. While processed meat continues to lead in the protein domain, the enhanced quality and growing availability of plant-based options are carving out a competitive space, especially among younger and urban consumers more open to reducing or substituting meat in their diets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Processed Meat Market Segment Analysis

By Meat Type:

Pork retains leadership, beef gains groundIn 2025, pork solidified its position as the leading segment in Europe's processed meat market, capturing 43.78% of the market share. This dominance is deeply rooted in the strong culinary traditions of countries such as Germany, Spain, and Poland, where pork-based products are a cornerstone of local diets. Products like sausages, ham, and bacon are not only staples in these regions but also enjoy widespread popularity across Europe due to their versatility and flavor.

Meanwhile, the beef segment is undergoing substantial growth, driven by the rising demand for premium and diverse meat options. Products such as premium burgers, pastrami, and bresaola are gaining traction among consumers who seek high-quality and gourmet processed meat offerings. This shift is fueled by changing dietary trends, including the growing preference for protein-rich diets and the increasing popularity of international cuisines that feature beef prominently. The segment is projected to grow at a CAGR of 4.48% through 2031, reflecting its expanding consumer base and the dynamic nature of the European processed meat market.

By Product Type:

Chilled dominates, frozen surgesIn 2025, chilled offerings emerged as the leading segment in the market, accounting for 60.72% of the market share. Consumers increasingly associate chilled products with freshness and artisanal quality, driving their popularity. This segment includes deli counters, sliced charcuterie, and grab-and-go ham sandwiches, which have become staples in supermarkets. These products cater to the growing consumer demand for convenience and premium options, making them a preferred choice for quick meals and high-quality ingredients.

The frozen segment, on the other hand, is experiencing significant growth, with a strong CAGR of 5.35%. This growth is primarily driven by advancements in flash-freezing technology, which effectively preserves the texture and quality of frozen products while extending their shelf life. These innovations have made frozen processed meat products highly attractive to budget-conscious consumers seeking cost-effective solutions without compromising on quality. Furthermore, the extended storage life of frozen products has positioned them as a practical choice for export buyers and households aiming to reduce food waste.

By Packaging:

Trays stay in front, vacuum expandsIn 2025, trays dominated the European processed meat market, accounting for a significant 44.65% market share. Their widespread adoption can be attributed to their transparency, which enables consumers to quickly and effectively evaluate the color and marbling of processed meat products. This feature is particularly important in building consumer trust and ensuring product quality. Additionally, trays are lightweight, easy to handle, and compatible with various packaging technologies, making them a preferred choice for manufacturers and retailers alike. The growing demand for visually appealing and hygienic packaging solutions further supports the dominance of trays in the market.

Meanwhile, vacuum packs are expected to grow at a CAGR of 4.34% during the forecast period. This growth is driven by the increasing focus of both retailers and consumers on reducing food waste and extending the shelf life of processed meat products. Vacuum packaging minimizes oxygen exposure, which helps preserve the freshness and quality of the meat for a longer duration. Furthermore, the rising awareness of sustainable packaging solutions and the need to maintain product integrity during transportation are contributing to the growing adoption of vacuum packs.

By Distribution Channel:

Off-trade commands, on-trade acceleratesIn 2025,off-trade channel delivered 61.74% of sales in Europe's processed meat market, highlighting the market's strong dependence on off-trade formats. Big-box retailers actively drive customer traffic by leveraging private labels and offering weekly promotions. Meanwhile, the on-trade segment is expanding at a faster pace, achieving a 6.92% CAGR as tourism rebounds and consumers dine out more frequently. Gastro-pubs and quick-service restaurants increasingly demand labor-saving, precooked options such as bacon, brisket, and tapas meats, which significantly reduce kitchen preparation times and improve operational efficiency.

Online grocery shopping, a trend that gained traction during the pandemic, continues to scale rapidly. This growth is particularly evident in premium products like Iberian ham and organic turkey slices, as customers increasingly value the convenience of doorstep delivery. Producers who supply multipacks for retail and bulk vacuum rolls for chefs are optimizing production processes and effectively managing raw-material risks to meet diverse demands. Convenience stores are boosting profits by offering single-serve snack sticks tailored to busy commuters, while delicatessens remain a key channel for showcasing high-margin artisanal products, appealing to consumers seeking premium quality.

Geography Analysis

Germany Processed Meat Market

Germany, in 2025, secured a dominant 23.85% share of the European processed meat market, establishing itself as a key player in the region. The country's strong foothold can be attributed to its well-established meat processing industry, high domestic consumption, and robust export activities. Germany's focus on innovation in meat processing techniques and the availability of a wide variety of processed meat products have further strengthened its position in the market. Additionally, the country's adherence to stringent quality standards and sustainability practices has enhanced consumer trust and boosted demand for its processed meat products both domestically and internationally.

Spain Processed Meat Market

Spain is set to be the fastest-growing contender in the European processed meat sector, with a projected CAGR of 3.67% through 2031. The growth in Spain is driven by increasing consumer demand for ready-to-eat and convenience food products, coupled with advancements in meat processing technologies. The rising popularity of Spanish processed meat products, such as chorizo and jamón, in international markets has also contributed to this growth. Furthermore, the country's investments in modernizing its meat processing facilities and expanding its export capabilities are expected to sustain its upward trajectory during the forecast period.

United Kingdom and Italy Processed Meat Market

The United Kingdom also plays a significant role in the European processed meat market. Despite challenges such as changing consumer preferences and regulatory shifts post-Brexit, the market remains resilient. The demand for processed meat products, particularly sausages and bacon, continues to be strong, supported by a growing inclination toward premium and organic meat options. Italy, known for its rich culinary heritage, contributes significantly to the processed meat market in Europe. The country is renowned for its traditional processed meat products, such as salami and prosciutto, which enjoy high demand both domestically and internationally. Italy's focus on quality and authenticity has helped it maintain a competitive edge in the market.

Regulatory Landscape

The European processed meat market operates under the EU food hygiene package, with Regulation (EC) No 853/2004 setting hygiene requirements for food of animal origin and establishment-level controls across meat preparation and processing. Market access and compliance requirements have been refined through updates such as Commission Delegated Regulation (EU) 2025/637, which clarifies certain rules affecting the entry and handling of processed animal-origin products and related materials used in processed meat supply chains.

On food safety and formulation, EU rules on additives under Regulation (EC) No 1333/2008 continue to shape reformulation activity, particularly for nitrites and nitrates used in cured meats. Ready-to-eat (RTE) processed meats face heightened scrutiny as tighter Listeria control requirements take effect in July 2026. At the same time, EU trade and tariff instruments are changing procurement conditions for meat inputs and processed goods, including the provisional application of the EU-Mercosur agreement from May 2026 and changes to customs duties via Council Regulation (EU) 2026/1463 effective from July 2026.

Competitive Landscape

The European processed meat market holds a moderately fragmented competitive landscape. This score indicates that while a few dominant players hold a significant share of the market, there is still considerable space for regional and local companies to compete effectively. The market features a mix of well-established multinational corporations and smaller, niche players, creating a dynamic environment. The moderate concentration level suggests that no single entity has overwhelming control, allowing for healthy competition and opportunities for new entrants to establish themselves.

Key players in the market are actively engaging in strategies to maintain or expand their market share. These strategies include product innovation, where companies are introducing new and diverse processed meat products to cater to changing consumer demands, such as healthier options or plant-based alternatives. Pricing strategies also play a critical role, as companies aim to balance affordability with profitability to attract a broader customer base. Additionally, the development of robust distribution networks, including partnerships with retailers and e-commerce platforms, has become a focal point for market players to ensure widespread availability of their products.

Furthermore, mergers, acquisitions, and partnerships are becoming increasingly common as companies seek to consolidate their positions in the market. These activities enable firms to expand their geographic reach, enhance their product portfolios, and achieve economies of scale. The competitive landscape is also shaped by advancements in processing technologies, which allow companies to improve efficiency and product quality. Additionally, the growing emphasis on sustainability and ethical sourcing is pushing market players to adopt environmentally friendly practices, further intensifying competition.

Europe Processed Meat Industry Leaders

-

WH Group Ltd

-

JBS S.A.

-

BRF S.A.

-

Tyson Foods Inc.

-

Premium Food Group ApS & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Europe Processed Meat Market Companies Covered in this Report

- WH Group Limited

- JBS S.A.

- Premium Food Group ApS & Co. KG

- Tyson Foods Inc.

- BRF S.A.

- Vion Holding N.V.

- Hormel Foods Corporation

- Conagra Brands, inc.

- Plukon Food Group

- Dawn Meats Group Ltd.

- Cranswick PLC

- Sigma Alimentos, S.A. de C.V.

- Sysco Corporation

- Leverandrselskabet Danish Crown AmbA

- Cargill, Incorporated

- Seaboard Corporation

- Mafrig Global Foods SA

- The Bigard Group

- Cherkizovo Group

- Lambert Dodard Chancereul Group

Market Opportunities and Future Outlook

Product reformulation and compliance-led innovation remain key opportunity areas as additive constraints and safety controls tighten for high-volume categories such as RTE and cured meats. The July 2026 step-up in EU Listeria controls for RTE foods, alongside ongoing reductions in permitted nitrite use under the EU additives framework, supports demand for processing technologies and packaging formats that protect shelf life and hygiene. This includes high-pressure processing (HPP), vacuum packaging, and improved cold-chain execution, which also aligns with the market shift toward chilled convenience foods.

Capacity modernization and higher-throughput facilities are another opportunity area, supported by announced investments that add scale and automation to European processed meat production. Campofrio has started construction on a new processed meat plant in Utiel, Spain (EUR 134 million, operations scheduled to start in 2027), and expansion programs in Hungary emphasize high-tech processing (including AI and robotics) along with higher slaughter and processing capacities. These moves support retailers and foodservice buyers seeking consistent specifications, longer shelf-life formats, and labor-saving product lines, while manufacturers look to manage cost volatility through more efficient operations and broader value-added portfolios.

Recent Industry Developments in Europe Processed Meat Market

- May 2026: JBS S.A. reported its first-quarter 2026 results and highlighted continued focus on expanding branded prepared foods alongside a balanced protein portfolio across its operations. The emphasis on value-added products supports European processed-meat competitiveness where retailers and foodservice buyers prioritize consistent specifications, safety assurance, and convenience-led formats.

- September 2025: Germanys Bundeskartellamt approved the acquisition of The Family Butchers Group by Tonnies International Management GmbH, part of Premium Food Group. The decision strengthened Premium Food Groups position in German processed meats, with implications for procurement scale, brand portfolio breadth, and retail bargaining dynamics.

- September 2024: Pilgrims Pride Corporation completed the acquisition of Moy Park from JBS S.A. for about USD 1.3 billion, adding poultry and prepared foods capacity across the United Kingdom and Continental Europe. The deal broadened Pilgrims Pride access to European prepared-meat channels and increased competitive intensity in value-added poultry-based processed products.

Europe Processed Meat Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market includes processed meat products sold across Europe that have been altered to improve taste or extend shelf life through methods such as curing, smoking, salting, fermentation, and preservatives.

Scope exclusions: Fresh, unprocessed raw meat sold without preservation or processing steps is not counted in this market value.

Segments Covered in This Report

-

By Meat Type

- Poultry

- Beef

- Pork

- Mutton

- Other Types

-

By Product Type

- Chilled

- Frozen

- Canned/Preserved

-

By Packaging

- Vacuum-Pack

- Trays

- Cartons

- Others

-

By Distribution Channel

-

Off-Trade

- Supermarkets & Hypermarkets

- Convinience Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- On-Trade

-

Off-Trade

-

By Geography

- Germany

- United Kingdom

- France

- Spain

- Italy

- Denmark

- Netherlands

- Sweden

- Belgium

- Russia

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer boundaries for Europe, and to understand what volumes and prices look realistic before we start modeling. We leaned on public production and trade statistics and category notes from sources such as Eurostat, FAOSTAT, UN Comtrade, and national statistical offices across major European countries. To keep definitions consistent, we also reviewed guidance and publications from food safety regulators and standards bodies, such as the European Commission and related agencies, along with trade association releases.

After that, we pulled supporting signals from company filings, investor presentations, retailer and brand announcements, and credible press coverage to check pricing moves, packaging shifts, and channel mix changes. Where public financial splits were limited, we used paid subscriptions for company financials and intelligence, plus an import and export shipment-level database to cross-check trade direction and unit values in key product codes. These desk research sources are not exhaustive, and many other public and internal references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how processed meat is priced and sold in practice, and on confirming what is actually counted as processed meat across chilled and frozen formats. We spoke with a spread of stakeholders across Europe, including manufacturers, ingredient and packaging suppliers, distributors, and retail or foodservice-facing roles, so assumptions from desk research could be tested and then adjusted where needed. Inputs were also used to confirm country weightings, channel mix shifts, and near-term demand signals that are hard to see cleanly in public datasets.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | |

| Mid tier: 45% | Functional/Unit leaders: 38% | |

| Smaller Players: 19% | Managers: 44% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where Europe demand is reconstructed from country-level consumption patterns, processed meat production indicators, and trade flows, and then the totals are reconciled back to value using realistic price ladders. To keep the model practical, we treated the market as a combination of chilled processed meat and frozen processed meat, and then checked that the split matched what industry participants see in shelves and foodservice menus.

To corroborate results, selective bottom-up approximations were run in parallel, such as sampled price per kilogram by product group multiplied by estimated category volumes, followed by channel checks for supermarkets, convenience stores, and online retail. Where company disclosures did not separate processed meat cleanly, gaps were handled by using peer benchmarks and applying conservative allocation keys that were validated through interviews. For forecasting, scenario analysis was used because cost inflation, consumer downtrading, and policy changes can move demand in different directions, and then each scenario was anchored to a small set of measurable inputs.

Key model inputs included processed meat price inflation versus overall food CPI, pork and poultry input cost direction, retail private label share shifts, cold-chain and packaging cost trends, and trade balance movements for prepared or preserved meat categories. When these signals moved in ways that did did not fit reported consumption behavior, assumptions were revisited until the story aligned with what respondents described and what public statistics can support.

Data Validation & Update Cycle

Outputs were checked at multiple steps so the final totals stay consistent with reality at both country and Europe-wide levels. We compared the modeled value trend against independent signals like category consumption direction, trade unit values, and inflation-adjusted pricing, and then investigated any sharp swings before sign-off.

A second analyst review is used to challenge scope, key assumptions, and any outliers that show up when country numbers are rolled up. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, disruption to meat supply, or large price shocks. Before delivery, a fresh pass is completed to ensure the market size and narrative reflect the latest available information.

Mordor Intelligence's Europe Processed Meat Market Size Compared Against Other Published Estimates

Published market sizes for Europe processed meat do not always match, even when they appear to describe the same industry, because the category boundary and pricing basis can shift the final number quite a lot. Differences also come from whether a source is closer to retail spend, wholesale value, or a mixed value definition, and from how countries outside the EU are treated in the roll-up.

By tracking price basis and refresh timing, Mordor Intelligence keeps the Europe processed meat total aligned to the chilled and frozen processed meat scope instead of blending in adjacent fresh categories or using wholesale-only valuation assumptions. In practice, the biggest gaps usually come from what gets counted as processed meat, whether foodservice and retail are combined consistently, and how currency conversion timing is handled when values are reported in USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.63 B (2026) | |

| Trade Data Publisher A | USD 147.80 B (2024) | Uses nominal wholesale pricing and a trade and consumption aggregation lens, which typically inflates value versus a defined packaged chilled and frozen processed meat market boundary. |

| Industry Research Outlet B | USD 54.47 B (2024) | Applies a broader product list and a different starting year, and it can mix multiple regions in the framing, which can shift what is included under Europe and how value is counted. |

The spread across sources is mainly explained by pricing basis (wholesale versus category value), the exact definition of processed meat, and whether Europe is treated as EU-only or a wider geography that includes additional countries. When scope rules are stated clearly and checks are run against production, trade, and price signals, the resulting estimate becomes easier to reproduce and more usable for planning.

Key Questions Answered in the Report

What is the current value of the Europe processed meat market?

The Europe processed meat market size is USD 39.63 billion in 2026 and is projected to reach USD 43.82 billion by 2031.

Which meat type leads sales in Europe?

Pork dominates, accounting for 43.78% of 2025 revenue, though beef is the fastest-growing segment at 4.48% CAGR to 2031.

How are convenience trends influencing product development?

Rising urban lifestyles favor ready-to-eat and portion-controlled formats, driving packaging innovation and boosting chilled and frozen sub-categories.

Why is vacuum packaging gaining traction in Europe?

Vacuum packs cut food waste and can extend shelf life up to 21 days, supporting retailers’ sustainability goals and export logistics.

Page last updated on: