Cryogenic Process Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

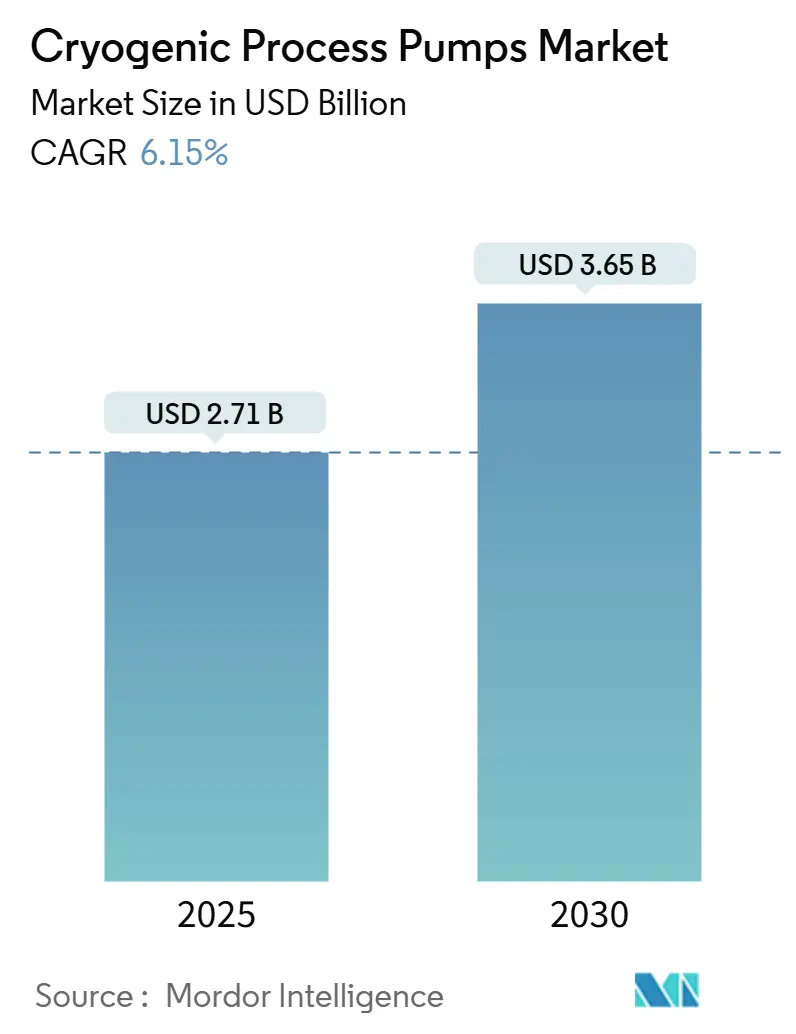

| Market Size (2025) | USD 2.71 Billion |

| Market Size (2030) | USD 3.65 Billion |

| Growth Rate (2025 - 2030) | 6.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryogenic Process Pumps Market Analysis by Mordor Intelligence

The Cryogenic Process Pumps Market size is estimated at USD 2.71 billion in 2025, and is expected to reach USD 3.65 billion by 2030, at a CAGR of 6.15% during the forecast period (2025-2030).

Robust capital deployment in liquefied natural gas (LNG) facilities, green-hydrogen hubs, and semiconductor fabs drives this expansion. Demand stems from cleaner energy goals, industrial decarbonization mandates, and manufacturing technologies that depend on ultra-pure cryogens. The Asia-Pacific region anchored 37.80% of global revenue in 2024, as China, Japan, and South Korea accelerated their hydrogen and LNG build-outs. Centrifugal pump designs captured 61.90% market share the same year, reflecting their reliability in high-volume transfer duties. Hydrogen-service equipment posted the fastest growth trajectory, outstripping traditional LNG projects. The June 2025 merger between Chart Industries and Flowserve produced a USD 19 billion flow-technology leader expected to intensify competition across aftermarket and project awards.

Key Report Takeaways

- By pump type, centrifugal units held 61.9% of the cryogenic process pumps market share in 2024, while reciprocating designs posted the highest 6.9% CAGR through 2030.

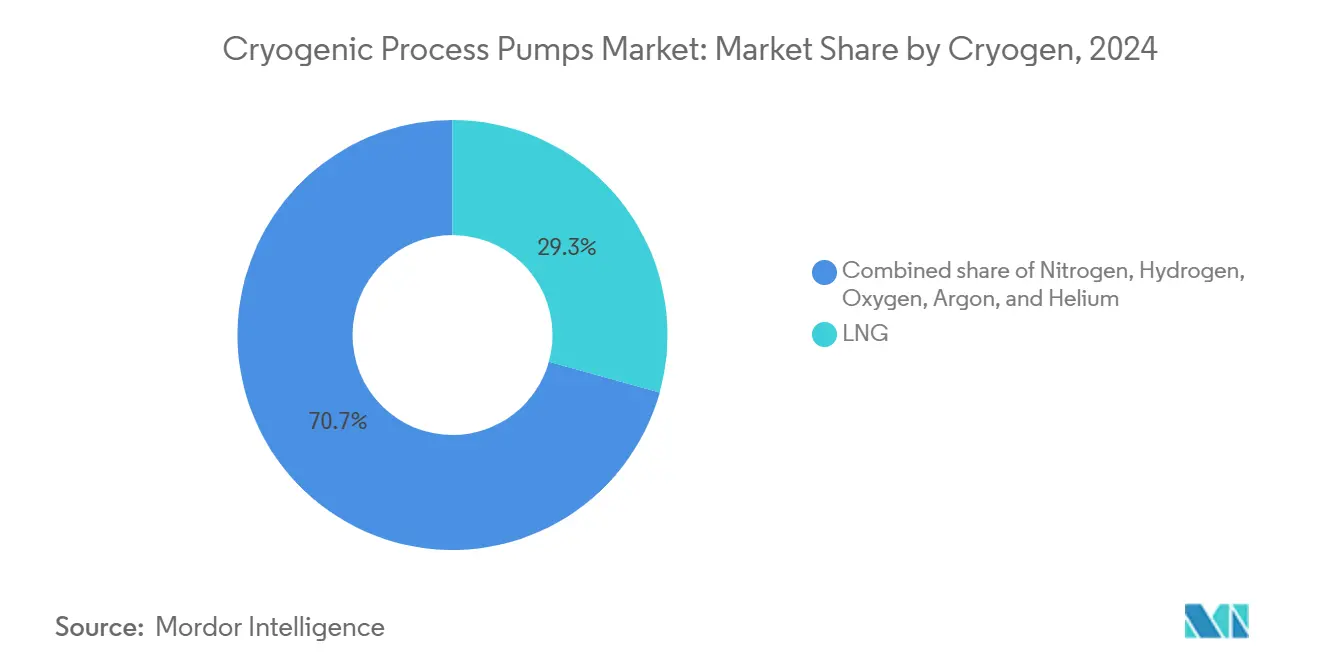

- By cryogen, LNG retained a 29.3% revenue share in 2024, whereas hydrogen pumps delivered a 10.8% CAGR to 2030.

- By application, storage-tank loading accounted for 37% of the cryogenic process pumps market size in 2024; fueling and bunkering stations advanced at a 9.7% CAGR over the same horizon.

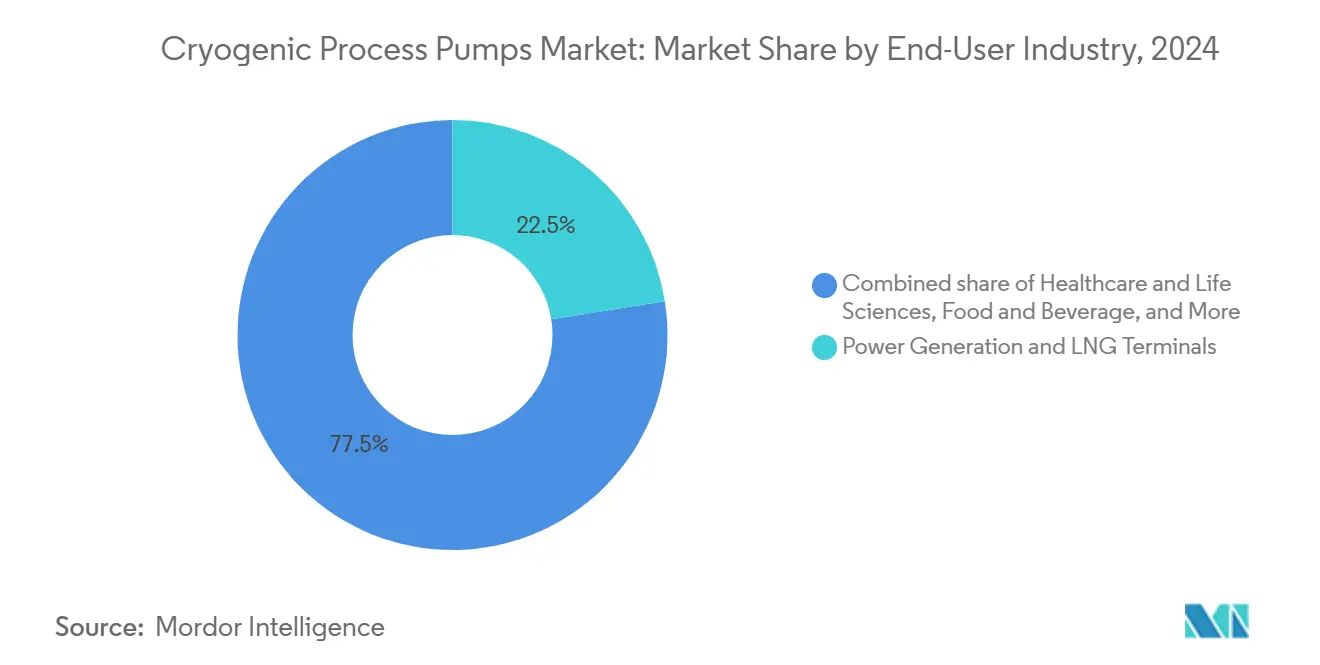

- By end-user industry, power generation and LNG terminals accounted for 22.5% of demand in 2024, while the healthcare and life sciences sector notched the fastest growth rate of 8.6% from 2024 to 2030.

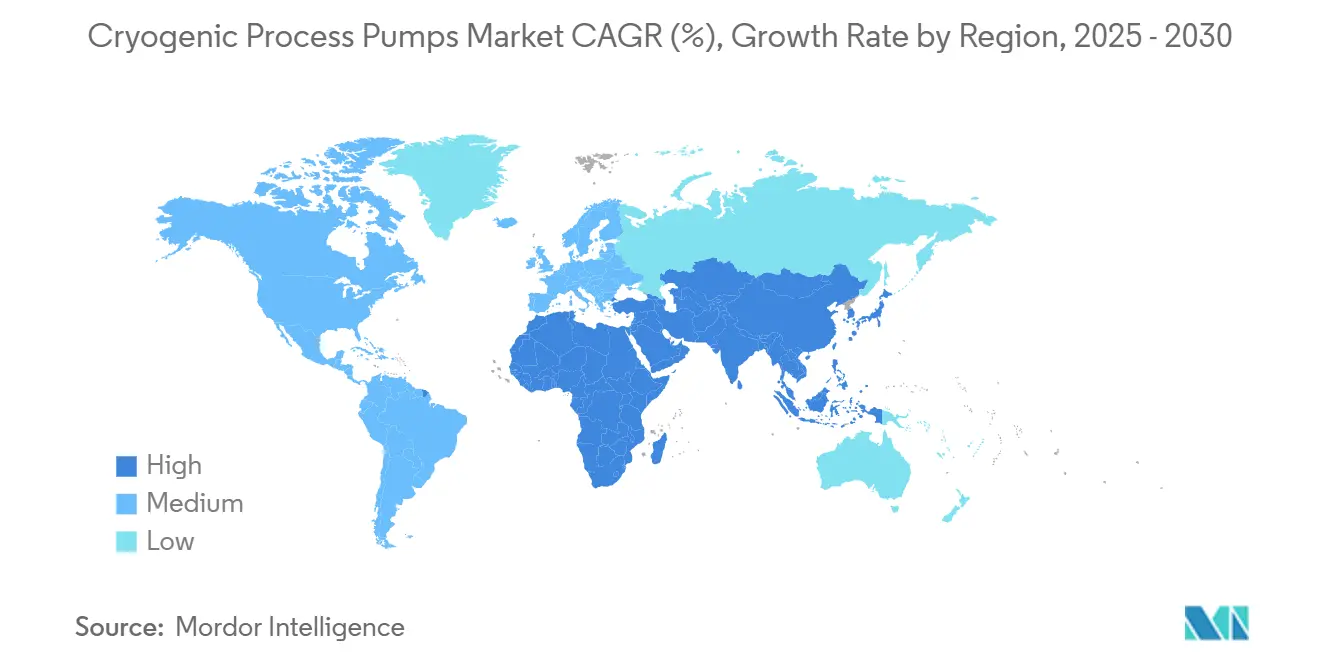

- By geography, Asia-Pacific commanded 37.8% revenue in 2024 and is set to grow at a 6.5% CAGR as China’s hydrogen pipeline and Japan’s liquid-hydrogen trials progress.

Global Cryogenic Process Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNG liquefaction build-out in emerging gas-export nations | 1.80% | Global, with concentration in Middle East, Asia-Pacific, and North America | Medium term (2-4 years) |

| Ramp-up of green hydrogen hubs requiring LH2 transfer pumps | 1.50% | Europe, North America, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Industrial gas recovery mandates boosting nitrogen-service pumps | 0.90% | Global, with early adoption in North America and EU | Short term (≤ 2 years) |

| Semiconductor fabs' sub-10 nm node investments (ultra-pure argon) | 0.70% | Asia-Pacific core, with expansion to North America | Medium term (2-4 years) |

| Ship-to-ship LNG bunkering regulations (IMO 2020/2030) | 0.60% | Global maritime routes, concentrated in major shipping lanes | Short term (≤ 2 years) |

| AI-data-center liquid-cooling adoption driving LN₂ demand | 0.40% | North America, Europe, with emerging presence in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LNG Liquefaction Build-out in Emerging Gas-Export Nations

Global LNG capacity additions underpin a 1.8 percentage-point uplift in the long-term CAGR. Qatar’s fifth natural-gas-liquids train, the UAE’s Ruwais LNG complex, and U.S. Gulf Coast mid-scale projects all require pumps able to handle –162 °C methane streams while operating in corrosive coastal environments. Equipment orders awarded to multi-train facilities validate sustained procurement pipelines for high-flow centrifugal machines. Operators are increasingly specifying variable-speed drives and predictive-maintenance sensors to reduce operating expenses and methane slip. Electrically driven liquefaction plants powered by renewables, such as those operated by Texas LNG, signal an industry shift toward lower Scope 1 emissions. These electrification strategies increase demand for low-vibration cryogenic pumps that are compatible with high-frequency motor controls.

Ramp-up of Green-Hydrogen Hubs Requiring LH₂ Transfer Pumps

Europe’s IPCEI Hy2Infra and Germany’s €4.6 billion hydrogen plan collectively stimulate over 3 GW of electrolyser builds, each tied to liquid-hydrogen storage and transport networks. With liquid hydrogen stored at –253 °C, transfer equipment must integrate advanced insulation, Invar or austenitic stainless-steel components, and vacuum-jacketed casings. EBARA’s full-scale LH₂ test facility, commissioned in 2024, showcases industry readiness to validate flow dynamics at sub-20 K conditions.[1]EBARA Corporation, “Full-Scale Liquid Hydrogen Pump Test Facility,” ebara.co.jpAsian OEMs, such as Nikkiso, have secured contracts for more than 20 LH₂ stations, revealing the early commercialization of liquid-hydrogen mobility.

Industrial-Gas Recovery Mandates Boosting Nitrogen-Service Pumps

EPA Subpart OOOOb requires zero-emission designs for new U.S. natural-gas facilities, thereby increasing demand for nitrogen-purging and blanketing systems.[2]Environmental Protection Agency, “Subpart OOOOb Final Rule,” epa.gov Semiconductor cleanroom expansions worth more than USD 100 billion annually require ultra-pure nitrogen delivery below 0 °C to support cryogenic etching and deposition. Updated safety guidelines from the European Industrial Gases Association tighten performance criteria for reciprocating pumps handling oxygen, argon, and nitrogen. These rules spur procurement of oil-free, contamination-resistant units capable of continuous duty in high-purity environments.

Semiconductor Fabs’ Sub-10 nm Node Investments (Ultra-Pure Argon)

The IEEE 2023 IRDS roadmap lists cryogenic electronics as a foundation for next-generation computing, reinforcing the need for argon circulation with a purity of greater than 99.999% at temperatures approaching those of liquid nitrogen.[3]IEEE, “2023 IRDS Cryogenic Electronics Roadmap,” ieee.orgLow-temperature transistor switching trials demonstrate 4× voltage cuts that can halve server power draw, thereby increasing liquid-argon demand across data centers. Fundamental science projects, such as the Deep Underground Neutrino Experiment, rely on 68,400 tons of argon, highlighting logistics challenges that can only be solved by high-capacity centrifugal pumps. Process-tool innovators, therefore, partner with pump suppliers to minimise vibration-induced wafer defects.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Helium supply volatility elevating CAPEX risk for transfer systems | -1.20% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| High OPEX of submerged motors in LNG peak-shaving plants | -0.80% | Asia-Pacific, North America, with emerging concerns in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Helium Supply Volatility Elevating CAPEX Risk for Transfer Systems

Global helium markets are facing structural shortages as historical stockpiles deplete and new liquefaction trains struggle to meet demand. Many laboratories receive only 45-65% of ordered volumes, prompting life-science and semiconductor facilities to redesign cryogenic loops and invest in more efficient pumps.[4]Peak Scientific, “Helium Shortage Impact on Labs,” peakscientific.com The U.S. Federal Helium Reserve's drawdown compounds import exposure, while the European Commission lists helium on its agenda of critical raw materials. Procurement team, therefore, encounters higher upfront costs and longer lead times for helium-qualified pump assemblies.

High OPEX of Submerged Motors in LNG Peak-Shaving Plants

LNG peak-shaving installations rely on submerged-induction motors whose maintenance cycles drive power bills and downtime. Process-simulation studies published in the Journal of Natural Gas Science and Engineering confirm that pump-hydraulic upgrades can reduce overall liquefaction energy consumption by 7-10%. Operators weigh the costs of retrofitting against potential savings, which dampens short-term pump orders but opens avenues for high-efficiency replacements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Dominance Drives Innovation

Centrifugal units commanded 61.90% of the cryogenic process pumps market size in 2024 and are forecast to expand at a 6.90% CAGR toward 2030. Continuous-flow architecture is well-suited for LNG baseload terminals and industrial gas pipelines that require low-maintenance, high-throughput operations. Research presented at the AIP Conference reported a 46% reduction in boil-off heat input when composite impellers replace conventional alloys.

Product developers are now exploring magnetic-bearing and composite-shaft assemblies that permit 25,000 rpm operation without lubrication, thereby enhancing mean-time-between-failure metrics. Reciprocating pumps are used for specialised duties, such as high-pressure hydrogen dispensing, where accurate metering is more important than flow volume. Screw, rotary-vane, and cryogenic-vacuum pumps service ultra-high-vacuum environments in semiconductor lithography and space simulation chambers. Their collective market presence supports diversification but does not threaten centrifugal leadership through 2030.

By Cryogen: Hydrogen Applications Accelerate Market Transformation

Hydrogen generated just 16.50% of the revenue in 2024, yet is projected to grow at a 10.80% CAGR, the swiftest among all cryogens. LNG accounted for 29.30% of global turnover that same year, benefiting from brownfield export-terminal debottlenecking. Hydrogen’s ascent tracks Europe’s Hydrogen Bank auctions and Asia’s mobility pilots, all of which require pumps tolerant to –253 °C and hydrogen embrittlement.

Technical papers in ACS Omega report process-energy cuts to 9.82 kWh/kg LH₂ with nitrogen precooling stages, indicating larger pump capacities per tonne of liquefied hydrogen. Magnetocaloric prototypes under test at European institutes could shrink specific energy by an additional 20-50%, creating fresh design parameters for future pump generations. Nitrogen remains vital to semiconductor batch processes and industrial-gas reclamation, whereas argon and helium sustain growth in research and medical imaging.

By Application: Fueling Infrastructure Drives Growth Acceleration

Storage-tank loading tasks accounted for 37% of global revenue in 2024, underscoring the dependence of LNG and industrial-gas hubs on reliable bulk transfer. Yet fueling and bunkering stations are expected to log a brisk 9.70% CAGR through 2030 as shipping lines and heavy-duty fleets adopt low-carbon fuels. IMO mandates that phase-in of greenhouse-gas pricing around 2027 will push ports to install high-flow LNG equipment, and, longer term, liquid-hydrogen nozzles.

The U.S. Bipartisan Infrastructure Law allocates USD 623 million for hydrogen-refueling networks, with Texas alone receiving USD 70 million, signalling pipeline growth for pump orders. Emerging projects such as DelHyVEHR target 5 t/h LH₂ dispensing, exceeding current flow-rate limits and driving engineering innovation in cavitation control and nozzle-temperature management. Beyond mobility, pipeline-boosting and cylinder-filling services supply industrial gases to metallurgy, food processing, and medical oxygen chains, safeguarding baseline demand.

By End-User Industry: Healthcare Sector Emerges as Growth Leader

Power generation and LNG terminals accounted for 22.50% of 2024 revenue, while healthcare and life sciences are poised to grow at an 8.60% CAGR through 2030. MRI magnets rely on helium-filled cryostats that must be continuously replenished; helium shortages therefore stimulate investment in recovery loops and high-efficiency pumps. The semiconductor segment, facing a USD 109 billion equipment outlay in 2024, commands argon and nitrogen volumes that require oil-free, particle-free circulation.

Chemical and petrochemical operators are adopting nitrogen purging to meet volatile organic compound regulations, thereby further increasing pump installation counts. Aerospace projects, including NASA’s methane-oxygen propulsion trials for lunar-gateway objectives, test turbopumps operating at pressures exceeding 100 bar discharge. Each of these verticals reduces the market's reliance on energy-sector CAPEX, thereby strengthening long-term growth fundamentals.

Geography Analysis

Asia-Pacific dominated the cryogenic process pumps market with a 37.80% share in 2024 and is projected to maintain a 6.50% CAGR through 2030. China’s 20 billion-yuan green-hydrogen corridor linking Ulanqab to Beijing underpins extensive pipeline and pump procurement. Japan advances large-scale liquid-hydrogen supply trials scheduled for commercial operation by 2030, reinforcing regional demand for –253 °C equipment.

Europe follows as a regulatory frontrunner, channeling EUR 6.9 billion in state aid to trans-border hydrogen networks that will install 2,700 km of pipelines and 3.2 GW of electrolysers. This policy certainty encourages OEMs to localise manufacturing and service facilities across Germany, France, and the Netherlands. The EU F-gas phase-down and methane-emission caps also prompt LNG terminals to modernize their pumps with near-zero leakage configurations.

North America benefits from LNG export terminal debottlenecks along the Gulf Coast and federal clean hydrogen tax incentives. Projects such as Cedar LNG utilize renewable-powered E-drive liquefaction, which requires variable-speed centrifugal pumps. The Middle East is leveraging its massive gas reserves to add low-carbon LNG capacity, with the UAE’s Ruwais complex and Qatar’s North Field expansions requiring high-duty cryogenic equipment. Africa and Latin America, although smaller today, continue to attract early-stage investments in floating storage and regasification units, which will open new pump-replacement cycles after 2028.

Competitive Landscape

Market consolidation advanced in June 2025 when Chart Industries and Flowserve finalised a merger that formed a USD 19 billion enterprise, commanding more than 5.5 million installed assets worldwide. The union pairs Chart’s cryogenic storage and vaporization heritage with Flowserve’s sealing and actuation portfolio, creating a one-stop offering for LNG, hydrogen, and industrial gas operators. Approximately 42% of combined revenue now originates from aftermarket services, ensuring predictable cash flows.

Alfa Laval closed its acquisition of Fives Energy Cryogenics in July 2025, gaining brazed-aluminium heat-exchanger and cryogenic-pump technologies that complement its plate-heat-exchanger range. Nikkiso continued portfolio expansion by purchasing Germany’s Cryotec Anlagenbau in 2024, securing process-plant expertise and European service hubs. EBARA’s 16 billion-yen LH₂ test centre underscores the intensity of the R&D race as OEMs chase super-low-temperature endurance and hydrogen embrittlement resistance.

Technological differentiation centers on composite materials, magnetic bearings, and digital twin diagnostics. OEMs prioritise vibration suppression to protect downstream valves and meters, while customers demand rapid spare part fulfillment and field service coverage. Medium-sized specialists in vacuum and niche-gas pumps find growth by licensing proprietary hydraulics to larger integrators or forming joint ventures for regional assembly.

Cryogenic Process Pumps Industry Leaders

Nikkiso Co. Ltd.

Atlas Copco AB

Ebara Corporation

Sulzer Ltd.

Flowserve Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Alfa Laval finalized the purchase of Fives Energy Cryogenics, adding cryogenic-pump and aluminium-heat-exchanger expertise to its clean-energy portfolio.

- June 2025: Chart Industries and Flowserve completed an all-stock merger, creating a USD 19 billion flow-technology leader with USD 3.7 billion in annual aftermarket revenue.

- March 2025: Cheniere Energy brought Train 1 of Corpus Christi Stage 3 online, marking the first LNG cargo from seven mid-scale trains exceeding 10 MTPA capacity.

- January 2025: Flowserve won a contract to supply supercritical CO₂ pumps and seals for ADNOC’s 1.5 Mt/y carbon-capture initiative in the UAE.

Global Cryogenic Process Pumps Market Report Scope

Cryogenic process pumps are vacuum pumps that capture gases and vapors by condensing them on a cold surface. However, they are only effective on certain gases. The efficacy is determined by the freezing and boiling points of the gas in relation to the temperature of the cryopump.

The cryogenic process pumps market is segmented by type, cryogen, end-user, and geography. By type, the market is segmented into dynamic pump and positive displacement pump; by cryogen, the market is segmented into nitrogen, argon, oxygen, LNG, hydrogen, and others; and by end-user, the market is segmented into power generation, chemical, healthcare, and others. The report also covers the market size and forecasts for the cryogenic process pumps market across major countries. For each segment, the market sizing and forecasts have been done based on revenue in USD billions.

| Centrifugal (Dynamic) |

| Reciprocating (Positive-Displacement) |

| Screw and Rotary Vane |

| Entrapment/Cryo-Vacuum |

| LNG (CH₄) |

| Nitrogen (LN₂) |

| Oxygen (LOX) |

| Argon (LAr) |

| Hydrogen (LH₂) |

| Helium (LHe) |

| Storage Tank Loading |

| Pipeline Boosting and Transfer |

| Fueling and Bunkering Stations |

| Cylinder Filling |

| Power Generation and LNG Terminals |

| Chemical and Petrochemical |

| Healthcare and Life-Sciences |

| Electronics and Semi-conductor |

| Metals and Metallurgy |

| Food and Beverage |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Pump Type | Centrifugal (Dynamic) | |

| Reciprocating (Positive-Displacement) | ||

| Screw and Rotary Vane | ||

| Entrapment/Cryo-Vacuum | ||

| By Cryogen | LNG (CH₄) | |

| Nitrogen (LN₂) | ||

| Oxygen (LOX) | ||

| Argon (LAr) | ||

| Hydrogen (LH₂) | ||

| Helium (LHe) | ||

| By Application | Storage Tank Loading | |

| Pipeline Boosting and Transfer | ||

| Fueling and Bunkering Stations | ||

| Cylinder Filling | ||

| By End-User Industry | Power Generation and LNG Terminals | |

| Chemical and Petrochemical | ||

| Healthcare and Life-Sciences | ||

| Electronics and Semi-conductor | ||

| Metals and Metallurgy | ||

| Food and Beverage | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current cryogenic process pumps market size?

The market was valued at USD 2.71 billion in 2025 and is projected to reach USD 3.65 billion by 2030.

Which pump type leads global sales?

Centrifugal pumps held 61.90% of 2024 revenue owing to their suitability for high-volume LNG and industrial-gas duties.

Which cryogen represents the fastest-growing opportunity?

Liquid hydrogen pumps are forecast to expand at 10.80% CAGR through 2030 as green-hydrogen hubs scale.

Which application segment is expected to grow fastest to 2030?

Fueling and bunkering stations are set to record a 9.70% CAGR, driven by maritime and heavy-duty transport decarbonization.

Why is helium supply a concern for pump buyers?

Helium shortages force laboratories and fabs to pay higher prices and invest in efficient transfer systems, exerting –1.2% drag on overall market CAGR.

How concentrated is the supplier landscape?

A concentration score of 6 suggests the top five OEMs account for roughly two-thirds of revenue, with mid-sized specialists retaining notable niche influence.

Page last updated on: