Crown Caps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

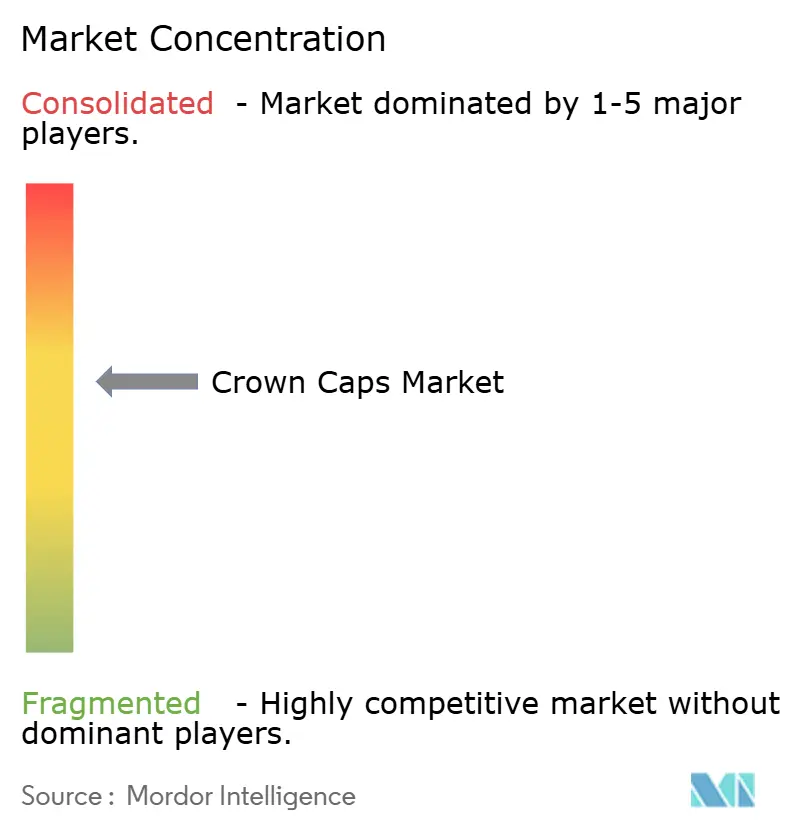

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crown Caps Market Analysis by Mordor Intelligence

The crown caps market size is expected to grow from USD 1.79 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.33 billion by 2031 at 4.48% CAGR over 2026-2031. Rising craft-beer production, premium glass packaging uptake, and liner technology upgrades continue to unlock new demand pockets. Leading suppliers focus on lightweight aluminum variants and PVC-free liners that anticipate regulatory tightening, while smart closures with QR or NFC functionality strengthen brand engagement and anti-counterfeiting defenses. At the same time, producers face intensified competition from PET bottles fitted with plastic screw caps, along with margin pressure stemming from tin-plate and aluminum price swings. Nonetheless, the superior tamper-evidence, carbonation retention, and high-speed line compatibility of metal crowns keep them entrenched across beverage, food, and pharmaceutical channels.[1]Glass Packaging Institute, “Glass Container Shipment Report,” gpi.org

Key Report Takeaways

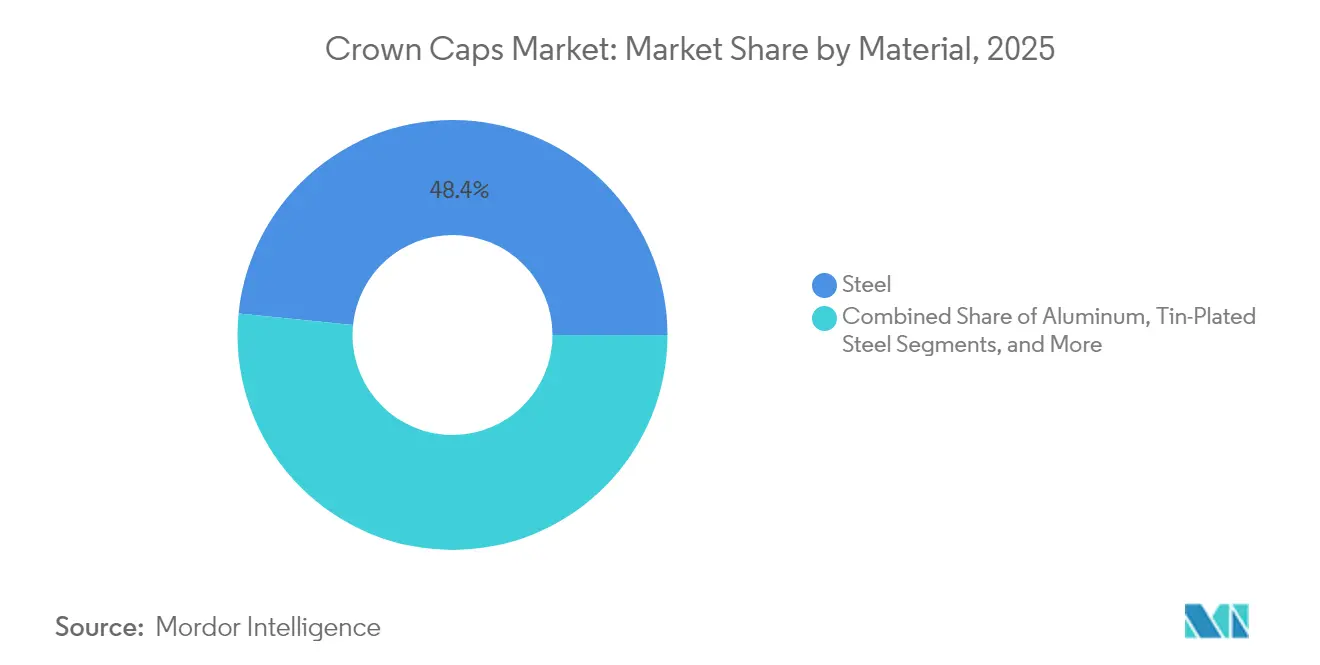

- By material, steel led with 48.40% of the crown caps market share in 2025; aluminum is projected to grow at a 5.56% CAGR through 2031.

- By closure type, pry-off closures captured 61.75% of the crown caps market size in 2025, while twist-off variants are expected to expand at a 5.89% CAGR between 2026-2031.

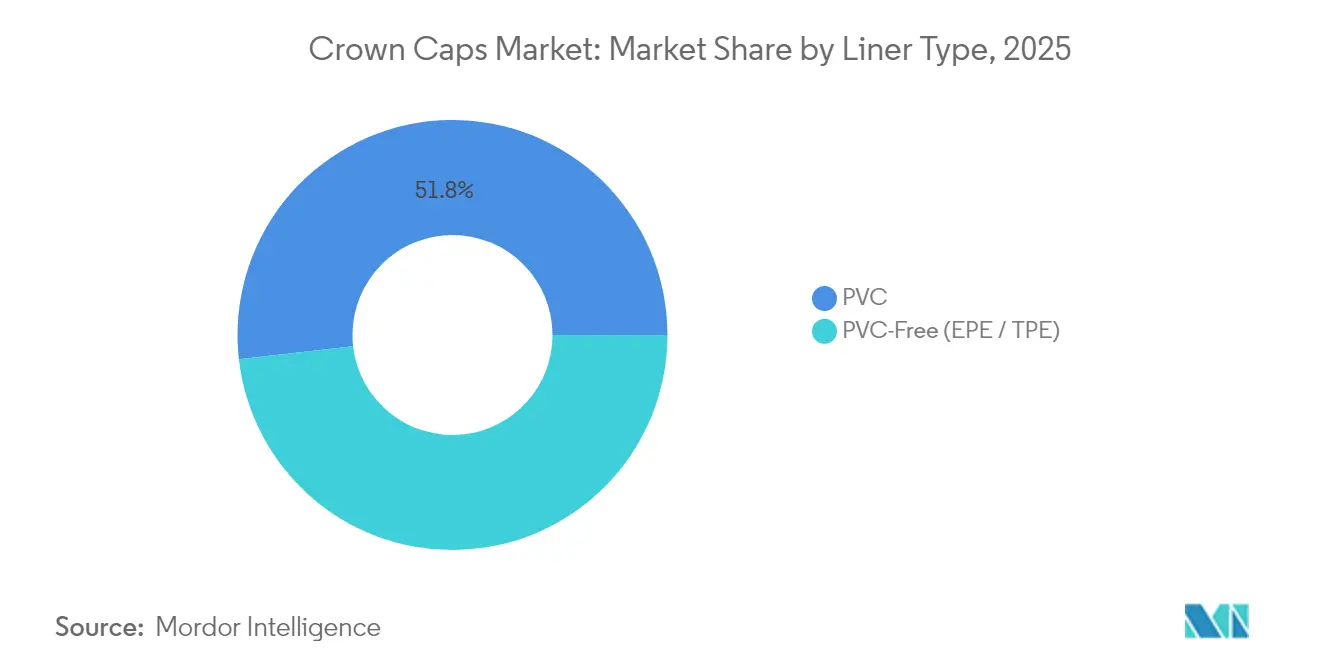

- By liner type, PVC accounted for 51.80% of the 2025 crown caps market size; PVC-free liners are forecast to post a 6.01% CAGR to 2031.

- By application, beverages dominated with a 61.95% share of the crown caps market size in 2025, whereas pharmaceuticals and nutraceuticals are advancing at a 5.87% CAGR through 2031.

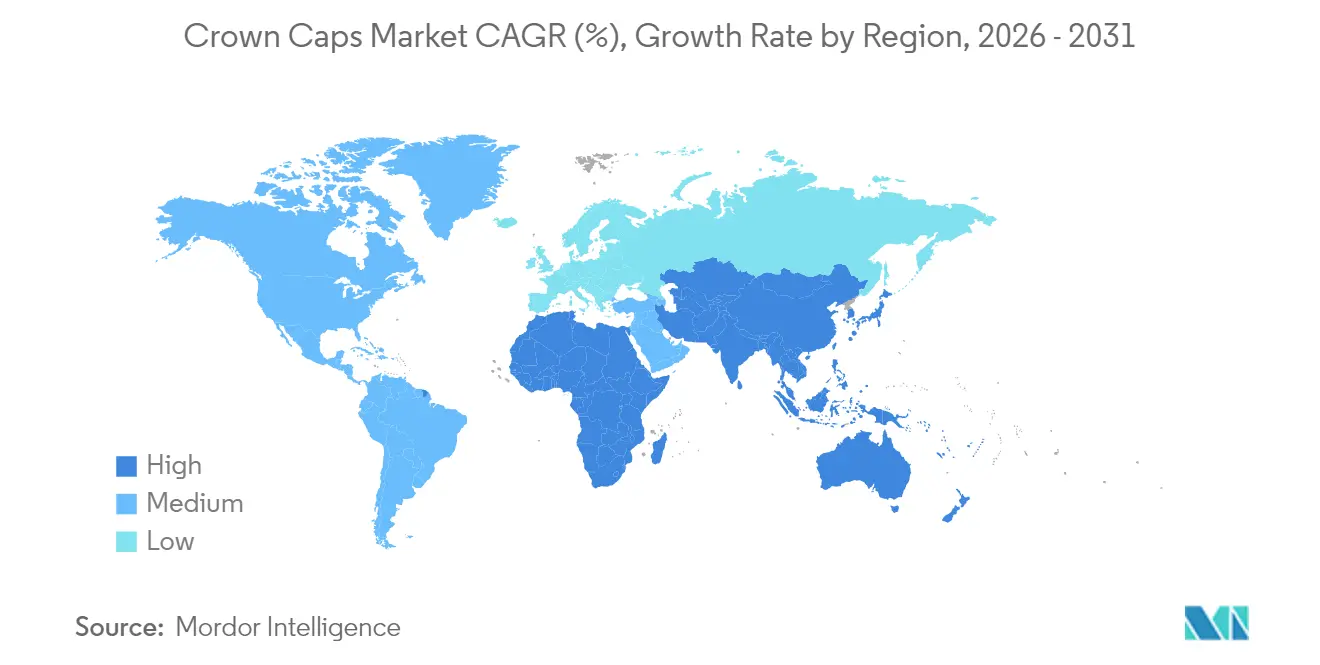

- By geography, Asia-Pacific held 40.10% of the crown caps market share in 2025 and is also the fastest-growing region at 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Crown Caps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising craft-beer micro-brewery expansion | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Regulation-driven shift toward PVC-free liners | +0.8% | Global, with EU and North America leading | Long term (≥ 4 years) |

| Resurgence of glass packaging in premium beverages | +0.9% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Interactive QR-coded crown caps boost brand engagement | +0.4% | North America & Europe initially | Short term (≤ 2 years) |

| Emerging demand from kombucha and functional drinks | +0.6% | Global, with North America and APAC leading | Medium term (2-4 years) |

| Advanced tamper-evident cap designs | +0.5% | Global, pharmaceutical focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Craft-Beer Micro-Brewery Expansion

More than 9,000 breweries operated in the United States in 2024, up 15% from 2023, and nearly all specify pry-off metal crowns because they seal carbonation reliably at small batch scales.[2]Brewers Association, “National Beer Sales & Production Data,” brewersassociation.org European microbreweries in Germany, Belgium, and the United Kingdom mirror this momentum, prompting converters to develop custom-printed crowns that preserve unique flavor profiles. As taproom-to-retail distribution widens, microbrewers demand liners with tighter oxygen transmission rates and overt tamper evidence. The segment’s premium-priced offerings also justify the adoption of lightweight aluminum to reinforce sustainability claims and shelf impact.

Regulation-Driven Shift Toward PVC-Free Liners

Global food-contact legislation is accelerating the migration from PVC to EPE or TPE liners. The FDA’s ongoing reassessment of plasticizers and the European Union’s Packaging and Packaging Waste Regulation (PPWR) push beverage brands to phase in recyclable, non-chlorinated solutions. The transition entails production line retrofits, resin validation, and higher raw material outlays, yet early adopters secure premium positioning with compliant, eco-friendly closures. Over the forecast period, suppliers that scale PVC-free capacity are expected to gain share as regulators heighten enforcement and brand owners expand life-cycle auditing.

Resurgence of Glass Packaging in Premium Beverages

Glass bottle shipments for alcoholic drinks grew 12% year on year in 2024, driven by premiumization and sustainability narratives that resonate with affluent consumers. Crown caps complement glass through superior CO₂ retention and heritage aesthetics, especially for seasonal craft spirits and artisanal sodas priced 20-30% above plastic counterparts. Premium food brands also leverage glass plus metal crowns to convey authenticity. As a result, demand for decorative crowns with embossing and color-matched shellac is accelerating, especially in limited-edition launches.

Interactive QR-Coded Crown Caps Boost Brand Engagement

Smart crowns transform closures into digital touchpoints. Early deployments by Coca-Cola show consumers willingly scanning personalized QR codes to unlock promotions, generating valuable behavioral data, and reinforcing loyalty programs. Implementation requires inline, high-resolution printing and vision systems that verify code readability. Over time, declining electronics costs and near-universal smartphone adoption will spread QR or NFC crowns from premium beverages into mainstream SKUs, creating ancillary revenue streams linked to direct-to-consumer marketing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight PET bottles with plastic screw caps | -1.1% | Global, particularly Asia-Pacific | Short term (≤ 2 years) |

| Volatility in tin-plate and aluminum pricing | -0.7% | Global, with manufacturing concentration in Asia | Medium term (2-4 years) |

| Policy push against single-use metal closures | -0.6% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Penetration of ring-pull crowns in ASEAN breweries | -0.4% | Southeast Asia, spillover to broader APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lightweight PET Bottles with Plastic Screw Caps

Bottle manufacturers now deliver PET packs that weigh 60-70% less than comparable glass containers and integrate tethered screw caps that satisfy the EU Single-Use Plastics Directive, eroding cost-conscious segments traditionally served by metal crowns. PET’s logistics savings and improved barrier resins increasingly threaten the carbonated soft drink niche, especially in emerging economies where freight expenses dominate value chains. Crown cap suppliers mitigate the substitution risk by emphasizing heritage aesthetics, recyclability, and premium positioning that PET struggles to replicate.

Volatility in Tin-Plate and Aluminum Pricing

Aluminum spot prices swung 25-30% during 2024, while tin-plate availability tightened amid geopolitical disruptions, compressing converter margins. Smaller players without long-term hedging contracts find it difficult to pass cost spikes through to annual beverage tenders. Currency fluctuations further complicate multi-regional sourcing, prompting consolidation moves-such as Sonoco’s USD 3.87 billion purchase of Eviosys-to secure backward integration and purchasing leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Dominance Faces Aluminum Challenge

Steel retained 48.40% share of the crown caps market in 2025 due to its low cost and robustness on high-speed lines. The crown caps market size attributed to steel will edge higher but cede mix to aluminum, whose 5.56% brand lightweighting targets and superior corrosion resistance fuel CAGR. Aluminum recyclability and premium aesthetics appeal to craft distillers that command price premiums covering the material differential. Suppliers experiment with 3104 and 5052 alloys that lower shell mass by up to 20% without compromising cap rigidity.

Second-tier materials such as tin-plated steel serve niche segments requiring glossy finishes or elevated barrier performance but face price sensitivity amid raw-material volatility. Hybrid designs that marry a steel inner shell with an aluminum skirt are emerging to balance cost with shelf appeal. Over the forecast horizon, material evolution may hinge on cradle-to-cradle audits by major beverage groups, making post-consumer scrap recovery rates a critical differentiator.

By Closure Type: Twist-Off Innovation Accelerates

Pry-off variants commanded 61.75% share in 2025, reflecting entrenched use in mainstream beer markets. Yet twist-offs are projected to outpace at 5.89% CAGR as aging demographics value easy opening and as premium non-alcoholic brands adopt resealability to support multi-serve consumption occasions. The crown caps market embraces thread-forming technologies that maintain seal pressure across repeated openings and closings. Investment in precision die sets and vision inspection drives unit costs higher, but converters recoup through product differentiation and value-added fees.

Hybrid formats combining twistability with overt tamper bands seek to satisfy regulatory scrutiny in pharmaceuticals. Additionally, the ring-pull derivatives pilot in ASEAN breweries, positioning convenience as an alternative growth lever. Suppliers successful in this segment will integrate tooling flexibility that permits rapid changeovers between pry-off and twist-off SKUs without protracted downtime.

By Liner Type: PVC-Free Transition Gains Momentum

PVC liners still represent 51.80% of 2025 shipments thanks to proven sealing performance. However, the crown caps market is pivoting to EPE or TPE linings, which are set to expand at a 6.01% CAGR after regulators in the EU and North America flagged chloride content and plasticizer migration concerns. Early-stage capacity constraints for PVC-free compounds inflate input costs, yet beverage majors accept price trade-offs to secure compliance and avoid recall liabilities.

Suppliers emphasize linear adhesion enhancements and micro-cellular structures that deliver equal or better torque retention. R&D roadmaps also explore bio-based elastomers derived from sugarcane or algae oils, targeting a 25% carbon footprint reduction versus legacy PVC. Over time, converters with high-shear compound mixers and automated wad applicators will outcompete smaller firms reliant on manual liner punches.

By Application: Pharmaceuticals Drive Premium Growth

Beverages maintained a 61.95% share in 2025 on the back of beer, carbonated soft drinks, and emerging functional drinks. Nevertheless, pharmaceutical and nutraceutical fills are set to clock a 5.87% CAGR as regulators tighten tamper-evidence standards on OTC syrups, tinctures, and liquid supplements. The crown caps market size derived from healthcare SKUs commands premium pricing, reflecting sterility validation and 100% camera inspection requirements.

Food applications-chiefly sauces and preserves-provide steady but slower growth, while specialty chemicals and personal-care lines furnish niche demand. Diversification across end-uses shelters suppliers from beverage seasonality. Firms with clean-room production and certified ISO 15378 processes will capture the highest-margin healthcare volumes.

Geography Analysis

Asia-Pacific led with a 40.10% share in 2025, and its 7.05% CAGR makes it the largest and fastest geography within the crown caps market. Rising disposable incomes in China, India, Indonesia, and Vietnam lift per-capita beer and soft-drink consumption, while foreign direct investment into brewery build-outs underpins closure volumes. Regional converters secure supply-chain resilience by co-locating shell stamping and liner compounding near bottling hubs, minimizing freight costs and customs exposure. Government incentives in China’s eastern provinces further encourage aluminum cap manufacturing, bolstering export competitiveness.

North America retains a robust position, fueled by over 9,000 breweries and a strong craft-beer culture. Regulations pushing PVC-free liners prompt early adoption, rewarding domestic suppliers that scale compliant wads ahead of enforcement deadlines. Aluminum import volumes worth USD 4.08 billion from Canada in 2022 underscore the integrated regional metals market supporting closure production.

Europe shows stable demand, anchored by premium beverages and stringent recycling targets. Implementation of deposit-return systems sharpens focus on detachable closure waste, nudging fillers toward tethered or resealable crowns. Producers respond with shell geometry tweaks that allow post-consumer collection without compromising heritage design cues. Meanwhile, breweries in Germany and Belgium pilot ring-pull formats to enhance consumer convenience.

South America and the Middle East and Africa present emerging growth corridors. Brazil’s established beer scene underpins steady closure consumption, whereas Mexico’s tequila exports drive demand for customized, tamper-evident crowns. In Africa, urbanization accelerates bottled soda uptake, though price sensitivity fosters competition from PET. Manufacturers that localize stamping lines or partner with regional beverage groups reduce import duties and shorten lead times, building a platform for long-term penetration.

Competitive Landscape

The crown caps market exhibits moderate concentration: the top five converters control roughly 55-60% of global capacity. Crown Holdings, Pelliconi, and Nihon Closures leverage multi-continent plants, vertical tin-plate sourcing, and proprietary liner chemistries to defend share. Digital inkjet presses integrated on crown lines enable multi-sku, low-MOQs that resonate with craft beverage rollouts. Pelliconi’s 2025 AI-driven quality system cuts liner defects by 15%, signaling convergence between traditional forming operations and Industry 4.0 analytics.

M&A shapes capacity distribution: Sonoco’s USD 3.87 billion acquisition of Eviosys in March 2025 created a metal packaging platform with expanded European footprint, diversified lid formats, and improved raw-material bargaining power. Smaller, regional specialists pursue niche focuses such as embossed aluminum or ring-pull variants to avoid direct scale competition. Patent filings show heightened activity in tamper-indicative skirt scoring and moisture-activated security inks, reinforcing non-price differentiation.

Sustainability remains a battleground. Finn-Korkki achieved carbon-neutral Finnish operations in 2024 by installing 325 kWp of rooftop PV and switching to 100% fossil-free electricity. Crown Holdings announced a USD 150 million Asia-Pacific expansion that embeds PVC-free liner capability and smart code print stations. Suppliers effective at integrating life-cycle assessments, renewable energy, and digital consumer engagement into their value propositions are likely to capture premium brand contracts.

Crown Caps Industry Leaders

Crown Holdings Inc.

Pelliconi & C. SpA

Nippon Closures Co., Ltd.

Silgan Holdings Inc.

Guala Closures Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sonoco closed its EUR 3.615 billion (USD 3.87 billion) purchase of Eviosys, adding 44 plants and broadening its crown lineup for European and emerging markets.

- February 2025: Crown Holdings committed USD 150 million to new aluminum crown lines in Asia-Pacific, including integrated QR-code printing and PVC-free liner systems.

- January 2025: Pelliconi unveiled an AI-based vision module that automates liner placement inspection, cutting waste by 15% and boosting uptime.

- December 2024: Finn-Korkki declared carbon-neutral production across Finland following renewable electricity and efficiency upgrades.

Global Crown Caps Market Report Scope

Crown caps, also known as crown corks, are disposable caps for packaging food, such as sauces, vinegar, and beverages in glass bottles. These caps are similar to the pilfer-proof caps, as both products are used to seal the bottle. The study tracks the revenue generated from selling various types of crown caps provided by vendors operating in the market.

The crown caps market is segmented by material (aluminum and steel and tin-plated), application (food and beverage), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa). The market sizes and values are provided in terms of value (USD) for all the above segments.

| Aluminum |

| Steel |

| Tin-Plated Steel |

| Pry-Off |

| Twist-Off |

| PVC |

| PVC-Free (EPE / TPE) |

| Beverages | Alcoholic Beverages | Beer |

| Wine | ||

| Spirits | ||

| Non-Alcoholic Beverages | Carbonated Soft Drinks | |

| Functional and Energy Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food | ||

| Pharmaceuticals and Nutraceuticals | ||

| Other Applications | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material | Aluminum | ||

| Steel | |||

| Tin-Plated Steel | |||

| By Closure Type | Pry-Off | ||

| Twist-Off | |||

| By Liner Type | PVC | ||

| PVC-Free (EPE / TPE) | |||

| By Application | Beverages | Alcoholic Beverages | Beer |

| Wine | |||

| Spirits | |||

| Non-Alcoholic Beverages | Carbonated Soft Drinks | ||

| Functional and Energy Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food | |||

| Pharmaceuticals and Nutraceuticals | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast revenue value for the crown caps market in 2031?

Published estimates place revenue at USD 2.33 billion by 2031 on a 4.48% CAGR track.

Which region contributes the largest volume of crown caps today?

Asia-Pacific leads with 40.10% of 2025 shipments, underpinned by brewery expansions across China, India, and Southeast Asia.

Which material is gaining share fastest in crown cap production?

Aluminum crowns are advancing at a 5.56% CAGR thanks to lightweighting and superior corrosion resistance.

Why are PVC-free liners becoming important?

Global regulations and brand sustainability targets favor EPE and TPE liners that avoid chlorine content and improve recyclability.

How are smart crown caps used by beverage brands?

QR-coded or NFC-enabled crowns deliver interactive promotions, collect consumer data, and enhance anti-counterfeiting protection.

What competitive strategy helps manufacturers offset raw-material price swings?

Vertical integration, hedging contracts, and M&A-such as Sonoco’s Eviosys acquisition-secure feedstock and improve bargaining power.

Page last updated on: