Vocational Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 654.82 Billion |

| Market Size (2031) | USD 856.58 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

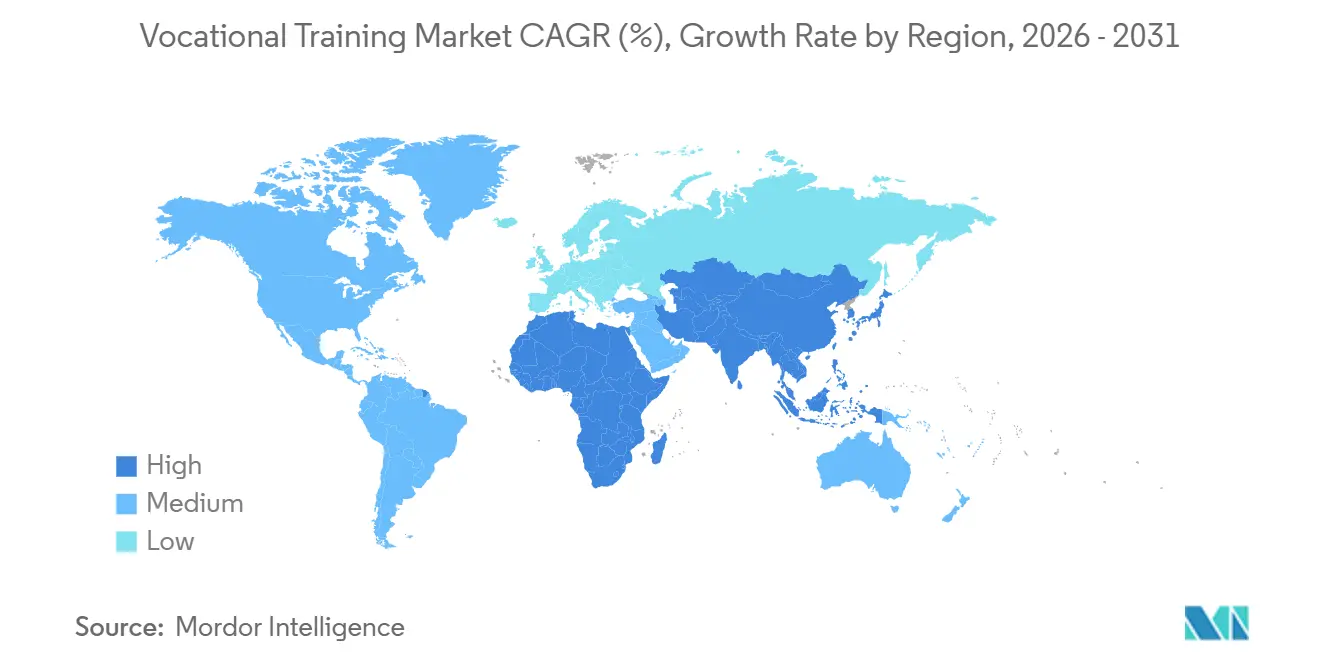

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

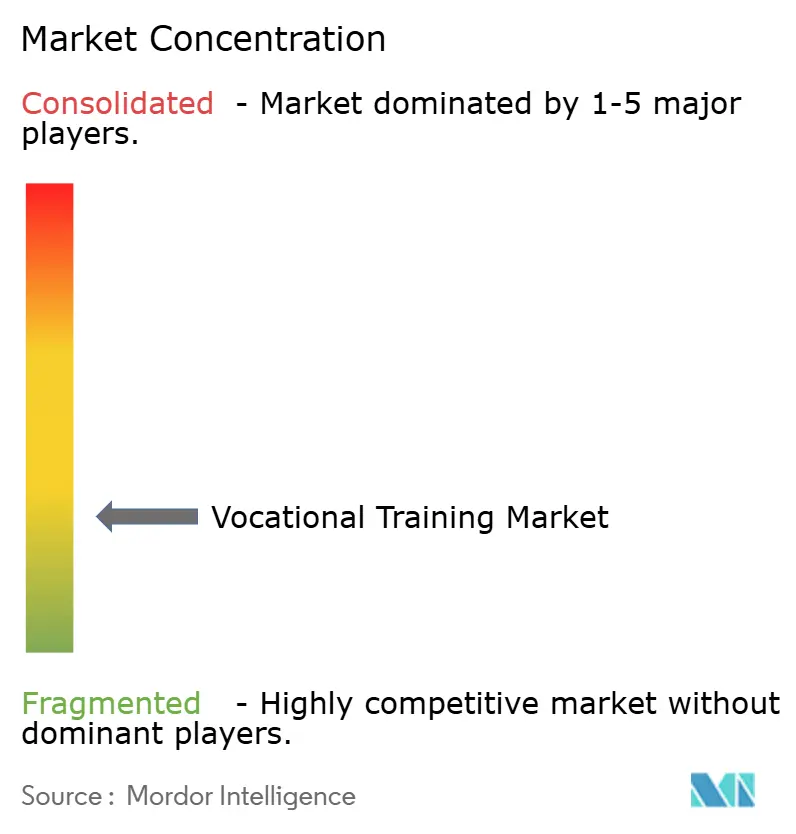

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vocational Training Market Analysis by Mordor Intelligence

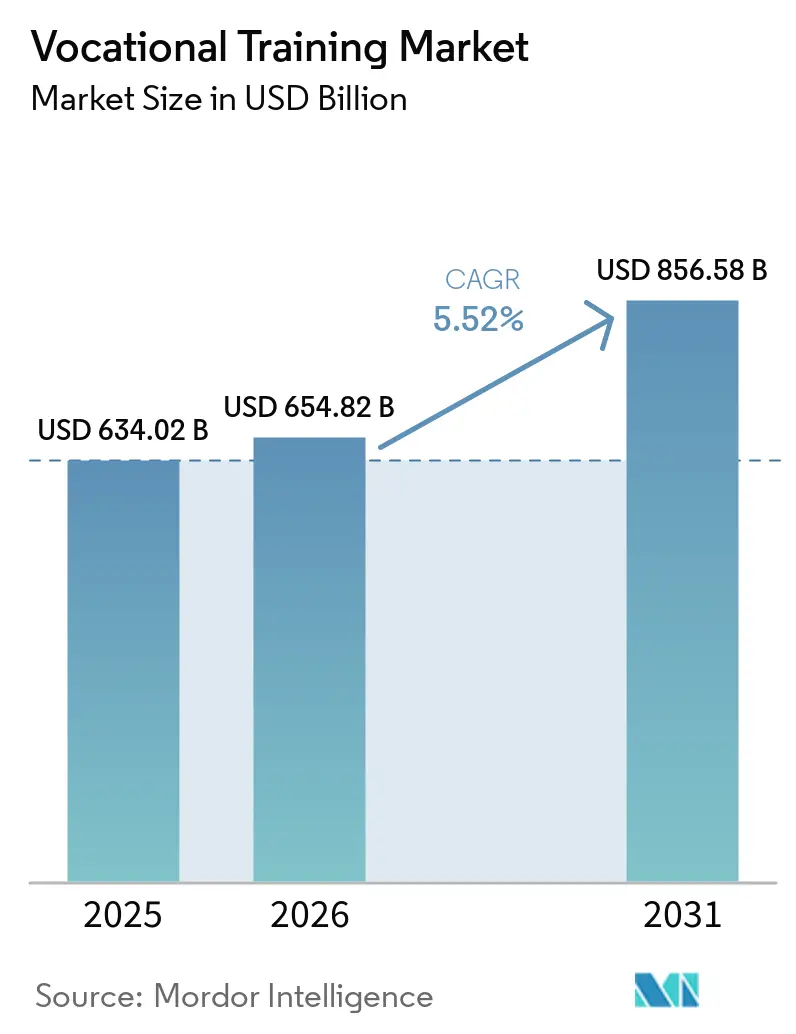

The Vocational Training Market size is expected to grow from USD 634.02 billion in 2025 to USD 654.82 billion in 2026 and is forecast to reach USD 856.58 billion by 2031 at 5.52% CAGR over 2026-2031.

Public investments in work-based learning, such as new United States Registered Apprenticeship expansion grants and the United Kingdom’s Technical Excellence Colleges, are strengthening pathways that connect training to employment outcomes. Adoption of employer-verified micro-credentials is rising as digital badges become portable and secure across issuer ecosystems, helping the vocational training market align instruction with hiring decisions. Asia-Pacific accounted for 34.3% of global revenue in 2025 and, together with the Middle East and Africa, is among the fastest-growing regions through 2031, setting the stage for shifting regional demand in the vocational training market. Blended learning is gaining momentum as providers merge virtual modules with hands-on practice, while online platforms are expanding at an 11.8% CAGR as flexibility and stackable credentials attract broader learner cohorts in the market. Providers that pair industry co-designed curricula with transparent placement data are best positioned as outcome-based funding models advance in the vocational training market.

Key Report Takeaways

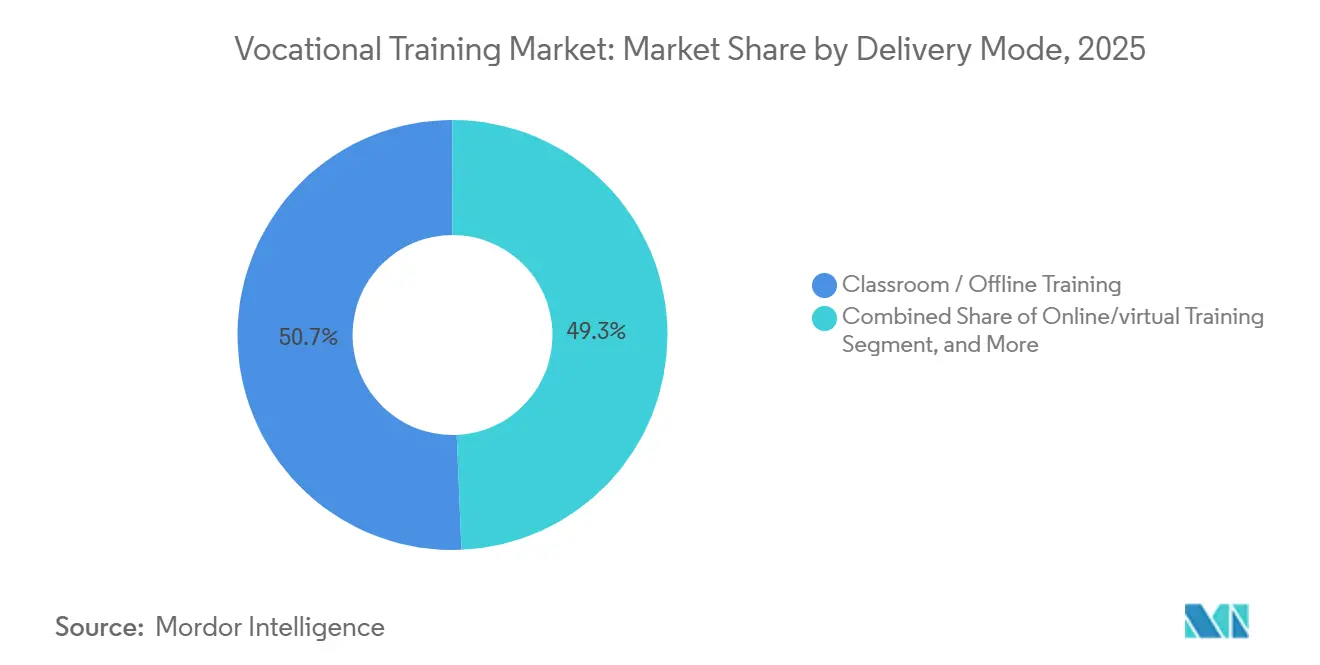

- By delivery mode, classroom and offline training led with 50.7% share of the vocational training market in 2025, while blended learning is forecast to grow at 14.4% CAGR through 2031.

- By training type, technical skills held 63.6% share of the vocational training market in 2025, and Information Technology is projected to expand at a 9.7% CAGR to 2031.

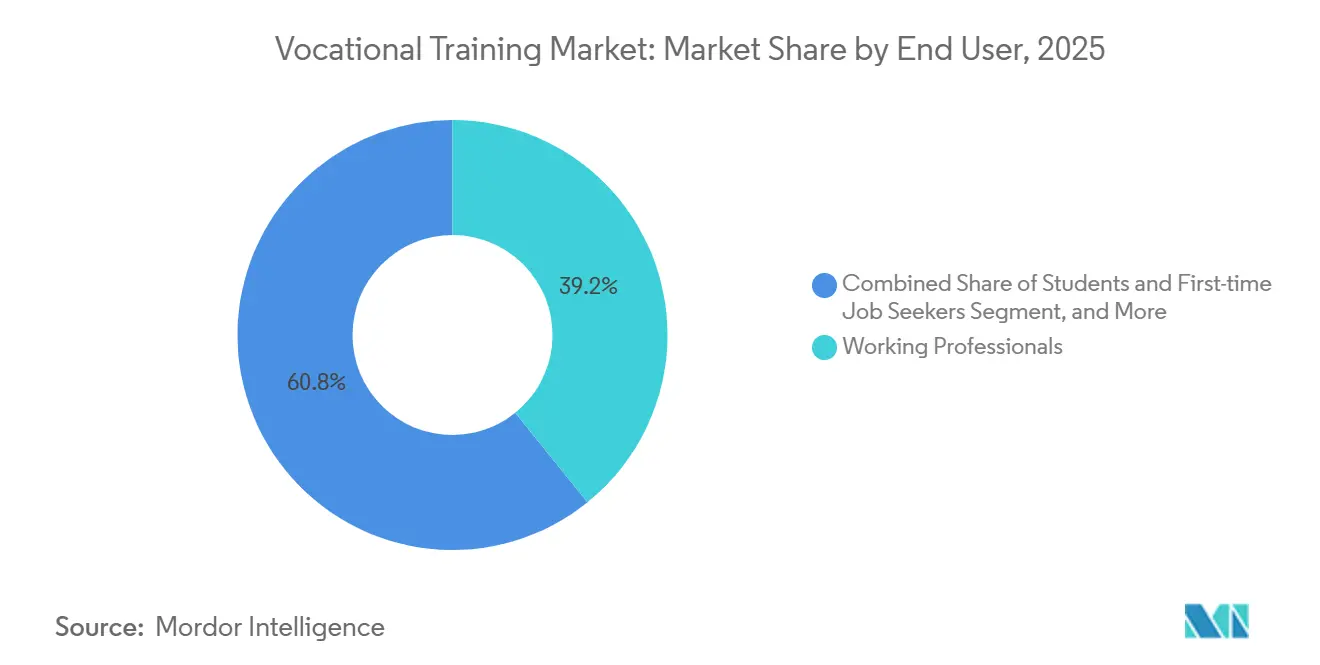

- By end user, working professionals accounted for 39.3% share of the vocational training market in 2025, while students and first-time job seekers are expected to grow at an 8.7% CAGR through 2031.

- By provider type, public and government institutes held 46.8% share of the vocational training market in 2025, with online EdTech platforms forecast to post an 11.8% CAGR to 2031.

- By geography, Asia-Pacific held 34.3% revenue share of the vocational training market in 2025, while the Middle East & Africa is projected to advance at a 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vocational Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills-based hiring overtakes degrees | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Employer-verified micro-credentials adopted | +0.9% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Subsidized apprenticeships scale globally | +1.0% | North America, Europe, MEA, APAC | Medium term (2-4 years) |

| Outcome-based training contracts expand | +0.6% | North America, Europe, early gains in Brazil, Mexico | Long term (≥ 4 years) |

| AI automation triggers reskilling demand | +1.3% | Global | Short term (≤ 2 years) |

| Procurement-linked skilling in contracts | +0.5% | North America, Europe, MEA (UAE, Saudi Arabia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills-Based Hiring Overtakes Degrees

Employers are placing more weight on demonstrable competencies and performance tasks, which strengthens demand for verified credentials and practical assessments across the vocational training market. State-level reforms that relax licensing barriers are improving mobility for trained workers in trades and care professions, supporting faster placement and career progression across regions[1]U.S. Department of Labor, “US Department of Labor Announces Availability of $85M in Grant Funding to Support Registered Apprenticeship Expansion, Modernization,” U.S. Department of Labor, dol.gov. This direction incentivizes providers to embed micro-credentials that map clearly to role requirements and safety standards. It also shifts selection toward objective skill checks, which align well with competency-based curricula in the vocational training market. Providers that co-design projects, assessments, and rubrics with employer consortia can signal job readiness more clearly to hiring teams. These steps tighten the feedback loop between instruction and labor-market demand in the vocational training market.

Employer-Verified Micro-Credentials Adopted

Verified digital badges are scaling across formal and non-formal education, with issuers emphasizing tamper-proof design, metadata-rich skill descriptions, and secure wallet storage to improve portability in the vocational training market. Interoperability through open badge standards supports adoption by colleges and training providers, while sector recognition continues to expand within IT, advanced manufacturing, and healthcare. The transparency of skill definitions and assessment evidence helps employers parse learning outcomes without reviewing long transcripts. This visibility also supports stackable pathways that bundle short-format credentials toward higher qualifications in the market. As quality frameworks evolve, alignment between badges and regulated certifications is improving in select jurisdictions. These developments reduce friction for learners and boost the signaling power of short-cycle credentials in the vocational training market.

Subsidized Apprenticeships Scale Globally

Performance-based grants in the United States are expanding Registered Apprenticeship capacity, with funds tied to growth in active apprentices, new entrants, and employer participation across priority sectors. The United Kingdom is building 19 Technical Excellence Colleges to train cohorts for clean energy, defense, advanced manufacturing, and digital roles, positioning colleges as national hubs that share curricula and instructor training[2]UK Department for Education, “Next Generation Empowered Through Technical Excellence Colleges,” GOV.UK, gov.uk. In Kenya, the PropelA initiative has embedded dual vocational models with employer partners and accreditation from the National Industrial Training Authority, creating structured two-year contracts that culminate in industry-recognized certification. Vietnam’s rural training programs coordinate across provincial departments to raise employment and self-employment through targeted upskilling, reflecting a whole-of-government approach to workforce readiness. These models increase employer co-investment, standardize on-the-job learning, and speed credentialing for in-demand roles in the vocational training market. They also align training throughput with industrial policies and regional development goals.

AI Automation Triggers Reskilling Demand

Rapid adoption of AI in production systems is elevating skill thresholds and shrinking the shelf life of technical competencies, which pushes time-sensitive upskilling across the vocational training market. Short-cycle programs that combine fundamentals with hands-on projects are gaining traction as implementation capacity depends on engineers, integrators, and project managers who can align models with business processes. Course patterns point to surging demand for entry-level AI literacy alongside advanced tracks in data, cybersecurity, and cloud, reinforcing modular pathways in the market. Outcome-oriented funding, including workforce initiatives that link instruction to placement and progression, is steering providers toward measured returns. Enterprise demand for faster rollouts and measurable productivity gains keeps the focus on applied learning. This momentum benefits providers that embed role-based labs and certifications in the vocational training market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low credential portability across borders | -0.7% | Global, acute in APAC and Latin America | Medium term (2-4 years) |

| Fragmented quality assurance standards | -0.6% | Global | Medium term (2-4 years) |

| Weak employer-curriculum co-design | -0.5% | Global, pronounced in developing regions | Long term (≥ 4 years) |

| Funding tied to seat-time, not outcomes | -0.4% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Credential Portability Cross-Borders

Recognition of vocational credentials varies widely across borders, which leads many workers to repeat training when relocating and reduces returns on learning investment in the vocational training market. National programs that coordinate ministries and provincial departments, such as Vietnam’s rural upskilling efforts, show how centralized governance can lift completion and employment outcomes by unifying standards and execution[3]Vietnam Government Portal, “Implementing a Program to Innovate and Improve the Quality of Rural Vocational Training by 2030,” Vietnam.vn, vietnam.vn. Kenya’s dual apprenticeship model, accredited by the National Industrial Training Authority, demonstrates portable certification aligned to employer demand and formal contract structures. Digital badge platforms improve interoperability of skills data, but regulated trades still depend on traditional accreditation pathways that move more slowly, limiting cross-border transfer in the vocational training market. Providers scaling across multiple countries face varying validation requirements that increase administrative costs. Alignment with regional frameworks remains uneven, which slows mobility and reduces barriers to entry in the vocational training market.

Fragmented Quality Assurance Standards

Outcomes measurement varies across programs and agencies, which weakens accountability for placement rates and wage gains and complicates funding decisions in the vocational training market. Quality assurance reforms in countries such as Australia tighten entry assessments for literacy, numeracy, and digital readiness to reduce non-completion and support better learner outcomes. Employers often gravitate toward recognized issuers and accreditation bodies in regulated sectors, which raises the bar for new entrants. Regional differences in governance and data-sharing also impede transparency in the vocational training market. Coordination with employers and sector councils can improve standard setting and curriculum alignment, but implementation remains uneven. Providers that offer clearer outcome metrics build trust faster with enterprise buyers in the vocational training market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Mode: Hybrid Models Close Skill Gaps Faster

Classroom and offline training accounted for 50.7% share of the global vocational training market size in 2025, as hands-on safety, lab work, and close supervision remain essential in engineering, healthcare, and trades. Blended learning is set to grow at 14.4% CAGR through 2031 as providers combine self-paced modules, virtual classrooms, and in-person practicums to improve flexibility and mastery in the vocational training market. Evidence from higher education shows blended formats enhance engagement and problem-solving when linked to simulations and project-based work[4]Frontiers Editorial Team, “Transforming Management Education: Blended Learning, International Collaboration, and Pedagogical Innovation—Current Trends and Future Directions,” Frontiers in Education, frontiersin.org. Providers are addressing infrastructure and pedagogy gaps through upskilling for instructors and incremental platform investments. Immersive technologies, including VR and AR, are gaining traction where error costs are high, which reinforces practical competencies in the vocational training market. Compliance frameworks in safety-critical fields are beginning to acknowledge simulation-based assessments where national or ISO standards are met.

Working professionals use online and virtual paths to balance learning with jobs and caregiving, and this behavior encourages short modules that fit into daily workflows in the vocational training market. Personalization matters as learners disengage when content does not match role and skill level, a signal that is pushing vendors to deploy recommendation engines and adaptive quizzes. Companies report lower travel, facility, and materials costs when shifting theory to digital formats while reserving in-person time for practice and coaching in the vocational training market. Colleges in the United Kingdom are embedding immersive labs and algorithmic guidance into blended curricula to improve readiness for applied tasks. As hybrid work patterns persist, blended designs will remain central to speed-to-skill strategies across the vocational training industry. This balance between digital scalability and live instruction strengthens outcomes for both learners and employers in the vocational training market.

By Training Type: IT Skills Outpace Broader Technical Growth

Technical skills held 63.6% of the vocational training market share in 2025, anchored by employer demand for engineering, industrial, IT, and healthcare competencies that are directly tied to production and service delivery. Information Technology is projected to expand at 9.7% CAGR to 2031 as organizations prioritize AI, cybersecurity, data, and cloud roles, which concentrates demand for role-based learning paths in the vocational training market. Government-backed apprenticeship initiatives in advanced manufacturing and clean energy are adding capacity for practical training at scale in major markets. Healthcare and allied programs are expanding due to persistent nurse and technician shortages and the need for up-to-date compliance and safety credentials. Non-technical tracks in hospitality, business, and arts maintain relevance for service economies and creative roles, though growth remains slower than in technical areas in the vocational training market. Employers emphasize soft skills alongside technical depth to ensure managers and frontline teams can adapt to evolving tools and workflows.

Reshoring and infrastructure priorities in the United States and the United Kingdom are widening capacity in shipbuilding, construction, and defense-related trades, which raises the throughput of job-ready graduates in the vocational training market. For IT, modular credentials and labs tied to vendor ecosystems improve signal strength for enterprise recruiters. Providers are expanding capstone projects, scenario-based assessments, and supervised practicums to verify readiness. The vocational training industry is also integrating professional English and communication skills for distributed teams. These patterns support faster placement and ramp-up in both small firms and large enterprises in the vocational training market. The net effect is a deeper pipeline for technical roles that face the highest hiring friction.

By End User: Students Gain Share as Degree Skepticism Rises

Working professionals held 39.3% in 2025 as employers funded upskilling to support role redesign and retention in the vocational training market. Students and first-time job seekers are projected to grow at 8.7% CAGR through 2031 as short-cycle credentials and apprenticeships gain traction as direct routes to employment in the market. Community colleges and trade schools are expanding paid placements and guaranteed interview programs with employer partners to attract new entrants. Enterprises are strengthening on-ramps to roles in cybersecurity, cloud operations, and AI support with curated learning paths and supervised projects. Public-sector employers continue to certify frontline workers to maintain service continuity and compliance. This mix aligns entry-level training to job vacancy patterns across regions in the vocational training market.

Corporate programs that underwrite tuition or commit to hiring on completion signal strong demand for verifiable skills in the vocational training market. Large employers that publish participation and placement outcomes establish proof points for scalable upskilling across job families. Government agencies use apprenticeships to expand supply in priority sectors, which lowers time-to-fill for technical roles while reducing barriers for underrepresented groups. The vocational training industry is responding with flexible schedules and modular curricula that enable progressive credentialing. Providers are also adapting support services to improve completion for working learners. Together, these shifts reinforce pathways from training to stable employment in the vocational training market.

By Provider Type: EdTech Platforms Exploit Legacy Gaps

Public and government institutes held 46.8% share of the global vocational training market size in 2025, as subsidized tuition, national mandates, and accreditation infrastructure sustained broad access. Online EdTech platforms are forecast to grow at 11.8% CAGR through 2031 as learners prioritize flexibility, stackable credentials, and AI-supported personalization across the vocational training market. Centralized governance in several countries coordinates curricula, instructor training, and employer links for public providers. Corporate training centers deliver custom programs aligned to proprietary stacks, which raise job-readiness but limit credential portability. Subscription-based models and AI-native content generation are reshaping the provider landscape in the market. Stronger analytics and outcome reporting differentiate vendors in enterprise buying cycles.

Private equity activity and strategic acquisitions signal confidence in scaled platforms and content ownership models in the vocational training market. Transactions such as KKR’s acquisition of Instructure and Accenture’s purchase of Udacity illustrate bets on recurring revenue and tighter integration of content with services. Employers are co-investing in workforce pipelines that guarantee interviews or roles on completion, which reduces friction for learners and hiring teams. Partnerships that embed language proficiency and foundational digital skills are expanding global reach for technical programs. Over time, providers that prove consistent placement and wage gains will consolidate their share. These dynamics continue to tilt the vocational training market toward outcome-driven models and integrated ecosystems.

Geography Analysis

Asia-Pacific led with 34.3% revenue share in 2025, while Middle East & Africa and Asia-Pacific are each projected to post a 9.1% CAGR through 2031 within the vocational training market size. Vietnam’s national program coordinates provincial departments to train rural workers through 2030, with targeted emphasis on non-agricultural sectors and structured oversight for funding and delivery. Australian reforms tighten standards for registered providers and align programs with labor-market needs as public TAFEs prioritize high-demand occupations in the vocational training market. These approaches improve relevance and completion, enhancing pipelines for manufacturing, logistics, and digital roles. Countries with demographic headwinds are leaning on automation and lifelong learning to preserve productivity. Providers that localize content and employer partnerships are gaining regional traction in the vocational training market.

The Middle East & Africa is expected to match Asia-Pacific as the fastest growing region through 2031, as governments push diversification and scale youth employment pathways in the vocational training market. In South Africa, multinationals run long-form apprenticeships for artisans and technicians that merge classroom work with supervised practice and placement. Kenya’s dual apprenticeship model demonstrates portable certification and employer co-investment with accredited training models and two-year contracts. National skills platforms and public incentives in Gulf economies are expanding capacity in IT, hospitality, and renewable energy. These measures increase completion rates and speed-to-hire in the vocational training market. As infrastructure programs continue, demand rises for safety, compliance, and plant operations training.

North America remains a large revenue base, supported by United States grants that expand Registered Apprenticeships and align funds to performance outcomes across priority sectors in the vocational training market. Policy steps that streamline adult education and workforce grants are improving coordination and reducing duplication in delivery. In Europe, public investment in skills and mobility is advancing through national hubs and specialized colleges that raise standards and connect providers to employers in the vocational training market. Early career and mid-career retraining programs are converging on modular credentials, language proficiency, and digital foundations to reach wider cohorts. As nearshoring expands in North America, bilingual training and cross-border recognition gain importance. Providers with transparent outcomes and strong employer networks are best positioned across both regions in the vocational training market.

Competitive Landscape

The vocational training market shows moderate fragmentation, with the top 10 providers holding about 35% of global revenue in 2025, which leaves room for regional specialists, enterprise academies, and digital platforms to expand. Incumbents such as Pearson, City & Guilds, Coursera, Udemy, and Skillsoft benefit from brand equity, accreditation networks, and enterprise distribution. Strategies now converge on AI-enabled content, modular credentials, and stronger analytics that link training to job outcomes in the vocational training market. Providers that co-design curricula with employers and publish placement and wage data are forming durable moats. Accreditation remains essential in regulated fields, which raises barriers to entry for niche challengers. This environment rewards platforms that combine scale with credible assessments in the vocational training market.

Private equity and corporate transactions are reshaping the vendor landscape in the vocational training market. KKR’s acquisition of Instructure and Accenture’s acquisition of Udacity highlight confidence in subscription learning and content ownership models that integrate training with consulting and services. Enterprise partnerships underscore demand for scaled-upskilling, with programs that retrain associates for higher-value roles and publish transparent outcomes in the market. Employers in industrial, digital, and service sectors are aligning tuition support and apprenticeships with hiring pipelines. These moves reduce onboarding time and improve retention. The net effect is stronger integration between learning systems and workforce planning in the vocational training market.

Product roadmaps are emphasizing AI-native features, simulation-based practice, and real-time performance feedback in the vocational training market. Role-based labs and supervised practicums remain central for demonstrating competency in safety-critical environments. Providers that fuse analytics with curriculum updates are improving alignment with technology stacks and compliance. Regional expansion depends on accreditation and recognition agreements, which can slow the time to market. As outcome-based contracts gain attention, transparent reporting becomes a competitive requirement in the vocational training market. Vendors that prove durable gains in placement and progression are positioned to consolidate share as customers standardize on fewer platforms.

Vocational Training Industry Leaders

Pearson plc

Coursera Inc.

Udemy Inc.

City & Guilds Group

Pluralsight LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The U.S. Department of Labor announced USD 85 million in State Apprenticeship Expansion Formula grants to support Registered Apprenticeship expansion and modernization, with performance-based funding linked to growth in active apprentices, new entrants, and employer participation.

- April 2026: The United Kingdom government invested GBP 175 million (USD 236.4 million) in 19 Technical Excellence Colleges specializing in advanced manufacturing, clean energy, defense, and digital technologies, with colleges acting as national hubs and training about 65,000 learners annually.

- February 2026: Vietnam’s Prime Minister approved Decisions No. 326 and No. 328 to innovate and improve rural vocational training until 2030, targeting about 1.5 million rural workers annually and coordinating implementation across provincial departments

- April 2026: India reported a 50% increase in enrollments under the National Apprenticeship Promotion Scheme (NAPS) during FY 2025–26, driven by reforms such as higher apprentice stipends and easier employer compliance rules, strengthening work-based vocational training demand

Global Vocational Training Market Report Scope

Vocational training equips individuals with practical education and job-specific skills, enhancing their career readiness and employability. This market encompasses trade schools, technical institutes, online training platforms, apprenticeships, certification programs, and corporate skill-development services.

The Vocational Training Market Report is Segmented by Delivery Mode (Classroom/Offline Training, Online/Virtual Training, and More), Training Type (Technical Skills, Non-Technical Skills), End User (Students & First-Time Job Seekers, and More), Provider Type (Public/Government Institutes, Private Institutes, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Classroom / Offline Training |

| Online / Virtual Training |

| Blended Learning |

| Technical Skills | Engineering & Industrial |

| Information Technology | |

| Healthcare & Allied | |

| Non-Technical Skills | Hospitality & Tourism |

| Business & Management | |

| Arts & Design |

| Students & First-time Job Seekers |

| Working Professionals |

| Corporates / Enterprises |

| Government & Public Sector |

| Public / Government Institutes |

| Private Institutes |

| Corporate Training Centers |

| Online EdTech Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Delivery Mode | Classroom / Offline Training | |

| Online / Virtual Training | ||

| Blended Learning | ||

| By Training Type | Technical Skills | Engineering & Industrial |

| Information Technology | ||

| Healthcare & Allied | ||

| Non-Technical Skills | Hospitality & Tourism | |

| Business & Management | ||

| Arts & Design | ||

| By End User | Students & First-time Job Seekers | |

| Working Professionals | ||

| Corporates / Enterprises | ||

| Government & Public Sector | ||

| By Provider Type | Public / Government Institutes | |

| Private Institutes | ||

| Corporate Training Centers | ||

| Online EdTech Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the global size and growth outlook for the vocational training market to 2031?

The vocational training market size is USD 654.82 billion in 2026 and is expected to reach USD 856.58 billion by 2031 at a 5.52% CAGR, reflecting steady expansion supported by public funding and employer demand.

Which region leads and which grows fastest in the vocational training market?

Asia-Pacific led with 34.3% share in 2025, while Middle East & Africa is each projected to grow at 9.1% CAGR through 2031 based on current program momentum and demographics.

Which delivery mode is growing fastest in the vocational training market?

Blended learning is the fastest-growing delivery mode at 14.4% CAGR to 2031, as providers combine virtual modules with supervised practice to balance flexibility and hands-on competency.

Which training categories are most important in the vocational training market?

Technical skills dominate with 63.6% share in 2025 and IT training is projected to grow at 9.7% CAGR to 2031, driven by AI, cybersecurity, data, and cloud roles.

How are governments supporting capacity in the vocational training market?

Governments are expanding performance-based grants and specialized colleges for high-demand sectors, exemplified by U.S. Registered Apprenticeship expansion and the United Kingdom’s Technical Excellence Colleges.

What limits the cross-border mobility of skilled workers in the vocational training market?

Credential portability remains uneven across countries, and many regulated trades still require legacy accreditation routes, which slows recognition and increases retraining when workers relocate.

Page last updated on: