Corneal Pachymetry Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

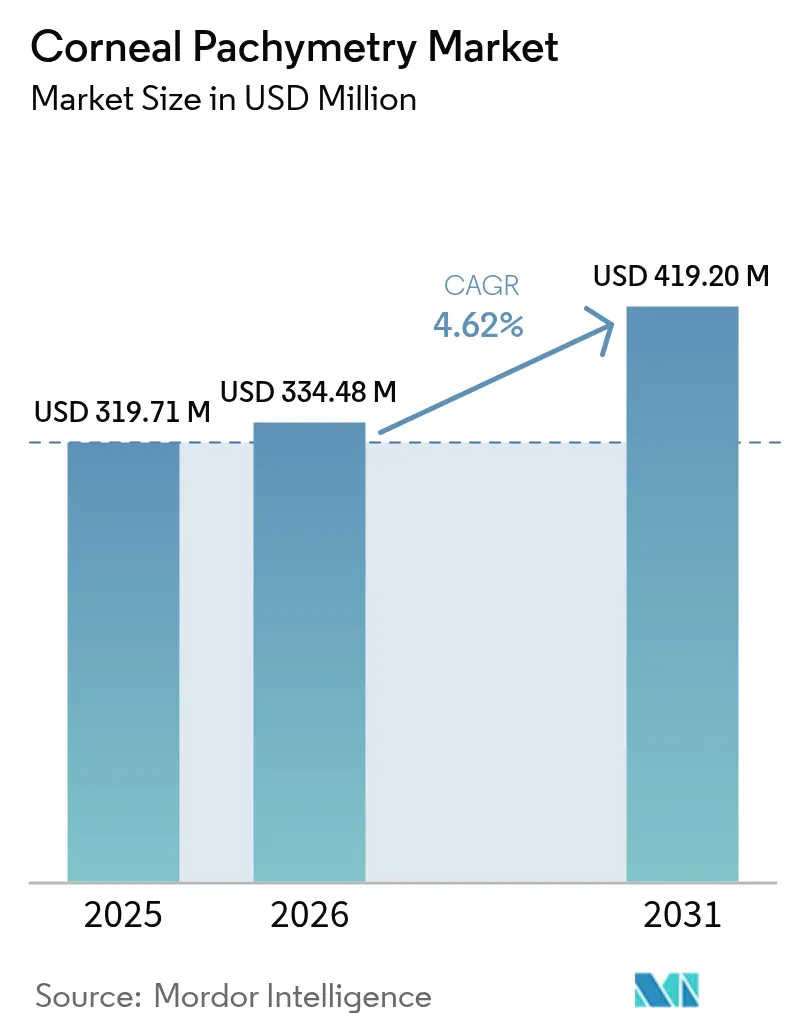

| Market Size (2026) | USD 334.48 Million |

| Market Size (2031) | USD 419.2 Million |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

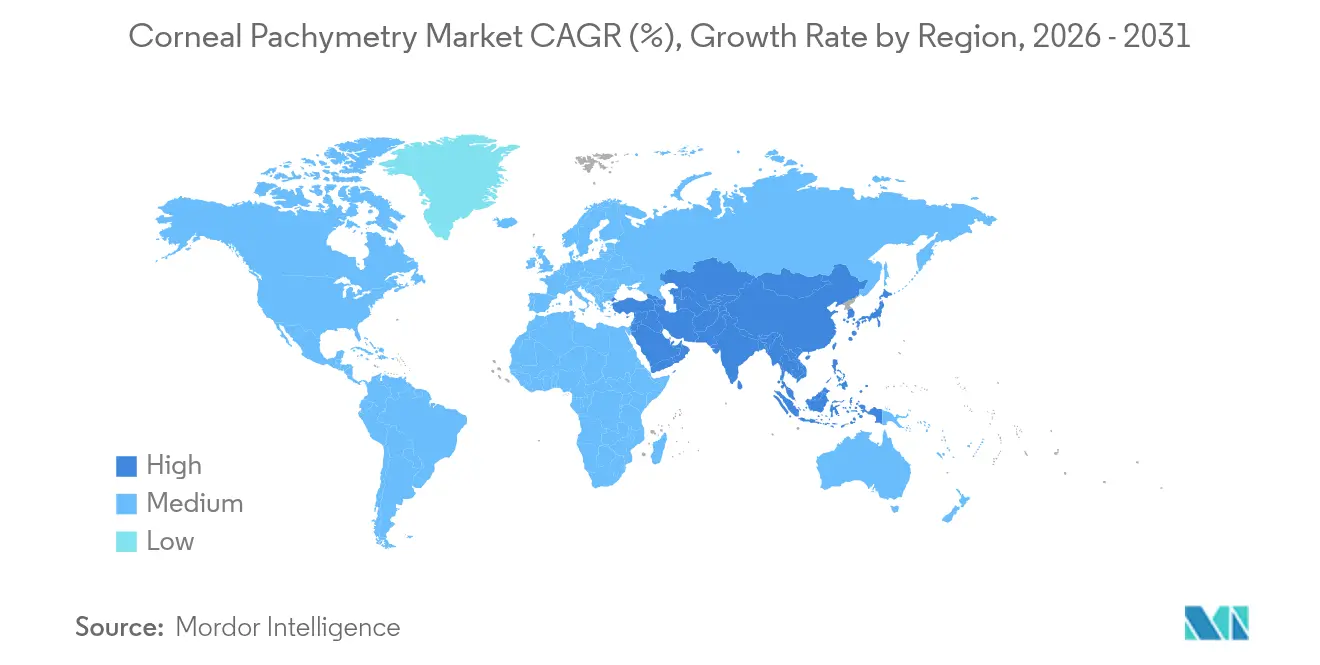

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

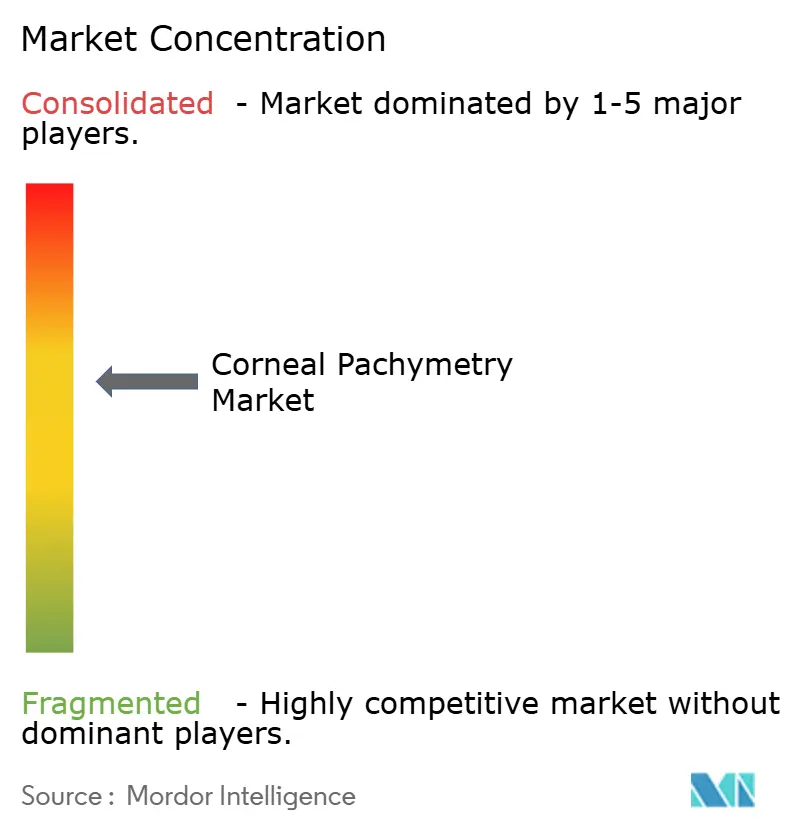

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corneal Pachymetry Market Analysis by Mordor Intelligence

The Corneal Pachymetry Market size is expected to grow from USD 319.71 million in 2025 to USD 334.48 million in 2026 and is forecast to reach USD 419.2 million by 2031 at 4.62% CAGR over 2026-2031.

Growth stems from the everyday use of corneal‐thickness measurement in glaucoma management, rising refractive‐surgery volumes, and a steady transition from ultrasonic to optical coherence tomography (OCT)-based systems. Hospitals, clinics, and ambulatory centers seek faster, contact-free devices that fit seamlessly into digital workflows, while aging populations and higher myopia prevalence keep procedure demand elevated. At the same time, faster reimbursement approvals in mature economies and expanding eye-care capacity in Asia support wider access to these diagnostics. Technology suppliers focus on AI integration and cloud connectivity to differentiate, but regulatory compliance costs and data-privacy rules temper near-term momentum.

Key Report Takeaways

- By type, ultrasonic methods held 55.62% of the corneal pachymetry market share in 2025; optical methods are projected to expand at a 6.89% CAGR through 2031.

- By application, glaucoma diagnostics led with 60.55% revenue share in 2025, while keratoconus and ectasia screening is advancing at an 7.71% CAGR.

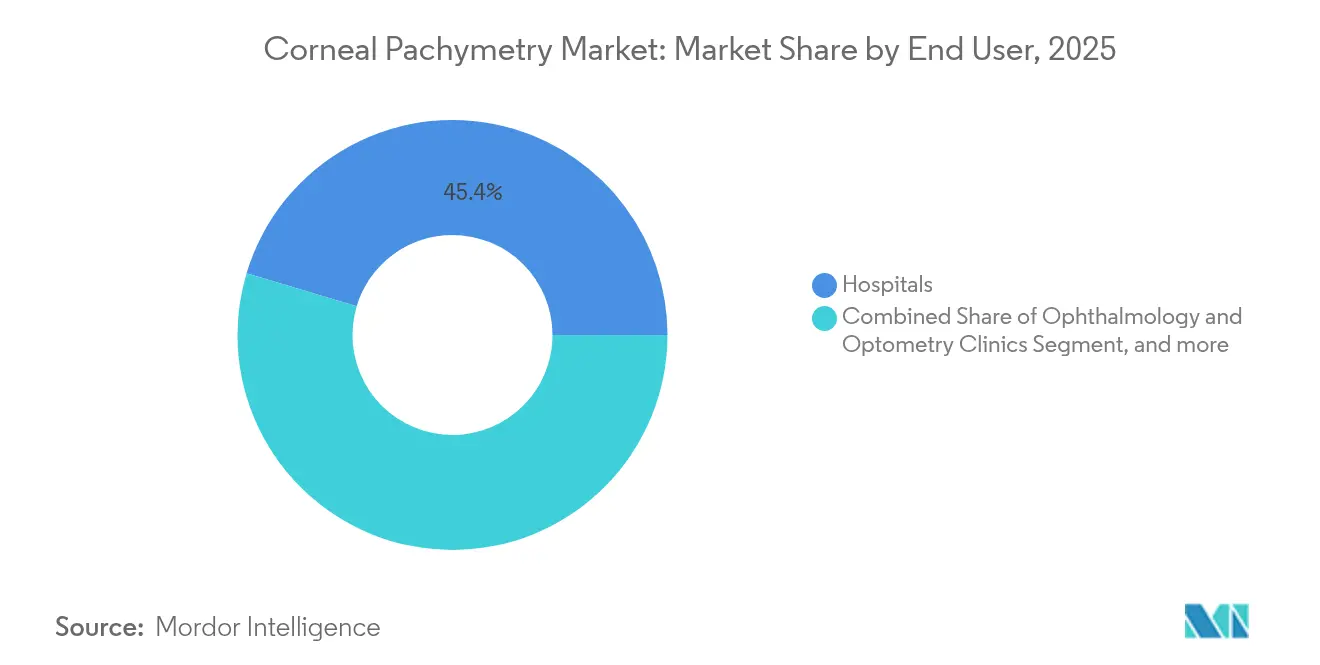

- By end user, hospitals captured 45.36% share of the corneal pachymetry market size in 2025; ambulatory surgical centers represent the fastest segment with an 8.12% CAGR.

- By geography, North America commanded 38.21% of 2025 revenue; Asia-Pacific is forecast to grow at 7.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Corneal Pachymetry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in prevalence of glaucoma & ocular hypertension | +1.2% | North America, Europe, Global | Long term (≥ 4 years) |

| Growing cataract & refractive-surgery volumes | +0.9% | Asia-Pacific, Global | Medium term (2-4 years) |

| Rapid adoption of AS-OCT & Scheimpflug non-contact systems | +0.8% | North America, EU, spill-over to APAC | Medium term (2-4 years) |

| Expansion of eye-care services in middle-income countries | +0.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Tele-ophthalmology push for handheld pachymeters | +0.5% | Rural Global | Short term (≤ 2 years) |

| AI-driven IOP-correction algorithms needing real-time CCT | +0.4% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Glaucoma & Ocular Hypertension

Central corneal thickness (CCT) is now accepted as a critical risk factor for glaucoma, after the Ocular Hypertension Treatment Study showed a 71% rise in conversion risk for every 40 µm reduction in CCT.[1]Steve Brito, “Central Corneal Thickness and Glaucoma Risk,” Dove Press, dovepress.com Routine pachymetry screening of adults over 50, therefore, becomes a non-negotiable element of preventive eye care. Health systems in North America and Europe reimburse pachymetry when combined with tonometry, which pushes device uptake in primary and specialist settings.[2]Aetna Medical Policy Bulletin, “Corneal Pachymetry,” aetna.com Ongoing monitoring also matters because CCT changes skew intraocular-pressure readings and can lead to mismanaged therapy. As the pool of glaucoma patients doubles each decade after 40, demand for accurate thickness data will keep rising, securing a steady pipeline for the corneal pachymetry market.

Growing Cataract & Refractive-Surgery Volumes

Cataract and laser vision-correction procedures continue to climb, with Asia-Pacific contributing the largest incremental volume. Surgical guidelines treat pachymetry as mandatory since corneal biomechanics steer lens selection, incision planning and postoperative healing. Alcon’s premium intraocular-lens portfolio illustrates how precise corneal metrics lift refractive outcomes. Similarly, refractive candidates undergo corneal mapping to avoid ectasia, making thickness profiling essential for screening out high-risk eyes. AI-driven surgical planners such as ZEISS VERACITY now import pachymetry data automatically, cutting chair time and lowering complication rates. These workflow linkages add repeat purchase drivers for advanced pachymeters.

Rapid Adoption of AS-OCT & Scheimpflug Non-Contact Systems

New optical platforms offer sub-5 µm repeatability without corneal contact, eliminating anesthesia risk and boosting patient comfort. Anterior-segment OCT supplies cross-sectional images that help surgeons gauge flap depth, angle, anatomy, and stromal remodeling.[3]Mary Smith, “Repeatability of AS-OCT Measurements,” MDPI Diagnostics, mdpi.com Scheimpflug cameras, typified by the Pentacam family, spot early keratoconus with tomographic maps that pick up curvature irregularities missed by ultrasound probes. Clinics value multipurpose use because a single device measures CCT, lens density, and anterior-chamber depth, raising return on investment. AI modules further reduce technician variability, adding momentum to the optical shift and lifting the corneal pachymetry market.

Expansion of Eye-Care Services in Middle-Income Countries

Government funding in China and India backs specialty hospitals, ambulatory centers, and tele-ophthalmology networks, which all require portable pachymeters. China’s state-directed healthcare investment fund has poured capital into vision-care consolidators, accelerating device procurement. Alcon’s Phaco Development program, which has trained more than 6,300 professionals in Asia-Pacific, speeds the clinical adoption curve by pairing technology supply with surgeon education. Outpatient cataract packages gain favor because they reduce cost and waiting time, so centers opt for handheld, battery-powered pachymeters that cover screening, surgery, and postoperative follow-up on one platform. The result is a rising share of global revenue flowing from emerging economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate reimbursement for pachymetry procedures | -0.8% | Emerging markets, Global | Long term (≥ 4 years) |

| Stringent device & data-privacy regulations | -0.6% | North America, EU | Medium term (2-4 years) |

| Lack of interoperability across imaging platforms | -0.4% | Integrated health systems | Short term (≤ 2 years) |

| Emergence of corneal-biomechanics devices as a substitute | -0.3% | North America, EU, spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inadequate Reimbursement for Pachymetry Procedures

Coverage gaps hinder routine use because many payers only reimburse pachymetry when linked to specific diagnoses. Medicare contractors vary widely in their local rules, and some private insurers tag pachymetry as investigational for screening, forcing providers to self-pay or forego testing. The financial uncertainty discourages primary-care clinics from including pachymetry in comprehensive eye exams, especially in emerging markets where out-of-pocket spending remains high. Without consistent payment codes the corneal pachymetry market cannot reach its full preventive-care potential.

Stringent Device & Data-Privacy Regulations

Design changes mandated by the FDA Quality System Regulation amendments that take effect in February 2026 will raise compliance costs, particularly for smaller innovators. In Europe, medical-device manufacturers also wrestle with General Data Protection Regulation rules, which compel robust encryption and strict consent protocols for cloud-based analytics. The dual burden of product safety testing and cybersecurity documentation lengthens time-to-market and may slow the refresh cycle for new pachymetry models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Optical Methods Drive Technology Transition

Ultrasonic pachymeters generated the majority of revenue, holding 55.62% of the corneal pachymetry market in 2025. Clinics appreciate their low price point and proven performance in edematous or scarred corneas. However, optical systems outpace them with a 6.89% CAGR, underscoring a clear pivot toward non-contact care. Occuity’s PM1 handheld device illustrates the user pull; clinical validation shows sub-5 µm repeatability without topical anesthesia. Optical units also deliver pachymetric maps, keratometry, and angle analysis in a single scan, enriching surgical planning.

Optical platforms pair naturally with telemedicine because technicians can capture scans and send raw data to remote experts for interpretation. AI overlays flag thinning zones and suggests keratoconus probability scores, which elevates diagnostic precision in high-throughput settings. As clinician confidence grows, and as service contracts bundle cloud analytics, optical share will keep expanding. Nevertheless, ultrasound retains a foothold for intraoperative measurement, especially in cases with corneal opacity where light-based devices struggle. The coexistence of both technologies therefore broadens the total corneal pachymetry market size without immediate cannibalization.

By Application: Keratoconus Screening Emerges as Growth Driver

Glaucoma diagnostics remained the most significant use case, bringing in 60.55% of 2025 revenue. Accurate CCT data recalibrate tonometry readings and refine risk scoring, so ophthalmologists incorporate pachymetry at every visit for patients with ocular hypertension. The corneal pachymetry market size linked to this task is stable, but incremental volume gains align with population aging. Refractive surgery planning is the next major segment because surgeons must rule out subclinical ectasia before corneal reshaping. Postoperative monitoring and corneal graft follow-up also rely on thickness trending to detect edema or rejection.

Keratoconus and ectasia screening stands out with an 7.71% growth rate. Multi-parameter indices mix pachymetric and biomechanical variables to spot disease earlier than topography alone. This need pulls high-resolution systems into optometry chains where young myopes first present, expanding the market’s addressable base. Insurers in some European markets now reimburse early keratoconus screening when combined with corneal tomography, creating a clear financial rationale. As awareness widens and contact-lens discomfort drives patients toward cross-linking, volumes should stay on a steep trajectory, deepening the corneal pachymetry market.

By End User: Ambulatory Centers Lead Adoption Trends

Hospitals still dominate sales, holding 45.36% revenue share because they handle complex corneal surgery, transplantation and trauma. Large academic centers integrate pachymetry into multimodal imaging suites that manage glaucoma clinics, cataract lanes and corneal specialty work. They also conduct clinical trials requiring longitudinal thickness tracking, further supporting unit demand. Clinics run by ophthalmologists and optometrists follow closely, using pachymetry for routine disease management and surgical comanagement.

Ambulatory surgical centers (ASCs) are the expansion hot spot, posting an 8.12% CAGR. Medicare counted 3.4 million beneficiaries treated in ASCs during 2023, and ophthalmology made up 18.5% of the volume. ASCs value portable or cart-mounted pachymeters that move easily between procedure rooms and pre-op bays, letting staff collect CCT data without slowing flow. Lower overhead and bundled payment models encourage device purchases when they shorten case duration. As more cataract and laser vision-correction work leaves hospitals, ASCs will claim a rising slice of the corneal pachymetry market share.

Geography Analysis

North America accounted for 38.21% of global revenue in 2025, anchored by high disposable income, insurance coverage, and established glaucoma screening guidelines. Medicare reimburses pachymetry linked to tonometry under CPT 76514, and private insurers follow similar rules, sustaining baseline demand. Clinics routinely upgrade to OCT-based platforms for integrated anterior-segment imaging, making the region a reliable early adopter of AI-enhanced workflows. FDA guidance is stringent but predictable, giving suppliers a clear development path and plenty of post-market feedback for product refinement.

Europe offers a mature but innovation-friendly landscape. Aging demographics increase cataract load, while public health systems prefer preventive checks that delay costly vision loss. CE-marked pachymeters gain access across member states, although compliance with the European Medical Device Regulation adds paperwork and cybersecurity safeguards. EssilorLuxottica’s acquisition of Heidelberg Engineering underscores the strategic value of imaging within integrated eye-care portfolios. University hospitals in Germany and Italy spearhead research on tomography-based keratoconus screening, keeping the region at the forefront of clinical evidence generation.

Asia-Pacific is expanding fastest, clocking a 7.32% CAGR. China funds ophthalmology chains to widen service reach, with investment banks noting steady deal flow in the sector. Rising myopia among children and young adults lifts demand for corneal assessment in refractive-surgery planning. Government insurance schemes in Japan cover pachymetry when used for glaucoma management, while private hospitals in India advertise LASIK packages that bundle complete corneal mapping. Training programs sponsored by multinationals accelerate device literacy, ensuring that local clinicians can extract full value from advanced pachymeters. The region, therefore, shapes the longer-term revenue shift within the corneal pachymetry market.

Competitive Landscape

The market remains moderately fragmented, with the top five suppliers holding significant combined revenue. Carl Zeiss Meditec, Topcon, NIDEK, Haag-Streit, and Oculus command mind share through optical platforms that link imaging with analytics. Zeiss deepened its surgical workflow offering by acquiring Dutch Ophthalmic Research Center, thereby bundling diagnostics with intraoperative tools. Topcon integrates pachymetry into its Maestro series, promoting one-stop exams for busy clinics.

Regional entrants carve out niches in handheld and value-tier ultrasound segments, while startups chase AI overlays that identify corneal disease with minimal operator input. Big Vision Medical raised USD 30 million to build a cloud-based screening platform that targets optometry chains. Portable units appealing to mobile screening programs add another competitive layer, with Occuity and other sensor innovators vying for price-performance leadership.

Strategic partnerships between device makers and software firms accelerate feature rollouts, especially for image sharing and electronic-record integration. Suppliers also court ambulatory centers with pay-per-use or rental models that lower upfront cost. The resulting arena rewards companies that balance global service networks with agile upgrades, keeping the corneal pachymetry market dynamic yet open to new entrants.

Corneal Pachymetry Industry Leaders

Reichert Inc.

Sonomed Escalon

DGH Technology, Inc

NIDEK Co. Ltd.

Lumibird Group (Quantel Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcon announced its acquisition of Lensar and its next-generation femtosecond laser-assisted cataract surgery portfolio, expanding its surgical technology capabilities and potentially integrating advanced corneal assessment technologies into comprehensive surgical planning platforms.

- December 2024: Bausch + Lomb completed the acquisition of Elios Vision Inc., developer of the ELIOS minimally invasive glaucoma surgery system using excimer laser technology, expanding treatment options for glaucoma patients who require comprehensive corneal assessment for surgical planning.

- July 2024: EssilorLuxottica acquired a majority stake in Heidelberg Engineering, a leading provider of ophthalmic diagnostic imaging technologies, strengthening its position in the corneal assessment and anterior segment imaging market.

- July 2024: Alcon acquired Belkin Vision for USD 81 million upfront, enhancing its glaucoma treatment portfolio and expanding capabilities in corneal biomechanical assessment technologies.

Global Corneal Pachymetry Market Report Scope

As per the scope of the report, a pachymeter is a medical device used to measure corneal thickness. It is also used to determine endothelial pump and corneal barrier functions. Moreover, it helps in determining intraocular pressure in the case of glaucoma. Corneal thickness greater than 640 m increases the risk of corneal decompensation. Ultrasound and optical pachymeters are the two devices used to perform pachymetry. The Corneal Pachymetry Market is Segmented by Type (Ultrasonic Method and Optical Method), Application (Glaucoma Diagnosis and Refractive Surgery), and Geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the market size and forecasts in value (USD million) for the above segments.

| Ultrasonic Method |

| Optical Method |

| Glaucoma Diagnostics |

| Refractive Surgery Planning |

| Keratoconus & Ectasia Screening |

| Post-operative Corneal Edema Monitoring |

| Corneal Transplant Evaluation |

| Hospitals |

| Ophthalmology & Optometry Clinics |

| Ambulatory Surgical Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Ultrasonic Method | |

| Optical Method | ||

| By Application | Glaucoma Diagnostics | |

| Refractive Surgery Planning | ||

| Keratoconus & Ectasia Screening | ||

| Post-operative Corneal Edema Monitoring | ||

| Corneal Transplant Evaluation | ||

| By End User | Hospitals | |

| Ophthalmology & Optometry Clinics | ||

| Ambulatory Surgical Centres | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the corneal pachymetry market?

The corneal pachymetry market is valued at USD 334.48 million in 2026.

Which segment grows fastest over 2025-2031?

Keratoconus and ectasia screening shows the highest growth with an 7.71% CAGR.

Why are optical pachymeters gaining share?

Optical platforms provide contact-free measurements, richer corneal maps and AI compatibility, driving a 6.89% CAGR for the segment.

How large is North America’s share of global revenue?

North America held 38.21% of total revenue in 2025.

What factors restrain wider adoption in emerging markets?

Limited reimbursement and high device compliance costs slow uptake despite growing procedure demand.

Which end-user setting posts the highest growth?

Ambulatory surgical centers expand fastest with an 8.12% CAGR as outpatient eye surgery volumes climb.

Page last updated on: