Corneal Topographers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

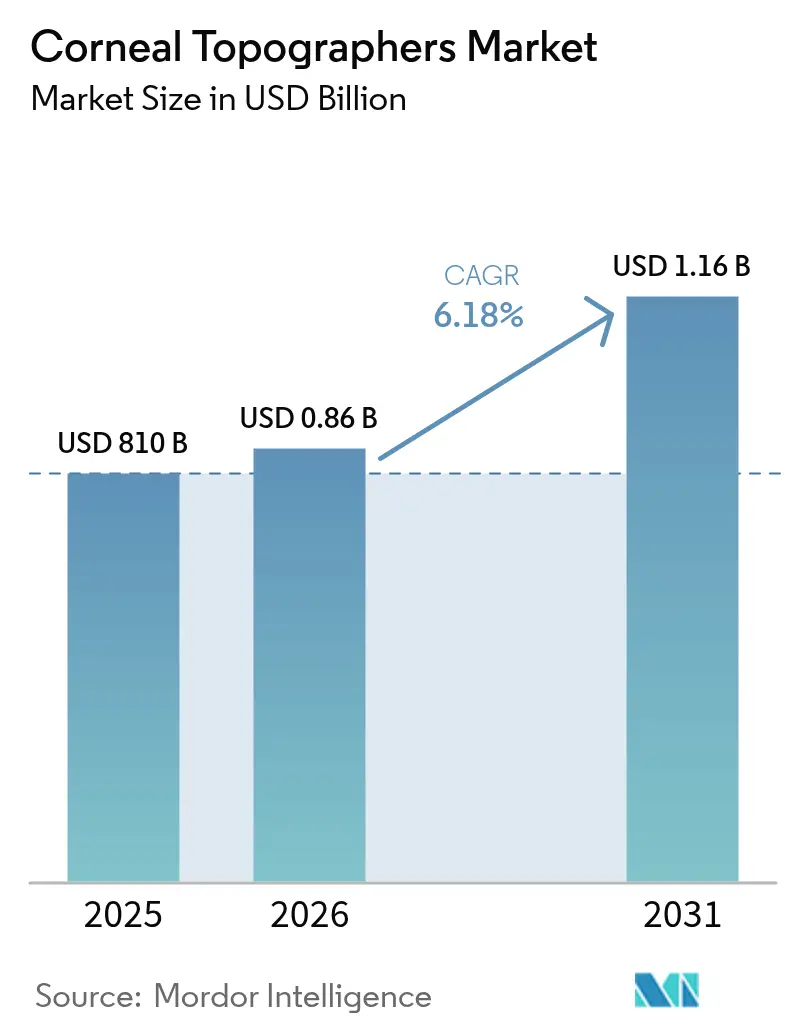

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

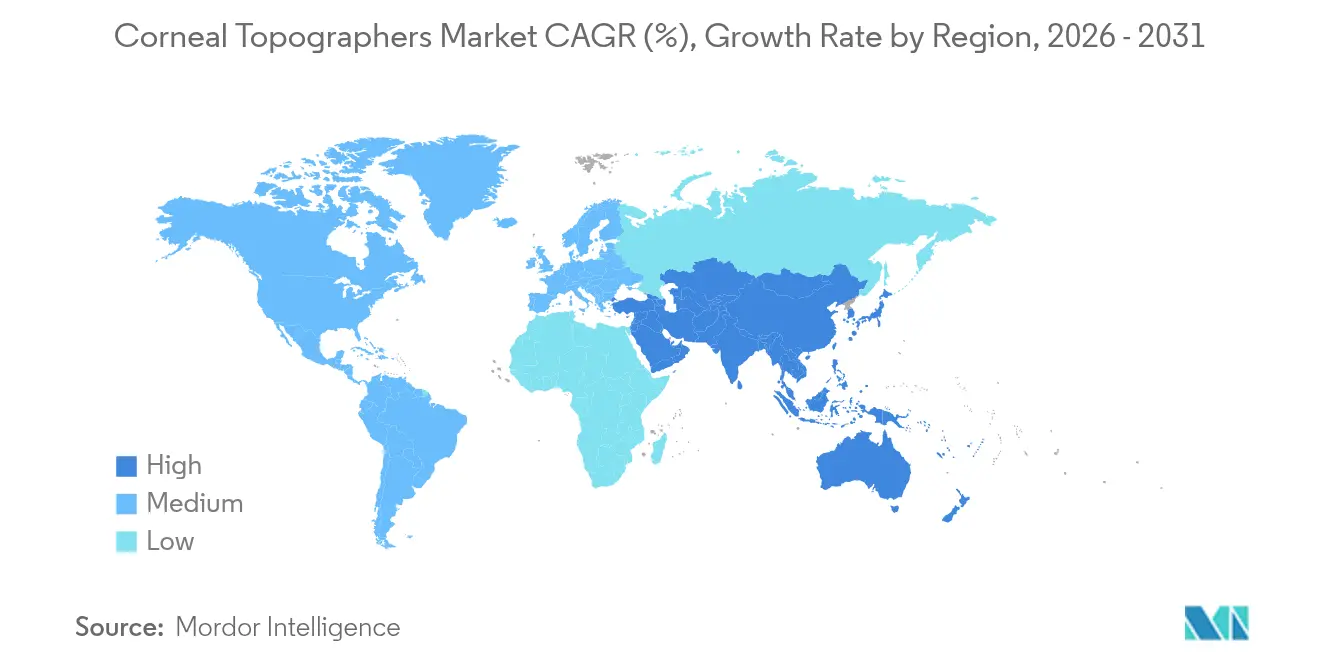

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corneal Topographers Market Analysis by Mordor Intelligence

The corneal topographers market size in 2026 is estimated at USD 860.9 million, growing from 2025 value of USD 810 million with 2031 projections showing USD 1.16 billion, growing at 6.18% CAGR over 2026-2031. Growth is propelled by the shift from single-purpose keratometry to comprehensive anterior-segment imaging that unites morphological and biomechanical assessment. Rising global myopia prevalence, an aging population demanding premium cataract and refractive procedures, and rapid integration of artificial intelligence are the chief engines of adoption. Cloud-connected, smartphone-based devices are bringing corneal analysis into primary care, while government-backed vision-screening programs create new purchase channels. Competitive intensity stays moderate; incumbents defend positions through portfolio expansions that combine Scheimpflug, Placido, and OCT technologies and through strategic acquisitions targeting workflow integration.

Key Report Takeaways

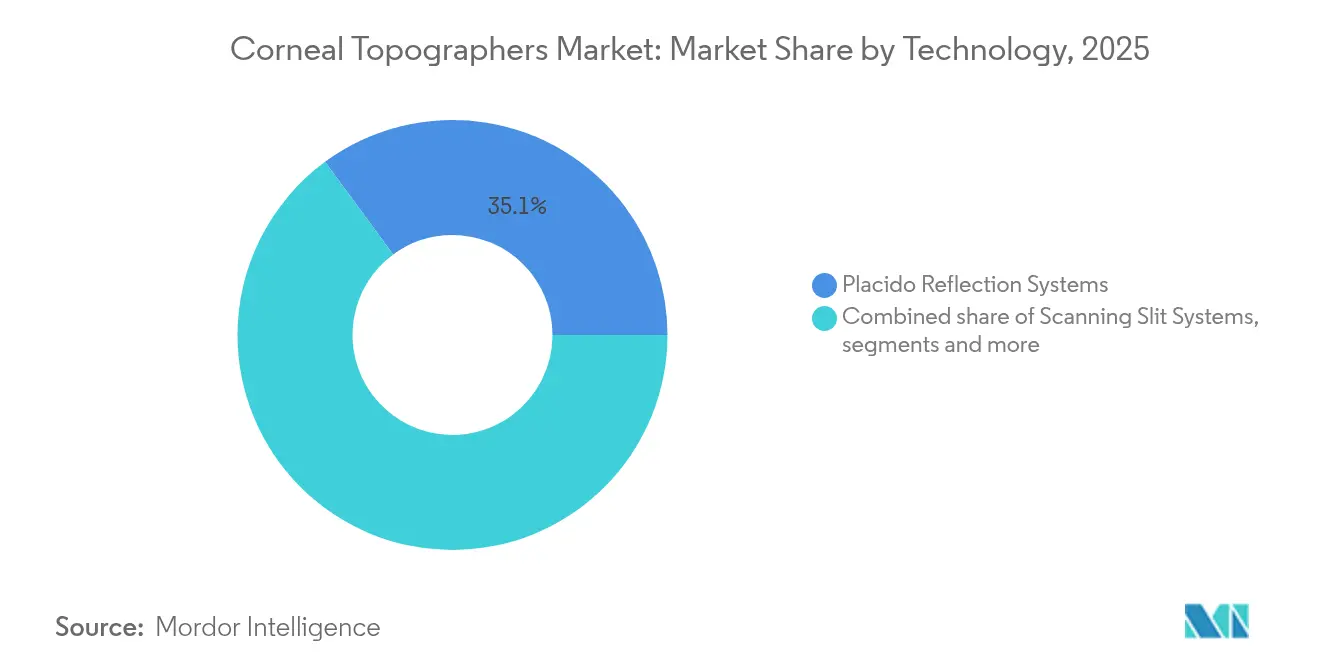

- By technology, Placido reflection systems led with 35.10% of corneal topographers market share in 2025; hybrid multi-modal systems are projected to expand at an 8.47% CAGR through 2031.

- By application, refractive surgery planning accounted for 39.55% share of the corneal topographers market size in 2025 while keratoconus & ectasia diagnosis is advancing at a 7.42% CAGR through 2031.

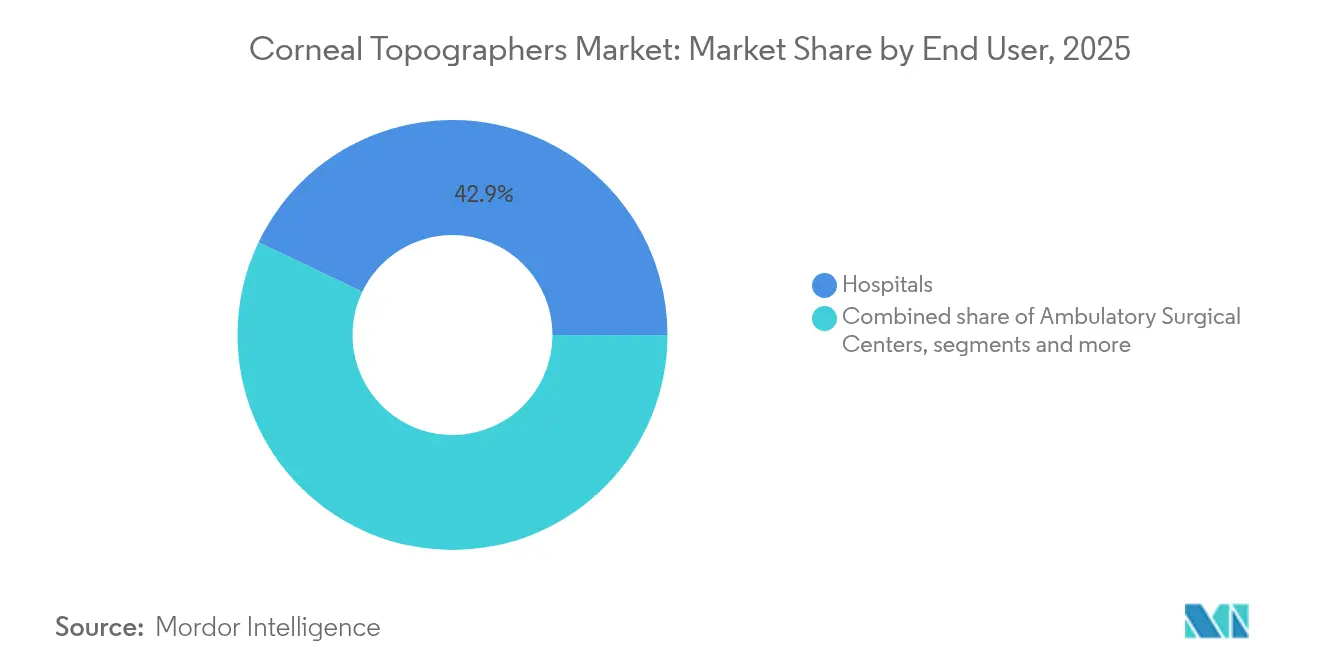

- By end user, hospitals held 42.90% of corneal topographers market share in 2025 whereas ambulatory surgical centers are poised for a 7.93% CAGR between 2026-2031.

- By geography, North America captured 38.40% share of the corneal topographers market size in 2025; Asia-Pacific is slated to register a 8.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Corneal Topographers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of myopia & keratoconus in paediatric & young-adult cohorts | +1.8% | Global, with APAC concentration | Medium term (2-4 years) |

| Aging demographic fuelling cataract & refractive surgeries | +1.2% | North America & EU primarily | Long term (≥ 4 years) |

| Government-funded vision-screening & tele-ophthalmology roll-outs | +0.9% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| AI-enhanced corneal tomography for early ectasia detection | +1.1% | Global, led by developed markets | Medium term (2-4 years) |

| Cloud-connected smartphone topographers opening primary-care channel | +0.7% | Global, accelerated in emerging markets | Short term (≤ 2 years) |

| Contact-lens industry demand for ortho-K fitting data integration | +0.5% | APAC & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising burden of myopia and keratoconus in paediatric and young-adult cohorts

Half the global population is projected to be myopic by 2050, and recent Chinese cross-sectional surveys already report 50.93% prevalence among schoolchildren, with urban rates even higher. Early-stage keratoconus detection is gaining urgency as paediatric incidence reveals under-diagnosed disease, prompting clinicians to widen screening protocols. The corneal topographers market benefits because orthokeratology fitting requires precise elevation maps and axial length measurement to validate myopia-control efficacy. OCULUS introduced Pentacam AXL Wave software in 2025, merging tomography with axial length for integrated myopia management. Lifelong monitoring needs in younger cohorts yield recurrent imaging demand, bolstering device utilization across primary care and specialty clinics.

Aging demographic fuelling cataract and refractive surgeries

The United States 65-plus population is forecast to climb from 56.1 million in 2020 to 73.1 million by 2030, pushing surgical volumes upward. Global cataract procedures are set to rise from 31 million in 2024 to 37 million in 2029, each case mandating corneal mapping to optimise toric and multifocal lens selection. Integration of corneal tomography with optical biometry, exemplified by Pentacam AXL, cuts chair time and heightens refractive predictability. Premium IOL adoption, which commands higher out-of-pocket spending, raises patient expectations for error-free outcomes, preserving demand for high-resolution topography. Consequently, the corneal topographers market secures a stable revenue base in advanced economies with aging demographics.

Government-funded vision screening and tele-ophthalmology roll-outs

Clear regulatory guidance and public-sector investment shorten procurement cycles for portable corneal devices. The FDA issued draft guidance for artificial-intelligence medical devices in June 2025, offering a definitive route to clearance for AI-enabled topographers.[1]Office of the Commissioner, “FDA Issues Comprehensive Draft Guidance for Developers of AI-Enabled Medical Devices,” fda.govIts Health Care at Home initiative encourages remote eye examinations, widening the corneal topographers market across home-based and community clinics. Asia-Pacific governments likewise fund large-scale school screening; India’s med-tech roadmap targets USD 50 billion by 2030, prioritising domestic ophthalmic manufacturing. Smartphone-centric platforms under FDA review aim to eliminate cost barriers for primary care, extending imaging services to rural populations. Public reimbursement that values early detection over late-stage treatment further accelerates uptake.

AI-enhanced corneal tomography for early ectasia detection

Artificial intelligence transforms corneal imaging from descriptive to predictive. The Brazilian BrAIN project fuses Scheimpflug and biomechanical data, raising diagnostic sensitivity for subclinical ectasia beyond either modality alone.[2]Renato Ambrósio Jr., “Advances in Corneal Ectasia Prevention,” CRSToday, crstoday.com Machine-learning models analysing topography attain 94.7% accuracy in flagging refractive-surgery candidates, limiting post-LASIK ectasia risk. The Tomographic and Biomechanical Index, commercialised in Pentacam, synthesises elevation and biomechanical metrics into one risk score clinicians can action in minutes. Earlier identification enables cross-linking at milder disease stages, lowering lifetime management costs. AI firmware updates also extend a system’s useful life, reinforcing annuity revenue streams within the corneal topographers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & maintenance cost of advanced systems | -1.4% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Shortage of skilled ophthalmologists & optometrists in EMs | -0.8% | Emerging markets primarily | Medium term (2-4 years) |

| Limited reimbursement for standalone corneal imaging | -0.6% | North America & EU focus | Short term (≤ 2 years) |

| Substitution threat from multi-modal anterior-segment OCT devices | -0.9% | Global, technology-driven | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High acquisition and maintenance cost of advanced systems

Flagship hybrid platforms list between USD 80,000 and USD 150,000, a figure that can climb 25-40% after import duties in price-sensitive markets.[3]Medical Technology, “MedTech's Digital Supply Chain Revolution,” medical-technology.nridigital.com Semiconductor shortages, which shaved 3-5% off some manufacturers’ 2024 revenue, keep component costs elevated, while sophisticated optics demand periodic calibration and proprietary software subscriptions. Total cost of ownership discourages smaller practices from system upgrades, nudging them to defer purchases or select lower-spec alternatives. Leasing and usage-based models relieve upfront expenditure, yet recurring fees stretch operating budgets. As the corneal topographers market tilts toward cloud-delivered analytics, operating costs risk offsetting capex savings, sustaining price as a long-run restraint.

Shortage of skilled ophthalmologists and optometrists in emerging markets

Ophthalmologist density varies from 114 per million in Japan to single digits in parts of sub-Saharan Africa, capping instrument utilisation potential. Advanced tomography demands adept interpretation; inadequate training can lead to misdiagnosis and underuse. Urban–rural disparities exacerbate the issue, concentrating expertise in major cities and leaving provincial areas under-served. Device makers sponsor workshops, but specialist development spans multiple years. AI-guided analysis mitigates the knowledge gap but regulatory acceptance for autonomous decision support is still nascent. As tele-ophthalmology matures, cross-site collaboration may partially unlock latent demand in the corneal topographers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hybrid Systems Drive Innovation

Placido reflection systems held a commanding 35.10% share in 2025, benefiting from affordability and entrenched clinical workflows. However, their curve-based algorithms struggle with posterior corneal irregularities, nudging ophthalmologists toward elevation-based imaging. Hybrid multi-modal platforms that meld Placido with Scheimpflug or OCT record an 8.47% CAGR, the fastest pace within the corneal topographers market. These workstations deliver pachymetry, posterior curvature, and anterior-segment tomography in a single capture, condensing pre-surgical evaluation into minutes. Scheimpflug-only systems retain relevance for premium intraocular lens planning, yet vendors augment them with AI modules to maintain competitiveness. LED color reflection solutions such as Cassini improve accuracy for post-surgical or scarred corneas by compensating for tear-film artefacts. Smartphone attachments and compact slit-scanning units occupy niche positions targeting primary care and mobile outreach. Continuous firmware upgrades that unlock new analytics postpone hardware obsolescence, binding users to brand ecosystems and reinforcing stickiness across the corneal topographers industry.

The vendor landscape coalesces around integrated imaging suites rather than stand-alone devices. Carl Zeiss Meditec’s Cirrus platform combines topography with OCT; Topcon bundles keratometers with slit-lamp cameras. Competitive stakes lie in algorithmic precision as much as optical hardware, prompting players to invest heavily in deep-learning datasets. Supply chain resilience, particularly access to high-grade image sensors, has become a differentiator after 2024 shortages. As cloud connectivity spreads, secure data pipelines and HIPAA-compliant storage emerge as purchase criteria alongside optical fidelity. Overall, technology diversification within the corneal topographers market fosters tiered pricing that aligns with facility budgets while preserving a premium niche for all-in-one surgical planning stations.

By Application: Surgical Planning Dominates Growth

Refractive surgery planning absorbed 39.55% of 2025 revenue, reflecting the need for precise ablation maps in LASIK, PRK, and SMILE procedures that target plano outcomes. Surgeons rely on combined curvature, elevation, and epithelial thickness data to customise nomograms and reduce enhancement rates. Keratoconus & ectasia diagnosis grows at 7.42% CAGR, propelled by clinical endorsement of early cross-linking regimens and the approach of Glaukos’ Epioxa epi-on therapy to market approval. Cataract IOL selection remains a steady contributor because toric and multifocal lenses demand accurate corneal power to avoid postoperative refractive errors. The corneal topographers market size for contact-lens fitting expands with the USD 3.2 billion orthokeratology segment, requiring detailed sagittal maps to design overnight lenses that modulate corneal curvature for myopia control.

Dry-eye assessment, ocular surface profiling, and research uses round out demand. Software modules quantify meibomian gland dropout and tear-film stability, enabling clinicians to overlay structural and functional insights. Academic laboratories continue to validate novel indices, such as epithelial thickness mapping, extending corneal analytics beyond surgery alone. As AI matures, predictive modelling will cross-link biomechanical, genetic, and tomographic variables, deepening clinical reliance on data-rich platforms. Therefore, diverse use cases insulate the corneal topographers market from cyclic swings in elective surgery volume, sustaining a multi-pronged revenue base across care pathways.

By End User: ASCs Challenge Hospital Dominance

Hospitals retained 42.90% share in 2025 by virtue of broad service mix and capital budgets capable of absorbing high-ticket devices. Yet ambulatory surgical centers grow 7.93% annually as ophthalmology migrates to outpatient settings for cost containment and scheduling flexibility. Smaller footprint, rapid turnover, and bundled case fees compel ASCs to favor compact, multi-function systems that fit restricted pre-op space. Ophthalmology clinics, typically surgeon-owned, invest in topographers to attract premium refractive patients and to deliver end-to-end care under one roof. Optometry and vision-care chains leverage topography for orthokeratology programs and co-managed cataract pathways, integrating outputs into electronic records to streamline referrals. Academic institutes procure advanced modalities for research, though their orders are episodic.

Digital integration now factors heavily into purchase decisions. Cloud dashboards permit ASC staff to review maps remotely, improving throughput. Subscription analytics convert capital purchases into ongoing service revenues, binding facilities to vendor ecosystems. Skills scarcity in rural hospitals amplifies interest in AI-embedded guidance that simplifies map interpretation. Combined, these dynamics redistribute device placements from tertiary hospitals toward nimble outpatient centers, enlarging the corneal topographers market without eroding overall hospital relevance.

Geography Analysis

North America’s 38.40% share in 2025 underscores its mature payer environment, rich R&D ecosystem, and early AI device adoption. Medicare coverage for topography when used for keratoconus or complex IOL planning softens out-of-pocket impact, while private insurers gradually expand indications. Alcon devoted USD 828 million to R&D in 2023, demonstrating industry commitment to continuous innovation. Regulatory scrutiny is rigorous, yet the FDA’s 2025 AI guidance lends transparency, encouraging manufacturers to accelerate algorithm submissions. Market saturation tempers growth, but replacement cycles for systems installed a decade earlier sustain steady demand. Institutions prioritise cybersecurity, pushing vendors to certify data-protection protocols before purchase. Although hospital budget pressure persists, reimbursement alignment preserves the corneal topographers market’s North American revenue base.

Asia-Pacific records the fastest 8.86% CAGR between 2026 and 2031. Skyrocketing myopia prevalence in urban children, exceeding 80% in some East Asian cities, drives parental willingness to pay for ortho-K assessments and early screening. China’s device-approval agency cleared Zeiss Visumax 800 for SMILE pro in February 2025, signalling regulatory openness to advanced refractive technology. India’s middle class spends more on preventive eye care as disposable income rises, while the Asian Development Bank’s USD 75 million health-tech investment facility eases financing for public hospitals. Local manufacturing clusters in Shenzhen and Pune shorten lead times and cut import tariffs, enhancing price competitiveness. However, clinician shortages and uneven reimbursement slow adoption in rural provinces, necessitating mobile screening units and tele-ophthalmology hubs that further diversify the corneal topographers market.

Europe maintains moderate expansion anchored in preventive medicine and ageing demographics. Harmonised MDR regulations streamline conformity assessment, yet Brexit adds complexity for UK market entry. Public health systems fund corneal imaging for cataract and keratoconus indications, though austerity budgets cap premium device penetration in Southern Europe. Middle East and Africa remain nascent but show momentum as oil-exporting nations diversify health spending and training programs expand. South America’s rebound from recent economic soft patches supports ophthalmology equipment tenders in Brazil and Argentina. Across regions, policy directives that valorise early intervention and digital health bolster a consistent upswing in the corneal topographers market.

Competitive Landscape

The corneal topographers market features a moderate concentration. Carl Zeiss Meditec, Topcon, and NIDEK anchor the top tier through global sales networks and contiguous imaging portfolios that range from slit-lamp cameras to hybrid tomography. Zeiss fortified its franchise with the 2024 acquisition of Dutch Ophthalmic Research Center, gaining retina and workflow assets that complement corneal devices. EssilorLuxottica entered the diagnostic arena via a majority stake in Heidelberg Engineering and the purchase of Espansione Group, positioning itself across both surgical and therapeutic verticals. Alcon moved to acquire Lensar in March 2025, integrating femto-laser systems with topography-guided cataract platforms.

Emerging challengers pivot around AI and portability. Avant Technologies’ partnership with Ainnova Tech aims to deliver a low-cost, AI-integrated retinal and corneal camera to remote clinics. Smartphone adapters leverage high-resolution phone cameras, reducing bill-of-materials and widening reach in resource-constrained settings. Meanwhile, semiconductor shortages expose single-source vulnerabilities, prompting OEMs to dual-source critical sensors and processors. Vendors investing in cloud cybersecurity, traceable supply chains, and local service hubs gain a defensible moat against price competition.

Product differentiation now resides as much in analytics as in optics. Proprietary indices like Tomographic Biomechanical Index or Belin/Ambrósio Enhanced Ectasia Display lock users into specific ecosystems through surgical nomograms. Subscription-based software licences smooth revenue and enable over-the-air algorithm upgrades. With FDA and EU regulators scrutinising dataset provenance, firms that amassed longitudinal multicentre databases enjoy an advantage in algorithm validation. As reimbursement codes evolve to recognise AI decision support, competitors able to prove clinical utility will secure premium pricing, sustaining value in the corneal topographers market.

Corneal Topographers Industry Leaders

Topcon Medical Systems Inc

OCULUS Optikgerate GmbH

Ziemer Group AG

Carl Zeiss AG

Cassini Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: China’s regulator approved the Zeiss Visumax 800 femtosecond laser with SMILE pro software, broadening access to advanced refractive surgery.

- February 2025: OCULUS launched the Myopia Software Package for Pentacam AXL Wave, merging axial length and corneal tomography for integrated management.

- December 2024: EssilorLuxottica agreed to acquire Espansione Group, adding non-invasive ophthalmic treatment devices.

- July 2024: EssilorLuxottica took a majority stake in Heidelberg Engineering, reinforcing its diagnostic footprint.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the corneal topographers market as all newly manufactured optical devices that digitally map anterior corneal curvature for diagnostic or surgical planning across hospitals, ambulatory surgical centers, and ophthalmic clinics worldwide. Systems built on Placido reflection, Scheimpflug imaging, scanning-slit, or hybrid multimodal platforms are within scope.

Scope exclusion: handheld keratometers without full-surface mapping and anterior-segment OCT units sold solely for retinal imaging are not considered.

Segmentation Overview

- By Technology

- Placido Reflection Systems

- Scanning Slit Systems

- Scheimpflug Imaging Systems

- Hybrid Multi-modal Systems

- Other Technologies

- By Application

- Refractive Surgery Planning

- Cataract Surgery IOL Selection

- Keratoconus & Ectasia Diagnosis

- Corneal Edema & Dystrophy Assessment

- Contact Lens Fitting

- Soft & RGP Lens Fitting

- Orthokeratology Lens Fitting

- Dry Eye & Ocular Surface Evaluation

- Research & Academic Use

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Ophthalmology Clinics

- Optometry & Vision-care Centers

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with corneal surgeons, optometrists, biomedical engineers, and purchasing heads across North America, Europe, China, India, and Brazil tested desk-research assumptions, refined average selling prices, and verified post-pandemic procedure recovery. Targeted surveys of device distributors and hospital procurement teams further checked shipment mixes and replacement cycles.

Desk Research

Mordor analysts began with openly available data from authorities such as the World Health Organization, U.S. CDC, Eurostat, and China National Health Commission to size patient pools for cataract, keratoconus, and refractive errors. Trade association releases from the American Academy of Ophthalmology, All India Ophthalmological Society, and International Agency for the Prevention of Blindness supplied surgical volumes and screening program statistics. Company 10-Ks, FDA 510(k) databases, patent filings via Questel, and curated news on Dow Jones Factiva informed pricing corridors and launch timelines.

Import and export codes for HS 900219 and HS 901850 were downloaded from Volza to validate regional equipment flows, while academic journals in PubMed clarified adoption rates of Scheimpflug versus Placido technology. The sources cited above are illustrative; many additional materials were consulted for corroboration and gap filling.

Market-Sizing & Forecasting

A top-down construct first linked annual cataract and refractive surgery volumes, screening penetration into the myopic population, and keratoconus prevalence to the addressable demand pool, which was then multiplied by validated device-to-procedure ratios. Select bottom-up cross-checks, supplier shipment roll-ups for six leading brands, and sampled ASP × units-adjusted totals where large divergences appeared. Key variables feeding the model include: 1) global LASIK and SMILE procedure counts, 2) keratoconus incidence per 100,000 inhabitants, 3) average device lifespan, 4) ASP progression by technology, and 5) public reimbursement rates for CPT 92025. Multivariate regression with scenario analysis translated these drivers into a five-year forecast, while ARIMA smoothing captured seasonal tender patterns. Data voids in smaller geographies were bridged with regional propensity factors benchmarked to diagnostic equipment spend per capita.

Data Validation & Update Cycle

Outputs pass three-layer review: statistical anomaly scans, peer analyst audit, and practice-leader sign-off before release. The model is refreshed annually, and extraordinary events such as major product recalls or reimbursement changes trigger an interim update so clients always receive the latest view.

Why Mordor's Corneal Topographers Baseline Is Dependable

Published values often differ because firms pick dissimilar technology mixes, assume unique ASP slopes, or update at uneven intervals. Our study aligns device scope with clinical reality, blends procedure-linked demand signals with shipment intelligence, and refreshes every twelve months, thereby limiting drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.81 billion | Mordor Intelligence | - |

| USD 0.79 billion (2024) | Global Consultancy A | excludes hybrid multimodal units and applies flat ASP |

| USD 0.97 billion (2024) | Industry Association B | uses shipment data without adjusting for dual-modality OCT cross-sales |

The comparison shows that narrower scopes or single-source inputs inflate or depress totals, whereas Mordor's disciplined mix of clinical demand metrics and cross-validated supplier data provides a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

Why are hybrid multi-modal corneal topographers gaining popularity among ophthalmologists?

They provide elevation, pachymetry, and curvature data in one scan, streamlining surgical planning and early ectasia screening while reducing the need for multiple single-function devices.

How is artificial intelligence changing everyday use of corneal topography in clinics?

AI algorithms now flag subtle corneal irregularities and automatically score ectasia risk, allowing non-expert staff to perform preliminary assessments and freeing specialists to focus on treatment decisions.

What makes Asia-Pacific a focal point for new corneal topographer launches?

High myopia prevalence and government-backed school screening programs create large screening volumes, encouraging manufacturers to introduce cost-effective, portable systems tailored to primary-care settings.

In what way do smartphone-based topographers expand access to corneal imaging?

They leverage ubiquitous phone cameras and cloud analytics, enabling basic curvature mapping in rural or resource-constrained clinics that cannot afford full-scale desktop instruments.

How are reimbursement trends influencing purchasing decisions for corneal imaging equipment?

Payers increasingly recognize the cost savings of early disease detection, so facilities are prioritizing devices that integrate diagnostics with workflow software to demonstrate clear clinical value.

Page last updated on: