Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

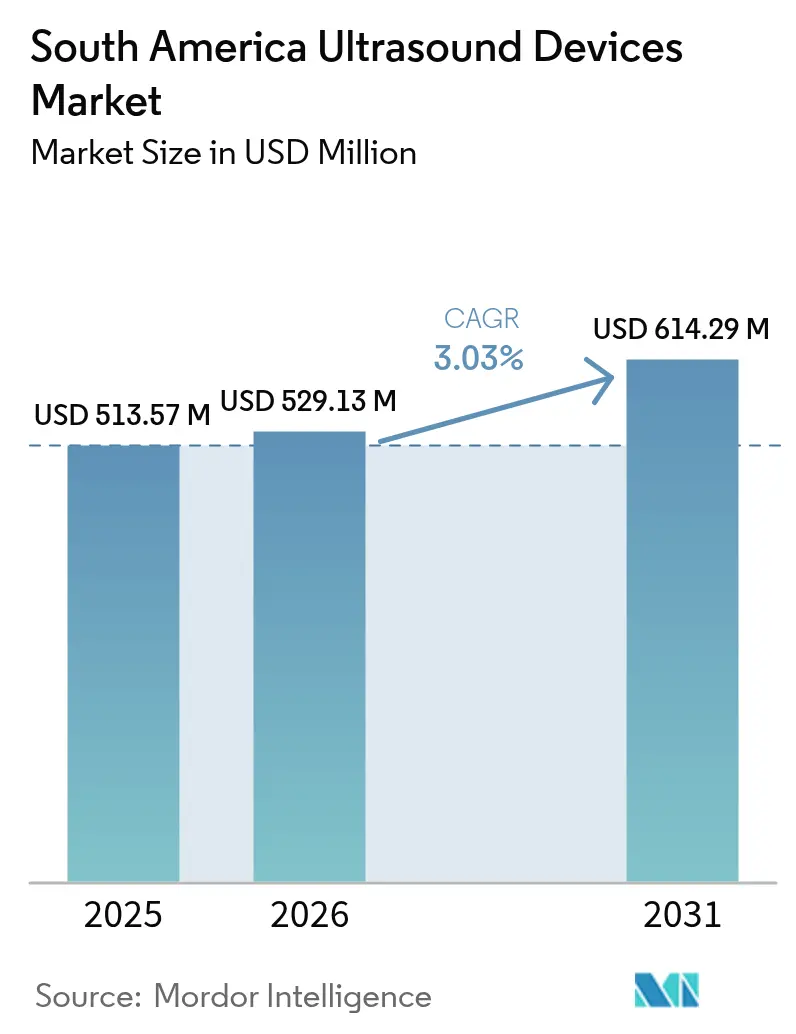

| Base Year Market Size (2025) | USD 513.57 Million |

| Market Size (2026) | USD 529.13 Million |

| Market Size (2031) | USD 614.29 Million |

| Growth Rate (2026 - 2031) | 3.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Ultrasound Devices Market Analysis by Mordor Intelligence

The South America Ultrasound Devices Market size was valued at USD 513.57 million in 2025 and estimated to grow from USD 529.13 million in 2026 to reach USD 614.29 million by 2031, at a CAGR of 3.03% during the forecast period (2026-2031).

Current growth is driven by wider reimbursement coverage, rising non-communicable diseases, and the steady roll-out of AI-enabled and wireless systems that improve workflow efficiency and expand access. Brazil continues to anchor the South America ultrasound devices market through a large installed base, while Argentina is setting the growth pace as public and private investment modernizes imaging infrastructure. Portable models are penetrating secondary cities, addressing physician shortages and catalyzing wider usage across point-of-care settings. High-intensity focused ultrasound (HIFU) is gaining traction as an adjunct therapy in oncology, stimulating incremental demand for next-generation platforms.

Key Report Takeaways

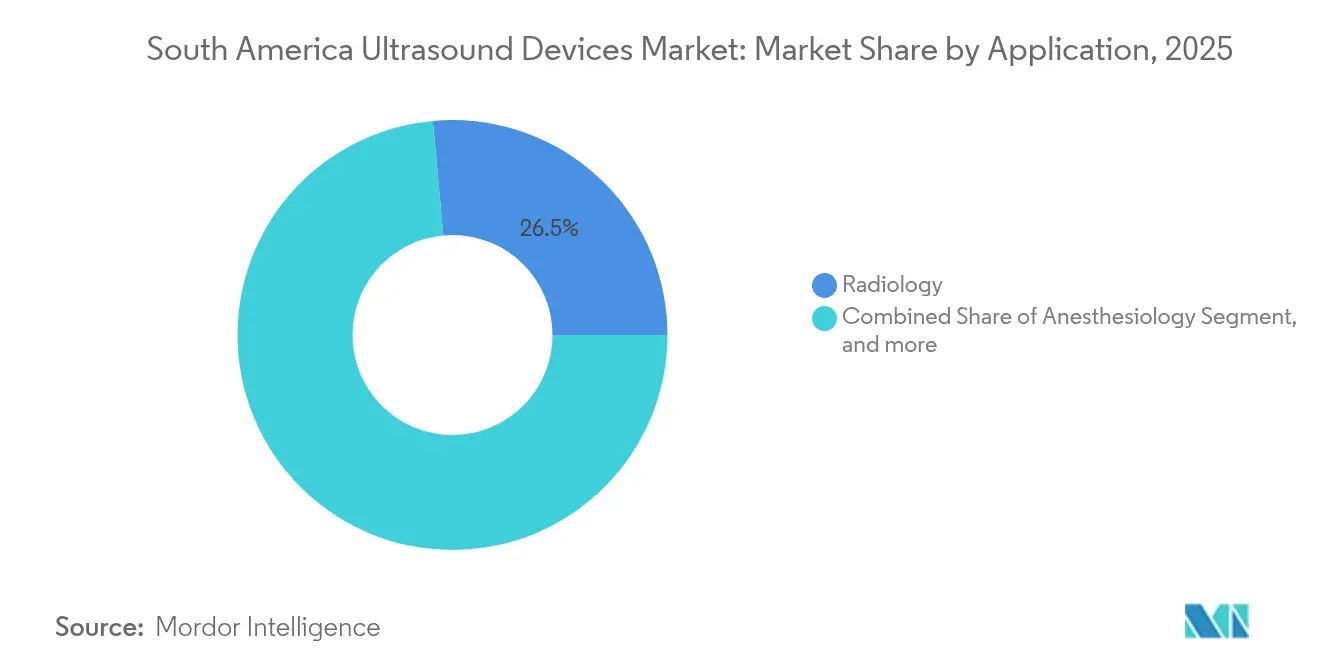

- By application, radiology held 26.46% of the South America ultrasound devices market share in 2025, while anesthesiology is forecast to post a 4.82% CAGR through 2031.

- By technology, 3D/4D imaging commanded 46.88% of the South America ultrasound devices market size in 2025; HIFU is projected to expand at a 5.02% CAGR between 2026-2031.

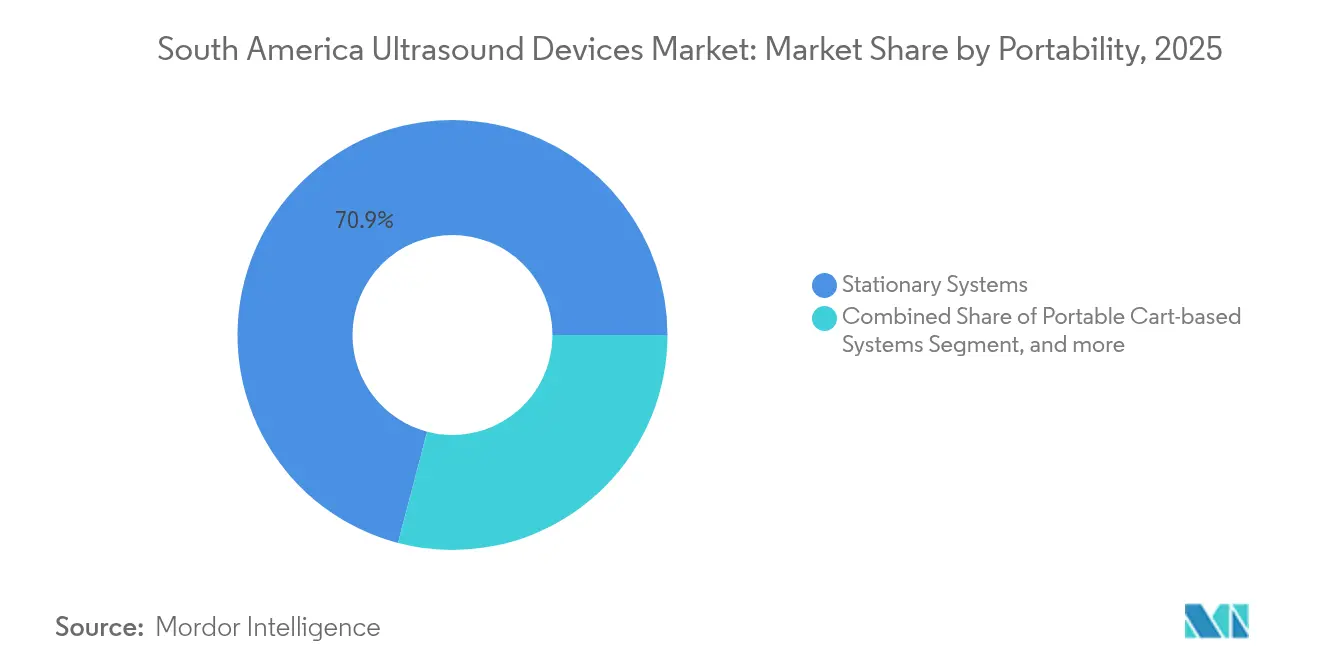

- By portability, stationary systems accounted for 70.92% of the South America ultrasound devices market size in 2025, whereas the hand-held/pocket segment is advancing at a 7.05% CAGR to 2031.

- By end user, hospitals and surgical centers controlled 57.62% of the South America ultrasound devices market size in 2025, and ambulatory care centers are on track for a 6.41% CAGR during 2026-2031.

- By country, Brazil captured 48.35% revenue share of the South America ultrasound devices market in 2025, and Argentina is forecast to deliver a 3.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of imaging reimbursement | +0.8% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Escalating non-communicable disease burden | +1.0% | All South America; highest in Brazil | Long term (≥4 years) |

| Adoption of AI-enabled & wireless solutions | +1.2% | Brazil, Chile, Colombia | Short term (≤2 years) |

| Government and private funding for R&D | +0.5% | Brazil, Argentina | Medium term (2-4 years) |

| Rising cancer incidence driving demand for radiation-free imaging | +0.7% | Colombia, Argentina | Long term (≥4 years) |

| Growth in portable & telemedicine-integrated ultrasound devices | +0.9% | Secondary cities across South America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expansion of Imaging Reimbursement Boosting Ultrasound Adoption

Broader reimbursement schemes are strengthening the South America ultrasound devices market by lowering out-of-pocket costs for patients and supporting provider economics. Brazil’s Medicare now reimburses an average USD 17,500 for histotripsy therapy, encouraging hospitals to procure high-end HIFU systems. Argentina added carotid and femoral ultrasound to preventive screening, revealing carotid plaques in 51% of asymptomatic adults, which underscores early detection value. Colombia extended telemedicine reimbursement to remote ultrasound interpretation, with 86% of facilities using ICTs for maternal care, fueling demand for cloud-connected probes.[1]Eduardo Capasso et al., “ICT Use in Maternal Care Facilities,” who.int These policy shifts reinforce supplier incentives to align product portfolios with reimbursed procedures. Healthy reimbursement further alleviates margin pressure for providers operating in cash-limited public systems.

Escalating Non-Communicable Disease Burden Driving Demand for Cardiac & Abdominal Ultrasound

Non-communicable diseases remain the largest mortality contributor in the region and elevate routine imaging needs. Colombia recorded 117,620 new cancer cases in 2024, accelerating uptake of real-time ultrasound for tumor staging and guidance. Vascular ultrasound studies in Argentina detected subclinical carotid plaques in more than half of tested adults, signifying a silent surge in atherosclerosis. Brazil’s elderly population is set to reach 37.8% by 2070, and life expectancy could climb to 83.9 years, broadening chronic disease management workloads. Continuous imaging underpins timely intervention, particularly for cardiac, abdominal, and vascular assessments. Consequently, hospitals are enlarging their ultrasound fleets while outpatient centers focus on portable devices for routine follow-up.

Adoption of AI-Enabled & Wireless Ultrasound Solutions Enhancing Workflow Efficiency

AI algorithms now automate fetal measurements and improve organ segmentation, reducing scan times by up to 40% on devices such as GE HealthCare’s Voluson Signature.[2]“Voluson Signature Launch,” gehealthcare.com Workflow acceleration helps mitigate shortages of certified sonographers, a major obstacle outside capital cities. Wireless probes integrate seamlessly with smartphones, fostering point-of-care use in ambulances and community clinics. AI-assisted interpretation expands the South America ultrasound devices market by enabling less-skilled personnel to conduct basic exams, while cloud connectivity supports specialist review. Rising connectivity in Chile and Colombia bolsters remote collaboration, accelerating decision-making and optimising resource allocation.

Government and Private Funding for R&D in Ultrasound Imaging

Policy makers recognise ultrasound’s cost advantage over CT or MRI and are channeling funds into next-generation systems. Argentina secured a USD 200 million Inter-American Development Bank loan in 2023 to enlarge diagnostic imaging coverage, directly benefiting public hospitals.[3]“Inter-American Development Bank Loan for Argentina Imaging,” iadb.org Venture investors committed USD 102 million to histotripsy developer HistoSonics, highlighting strong appetite for therapeutic ultrasound platforms. These inflows encourage collaboration between academia and suppliers, focusing on improved transducer materials, battery life, and AI firmware. Over the medium term, faster innovation cycles will broaden clinical indications and maintain pricing flexibility, reinforcing the South America ultrasound devices market growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged & divergent regulatory approval processes | -0.6% | All South America; strongest in smaller markets | Medium term (2-4 years) |

| Limited availability of certified sonographers and radiologists | -0.9% | Secondary cities across all countries | Long term (≥4 years) |

| High equipment costs & maintenance burden | -0.7% | Low-income regions across South America | Short term (≤2 years) |

| Limited access in remote & underserved regions | -0.5% | Rural areas in Andes and Amazon corridors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Prolonged & Divergent Regulatory Approval Processes

Medical device firms face heterogeneous and often lengthy approval frameworks that slow product launches. Brazil’s ANVISA requires Class III and Class IV systems to obtain full registration and Brazil-Good Manufacturing Practice certificates, extending timelines by 5-6 months. Although 2024 regulations permit reliance on foreign approvals, discordant documentation rules across neighboring countries still impose added compliance cost. The constraint curbs initial market entrance for smaller innovators and prolongs access to the latest features, dampening the competitive intensity within the South America ultrasound devices market.

Limited Availability of Certified Sonographers and Radiologists in Secondary Cities

Specialist shortages limit service expansion beyond metropolitan hubs. The PROVAR+ echocardiography program in Brazil demonstrated that simplified protocols executed by nurses uncovered major heart disease in 29.2% of patients, signalling the hidden burden due to limited screening capacity. Rural hospitals often operate a single ultrasound unit staffed by rotating technicians, leading to long wait lists. This bottleneck can delay diagnoses, prompt patients to travel to urban centers, and constrain equipment utilisation rates, collectively tempering growth momentum in the South America ultrasound devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Diagnostic Dominance Amid Accelerating Anesthesiology Growth

Radiology upheld supremacy in the South America ultrasound devices market with 26.46% share in 2025, backed by its integral role in multi-specialty diagnostics and the growing integration of AI-powered measurement tools. The South America ultrasound devices market size for radiology benefited from faster workflow, as seen with Siemens Acuson Sequoia 3.5 that automates organ labeling. Cardiology and gynecology/obstetrics remain sizable due to heightened screening, while critical care leverages point-of-care scanning for rapid triage.

Anesthesiology is projected to log a 4.82% CAGR through 2031, marking the quickest rise among applications. Wider uptake of ultrasound-guided nerve blocks improves procedural success and patient outcomes; Mindray’s regional anesthesia education series strengthens clinician proficiency. Hospital procurement teams now bundle portable probes with operating-room carts, sustaining momentum. Rising surgical volumes and enhanced patient safety protocols will continue to propel anesthesiology’s contribution to the South America ultrasound devices market.

By Technology: 3D/4D Lead as Therapeutic HIFU Accelerates

The 3D/4D technology tier captured 46.88% of the South America ultrasound devices market share in 2025, driven by superior volumetric clarity essential for fetal assessments and oncology staging. AI-enabled platforms like GE Voluson Signature 20 shorten second-trimester exams by 40%, underscoring efficiency gains. Conventional 2D remains relevant through AI-enhanced image optimisation, while Doppler supports cardiovascular evaluation.

HIFU systems will record a 5.02% CAGR to 2031, the fastest among technologies, buoyed by non-invasive tumor ablation success. Liver cancer histotripsy cases surpassing 300 globally demonstrate clinical acceptance. Expansion into prostate and uterine fibroid therapy will widen indications, adding momentum to the South America ultrasound devices market size growth for therapeutic platforms.

By Portability: Stationary Systems Retain Scale as Handheld Units Surge

Stationary consoles delivered 70.92% revenue in 2025 owing to comprehensive transducer arrays and full imaging suites required by tertiary hospitals. Acoustic Intelligence embedded in Mindray Resona A20 enhances diagnostic certainty, sustaining demand. Service agreements and upgrade pathways further entrench installed bases among large institutions.

Handheld/pocket models will progress at a 7.05% CAGR, more than double the overall market rate. Butterfly iQ3's lighter design and 3D capabilities resonate with emergency and primary-care clinicians. Cloud-based quality assurance aids training, compressing the skills gap. As procurement policies shift toward mobility, portable cart systems bridge functionality and transportability, reinforcing incremental adoption across the South America ultrasound devices market.

By End User: Hospital Leadership with Outpatient Momentum

Hospitals accounted for 57.62% of 2025 sales and continue to serve as reference sites for new product launches, including GE Versana Premier equipped with AI tools for multi-specialty workflows. Intensifying surgery throughput and the need for intraoperative guidance uphold console purchases.

Ambulatory care centres should clock a 6.41% CAGR to 2031 as cost-conscious payers steer procedures to outpatient settings. Compact and battery-operated units allow fast turnover and lower capital expenditure. Diagnostic imaging centres maintain volume for specialised exams, while physician offices and home-care programs gradually adopt mobile probes, extending market reach.

Geography Analysis

Brazil controlled 48.35% of the South America ultrasound devices market in 2025 underpinned by the continent’s largest healthcare budget and ongoing reimbursement expansion. ANVISA’s 2024 acceptance of foreign regulatory certificates trims approval timelines and encourages first-to-market launches. Tele-cardiology pilots like PROVAR+ illustrate remote reading feasibility, increasing utilisation across public clinics.

Argentina is forecast to achieve a 3.99% CAGR, benefiting from a USD 600 million credit line aimed at imaging upgrades. Prevalence of subclinical atherosclerosis revealed via vascular ultrasound highlights unmet need and supports volume growth. Chile and Colombia advance on the back of digital health readiness, with Colombia’s 86% ICT adoption in maternal care underpinning tele-ultrasound uptake.

Rest of South America, including Peru and Uruguay, exhibits sizeable whitespace for portable devices that bypass infrastructure constraints, while regulatory simplification could expedite entry in smaller markets. Steady urban migration and rising chronic disease prevalence ensure sustained demand, expanding the South America ultrasound devices market footprint across diverse economic contexts.

Regulatory Landscape

Regulatory oversight for ultrasound devices in South America is country-specific, with Brazil, Argentina, and Colombia setting the pace on registration, post-market controls, and traceability. In Brazil, ANVISA applies quality and safety requirements for medical ultrasound equipment under Instrucao Normativa (IN) No 96 (2021), including acceptance and quality control testing practices that affect hospital commissioning and service schedules. ANVISA is also advancing Unique Device Identification (UDI) labeling under RDC No 591 (2021), with UDI labeling requirements already in force for Class IV devices since July 2025 and for Class III devices since January 2026.

Digital traceability infrastructure is becoming a practical compliance gate for manufacturers and importers. ANVISA published IN No 426 (2026) establishing the SIUD database for UDI data submission, effective March 1, 2026, increasing the need for aligned labeling, packaging, and data governance for ultrasound system components placed on the Brazilian market. In Argentina, ANMAT issued Disposicion 236/2026 (February 2026) covering risk Class I and II medical products (and certain IVD products) of foreign origin, while establishment habilitation processes are increasingly handled through digital systems such as THEMIS (per Disposicion 8799/2025). In Colombia, INVIMA is implementing UDI and semantic coding requirements under Resolucion 1405 of 2022, including mandatory UDI-DI reporting deadlines (for example, a February 9, 2026 requirement for certain Class IIa devices registered before February 2024), reinforcing cross-country emphasis on device identification and lifecycle surveillance.

Competitive Landscape

The vendor landscape shows moderate concentration, dominated by global majors yet open to niche challengers. GE HealthCare enlarged its portfolio through the USD 51 million purchase of Intelligent Ultrasound in July 2024, reinforcing AI capabilities. Philips, Siemens Healthineers, and Samsung Medison invest heavily in ergonomic transducers and cloud ecosystems. Samsung’s acquisition of Sonio underlines an escalating focus on fetal AI.

Portable specialists Butterfly Network and Clarius Mobile Health target frontline clinicians with subscription-based imaging platforms. Partnerships such as Mindray–TeleRay integrate streaming to support remote interpretation and training. Emerging robotic solutions like FARUS automate thyroid scanning, hinting at future disruption that might reset competitive boundaries within the South America ultrasound devices market.

South America Ultrasound Devices Industry Leaders

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

Canon Medical Systems Corporation

FUJIFILM Holdings Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space in South America remains in secondary cities and underserved corridors where point-of-care ultrasound can bypass infrastructure constraints and specialist shortages. Butterfly Network expanded availability of its iQ+ and iQ3 handheld ultrasound devices and mobile application in Brazil via authorized distribution partners in 2026, broadening access to frontline settings and increasing competitive intensity in the handheld/wireless segment where subscription and app-based workflows are part of the offering. Similar whitespace exists for cloud-connected probes and workflow tools that support remote oversight, aligning with telemedicine-integrated ultrasound adoption in countries such as Colombia.

Institutional modernization programs and procurement centralization create another opportunity axis, particularly in Brazil where the Ministry of Health launched a National Investment Plan for the SUS Medical Device Park for 2026-2031, coordinated through the CT-Equipo technical chamber to guide technology upgrades and access to diagnostics. Suppliers that align product configurations, service models, and interoperability to public-sector workflows can compete for replacement and fleet expansion cycles in hospitals and outpatient networks. At the same time, tightening traceability requirements are shaping go-to-market priorities: ANVISA has been rolling out UDI obligations and the SIUD database (effective March 2026), making data readiness, labeling compliance, and local regulatory operations a differentiator for sustained participation across Brazil and, by extension, for multi-country launches where UDI and digital reporting are increasingly mirrored by regulators such as ANMAT and INVIMA.

Recent Industry Developments

- July 2026: Butterfly Network expanded commercial availability of its iQ+ and iQ3 handheld ultrasound devices and its mobile application in Brazil through authorized distribution partners. The move broadens access to handheld scanning in point-of-care settings and increases competitive intensity in the handheld/wireless segment where subscription and app-based workflows are part of the offering.

- May 2025: Argentina's ANMAT advanced establishment habilitation processes through the THEMIS digital system under Disposicion 8799/2025, signaling regulatory digitalization progress that affects how foreign-origin medical devices are registered and monitored.

- July 2024: GE HealthCare acquired Intelligent Ultrasound for USD 51 million, strengthening its AI ultrasound software and automation portfolio and reinforcing the shift toward AI-enabled workflows that address sonographer shortages.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from ultrasound systems used for medical imaging and procedure guidance across South America, including sales into hospitals, surgical centers, and other care settings. The scope includes both stationary and portable equipment.

Scope exclusions: Standalone service revenues from imaging procedures and installation-only contracts are not counted unless they are bundled within the device sale.

Segmentation Overview

- By Application

- Anesthesiology

- Cardiology

- Gynecology / Obstetrics

- Musculoskeletal

- Radiology

- Critical Care

- Other Applications

- By Technology

- 2D Ultrasound Imaging

- 3D & 4D Ultrasound Imaging

- Doppler Imaging

- High-intensity Focused Ultrasound (HIFU)

- Other Technologies

- By Portability

- Stationary Systems

- Portable Cart-based Systems

- Handheld / Wireless Systems

- By End User

- Hospitals & Surgical Centers

- Diagnostic Imaging Centers

- Ambulatory Care & Emergency Centers

- Other End Users

- By Country

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the healthcare and medtech context across South America, country by country, so the demand pool aligns with how ultrasound devices are procured and used locally. We draw on public sources such as PAHO health statistics, World Bank macro and health spending indicators, WHO datasets where relevant, and UN Comtrade trade flows for medical devices as directional signals.

To ground the market in purchase behavior, we also review tender and procurement portals where available, local regulatory and device registration notes, and manufacturer public materials such as annual reports and investor presentations. Patent databases are checked to understand technology direction, including Doppler and 3D or 4D features, and to see where innovation is concentrated. The sources listed here are illustrative, and additional public and paid sources were used for collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work is used to test what is hard to see in public data, especially purchase cycles, replacement rates, and how portability preferences change by care setting. We speak with manufacturers, distributors, hospital buyers, radiology and OB-GYN users, and biomedical engineering teams across Brazil, Argentina, and the rest of South America, and then use the inputs to confirm assumptions and align pricing and volume logic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 41% | EMEA: 33% |

| Smaller Players: 14% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

The sizing model begins with a top-down build where healthcare activity and equipment adoption are translated into device demand for South America, followed by a country split that reflects relative procedure intensity and installed base maturity. To keep totals realistic, selective bottom-up checks are added, such as sampled ASP times unit volumes from channel feedback, along with supplier and distributor sell-in patterns. The model is adjusted when the two views do not align.

A few inputs that materially shape the totals include the share of portable systems in annual procurement, replacement cycles for cart-based units, mix shifts between 2D and advanced modalities (3D or 4D and Doppler), and the end-user balance between hospitals and other care sites. Where the data is thin for smaller countries, we fill gaps using proxy indicators such as population, direction of healthcare spend, and import trends, then validate the implied per-facility equipment intensity with interviews.

For forecasting, scenario analysis is applied so the outlook reflects realistic purchasing constraints and upgrade timing, rather than a single straight-line growth path. Assumptions on pricing movement, modality mix, and public procurement pacing are carried forward only after they match the consensus signals we heard from local channel and provider respondents.

Data Validation & Update Cycle

Validation is done by checking the model against independent signals, including trade direction, procurement visibility, and whether the implied installed base replacement flow fits what users report. When outliers appear, assumptions are revisited and, where needed, respondents are re-contacted to confirm whether the change is a one-time event or a lasting shift.

Before sign-off, the model is reviewed in steps so calculation logic, unit economics, and country splits remain consistent with the market story. Reports are refreshed annually, and interim updates are made when material events occur, such as policy changes, currency moves that affect device pricing, or a notable shift in public purchasing. Right before delivery, we run a final pass so clients receive the most up-to-date view available at that time.

Mordor Intelligence's South America Ultrasound Devices Market Market Estimate Compared With Other Published Estimates

Published market values for ultrasound devices in South America can vary even when they appear to cover the same topic. The gaps typically come from differences in geography coverage, what is counted as an ultrasound device, the pricing basis used, and how older base years are carried forward.

The main gap comes from mixing Latin America totals or including therapeutic ultrasound in the same pool. Mordor Intelligence counts only the South America ultrasound devices scope using a device-revenue lens, and it validates pricing and modality mix (2D, Doppler, and 3D or 4D) through local channel checks. Currency timing also matters, since some publishers convert at a single annual rate while others blend periods, which changes USD totals in volatile years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 513.57 M (2025) | |

| Regional Consultancy A | USD 715.00 M (2024) | Uses a different base year and applies a faster growth curve through 2031, with limited clarity on price-mix validation and whether adjacent device categories are included in the same revenue pool. |

| Industry Publisher B | USD 904.80 M (2023) | Covers Latin America rather than South America only, and the scope explicitly includes diagnostic and therapeutic ultrasound, which lifts totals versus a diagnostic device-only view in the region. |

The comparison shows that geography coverage and what is counted as an ultrasound device drive most of the spread, followed by base-year choice and USD conversion timing. By tying the total to clear demand and mix variables and then re-checking them with local interviews, the estimate stays traceable and easier for decision-makers to replicate and stress-test.

Key Questions Answered in the Report

What is the current size of the South America ultrasound devices market?

The South America ultrasound devices market size is USD 529.13 million in 2026 and is projected to reach USD 614.29 million by 2031.

Which technology segment is growing the fastest?

High-intensity focused ultrasound (HIFU) is expanding at a 5.02% CAGR due to its non-invasive oncology applications.

Why are handheld ultrasound devices gaining popularity?

Handheld units deliver near-cart image quality, cost less, and support telemedicine, enabling wider access in secondary cities and rural areas.

How does reimbursement influence market growth?

New reimbursement codes, such as Brazil’s coverage for histotripsy therapy, improve hospital ROI and hasten adoption of advanced ultrasound systems.

Which country is the fastest-growing market?

Argentina is forecast to grow at a 3.99% CAGR through 2031, powered by public-sector imaging upgrades and rising preventive screening.

What are the main barriers to wider adoption?

Extended regulatory timelines, specialist shortages in non-urban locations, and high equipment costs remain key restraints across the region.

Page last updated on: