Continuous Integration Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

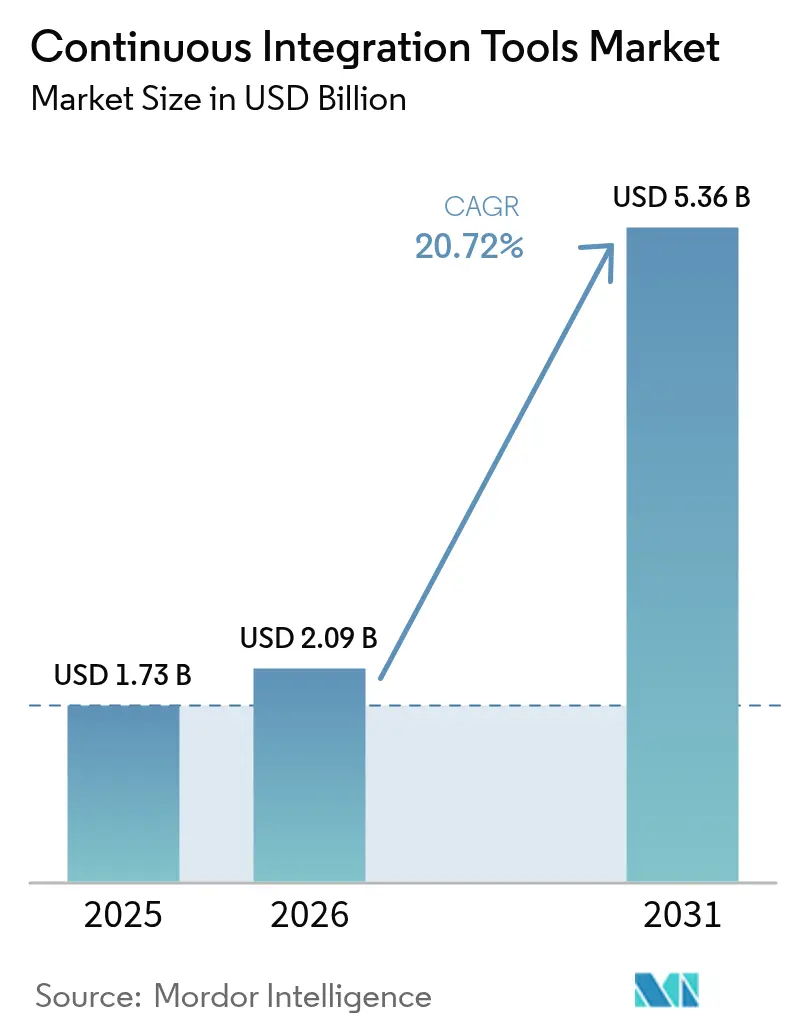

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 20.72% CAGR |

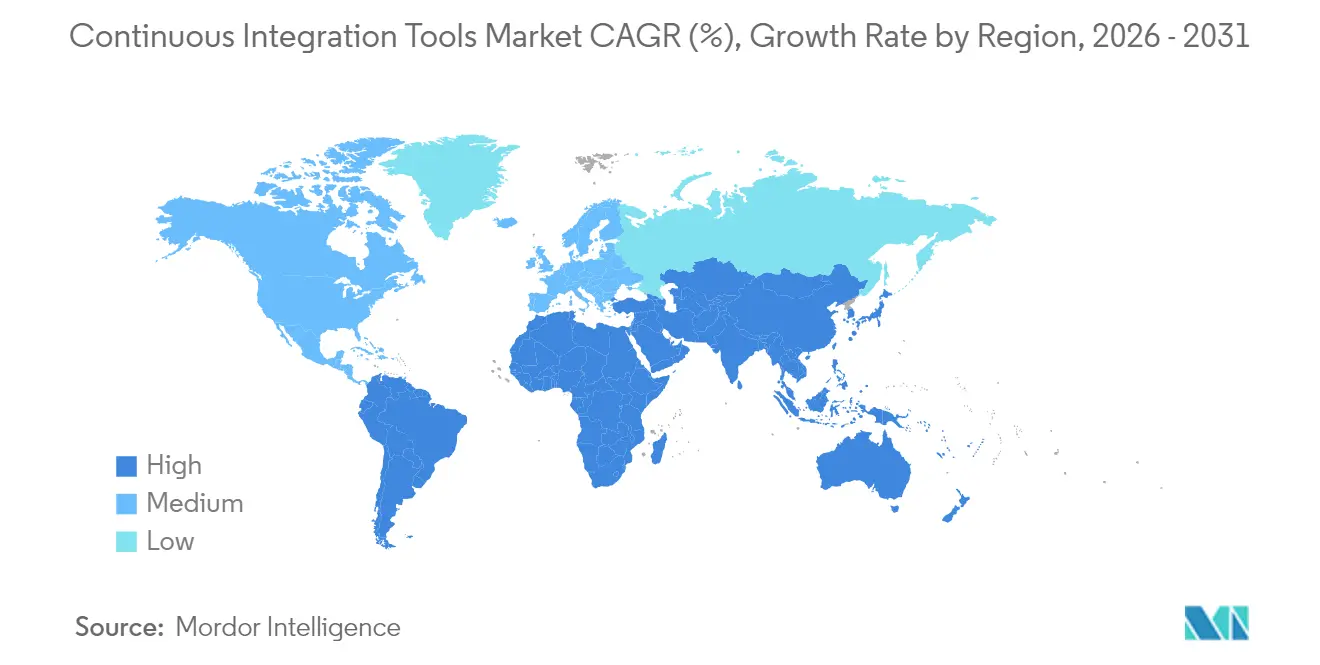

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Continuous Integration Tools Market Analysis by Mordor Intelligence

The Continuous Integration Tools Market size was valued at USD 1.73 billion in 2025 and estimated to grow from USD 2.09 billion in 2026 to reach USD 5.36 billion by 2031, at a CAGR of 20.72% during the forecast period (2026-2031). This rapid lift stems from enterprises compressing release cycles to hours, adopting multi-cloud architectures, and embedding security checks earlier in the pipeline. Vendors that align with AI-assisted coding, supply chain security automation, and hybrid deployment flexibility are capturing outsized demand. Cloud-native SaaS adoption remains a leading trend, but it is no longer dominant. Regulated industries are increasingly piloting hybrid models to keep sensitive workloads on-premises while maintaining cloud scalability. Competitive intensity is rising as well-funded platforms expand into end-to-end DevSecOps suites, while open-source incumbents defend their share through plugin ecosystems and enterprise support offerings.

Key Report Takeaways

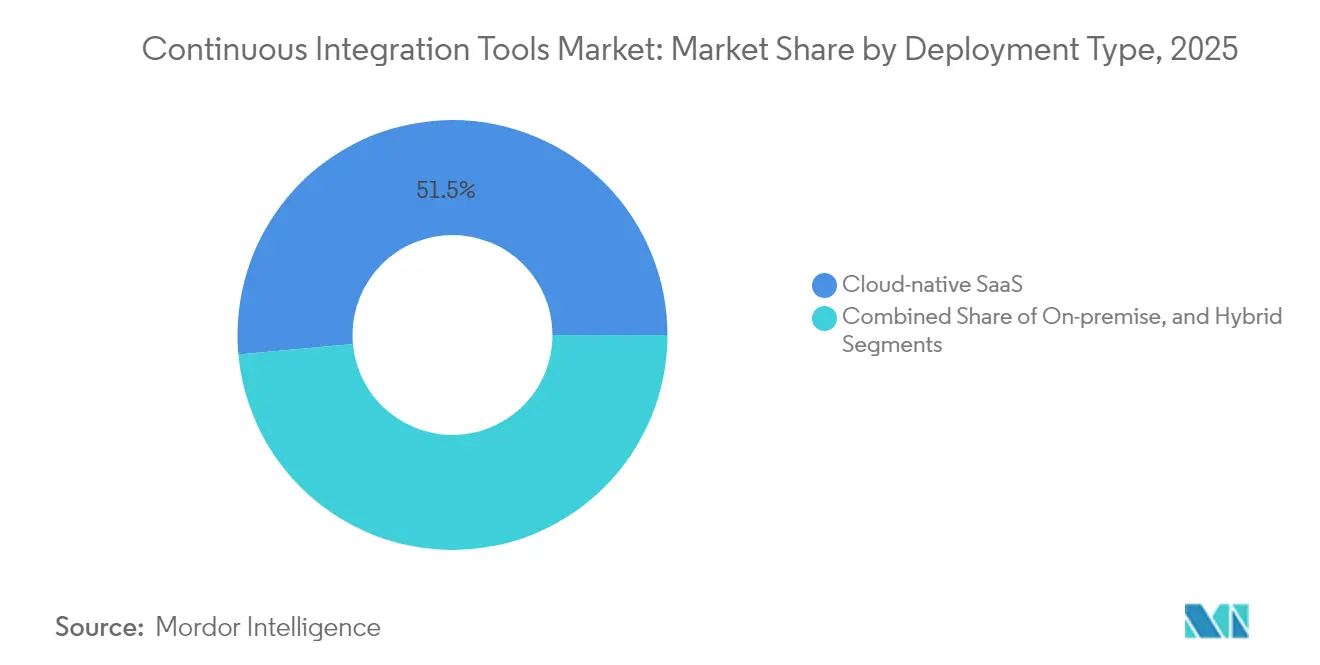

- By deployment type, cloud-native SaaS held 51.45% of the continuous integration tools market share in 2025, while hybrid deployment is projected to expand at a 15.52% CAGR through 2031.

- By organization size, large enterprises commanded a 60.58% share of the continuous integration tools market size in 2025; small and medium enterprises are expected to advance at an 11.22% CAGR through 2031.

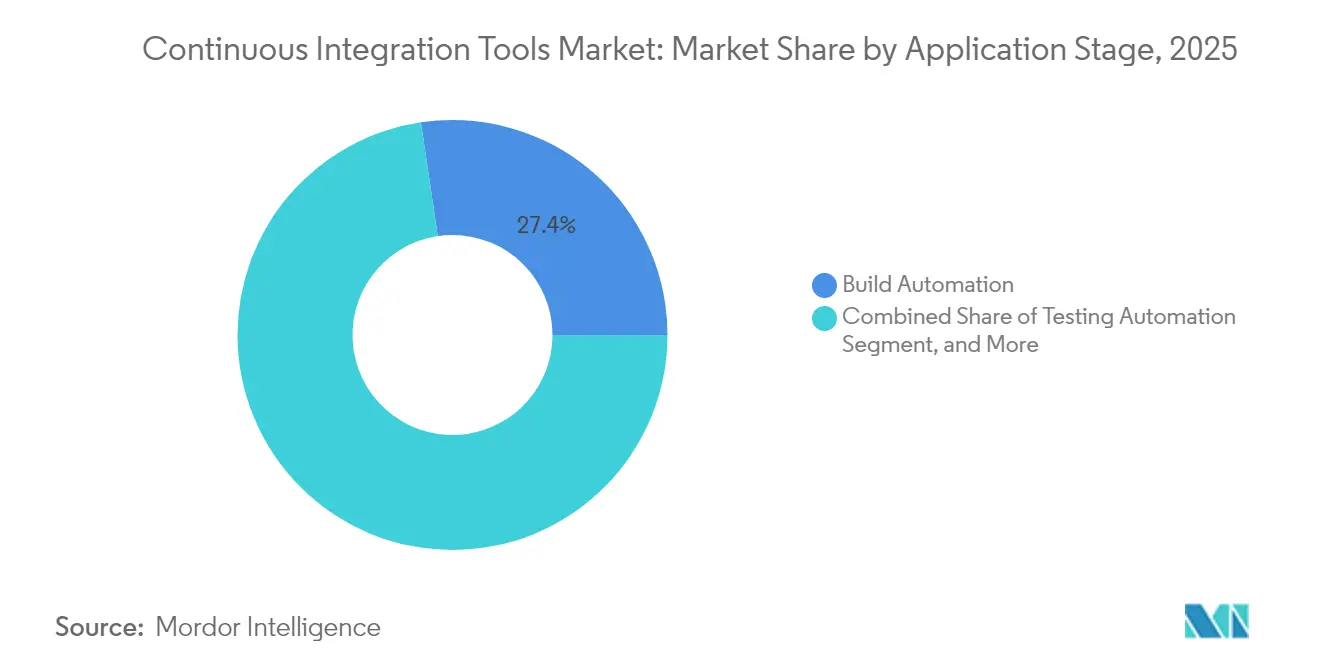

- By the application stage, build automation is expected to lead with a 27.35% revenue share in 2025; testing automation is projected to grow at a 16.10% CAGR through 2031.

- By end-user industry, IT and telecommunications captured 26.12% of the continuous integration tools market in 2025, whereas the healthcare and life sciences sector is projected to post the fastest growth of 14.28% CAGR through 2031.

- By geography, North America accounted for 36.05% of 2025 revenue, while Asia-Pacific is forecast to post a 14.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Continuous Integration Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing DevOps adoption and shorter releases | +6.2% | North America, Europe | Medium term (2-4 years) |

| Rising cloud-native software development | +5.8% | Global; strong Asia-Pacific momentum | Long term (≥ 4 years) |

| Remote/hybrid work model expansion | +3.4% | North America, Europe | Short term (≤ 2 years) |

| AI-assisted coding lifts build frequency | +4.1% | North America, Europe, and and emerging Asia-Pacific | Medium term (2-4 years) |

| Shift-left security mandates | +2.9% | United States, European Union | Long term (≥ 4 years) |

| Supply-chain security focus (SBOM) | +2.2% | Government and regulated sectors worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing DevOps adoption and need for shorter release cycles

Enterprises are rearchitecting their delivery pipelines to match cloud-native competitors that deploy dozens of times a day. An IBM 2024 survey reveals that 83% of executives rank modernization as a top priority, yet only 27% have completed the transition [1]Gurpreet Singh, “Application Delivery Future,” IBM Think, ibm.com. That execution gap fuels sustained investment in platforms that collapse build, test, and deploy into a single automated workflow. Integrated tool chains also reduce handoffs, eliminating latency caused by point solutions. Consequently, vendors offering consolidated suites are steadily displacing standard-built servers in the continuous integration tools market.

Rising cloud-native software development

The global stock of cloud-native applications is expected to hit 750 million by 2025. Containerized microservices require CI/CD pipelines that can orchestrate concurrent builds, dynamic test environments, and GitOps-style deployments. Legacy solutions, such as self-hosted Jenkins, rely on plugins to meet those needs, creating additional maintenance overhead. Enterprises therefore gravitate toward offerings with native Kubernetes integration and multi-cloud support, reinforcing hybrid and SaaS models inside the continuous integration tools market.

AI-assisted coding increases build frequency

GitHub Copilot surpassed 15 million users in 2025, quadrupling its user base year-over-year. AI-generated pull requests raise the volume of builds that must execute continuously while maintaining quality gates. Platforms are responding with intelligent test selection, automated remediation, and predictive failure analytics. Solutions that incorporate these AI-driven guardrails reduce developer toil and unlock faster cycle times, strengthening their foothold in the continuous integration tools market.

Expansion of remote/hybrid work models

Permanent distributed teams push organizations toward cloud-hosted and browser-based CI services that developers can reach from anywhere. CircleCI’s sustained revenue climb to USD 750 million illustrates demand for SaaS pipelines among globally dispersed teams. Small enterprises, in particular, avoid upfront infrastructure costs through pay-as-you-go consumption, thereby widening addressable demand and democratizing capabilities once confined to Fortune 500 budgets within the continuous integration tools market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skill shortages in platform engineering | -3.8% | North America, Europe | Medium term (2-4 years) |

| Legacy toolchain complexity and migration cost | -2.9% | Global, large enterprises | Long term (≥ 4 years) |

| Escalating cloud cost scrutiny (FinOps) | -2.1% | Cost-sensitive enterprises worldwide | Short term (≤ 2 years) |

| Regulatory data-sovereignty for SaaS CI | -1.7% | European Union, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skill shortages in CI/CD platform engineering

The demand for personnel who can script pipelines, secure Kubernetes clusters, and manage GitOps deployments exceeds the supply, driving hiring delays and increased consulting fees. The scarcity elevates the total cost of ownership and slows adoption timelines. Vendors respond with low-code pipeline designers and managed services that reduce the need for in-house expertise. Still, the talent gap hinders the adoption velocity of continuous integration tools in complex enterprise environments.

Legacy toolchain complexity and migration costs

Enterprises that customized Jenkins with hundreds of plugins face months of refactoring and retesting before switching platforms. The risk of downtime during migration leads many organizations to postpone upgrades despite recognized productivity benefits. This inertia grants entrenched incumbents a buffer against newer entrants, tempering the overall growth potential of the continuous integration tools market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid models bridge enterprise security gaps

Cloud-native SaaS deployment retained revenue as it removes infrastructure maintenance and accelerates onboarding. Hybrid deployment, however, is forecast to log the highest 15.52% CAGR, underscoring that regulated buyers want local control over sensitive workloads. The continuous integration tools market size for hybrid implementations is projected to expand sharply as vendors roll out flexible deployment blueprints that mirror zero-trust recommendations from NIST.SP 800-204D. SaaS providers that incorporate private-agent execution or customer-managed encryption keys address compliance barriers without compromising the usability edge that originally drove cloud adoption.

Enterprises increasingly adopt a “best of both” stance, hosting build workers on-premise while leveraging cloud dashboards for visibility and analytics. This architecture limits data egress yet preserves elastic scaling for burst workloads, a balance that resonates within the continuous integration tools market. Vendors able to synchronize artifact stores, secrets management, and policy enforcement across environments are emerging as preferred partners.

By Organization Size: SME acceleration democratizes enterprise capabilities

Large enterprises currently hold 60.58% revenue share, reflecting their historical lead in DevOps maturity and resource availability. Nonetheless, the continuous integration tools market size attributed to small and medium enterprises is rising quickly due to the affordability of consumption-based pricing and freemium tiers. CircleCI’s entry-level plans at USD 360 per seat illustrate low barriers for start-ups. As SMEs scale, they naturally grow usage hours, boosting vendor recurring revenue.

The democratization trend broadens the customer base and pushes vendors to streamline onboarding with opinionated templates, automated governance, and embedded security scanning. Those improvements also benefit large organizations seeking to reduce internal overhead, creating a virtuous cycle that underpins the expansion of the continuous integration tools market.

By Application Stage: Testing automation becomes the differentiation battleground

Build automation is a baseline necessity, retaining the largest 27.35% share. Yet, testing automation, which is expanding at a 16.10% CAGR, now drives purchasing criteria as enterprises prioritize shift-left quality assurance. The continuous integration tools market share for AI-generated test cases and intelligent selection is growing, as platforms such as Harness embed machine-learning models that reduce regression suites by 60% while preserving coverage .

The release, deployment, and feedback stages are no longer optional add-ons; buyers increasingly treat end-to-end orchestration as a table stake. Providers that incorporate progressive delivery, canary controls, and automated rollback can shorten the mean-time-to-repair and enhance the customer experience, further raising switching barriers within the continuous integration tools market.

By End-User Industry: Healthcare compliance drives unexpected growth

IT and telecommunications captured 26.12% revenue in 2025, thanks to its mature DevOps culture. Healthcare and life sciences, however, are expected to post the strongest growth rate of 14.28%, as FDA and PCI DSS rules drive the adoption of SBOM generation and traceability. Platforms that automate compliance evidence are winning pilots among medical-device makers, hospital networks, and biotech firms.

BFSI, retail, and manufacturing also accelerate adoption to meet digital transformation and Industry 4.0 use cases, but their growth pace is muted compared with healthcare. Vendors tailoring pre-configured policy packs for HIPAA, PCI DSS v4, and SOC 2 audits differentiate in this segment of the continuous integration tools market.

Geography Analysis

North America contributes 36.05% revenue, fueled by deep DevOps penetration, venture capital, and defense procurement that now requires SBOM reporting. U.S. enterprises prefer comprehensive suites that combine CI, CD, security scanning, and infrastructure provisioning, reinforcing platform consolidation in the continuous integration tools market. Canada and Mexico provide supplemental growth through near-shoring initiatives and cloud adoption among mid-sized manufacturers.

The Asia-Pacific region is projected to experience the fastest growth, with a 14.32% CAGR. Government incentives in India, South Korea, and Singapore subsidize cloud migration; however, data-localization laws prompt buyers to opt for hybrid deployments. China’s preference for private-cloud AI models aligns with on-premise runners managed from hosted control planes, opening an avenue for flexible vendors. CERT-In’s 2024 SBOM mandate likewise drives demand for compliance automation across India.

Europe maintains steady momentum underpinned by GDPR and the forthcoming EU Cyber Resilience Act, both of which elevate supply-chain security requirements. Buyers validate solutions that can guarantee data residency and produce automated audit trails, steering budget toward providers with regional hosting and encryption certificates. Germany, France, and the United Kingdom remain the largest contributors, while Scandinavian and Eastern European countries represent expanding greenfield demand in the continuous integration tools market.

Competitive Landscape

Top Companies in Continuous Integration Tools Market

The market exhibits moderate fragmentation. Jenkins still powers many pipelines, but its 47.13% stake is slowly eroding as enterprises seek managed offerings. Atlassian’s Bitbucket retains an 18.36% slice, leveraging integration with Jira and Confluence, while CircleCI holds 5.85% through a developer-friendly SaaS approach. Despite the incumbent's heft, venture capital continues to pour in; Harness has amassed USD 425 million and merged with Traceable in March 2025 to deliver AI-native DevSecOps at an enterprise scale.

Strategic patterns highlight convergence around full-stack platforms. GitLab bundles source control, security scanning, and deployment, positioning itself as a single interface from commit to production. Microsoft pushes GitHub Actions integrated with Azure while layering Copilot AI to lock in developers. IBM’s acquisition of HashiCorp extends OpenShift with infrastructure-as-code and policy enforcement, closing orchestration gaps[4]Mike Wheatley, “IBM Misses on Revenues but Foresees Growth from HashiCorp Purchase,” siliconangle.com. These moves intensify differentiation based on ecosystem breadth and AI-driven automation in the continuous integration tools market.

White-space opportunities center on intelligent cost optimization, multi-tenant isolation for heavily regulated workloads, and auto-generated attestation aligned with NIST-recommended zero-trust principles. Niche players innovate in these areas, but scale players possess go-to-market muscle to productize breakthroughs quickly. As a result, additional mergers are likely, and the market is expected to consolidate around 5-6 broad-based platforms that can serve both Fortune 100 and start-up customers in the continuous integration tools market.

Dynamic Market Structure with Strong Consolidation Trends

The continuous integration tools market exhibits a mix of global technology conglomerates and specialized DevOps solution providers competing for market share. Large players like IBM, Microsoft, and AWS leverage their extensive cloud infrastructure and enterprise relationships to offer integrated CI solutions as part of broader development platforms. Meanwhile, specialized players like GitLab, CircleCI, and CloudBees focus on delivering best-of-breed CI capabilities with deep integration possibilities. The market is witnessing increased consolidation through strategic acquisitions, as evidenced by CloudBees acquiring CodeShip, Harness acquiring Drone.io, and other similar moves aimed at expanding technical capabilities and market reach.

The competitive dynamics are characterized by a high intensity of rivalry, with companies competing on factors like ease of integration, automation capabilities, and pricing models. Market participants are increasingly focusing on industry-specific solutions and compliance requirements, particularly in regulated sectors. The emergence of open-source platforms and community-driven development has also influenced the competitive landscape, with companies adopting hybrid approaches that combine proprietary solutions with open-source compatibility. Partnership ecosystems play a crucial role in market success, with vendors forming alliances to enhance their service offerings and expand their customer base.

Innovation and Integration Drive Market Success

For incumbent players to maintain and expand their market share, several key strategies have emerged as critical success factors. These include continuous investment in R&D to enhance automation capabilities, improved security features, and seamless integration with popular software development tools and platforms. Companies need to focus on developing industry-specific solutions that address unique compliance and regulatory requirements across different sectors. Building strong partner ecosystems, offering flexible deployment options, and providing comprehensive support services are also essential for maintaining a competitive advantage. Additionally, incumbents must balance the need for standardization with customization capabilities to meet diverse customer requirements.

New entrants and contenders in the market can gain ground by focusing on specialized use cases or industry verticals where larger players may have gaps in their offerings. Innovation in areas like artificial intelligence, machine learning, and advanced analytics for CI/CD workflows presents opportunities for differentiation. The relatively moderate barriers to entry in terms of capital requirements allow new players to enter with innovative solutions, though they must overcome challenges related to brand recognition and enterprise trust. The risk of substitution is relatively low due to the essential nature of CI software in modern software development, but companies must stay ahead of technological changes and evolving development methodologies to remain relevant.

Continuous Integration Tools Industry Leaders

Atlassian Corporation PLC

Amazon Web Services, Inc.

Microsoft Corporation

Circle Internet Services, Inc.

GitLab, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The U.S. Army began enforcing SBOM requirements for new software contracts, elevating demand for compliance-ready pipelines.

- January 2025: Harness completed the Traceable merger to integrate API security and WAF features into its CI/CD suite.

- October 2024: CERT-In issued official SBOM guidelines that apply to critical information infrastructure projects.

- September 2024: Harness launched multi-agent AI automation to self-heal builds, tests, and deployments.

- August 2024: CISA released a software acquisition guide mandating CI/CD security checks for U.S. federal buyers.

Global Continuous Integration Tools Market Report Scope

Continuous Integration Tools (CI Tools) are an essential component of DevOps and are used to integrate various DevOps stages. It includes an automated testing process, which enables multiple developers to contribute to and collaborate on a shared codebase at a rapid pace. Continuous Integration (CI) tools further help the development team make changes to version control, where software developers share and merge their changes at the time of completion of every project task.

The Continuous Integration Tools Market is segmented by Deployment Mode (On-Premise, On-Cloud), End-User Industry (IT & Telecom, Retail & Ecommerce, Healthcare & Lifesciences, BFSI, Media & Entertainment, Others), and Geography (North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| On-premise |

| Cloud-native SaaS |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Build Automation |

| Testing Automation |

| Release and Deployment |

| Monitoring and Feedback |

| IT and Telecom |

| BFSI |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Education |

| Manufacturing |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Type | On-premise | ||

| Cloud-native SaaS | |||

| Hybrid | |||

| By End-user Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Application Stage | Build Automation | ||

| Testing Automation | |||

| Release and Deployment | |||

| Monitoring and Feedback | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Retail and E-commerce | |||

| Healthcare and Life Sciences | |||

| Media and Entertainment | |||

| Education | |||

| Manufacturing | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How big is the Continuous Integration Tools Market?

The Continuous Integration Tools Market size is expected to reach USD 2.09 billion in 2026 and grow at a CAGR of 20.72% to reach USD 5.36 billion by 2031.

How large will the continuous integration tools market be in 2031?

The continuous integration tools market size is projected to reach USD 5.36 billion by 2031.

Which deployment model is growing fastest?

Hybrid deployment is the fastest-growing model, advancing at a 15.52% CAGR as firms balance control with cloud scalability.

Why is testing automation gaining momentum?

AI-driven test generation and shift-left quality mandates are pushing testing automation to a 16.10% CAGR, making it the quickest-expanding application stage.

Which region will see the highest growth?

Asia-Pacific is poised for the highest regional growth, posting a 14.32% CAGR through 2031 due to government digital initiatives and increasing compliance requirements.

Page last updated on: