Contact Center Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

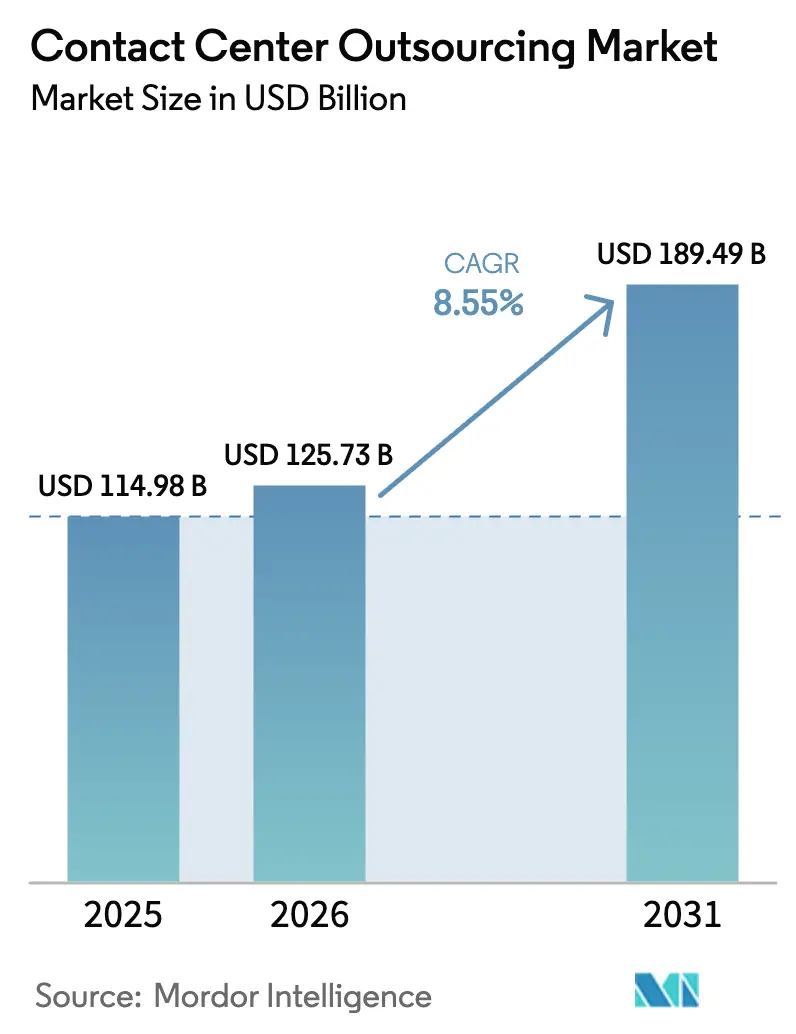

| Market Size (2026) | USD 125.73 Billion |

| Market Size (2031) | USD 189.49 Billion |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

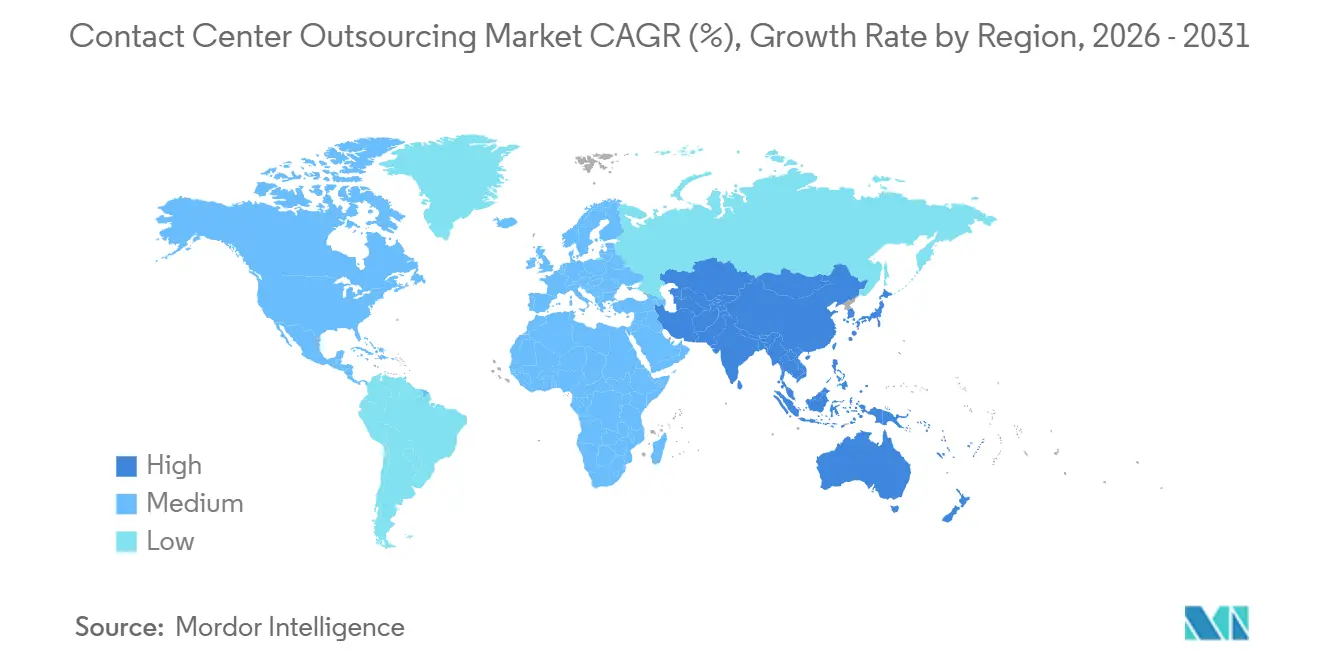

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contact Center Outsourcing Market Analysis by Mordor Intelligence

The Contact Center Outsourcing Market size is expected to grow from USD 114.98 billion in 2025 to USD 125.73 billion in 2026 and is forecast to reach USD 189.49 billion by 2031 at 8.55% CAGR over 2026-2031.

Shifting enterprise priorities now favour rapid deployment of cloud-native platforms, generative-AI copilots, and omnichannel orchestration over pure wage-arbitrage models. Vendor selection criteria increasingly center on AI maturity, data-residency compliance, and the ability to spin up multi-language operations on short notice. Buyers also view nearshore capacity in Mexico, Colombia, Poland, and Egypt as a hedge against geopolitical and currency risk, while flexible work-from-home frameworks help providers broaden talent pools and contain real-estate costs. Competitive differentiation rests on bundling proprietary AI layers with CCaaS stacks, offering outcome-based pricing, and demonstrating measurable improvements in customer-experience metrics. Heightened regulatory scrutiny around privacy, cyber resilience, and AI governance adds complexity but also creates opportunities for vendors that turn compliance into a value proposition.

Key Report Takeaways

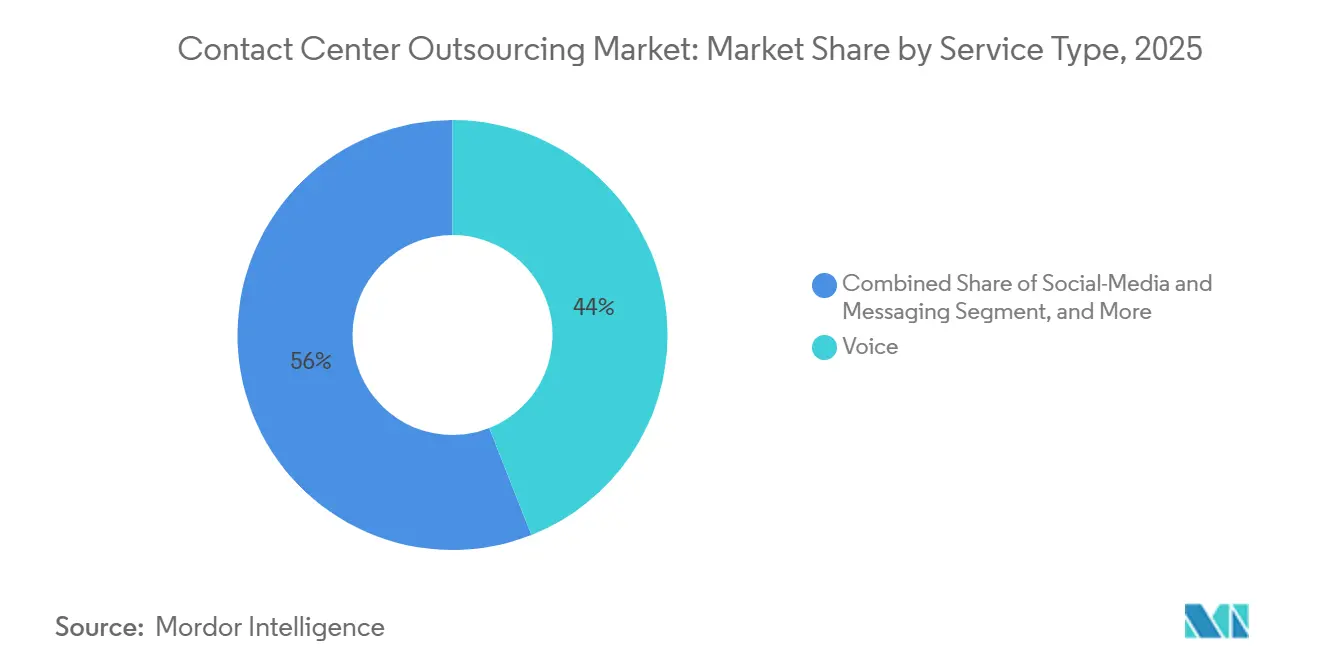

By service type, voice support led with 44.01% of the contact center outsourcing market share in 2025. Social-media and messaging workloads are forecast to expand at an 8.99% CAGR to 2031.

By end-user industry, BFSI commanded 21.34% revenue share of the contact center outsourcing market size in 2025. Healthcare and life sciences are advancing at an 8.71% CAGR through 2031.

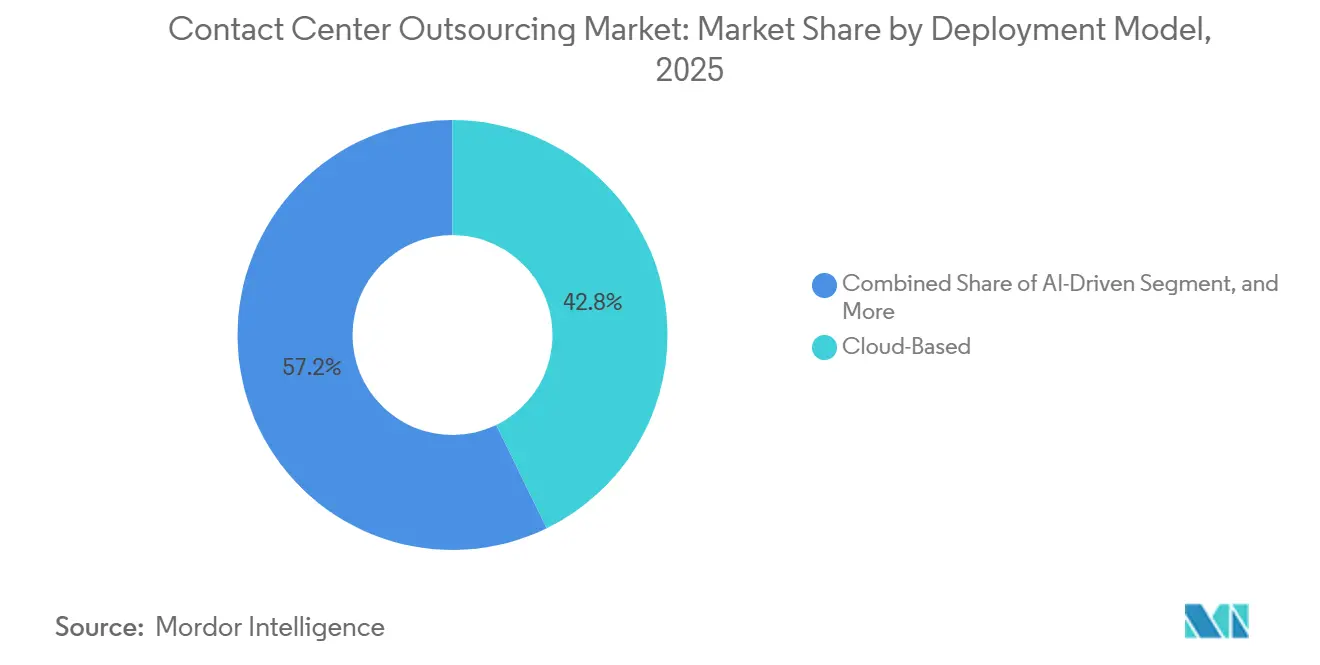

By delivery model, offshore centers retained 56.71% share in 2025, while virtual and remote centers are growing at a 9.04% CAGR to 2031. AI-driven architectures are projected to post the fastest 9.22% CAGR between 2026 and 2031.

By geography, North America held 37.42% in 2025, whereas Asia Pacific is poised for a 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Contact Center Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud Migration and CCaaS Adoption Surge | +1.80% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Digital-First Omni-Channel CX Mandates | +1.50% | Global, led by retail and e-commerce sectors in North America, Europe, and Asia Pacific | Short term (≤ 2 years) |

| Post-Pandemic Cost-to-Serve Pressure | +1.20% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Near-Shore Talent Scalability in N. LATAM and E. Europe | +1.00% | North America sourcing from Mexico and Colombia; Europe sourcing from Poland and Romania | Medium term (2-4 years) |

| Gen-AI Copilots Elevate Agent Productivity | +1.60% | Global, with fastest uptake in BFSI and IT/Telecom sectors | Medium term (2-4 years) |

| Sovereign-Cloud and Data-Residency Incentives | +0.90% | Europe (GDPR), Middle East, China, and regulated sectors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration and CCaaS Adoption Surge

Contact-center-as-a-service platforms provide elastic capacity, seamless CRM integrations, and out-of-the-box AI components, making them the default architecture for new outsourcing contracts. Multi-year on-premises refresh cycles are giving way to subscription models that cut implementation time from months to weeks. Shorter switching costs intensify competition, so providers respond by embedding proprietary analytics, vertical templates, and outcome-based pricing. As a result, the contact center outsourcing market increasingly rewards technology leadership over seat-count scale.[1]Cisco Systems, “Cisco Contact Center Portfolio,” cisco.com

Digital-First Omni-Channel CX Mandates

Consumers expect effortless transitions across chat, email, voice, and social channels, forcing enterprises to collapse siloed systems into unified customer timelines. Vendors offering pre-integrated omnichannel stacks alleviate the heavy lift of multi-year IT programs, securing stickier contracts in retail, e-commerce, and media. Success is judged on first-contact resolution and customer-effort scores, not channel breadth alone. Providers unable to prove quantifiable gains risk relegation to commodity overflow tasks.

Gen-AI Copilots Elevate Agent Productivity

Real-time transcription, sentiment detection, and next-best-action prompts allow junior agents to perform at expert levels, trimming average handle time and boosting upsell conversions. Early adopters report 30-45% efficiency gains, yet results hinge on proprietary training data, rigorous model governance, and continuous retraining. The productivity gap creates a moat for vendors investing in dedicated AI labs and co-development partnerships with hyperscalers.[2]TTEC Holdings, “Remote Contact Center Associate Solutions,” ttec.com

Near-Shore Talent Scalability in Latin America and Eastern Europe

U.S. buyers increasingly favour Mexico and Colombia for time-zone alignment, English proficiency, and rising bilingual talent pools, while Western European firms turn to Poland and Romania for EU-compliant delivery at lower cost. Governments court BPO investments with tax incentives and training grants, making near-shore locations strategic complements to Asian delivery hubs. Providers able to orchestrate multi-country footprints command premium retainers from risk-averse clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Data-Sovereignty Regulations | -0.70% | Europe (GDPR), China, Middle East, and regulated sectors globally | Long term (≥ 4 years) |

| Cyber-Security and Privacy Breach Risk | -0.60% | Global, with heightened scrutiny in BFSI and healthcare sectors | Short term (≤ 2 years) |

| Chronic Agent Attrition and Wage Inflation | -0.90% | Global, particularly acute in North America, Western Europe, and urban centers in Asia | Medium term (2-4 years) |

| Gen-AI Bias, Regulatory and Compliance Liabilities | -0.50% | North America, Europe, and regulated industries (BFSI, healthcare, government) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Agent Attrition and Wage Inflation

Global turnover rates that spiked to near-80% in the immediate post-pandemic period have moderated but remain well above the 30-45% norm, driving up rehiring and training costs. Experienced agents leverage scarcity to negotiate higher pay, squeezing the labour-arbitrage margin that underpinned the first wave of outsourcing. Providers counter with AI-led coaching, flexible scheduling, and career pathways, but these require upfront investment that erodes short-term profitability, especially for thin-margin voice portfolios.

Cyber-Security and Privacy Breach Risk

Contact centers handle payment credentials, health records, and personal data that attract sophisticated cyber threats. Remote-agent models widen the attack surface, while GDPR, HIPAA, and similar statutes expose vendors to penalties up to 4% of global revenue per breach. Zero-trust architectures, continuous monitoring, and mandatory ISO-27001 certification have become table stakes, raising capital intensity. A single breach can trigger clawbacks and brand damage that reverberate across multi-year deals, making cyber resilience a critical differentiator.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Messaging Channels Rise Beside Voice Leadership

Voice support retained 44.01% of the contact center outsourcing market share in 2025 as complex disputes and high-value sales still favour real-time dialogue. The contact center outsourcing market size linked to social-media and messaging channels, however, is projected to post the fastest 8.99% CAGR to 2031 as digital-native customers embrace asynchronous chat that AI bots can resolve without queuing. Vendors integrate chatbots for tier-1 issues and escalate nuanced cases to human agents, blending cost control with empathy.

Email remains a cost-effective workhorse for non-urgent issues, while emerging video and co-browse use cases flourish in wealth management and telehealth. Providers now package unified agent desktops so staff can pivot among voice, chat, and messaging without losing context, a capability that boosts first-contact resolution and earns premium rates. Those still running siloed service lines struggle to win omnichannel bids.

By End-User Industry: Healthcare Momentum Offsets BFSI Maturity

BFSI commanded 21.34% of 2025 revenue, reflecting its long outsourcing history, stringent compliance needs, and high transaction volumes. Growth decelerates as large banks have already externalized most simple interactions, shifting deals toward niche fraud management and wealth-advisory support. In contrast, healthcare and life sciences are forecast for an 8.71% CAGR through 2031 as telehealth, electronic prior authorization, and patient-engagement mandates generate new outsourcing waves.

Vendors invest in HIPAA-compliant infrastructure and nurse-practitioner talent pools to manage triage, scheduling, and benefits verification, unlocking higher margins than voice-only BFSI work. Retail, e-commerce, and technology remain sizeable but competitive, encouraging providers to differentiate through AI-assisted sales enablement and data-driven personalization.

By Delivery Model: Virtual Frameworks Challenge Offshore Dominance

Offshore sites in India, the Philippines, and Egypt still held 56.71% of 2025 volume. Yet secure virtual-agent ecosystems are expanding at a 9.04% CAGR, enabling providers to recruit from previously untapped labour pools, including veterans and caregivers.

Work-from-home arrangements cut facility overhead, improve schedule adherence, and widen diversity, but demand sophisticated endpoint security and performance analytics. Nearshore hubs in Mexico, Colombia, Poland, and Romania attract clients seeking cultural affinity and faster issue escalation, while onshore centers cater to regulated verticals. Vendors able to blend onshore, nearshore, offshore, and virtual nodes into a single contract win larger, multi-year deals.

By Deployment Model: AI-Driven Architectures Redefine Infrastructure

In 2025, cloud deployments accounted for 42.78% of the market, showcasing their adaptability and smooth integration with CRM and workforce management systems. The scalability and cost-efficiency of cloud solutions have made them a preferred choice for businesses aiming to streamline operations and enhance flexibility. Meanwhile, hybrid setups cater to clients hesitant to fully transition from their aging on-premises assets, albeit at the cost of added governance complexities. These hybrid models allow organizations to leverage the benefits of cloud technology while maintaining control over critical legacy systems, ensuring a balanced approach to modernization.

AI-driven centers, which incorporate features like real-time transcription and predictive routing, are projected to achieve a 9.22% CAGR through 2031, positioning them as the industry's fastest-growing deployment model. These centers are transforming customer service operations by enabling faster issue resolution and personalized customer interactions. Providers are strategically placing their proprietary AI layers as tools for revenue sharing, opting to charge clients based on the cost per resolved ticket. This approach, diverging from traditional seat-hour billing, has garnered favor among CFOs who prioritize alignment with tangible outcomes. The shift toward outcome-based pricing models reflects a broader trend in the industry, emphasizing efficiency and measurable results over conventional metrics.

By Interaction Flow: Omnichannel Complexity Fuels Outsourcing Appeal

Inbound calls, holding steady at 62.39%, face a plateau as self-service tools increasingly handle simpler queries. This shift reflects the growing adoption of automation and AI-driven solutions, which streamline customer interactions by addressing routine concerns without human intervention. Meanwhile, omnichannel interactions are poised to grow at a 9.61% CAGR, driven by consumers' desire for context continuity across chat, email, voice, and social platforms. Customers now expect seamless transitions between channels, with their interaction history readily accessible to ensure personalized and efficient service.

Competitive proposals now hinge on unified routing engines, knowledge graphs, and sentiment analytics. These technologies enable businesses to optimize customer journeys by providing real-time insights and predictive capabilities. Providers lacking the ability to offer a comprehensive view of cross-channel journeys risk relegation to overflow voice queues, grappling with diminishing margins. As the market evolves, the ability to deliver single-pane visibility and actionable insights across all touchpoints is becoming a critical differentiator for sustained growth and profitability.

Geography Analysis

North America generated 37.42% of 2025 revenue, anchored by mature BFSI, healthcare, and technology buyers that insist on multi-site redundancy, ISO certifications, and AI-supported quality assurance. Wage inflation and high turnover encourage nearshoring to Mexico and Colombia, both offering bilingual talent and overlapping time zones. Vendors that weave those nodes into existing Philippine and Indian networks mitigate currency and political risk while accelerating contract wins.

Europe presents a mixed landscape: GDPR drives in-country delivery in Germany and France, whereas nearshore hubs in Poland and Romania satisfy language and compliance needs for U.K. and Nordic buyers at lower cost. Regional cloud-sovereignty initiatives spur investments in local data centers, favouring providers with capital to build or lease secure infrastructure.

Asia Pacific posts the fastest 9.12% CAGR to 2031. India and the Philippines retain scale leadership, adding AI labs and vertical domain academies to defend share. Emerging ASEAN markets such as Vietnam, Thailand, and Malaysia are pulling pilot projects but grapple with infrastructure gaps. China’s vast domestic opportunity remains largely closed to foreign vendors, yet multinational clients seek Mandarin support from offshore Thailand and Malaysia operations, hedging geopolitical exposure.

Middle East and Africa grow off a smaller base. Egypt stands out with large-scale trilingual talent and pro-BPO incentives. Concentrix, Foundever, and Alorica have each commissioned multithousand-seat Cairo campuses, citing cost parity with major Indian metros and three-hour proximity to European capitals. South Africa services U.K. and Australian accounts, though power-grid instability limits round-the-clock reliability. Gulf Cooperation Council countries outsource selective citizen-services but often require onshore hosting within national borders.[3]David Gomez, “Colombia vs Mexico for Nearshore Technology Outsourcing,” Alcor, alcor-bpo.com

South America beyond Colombia sees Brazil commanding Portuguese programs for regional banks and e-commerce giants, while Chile and Guatemala court specialized Spanish contact flows. Macroeconomic volatility prompts clients to diversify among at least two Latin American sites, a trend favouring networked providers over single-country specialists.

Competitive Landscape

Market concentration is Low, with the top five firms holding about 38% of global billings. Teleperformance merged with Majorel to unlock technology and training synergies, while Concentrix’s acquisition of SAI Digital added consulting depth that elevates its seat-based model into transformation advisory. Foundever and Alorica pursue industry specialization and analytics-led upsell, whereas TTEC leans on its work-from-home platform for hyper-scalable retail peak management. Smaller disruptors such as TaskUs (gaming, fintech) and Firstsource (healthcare revenue-cycle) defend niches through domain certification and proprietary workflows.

Partnership ecosystems blur the line between software and services. Providers bundle CCaaS licenses from Five9, Genesys, and NICE with managed agents, positioning as end-to-end CX partners. Investments in proprietary AI studios, zero-trust security stacks, and cyber-insurance coverage become prerequisites for Fortune 500 RFP shortlists. Vendors lacking capital for these upgrades face relegation to subcontract roles.

Strategic bifurcation is apparent: global integrators chase breadth across geographies, languages, and verticals, while specialists double down on depth compliance mastery, unique data sets, and outcome-based SLA frameworks. Clients increasingly split portfolios, sending commoditized volumes to mega-vendors and reserving complex or regulated work for niche experts.

Contact Center Outsourcing Industry Leaders

Atento S.A

Sykes Enterprises, Incorporated

DATAMARK Inc.

Teleperformance, SA

Concentrix Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Teleperformance reported Q1 2025 revenue of EUR 2.613 billion (USD 2.87 billion), growing 2.8%, and committed EUR 100 million (USD 110 million) to AI partnerships through 2025.

- March 2025: Concentrix posted USD 2.37 billion Q1 2025 revenue and announced USD 240 million in dividends and buybacks while scaling its GenAI suite.

- February 2025: Firstsource Solutions logged INR 21.02 billion (USD 249 million) Q3 FY25 revenue, up 31.7%, securing healthcare and consumer-tech contracts.

- February 2025: Teleperformance finalized the acquisition of ZP, a specialist in deaf and hard-of-hearing services, augmenting its Specialized Services arm.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the contact center outsourcing market as the aggregated annual revenue earned by third-party providers that handle voice, email, chat, social, and self-service interactions on behalf of client enterprises, whether delivered from on-shore, near-shore, offshore, or fully virtual sites. All deployment models, on-premise, cloud native, and hybrid platforms, are included because buyers typically pay for a bundled service rather than the technology alone.

Scope exclusion: our figures do not count in-house captive contact centers or standalone CCaaS software licenses.

Segmentation Overview

- By Service Type

- Voice (On-Shore)

- Voice (Off-Shore)

- Email Support

- Chat / Live-Chat Support

- Social-Media and Messaging

- Video and Co-Browse Support

- Self-Service / Bots

- By End-User Industry

- BFSI

- Retail and E-Commerce

- Healthcare and Life Sciences

- IT and Telecom

- Government and Public Sector

- Travel and Hospitality

- Utilities and Energy

- Media and Entertainment

- By Delivery Model (Location)

- On-Shore Outsourcing

- Near-Shore Outsourcing

- Off-Shore Outsourcing

- Virtual / Remote Contact Centers

- By Deployment Model (Technology)

- Cloud-Based Contact Centers

- On-Premise Contact Centers

- Hybrid Contact Centers

- AI-Driven Contact Centers

- By Interaction Flow

- Inbound Services

- Outbound Services

- Omnichannel Communication

- Self-Service and Automation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Colombia

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Russia

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East

- Turkey

- UAE

- Saudi Arabia

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview delivery center directors, vendor selection consultants, and procurement heads across North America, Europe, Asia Pacific, and Latin America. The conversations validate utilization rates, cloud migration pace, Gen-AI adoption, and seat pricing spreads, helping us refine model assumptions and close data gaps identified in secondary material.

Desk Research

Mordor analysts first collate publicly available indicators such as US Bureau of Labor Statistics agent head-count trends, Reserve Bank of India services export data, EU Eurostat ICT spending, TeleGeography global telephony tariffs, and customer experience white papers released by trade groups such as the Global Sourcing Association. Company 10-Ks, investor decks, and major press releases provide contract values and capacity additions, while patent records from Questel reveal automation intensity.

These structured signals build a historical spine that anchors volume, average seat price, and delivery mix. Additional insights are pulled from D&B Hoovers for provider financials and Dow Jones Factiva for deal flow. The sources listed are illustrative; many other public and paid references inform our desk work.

Market-Sizing & Forecasting

A top-down reconstruction begins with service export receipts, captive-to-outsourced penetration, and regional seat density, which are then split by delivery location. Select bottom-up checks, sampled provider revenue roll-ups and average seat price multiplied by seat counts, temper the totals before finalization. Key variables informing the model include agent wage inflation, cloud contact center adoption, near-shore capacity build-outs, customer experience outsourcing penetration in BFSI and healthcare, and average handle-time efficiency gains. Forecasts employ multivariate regression blended with scenario analysis to reflect wage, FX, and technology uptake sensitivities.

Data Validation & Update Cycle

Outputs pass multi-step peer review, variance checks against independent benchmarks, and anomaly flags triggered by quarterly earnings or policy shifts. We refresh models every twelve months, issuing interim tweaks when material events occur so clients receive the most current view.

Why Mordor's Contact Center Outsourcing Baseline Earns Trust

Published estimates can diverge because firms pick different service scopes, convert currencies at varied points, or refresh their work on uneven cadences.

Key gap drivers often include whether cloud-only contracts are counted, how seat prices are normalized, and if near-shore captive revenues are lumped with third-party fees. Mordor's disciplined scope, annual refresh, and dual-track, top-down plus selective bottom-up, validation reduce such skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 117.5 B (2025) | Mordor Intelligence | - |

| USD 97.3 B (2024) | Global Consultancy A | excludes virtual agents and uses 2023 FX rates |

| USD 101.5 B (2024) | Trade Journal B | counts only voice and email services |

| USD 109.3 B (2024) | Industry Association C | relies on voluntary revenue disclosures without seat-price checks |

The comparison shows that when scope or currency choices shift, totals swing widely; Mordor's balanced blend of clear inclusions, verified seat economics, and timely updates provides a stable, decision-ready baseline.

Key Questions Answered in the Report

How large is the contact center outsourcing market today?

The contact center outsourcing market size reached USD 125.73 billion in 2026 and is projected to climb to USD 189.49 billion by 2031.

Which customer-support channel is growing the fastest?

Social-media and messaging workloads are forecast to expand at an 8.99% CAGR through 2031 as consumers favor asynchronous digital engagement.

Why are healthcare organizations increasing outsourcing?

Telehealth growth, patient-engagement mandates, and back-office complexity drive an 8.71% CAGR for healthcare and life-sciences outsourcing demand.

What delivery model is disrupting traditional offshore centers?

Secure virtual and remote contact centers are growing at a 9.04% CAGR, letting providers tap wider talent pools without investing in brick-and-mortar sites.

How are vendors differentiating beyond labor cost?

Providers bundle proprietary AI layers with CCaaS platforms, offer outcome-based pricing, and invest in zero-trust security to meet stringent compliance requirements.

Which regions show the highest growth potential?

Asia Pacific leads with a 9.12% CAGR to 2031, fueled by continued investments in AI-enabled capacity across India and the Philippines.

Page last updated on: