Consumer Discrete Semiconductors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

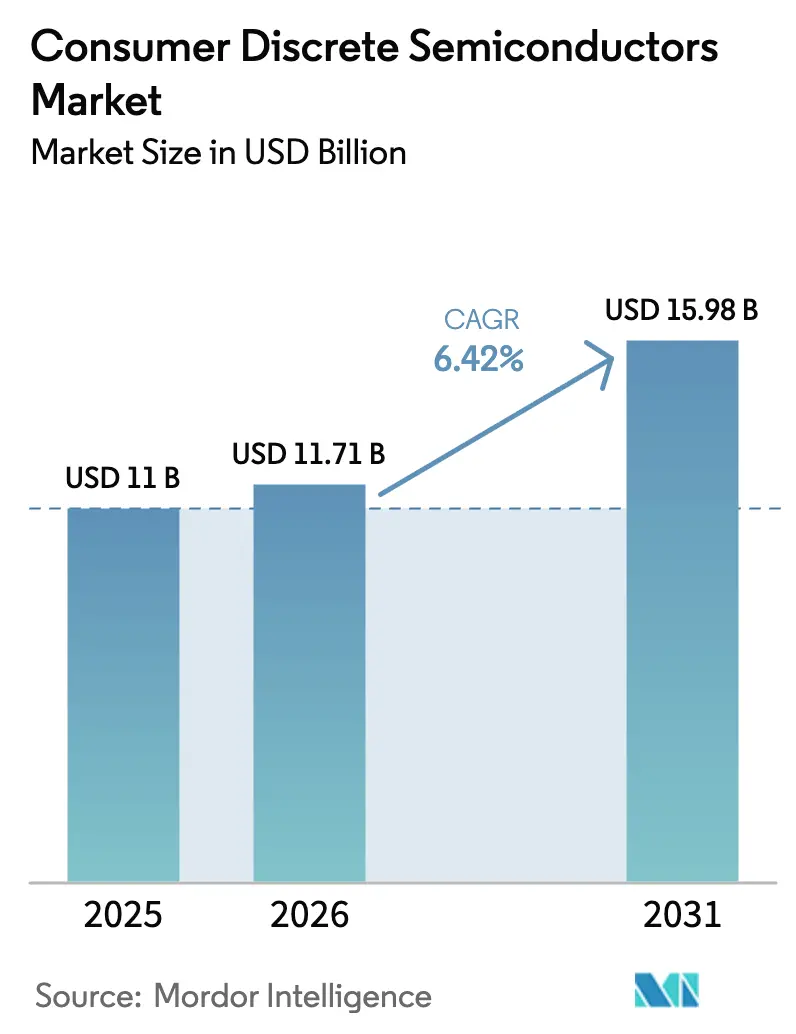

| Market Size (2026) | USD 11.71 Billion |

| Market Size (2031) | USD 15.98 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

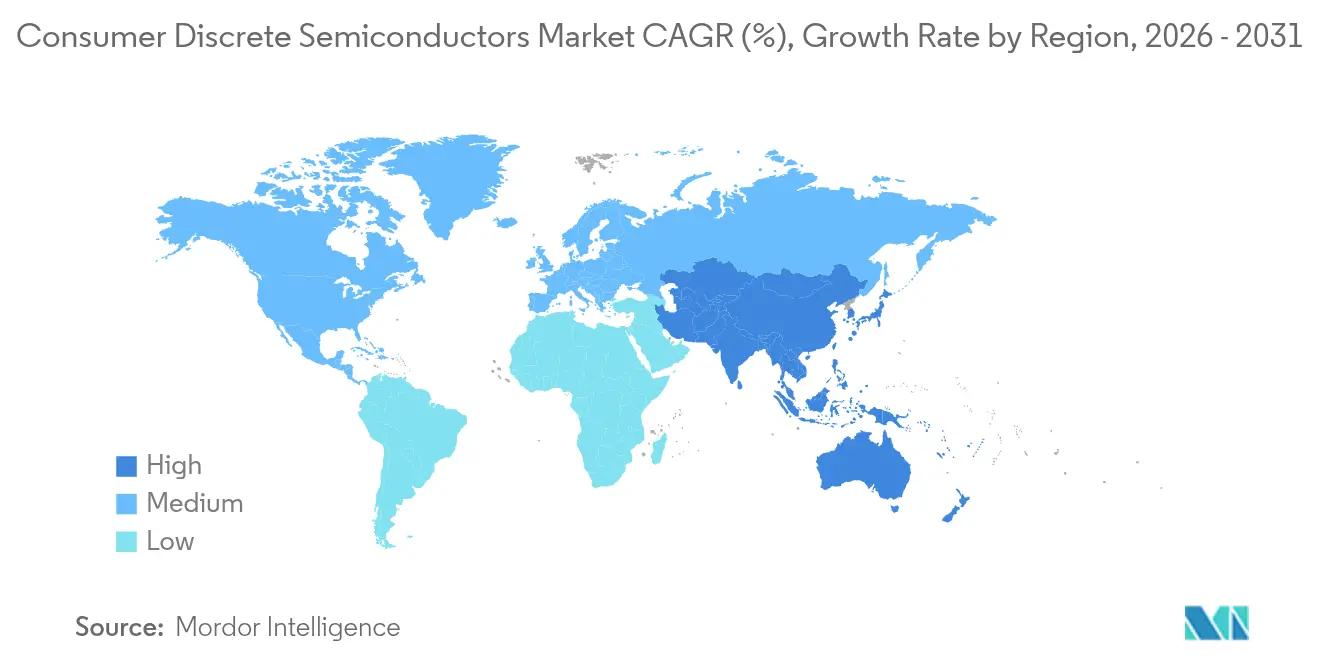

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

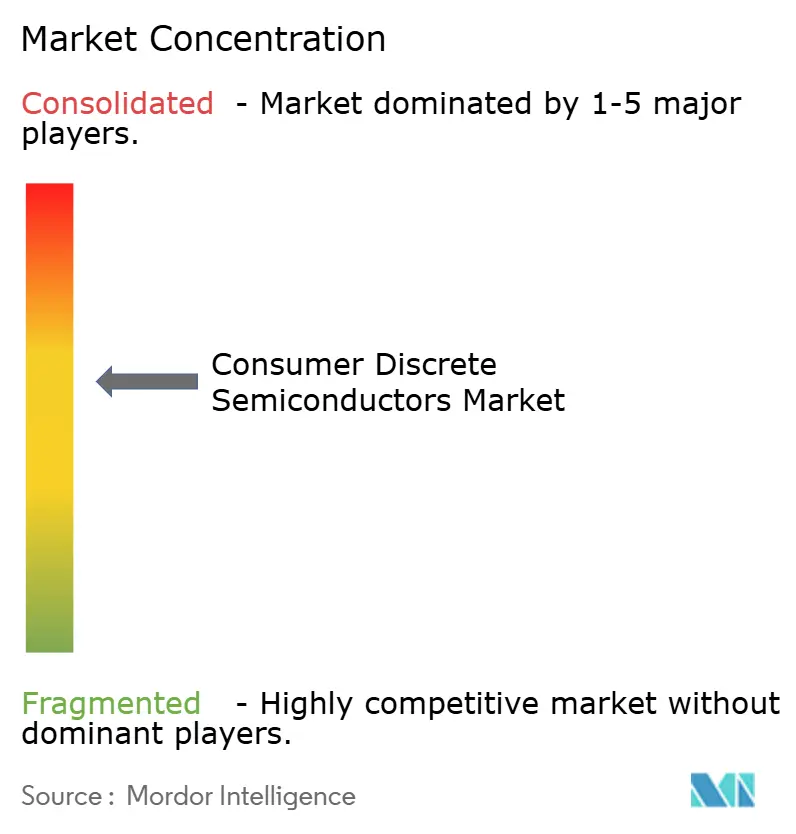

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Consumer Discrete Semiconductors Market Analysis by Mordor Intelligence

The consumer discrete semiconductor market size was valued at USD 11.00 billion in 2025 and estimated to grow from USD 11.71 billion in 2026 to reach USD 15.98 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031). Strong demand for energy-efficient power management, fast-charging adapters, and connected-home electronics is sustaining growth despite lingering supply-chain volatility. Wide bandgap (WBG) materials, notably Silicon Carbide (SiC) and Gallium Nitride (GaN), are expanding at a 19.2% CAGR and pushing discrete component efficiency to new levels.[1]Infineon Technologies, “Infineon at PCIM Europe 2025: Driving Decarbonization and Digitalization,” infineon.com Asia-Pacific retains leadership thanks to its integrated manufacturing ecosystem, while premium opportunities are emerging in North America and Europe as regulatory mandates tighten standby-power limits. Packaging innovation also matters, surface-mount devices dominate, yet wafer-level solutions are the fastest-growing format as OEMs pursue slimmer, lighter products. The convergence of these forces keeps the consumer discrete semiconductor market resilient and opportunity-rich for suppliers able to combine higher efficiency with aggressive cost control.

Key Report Takeaways

- By product type, power transistors led with 37.74% revenue share in 2025; GaN- and SiC-based devices in this category are set to post a robust 13.68% CAGR to 2031.

- By material, silicon held 88.05% of the consumer discrete semiconductor market share in 2025, while SiC is the fastest-growing material segment at a 18.24% CAGR.

- By packaging, surface-mount devices accounted for 73.92% of the consumer discrete semiconductor market size in 2025, whereas wafer-level/chip-scale packages are projected to expand at a 9.93% CAGR.

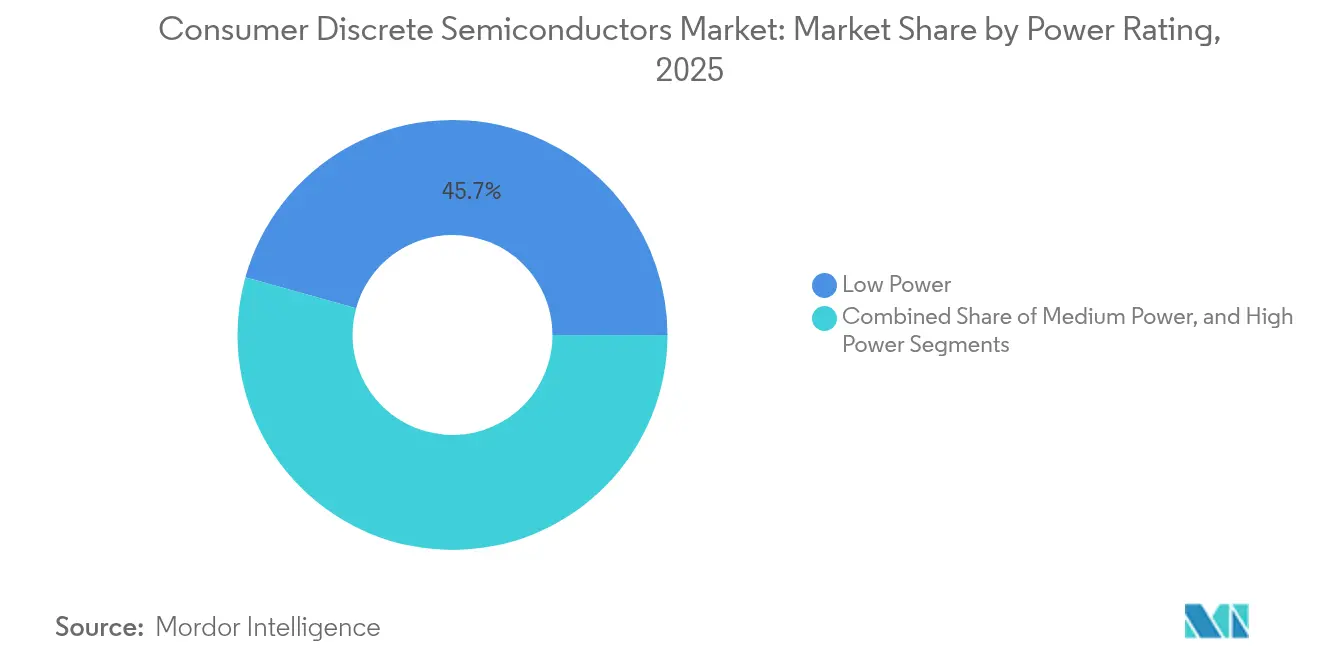

- By power rating, low-power (<1 A) discrete captured 45.68% of the consumer discrete semiconductor market size in 2025, yet the >20 A high-power class is posting the quickest 6.72% CAGR.

- By application, smartphones and tablets retained a 41.74% share in 2025; smart-home devices represent the fastest-growing application at a 8.74% CAGR through 2031.

- By geography, Asia-Pacific controlled 40.05% of global revenue in 2025 and is forecast to rise at 7.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consumer Discrete Semiconductors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of GaN and SiC Discrete in High-Watt Smart-Home Chargers | +1.7% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Smartphone OEM Demand for Ultra-Low-Leakage TVS Diodes in Foldables | +1.1% | Asia-Pacific, particularly China and Korea | Short term (≤ 2 years) |

| Growth of Wi-Fi 7 Routers Driving RF Switch Discrete Volumes | +0.8% | Global, with a concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Consumer Drone Electrification Requiring High-Current MOSFET Arrays | +0.6% | Global, with early adoption in North America and China | Medium term (2-4 years) |

| European Eco-Design Regulations Mandating Stand-by Efficiency <0.5 W | +1.0% | Europe, with spillover to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of GaN and SiC Discrete in High-Watt Smart-Home Chargers

High-watt wall adapters above 65 W shifted rapidly to GaN and SiC devices, trimming charger volume by 40% while lifting conversion efficiency up to 25% versus silicon solutions. Smart-home hubs and always-on speakers increasingly demand compact, cool-running power bricks, pulling WBG discrete into mainstream consumer price points. Infineon forecasts that cost reductions from 300 mm GaN wafers will widen adoption to mid-range appliances by 2027. Scale benefits are expected to spill over to <30 W USB-C segments, accelerating the consumer discrete semiconductor market transition toward WBG technology.

Smartphone OEM Demand for Ultra-Low-Leakage TVS Diodes in Foldables

Foldable handsets surged in popularity during 2024, and their flexible OLED displays require suppression diodes that leak below 100 nA while surviving 8 kV discharges. Vishay introduced bi-directional TransZorb® devices able to meet these specifications without raising standby drain. The discrete upgrade helps OEMs extend battery runtime and preserve screen lifespan, keeping the consumer discrete semiconductor market aligned with premium handset innovation cycles.

Growth of Wi-Fi 7 Routers Driving RF Switch Discrete Volumes

Wi-Fi 7 chipsets such as Qualcomm’s IPQ5322 require multi-link operation across 2.4 GHz, 5 GHz, and 6 GHz bands, elevating the need for low-loss, high-isolation RF switches.[2]Qualcomm / Lisle Apex, “Wi-Fi 7 Smart-Home Network Solution,” lisleapex.com Router vendors are therefore boosting discrete RF content per system, opening additional sockets for GaAs and SOI switch matrices. The ramp overlaps with the smart-home connectivity wave, reinforcing volume upside for specialized RF discrete across the consumer discrete semiconductor market.

European Eco-Design Regulations Mandating Standby Efficiency < 0.5 W

EU directives enacted in 2024 compel consumer devices shipped into the single market to limit standby draw below 0.5 W, prompting power-tree redesigns that favour low-quiescent MOSFETs and synchronous rectifiers. Leading OEMs now standardize global platforms on the stricter European limit to simplify logistics, enlarging global demand for ultra-efficient discrete. The regulation will underpin a structural lift in efficiency-oriented bill-of-materials across the consumer discrete semiconductor market through the end of the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Exposure to 6-inch Fab Capacity for Legacy Diodes | -1.1% | Global, with a severe impact in Asia-Pacific | Short term (≤ 2 years) |

| Thermal-Management Limits in Ultra-Thin Smartphones: Constraining Power Density | -0.8% | Global, with a concentration in Asia-Pacific | Medium term (2-4 years) |

| High SiC Wafer Pricing Slowing Adoption Below 65 W Devices | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Exposure to 6-Inch Fab Capacity for Legacy Diodes

Standard-recovery diode lines still rely heavily on 6-inch wafers concentrated in a handful of foundries. Recent geopolitical frictions and capacity reallocations created allocation risk for consumer OEMs, trimming discrete availability and muting near-term unit growth. Suppliers are qualifying 8-inch drop-in replacements, yet tooling and test-time investments prolong conversion schedules and temper overall consumer discrete semiconductor market expansion.

Thermal-Management Limits in Ultra-Thin Smartphones: Constraining Power Density

Smartphone chassis dipping below 7 mm restricts heat-spreading volume, limiting how much power discrete components can safely handle. Nagoya University’s 0.3 mm loop heat pipe prototype dissipates 10 W while offering 45 times copper thermal conductivity, but integration at scale remains two to three years away. Until advanced cooling methods mature, OEMs must throttle power budgets, keeping a lid on the high-power slice of the consumer discrete semiconductor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Power Transistors Lead Innovation Drive

Power transistors accounted for 37.74% of the consumer discrete semiconductor market in 2025 and are tracking a 13.68% CAGR through 2031. This scale places the segment at the centre of efficiency mandates and fast-charging trends. The emergence of trench-structured MOSFETs and copper-clip surface-mount packages is cutting R_DS(on) and thermal resistance, lifting current density without enlarging footprint. SiC and GaN variants continue to penetrate fast chargers and gaming consoles, replacing silicon in >500 kHz switchers where loss budgets are tight. Lower conduction losses unlock slimmer thermal stacks that align with ultra-thin product roadmaps. Application-specific transistors integrating synchronous rectifier logic are also rising, flattening PCB area and helping smartphone OEMs hit standby targets.

Diodes, rectifiers, and thyristors still underpin protection, rectification, and phase-control tasks, yet face incremental displacement when integrated power modules improve cost-per-function. Small-signal transistors retain roles in sensor interfaces and audio drivers; however, more of these tasks now migrate into SoCs, trimming the discrete count. That shift raises the stakes for discrete suppliers to deliver demonstrable system-level savings or risk socket erosion. Consequently, investment priorities concentrate on WBG process migration, lower-loss packages, and licensing deals that can broaden addressable sockets across the consumer discrete semiconductor market.

By Material: Silicon Foundation Challenged by WBG Revolution

Silicon supplied 88.05% of 2025 revenue share, reflecting decades of capital amortization and robust cost competitiveness. Yet SiC output will expand fast, underpinned by 8-inch wafer migration that promises 20% die-cost relief by 2026. SiC’s 10-fold higher breakdown field strength enables compact 650 V transistors capable of supplanting bulky silicon super-junction devices in television power supplies. GaN is rising in 30-150 W USB-C PD chargers, where its low output capacitance supports MHz-class resonant topologies.

Gallium Arsenide remains the incumbent for RF switches, but suppliers now co-opt SOI and GaN-on-Si alternatives to squeeze cost. Meanwhile, experimental materials such as diamond-like carbon timeline for post-2030 remain research concepts rather than near-term market factors. Over the forecast horizon, the ballast of silicon volume will keep blended ASPs affordable, but value capture will concentrate in WBG nodes, reinforcing a two-tier structure within the consumer discrete semiconductor market.

By Packaging: Surface-Mount Dominance with Wafer-Level Acceleration

Surface-mount formats delivered 73.92% of 2025 revenue, reflecting unrivalled assembly throughput and maturing thermally enhanced lead frames. Copper-clip packages lowered loop inductance, permitting GaN transistors to switch at >2 MHz with minimal overshoot. Plastic-encapsulated SMD devices now serve up to 200 A bursts, eclipsing through-hole TO-220 options for many consumer applications.

Wafer-level and chip-scale packages are scaling at a 9.93% CAGR as smartphones and hearables chase millimetre-class footprints. Infineon’s 1.8 × 1.6 × 0.4 mm eSIM illustrates how package-free die stacking slashes board area by 75%, cuts leakage, and boosts ESD immunity. Thermal constraints once capped wafer-level adoption, yet under-fill materials with higher thermal conductivity now permit sustained 3 W-5 W dissipation. The convergence of these advances’ positions wafer-level packaging to seize incremental share inside the consumer discrete semiconductor market.

By Power Rating: Low-Power Leadership with High-Power Growth

Low-power (<1 A) parts anchored 45.68% of the consumer discrete semiconductor market size in 2025, spanning TVS arrays, level-shifting FETs, and rectifiers inside wearables. Leakage suppression is the competitive differentiator, with below-50 nA offerings earning design wins in IoT sensors. Medium-power (1-20 A) discrete address notebook adapters and smart speakers, where surge capability and EMI compliance dominate specifications. Design trends blending synchronous rectification with intelligent sleep modes continue to blur the historical boundary between low and medium buckets.

High-power discrete above 20 A, while accounting for a smaller unit share, will post the swiftest 6.72% CAGR. Demand originates from 240 W USB-C PD chargers, AR/VR headgear base stations, and mini-gaming desktops. Thermal dissipation remains the gating factor: adaptive loop heat pipes embedded in system frames provide thermal conductivities exceeding 11,300 W/m·K, thereby legitimizing high-current GaN modules in compact shells. These cooling gains extend the application reach for high-power discrete and raise the value density inside the consumer discrete semiconductor market.

By Application: Smartphones Dominate While Smart-Home Accelerates

Smartphones and tablets contributed 41.74% of revenue in 2025, thanks to large build volumes and multichip power architectures. Battery charging, audio amplification, and display protection together consumed hundreds of billions of discrete. Foldable phones raised specification bars for leakage, ESD, and bending fatigue, prompting OEMs to source premium TVS devices. PCs, consoles, and set-top boxes still represent sizeable sockets for bridge rectifiers and MOSFET half-bridges, though refresh cycles are lengthening.

Smart-home appliances, ranging from voice assistants to robotic vacuums, register the sharpest 8.74% CAGR through 2031 as artificial intelligence adds standby power draws and voice-wake functionality. The segment leans heavily on GaN-based flyback converters and current-mode LED drivers to achieve sub-0.5 W standby budgets. Wearables and hearables show double-digit unit growth but have stringent height restrictions, motivating wafer-level zener arrays and 0.35 mm-thick voltage regulators. Consumer drones and personal mobility gadgets form a nascent yet vibrant segment for high-current MOSFET arrays, further widening the addressable field for suppliers in the consumer discrete semiconductor market.

Geography Analysis

Asia-Pacific dominated the consumer discrete semiconductor market with a 40.05% share in 2025 and is slated to deliver an 7.74% CAGR to 2031. Mainland China accelerated capital deployment into mature-node fabs, supported by national incentives exceeding USD 1.5 billion that target SiC substrate and epi production. Korea leverages its smartphone dominance to pilot advanced packaging nodes, while Japan retains niche strength in automotive-grade discrete. Local governments sponsor power-device clusters, ensuring ecosystem density and shortening qualification loops for consumer OEMs.

North America remains critical for architecture definition and WBG process innovation. The CHIPS Act earmarked USD 39 billion in grants and a further USD 11 billion for R&D, parts of which underwrite GaN pilot lines and SiC boule scaling. U.S. energy-security policies favour domestic WBG capacity, benefitting companies able to co-locate R&D with high-mix assembly. Canada’s MEMS and packaging expertise complements this value chain, especially in RF modules and ultra-low-leakage diodes.

Europe commands a share through automotive-oriented, discrete, and rigorous eco-design regulation. Infineon and STMicroelectronics anchor continental production, while the ESMC joint venture in Dresden will add 40,000 wafers per month of advanced capacity once ramped. Compliance with standby limits <0.5 W drives brisk demand for synchronous rectifiers and ultra-low-quiescent LDOs. Elsewhere, South America, the Middle East, and Africa are still emerging but log double-digit import growth of LED drivers and smartphone chargers, foreshadowing incremental opportunities for the consumer discrete semiconductor market over the next decade.

Competitive Landscape

The consumer discrete semiconductor market exhibits moderate concentration. ON Semiconductor, Infineon Technologies, and STMicroelectronics together controlled roughly 28% of 2024 revenue, leveraging vertically integrated wafer lines, differentiated packaging, and broad sales channels. ON Semiconductor’s January 2025 acquisition of Qorvo’s SiC JFET portfolio exemplifies the outsize value of intellectual-property pools that accelerate time-to-market for WBG discrete. Infineon’s 300 mm GaN wafer initiative promises die-cost advantages and underlines how scale can further entrench incumbency.

Challenger firms such as Navitas Semiconductor and Cambridge GaN Devices emphasize monolithic integration of gate drivers and FETs, simplifying reference designs for chargers and VR boosters. These newcomers often outsource to foundry partners like TSMC to sidestep heavy capital outlays. Nexperia’s broader GaN e-mode rollout in 2025 highlights how mid-tier players pivot toward WBG to stay relevant.

Supply-chain resilience shapes strategies as much as device physics. Leading vendors dual-source assembles across Southeast Asia and Eastern Europe to buffer geopolitical shocks. Simultaneously, partnership programs with cloud providers test discrete reliability in edge-AI workloads, elevating design-in prospects. As cost envelopes tighten, differentiation will continue to hinge on energy efficiency, thermal performance, and turnkey reference designs tailored to fast-moving consumer lifecycles within the consumer discrete semiconductor market.

Consumer Discrete Semiconductors Industry Leaders

-

ON Semiconductor Corporation

-

Infineon Technologies AG

-

STMicroelectronics N.V.

-

Nexperia B.V.

-

Vishay Intertechnology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon displayed CoolSiC® JFET power modules and CoolGaN™ solutions at PCIM Europe 2025 to advance high-efficiency consumer power supplies.

- April 2025: Nagoya University engineered a 0.3 mm loop heat pipe capable of 10 W dissipation, addressing thermal limits in ultra-slim smartphones.

- February 2025: NXP acquired Kinara for USD 307 million, adding energy-efficient neural processing to its edge portfolio.

- January 2025: ON Semiconductor purchased SiC JFET technology from Qorvo for USD 118.8 million to bolster its WBG roadmap.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the consumer discrete semiconductors market as all newly manufactured diodes, small-signal transistors, power transistors (MOSFETs, IGBTs and equivalents), rectifiers, and thyristors that ship inside finished consumer devices such as smartphones, wearables, laptops, set-top boxes, gaming consoles, and smart-home hardware. According to Mordor Intelligence, products sold to automotive, industrial, or telecom equipment makers, even if later embedded in consumer end-goods, sit outside this study.

Scope exclusion: modules that combine discretes with integrated circuits in a single package (e.g. SiP power stages) are not counted.

Segmentation Overview

-

By Product Type

- Diode

- Small-Signal Transistor

-

Power Transistor

- MOSFET Power Transistor

- IGBT Power Transistor

- Other Power Transistors

- Rectifier

- Thyristor

- Other Types

-

By Material

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Other Materials

-

By Packaging

- Through-Hole

- Surface-Mount (SMD/SMT)

- Wafer-Level / Chip-Scale Packages

-

By Power Rating

- Low Power (<1 A)

- Medium Power (1 – 20 A)

- High Power (>20 A)

-

By Application

- Smartphones and Tablets

- Wearables and Hearables

- PCs and Laptops

- Gaming Consoles and Set-Top Boxes

- Smart-Home Devices (TV, Smart Speakers, Appliances)

- Consumer IoT Sensors and Drones

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- France

- United Kingdom

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We then interviewed packaging engineers at Asian OSATs, sourcing managers at leading consumer electronics brands in North America and Europe, and sales directors at discrete device suppliers. Their insights fine-tuned our assumptions on charger attach rates, seasonal demand swings, and WBG material pricing, helping us close gaps that literature alone could not bridge.

Desk Research

Our analysts first compiled multi-year unit and value data from public sources such as JEITA handset statistics, WSTS device category shipments, UN Comtrade tariff codes for HS85.41/42, and trade association releases on GaN and SiC adoption. Complementary inputs came from company 10-Ks, investor decks, and press releases that reveal average selling prices and product mix shifts. Access to paid databases, including D&B Hoovers for OEM financials and Questel for power device patent counts, enabled richer competitive context.

These references illustrate, not exhaust, the wider desktop evidence pool consulted.

Market-Sizing & Forecasting

A top-down build began with 2024 global shipments of smartphones, PCs, smart-home hubs, and wearables, which are then multiplied by device-level discrete content and blended ASPs to reach the 2025 baseline. Bottom-up checks, supplier revenue roll-ups, and channel stock audits validated totals and adjusted for double counting. Key variables include smartphone unit outlook, GaN charger penetration, SiC die cost curves, average power stage count per smart speaker, and SMD share of total packaging. For forecasts, we ran a multivariate regression and ARIMA blend, with independent variables vetted by primary respondents, before scenario analysis tested upside and downside shocks.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst, senior peer, and research manager, where variances versus external indices trigger re-work. We refresh every twelve months and issue interim revisions when material supply chain or policy events occur, ensuring clients see the latest viewpoint.

Why Mordor's Consumer Discrete Semiconductors Baseline Stands Firm

Published figures often diverge because firms differ in scope choices, ASP inflation methods, and refresh cadence. Our study anchors only stand-alone discretes shipped into finished consumer gear, and it uses a disciplined mix of public trade data and live OEM feedback, which competitors may bypass.

Key gap drivers include some services bundling industrial and automotive demand into 'consumer' totals, others inflating value by pricing mixed-signal modules as pure discretes, or projecting volume from dated three-year-old handset baselines that our annual refresh has already corrected.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.00 Bn (2025) | Mordor Intelligence | - |

| USD 57.97 Bn (2025) | Global Consultancy A | Combines discrete, analog, and sensor dies; includes industrial IoT units |

| USD 48.06 Bn (2025) | Industry Whitepaper B | Applies overall discrete market value, then tags consumer share qualitatively |

| USD 10.27 Bn (2025) | Online Intelligence C | Uses supplier shipment quotes without channel inventory adjustment |

Taken together, the comparison shows that our transparent device-level scoping, double-sourced variables, and yearly update rhythm give decision-makers a balanced, reproducible baseline they can rely on for planning and benchmarking.

Key Questions Answered in the Report

What is the current size of the consumer discrete semiconductor market?

The consumer discrete semiconductor market was valued at USD 11.71 billion in 2026 and is expected to reach USD 15.98 billion by 2031.

Which product category holds the largest share?

Power transistors led the market with 37.74% revenue share in 2025, driven by strong demand for efficient power conversion.

How fast are wide-bandgap materials growing?

SiC and GaN discrete are expanding at a 18.24% CAGR through 2031 as chargers, AI devices, and smart-home systems seek higher efficiency.

Why is Europe important despite having a smaller share?

Strict eco-design rules limiting standby power to <0.5 W are forcing global OEMs to adopt ultra-efficient discrete, boosting European influence on technical roadmaps.

What packaging trend should suppliers watch?

Wafer-level and chip-scale packages are the fastest-growing formats at a 9.93% CAGR, enabling thinner phones and compact wearables.

Page last updated on: