Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

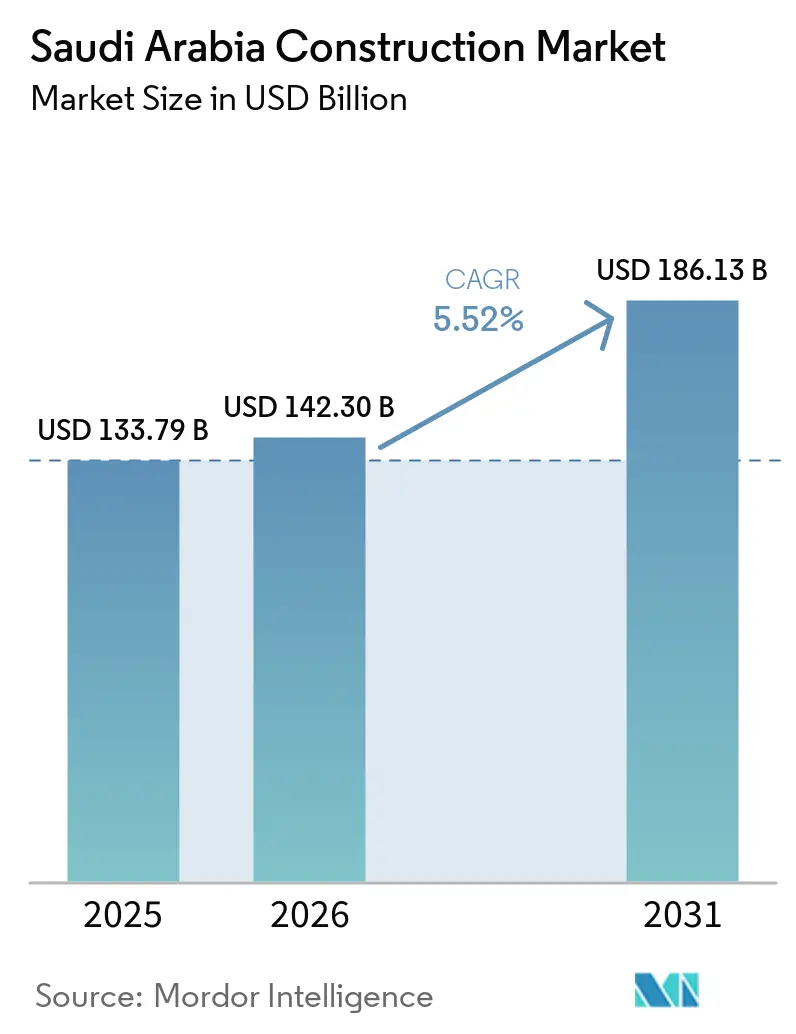

| Base Year Market Size (2025) | USD 133.79 Billion |

| Market Size (2026) | USD 142.30 Billion |

| Market Size (2031) | USD 186.13 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Construction Market Analysis by Mordor Intelligence

The Saudi Arabia Construction Market size is projected to be USD 133.79 billion in 2025, USD 142.30 billion in 2026, and reach USD 186.13 billion by 2031, growing at a CAGR of 5.52% from 2026 to 2031.

Transport corridors, giga-projects under Vision 2030, and aggressive grid upgrades continue to anchor long-run demand. Residential activity is accelerating as Sakani’s two-million-unit mandate pushes private developers into prefab and modular solutions that shorten build times. Logistics and data-center projects are benefiting from new railway freight lines and airport expansions that position the Kingdom as a regional trade gateway. Renewable assets and a USD 126 billion grid program are generating steady utility work, while cost-inflation risk is being partly offset by escalation clauses that protect contractor margins. Competitive rivalry is intensifying as local champions form joint ventures with global majors to secure technology and balance-sheet strength for multi-billion-dollar awards.

Key Report Takeaways

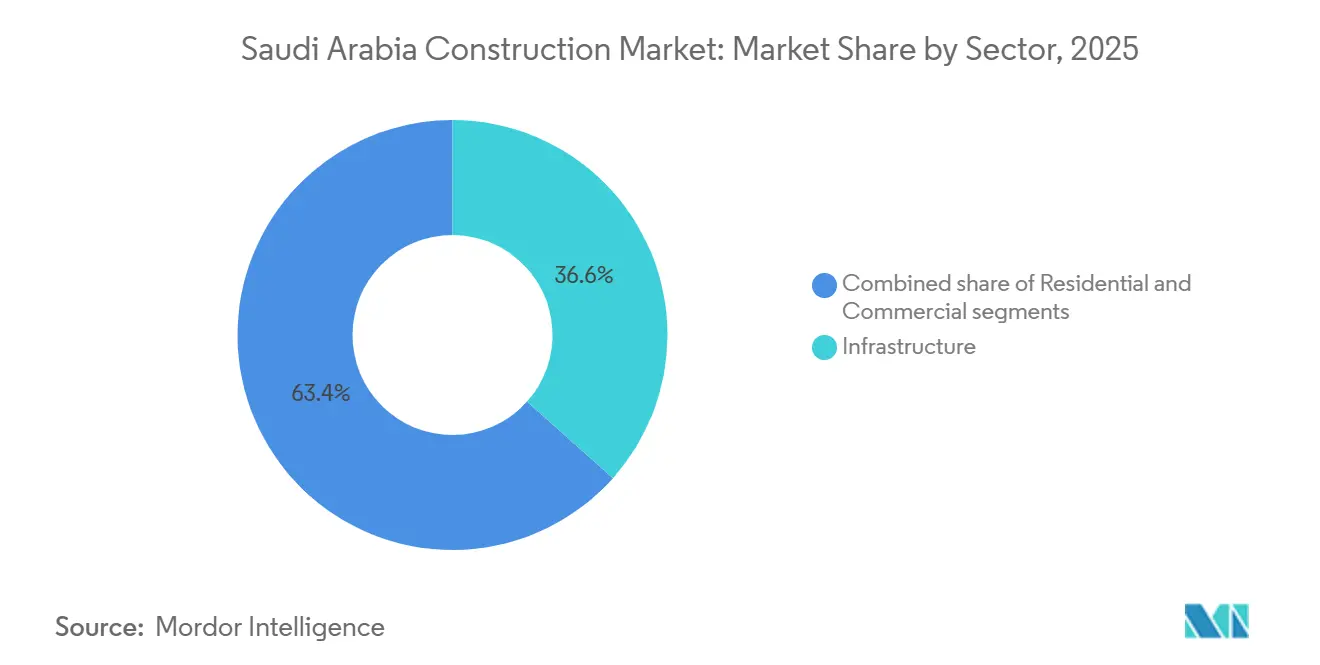

- By sector, infrastructure led with 36.6% of 2025 revenue, while residential is projected to post the fastest CAGR of 6.55% through 2031.

- By construction type, new construction dominated with an 81.2% share in 2025, whereas renovation is forecast to advance at a 6.91% CAGR over 2026-2031.

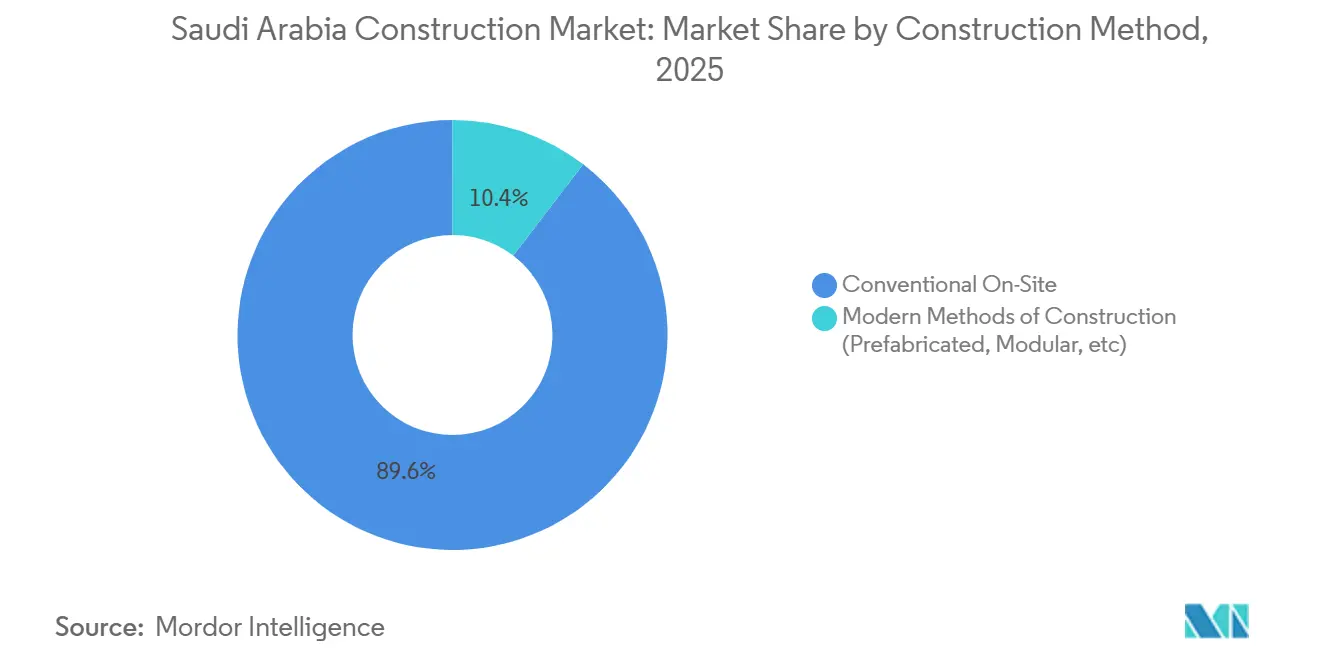

- By construction method, conventional on-site work accounted for 89.6% of the 2025 value, while modern methods of construction are expanding at a 7.55% CAGR.

- By investment source, public spending accounted for 71.5% of 2025 activity, and private capital is expected to grow at a 7.10% CAGR during 2026-2031.

- By city, Riyadh accounted for 36.1% of the 2025 construction value, and the Rest of Saudi Arabia cluster is anticipated to grow at a 7.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga- and mega-projects anchoring multi-year construction pipelines | +1.8% | National, with primary hubs in NEOM, Red Sea, Diriyah, and Qiddiya | Long term (≥ 4 years) |

| Housing programs and community infrastructure supporting rapid urbanization | +1.5% | Major metropolitan areas and emerging secondary cities | Short term (≤ 2 years) |

| Energy transition investments in renewables, grid modernization, hydrogen, and carbon capture | +1.3% | Northern and eastern renewable clusters, including NEOM | Long term (≥ 4 years) |

| Transport and logistics expansion across rail, metro, ports, and airports | +1.2% | Riyadh, Jeddah, Dammam, and the national logistics corridors | Medium term (2–4 years) |

| Water security investments in desalination, transmission, and wastewater reuse | +0.9% | Coastal desalination hubs and inland transmission networks | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga- and Mega-Projects Anchoring Multi-Year Pipelines

Landmark schemes such as NEOM, Red Sea, Diriyah, and Qiddiya are locking in multi-billion-dollar work scopes that span housing, utilities, and leisure assets. NEOM’s green-hydrogen plant reached 80% completion in 2025 and requires four gigawatts of dedicated renewables, creating follow-on packages for substations and transmission. Red Sea Global awarded USD 3.9 billion in early 2026 for 16 island resorts that use modular hotel blocks to safeguard reef ecosystems. Heritage-sensitive infrastructure at Diriyah Gate attracted USD 2.7 billion in 2025 bids that must conform to UNESCO protocols. Qiddiya is developing a 320,000-square-meter indoor venue alongside a Six Flags park, reinforcing long-term construction visibility. Collectively, these pipelines underpin stable order books yet add permitting complexity that can extend start dates by up to 18 months.

Housing Programs and Community Infrastructure Supporting Urban Populations

Sakani drove 1.05 million units by Q3 2024 and targets two million homes by 2030, elevating homeownership to 70%[1]National Housing Program, “Sakani Milestones,” housing.gov.sa. ROSHN let USD 1.2 billion in villa contracts in 2025 across three cities, using prefabricated wall panels that trim cycle time by 30%. National Housing Company issued USD 800 million in 2026 to fund 4,500 solar-ready apartments, reinforcing demand for MEP specialists. Subsidized mortgages lifted penetration to 28% of 2025 deals, unlocking latent demand among first-time buyers. Title-transfer delays in coastal municipalities still run 6-9 months, nudging developers to stagger launches so that supply aligns with credit approvals.

Energy Transition Capex Driving Civil and Utility Works

Saudi Electricity Company committed USD 126 billion through 2030 for 380-kilovolt substations and 12,000 kilometers of high-voltage lines that integrate northern and eastern renewable clusters[2]Saudi Electricity Company, “Grid Expansion Plan 2030,” se.com.sa. ACWA Power’s Round 7 awards in 2025 added 5.3 gigawatts of solar and wind, with commercial operations slated for 2028. Aramco’s USD 1.7 billion Jubail carbon-capture hub broke ground in 2025 and will inject nine million tons of CO₂ annually by 2027. Qurayyah’s 3-gigawatt expansion completed major civil works in 2025, signaling further opportunities for turbine foundations and cooling infrastructure. Specialized labor for high-pressure pipe welding and hydrogen compression remains scarce, prompting mega-projects to impose on-site training quotas.

Transport and Logistics Expansion Positioning the Kingdom as a Trade Hub

Railway freight corridors and metro extensions are reshaping domestic mobility and export competitiveness. Riyadh Metro’s 35-kilometer northern leg, awarded in 2025, will link the capital airport to industrial zones and carry 3.6 million daily riders by 2030. King Salman International Airport targets 120 million passengers on its first phase, a program involving 8 million m³ of earthworks and 1.2 million m² of terminal area. A USD 2.1 billion rail tender connects Jeddah and Dammam ports, aiming to divert 30% of containers from trucks by 2032. Jeddah Islamic Port’s USD 1.6 billion quay upgrade will add four million TEU of annual capacity, attracting build-to-suit warehouses for petrochemical exporters. These corridors stimulate private logistics real estate demand and sustain civil works backlogs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delivery capacity constraints and skilled labor shortages | -1.1% | Riyadh, NEOM, and Red Sea development zones | Short term (≤ 2 years) |

| Cost inflation and higher financing costs | -0.8% | Nationwide, with stronger impact on private sector projects | Medium term (2–4 years) |

| Regulatory, land acquisition, and environmental permitting complexity | -0.6% | Coastal zones and heritage-sensitive development areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Delivery Capacity Constraints and Skilled Labor Shortages

The active workforce reached 2.8 million in 2024, yet overlapping mega-projects have exposed gaps in welding, BIM coordination, and high-voltage assembly. Saudization rules raise the local labor quota to 30% by 2027, forcing contractors to invest in training academies that certify 500 workers annually in critical skills[3]Technical and Vocational Training Corporation, “Annual Graduate Report 2024,” tvtc.gov.sa. Visa transfer limits hinder the redeployment of expatriate teams between sites, aggravating spot shortages. Rental rates for 400-ton cranes in Riyadh jumped 25% in 2025 and lead times stretched to eight months, inflating preliminaries. Developers respond by packaging work in smaller lots and staggering tender releases to ease pressure on resources.

Cost Inflation and Higher Financing Costs Pressuring Feasibility

Steel rebar rose 15-20% in 2024, and cement increased 8% as demand from giga-projects outran kiln additions. SAIBOR averaged 5.2% in 2025, doubling interest expense for leveraged developers. Fixed-price contracts signed before inflation left mid-tier builders earning 4-6% EBITDA in 2025, down from 8-10% two years earlier. Red Sea Global inserted index-linked escalation clauses in 2025 awards that reimburse 70% of material hikes above a 5% band, offering partial relief. Some proponents are now phasing projects or pivoting to public-private partnerships to de-risk cash flow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Demand Outpaces Infrastructure Spending

Infrastructure held 36.6% of the Saudi Arabian construction market share in 2025, yet residential work is tipped to grow the fastest at a 6.55% CAGR through 2031. Sakani’s pledge to supply 2 million homes and to offer easier mortgages is steering buyers toward villas, townhouses, and mid-rise apartments. ROSHN plans to let USD 1.2 billion of villa packages in 2025 that use prefabricated walls and modular MEP kits to trim build times and ease labor pressure. Early 2026 saw National Housing Company float USD 800 million for solar-ready apartments in Riyadh, while mortgage penetration climbed to 28% in 2025 after subsidized loans lowered borrowing costs.

Transport, power, and water jobs still anchor long pipelines. Saudi Electricity Company has earmarked USD 126 billion for grid upgrades through 2030, and Riyadh Metro awarded extensions in 2025 linking the airport with industrial zones. Commercial activity is also firming: Aramco Trading leased 500,000 m² of warehouse space in Dammam, Riyadh’s key office district cut vacancy to 12%, and Diriyah Gate put USD 2.7 billion of heritage-linked retail corridors out to bid.

By Construction Type: New Construction Dominates Greenfield Development

New Construction captured 81.2% of the Saudi Arabian construction market in 2025, as giga-projects and housing drove greenfield sites. NEOM’s green-hydrogen plant is already 80% complete and will soon draw on 4 gigawatts of solar and wind power. King Salman International Airport, designed for 120 million travelers, requires 8 million m³ of earthworks and 1.2 million m² of terminal floor area. Red Sea Global released USD 3.9 billion for 16 hotels in early 2026, insisting on modular techniques to protect reefs.

Renovation, though a smaller slice, is projected to be the fastest-growing construction type at a 6.91% CAGR between 2026 and 2031. Retrofit work is gathering pace in Riyadh, Jeddah, and Dammam as owners comply with 2024 energy-efficiency rules. Typical upgrades—LED lighting, VRF HVAC, and smart controls—trim power use by 20-30%. Jeddah’s Al-Balad district landed USD 150 million for heritage repairs that mix coral-stone façades with new seismic bracing. Margins, however, stay slim at 4-5% because hidden defects often surface mid-job.

By Construction Method: Modern Methods Gain Momentum Amid Labor Constraints

Within the construction industry in Saudi Arabia, conventional on-site still accounts for 89.6% of 2025 output, but Modern Methods of Construction (MMC) are advancing at a 7.55% CAGR through 2031. China Harbour Engineering’s 500,000 m² Riyadh precast hub, opened in 2025, produces enough panels for 2,000 villas a year and holds ISO 9001:2015 certification, ensuring tolerances within 2 millimeters. NEOM chose fully fitted modular units for 10,000 worker rooms, needing only foundations and hook-ups on site. Red Sea resorts will ship in prefabricated frames from 2026, halving enclosure time and cutting dust near sensitive corals.

Cast-in-place concrete and steel erection remains the norm for heavy highways, bridges, and plants, but rising steel costs of 15-20% in 2024 and 25% higher crane rentals in 2025 are squeezing budgets. Hybrid schemes now appear more often; Qiddiya’s indoor arena pairs precast façades and modular risers with poured-in-place cores to handle complex loads.

By Investment Source: Private Capital Accelerates as Giga-Projects Mature

Public bodies still funded 71.5% of spending in 2025, highlighting their central role in the construction industry in Saudi Arabia, with the Public Investment Fund alone directing USD 40 billion into NEOM, Red Sea, and Qiddiya between 2024 and 2026. Sovereign guarantees back the Saudi Electricity Company’s USD 126 billion grid push, while the National Housing Company relies on land grants and soft loans.

Private money, though smaller, is growing at a 7.10% CAGR as projects move from site prep to revenue-generating phases. Aramco Trading’s 500,000 m² build-to-suit lease in Dammam shows corporate appetite for long leases with inflation clauses. Red Sea Global secured USD 1.2 billion from Gulf wealth funds in 2025, and Riyadh Metro’s latest extensions include 10-year operate-and-maintain deals that hand ridership risk to consortia. High SAIBOR rates of 5.2% in 2025 are still pinching returns and have pushed some developers to stage land purchases until borrowing costs ease.

Geography Analysis

Riyadh’s share of the Saudi Arabia construction market held steady at 36.1% in 2025 on the back of mega-terminal earthworks, metro tunneling, and villa suburbs that absorb the city’s rising population. Sub-markets near King Khalid Airport enjoy spillover demand for warehouses as free-zone incentives draw light manufacturing. Public entities continue to issue phased contracts that maintain a stable pipeline without overheating local labor.

Jeddah’s growth is driven by a USD 1.6 billion port upgrade that adds automated berths and deepens approach channels to anchor larger container ships. The city blends heritage and modernity, with Al-Balad restorations running in parallel with waterfront condos aimed at young professionals. Retail footprints increasingly favor experiential formats that merge shopping with leisure, a trend amplified by rising domestic tourism.

Outlying regions such as Tabuk, Medina, and the Red Sea coast, collectively classified as the Rest of Saudi Arabia, are recording the fastest CAGR of 7.81% through 2031. NEOM’s renewable corridors and tech campuses require extensive road networks, substations, and housing, thereby redirecting engineering talent from the center. Diriyah and Al-Ula revitalizations expand craft construction and boutique hospitality, while inland rail links open mining provinces to export routes. These geographies are gradually balancing the nation’s economic map, but must navigate stricter environmental and archaeological compliance.

Competitive Landscape

Competition is moderate, with the top ten firms accounting for a significant portion of total market turnover in 2025. Saudi Binladin Group leveraged its desert logistics expertise to secure more than USD 5 billion in NEOM infrastructure contracts in 2025, including access roads and utility corridors. China State Construction Middle East clinched a USD 1.8 billion metro extension in Riyadh by pairing balance-sheet strength with rapid mobilization capability. Larsen & Toubro Saudi Arabia secured a USD 1.2 billion high-voltage substation package for the national grid, demonstrating competitive pricing backed by its parent company's procurement power.

Local heavyweights such as Nesma & Partners, Al Rashid Trading, and Almabani are forming alliances with European and Asian specialists to fill technology gaps. Nesma’s venture with Austria’s Strabag will supply 10,000 modular housing units to NEOM by 2027, an arrangement that transfers DfMA expertise and reduces on-site headcount. Contractors differentiate through digital workflows; ROSHN insists on BIM-to-fabrication integration that cuts rework by 15%, a requirement that favors firms with advanced design centers.

White-space niches in logistics warehouses, data centers, and carbon capture attract new entrants. Only two million m² of Grade A logistics space existed nationwide in 2024, leaving Aramco Trading’s 500,000 m² lease a wake-up call for developers. The Saudi Data & AI Authority seeks 300 MW of data center IT load by 2030, calling for contractors with experience in liquid cooling and resilient power. Aramco’s USD 1.7 billion Jubail CCUS hub is the first of its scale, creating premium demand for ASME-certified welding crews and high-pressure pipe fabricators.

Saudi Arabia Construction Industry Leaders

Saudi Binladin Group

Nesma & Partners

Al Rashid Trading & Contracting

Almabani General Contractors

Al Ayuni Investment & Contracting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Red Sea Global awarded USD 3.9 billion for 16 modular hotels, marina works, desalination, and microgrids, with delivery by 2028.

- January 2026: National Housing Company tendered USD 800 million for 4,500 solar-equipped apartments in Riyadh, completion by 2028.

- December 2025: China Harbour Engineering opened a 500,000 m² precast factory in Riyadh, annual capacity of 2,000 villas.

- November 2025: Qiddiya broke ground on a 320,000 m² indoor venue within an USD 8 billion first phase, completion by 2028.

- October 2025: Diriyah Gate tendered USD 2.7 billion of heritage infrastructure to be finished by 2030.

Saudi Arabia Construction Market Report Scope

The construction market includes upcoming, ongoing, and growing construction projects in different sectors. These include but are not limited to geotechnical (underground structures) and superstructures in residential, commercial, and industrial structures, as well as infrastructure construction (like roads, railways, and airports) and power generation and transmission-related infrastructure.

A complete background analysis of the Saudi Arabia Construction market, which includes an assessment of the sector and the contribution of the industry to the economy, market overview, market size estimation for critical segments, key regions, and emerging trends in the market segments, market dynamics, and essential production and consumption statistics, is covered in the report.

The Saudi Arabia Construction Market Report is Segmented by Sector (Residential, Commercial, Infrastructure), by Construction Type (New Construction, Renovation), by Construction Method (Conventional On-Site, Modern Methods of Construction), by Investment Source (Public, Private), and by City (Riyadh, Jeddah, DMA, Rest of Saudi Arabia). Market Forecasts are Provided in Terms of Value (USD).

By Sector

| Residential | Apartments / Condominiums |

| Villas / Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial & Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Sector | Residential | Apartments / Condominiums |

| Villas / Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial & Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By City | Riyadh | |

| Jeddah | ||

| DMA (Dammam Metropolitan Area) | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

How large will construction spending in the Kingdom be by 2031?

The Saudi Arabia construction market size is projected to reach USD 186.13 billion by 2031, expanding at a CAGR of 5.52%.

Which sector is expected to grow the fastest through 2031?

The residential sector is expected to lead growth, with a CAGR of 6.55%, supported by Sakani and national housing initiatives targeting two million new homes.

What share of construction spending is still driven by public funding?

Public sector entities accounted for approximately 71.5% of total construction spending in 2025, although private sector participation is increasing at a CAGR of 7.10%.

Why are modern construction methods gaining adoption?

Prefabricated and modular construction methods reduce project timelines by up to 30% and help mitigate skilled labor shortages and delivery constraints.

Where are the most attractive white-space opportunities emerging?

High-growth opportunities include Grade A logistics parks, hyperscale data centers, and carbon capture infrastructure, driven by limited domestic expertise and strong demand.

Page last updated on: