Concrete Mixer Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 6.37 Billion |

| Market Size (2031) | USD 8.91 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

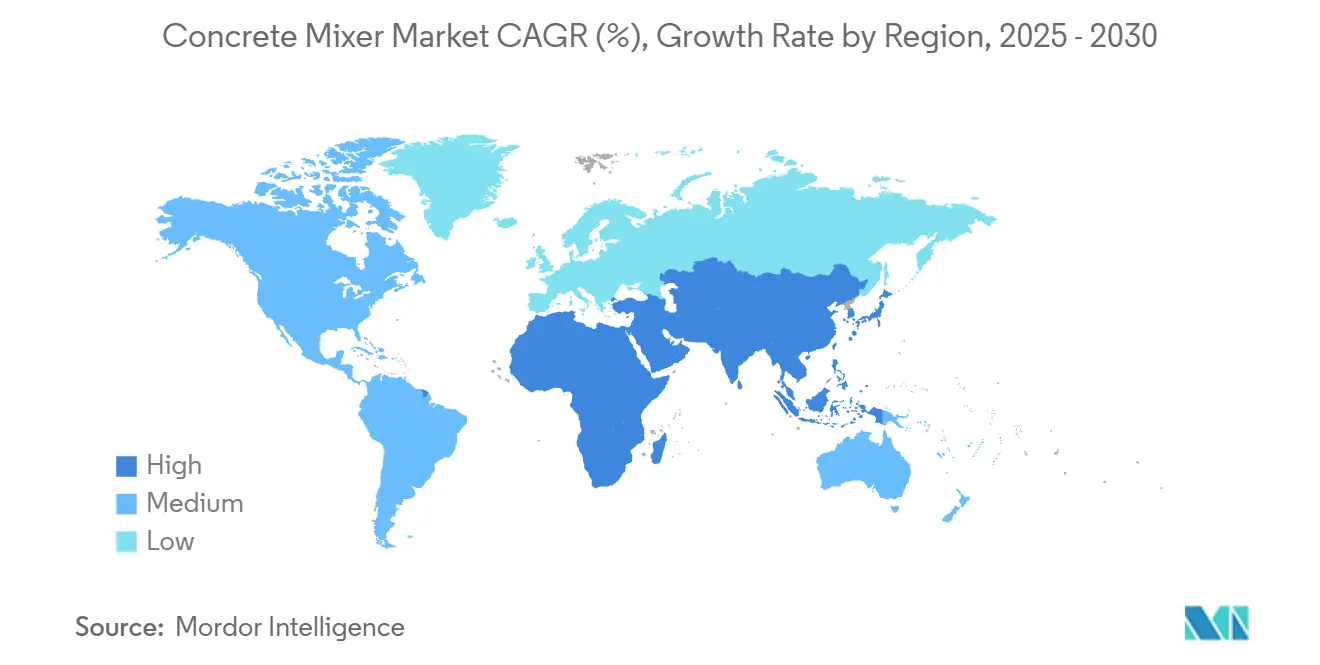

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Concrete Mixer Market Analysis by Mordor Intelligence

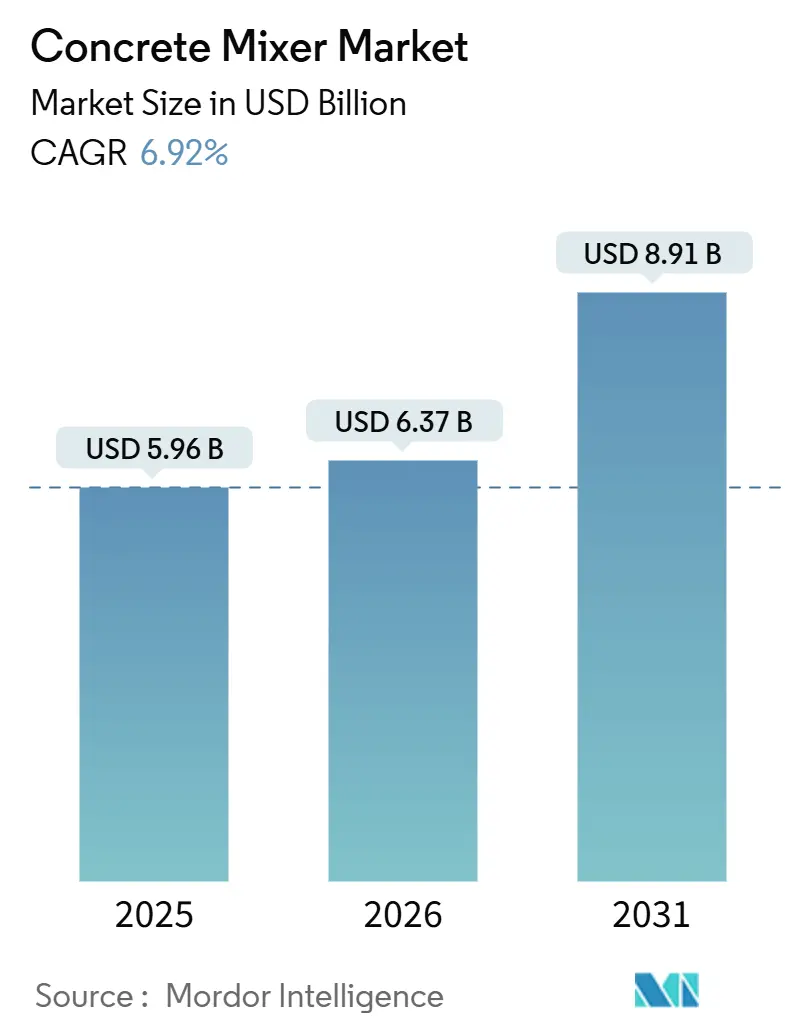

The Concrete Mixer Market size was valued at USD 5.96 billion in 2025 and is estimated to grow from USD 6.37 billion in 2026 to reach USD 8.91 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). Strong public-works pipelines in Asia-Pacific and the Middle East, stricter CO₂ and noise regulations in Europe and North America, and the accelerating pivot to rental and equipment-as-a-service contracts are reshaping procurement strategies. Contractors are splitting purchases between high-capacity stationary plants for mega-projects and portable electric units for urban infill sites, while fleet operators in California and the EU are advancing diesel retirements ahead of depreciation cycles. Twin forces, mega-infrastructure spending and electrification mandates, are therefore nudging demand toward larger, automated, and increasingly battery-powered models. Competitive intensity is moderate, yet Chinese entrants that bundle telematics at zero cost are pressuring incumbent margins, pushing European and U.S. OEMs to pivot toward subscription models with guaranteed uptime.

Key Report Takeaways

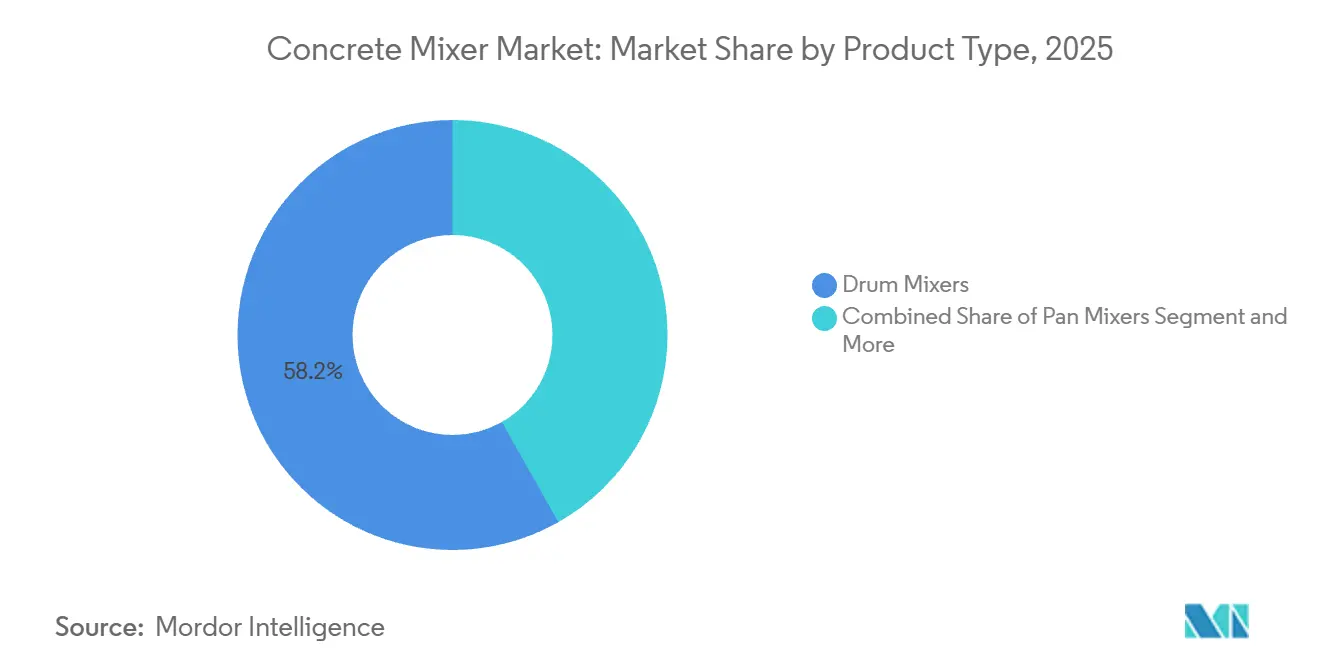

- By product type, drum mixers led with 58.16% revenue share in 2025, while self-loading and volumetric units are projected to expand at a 16.52% CAGR through 2031.

- By capacity, 5 m³ to 10 m³ units accounted for 51.08% of the concrete mixer market share in 2025, whereas sub-2 m³ models are forecast to grow at a 9.82% CAGR to 2031.

- By application, non-residential and commercial construction held 47.04% of 2025 demand; residential projects are set to advance at an 8.34% CAGR on the back of North American housing starts and Southeast Asian affordable-housing schemes.

- By model, stationary equipment accounted for 42.12% of 2025 revenue, yet portable units are advancing at a 9.44% CAGR as zoning constraints and job-site flexibility are driving decisions toward mobile platforms.

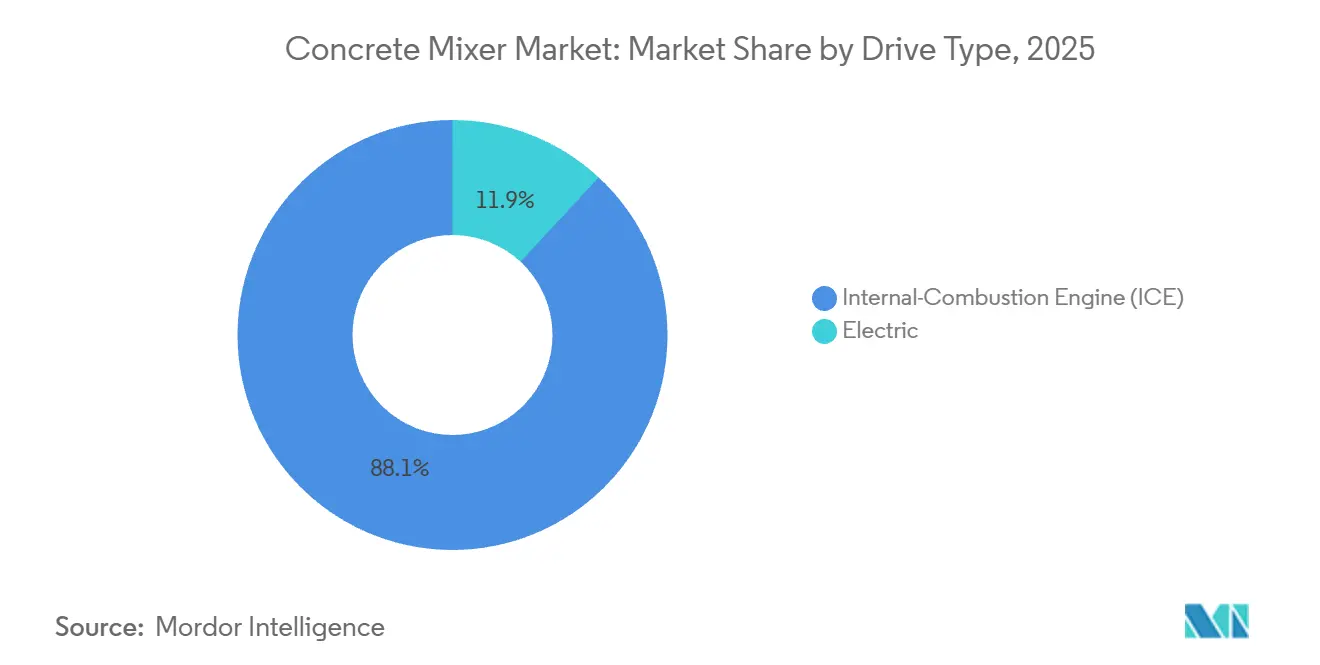

- By drive type, internal-combustion engines dominated with 88.08% of 2025 shipments, while electric variants are climbing at a 16.56% CAGR owing to EU and California zero-emission rules.

- By operating mode, semi-automatic systems held 46.11% share in 2025; fully automatic mixers are on course for a 9.83% CAGR as labor shortages and safety standards spur higher automation.

- By geography, Asia-Pacific accounted for 44.16% of global revenue in 2025 and is forecast to grow at 6.18% through 2031, driven by China’s Belt and Road initiatives and India’s Gati Shakti corridor investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Concrete Mixer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Mega-Infrastructure Spending (2026-2031) | +1.5% | Global, concentrated in Asia-Pacific, Middle East, and select North American corridors | Medium term (2-4 years) |

| Rapid Adoption of Self-Loading and Volumetric Mixers on Remote Sites | +1.0% | Asia-Pacific core, spill-over to Latin America and Africa | Short term (≤ 2 years) |

| Electrification of On-Road Mixer Fleets Amid CO₂ Regulations | +0.9% | North America and EU, early pilots in China | Medium term (2-4 years) |

| Job-Site Digitalization (IoT, Telematics and Predictive Maintenance) | +0.7% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Growth of Rental and “Equipment-As-a-Service” Business Models | +0.6% | North America and EU, emerging in urban APAC | Short term (≤ 2 years) |

| Integration of Advanced Safety and Automation Technologies | +0.5% | Global, regulatory push in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Mega-Infrastructure Spending (2026-2031)

Governments worldwide committed USD 2.3 trillion to infrastructure projects in 2025, with Asia-Pacific accounting for approximately 58% of the announced pipeline value[1]"BloombergNEF Finds Global Energy Transition Investment Reached Record $2.3 Trillion in 2025, Up 8% from 2024," BloombergNEF, about.bnef.com.. India's National Infrastructure Pipeline alone targets USD 1.4 trillion in capital outlays through 2030[2]"Bridging India's infrastructure funding gap by 2025," Steer Group, steergroup.com., prioritizing highways, metro rail, and industrial corridors that require continuous concrete supply. Saudi Arabia's NEOM megacity and Egypt's New Administrative Capital are absorbing high-capacity stationary mixers at rates that exceed historical norms for Middle Eastern projects, as contractors seek to minimize truck cycles on remote desert sites. Estimates suggest that every USD 1 billion in infrastructure spending generates demand for approximately 120 to 150 concrete mixer units, depending on project density and the proximity of batching plants. This multiplier effect is most pronounced in Asia-Pacific, where fragmented supply chains and limited ready-mix penetration compel contractors to deploy on-site mixing capacity, thereby sustaining double-digit order books for drum and twin-shaft models through 2028.

Rapid Adoption of Self-Loading and Volumetric Mixers on Remote Sites

Self-loading and volumetric mixers are expanding at 16.52% CAGR, outpacing traditional drum units, because remote mining camps, wind-farm foundations, and modular housing projects cannot justify the capital cost of fixed batching plants. A 2025 study by the National Renewable Energy Laboratory found that modular construction sites reduce concrete waste when using volumetric mixers, as operators can adjust mix designs in real time to match structural specifications. In Australia, Rio Tinto deployed 47 self-loading units across its Pilbara iron-ore operations in 2025, citing a 22% reduction in concrete delivery lead times compared to truck-mounted drum mixers. The UK Department for Transport reviewed volumetric mixer weight limits in 2024. It proposed increasing the weight limit to 44 tons gross vehicle weight, allowing operators to carry larger aggregate payloads and further enhancing the economics of remote sites. These units also appeal to contractors in Latin America and Sub-Saharan Africa, where road infrastructure is inadequate for heavy ready-mix trucks, making self-contained batching the only viable option for rural electrification and irrigation projects.

Electrification of On-Road Mixer Fleets Amid CO₂ Regulations

The European Union's Heavy-Duty Vehicle CO₂ standards, finalized in 2024, mandate a 45% reduction in fleet-average emissions by 2030 relative to 2019 baselines[3]"2025 Automotive Package – Proposed targeted amendment to CO₂ emission standards for heavy-duty vehicles," European Commission, climate.ec.europa.eu., effectively requiring concrete-mixer operators to transition at least 30% of new purchases to battery-electric or hydrogen powertrains. California's Advanced Clean Fleets rule, which took effect in January 2024, prohibits large fleets from purchasing diesel concrete mixers after 2027, accelerating the shift to zero-emission models. Volvo delivered the first production-series electric concrete mixer to CEMEX in 2023. By mid-2025, CEMEX had expanded its electric-mixer pilot to 12 units across Germany and the Netherlands, reporting a 68% reduction in total cost of ownership over five years, factoring in fuel savings and lower maintenance costs. Putzmeister's iONTRON e-Mixer, launched in 2024, uses a 350 kWh battery pack that enables 8-hour shifts without mid-day charging, addressing the primary operational concern of ready-mix fleet managers. However, a 2025 UC Davis study comparing battery-electric and fuel-cell-electric concrete mixers concluded that grid-carbon intensity in coal-dependent regions such as Poland and India can negate lifecycle emissions benefits, underscoring the need for parallel investments in renewable electricity generation.

Job-Site Digitalization (IoT, Telematics, and Predictive Maintenance)

Caterpillar reported in its 2025 annual filing that 78% of its new concrete-mixer shipments include factory-installed telematics modules, up from 54% in 2023, enabling fleet managers to monitor drum rotation speed, hydraulic pressure, and engine diagnostics in real time. Komatsu's Smart Construction platform, deployed on over 12,000 construction sites globally by the end of 2025, integrates concrete-mixer data with excavator and loader feeds to optimize material flow and reduce idle time by an average of 14%.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel and Component Price Volatility Squeezing OEM Margins | −0.8% | Global, acute in regions dependent on imported steel | Short term (≤ 2 years) |

| Grid-Power Scarcity Limiting Uptake of Full-Electric Mixers in EMs | −0.4% | South Asia, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Tightening Global Noise-Emission Limits for Diesel Drum Trucks | −0.3% | EU, North America, select Asia-Pacific urban centers | Medium term (2-4 years) |

| High Initial Investment and Maintenance Costs Restricting Growth | −0.5% | Global, acute for small and mid-sized contractors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel and Component Price Volatility Squeezing OEM Margins

Hot-rolled coil steel prices averaged USD 720 per tonne in 2025, down from the 2022 peak of USD 1,150 but still 38% above 2019 levels, according to the OECD Steel Committee's 2025 outlook. Concrete-mixer manufacturers typically lock in steel contracts 6 to 9 months ahead of production, exposing them to margin compression when spot prices spike; Zoomlion disclosed in its 2024 annual report that raw-material inflation eroded gross margin by 210 basis points year-over-year, forcing the company to raise list prices by 4.5% in early 2025. Engineering News-Record's Q3 2025 cost report noted that hydraulic components, electric motors, and electronic control units saw price increases of 12% to 18% in 2024-2025, driven by semiconductor shortages and tariff escalations on Chinese-manufactured parts. The International Monetary Fund's October 2025 metals-price update projects that nickel and copper—critical inputs for electric-mixer battery packs and wiring harnesses—will remain 25% above long-term averages through 2027, sustaining cost pressure on zero-emission product lines. Smaller OEMs with limited hedging capacity are most vulnerable: several European manufacturers delayed new-model launches in 2025 to avoid locking in unfavorable component contracts, ceding market share to vertically integrated Chinese competitors that produce steel and hydraulics in-house.

Grid-Power Scarcity Limiting Uptake of Full-Electric Mixers In Emerging Markets

India's Ministry of Power reported that industrial electricity demand exceeded grid capacity by an average of 8% during peak construction months in 2025, forcing contractors to rely on diesel generators for job-site power and rendering battery-electric mixers impractical for projects beyond urban centers. Sub-Saharan Africa faces similar constraints: the World Bank's 2025 Africa Infrastructure Diagnostic found that 43% of construction sites in Nigeria, Kenya, and Tanzania lack reliable grid connections, compelling contractors to specify internal-combustion mixers despite higher fuel costs. In Brazil, transmission-line upgrades lag behind renewable-generation capacity additions, creating localized bottlenecks that prevent fast-charging infrastructure for electric construction fleets; Volvo suspended deliveries of its electric mixer to São Paulo-based ready-mix operators in mid-2025 after grid outages caused three units to miss scheduled pours. The International Energy Agency's 2025 Electricity Market Report estimates that emerging markets would need to invest USD 180 billion in distribution-grid upgrades by 2030 to support widespread electrification of heavy-duty vehicles, a funding gap that current public budgets and multilateral lending cannot close. Until grid reliability improves, electric-mixer adoption in these regions will remain confined to government-backed pilot projects and multinational contractors with access to on-site solar-plus-storage systems.

Segment Analysis

By Product Type: Drum Dominance Faces Self-Loading Disruption

Drum mixers delivered 58.16% of 2025 revenue, reflecting entrenched positions in ready-mix fleets that value continuous discharge and high throughput. The concrete mixer market size for self-loading and volumetric units is projected to expand at a 16.52% CAGR through 2031 as remote-site economics reward on-demand batching. Pan and planetary variants serve niche precast and refractory segments in Europe and Japan, while twin-shaft designs are gaining momentum in China and India’s industrialized construction drive. Price-sensitive mining operators in Australia and Sub-Saharan Africa increasingly specify self-loading models to slash haul distances, a pivot that is eroding drum dominance in those geographies.

Twin-shaft mixers are securing a foothold in precast factories that prioritize homogeneity and rapid cycle times. Planetary types remain favored for ultra-high-performance concrete in petrochemical and aerospace projects, suggesting long-cycle, stable demand. Pan mixers occupy a niche where strict quality control trumps output volume. Consequently, OEMs are broadening portfolios to straddle both high-capacity stationary plants and agile self-loading solutions, aiming to retain wallet share as project profiles splinter.

Note: Segment shares of all individual segments available upon report purchase

By Capacity: Mid-Range Dominates, Small Units Surge

Mixers rated 5 m³ to 10 m³ accounted for 51.08% of 2025 shipments, aligning with standard heavy-truck payload limits and the batch sizes required for logistics warehouses, metro stations, and mid-rise offices. Sub-2 m³ units are growing at a 9.82% CAGR through 2031 as the do-it-yourself segment and suburban housing boom favor maneuverable, lower-cost gear. Above-10 m³ giants serve dams, runways, and megacity foundations where continuous pours demand maximum drum capacity to cut truck cycles.

The concrete mixer market share for the 2 m³ to 5 m³ band is eroding as contractors either trade up to exploit economies of scale or trade down to tap renovation niches, creating a barbell distribution in capacity preferences. Revised ISO 18650 metrics now align European and U.S. definitions, simplifying cross-border sales and enabling OEMs to platform-share more aggressively across weight classes.

By Application: Residential Gains, Infrastructure Holds

Non-residential and commercial projects claimed 47.04% of 2025 demand, buoyed by logistics hubs, data centers, and mixed-use urban complexes that require high-volume, tightly scheduled pours. Residential construction is advancing at an 8.34% CAGR through 2031 as single-family starts rebound in North America and Southeast Asia roll out affordable housing schemes. Infrastructure—roads, bridges, and ports—remains the largest absolute volume driver, with every kilometer of new expressway absorbing 12,000–15,000 m³ of concrete.

Regional policy packages, such as the U.S. Infrastructure Investment and Jobs Act and India’s urban housing push, anchor medium-term visibility. Mining, energy, and industrial projects swing with commodity cycles, lending volatility to the “others” bucket. Yet modular housing and prefabrication are gently lowering concrete intensity per unit, so sustained volume growth hinges on project proliferation rather than per-project material demand.

By Model Type: Portable Flexibility Challenges Stationary Scale

Stationary mixers accounted for 42.12% of 2025 revenue, due to ready-mix and precast facilities that amortize fixed assets over high throughput. Portable units are expected to grow at a 9.44% CAGR through 2031, appealing to contractors seeking mobility amid zoning hurdles and shorter project lead times. Below 800 m³ per month, portable systems beat stationary plants on total cost, while mega-projects rely on stationary plants linked to twin-shaft mixers that deliver 240 m³ per hour.

Asia’s constrained urban cores, from Mumbai to Manila, now favor portable electric units that can relocate around diesel-ban districts. Conversely, Saudi Arabia’s NEOM relies on six giant stationary plants for mass pours across a contiguous desert site. Rental houses fuel portable demand, maximizing fleet utilization across sequential jobs while avoiding stranded-asset risk tied to stationary batching permits.

By Drive Type: ICE Incumbency Meets Electric Momentum

Internal-combustion engines accounted for 88.08% of the target market's 2025 shipments due to lower sticker prices and the ubiquity of diesel supply chains. Electric drives are growing at a 16.56% CAGR through 2031, driven by EU and California regulations and falling battery costs. A concrete mixer market size comparison shows that electric models achieve 68% lower five-year total costs in low-carbon grids, yet yield smaller gains in coal-dominated grids.

Hybrid systems offer 30% fuel cuts without charging infrastructure, acting as a bridge technology. Norway’s penetration already stands at 18%, while India and Brazil remain below 2% due to grid unreliability and weak subsidies. Emissions credits and urban noise rules are expected to widen regional adoption gaps through 2031.

By Operating Mode: Automation Erodes Manual Share

Semi-automatic modes accounted for 46.11% of 2025 shipments, balancing operator oversight with automated batching to reduce errors. Fully automatic systems are forecast for a 9.83% CAGR through 2031, propelled by labor shortages that inflate skilled-operator wages 30% above the construction average. Manual units persist in cost-sensitive emerging markets but face regulatory headwinds as new safety standards raise the baseline for automation.

Automated slump control and sensor-driven water dosing reduce rejection rates and improve sustainability by limiting over-watering. Remote-operation suites allow fleet managers to start batches and monitor drum health from mobile dashboards, shrinking the need for on-site crews and improving asset utilization across multiple concurrent jobs.

Geography Analysis

Asia-Pacific contributed 44.16% of 2025 revenue and is set for a 6.18% CAGR to 2031, driven by China’s metro tie-ups and India’s USD 1.4 trillion Gati Shakti program. Chinese tier-2 cities such as Chengdu and Wuhan approved 18 new metro lines in 2025, each requiring roughly 340,000 m³ of concrete per month. India added self-loading mixers along highway corridors to curb haul times and mitigate ready-mix undersupply. Japan’s shipments dipped 3.2% as new builds slowed, yet electric uptake rose due to Tokyo’s diesel exclusion zone, which began in 2027. South Korea shifted its budget to bridge rehab, elevating demand for compact portable units.

North America and Europe jointly delivered 38% of 2025 sales. The U.S. Infrastructure Act’s USD 110 billion allocation sustains mixer utilization above 70% through 2026. Germany’s output slipped 1.8% under higher interest rates, but electric mixer sales grew 42% as fleets pre-complied with 2030 CO₂ caps. The UK faced labor shortages and customs friction, nudging contractors toward portable rentals. France’s Grand Paris Express buoyed stationary mixer orders, while Italy’s seismic retrofits favored portable solutions for historic cores. Spain’s coastal housing revival relied heavily on rental fleets rather than outright purchases.

South America, the Middle East, and Africa together held roughly 18% of revenue. Brazil’s USD 24 billion infrastructure push buttressed sales in the Amazon and Northeast, yet grid weaknesses limited electric penetration outside São Paulo. Argentina’s austerity led to a 7.2% contraction in the market. Saudi Arabia’s NEOM and Egypt’s New Capital absorbed 68 high-capacity mixers in 2025 for desert pours. The UAE leveraged Expo 2025 legacy projects to sustain demand despite softer residential starts. South Africa’s load-shedding episodes disrupted our schedules, hurting the adoption of battery units. Turkey rebounded 9.4% on earthquake reconstruction and airport expansion, though currency volatility raised unit costs by 18%.

Competitive Landscape

The concrete mixer market shows moderate concentration, with the top five OEMs accounting for a significant share of global shipments. Chinese challengers undercut incumbents by 15–20% with in-house steel and hydraulics, plus free telematics, squeezing incumbent margins. North American rental penetration above 55% is forcing legacy manufacturers to launch subscription tiers bundling predictive maintenance and uptime guarantees, effectively recasting themselves as fleet-service providers.

Technology is the main battleground. Caterpillar’s 2025 telematics suite enabled remote batching and reduced downtime by 27%, supporting 8% price premiums. Volvo’s minority stake in Ramirent marks a vertical-integration play to lock in recurring revenue streams. Patent filings hint at strategic priorities: Liebherr targets thermal management for electric mixers, while SANY focuses on hydraulic fuel efficiency. ISO 15143-3 interoperability opens the door for third-party software, potentially eroding brand lock-in and heightening competitive churn.

Regulatory arbitrage persists: some manufacturers ship non-compliant diesel units at steep discounts into Africa and Latin America, creating a two-tier market. Meanwhile, white-space opportunities in charging infrastructure, modular self-loading platforms, and AI batching optimization attract startups and joint ventures, suggesting the next wave of disruption could come from outside traditional heavy-equipment circles.

Concrete Mixer Industry Leaders

-

Liebherr Group

-

Sany Group

-

Zoomlion Heavy Industry Science & Technology Co. Ltd

-

Terex Corporation

-

Shantui Construction Machinery Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Revolution Concrete Mixers announced the expansion of its U.S. manufacturing operations with a fully equipped facility in Rochester, Minnesota, to meet strong demand driven by increased capacity for commercial, infrastructure, and essential construction sectors. The move is intended to accelerate production timelines and deliver greater capacity to contractors and concrete producers across North America.

- January 2024: Cemen Tech launched its new-generation CD2 dual-bin volumetric concrete mixer. The new model features a unique split bin with individual compartments for transporting and blending various supplementary cementing materials (SCMs).

Global Concrete Mixer Market Report Scope

A concrete mixer is a device that mixes cement, aggregate (such as sand or gravel), and water to create concrete. To mix the components, a standard concrete mixer employs a spinning drum.

The concrete mixer market is segmented by type, drive type, operating mode, application, and geography. By type, the market is segmented into fixed and portable. By drive type, the market is segmented into ICE and electric. By operating mode, the market is segmented into manual, semi-automatic, and fully automatic. By application, the market is segmented into residential and commercial. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

The report offers the market size and forecasts for all the above segments in value (USD ).

| Drum Mixers |

| Pan Mixers |

| Planetary Mixers |

| Twin-Shaft Mixers |

| Below 2 m³ |

| 2 – 10 m³ |

| Above 10 m³ |

| Residential Construction |

| Commercial Construction |

| Infrastructure Development |

| Roads and Bridges |

| Others |

| Portable Mixers |

| Stationary Mixers |

| Internal-Combustion Engine (ICE) |

| Electric |

| Manual |

| Semi-Automatic |

| Fully-Automatic |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey |

| By Product Type | Drum Mixers | |

| Pan Mixers | ||

| Planetary Mixers | ||

| Twin-Shaft Mixers | ||

| By Capacity | Below 2 m³ | |

| 2 – 10 m³ | ||

| Above 10 m³ | ||

| By Application | Residential Construction | |

| Commercial Construction | ||

| Infrastructure Development | ||

| Roads and Bridges | ||

| Others | ||

| By Model Type | Portable Mixers | |

| Stationary Mixers | ||

| By Drive Type | Internal-Combustion Engine (ICE) | |

| Electric | ||

| By Operating Mode | Manual | |

| Semi-Automatic | ||

| Fully-Automatic | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

Key Questions Answered in the Report

How fast is the concrete mixer market growing through 2031?

It advances at a 6.92% CAGR from 2026 to 2031, reaching USD 8.91 billion by 2031.

Which region contributes the most to global concrete mixer revenue?

Asia-Pacific leads with 44.16% of 2025 revenue and shows a 6.18% growth outlook through 2031.

What mixer type is gaining traction on remote construction sites?

Self-loading and volumetric models are expanding at a 16.52% CAGR because they batch concrete on demand without fixed plants.

How do rental and equipment-as-a-service trends influence procurement?

Rental penetration topped 55% in North America during 2025, pushing OEMs to package mixers with telematics and uptime guarantees via subscription contracts.

What is the main obstacle to adopting electric concrete mixers in emerging markets?

Grid-power scarcity limits fast-charging infrastructure, forcing contractors to rely on diesel gensets and delaying widespread electric uptake.