Computer Numerical Controls (CNC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

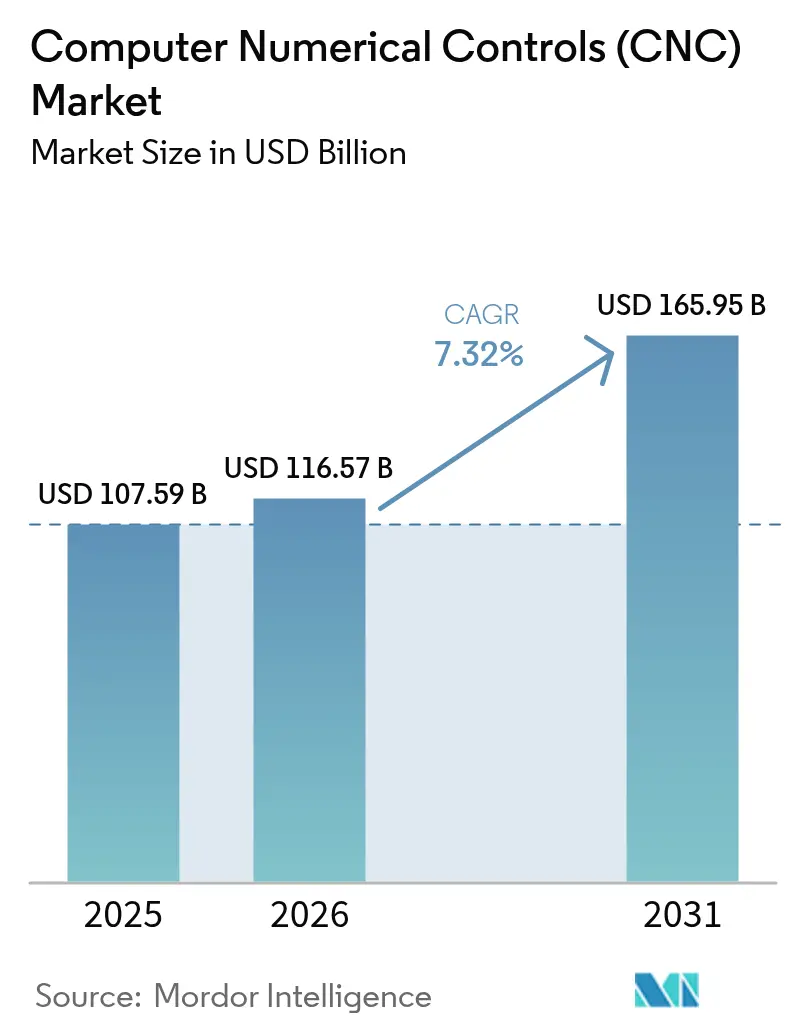

| Market Size (2026) | USD 116.57 Billion |

| Market Size (2031) | USD 165.95 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

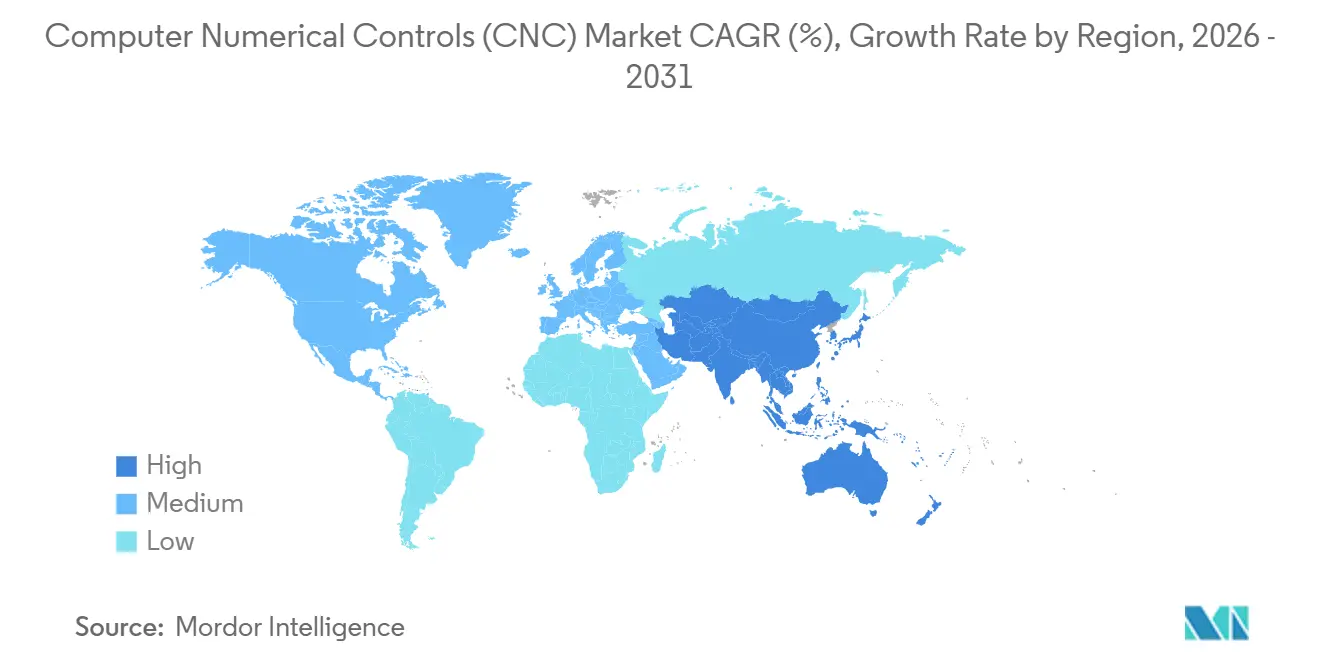

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

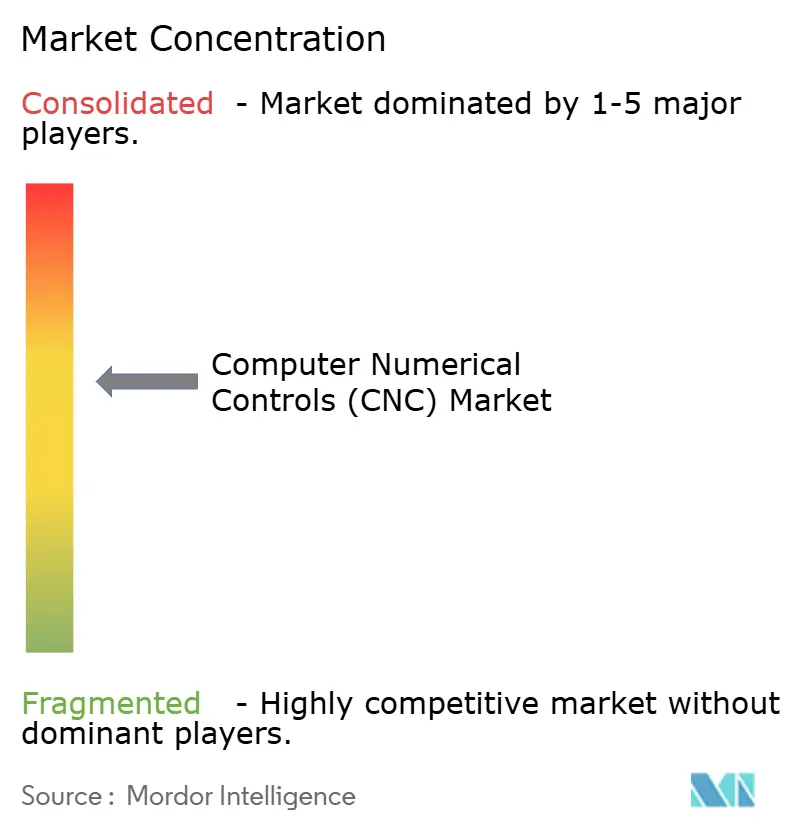

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Computer Numerical Controls (CNC) Market Analysis by Mordor Intelligence

The Computer numerical controls (CNC) market size is projected to be USD 107.59 billion in 2025, USD 116.57 billion in 2026, and reach USD 165.95 billion by 2031, growing at a CAGR of 7.32% from 2026 to 2031. Widespread electrification in automotive manufacturing, government-funded on-shoring incentives, and rapid uptake of Industry 4.0 digital-twin retrofits are expanding the Computer numerical controls (CNC) market across both advanced and emerging economies. Multi-axis machining demand is rising as EV power-train housings, turbine blades, and micro-medical implants require compound-curve geometries that legacy 3-axis mills cannot meet, prompting global tier-1 suppliers to adopt closed-loop servo architectures with sub-micron repeatability. Integrated cells that couple CNC machines with collaborative robots now capture more than half of new installations, a direct response to skilled-labor shortages in North America and Europe. At the same time, semiconductor motion-control chip shortages and volatile raw-material prices temper near-term purchasing appetite, especially among small and medium enterprises that operate on tightening margins.

Key Report Takeaways

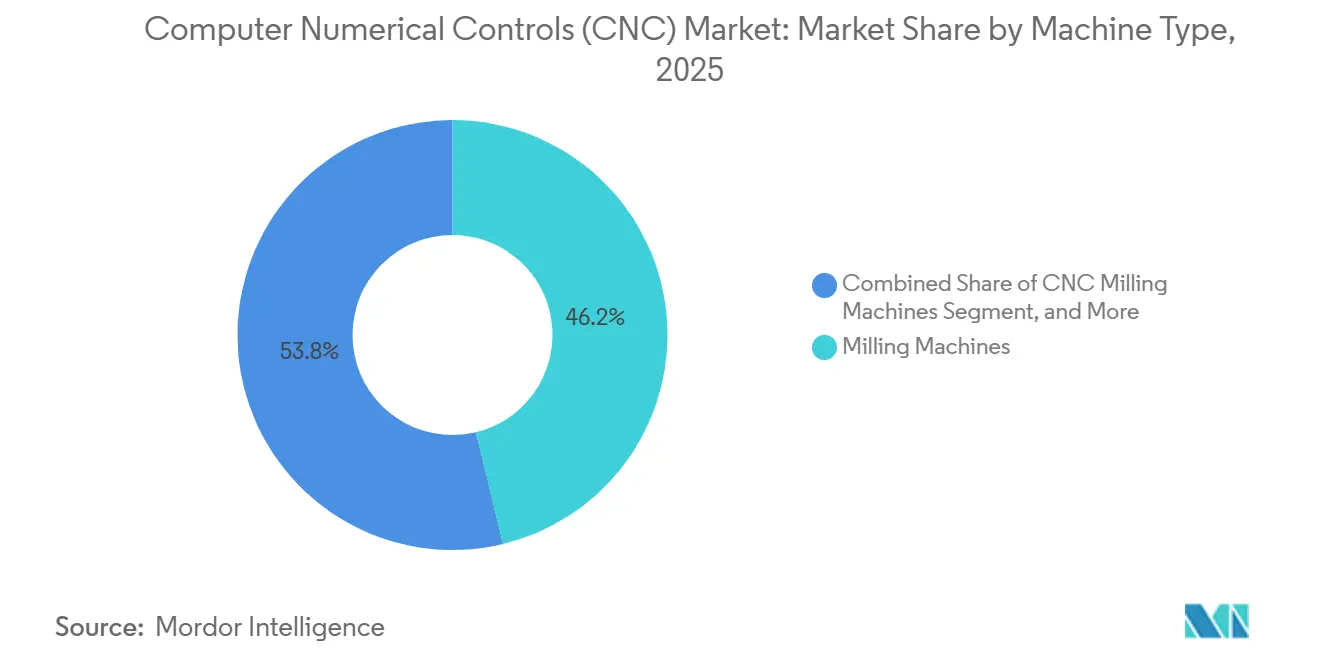

- By machine type, milling equipment led with 46.23% of Computer numerical controls (CNC) market share in 2025, while simultaneous 5-axis centers are expanding at an 8.04% CAGR through 2031.

- By axis type, 3-axis machines held 48.54% revenue in 2025, yet 5-axis and above configurations are the fastest-growing at an 8.98% CAGR.

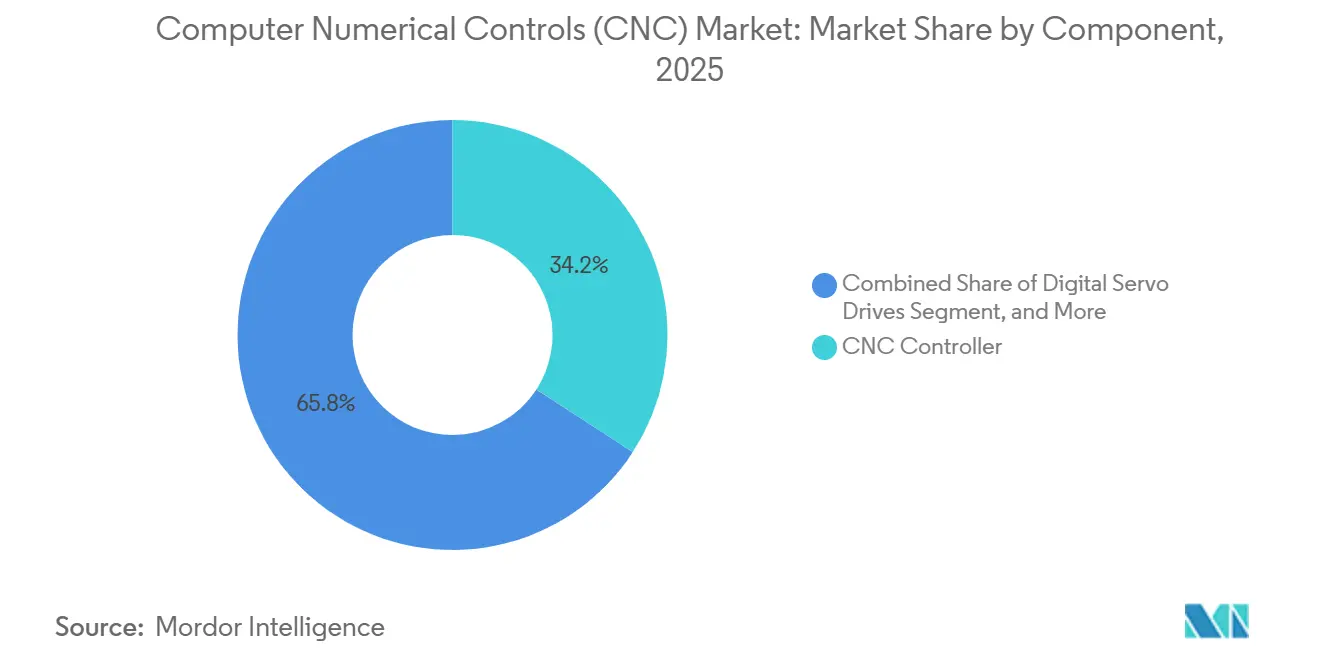

- By component, CNC controllers captured 34.16% of the Computer numerical controls (CNC) market size in 2025, whereas digital servo drives are forecast to post a 9.45% CAGR to 2031.

- By control system, closed-loop architectures dominated with 62.23% revenue in 2025 and are advancing at 7.59% per year through 2031.

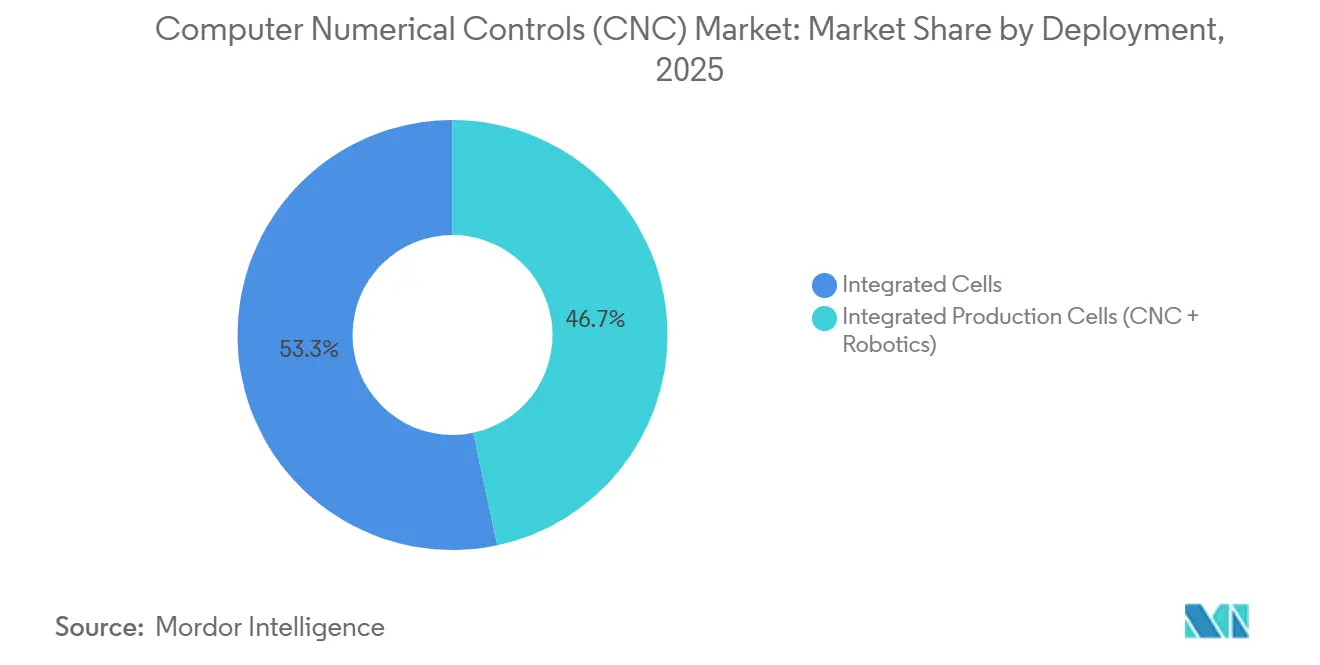

- By deployment, integrated production cells commanded 53.34% value in 2025 and are growing at an 8.21% CAGR as lights-out factories spread across North America and Europe.

- By end user, automotive remained the largest buyer at 31.11% of 2025 spending, whereas medical devices deliver the quickest expansion at a 9.87% CAGR to 2031.

- By geography, North America captured 47.87% of 2025 revenue, Asia-Pacific is the fastest-growing at a 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Computer Numerical Controls (CNC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV powertrain complexity boosting multi-axis CNC demand | +1.2% | Global, with concentration in China, Germany, United States | Medium term (2-4 years) |

| Industry 4.0 digital-twin-enabled CNC retrofits drive OEE | +1.0% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Automated CNC cells mitigate global skilled-labor gaps | +0.9% | North America, Europe, Australia | Long term (≥ 4 years) |

| Micro-CNC boom in minimally invasive medical devices | +0.7% | United States, Germany, Japan, Switzerland | Medium term (2-4 years) |

| Additive-subtractive hybrid CNCs shorten build-times | +0.6% | Aerospace hubs: United States, France, United Kingdom | Medium term (2-4 years) |

| On-shoring incentives accelerate SME CNC upgrades | +0.8% | United States, European Union, India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Power-Train Complexity Boosting Multi-Axis CNC Demand

Electric-vehicle battery housings, motor casings, and inverter heat-sinks require ±0.05 mm tolerances over compound curves, a specification only simultaneous 5-axis platforms routinely achieve. Tesla’s Texas Gigafactory cut battery-tray cycle time from 47 minutes to 19 minutes by installing 120 Fanuc Robodrill 5-axis mills in 2024.[1]Fanuc Corp., “Automotive Applications,” fanuc.com BYD lifted 5-axis procurement 340% between 2024 and 2025 to support its Blade Battery ramp toward 3 million packs annually by 2027. European tier-1 supplier Guhring invested EUR 85 million in 2025 retrofitting legacy machining centers with TNC7 controllers for EV geometries. Lightweighting regulations and part-count consolidation mean each EV needs fewer but more intricate components, locking in demand for multi-axis Computer numerical controls (CNC) market solutions.

Industry 4.0 Digital-CNC Retrofits Lift OEE

Digital-twin overlays predict spindle wear up to 72 hours before failure, cutting unplanned downtime roughly 70%. Siemens’ Sinumerik ONE controller, installed on 1,200 European cells in 2025, couples edge-computing vibration analytics with automated tool changes, trimming cycle times 6-9%.[2]Siemens AG, “Sinumerik CNC Systems,” siemens.com A 2024 Applied Sciences study validated 9.8% throughput and 12.3% energy savings after retrofits in an aerospace shop. Government subsidies, such as Japan’s JPY 12 billion IoT grant, further accelerate adoption through 2027.[3]Ministry of Economy, Trade and Industry (Japan), “Subsidies for IoT Retrofits,” meti.go.jp

Automated CNC Cells Ease Skilled-Labor Gaps

The U.S. Bureau of Labor Statistics forecasts a 375,000-machinist shortage by 2030. Integrated cells pair mills with collaborative robots so a single operator can run four to six stations, quadrupling output per labor hour. Okuma’s MULTUS U3000 integrates a 12-second gantry robot, enabling 16-hour lights-out shifts and dropping unit labor cost 28% in German deployments during 2025. Similar labor-saving economics underpin 63% of North American automation projects sampled in the 2024 A3 survey.

Micro-CNC Boom in Minimally Invasive Medical Devices

Demand for sub-50-micron titanium parts is surging as outpatient arthroplasty and transcatheter therapies scale. The U.S. FDA cleared 147 micro-machined implants in 2025, 22% more than 2024. SwissNano and Cincom lathes now achieve 0.5-micron repeatability on millimeter-size stent components, lowering scrap and unlocking new device geometries. Stryker’s Mako platform drove USD 1.1 billion revenue in 2025 through such precision implants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor motion-control chip shortages | -0.8% | Global, acute in Asia-Pacific electronics hubs | Short term (≤ 2 years) |

| High CAPEX of 5-axis / hybrid machines for SMEs | -0.6% | North America, Europe, India | Medium term (2-4 years) |

| Cybersecurity risks in networked CNC environments | -0.3% | Europe, North America (IEC 62443 compliance zones) | Long term (≥ 4 years) |

| Volatile steel and aluminum prices squeeze ROI | -0.5% | Global, with acute impact in commodity-importing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor Motion-Control Chip Shortages

Lead times for servo-drive power modules peaked at 38 weeks in early 2025 as TSMC constrained 28 nm automotive-grade capacity, forcing CNC builders to redesign around alternate microcontrollers. Fanuc saw a 14% sequential drop in controller shipments during Q1 2025 as Infineon IGBT supplies tightened. Japan’s Machine Tool Association estimated USD 2.3 billion in deferred orders, with normalization expected by late 2026 when new fabs come online.

High CAPEX of 5-Axis and Hybrid Machines for SMEs

Entry-level simultaneous 5-axis mills start near USD 275,000; hybrid additive-subtractive systems exceed USD 2 million, stretching job-shop balance sheets. Although payback on aerospace or medical parts can be under 24 months, 54% of small enterprises cite financing barriers despite U.S. SBA low-interest loans and EU credit lines. Resulting investment hesitancy slows penetration of advanced Computer numerical controls (CNC) market technologies among firms with fewer than 50 employees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Milling Dominance Meets 5-Axis Disruption

Milling platforms commanded 46.23% of the Computer numerical controls (CNC) market size in 2025, reflecting their versatility for automotive, aerospace, and industrial components. Single-setup 5-axis models cut turbine-blade machining time from 18 hours to 7 hours for Airbus suppliers, explaining the segment’s 8.04% CAGR to 2031. Lathe systems held roughly 22% share, serving high-volume turned parts, though EV drivetrains are displacing conventional shafts. Laser-cutting machines secured 12% as battery and chassis fabricators expanded capacity, while plasma, EDM, and grinding platforms jointly contributed under 15%, focused on mold and die applications.

Adoption momentum increasingly favors multifunction units that merge milling, laser texturing, or additive deposition. DMG MORI’s DMU 50 3rd Gen integrates laser surface finishing, removing secondary operations and lowering total process time 40%. Entry-level 5-axis options such as Haas’ UMC-750SS priced at USD 275,000 have widened access for North American job shops, shipping 1,200 units in 2025 alone. These dynamics indicate a steady migration toward advanced platforms despite capital hurdles, keeping the Computer numerical controls (CNC) market on an innovation trajectory.

By Axis Type: 3-Axis Incumbency Challenged by 5-Axis Upswing

Three-axis machines kept 48.54% Computer numerical controls (CNC) market share in 2025 due to familiar programming and lower ticket prices between USD 50,000 and 150,000. Yet 5-axis systems grow at 8.98% per year, driven by aerospace and medical brackets that complete in one 4-hour cycle versus 11 hours across multiple 3-axis setups. Four-axis horizontals remain popular for automotive block machining at 18% share, offering indexed rotation without simultaneous contouring. Retrofit kits, such as Mitsubishi’s USD 40,000 rotary fourth axis, extend the life of 3-axis assets for cost-sensitive users.

Simultaneous 5-axis machining eliminates fixture complexity and raises material-removal rates 35% on titanium landing-gear parts, validating its premium pricing for defense primes. Mazak’s INTEGREX i-630V merges turning and 5-axis capabilities inside a 4 m envelope, giving oil-and-gas valve builders a one-machine solution. As German and Italian buyers pushed 5-axis orders to 31% of new bookings in 2025, the axis-shift became a leading growth lever for the broader Computer numerical controls (CNC) market.

By Component: Controllers Rule, Servo Drives Surge

Controllers represented 34.16% revenue in 2025, making them the computational core of the Computer numerical controls (CNC) industry. Siemens’ Sinumerik ONE edges in on software subscriptions, while Fanuc’s 30i-B Plus embeds AI thermal-compensation for ±2 µm accuracy. Servo drives, at roughly 28%, are the fastest-growing component, advancing 9.45% annually to 2031 thanks to higher-torque silicon-carbide units like Mitsubishi’s MELSERVO-J5W. High-resolution encoders and probes account for about 18%, enabling closed-loop feedback that meets FDA implant standards.

Spindles, tool-changers, and coolant systems make up the balance. NSK’s 60,000 RPM micro-spindle and Bosch Rexroth’s regenerative IndraDrive cut energy use by 18%, underscoring how incremental component gains aggregate to meaningful OEE improvements. As controller and drive architectures converge with edge-AI, software content per machine rises, reshaping profit pools within the Computer numerical controls (CNC) market.

By Control System: Closed-Loop Precision Prevails

Closed-loop machines held 62.23% revenue in 2025, climbing 7.59% a year as medical and aerospace users demand ±1 µm accuracy. Encoder feedback corrects positioning errors in real time, whereas open-loop steppers suffice for wood and plastics within ±50 µm. Hybrid modes, like Fanuc’s 0i-F Plus, allow shops to toggle between cost and precision, stretching budget flexibility.

Heidenhain’s TNC7 applies adaptive algorithms that offset thermal drift, maintaining 1.5 µm accuracy over 12-hour shifts without manual resets. NUM’s Flexium+ couples closed-loop control with digital-twin simulation, letting engineers validate tool-paths virtually and slash commissioning 40%. Regulatory nudges, notably FDA guidance mandating process monitoring for implant machining, cement closed-loop as the long-term default in the Computer numerical controls (CNC) market.

By Deployment: Integrated Cells Capture Automation Premium

Integrated robotic cells secured 53.34% of 2025 spending, leveraging lights-out production to offset labor scarcity. Fanuc’s Robodrill cell raised utilization from 65% to 88% across 420 units installed at North American auto suppliers. DMG MORI’s MATRIS links a dozen machines via autonomous mobile robots, creating flexible job routing and 24/7 operation using a single supervisor. Stand-alone equipment still dominates low-volume job shops—particularly in emerging economies—but the share gap narrows each year as cobot prices fall.

Mazak’s Palletech 30-pallet pool runs 180 part numbers weekly with four operator hours, illustrating throughput economics that justify premium capex. European laser-cutting cells now merge bending and inspection in the same envelope, trimming sheet-metal lead times 55%. Automation-first deployment therefore stands out as a structural vector for Computer numerical controls (CNC) market expansion.

By End User: Automotive Dominates, Medical Accelerates

Automotive applications claimed 31.11% spending in 2025, buoyed by battery-tray and aluminum-casting work for EVs. Aerospace and defense remained sizeable at 24%, with Boeing saving USD 18 million in material via hybrid additive-subtractive machining. Power generation machinery followed at 14%, while industrial equipment held 12% and electronics about 8%, driven by wafer-handling robotics.

Medical devices, however, deliver the fastest 9.87% annual growth as outpatient orthopedics boom. Zimmer Biomet’s Persona IQ smart knee illustrates micro-machining’s role in sensorized implants, generating USD 340 million in 2025 sales. Mining, marine, and construction collectively represent 11%, with Caterpillar deriving 18% of 2025 revenue from CNC-machined hydraulic components. Such diversification provides resilience, ensuring the Computer numerical controls (CNC) market grows despite cyclical slowdowns in any one vertical.

Geography Analysis

North America generated 47.87% of Computer numerical controls (CNC) market revenue in 2025 as USD 1.2 billion of reshoring-linked orders flowed to aerospace and automotive suppliers taking advantage of CHIPS Act subsidies. The United States remains the epicenter, while Mexico attracted USD 8.4 billion in automotive investment leveraging USMCA incentives and cost-competitive labor. Canada’s Quebec and Ontario aerospace corridors consumed CAD 1.1 billion in CNC tools during 2025 as Bombardier expanded turbine machining.

Asia-Pacific is the fastest-growing at a 7.78% CAGR to 2031, driven by China’s goal to build 800,000 industrial robots yearly, many with CNC end-effectors. Domestic builders like Dalian Machine Tool lifted share to 42% of China’s 1.2 million-unit output. India’s INR 145 billion PLI scheme subsidizes 5-axis acquisitions, while Japan’s Fanuc, Mazak, Okuma, and DMG MORI shipped 68,000 machines worldwide in 2025.

Europe captured roughly 28% of value, anchored by Germany, Italy, and Switzerland, which accounted for 23% of global 5-axis deliveries. Volkswagen’s EUR 180 billion electrification drive underpins fresh demand across its 120 facilities. The UK, France, and Spain round out activity with aerospace and automotive retooling programs that rely heavily on precision CNC equipment.

South America, the Middle East, and Africa collectively account for under 10% but display green-shoots: Brazil’s Embraer upgrades, Saudi Arabia’s 14 new CNC plants, and South African mining refurbishment all signal latent upside. These pockets will progressively expand the Computer numerical controls (CNC) market footprint beyond its historic tri-continental core.

Competitive Landscape

The Computer numerical controls (CNC) market is moderately concentrated, the top 10 vendors captured roughly 52% revenue in 2025, yet Chinese challengers erode pricing power. Incumbents pivot toward software-rich offerings—Siemens’ Sinumerik ONE Edge adds predictive-maintenance subscriptions that return 22% gross margins versus 15% for hardware alone. DMG MORI’s CELOS interface locked in 8,400 active users by end-2025, reinforcing ecosystem stickiness.

Hybrid additive-subtractive machines represent an 11% growth niche where startups like Meltio deliver sub-USD 300,000 units, pressuring higher-priced incumbents. Cybersecurity compliance under IEC 62443 tilts the field toward integrated vendors that bundle secure controllers with firewalls, elevating total cost of ownership but lowering breach risk. Patent filings mirror this software tilt: Fanuc registered 47 U.S. patents on AI machining in 2024-2025, while Mitsubishi’s M800 series embeds real-time feed-rate optimization for titanium parts.

Regional specialists still flourish: GSK CNC and Dalian controlled 42% of China’s domestic market by offering 5-axis mills at 40-50% price discounts, though export traction remains limited due to tighter spindle and thermal-stability standards abroad. Indian players such as Ace Micromatic are leveraging PLI subsidies to localize controller manufacturing and aim for 25% import substitution by 2027. Overall, competitive intensity continues to pivot on software ecosystems, cybersecurity readiness, and the speed of multi-axis innovation.

Computer Numerical Controls (CNC) Industry Leaders

Siemens AG

JTEKT Corporation

Hurco Companies Inc

Haas Automation, Inc.

Fanuc Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens launched Sinumerik ONE Edge with 5G and edge-AI, trimming 5-axis cycle times by up to 11% in its first 140 automotive installations.

- December 2025: DMG MORI opened a USD 180 million Pune plant to produce 2,400 machines annually for South Asian exporters.

- November 2025: Fanuc and Nvidia partnered on AI-embedded controllers that lowered scrap 14% in 22 aerospace pilots.

- September 2025: Haas released the UMC-1000SS 5-axis VMC at USD 325,000, targeting SME aerospace and medical shops.

Global Computer Numerical Controls (CNC) Market Report Scope

Computer numerical control (CNC) machining is the process through which computers control machine-based processes in manufacturing. The kinds of machines controlled include lathes, mills, routers, and grinders all of which are used for the manufacturing of metal and plastic products. Applications are in automotive. oil and gas, aerospace and defense, and others.

The Computer Numerical Controls (CNC) Market Report is Segmented by Machine Type (Lathe, Milling, Laser Cutting, Plasma Cutting, EDM, Grinding, Winding, Welding, Other), Axis Type (3-Axis, 4-Axis, 5-Axis and Above), Component (Controller, Servo-Motor Drive, Sensors and Feedback, Other), Control System (Open-loop, Closed-loop), Deployment (Stand-alone, Integrated Cells), End-User (Automotive, Aerospace, Power, Industrial, Medical, Electronics, Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| CNC Lathe Machines |

| CNC Milling Machines |

| CNC Laser Cutting Machines |

| CNC Plasma Cutting Machines |

| CNC EDM Machines |

| CNC Grinding Machines |

| CNC Winding Machines |

| CNC Welding Machines |

| Other Machine Types |

| 3-Axis |

| 4-Axis |

| 5-Axis and Above |

| CNC Controller |

| Servo-Motor Drive |

| Sensors and Feedback |

| Other Components |

| Open-loop |

| Closed-loop |

| Stand-alone CNC Machines |

| Integrated Production Cells (CNC + Robotics) |

| Automotive (incl. EV) |

| Aerospace and Defence |

| Power and Energy |

| Industrial Machinery |

| Medical Devices |

| Electronics and Semiconductor |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Machine Type | CNC Lathe Machines | |

| CNC Milling Machines | ||

| CNC Laser Cutting Machines | ||

| CNC Plasma Cutting Machines | ||

| CNC EDM Machines | ||

| CNC Grinding Machines | ||

| CNC Winding Machines | ||

| CNC Welding Machines | ||

| Other Machine Types | ||

| By Axis Type | 3-Axis | |

| 4-Axis | ||

| 5-Axis and Above | ||

| By Component | CNC Controller | |

| Servo-Motor Drive | ||

| Sensors and Feedback | ||

| Other Components | ||

| By Control System | Open-loop | |

| Closed-loop | ||

| By Deployment | Stand-alone CNC Machines | |

| Integrated Production Cells (CNC + Robotics) | ||

| By End-User | Automotive (incl. EV) | |

| Aerospace and Defence | ||

| Power and Energy | ||

| Industrial Machinery | ||

| Medical Devices | ||

| Electronics and Semiconductor | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Computer numerical controls (CNC) market be by 2031?

It is forecast to reach USD 165.95 billion by 2031, reflecting a 7.32% CAGR from 2026 to 2031.

Which end-user segment is expanding fastest?

Medical-device manufacturers lead with a 9.87% CAGR thanks to demand for micro-machined implants approved under the U.S. FDA’s 510(k) pathway.

Why are 5-axis machines gaining share over 3-axis platforms?

A single 5-axis setup completes complex parts hours faster and eliminates costly fixturing, accelerating adoption despite higher upfront prices.

How are digital-twin retrofits improving CNC profitability?

Predictive-maintenance analytics reduce unplanned downtime up to 70% and cut cycle times around 8%, lifting overall equipment effectiveness.

What limits rapid CNC adoption among small enterprises?

High capital costs—often exceeding USD 350,000 for advanced 5-axis units—and tighter lending criteria hamper financing for SMEs.

Page last updated on: