Compressed Natural Gas (CNG) Dispenser Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

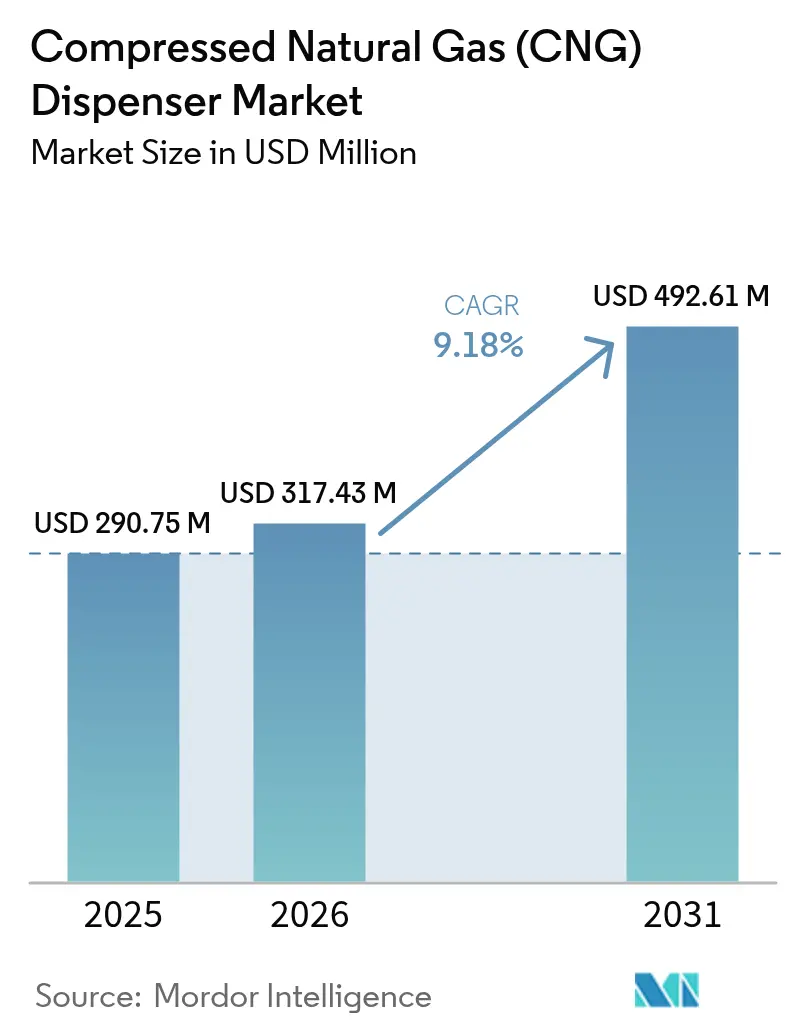

| Market Size (2026) | USD 317.43 Million |

| Market Size (2031) | USD 492.61 Million |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

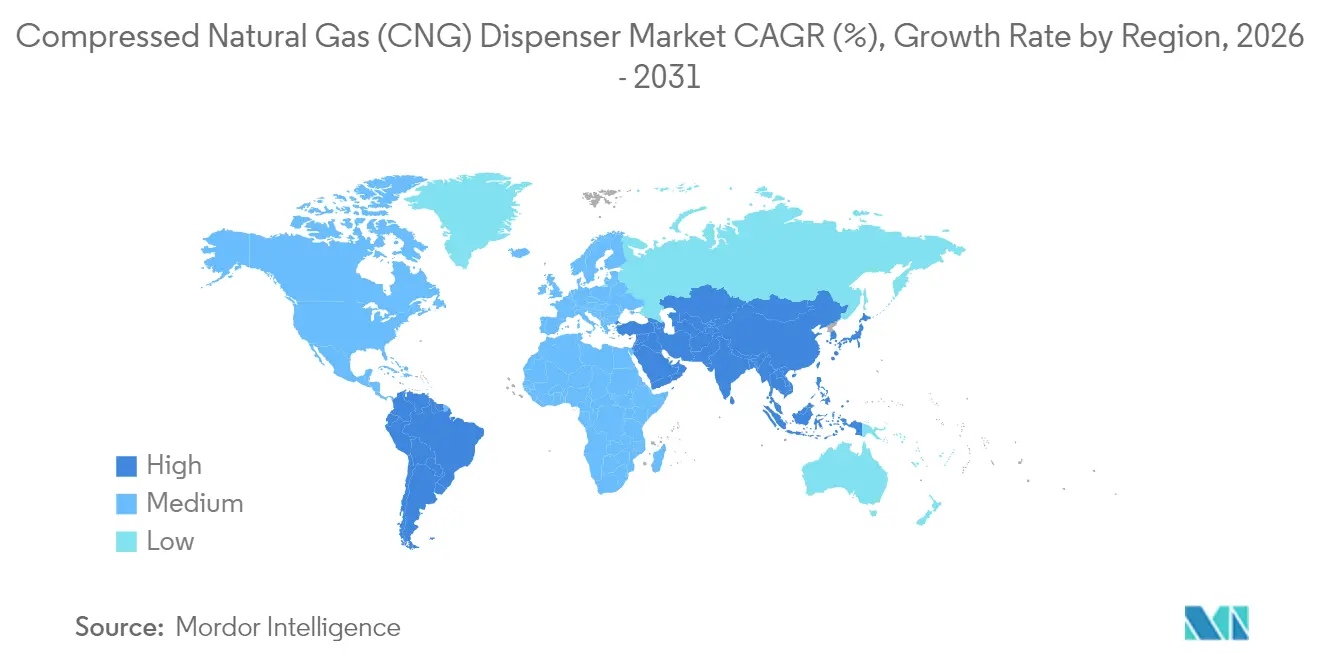

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compressed Natural Gas (CNG) Dispenser Market Analysis by Mordor Intelligence

The Compressed Natural Gas Dispenser Market size is expected to grow from USD 290.75 million in 2025 to USD 317.43 million in 2026 and is forecast to reach USD 492.61 million by 2031 at 9.18% CAGR over 2026-2031.

Global demand is gaining momentum from stringent emission mandates, USD 635 million in U.S. federal grants for alternative-fuel stations, and accelerated fleet conversions, collectively shortening the payback periods for new outlets. Growing natural-gas vehicle (NGV) sales in Asia, federal corridor build-outs in North America, and meter upgrade cycles driven by methane-slip rules further underpin the upward trajectory of the CNG dispenser market. Competitive positioning centers on hydrogen-ready modular systems, IoT-enabled uptime optimization, and acquisition-led scale building that reinforce integrated clean-energy portfolios. Government support outweighs capital hurdles in most core regions, yet budget shifts toward EV charging and gas-quality variability introduce operational and funding headwinds for traditional participants in the CNG dispenser market.

Key Report Takeaways

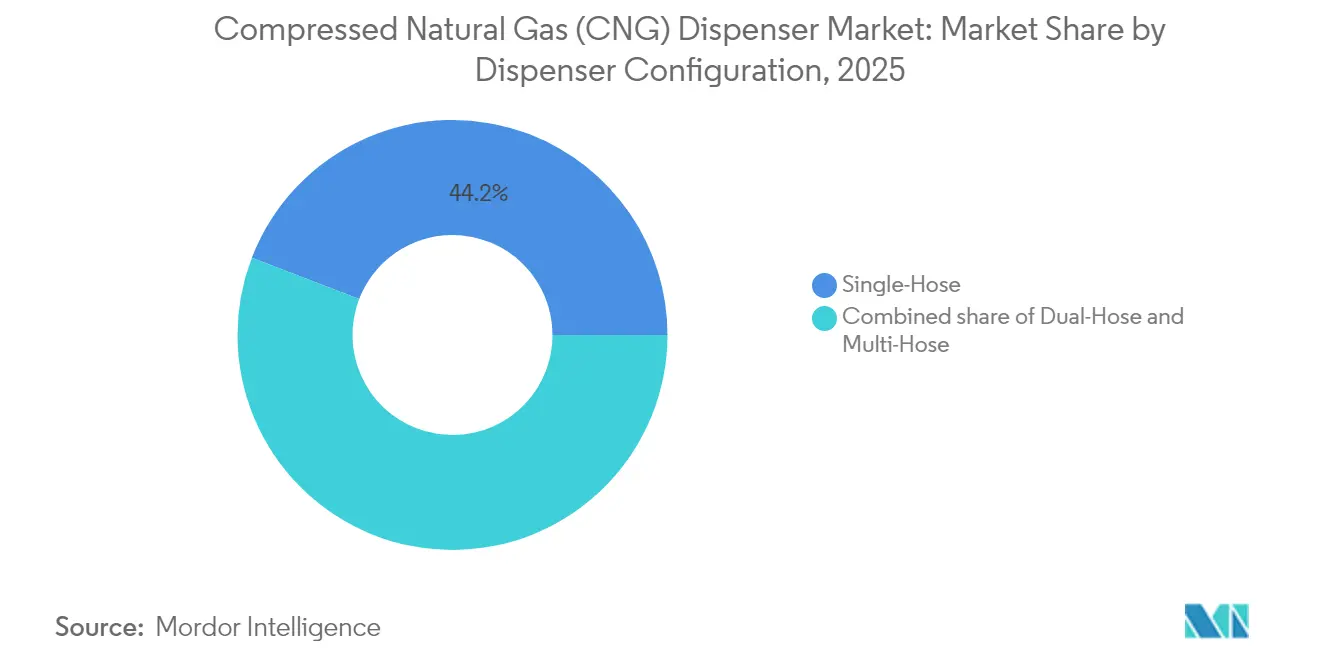

- By dispenser configuration, single-hose units held 44.15% of the CNG dispenser market share in 2025; multi-hose systems are projected to post a 12.7% CAGR through 2031.

- By station type, fast-fill outlets accounted for 59.05% of the CNG dispenser market size in 2025, while mobile/portable units are forecasted to expand at a 13.3% CAGR through 2031.

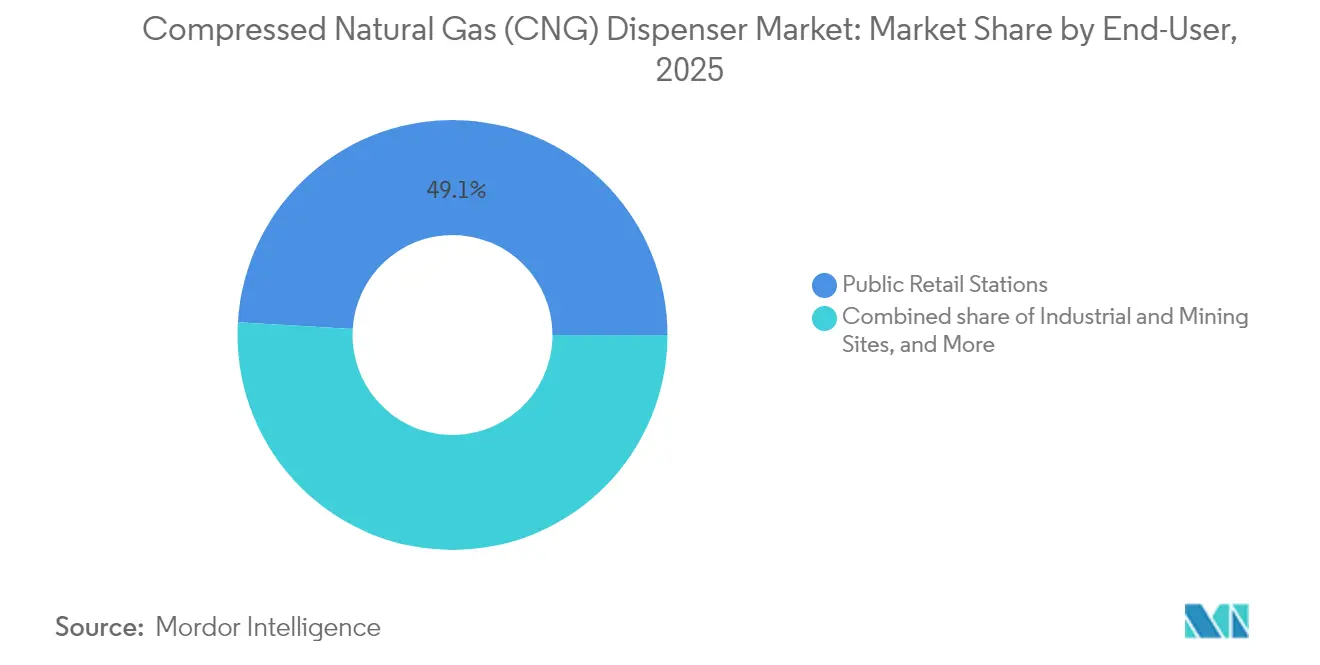

- By end-user, public retail locations accounted for 49.05% of demand in 2025, while industrial and mining sites recorded the fastest growth at a 12.4% CAGR.

- By geography, the Asia-Pacific region led with 47.95% revenue in 2025; it is anticipated to maintain a 10.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compressed Natural Gas (CNG) Dispenser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives & rapid CNG station build-outs | 2.10% | North America, Asia-Pacific | Medium term (2-4 years) |

| Lower total-cost-of-ownership for fleet operators | 1.80% | Global, stronger in Asia-Pacific & South America | Long term (≥ 4 years) |

| Rising NGV sales in Asia & South America | 1.50% | Asia-Pacific core, spill-over to South America | Medium term (2-4 years) |

| IoT-enabled predictive maintenance | 1.20% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Hydrogen-ready modular dispensers | 0.90% | EU & North America | Long term (≥ 4 years) |

| Stricter methane-slip monitoring | 0.70% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government incentives & rapid CNG station build-outs

Federal backing reshapes economic fundamentals for the CNG dispenser market. The United States awarded USD 635 million in 2025 grants covering 27 states, directly subsidizing dispenser installations for freight corridors.[1]U.S. Department of Transportation, “FHWA Announces Alternative Fuel Corridor Grants,” transportation.gov The Infrastructure Investment and Jobs Act earmarks USD 2.5 billion over five years for alternative-fuel corridors, providing multi-layered funding that reduces capital risk. California adds USD 95.2 million through its Clean Transportation Program, while a 30% federal tax credit lowers out-of-pocket hardware costs.[2]Internal Revenue Service, “Alternative Fuel Vehicle Refueling Property Credit,” irs.gov Similar provincial incentives in Canada and conversion credits in Utah and Georgia expand the support network. Reduced effective project costs shorten payback periods and encourage operators to specify higher-throughput, hydrogen-compatible dispensers that future-proof installations.

Lower total-cost-of-ownership for fleet operators

Natural gas maintains a durable price discount to diesel, averaging USD 1.17 per diesel gallon equivalent in 2025.[3]U.S. Energy Information Administration, “Weekly Natural Gas Price Update,” eia.gov Heavy-duty engines, such as Cummins’ X15N, provide 1,850 lb-ft of torque while eliminating the need for diesel exhaust fluid, thereby cutting running expenses and maintenance downtime.[4]Cummins Inc., “X15N Engine Specifications,” cummins.com Light-duty bi-fuel pickups achieve combined ranges of nearly 650 miles and realize emission reductions of 13–40% compared to gasoline alternatives. Fleet operators leveraging private time-fill depots lock in multiyear gas contracts, insulating budgets from oil-price volatility. Collectively, these economics bolster procurement plans and funnel recurring demand into the CNG dispenser market.

Rising NGV sales in Asia & South America

India aims to have 7.5 million CNG vehicles by FY 2025, supported by an expansion from 1,081 to approximately 7,400 stations over the decade. China consumed 38.9 billion cubic meters of CNG-grade gas in 2023, under its natural-gas transition strategy, providing a scale for dispenser deployment. South America operates more than 5 million NGVs, with Bolivia nearing a 52% penetration rate. Petrobras is commissioning 1.2 million m³/d of biomethane supply, increasing the potential for lifting station throughput. Subsidized pump prices and mandatory low-emission fleet rules across Buenos Aires, Bogotá, and São Paulo further stimulate regional uptake.

IoT-enabled predictive maintenance

Advanced sensor suites and edge analytics reduce unplanned downtime by roughly 80% for gas-distribution equipment, according to peer-reviewed field studies. Low-power SCADA modules transmit pressure, temperature, and flow data over GSM or Wi-Fi, consuming under 4 W, enabling sub-$50 retrofit kits suitable for legacy dispensers. Dover Fueling Solutions embeds remote diagnostics in its newest hydrogen-ready models, enabling cloud-based firmware updates that reduce the need for on-site service visits. Higher uptime directly increases daily fuel volumes, which improves revenue yields and strengthens the investment case for smart dispensers within the CNG dispenser market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front CAPEX for fast-fill stations | –1.4% | Emerging markets globally | Medium term (2-4 years) |

| EV-charging roll-out diverting budgets | –1.1% | North America & EU | Long term (≥ 4 years) |

| Gas-quality variability | –0.8% | Global | Short term (≤ 2 years) |

| Lack of heavy-duty connector standards >300 bar | –0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High up-front CAPEX for fast-fill stations

Turn-key installation for a four-lane fast-fill site can exceed USD 1.8 million, roughly double the outlay of a comparable diesel facility. Financing hurdles rise in rural corridors where throughput forecasts remain uncertain, leading to bank reluctance or higher interest rates. Smaller operators often pivot to time-fill or mobile trailers, postponing large-scale station construction. Although a 30% U.S. federal credit softens cash demands, many projects stall until anchor-tenant agreements guarantee baseline volume.

EV-charging roll-out diverting infrastructure budgets

Policy and investor sentiment lean toward electrification. Washington’s National Electric Vehicle Infrastructure program allocates USD 5 billion exclusively for chargers through 2028, dwarfing appropriations for gaseous fuels. California alone aims to target 1.01 million chargers by 2030, diverting public and private capital away from gas-based initiatives. Retailers balancing portfolio risk prioritize quick-service 350 kW chargers that meet Zero-Emission Vehicle mandates, tightening funding channels available to the CNG dispenser market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dispenser Configuration: multi-hose systems lift throughput

The single-hose format retained a 44.15% revenue share in 2025 due to its low entry cost, while multi-hose models are slated for a 12.7% CAGR as operators pursue faster queue turnover during peak hours. Dual-hose units serve midsize fleets that value redundancy without the footprint of four-lane skids. The Wayne Helix 6000 II features cloud telemetry, enabling remote flow validation and predictive part replacement, which reduces life-cycle costs. Shorter fill times translate into higher daily transactions per nozzle, improving return on investment and intensifying capital expenditure for advanced heads in the CNG dispenser market, particularly for configuration upgrades.

Across retrofit programs, station owners replace single hoses with two-hose swing arms that accommodate both 3,000 psig and 3,600 psig vehicles while retaining the original island. Adoption accelerates at metropolitan bus depots that must refuel up to 300 units nightly. Multi-hose up-ratings also dovetail with 15 psi inlet-pressure boosts stemming from grid-compression expansions, which allow tanks to reach nominal cut-out faster and cycle more customers during the same service window.

By Station Type: mobile units extend coverage

Fast-fill facilities captured 59.05% of the 2025 revenue pool, favored for public retail and large trucking corridors. Portable skids mounted on trailers are growing at the fastest rate, with a 13.3% CAGR, bridging service gaps in satellite towns and construction zones. Delhi and Mumbai host 1.5-ton mobile pods that refuel up to 150 cars per deployment, illustrating how flexible assets relieve congestion at fixed forecourts. Time-fill depots remain integral for private fleets with overnight dwell times, where capital-light compressors and cascade banks suffice.

California’s Kern County awards of USD 0.5 million enable rural school districts to lease portable dispensers for seasonal bus operations, sidestepping multi-million-dollar fixed builds. Event-based models in Europe dispatch trailer tanks to music festivals, demonstrating the service elasticity that underpins the growth of marquee players in this segment of the CNG dispenser market.

By End-User: industrial sites accelerate heavy-duty adoption

Public retail retained 49.05% of 2025 demand but faces a moderated 7.6% forward CAGR, whereas industrial and mining complexes lift orders at 12.4%. Cummins’ X15N debut in Class 8 tractors gives mines the torque to haul overburden while trimming NOx emissions by 90%, enabling sites to meet tougher Scope 1 targets. Transit authorities extend the life of existing bus fleets by adding particulate-trap upgrades and shifting to RNG contracts that pair with existing 250-bar plumbing.

Private depots add CNG to hedge against diesel price swings, especially for top-20 logistics players that refuel on-premise. BHP’s Australian iron-ore division pilots dual-fuel haul trucks, signalling cross-sector uptake. Together, these heavy-duty conversions reinforce a steady revenue backlog for dispenser makers and service contractors in the CNG dispenser market.

Geography Analysis

The Asia-Pacific region dominates the global landscape, accounting for a 47.95% revenue share in 2025 and is projected to grow at a 10.4% CAGR through 2031. India’s station count is on track to surpass 7,400 by FY 2025, anchoring regional infrastructure depth. China’s 38.9 billion m³ CNG consumption in 2023 underscores the massive scale, and municipal air-quality rules are pushing additional bus fleet conversions. Japan and South Korea contribute technology exports—valves, sensors, and payment terminals—creating a vertically integrated supply chain that favors local assembly of advanced dispensers.

North America leverages USD 2.5 billion in corridor funding plus USD 635 million in discretionary awards to extend coverage across 27 states. California’s 30% tax credit and 95.2 million clean-transport budget catalyze incremental forecourt builds. The region hosts about 156,000 NGVs—concentrated in trash collection, parcel delivery, and municipal fleets—providing predictable throughput for operators and a stable aftermarket for upgrade kits within the CNG dispenser market.

South America sustains over 5 million NGVs, spearheaded by Argentina’s aftermarket conversion market and Bolivia’s 52% penetration. Petrobras is installing 1.2 million m³/d biomethane capacity that will feed existing gas grids, ensuring a stable supply for dispensers. Policy-driven pump-price discounts and widening trucking bans on Euro III diesel engines are expected to bolster medium-term demand.

Europe lags in NGV volumes but sets the technical direction through hydrogen-ready forecourt standards. Germany’s 1,000th combined H₂/CNG sausage-type dispenser came online in 2025, marking the evolution of dual-fuel sites. The continent’s focus on renewable gas certificated via RED II drives meter upgrades and traceability modules, compelling service contracts that enrich the European slice of the CNG dispenser market.

Mordor Intelligence provides coverage of the compressed natural gas (cng) dispenser market across other key regional markets, including Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The market shows moderate consolidation as top players pursue portfolio diversification. Dover Corporation spent USD 1.3 billion across four acquisitions in 2024, folding cryogenic valves and control electronics into its fueling division. Gilbarco Veeder-Root secured USD 59 million in HPCL dispenser orders, reinforcing its 50-year presence in India. Chart Industries expanded its Nordic service coverage through the acquisition of CSC Cryogenic Service Center AB, which supports LNG truck stops and CNG maintenance.

Technology race points to IoT dashboards, remote firmware upgrades, and 700-bar compatibility. Dover’s dual-nozzle hydrogen/CNG unit ships with embedded LTE telemetry that pushes diagnostics to a cloud portal, cutting field service dispatches by 30%. Gilbarco pilots blockchain-based fuel provenance tags for RNG blends, responding to traceability demands under Europe’s RED II. Specialized firms producing trailer-mounted skids enter at a lower capital cost, contesting a niche that grows at a 13.8% CAGR yet remains thinly served by multinationals, revealing white-space in the CNG dispenser market.

Compressed Natural Gas (CNG) Dispenser Industry Leaders

Gilbarco Veeder Root

Tatsuno Europe AS

Scheidt & Bachmann Gmbh

Kraus Global

Bennett Pump Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Daimler Truck NA started production of the Freightliner Cascadia equipped with the Cummins X15N, the first 15-liter natural-gas engine for heavy-duty trucks.

- April 2025: Trillium Energy Solutions bought U.S. Energy’s CNG network, expanding to 107 locations in North America.

- March 2025: CIMC Enric secured orders for 1,000 dual 1,500 L LNG cylinders worth RMB 1.285 billion (USD 178.5 million).

- January 2025: The U.S. DOT announced USD 635 million in grants for alternative-fuel infrastructure, with 67% of the funding directed to disadvantaged communities.

Global Compressed Natural Gas (CNG) Dispenser Market Report Scope

The compressed natural gas (CNG) dispenser market report include:

| Single-Hose |

| Dual-Hose |

| Multi-Hose |

| Fast-Fill |

| Time-Fill |

| Mobile/Portable |

| Public Retail Stations |

| Private Fleet Depots |

| Transit and Bus Fleets |

| Industrial and Mining Sites |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Dispenser Configuration | Single-Hose | |

| Dual-Hose | ||

| Multi-Hose | ||

| By Station Type | Fast-Fill | |

| Time-Fill | ||

| Mobile/Portable | ||

| By End-User | Public Retail Stations | |

| Private Fleet Depots | ||

| Transit and Bus Fleets | ||

| Industrial and Mining Sites | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the CNG dispenser market in 2026?

The CNG dispenser market size reached USD 317.43 million in 2026 and is set for robust expansion toward USD 492.61 million by 2031.

What is the expected growth rate through 2031?

Global revenue is projected to rise at a 9.18% CAGR, supported by policy incentives and fleet conversions.

Which region currently leads demand?

Asia-Pacific holds 47.95% of 2025 revenue thanks to large NGV fleets in India and China.

Which segment grows fastest by station type?

Mobile and portable dispensers are forecast to post a 13.3% CAGR as operators target underserved areas.

What technology trend gains the most traction?

Hydrogen-ready modular dispensers equipped with IoT diagnostics are becoming mainstream as forecourts prepare for multi-energy offerings.

Who are the key industry players?

Dover Corporation, Gilbarco Veeder-Root, Chart Industries, OPW, and Hexagon Agility form the core group with expanding global footprints.

Page last updated on: