LPG Tanker Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

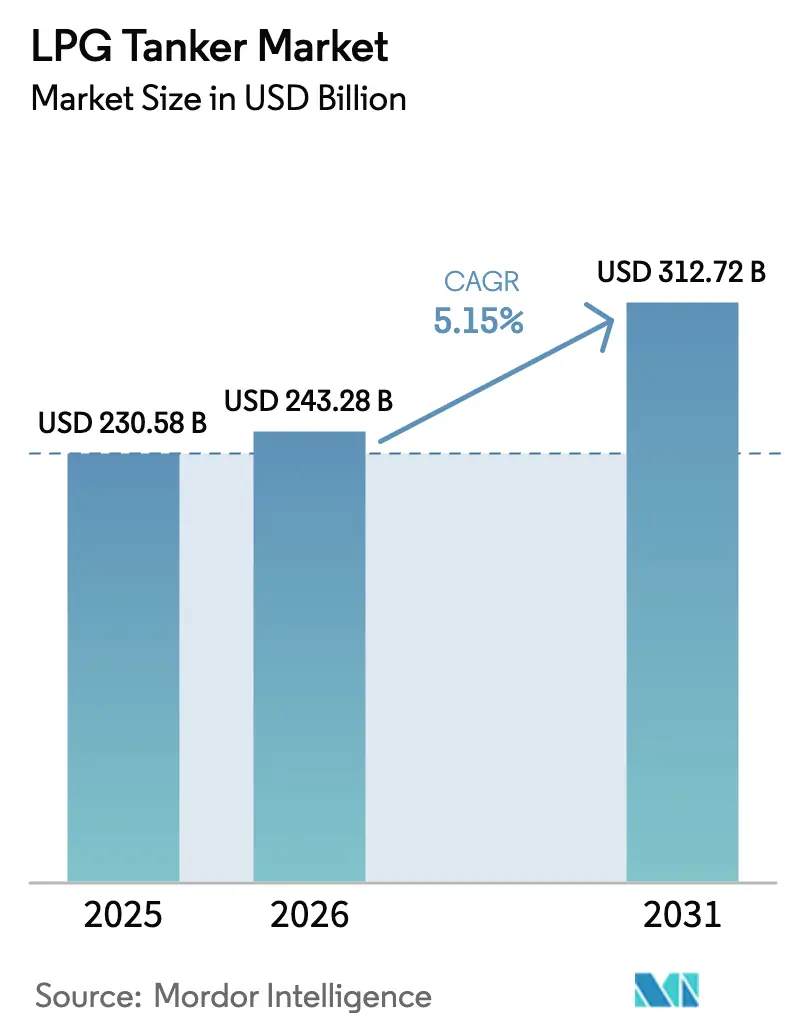

| Market Size (2026) | USD 243.28 Billion |

| Market Size (2031) | USD 312.72 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

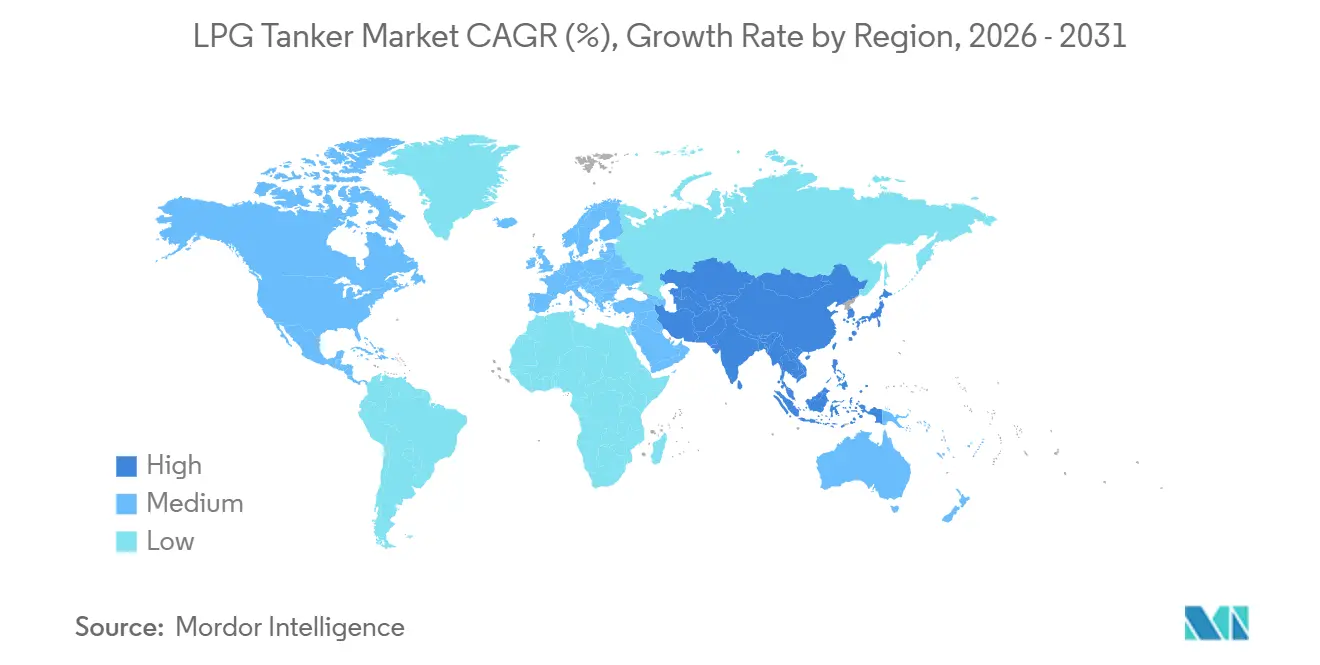

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LPG Tanker Market Analysis by Mordor Intelligence

The LPG Tanker Market size is projected to expand from USD 230.58 billion in 2025 and USD 243.28 billion in 2026 to USD 312.72 billion by 2031, registering a CAGR of 5.15% between 2026 to 2031.

Healthy arbitrage economics on United States–to–Asia flows, steady fleet renewal prompted by the International Maritime Organization’s (IMO) Carbon Intensity Indicator (CII) rules, and propane‐dehydrogenation (PDH) capacity additions across China and the Middle East underpin this expansion. VLGC charter earnings remain resilient because every incremental US Gulf cargo adds a 40-day round voyage, tightening effective vessel supply even as newbuild deliveries accelerate. Meanwhile, Asia-Pacific’s switch from biomass and coal to LPG for household cooking, together with PDH capacity that locks in long-term propane demand, raises utilization across medium and small gas carriers that service coastal distribution. Lastly, the dual-fuel retrofit wave, driven by shipowners seeking compliance with FuelEU Maritime and IMO CII benchmarks, cements LPG’s near-term position as both cargo and fuel.

Key Report Takeaways

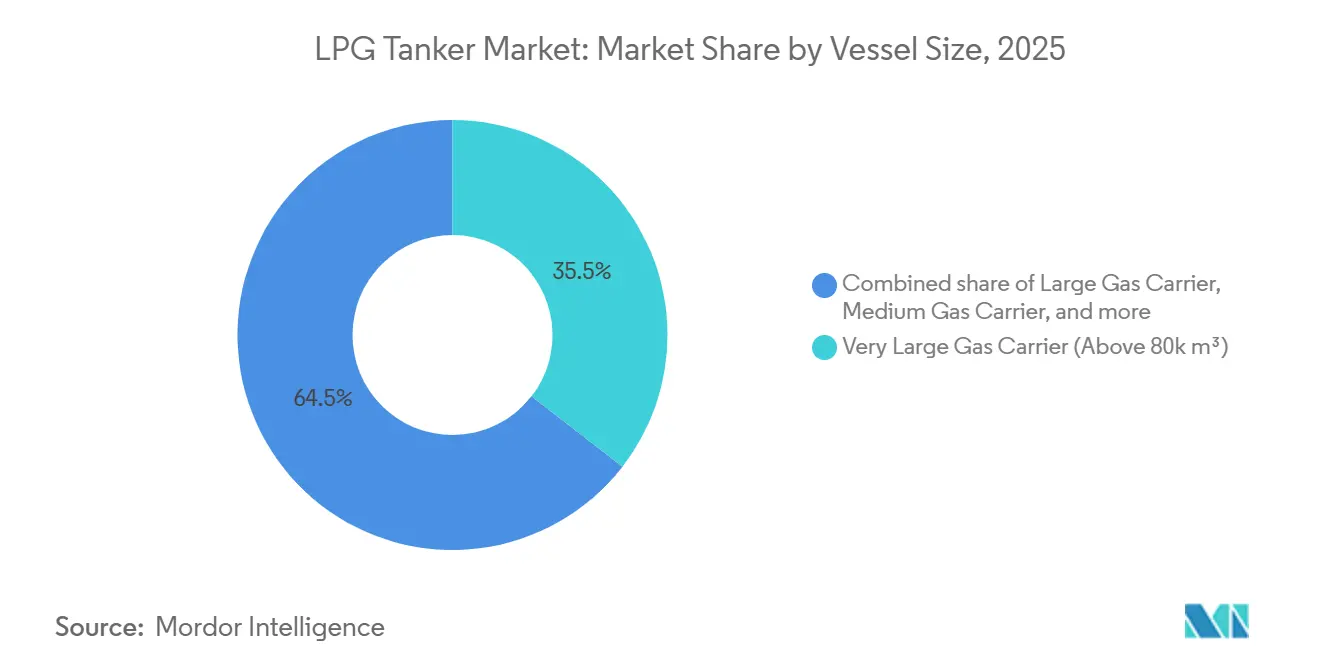

- By vessel size, Very Large Gas Carriers (VLGCs) above 80,000 m³ captured 35.5% of the LPG tanker market share in 2025 and are advancing at a 5.7% CAGR through 2031.

- By cargo containment, fully pressurized systems accounted for 41.8% of the LPG tanker market size in 2025, while ethylene-capable extra-refrigerated designs posted the fastest 6.9% CAGR to 2031.

- By geography, Asia-Pacific held 38.1% of the LPG tanker market share in 2025, and regional revenue is expanding at a 6.0% CAGR on surging Chinese PDH feedstock imports and Indian clean-cooking adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LPG Tanker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shale-gas export volumes from the United States | +0.8% | Global, with primary flows to Asia-Pacific | Medium term (2-4 years) |

| Rising LPG demand for domestic heating & cooking in emerging Asia | +1.2% | Asia-Pacific core, spill-over to South Asia | Long term (≥ 4 years) |

| Expansion of downstream propane-dehydrogenation & petrochemical capacity | +0.9% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| IMO CII rules accelerating replacement with fuel-efficient VLGCs | +0.7% | Global | Short term (≤ 2 years) |

| Adoption of LPG as a low-carbon marine bunker fuel | +0.4% | Global, early adoption in Europe & Asia | Long term (≥ 4 years) |

| Larger Neopanamax transit slots on the Panama Canal lowering tonne-mile costs | +0.3% | Global, US Gulf to Asia-Pacific routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Shale-Gas Export Volumes from the United States

Surging U.S. shale output has positioned the country as the swing supplier for the LPG tanker market, displacing Middle Eastern cargoes on Pacific trades. Enterprise Products Partners expanded Mont Belvieu terminal capacity by 300,000 barrels per day in 2024, binding long-term volumes to Chinese and Indian buyers.[1]Enterprise Products Partners, “Operations and Facilities,” enterpriseproducts.com Each additional Gulf cargo travels roughly 13,000 nautical miles to Northeast Asia, versus 6,500 nautical miles from the Arabian Gulf, effectively tightening the VLGC pool for 40 days per round voyage. The U.S. Energy Information Administration projects outbound LPG to keep climbing while Henry Hub gas prices stay under USD 3 per MMBtu, sustaining healthy arbitrage windows.[2]International Energy Agency, “Gas Market Report 2024,” iea.org Although federal permitting delays could defer Gulf Coast greenfield terminals, prevailing bilateral offtake agreements protect baseline flows. As a result, tonne-mile demand stays buoyant, enabling shipowners to lock in premium period charters and reinforcing confidence in the LPG tanker market’s mid-term trajectory.

Rising LPG Demand for Domestic Heating & Cooking in Emerging Asia

Urbanization drives millions of households in China, India, and ASEAN states to swap biomass and coal for LPG stoves, a transition championed by subsidy programs and air-quality mandates that favor the LPG tanker market.[3]International Energy Agency, “Gas Market Report 2024,” iea.org This household shift is relatively price inelastic, protecting volume growth even when crude benchmarks swing. China augmented import requirements after commissioning 15 million tonnes of PDH and steam-cracker capacity in 2024, lifting its annual LPG seaborne demand forecast to 36 million tonnes.[4]Argus Media, “VLSFO Price Assessment,” argusmedia.com Intercontinental lifts absorb VLGCs, whereas subsequent coastal redistribution relies on medium gas carriers, spreading utilization benefits across fleet classes. The emerging Asia demand pool also dampens exposure to Middle East geopolitical interruptions because diversification toward U.S. Gulf and Canadian cargos broadens supply options. Collectively, these consumer-side fundamentals anchor a sizeable portion of future LPG tanker market growth.

Expansion of Downstream PDH & Petrochemical Capacity

Integrated petrochemical groups in China, Saudi Arabia, and Iran are rolling out PDH projects that secure captive propylene feedstock and long-horizon LPG offtake contracts. APOC’s 843,000 tpy propylene plant, slated for a 2026 start-up, will alone need roughly 1.6 million tonnes per year of imported propane. Ethane-derived ethylene economics have narrowed, pushing firms toward direct propane cracking, which structurally elongates LPG supply chains and benefits the LPG tanker market. While Chinese PDH margins compressed to a 76% utilization average in 2024, the cumulative wave of units entering service tilts overall regional feedstock balances toward imported propane. Resulting long-haul voyages support VLGC employment, justify newbuild commitments, and encourage owners to favor ethylene-capable cargo tanks that toggle between propane and derivative gases. Consequently, PDH expansion contributes a reliable uplift to fleet demand for most of the forecast horizon.

IMO CII Rules Accelerating Replacement with Fuel-Efficient VLGCs

The IMO’s CII grading, encoded under MEPC.346(78) and amended by MEPC.388(81), publicly ranks vessels by gram-per-ton-mile emissions and compels corrective plans for underperformers. More than 25% of the active VLGC cohort was built before 2010 and struggles to meet reference lines without costly retrofits. Solvang ordered two fuel-efficient VLGCs from HD Hyundai Heavy Industries for USD 230 million, a direct response to impending step-down limits that accelerate scrapping. BW LPG already operates 22 dual-fuel VLGCs that burn cargo boil-off, improving EEXI baselines and demonstrating commercial proof of concept. Because newbuild slots are booked into 2028 at major Korean and Chinese yards, any wave of unscheduled scrapping could create temporary tightness, elevating spot earnings. Thus, regulatory pressure, although intended to curb emissions, paradoxically lifts near-term revenue prospects in the LPG tanker market.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile bunker-fuel & crude-oil prices | -0.6% | Global | Short term (≤ 2 years) |

| Geopolitical chokepoint disruptions (Hormuz, Red Sea, etc.) | -0.5% | Middle East, Red Sea, Strait of Hormuz | Short term (≤ 2 years) |

| Competition from carbon-neutral gases (ammonia, methanol) in future fuel mix | -0.3% | Global, early adoption in Europe | Long term (≥ 4 years) |

| Environmental-permitting delays for new US Gulf export terminals | -0.2% | North America, with downstream impact on Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Bunker-Fuel & Crude-Oil Prices

Bunker expenses absorbed 30-40% of voyage outlays in 2024 when VLSFO ranged USD 500–700 per tonne, yoking earnings for LPG tanker market participants to crude price swings. Non-dual-fuel vessels remain exposed because they cannot pivot to cheaper cargo boil-off gas during spikes. Brent oscillated between USD 70 and 90 per barrel through 2025, widening volatility bands for freight breakevens. Owners shelter earnings by inserting bunker-adjustment clauses and locking multiyear charters, but such hedges thin spot liquidity, limiting market discovery. Higher fuel costs also compress PDH cracker margins, occasionally trimming propane imports and cargo movements. Even so, resilience in household LPG demand shelters baseline flows, tempering the overall drag on the LPG tanker market.

Geopolitical Chokepoint Disruptions (Hormuz, Red Sea)

Drone and missile attacks around Bab el-Mandeb forced diversions around the Cape of Good Hope in late 2024, stretching voyages by up to 14 days and lifting war-risk premiums 50–100 basis points. Although longer distances raise tonne-miles, insurance and fuel overheads pare net voyage returns. The Strait of Hormuz remains exposed to Iranian naval drills, jeopardizing roughly 20% of global LPG liftings. Charterers mitigate exposure by sourcing more volumes from the U.S. Gulf and West Coast Canada, but those cargoes strain VLGC availability on Pacific legs. Persistent chokepoint threats thus inject operational uncertainty and modestly restrain CAGR gains for the LPG tanker market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vessel Size: Economies of Scale Cement VLGC Leadership

VLGCs larger than 80,000 m³ captured 35.5% of the LPG tanker market share in 2025 and will grow 5.7% annually through 2031, reflecting unrivaled per-ton transport economics on intercontinental routes. Modern VLGC designs now load 91,000–93,000 m³ within Neopanamax beam limits, enabling Panama Canal transits that shave 12–15 days off US-to-Asia voyages and lower fuel burn 15–20%. Consolidators such as BW LPG, following its USD 1.05 billion purchase of 12 Avance Gas VLGCs, leverage fleet scale to bargain down dockyard slots and bunker prices, reinforcing dominance. In contrast, Large Gas Carriers (LGCs) of 60,000–80,000 m³ serve Mediterranean and Southeast Asian ports where draft constraints rule out VLGCs, while Medium Gas Carriers (MGCs) between 20,000–60,000 m³ handle intra-regional trades and coastal redistribution. Niche Small & Pressurized tankers below 20,000 m³, although structurally versatile for island chains, contend with rising crew costs and stricter IMO efficiency curves that erode rate premiums. Altogether, scale efficiencies, slot access, and fuel-saving retrofits anchor VLGCs at the heart of the LPG tanker market.

Second-generation VLGCs increasingly feature dual-fuel main engines and shaft generators that repurpose cargo boil-off as propulsion fuel, a technology that saves roughly 15 metric tonnes of VLSFO per day on a Houston–Ningbo round trip. Retrofitting older VLGCs costs USD 7–9 million per hull but extends CII compliance windows and lifts time-charter premiums by USD 4,000–5,000 per day. Parallel interest in very large ethane/ethylene carriers (VLECs) underscores hull commonality; Jiangnan Shipyard’s USD 1.9 billion contract for 9 VLECs and 4 very large ammonia carriers for ADNOC L&S and Wanhua Chemical reflects growing appetite for dual-service designs. The cross-pollination of containment technology boosts resale values because vessels can switch between propane, butane, ethane, or ethylene cargoes as arbitrages evolve. Consequently, owners view VLGCs and VLECs as complementary tonnage pools that collectively reinforce the medium-term momentum of the LPG tanker market.

By Cargo Containment System: Ethylene Capability Redefines Flexibility

Fully pressurized hulls held 41.8% of the LPG tanker market size in 2025, mainly supplying short-sea and river trades where low capital cost outweighs refrigeration efficiency. Yet, fleet renewal leans toward fully refrigerated and extra-refrigerated solutions that maximize cargo density on long hauls. Semi-pressurized/-refrigerated MGCs remain the workhorse of Mediterranean and intra-Asian cabotage because they balance CAPEX against mixed cargo flexibility. The fastest-growing design class is ethylene-capable extra-refrigerated tonnage, poised for a 6.9% CAGR to 2031 as petrochemical importers value ships that load ethylene one way and propane the next without prolonged tank warm-up cycles.

ADNOC L&S and Wanhua’s 13-ship order illustrates this convergence between petrochemical gases; each vessel can swap between -104 °C ethylene and -42 °C LPG cargoes without hardware changes, improving utilization across demand cycles. Zhejiang Satellite Petrochemical similarly chartered eight ultra-large ethane carriers that default to LPG sooner than ballasting, further enlarging optionality. Onboard reliquefaction units lower daily boil-off to under 0.07% of cargo, helping owners capture incremental tonnes in a congested VLGC spot market. Although extra-refrigeration installs add roughly USD 6 million to yard invoices, faster payback arises from higher multipurpose charter rates. Technological spill-overs from LNG membrane containment systems accelerate insulation advances, narrowing opex differentials versus legacy designs. For these reasons, ethylene-ready tonnage is now the blueprint for new orders, sharpening the competitive edge of integrated fleets in the LPG tanker market.

Geography Analysis

Asia-Pacific dominated revenue with 38.1% of the LPG tanker market size in 2025, growing at a 6.0% CAGR as PDH start-ups and household adoption broaden import appetite. China’s midstream build-out added 6 dedicated LPG terminals over 2024–2025, supporting larger parcel sizes that prefer VLGC or VLEC lifts. India extended subsidized cylinder coverage to 90 million low-income households by 2025, cementing LPG as the preferred urban cooking fuel. ASEAN economies, notably Indonesia and Vietnam, expand small cylinder distribution, anchoring demand for MGCs and pressurized carriers serving shallow-draft ports. Japan and South Korea maintain mature baseline requirements, but their re-export hubs redistribute partial cargoes to Pacific islands, sustaining short-haul fixtures.

North America sits at the supply center of the LPG tanker market, accounting for more than 50% of net long-haul exports in 2025. Enterprise Products’ Mont Belvieu expansion and Targa Resources’ capacity lift, both completed in 2024, promise an additional 400,000 bpd of propane-plus output, mainly destined for Asia. Canada’s Ridley Island Propane Export Terminal logs steady coastal tanker rotations to Japan, leveraging shorter Pacific routes. Mexico remains a net importer served by pressurized coastal tankers operating from U.S. Gulf loadings.

Europe’s demand has tilted toward imports from the U.S. Gulf and Algeria after sanctions squeezed Russian Baltic and Black Sea flows. Germany, France, and the United Kingdom absorb combined seasonal peaks exceeding 1.7 million tonnes per quarter, driving fringe demand for handy-sized pressurized carriers. South America displays patchy flows; Brazil’s dry-season cylinder sales spur medium carrier charters, while Chile functions as a bunkering and redistribution node.

Middle East and Africa present a dualistic pattern. Saudi Arabia and the United Arab Emirates ship propane to Asia, exercising term charters that anchor regional tonne-miles. In contrast, South Africa, Kenya, and West African nations import cylinders via pressurized carriers, supported by port upgrades in Lagos and Mombasa. Nigeria’s NLNG Bonny expansion promises incremental LPG export barrels in 2026, yet civil unrest risks could intermittently disrupt loadings. Overall, geographic diversification cushions the LPG tanker market against localized shocks, sustaining a balanced global employment landscape.

Competitive Landscape

The LPG tanker market is moderately concentrated: the top five owners command roughly 40% of VLGC capacity, while the balance of the 1,600-plus-ship fleet is dispersed among regional specialists and single-tonnage operators. BW LPG’s 2024 purchase of 12 Avance Gas VLGCs, bringing its fleet to 53 units, underscores consolidation that yields scale in bunker procurement and maintenance contracting. Dorian LPG and Petredec Holdings expand fleets through staggered newbuilds and selective retrofits, each holding 8–10% shares in the large-carrier segment. Smaller owners defend margins by focusing on niche trades such as Mediterranean small-pressurized shuttle routes or intra-Chinese coastal liftings.

Shipyard competition is led by South Korea’s Samsung Heavy Industries, HD Hyundai Heavy Industries, and Hanwha Ocean, which together control almost 60% of the VLGC orderbook thanks to membrane containment patents and dual-fuel engine packages. Chinese builders, Jiangnan Shipyard, Yangzijiang, and Hudong-Zhonghua, secure price-sensitive contracts for MGCs and VLECs, often bundling financing support from state banks to shorten delivery lead times. HD Hyundai Heavy Industries’ January 2024 order for two VLGCs at USD 235 million and Samsung Heavy’s USD 3.45 billion LNG deal illustrate the yards’ cross-segment scale.

Technology race lines blur across fuel types: MAN Energy Solutions and WinGD unveil ammonia-ready and methanol-ready main engines, prompting speculation about future fuel mix displacement. Nevertheless, LPG’s existing bunkering footprint at Houston, Singapore, and Rotterdam harbors gives it a first-mover cost edge. Digitalization shapes cost structures as well; predictive maintenance reduces off-hire days by 15-20%, while voyage-optimization software cuts fuel burn by 3–4%. Collectively, these strategies yield incremental savings that owners reinvest in dual-fuel conversions, reinforcing competitive durability and supporting lasting value creation in the LPG tanker market.

LPG Tanker Industry Leaders

Samsung Heavy Industries Co. Ltd.

Mitsubishi Heavy Industries Ltd.

HD Hyundai Heavy Industries Co. Ltd.

Hanwha Ocean Co. Ltd.

Mitsui OSK Lines Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Hafnia, a global product tanker owner, is pursuing a merger with TORM, focusing on product tanker consolidation. While not directly targeting LPG carriers, the merger could impact broader tanker markets, including LPG transport, as operational synergies and fleet integration develop.

- June 2025: Al Seer Marine and B International Shipping & Logistics established ASBI Shipping FZCO to manage mid-size LPG and product tankers. The venture acquired two 22,000 cbm semi-refrigerated LPG vessels under a 10-year charter with BGN INT DMCC, enhancing regional LPG logistics and improving market accessibility.

- February 2025: Transpetro issued tenders to increase its LPG fleet from six to 14 vessels, including five pressurized LPG tankers (7,000 m³ and 14,000 m³) and three semi-refrigerated LPG/ammonia carriers. This expansion aims to boost capacity and modernize fleet efficiency for LPG transport in Brazil.

- February 2025: NYK established NYK Energy Ocean (NEO) after acquiring 80% of ENEOS Ocean’s shipping business. The new subsidiary operates 47 vessels, including 18 LPG carriers, positioning NYK as one of the largest LPG carrier operators globally and enhancing its LPG shipping capabilities.

Global LPG Tanker Market Report Scope

A liquified Petroleum Gas (LPG) tanker is a gas transporter that carries massive volumes of petroleum gases and is made up of separate reservoirs stacked in cargo holds. Small pressurized tanks, shielded or refrigerated seagoing tanks, and semi-pressurized tanks are the commonly used LPG tankers.

The LPG tanker market is segmented by vessel size, cargo containment system, and geography (North America, Europe, Asia Pacific, South America, and the Middle East and Africa). By vessel size, the market is segmented into very large gas carriers (above 80k m³), large gas carriers (60 to 80k m³), medium gas carriers (20 to 60k m³), and small and pressurized (up to 20k m³). By cargo containment system, the market is segmented into fully refrigerated, semi-pressurized/semi-refrigerated, fully pressurized, and ethylene-capable (extra-refrigerated). The report also covers the market size and forecasts for the LPG tanker market across major regions, such as Asia-Pacific, North America, Europe, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Very Large Gas Carrier (Above 80k m³) |

| Large Gas Carrier (60 to 80k m³) |

| Medium Gas Carrier (20 to 60k m³) |

| Small and Pressurized (Up to 20k m³) |

| Fully Refrigerated |

| Semi-pressurized/Semi-refrigerated |

| Fully Pressurized |

| Ethylene-capable (Extra-Refrigerated) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Vessel Size | Very Large Gas Carrier (Above 80k m³) | |

| Large Gas Carrier (60 to 80k m³) | ||

| Medium Gas Carrier (20 to 60k m³) | ||

| Small and Pressurized (Up to 20k m³) | ||

| By Cargo Containment System | Fully Refrigerated | |

| Semi-pressurized/Semi-refrigerated | ||

| Fully Pressurized | ||

| Ethylene-capable (Extra-Refrigerated) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the LPG tanker market in 2031?

Forecasts show the LPG tanker market reaching USD 312.72 billion by 2031 on a 5.15% CAGR.

Which vessel class commands the largest share of global LPG shipping revenue?

VLGCs above 80,000 m³ hold 35.5% of 2025 revenue and continue to dominate long-haul exports.

Why is Asia-Pacific the fastest-growing import region?

Chinese PDH additions, Indian household LPG adoption, and ASEAN infrastructure upgrades push Asia-Pacific revenue at a 6.0% CAGR.

How do IMO CII rules influence fleet renewal?

Stricter carbon-intensity scores force owners to scrap or retrofit older tonnage, accelerating newbuild demand and tightening near-term supply.

Are dual-fuel retrofits commercially viable for existing VLGCs?

Yes, conversions that let engines burn LPG boil-off lower fuel costs and lift charter premiums enough to repay USD 7-9 million retrofit costs within five years.

Page last updated on: