Composites In United States Defense Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

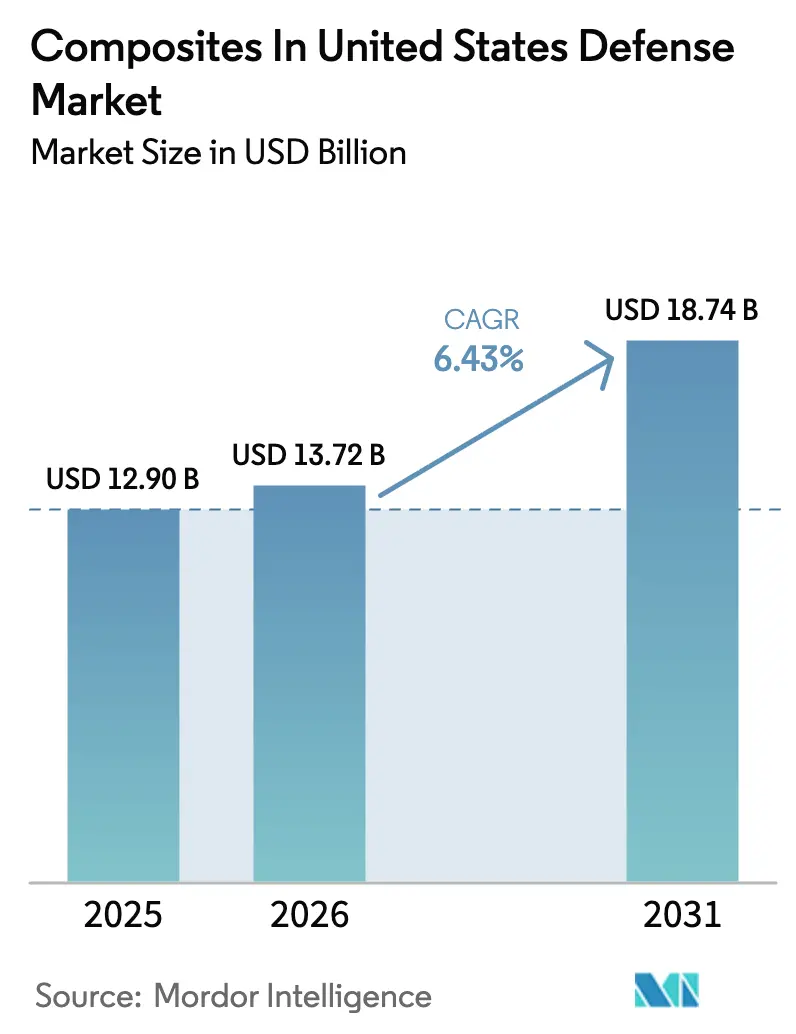

| Base Year Market Size (2025) | USD 12.90 Billion |

| Market Size (2026) | USD 13.72 Billion |

| Market Size (2031) | USD 18.74 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

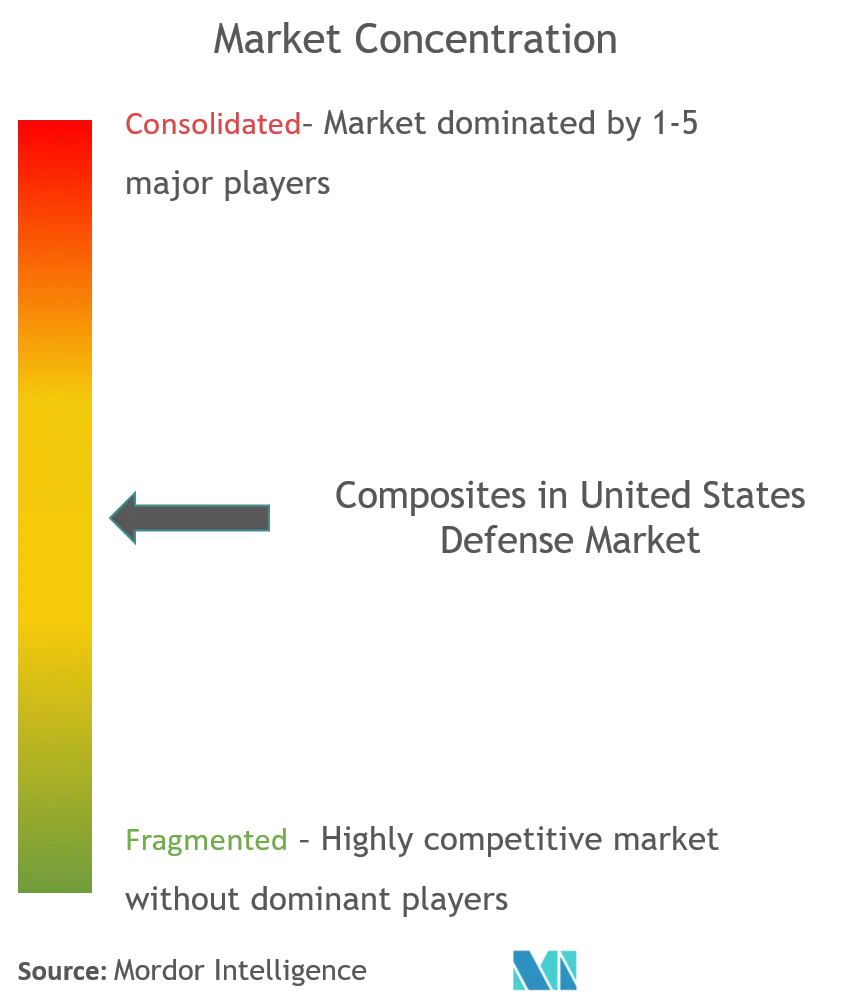

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composites In United States Defense Market Analysis by Mordor Intelligence

The composites in the United States defense market size is expected to grow from USD 12.90 billion in 2025 to USD 13.72 billion in 2026 and is forecast to reach USD 18.73 billion by 2031 at a 6.43% CAGR over 2026-2031. Rapid procurement of lighter, low-observable platforms for multi-domain operations underpins this growth, while vertical integration at major primes keeps supply risk in check. Demand momentum is strongest where composite weight savings extend range, payload, and endurance, especially for unmanned aircraft and next-generation bombers. Platform programs such as DDG(X), Constellation-class frigates, and Joint Light Tactical Vehicles reinforce volume in naval and ground segments, and the Department of Defense’s recyclability mandate accelerates the adoption of thermoplastic matrices for non-structural parts. Cost headwinds from PAN-based fiber inflation persist, but Title III investments and new domestic precursor capacity are expected to temper volatility from 2028 onward.

Key Report Takeaways

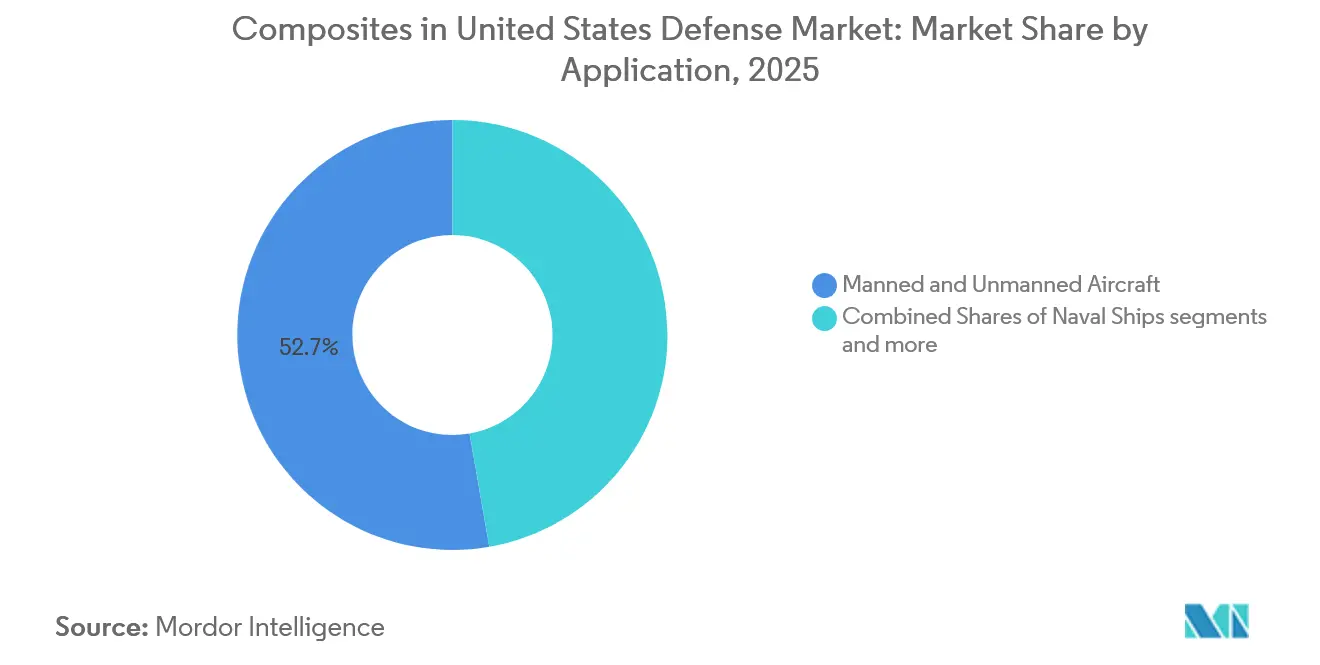

- By application, Manned and Unmanned Aircraft led with 52.74% of the composites in the United States defense market share in 2025; protective equipment is forecast to expand at a 5.48% CAGR through 2031.

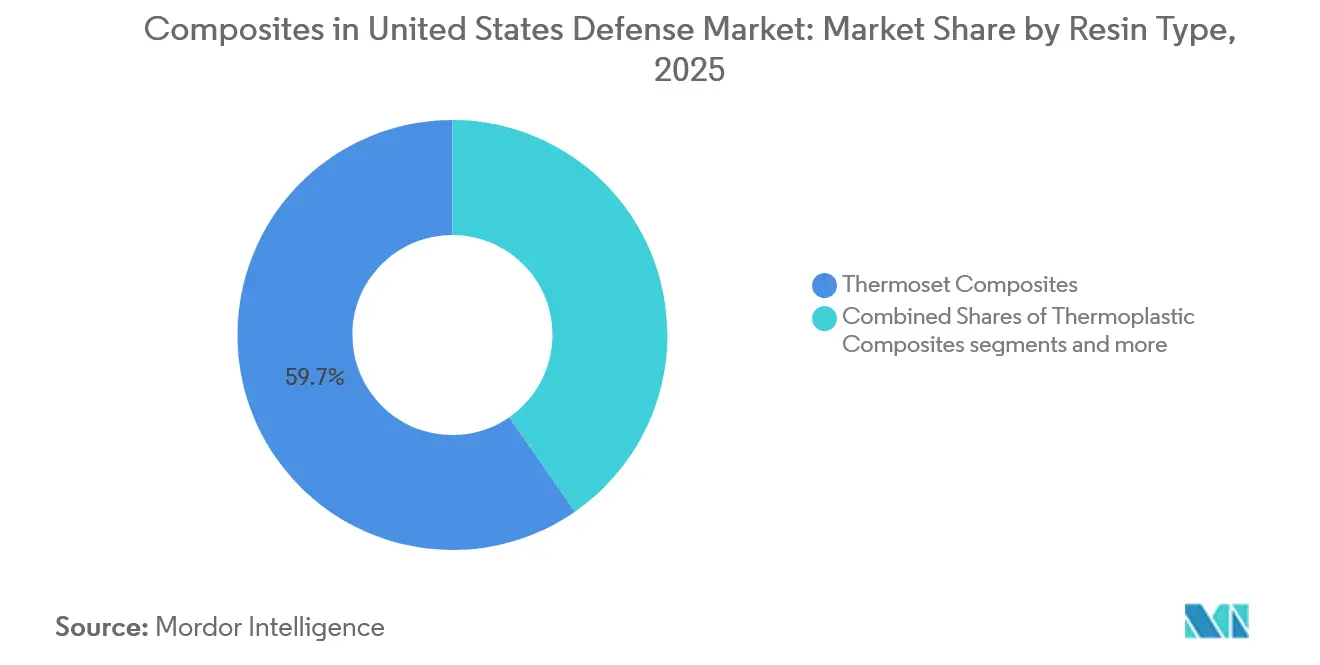

- By resin type, Thermoset Composites commanded 59.65% share of the composites in the United States defense market size in 2025, while thermoplastic composites are projected to advance at a 6.14% CAGR between 2026 and 2031.

- By fiber type, PAN-based fibers accounted for 79.17% share of the composites in the United States defense market size in 2025, and Pitch-based fibers are growing at a 5.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Composites In United States Defense Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight next-generation aircraft demand | 1.80% | California, Texas | Medium term (2–4 years) |

| High-temperature CMCs for hypersonic systems | 1.20% | California, Alabama | Long term (≥ 4 years) |

| Ground-vehicle composite armor upgrades | 1.10% | Michigan, South Carolina | Medium term (2–4 years) |

| Naval signature-reduction programs | 0.90% | Virginia, Mississippi | Long term (≥ 4 years) |

| Additive manufacturing for forward-deployed spares | 0.70% | Florida, Oklahoma | Short term (≤ 2 years) |

| Sustainability mandates for recyclable thermoplastics | 0.60% | Nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lightweight Next-Gen Aircraft Demand

The Air Force aims to field the Next Generation Air Dominance family of systems by 2030, calling for 20%–25% lighter airframes than legacy fighters to exceed a 1,500-nautical-mile unrefueled combat radius.[1]U.S. Air Force, “Next Generation Air Dominance Fact Sheet,” af.mil Lockheed Martin’s 2025 F-47 demonstrator is already 65% composite by weight, using HexTow IM2C fiber in a toughened epoxy that meets strict flammability and durability standards.[2]Hexcel Corporation, “Investor Day 2026,” hexcel.com Collaborative Combat Aircraft prototypes from Boeing and General Atomics adopt out-of-autoclave prepregs to avoid large autoclave infrastructure and enable distributed production. Each B-21 Raider consumes about 180 metric tons of carbon-epoxy prepreg, three times the B-2 baseline, highlighting the scale of raw-material pull. FAA Part 25 Appendix F and MIL-STD-3039 govern toxicity and heat-release parameters, pushing suppliers toward higher-toughness resin systems. Unmanned platforms are a key second-tier beneficiary because the Air Force places a 40% higher payload fraction requirement on the MQ-9 Reaper replacement, feasible only through composite structures.

Ground-Vehicle Composite Armor Upgrades

The Armored Multi-Purpose Vehicle uses ceramic-composite appliqué armor to achieve Level III ballistic protection at 68% of the density of rolled homogeneous steel.[3]U.S. Army, “Soldier Lethality CFT,” army.mil Silicon-carbide tiles from CoorsTek are bonded to carbon-fiber backers supplied by Hexcel, distributing impact energy and preventing spall formation.[4]U.S. Navy, “DDG(X) Technical Overview,” navy.mil The Joint Light Tactical Vehicle extends the architecture by installing S-2 glass-fiber blast shields that absorb 15 kilojoules of explosive energy at one-meter standoff. Facing desert, arctic, and littoral exposures, these composites pass MIL-DTL-46593 aging protocols and MIL-STD-662F ballistic standards. Although composite armor costs USD 1,200–1,800 per m² versus USD 400 for steel, a typical 2,000-pound weight reduction saves roughly 12,000 gallons of diesel over a 10,000-hour life, offsetting price premiums at Defense Logistics Agency bulk rates.

Naval Signature-Reduction Programs

The DDG(X) destroyer specifies a composite deckhouse and mast that cuts radar cross-section by 90% in X-band frequencies relative to steel superstructures.[4]U.S. Navy, “DDG(X) Technical Overview,” navy.mil Shipyards at Huntington Ingalls and Bath Iron Works fabricate carbon-fiber sandwich panels co-cured in 40-foot presses to eliminate electromagnetic discontinuities. Constellation-class frigates adopt a composite mast housing the AN/SPY-6(V)3 radar array, saving 18 metric tons topside and freeing weight margin for additional launch cells. MIL-DTL-24768 and NAVSEA shock guidelines require structures to survive 1,000-psi underwater blasts without delamination. The Navy’s 2025 Navigation Plan emphasizes distributed lethality, and composite superstructures directly convert weight savings into magazine depth.

High-Temperature CMCs for Hypersonic Systems

Silicon-carbide fiber-reinforced CMCs sustain 1,400°C–1,650°C during Mach 5+ flight profiles, outperforming carbon–carbon designs that need active cooling. GE Aerospace provides CMC nose caps for the AGM-183A ARRW that remain dimensionally stable within ±0.5 mm under 2,000°C peak heating. The Long Range Hypersonic Weapon and Conventional Prompt Strike share a common glide body with oxidation-resistant CMC control surfaces that cut TPS mass by 40%. Supply is tight. GE’s Huntsville plant turns out 12 metric tons annually, enough for fewer than 100 vehicles, so the Air Force Research Laboratory funded an expansion targeting USD 800/kg by 2030. Design allowables follow MIL-HDBK-17 and ASTM C1793, requiring 50-specimen thermal flexural characterization.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High material acquisition costs | –0.8% | Nationwide | Short term (≤ 2 years) |

| Lengthy MIL-STD qualification cycles | –0.6% | Nationwide | Medium term (2–4 years) |

| PAN-precursor supply chain risk | –0.5% | Nationwide | Short term (≤ 2 years) |

| Limited battlefield repair know-how | –0.3% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Material Acquisition Costs

Aerospace-grade prepreg prices rose 12% year-on-year through Q2 2026, touching USD 85–110/kg as acrylic-monomer shortages squeezed PAN precursor output in Japan and China. Toray declared force majeure in late 2025 after an ethylene-cracker outage deferred 1,200 metric tons of deliveries, pushing spot premiums to 30%. High-volume programs such as the F-35 shielded themselves via multi-year contracts locked at 2024 levels, but low-rate builds like the B-21 face 18%–22% higher material bills. Title III funding of USD 45 million for domestic PAN precursor will cover just 15% of the 2028 defense demand, leaving continued exposure to imports. Smaller fabricators endure 90-day payment terms while holding 120-day inventory, deepening working-capital gaps.

Lengthy MIL-STD Qualification Cycles

A single structural prepreg variant can take 24–36 months and USD 2–5 million to clear full MIL-STD-3039 testing, including 15 thermal and environmental conditions. Solvay’s Cycom 5320-1 epoxy took 30 months to qualify for the CH-53K, delaying retrofit weight savings by two fiscal years. Each qualified material requires its own specification control drawing and source approval, administrative loads that boutique suppliers struggle to bear. HexPly 8552, cleared in 2008, still dominates 14 active programs because program managers avoid re-qualification risk. A 2025 standardization push aims to harmonize MIL-STD-3039 with ASTM D8521, but savings will not materialize before 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Manned and Unmanned Aircraft accounted for 52.74% of the composites in the United States defense market share in 2025, with the highest absolute spending across segments. The composites market in the United States defense market for air platforms is growing in line with the Collaborative Combat Aircraft program, where 70% composite primary structure keeps unit flyaway cost near USD 20–25 million, half that of a manned fighter. Protective Equipment demonstrates the fastest expansion, advancing at a 5.48% CAGR as the Soldier Lethality Cross-Functional Team fields 200,000 Enhanced Small Arms Protective Inserts by 2027, each employing boron-carbide and UHMWPE laminates that reduce areal density by 40% compared with legacy armor.

Naval Ships and Land Vehicles both chart mid-single-digit CAGRs as DDG(X) and AMPV procurements replace aging fleets, stabilizing composite demand through 2031. Other Applications, spanning missile radomes and satellite structures, rise at a 4.8% CAGR, buoyed by hypersonic programs such as AIM-260, which deploy quartz-fiber radomes that maintain 95% RF transparency through Mach 4 heating. Enhanced armor for the Joint Light Tactical Vehicle provides Level III protection at 68% of steel’s areal density, reinforcing the volume of vehicular composites. The Marine Corps Plate Carrier III specifies thermoplastic-backed ceramics for field-repair capability via heat-press consolidation, an option not available with thermosets.

By Resin Type: Thermoplastics Gain Despite Cost Premium

Thermoset systems accounted for 59.65% of revenue in 2025 because qualified epoxies such as HexPly 8552 and Cycom 5320-1 remain entrenched on legacy airframes. Yet the composites in the United States defense market expect thermoplastic composites to clock a 6.14% CAGR, underpinned by a recyclability mandate that requires 25% thermoplastic content in non-structural parts after 2028. Solvay APC-2 PEEK and Toray Cetex PPS systems melt for re-extrusion, allowing mechanical recycling and saving USD 8 million in disposal costs on the T-7A program.

Ceramic Matrix Composites rise 5.9% annually, powered by hypersonic weapons that need 1,600°C capability. GE Aerospace’s silicon-carbide CMCs suit ARRW and HACM vehicles, trimming TPS mass 40% compared with carbon–carbon. Thermosets retain dominance in load-bearing wings and longerons thanks to superior out-time and a lower USD 70/kg price tag, compared with USD 85/kg for PEEK. Thermoplastic cycle time, however, is attractive; PPS empennage skins on the T-7A consolidate in 12 minutes, halving touch labor over epoxy autoclaves. CMC availability remains the bottleneck, with only 12 metric tons produced domestically per year.

By Fiber Type: PAN Dominance Persists Amid Pitch-Based Gains

PAN-based fibers accounted for 79.17% of the 2025 demand because intermediate-modulus grades such as IM2C deliver a modulus of 290–310 GPa at USD 55–70/kg, balancing strength, stiffness, and cost. The composites in the United States defense market size linked to PAN fibers grow in lockstep with tactical aircraft and naval mast builds. Pitch-based fibers expand at a 5.71% CAGR to serve hypersonic thermal-management skins, where Mitsubishi’s K13D2U conducts 900 W/m-K heat triple PAN grades and cools electronics on glide bodies.

PAN supply risk lingers due to Japanese concentration; domestic precursor funded under Title III meets only 15% of 2028 demand. Pitch fiber remains 3× as expensive at USD 180–220/kg, limiting penetration to high-heat or radar-absorbing niches. ITAR caps exports of fibers over 500 GPa, complicating allied coproduction on programs such as F-35.

Geography Analysis

The entire composites in the United States defense market activity resides within the United States, but manufacturing clusters exert a distinct influence. California and Texas host high-volume airframe fabrication: Northrop Grumman’s Palmdale plant produces B-21 fuselage barrels with automated fiber placement, while Spirit AeroSystems in Wichita supplies F-35 forward sections, together consuming 4,500 metric tons of prepreg yearly. The Southeast adds final-assembly heft; Boeing’s Charleston campus molds composite fuselages, and Fleet Readiness Center Southeast in Jacksonville repairs helicopter blades.

Michigan and Ohio center ground-vehicle armor integration. BAE Systems installs ceramic-composite tiles at York, Pennsylvania, using silicon carbide sourced from Colorado and carbon-fiber backing from Alabama. Virginia and Connecticut concentrate naval structures; Huntington Ingalls and Electric Boat co-locate near NAVSEA Carderock for hydrodynamic qualification on Columbia-class composite planes.

The market grew 5.8% annually from 2020-2025 despite pandemic disruptions. Catch-up demand raises the 2026-2031 CAGR to 6.43% as F-35 output climbs to 156 jets per year by 2027. Divergent state policy underpins regional competitiveness: California funds a USD 25 million apprenticeship scheme for composite technicians, while Texas grants USD 18 million property-tax abatements to Lockheed Martin’s Fort Worth wing line. The Defense Logistics Agency lists 14 single-source composite suppliers concentrated in three states, indicating vulnerability to localized shocks.

Competitive Landscape

Top suppliers Hexcel Corporation, Solvay Group, Toray Group, Huntsman International LLC, and Honeywell International Inc. captured a majority of 2025 revenue, leaving the remaining share to more than 100 specialized fabricators. Qualification barriers, running 24–36 months, and USD 2–5 million per prepreg system, slow market entry. Hexcel exploits vertical integration by channeling IM2C fiber into its own HexPly lines, while Northrop Grumman manufactures B-21 fuselage sections in-house to compress schedule. Toray spent USD 180 million to expand Alabama precursor output by 30% in 2026, reinforcing domestic resilience. Solvay purchased Composite Technology Development for USD 95 million in 2025, adding automated tape-laying expertise and a Spirit AeroSystems relationship.

White-space revolves around additive manufacturing and deployable repair. The Rapid Sustainment Office field-printed UAV ribs in 2025, cutting lead time by 97%, and creating pull for portable large-format printers. Swiss startup 9T Labs raised USD 17 million in 2024 to commercialize additive-compression hybrid molding that achieves autoclave quality at one-third cycle time. Patent filings rose sharply in 2024-2025: Hexcel logged 14 out-of-autoclave prepreg filings, and Northrop Grumman patented composite-to-metal bonding that removes 40% of fasteners on the B-21 airframe. Suppliers must also meet NIST SP 800-171 cybersecurity clauses under the Defense Federal Acquisition Regulation Supplement.

Composites In United States Defense Industry Leaders

Hexcel Corporation

Solvay Group

Toray Group

Huntsman International LLC

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: At the Paris Air Show, Kongsberg Defence & Aerospace and HEXCEL Corporation signed a five-year partnership agreement. Under this collaboration, HEXCEL will supply HexWeb engineered honeycombs and HexPly prepregs to support KONGSBERG's strategic production programs.

- December 2024: Hexcel Corporation partnered with Boeing to incorporate the Flex-Core HRH-302 honeycomb core into the MQ-25 Stingray, enhancing the use of composite materials in aerospace and defense applications.

- January 2024: DuPont entered into a strategic partnership with Point-Blank Enterprises (PBE) to provide body armor made with Kevlar EXO aramid fiber. This partnership ensures that state and local law enforcement agencies across North America have access to advanced protective equipment featuring the latest aramid fiber technology.

Composites In United States Defense Market Report Scope

A composite material is a material formed by combining two or more materials with different physical and chemical properties. The study includes all types of composites used in military applications in the United States. The market is segmented based on application into manned and unmanned aircraft, naval ships, land vehicles, protective equipment, and other applications. Both fixed-wing aircraft and rotorcraft are included under the manned and unmanned aircraft segment. The market is also segmented by resin type into thermoset, thermoplastic, and ceramic matrix composites, and by fiber type into PAN-based and Pitch-based. The market sizing and forecasts have been provided in value (USD).

| Manned and Unmanned Aircraft |

| Naval Ships |

| Land Vehicles |

| Protective Equipment |

| Other Applications |

| Thermoset Composites |

| Thermoplastic Composites |

| Ceramic Matrix Composites |

| PAN-based |

| Pitch-based |

| By Application | Manned and Unmanned Aircraft |

| Naval Ships | |

| Land Vehicles | |

| Protective Equipment | |

| Other Applications | |

| By Resin Type | Thermoset Composites |

| Thermoplastic Composites | |

| Ceramic Matrix Composites | |

| By Fiber Type | PAN-based |

| Pitch-based |

Key Questions Answered in the Report

What is the current value of the composites in United States defense market?

The composites in United States defense market size is USD 13.72 billion in 2026, with a forecast of USD 18.74 billion by 2031.

Which application segment generates the most revenue?

Manned and Unmanned Aircraft hold 52.74% of 2025 revenue, driven by high composite content in the B-21 bomber and Collaborative Combat Aircraft.

Which resin category is growing fastest?

Thermoplastic composites lead growth at a 6.14% CAGR, spurred by mandated recyclability for non-structural parts.

How concentrated is supply among leading vendors?

The top five companies control about 48% of revenue, placing the market in a moderately concentrated position with a score of 6.

What is the main cost headwind facing suppliers?

PAN-based carbon fiber prices climbed 12% year-on-year through Q2 2026 due to feedstock shortages and limited domestic precursor capacity.

How are composite materials recycled in defense applications?

Thermoplastic matrices such as PEEK and PPS can be ground and re-extruded, enabling DoD targets for 40% landfill diversion of composite scrap by 2030.

Page last updated on: