South America Defense Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

| Market Size (2026) | USD 24.41 Billion |

| Market Size (2031) | USD 31.30 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

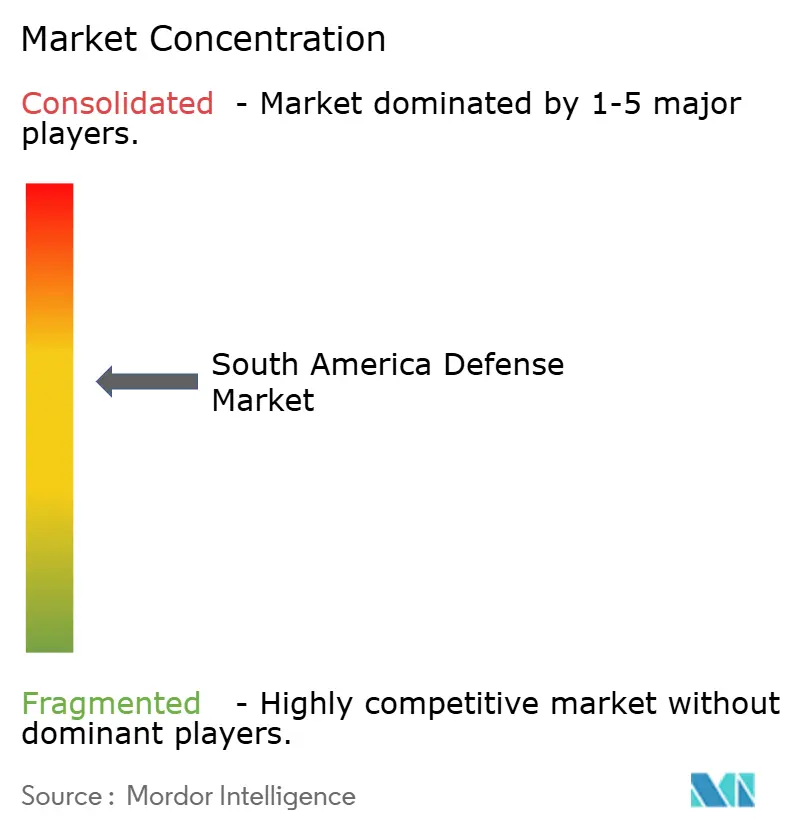

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Defense Market Analysis by Mordor Intelligence

The South America defense market size stood at USD 24.41 billion in 2026 and is projected to reach USD 31.30 billion by 2031, advancing at a 5.10% CAGR. Continuous recapitalization of Cold War-era inventories, resurging territorial disputes such as the Venezuela-Guyana Essequibo clash, and widening border-security missions are influencing procurement priorities across every armed service. Accelerated fighter and ISR aircraft acquisitions in Argentina, Peru, and Brazil underscore the shift toward air-power modernization, while satellites ordered under Brazil’s PESE program signal that space capability is emerging as a new competitive arena. At the same time, commodity-price swings and anti-corruption probes remain structural restraints, often delaying contract execution and adding risk premiums for suppliers.

Key Report Takeaways

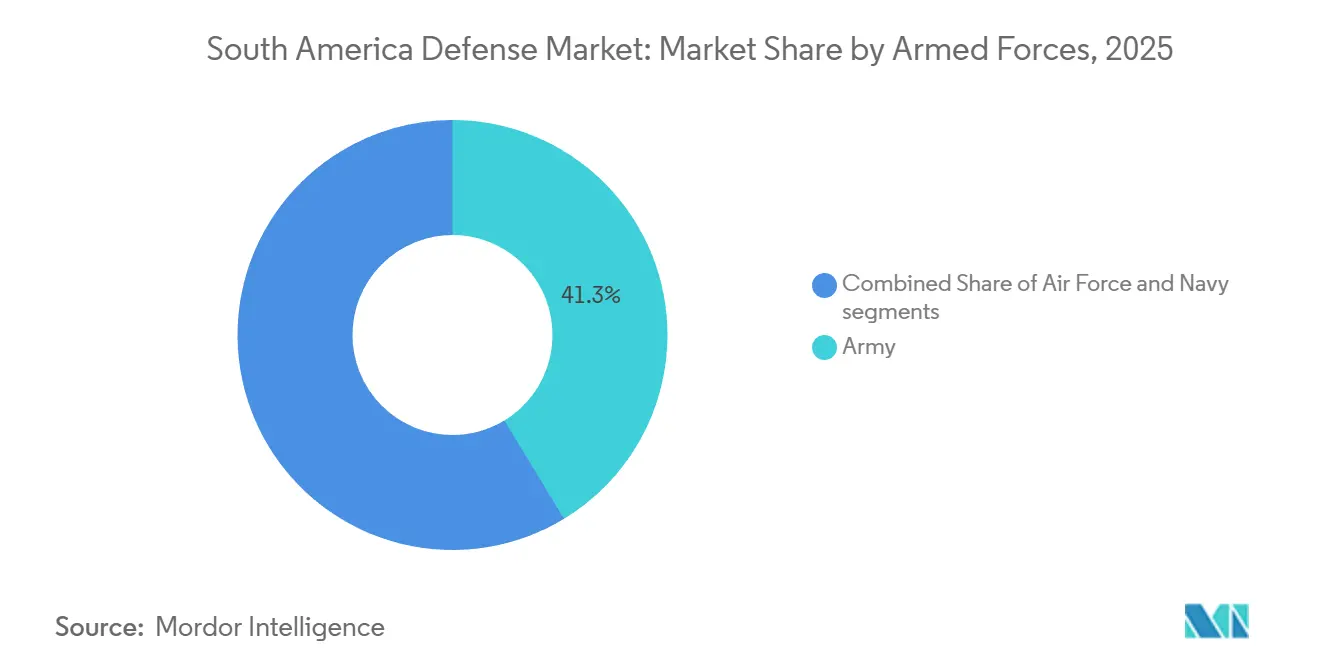

- By armed forces, the Army segment held a 41.32% share of the South America defense market in 2025, while the Air Force segment is forecasted to expand at a 5.34% CAGR through 2031.

- By type, vehicles accounted for 25.01% of the South America defense market size in 2025, but unmanned systems led growth with a 5.45% CAGR to 2031.

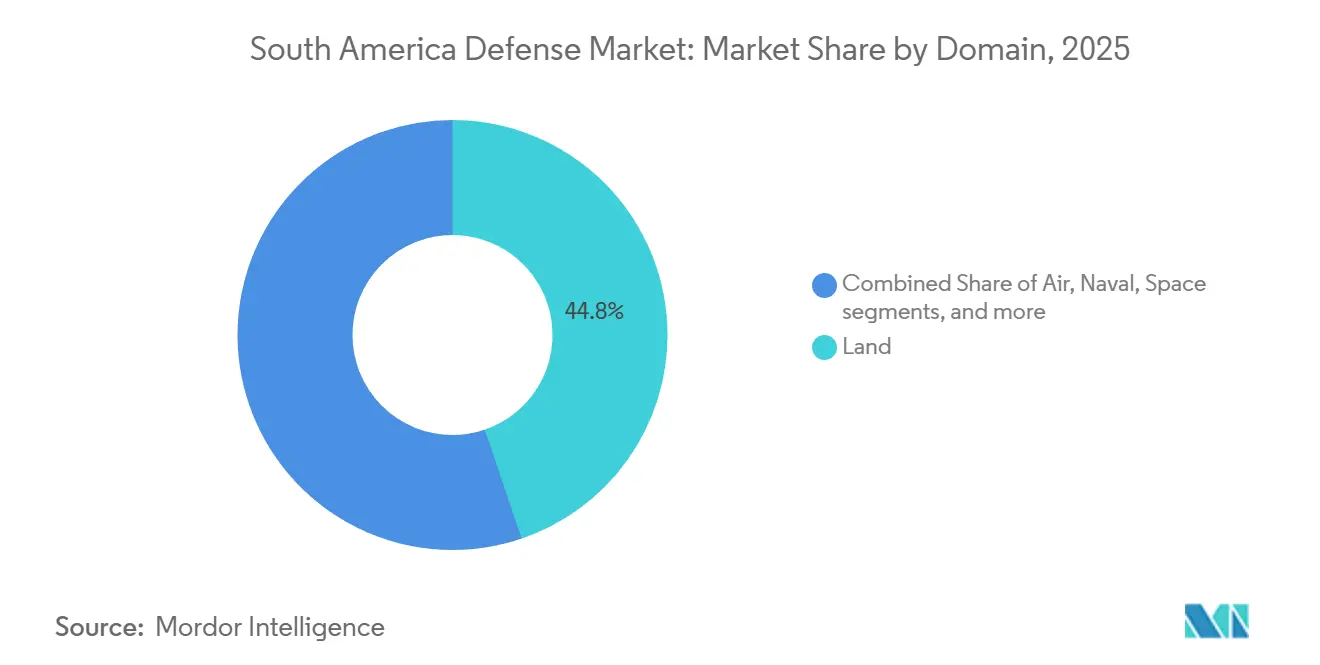

- By domain, land systems commanded a 44.78% share of the South American defense market size in 2025; however, space assets are projected to advance at a 6.24% CAGR through 2031.

- By procurement nature, foreign purchases accounted for 56.78% of 2025 spending, whereas indigenous production is expected to grow at a 6.86% CAGR, driven by stringent offset clauses.

- By geography, Brazil led with 54.23% of 2025 outlays, while Colombia registered the fastest growth at a 6.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated recapitalization of ageing and legacy defense inventories | +1.2% | Brazil, Argentina, Chile, Peru | Medium term (2-4 years) |

| Re-emergence of interstate tensions strengthening territorial defense priorities | +0.9% | Venezuela-Guyana, Peru-Ecuador, Argentina-Chile maritime zones | Short term (≤ 2 years) |

| Expansion of border security and surveillance programs driving UAV and C4ISR procurement | +1.0% | Brazil, Colombia, Peru | Medium term (2-4 years) |

| Force multiplier impact of external military financing and security assistance | +0.7% | Colombia, Peru, Ecuador | Long term (≥ 4 years) |

| Rising defense allocations for protection of strategic natural resource corridors | +0.6% | Brazil, Chile-Argentina, Peru | Long term (≥ 4 years) |

| Early adoption of low-earth-orbit (LEO) satellite programs increasing demand for secure SATCOM | +0.5% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Recapitalization of Ageing Defense Inventories

Most South American platforms entered service during the 1970s and 1980s, leaving readiness gaps that are being addressed through large-scale replacement programs. Argentina accepted its first six F-16 fighters in December 2025, marking the country’s first new combat aircraft delivery in nearly four decades and launching a Lockheed Martin upgrade cycle that will run through 2032. Brazil’s Gripen E/F line at Embraer’s Gavião Peixoto site is delivering locally assembled aircraft, achieving 40-50% domestic content and pointing to deeper industrial participation. Continued retirements of 30-year-old fighters and 25-year-old surface combatants ensure sustained volumes for the South America defense market through the forecast horizon.

Re-Emergence of Interstate Tensions Strengthening Territorial Defense Priorities

The Venezuela-Guyana Essequibo dispute escalated through 2025, prompting Guyana’s defense budget to soar by 78% in 2024 and driving neighboring Brazil and Colombia to reinforce northern garrisons and riverine patrols. Similar unresolved boundaries between Peru and Ecuador, as well as maritime interests of Argentina and Chile, are steering spending away from internal security toward conventional deterrence, notably long-range surveillance radars and strike platforms.

Expansion of Border Security and Surveillance Programs Driving UAV and C4ISR Procurement

Brazil’s USD 2.8 billion SISFRON program extended sensor coverage along 16,886 km of its frontier. At the same time, Colombia’s USD 300 million Atlante II UAV deal will deliver sixteen UAVs between 2027 and 2030 for counter-narcotics surveillance. Complementary C4ISR upgrades, such as Embraer’s BRL 102 million (USD 18.48 million) SABER M200 Vigilante radar order, show a convergence of sensing and engagement systems that support holistic border defense.

Force Multiplier Impact of External Military Financing and Security Assistance

The US Foreign Military Financing of USD 550 million in FY2024 and USD 462.5 million in FY2025 underpins Colombia’s rotary-wing renewal and C4ISR upgrades, thereby amplifying local budgets. Similar financing frameworks for Peru’s pending F-16 Block 70 deal broaden supplier reach and embed interoperability with US assets, elevating overall capability across the South America defense market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Defense spending pressure from commodity price driven fiscal volatility | -0.8% | Peru, Argentina, Venezuela, Chile | Short term (≤ 2 years) |

| Procurement delays linked to governance and anti-corruption investigations | -0.6% | Brazil, Peru, Argentina | Medium term (2-4 years) |

| Limited indigenous defense industrial capacity causing program execution slippages | -0.4% | Regional, acute in Colombia, Peru, Ecuador | Long term (≥ 4 years) |

| Stringent offset and local content requirements increasing total program costs | -0.5% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Defense Spending Pressure from Commodity-Price-Driven Fiscal Volatility

Peru’s heavy copper exposure constrained financing for its USD 3.42 billion F-16 Block 70 package after the USD 64 billion mining pipeline stalled amid price swings, narrowing fiscal space for defense.[1] International Monetary Fund Analysts, “Peru Economic Outlook and Mining Sector Analysis,” imf.org Argentina’s rising inflation similarly delayed fighter procurement until parliamentary approval unlocked USD 941 million in 2024.[2]Bloomberg Editors, “Argentina Inflation and Defense Budget Constraints,” bloomberg.com Oil-dependent Venezuela and copper-reliant Chile face parallel budget uncertainties, which embed volatility into the South American defense market outlook.

Procurement Delays Linked to Governance and Anti-Corruption Investigations

Brazil’s Prosub submarine effort and Saab’s Gripen deal have come under renewed scrutiny, slowing nuclear-submarine milestones and second-batch fighter negotiations. In Peru, “Rolexgate” stalled decisions on F-16 and naval tenders. At the same time, Argentina’s mandatory judicial reviews routinely extend contract cycles by over a year, jointly dampening the South America defense market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armed Forces: Ground Dominance Meets Air-Power Resurgence

The Army accounted for 41.32% of the 2025 regional expenditure, as infantry, armor, and artillery remain pivotal for counter-insurgency and border defense across the South America defense market. Brazil’s Guarani 6×6 program, Colombia’s Pandur II deliveries, and Argentina’s TAM tank upgrades collectively exceed USD 500 million in active contracts, ensuring a steady stream of vehicle deliveries. In parallel, artillery modernization under Brazil’s Astros 2020 and mobile mortar projects enhances responsive fire support, which is essential for jungle and mountain operations.

The air force is regaining prominence, poised to expand at a 5.34% CAGR through 2031, driven by multinational fighter recapitalization. Argentina’s first F-16 batch restores an air superiority role that has been dormant since the 1980s, while Peru’s DSCA-cleared F-16C/D Block 70 order, once financed, will retire its aging Mirage 2000 and MiG-29 fleets. Brazil’s Gripen rollout and potential 34-unit follow-on lot consolidate an indigenous final assembly ecosystem, lifting local avionics and mission system expertise. Continuous ISR aircraft integration further strengthens situational awareness across the South America defense market.

By Type: Vehicles Lead, Unmanned Systems Accelerate

Vehicles represented 25.01% of 2025 revenue, with flagship programs such as Guarani APCs, Leopard 2 maintenance, and Pandur II transports underpinning order books. Sustained ammunition contracts, notably Brazil’s more than USD 1 billion tranche with CBC, reassure suppliers of predictable consumption rates, reducing import reliance and aligning with offset objectives.

Unmanned systems show the fastest expansion at 5.45% annually through 2031, reflecting Colombia’s Atlante II contract, Brazil’s Hermes 900 fleet reinforcement, and Chile’s adoption of the rotary-wing CAMCOPTER S-100. Local innovation is emerging: Colombia’s Dragom UAV signals a move toward co-development, while Brazil’s loitering-munition roadmap indicates demand for armed UAV capabilities. Synergies with C4ISR and EW procurement are building an integrated kill chain across the South America defense market.

By Domain: Land Primacy, Space Emergence

Land systems maintained a 44.78% share of the 2025 South America defense market, driven by the sheer expanse of unguarded frontiers and sustained insurgent threats. Continuous investments in mobile artillery, tactical UAVs, and armored mobility support rapid response over jungle, desert, and mountain terrain.

Space functions are advancing at a 6.24% CAGR, the highest across domains, anchored by Brazil’s PESE constellation and complementary Argentine and Chilean projects. Coupled with Chinese-built ground stations scattered across the continent, these satellites enhance persistent ISR and secure communications, cementing outer-space capability as a new pillar of the South America defense market.

By Procurement Nature: Offset Mandates Tilt Toward Indigenous Production

Foreign procurement accounted for 56.78% of the 2025 outlays due to the limited local capacity to manufacture fighters, submarines, or sophisticated sensors. Yet indigenous production is projected to rise at a 6.86% CAGR as Brazil’s 100% offset rule compels primes to localize tasks ranging from final assembly to subsystem fabrication. Embraer’s USD 139 million in defense revenue for the first quarter of 2025, combined with a USD 4.2 billion backlog, demonstrates the commercial upside of this model.[3]Embraer Investor Relations Team, “First-Quarter 2025 Results,” ri.embraer.com.br

Elsewhere, Avibras Indústria Aeroespacial and CBC Global Ammunition secure niche wins in rockets, ammunition, and small arms. Colombia’s COTECMAR and Chilean yards focus on MRO and selective shipbuilding, showing that industrial participation is scaling beyond Brazil, albeit unevenly. These dynamics collectively reshape supply chains inside the South America defense market.

Geography Analysis

Brazil accounted for 54.23% of regional spending in 2025, driven by multibillion-dollar surface and subsurface combatant programs, the Gripen fighter line, and the SISFRON border network.[4]Naval News Correspondents, “Brazil Commissions Third Riachuelo-Class Submarine S42,” navalnews.com Space projects under PESE and an embryonic cyber-defense command underscore Brasília’s multidomain ambitions. Colombia is advancing at a 6.22% CAGR, supported by more than USD 1 billion in combined US Foreign Military Financing across FY2024-2025 and persistent drug-interdiction operations. The Atlante II UAV buy, Pandur II APC fleet, and COTECMAR-Damen frigate build mark the country’s most robust modernization cycle in decades, embedding co-production in naval construction and inaugurating an indigenous drone capability.

Argentina, Chile, Peru, and the rest of the continent share the remaining slice of the South America defense market. Argentina’s inaugural batch of F-16s revives combat-aircraft capability despite inflation-linked funding stress. Chile sustains Leopard 2 and F-16 fleets with copper revenues, although price softness is squeezing discretionary outlays. Peru’s USD 3.42 billion F-16 Block 70 package and USD 463 million Hyundai ship deal hinge on the recovery of the copper market and political stability following 2024 corruption probes.

Competitive Landscape

Global primes account for more than 50% of platform deliveries, indicating a moderately concentrated South America defense market. Lockheed Martin Corporation retains critical upgrade work through its USD 265.90 million avionics contract for Argentina’s F-16s, ensuring long-term revenue even on second-hand transfers. Saab AB, through its partnership with Embraer S.A., satisfies Brazil’s offset policy while preserving intellectual property over high-end subsystems.

Embraer’s portfolio, which includes A-29 Super Tucano exports to Portugal and Uruguay, C-390 transports, and SABER radars, confirms its status as the only regional Tier 1 integrator, with 72% year-on-year revenue growth in the first quarter of 2025. Avibras Indústria Aeroespacial and CBC Global Ammunition fill capability niches in rockets, ammunition, and sidearms, reflecting successful specialization strategies under offset frameworks. Competitive pressure is rising from Chinese, Russian, and Iranian entrants offering flexible financing, as illustrated by Venezuela’s November 2025 purchase of Shahed UAVs. Compliance regimes, such as the US FCPA and Brazil’s Clean Company Act, introduce legal uncertainties.

South America Defense Industry Leaders

Lockheed Martin Corporation

Saab AB

Airbus SE

Avibras Indústria Aeroespacial S/A

Embraer S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Denmark delivered the first F-16 aircraft to Argentina under a defense agreement involving 24 aircraft, with deliveries planned in stages through 2028, strengthening bilateral defense cooperation and advancing Argentina's military capabilities.

- September 2025: Brazil signed a USD 900 million contract with the US for the acquisition of Javelin missiles, becoming the first South American country to join the exclusive group of operators for this advanced missile system.

- July 2025: Argentina and the US signed an agreement for the delivery of eight new Stryker M1126 armored vehicles, with shipments scheduled to begin in early 2026, marking a significant step in their defense collaboration.

South America Defense Market Report Scope

The South America defense market encompasses all aspects of military vehicle procurement, armament, and other equipment, as well as upgrade and modernization plans. The report also provides insights into the budget allocation and spending of each country present in the region in the past, present, and forecast periods.

The South America defense market is segmented by armed forces, type, domain, procurement nature, and country. Armed forces segment the market into the army, navy, and air force. By type, the market is classified into personnel training and protection, C4ISR and electronic warfare (EW), vehicles, weapons and ammunition, unmanned systems, and space and cyber systems. By domain, the market is segmented into land, air, naval, space, and cyber and electromagnetic spectrum. By procurement nature, the market is segmented into indigenous production and foreign procurement. The report also offers the market size and forecasts for countries across the region. The market size is provided for each segment in terms of value (USD).

| Air Force |

| Army |

| Navy |

| Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

| Indigenous Production |

| Foreign Procurement |

| Argentina |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement | |

| By Geography | Argentina |

| Brazil | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America defense market today?

The South America defense market size reached USD 24.41 billion in 2026 and is forecasted to climb to USD 31.30 billion by 2031, reflecting a 5.10% CAGR.

Which country spends the most on defense in South America?

Brazil accounted for roughly 54.23% of regional defense spending in 2025, driven by multibillion-dollar air, sea, land, and space programs.

What segment is growing fastest across South American defense budgets?

Unmanned systems lead growth, expanding at a 5.45% CAGR through 2031 as nations procure UAVs for surveillance and strike missions.

Why are satellite programs important for South American militaries?

LEO constellations offer sub-meter imagery and secure communications that improve border monitoring and maritime domain awareness.

How do offset requirements influence procurement?

Brazil’s offset mandate compels foreign primes to localize assembly and technology transfer, accelerating indigenous capacity and lifting regional production CAGR to 6.86%.

Page last updated on: