Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

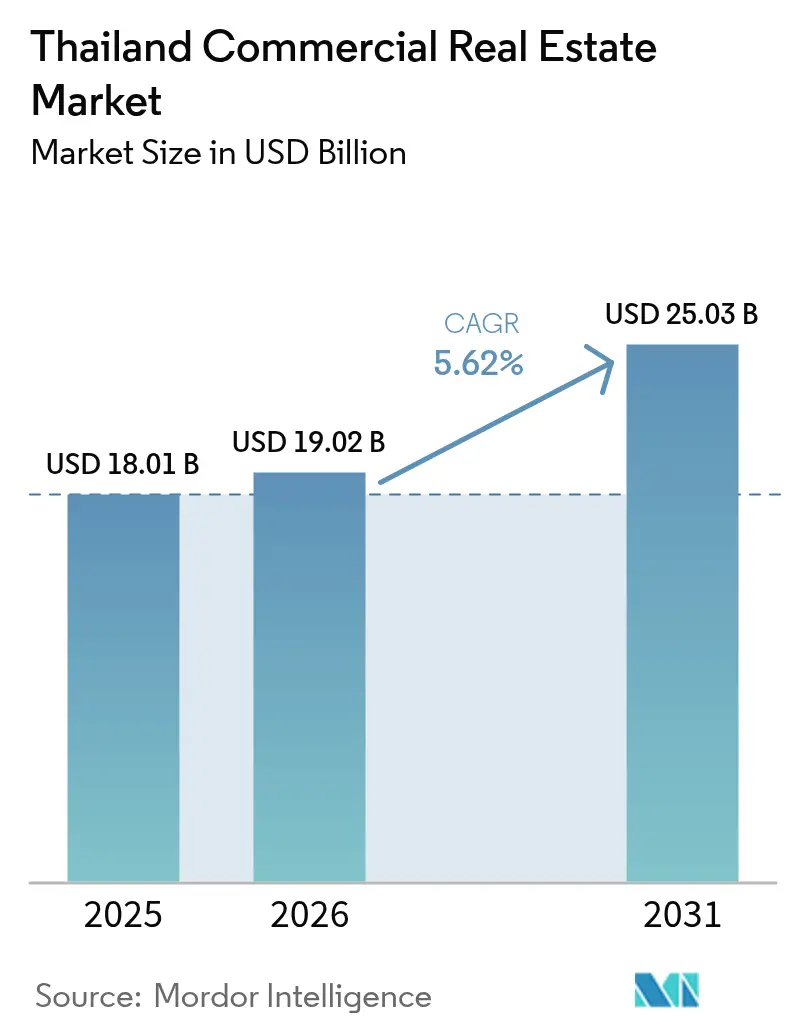

| Base Year Market Size (2025) | USD 18.01 Billion |

| Market Size (2026) | USD 19.02 Billion |

| Market Size (2031) | USD 25.03 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

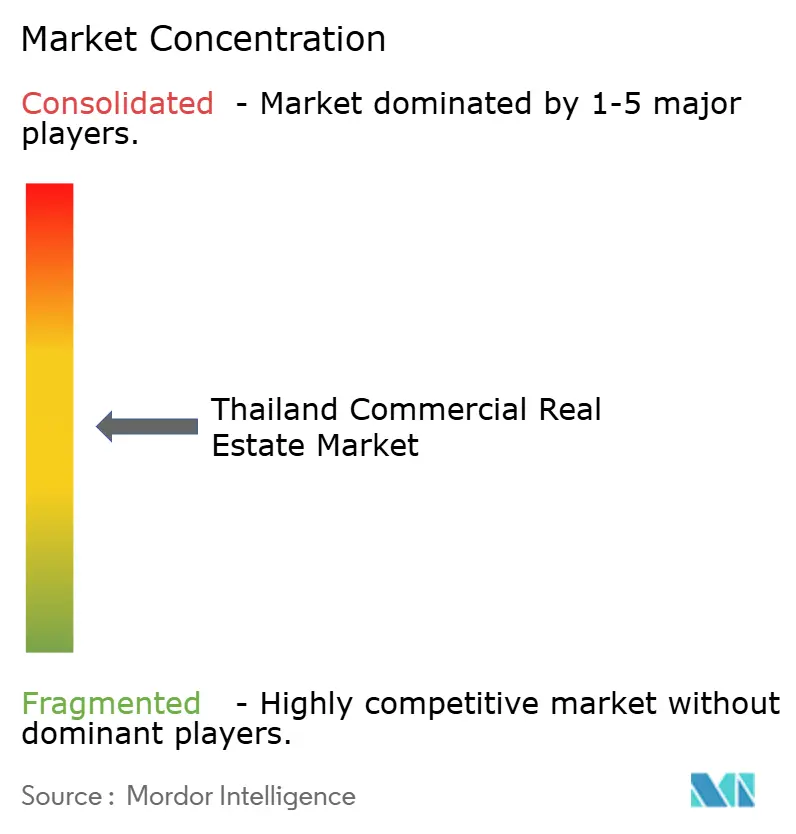

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Commercial Real Estate Market Analysis by Mordor Intelligence

Thailand Commercial Real Estate Market size in 2026 is estimated at USD 19.02 billion, growing from 2025 value of USD 18.01 billion with 2031 projections showing USD 25.03 billion, growing at 5.62% CAGR over 2026-2031. Robust logistics connectivity, record-level data-center approvals, and investor-friendly reforms together reinforce the long-term expansion path. Corporate requirements for energy-efficient offices, hospitality demand linked to the tourism revival, and e-commerce-driven warehouse uptake combine to sustain leasing volumes even as legacy stock weighs on headline vacancy. Continuous government spending, highlighted by the USD 17.8 billion transport pipeline that links Bangkok, the Eastern Economic Corridor (EEC), and deep-sea ports, adds capacity exactly where foreign direct investment is landing. Private developers are responding with sustainability-linked bonds and mixed-use formats that capture multiple income streams while positioning portfolios for future ESG screening.

Key Report Takeaways

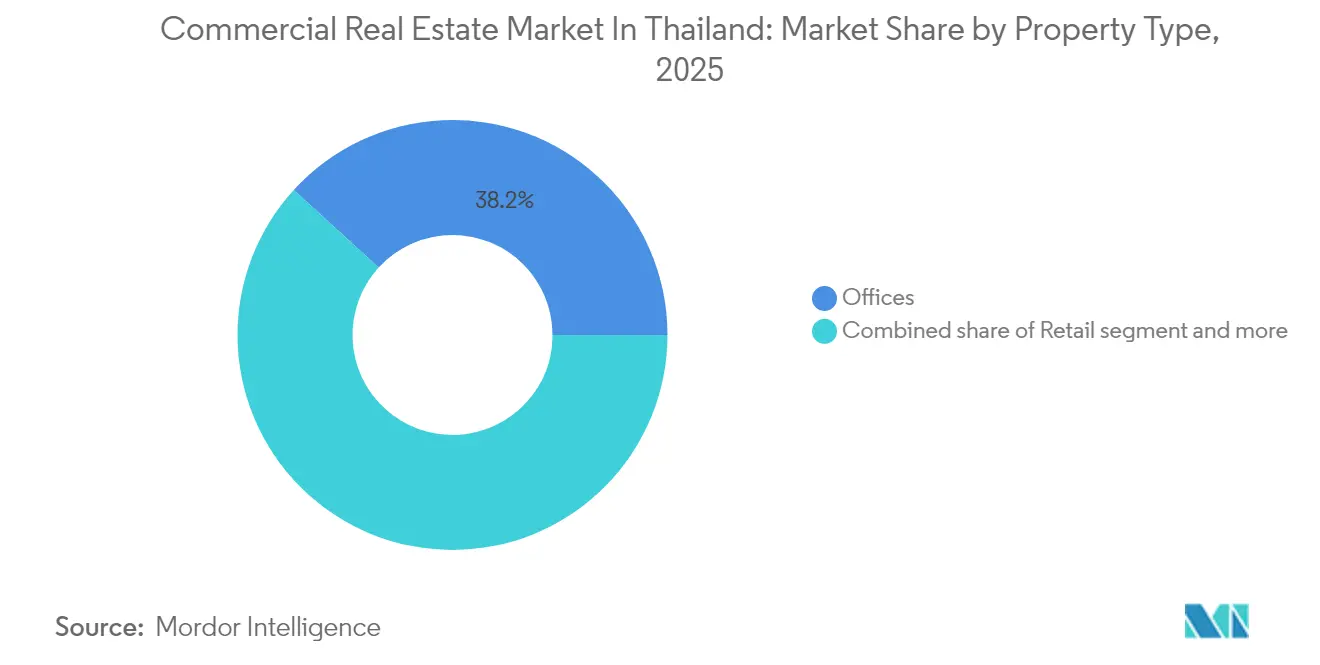

- By property type, offices held 38.22% of Thailand's commercial real estate market share in 2025, whereas other assets are advancing at a 8.74% CAGR through 2031.

- By business model, rentals commanded a 69.15% share of Thailand's commercial real estate market size in 2025, while sales are projected to expand at an 7.63% CAGR to 2031.

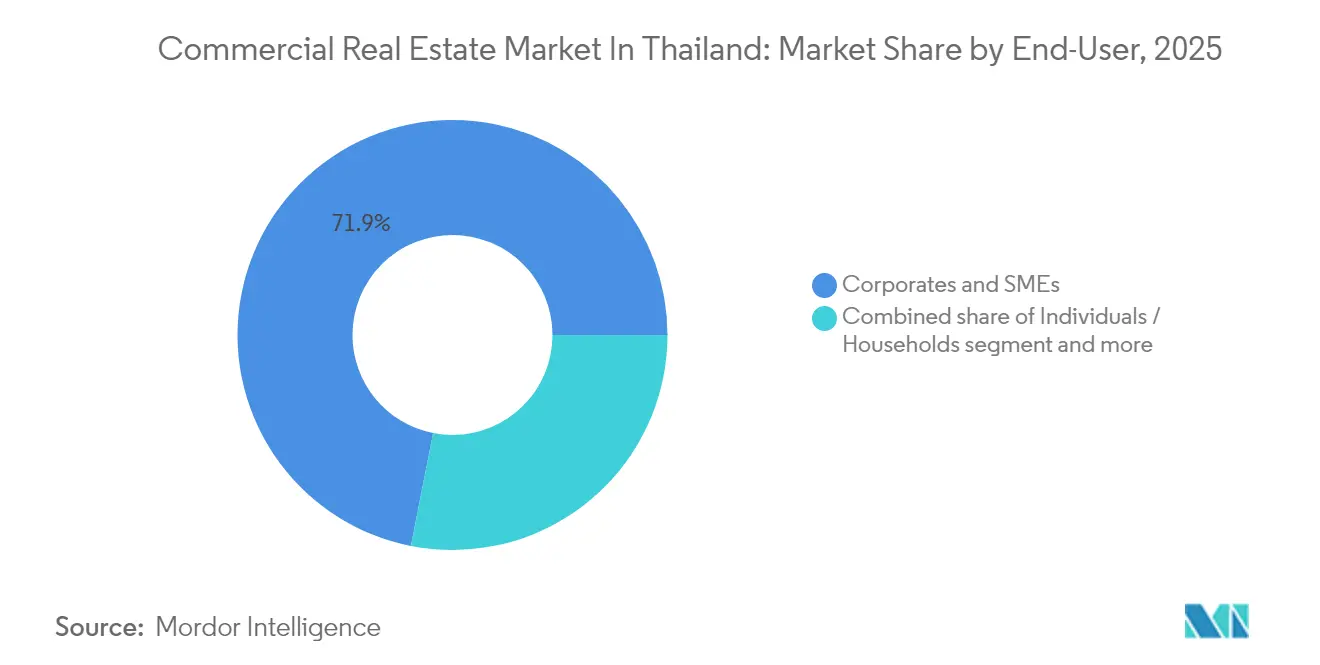

- By end-user, corporate and SME occupiers accounted for 71.90% of Thailand's commercial real estate market size in 2025, whereas household participation is rising at an 8.34% CAGR through 2031.

- By geography, Bangkok captured 41.96% of Thailand's commercial real estate market share in 2025; regions outside Phuket are expected to grow at a 5.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eastern Economic Corridor incentives are attracting industrial FDI | +1.5% | Chonburi, Rayong, Chachoengsao | Long term (≥ 4 years) |

| Flight-to-quality demand for Grade-A green offices | +1.2% | Bangkok, Chiang Mai, Phuket | Medium term (2-4 years) |

| Data-center localization mandates spurring specialized assets | +1.0% | EEC region, Bangkok periphery | Long term (≥ 4 years) |

| E-commerce fulfillment hubs expanding logistics take-up | +0.9% | EEC region, Greater Bangkok | Medium term (2-4 years) |

| Tourism-led rebound boosting hospitality & retail footfalls | +0.8% | Phuket, Koh Samui, Bangkok | Short term (≤ 2 years) |

| Hybrid-work space re-configuration services revenue stream | +0.4% | Bangkok metropolitan area | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Eastern Economic Corridor incentives are Attracting Industrial FDI

The EEC Board of Investment approved USD 2.7 billion of data-center projects in the first five months of 2024, validating the special zone’s pull for high-load digital infrastructure. A 10-year EEC Visa offering a flat 17% income tax eliminates a top talent barrier, while expressway and high-speed-rail links backed by USD 17.8 billion in public funding bind the corridor to Bangkok ports and airports. Industrial land values reached USD 169,000 per rai in H1 2024, up 17% year over year, signaling tightening supply. Relocation from China amid trade-war drag accelerated the trend; TCC Group’s USD 545 million park outside Bangkok is designed expressly for such entrants.

Flight-to-Quality Demand for Grade-A Green Offices

Corporate occupiers are moving swiftly toward buildings that satisfy international ESG frameworks, and 90% of all new leases signed in 2024 landed in assets holding LEED Gold or comparable labels. The Clean Air Management Act adds regulatory urgency by linking operational emissions to tenant reporting obligations. Financing is following the same path: Central Pattana’s USD 218 million sustainability-linked bond successfully priced below conventional debt, confirming robust investor appetite. Bangkok’s stock is aging; 60% now exceeds 20 years, so landlords unable to fund retrofits face rising obsolescence risk. New towers such as Mitsubishi Estate’s One City Centre capture the countertrend, booking blue-chip tenants at premium rents that outpace broader market declines[1]Central Pattana, “Sustainability-Linked Bond Offering Press Release,” Central Pattana Public Company Limited, cpn.co.th.

E-commerce Fulfillment Hubs are Expanding Logistics Take-Up

Revised VAT rules effective May 2024 removed mini-parcel exemptions, pushing cross-border sellers toward bonded warehouses that enable staged duty payment. Mitsui O.S.K. Lines answered with the automated “OMEGA 1 Bang Na” facility, due February 2027, to support same-day metropolitan delivery windows. WHA Corporation’s logistics revenue surged 61% year on year in Q1 2024, a direct result of electronics and auto manufacturers integrating omnichannel distribution networks around Bangkok. The Industrial Estate Authority’s single-window approvals shorten build-to-suit timelines, while DACHSER’s Asia expansion plan aims for 10% of its global revenue to originate in Thailand by 2027[2]Industrial Estate Authority of Thailand, “One-Stop Service Guidelines for Warehouse Development,” Industrial Estate Authority of Thailand, ieat.go.th.

Tourism-Led Rebound Boosting Hospitality & Retail Footfalls

Arrivals under Thailand’s “Amazing Thailand 2025” campaign climbed above pre-pandemic monthly highs by early 2025, and luxury resorts in Phuket now command average daily rates near USD 109. Retail landlords are integrating destination entertainment, illustrated by The Mall Group’s USD 1.36 billion mixed-use arena that targets international events and concerts. Asset World Corp reported hotel revenue 63% above 2019 comparable, validating pent-up demand once borders reopened. Yet geographic divergence is apparent: secondary beach towns retain discount pricing to defend occupancy, and escalating climate-risk insurance premiums are eroding margins along exposed coastlines[3]Chayaporn Supawong, “International Tourist Arrivals Dashboard 2025,” Ministry of Tourism & Sports, mot.go.th.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surplus legacy office stock is pressuring effective rents | -0.7% | Bangkok CBD, secondary cities | Medium term (2-4 years) |

| Cumbersome land-lease tenure for foreign investors | -0.5% | Nationwide, especially resort areas | Long term (≥ 4 years) |

| High household debt is limiting retail spending | -0.4% | Urban centers | Short term (≤ 2 years) |

| Climate-risk insurance costs for coastal hospitality | -0.3% | Phuket, Koh Samui, Gulf & Andaman coasts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surplus Legacy Office Stock is Pressuring Effective Rents

Vacancy in Bangkok climbed to 27.8% by Q4 2024 as 300,000 m² of new supply entered a market already softened by hybrid work. A bifurcation has emerged: ESG-certified towers achieve high take-up, while buildings from the late-1990s struggle to attract interest without major capex. Landlords delaying upgrades risk multi-year vacancies that undercut debt-service coverage.

Cumbersome Land-Lease Tenure for Foreign Investors

The Supreme Court’s 2024 clampdown on de facto freehold structures rekindled uncertainty just as inbound capital was rebounding. The proposed 99-year lease bill promises clarity, yet parliamentary passage remains elusive, freezing some pipeline deals. Hospitality projects in resorts are hit hardest because operators seek long control periods to match capex returns. Frasers Property cited these barriers among factors reducing its Thailand allocation for 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices Sustain Scale While “Others” Accelerate

The office segment retained 38.22% of Thailand's commercial real estate market share in 2025, even as vacancies widened; premium ESG-ready towers kept occupancy near 90% and lifted blended rents by 4%. Lease renegotiations increasingly bundle coworking passes and hotel club memberships, indicating a broadening service envelope. Retail space is moving back into favor as tourism rebounds, and Central Pattana’s USD 3.68 billion expansion program targets 200 sites by 2028 with entertainment-anchored designs. Logistics square footage is growing roughly 6% annually on the back of omni-channel fulfillment, with automated racking and mezzanine floors now standard for build-to-suit deals.

Others, industrial parks, data centers, and hospitality, represent the fastest-growing slice, logging a 8.74% CAGR outlook. Board-of-Investment incentives for cloud and semiconductor assembly are shifting land absorption further east into Chonburi and Rayong. Data-center approvals worth USD 2.7 billion illustrate how digital infrastructure has become a discrete asset class inside the Thailand commercial real estate market. Hotel RevPAR at Asset World Corp properties exceeded 2019 levels by 63%, underscoring resilience even as climate insurance costs mount for coastal holdings. The Board of Investment’s push to host mega-events adds a new demand stream for MICE-capable hotels.

By Business Model: Rental Dominance with Sales Momentum

Rental income streams generated 69.15% of Thailand's commercial real estate market size in 2025, reflecting tenant preference for balance-sheet flexibility and a mature REIT ecosystem that channels institutional capital into stabilized assets. Asset World Corp alone closed 16,000 m² of fresh leases in Q2 2024, using co-living and food-hall formats to lift stay durations. Updated Stock Exchange rules eliminated minimum-capital tests, lowering hurdles for mid-tier developers to seed public vehicles, which should deepen liquidity for the Thailand commercial real estate industry.

Sales transactions, while only 30.85% of volume, are advancing at an 7.63% CAGR as liberalizing ownership rules entice foreign buyers into resort and industrial assets. Average condominium pricing in prime districts reached USD 3,600 per m², signaling a tilt to premium stock as developers hedge against cost inflation. Passage of the 99-year lease bill would make outright acquisitions more attractive to cross-border funds, potentially accelerating the sales share of the Thailand commercial real estate market.

By End-user: Corporate Core, Household Catch-up

Corporate and SME occupiers consumed 71.90% of total space in 2025, and multinationals alone leased 65% of Grade-A offices, validating Thailand’s role as a regional headquarters node. EEC incentives attracted 317 foreign firms in the first five months of 2024, turbocharging demand for industrial sheds and flexible workspace. Household participation is climbing as the Leasehold Asset Act extends terms to 99 years, allowing families to treat shop-houses and strata offices as generational wealth.

Institutional investors and REITs, the “Others” category, are scaling quickly, driven by ESG mandates that steer global funds into green-certified real assets. Central Pattana’s oversubscribed bond and the inclusion of 54 SET-listed companies in the SETTHSI sustainability index spotlight the growing influence of capital-market screens. The trend anchors durable demand for efficient buildings, a virtuous loop that benefits the Thailand commercial real estate market.

Geography Analysis

Bangkok anchors 41.96% of the value owing to its transport hub status and concentration of headquarters. The USD 36.5 billion “Bangkok 2” smart-city in nearby Huai Yai will house 350,000 residents and 200,000 jobs once complete, reinforcing the capital region’s pull. Yet vacancy above 27% signals a pivot toward quality as hybrid work bites. High-speed rail and U-Tapao airport upgrades connect the metro to seaports, keeping the Thailand commercial real estate market integrated with regional supply chains.

Phuket stands out as the fastest-growing node at a 6.02% CAGR through 2031. Hotel occupancy hit 75% in 2024, and ADR averaging USD 109 supports the redevelopment of beachfront stock into upscale formats. Co-investment models between local owners and foreign flags are proliferating, while climate-risk premiums push builders to elevate land and reinforce coastal setbacks.

The Rest-of-Thailand bucket, mainly EEC provinces, shows industrial land purchases up 53% year on year, with asking prices around USD 169,000 per rai. Google and GDS IDC Services are investing USD 1.8 billion in hyperscale sites in Chonburi, underlining digital-infrastructure momentum. The EEC Visa’s 10-year term assures skilled-labor availability, making Rayong and Chachoengsao credible alternatives to Bangkok for advanced manufacturing and data-heavy operations.

Competitive Landscape

Moderate fragmentation defines the Thailand commercial real estate market, with the top five developers controlling near-34% of completed stock. Central Pattana leads via its “Ecosystem for All” roadmap, channeling USD 3.68 billion into 200 projects and issuing USD 218 million of sustainability-linked debt that priced inside the corporate curve. WHA Corporation dominates industrial logistics, managing almost 3 million m² and inking 917 MW of power deals to anchor data-center tenants.

Asset World is blending hospitality, retail, and workspace; its mixed-use projects secured 16,000 m² of new contracts in a single quarter. Technology tie-ups are multiplying: Mitsui O.S.K. Lines and CapitaLand will deliver an automated warehouse by 2027, whereas Mitsubishi Estate partnered with Raimon Land for Grade-A offices aimed at global banks. Updated REIT rules reduce listing frictions, enabling mid-sized builders to monetize stabilized assets while retaining development upside. The net result is an ecosystem where green design and partnership capability are eclipsing sheer land bank scale.

Thailand Commercial Real Estate Industry Leaders

Central Pattana PLC

WHA Corporation PCL

Amata Corp PLC

Frasers Property Thailand

Supalai PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Thailand BOI approved USD 2.7 billion of data-center and cloud projects, led by Beijing Haoyang Cloud’s 300 MW campus (USD 1.98 billion) and GSA Data Center 02’s 35 MW hub.

- January 2025: TikTok secured BOI consent for a USD 3.76 billion multi-site data-center rollout across Bangkok, Samut Prakan, and Chachoengsao.

- November 2024: Google and GDS IDC Services obtained permits for USD 1.8 billion hyperscale facilities in Chonburi; total filings reached 47 projects worth USD 5.1 billion.

- November 2024: Mitsui O.S.K. Lines and CapitaLand unveiled the fully automated OMEGA 1 Bang Na warehouse, a USD? million build, completing in Feb 2027.

Thailand Commercial Real Estate Market Report Scope

Commercial real estate (CRE) is a property used solely for business or a workspace rather than residential. Commercial real estate is often leased to tenants to conduct income-generating activities.

The Thailand commercial real estate market is segmented by type (office, retail, industrial and logistics, hospitality, and others) and key cities (Bangkok, Chiang Mai, Hua Hin, and Koh Samui). The report offers market size and forecast in value (USD billion) for all the above segments. The report also covers the impact of COVID-19 on the market.

By Property Type

| Offices |

| Retail |

| Logistics |

| Others (industrial real estate, hospitality real estate, etc.) |

By Business Model

| Sales |

| Rental |

By End-user

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Geography

| Bangkok |

| Chiang Mai |

| Phuket |

| Hua Hin |

| Koh Samui |

| Rest of Thailand |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (industrial real estate, hospitality real estate, etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Geography | Bangkok |

| Chiang Mai | |

| Phuket | |

| Hua Hin | |

| Koh Samui | |

| Rest of Thailand |

Key Questions Answered in the Report

How large is the Thailand commercial real estate market in 2026?

The market is valued at USD 19.02 billion and is projected to hit USD 25.03 billion by 2031.

What CAGR is expected for Thailand’s commercial real estate through 2031?

A 5.62% CAGR is forecast, led by industrial, hospitality, and data-center assets.

Which property type is growing fastest?

The “Others” segment, industrial parks, hospitality, and data centers, shows the highest forecast CAGR at 8.74%.

Why is the Eastern Economic Corridor significant?

EEC tax incentives and infrastructure worth USD 17.8 billion are attracting high-tech FDI, boosting industrial land and data-center demand.

Page last updated on: